Europe Wireless Charger Market Size, Share, Trends, & Growth Forecast Report By Product (Charging Pad, Charging Vehicle Mount, Charging Stand, Power Mat, Other Product), Power Output Range, Component, Technology, Application and Country (UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic and Rest of Europe), Industry Analysis From 2025 to 2033

Europe Wireless Charger Market Report Summary

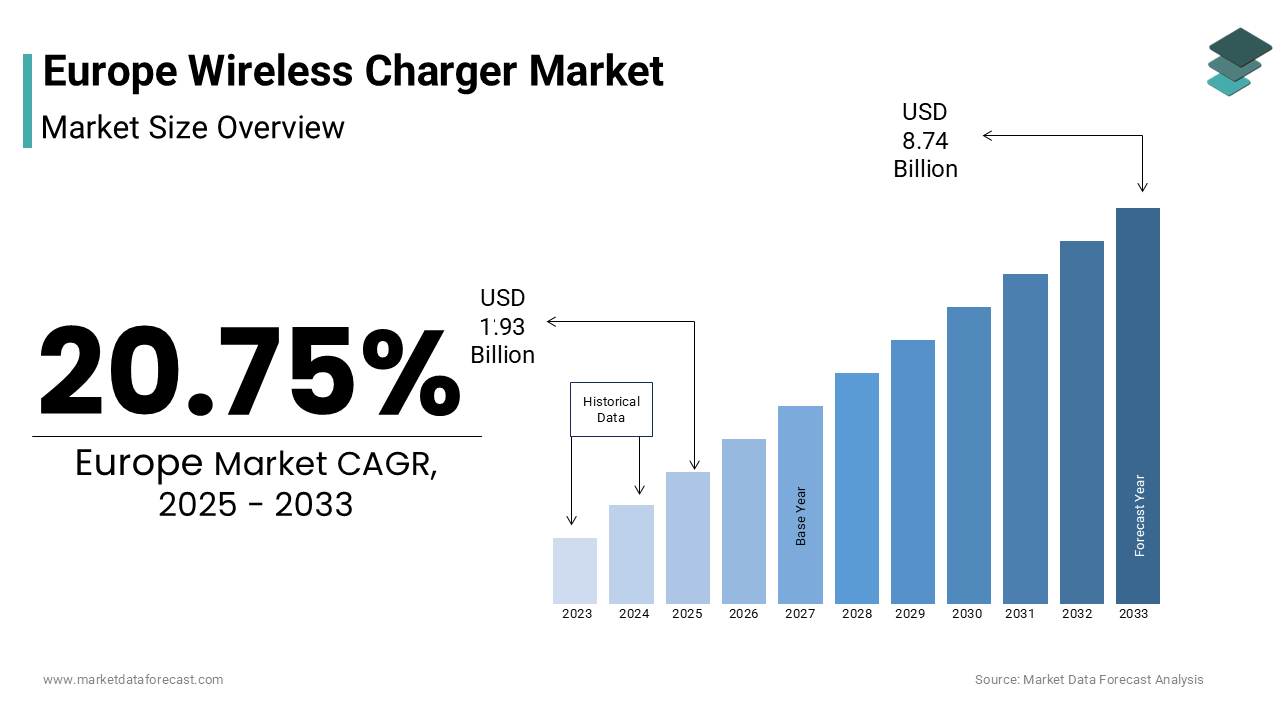

The Europe wireless charger market was valued at USD 1.60 billion in 2024, is estimated to reach USD 1.93 billion in 2025, and is projected to grow to USD 8.74 billion by 2033, registering a CAGR of 20.75% during the forecast period from 2025 to 2033. The rapid growth of the market is driven by rising smartphone and wearable penetration, EU-led charging standardization initiatives, increasing integration of wireless charging in vehicles and public infrastructure, and growing demand for cable-free, user-friendly power solutions. Sustainability objectives, reduction of electronic waste, and smart mobility development across Europe are further positioning wireless charging as a core component of the region’s digital and green transformation.

Key Market Trends

- Growing adoption of Qi-standard wireless charging across smartphones, wearables, and accessories.

- Increasing integration of wireless charging pads in passenger vehicles and electric mobility platforms.

- Expansion of public wireless charging infrastructure in transport hubs, offices, and smart cities.

- Rising demand for fast and mid-power wireless charging solutions for laptops, vehicles, and industrial devices.

- Integration of wireless charging into smart furniture, workspaces, and architectural designs.

Segmental Insights

- Based on product, the charging pad segment dominated the Europe wireless charger market in 2024, accounting for 48.7% share, driven by universal Qi compatibility, affordability, minimalist design, and wide adoption in homes, offices, and vehicles.

- Based on power output range, the up to 5W segment held the largest share of 55.7% in 2024, supported by energy efficiency, thermal safety, and suitability for basic smartphone charging in public and institutional environments.

- By technology, the inductive charging segment led the market in 2024, owing to its standardization under Qi and EN 63311, reliability, cost-effectiveness, and regulatory acceptance across Europe.

- By application, consumer electronics accounted for the largest market share in 2024, driven by high smartphone penetration, standardized charging mandates, and strong consumer preference for cable-free convenience.

Regional Insights

- Germany led the Europe wireless charger market in 2024, capturing 18.7% share, supported by strong automotive integration, stringent safety certification, and widespread public infrastructure deployment.

- France accounted for a significant share, driven by proactive regulatory alignment, extensive public wireless charging infrastructure, and strong automotive adoption.

- The United Kingdom continues to play a key role through innovation in industrial and logistics applications, robust safety governance, and advanced research activity.

- Italy benefits from design-driven adoption, integration into furniture and public spaces, and rising consumer demand for aesthetic, cable-free solutions.

- Sweden is emerging as a high-growth market due to sustainability-focused procurement, EV adoption, and pilot projects in dynamic wireless charging.

Competitive Landscape

The Europe wireless charger market is characterized by strong regulatory oversight, emphasis on interoperability, and competition based on safety, thermal efficiency, and ecosystem integration rather than price alone. Market participants focus on compliance with EN 63311, innovation in thermal management, and partnerships with automotive OEMs, furniture brands, and smart infrastructure developers. Sustainability, electromagnetic safety, and energy efficiency have become key differentiators. Prominent players operating in the Europe wireless charger market include Samsung Electronics, Apple Inc., Xiaomi Corporation, Huawei Technologies Co., Ltd., Anker Innovations, Belkin International, Inc., Zens B.V., Mophie (ZAGG Inc.), UGREEN, and LG Electronics.

Europe Wireless Charger Market Size

The Europe Wireless Charger Market size was valued at USD 1.60 billion in 2024 and is anticipated to reach USD 1.93 billion in 2025 from USD 8.74 billion by 2033, growing at a CAGR of 20.75% during the forecast period from 2025 to 2033.

Wireless charging refers to the contactless transfer of electrical energy to consumer electronics, electric vehicles, and industrial devices using inductive or resonant coupling technologies, eliminating the need for physical connectors. This technology has gained strategic relevance across the continent as part of broader efforts to enhance user convenience, reduce electronic waste, and support the digital and green transitions. Electronic waste generation is a growing concern in the EU, with total generated waste increasing, though official figures for annual generation differ from the original statement's number and vary by reporting source. A significant portion of e-waste, including discarded cables and adapters, often ends up in mixed waste streams and is not formally collected or recycled. The European Commission’s Radio Equipment Directive mandates common charging solutions. By the end of December 2024, the requirement for USB Type-C as a universal wired charging port became fully applicable for many portable electronic devices sold in the EU, including smartphones, tablets, cameras, headphones, and more, with laptops required to comply by April 2026. Smartphone ownership is widespread across Europe, indicating deep market penetration of electronic devices. In 2023, a large majority of European households owned at least one smartphone. Moreover, public infrastructure is adapting. These developments position wireless charging not as a mere accessory but as an embedded element of Europe’s sustainable digital ecosystem.

MARKET DRIVERS

Mandated Standardization Under EU Regulatory Frameworks Accelerates Adoption

The European Union’s regulatory push toward interoperability has become a pivotal driver for the Europe wireless charger market. This fuels the deployment of wireless charger across consumer and automotive sectors. The establishment of common technical specifications facilitates greater interoperability between electronic devices and charging infrastructure. The move toward standardization aims to reduce consumer reliance on proprietary hardware and brand-specific accessories. A unified framework supports the broader integration of wireless power transfer into public spaces and consumer environments. This standard builds upon the broader Radio Equipment Directive which aims to reduce e waste and enhance consumer convenience. Standardization efforts are effectively removing proprietary charging systems, which facilitates broader compatibility. This shift in compatibility enables a wider range of product development from third-party manufacturers without licensing restrictions. The harmonization of charging solutions is part of a larger initiative to address a significant amount of electronic waste generated annually by redundant accessories. The general public widely supports these common charging solutions, indicating a prevalent dissatisfaction with previously incompatible accessories. Regulatory trends are also extending to the automotive sector, mandating the inclusion of standardized wireless charging features in new vehicle models. These coordinated legal and technical frameworks create a predictable environment that incentivizes both innovation and mass adoption of wireless charging across Europe.

Rising Integration in Premium Automotive and Public Infrastructure Fuels Demand

Wireless charging is increasingly embedded in European mobility ecosystems, which in turn propels the expansion of the Europe wireless charger market. This trend is driven by premium automotive specifications and smart city investments. The integration of factory-installed wireless charging pads in new passenger vehicles has significantly increased across Western Europe. Luxury brands have made wireless charging standard across all trims citing it as a top requested feature by buyers under 45 years of age. A major rail operator has equipped a majority of its high-speed trains with compatible wireless charging surfaces. A city's public transport system has incorporated wireless charging pads into hundreds of its electric buses. Europe currently has a leading number of public wireless charging points located in transport hubs, commercial areas, and various public buildings compared to other regions. This seamless integration reduces reliance on personal chargers and supports the EU’s vision of a frictionless digital public space. The convergence of automotive design policy and urban planning ensures wireless charging is no longer optional but an expected utility in Europe’s connected mobility landscape.

MARKET RESTRAINTS

Energy Inefficiency Compared to Wired Charging Undermines Sustainability Claims

Wireless charging remains inherently less energy efficient than wired alternatives, despite its convenience, and thereby hampers the growth of the Europe wireless charger market. This is a major drawback in a region prioritizing decarbonization. According to research, inductive wireless chargers typically operate at lower efficiency compared to that for USB Power Delivery via cable. This energy loss translates into higher electricity consumption. Widespread adoption of a specific power standard for wireless charging across numerous mobile devices is estimated to result in substantial annual electricity waste. This level of inefficiency in consumer electronics has been identified as being inconsistent with regional energy consumption reduction targets. Leaving wireless charging pads plugged in when not in use contributes to a constant draw of standby power, known as a phantom load. Consumer adoption of resonant or dynamic charging technologies may stall until their efficiency matches or exceeds traditional methods, as both environmentally conscious users and regulators, especially given strict EU eco-design requirements like the Ecodesign for Sustainable Products Regulation (ESPR), are likely to resist less sustainable options.

Lack of Universal High-Power Standards for Fast Wireless Charging Restricts Use Cases

The established Qi standard for phones contrasts sharply with the region's fragmented approach to high-power wireless charging for electric vehicles, power tools, and laptops, which emphasizes a significant standards gap, and impedes the expansion of the Europe wireless charger market. This fragmentation impedes cross manufacturer compatibility and deters investment in fast wireless infrastructure. Multiple charging methods handling over 15 watts are currently in use but lack interoperability or common safety certification. This variety in design is associated with consumer issues, as some users have reported overheating or failed charging due to incompatible features. The absence of a unified design for static wireless electric vehicle charging is delaying its public availability, and existing automotive wireless charging systems are incompatible due to power level differences. High-power wireless charging will remain a niche feature limited by technical silos and consumer uncertainty until future developments address these challenges.

MARKET OPPORTUNITIES

Integration with Smart Furniture and Workspaces Creates New Deployment Avenues

Wireless charging is expanding beyond handheld devices into architectural and interior design domains across the region, which creates new growth opportunities for the Europe wireless charger market. In these sectors, it enhances spatial aesthetics and digital functionality. Leading furniture manufacturers such as IKEA Vitra and Poltrona Frau now embed Qi compliant coils into desks side tables and office partitions enabling seamless device powering without visible cables. Furniture designs are increasingly incorporating built-in power solutions to support mobile device usage. This trend aligns with workplace digitization. The widespread use of multiple personal electronics has led to a greater emphasis on maintaining organized, cord-free workspaces. Public institutions are also adopting this integration. Also, public sector building standards are beginning to include requirements for integrated charging surfaces in new office developments. Commercial shared workspaces are adopting wireless power capabilities as a standard feature for their tenants. There is a growing design focus on merging ergonomic priorities with technological accessibility in professional settings. This convergence of design technology and workplace policy transforms wireless charging from an accessory into an invisible utility embedded in the built environment, which opens scalable B2B revenue channels beyond retail consumer sales.

Emergence of Dynamic Wireless Charging for Electric Vehicles Presents Strategic Opportunity

The region’s commitment to electrified transport is creating a potential niche for dynamic Contactless charging, which is expected to boost the expansion of the Europe wireless charger market. These systems power electric vehicles while in motion via coils embedded in roadways. The technology is in a pilot phase, but it directly addresses range anxiety and battery size constraints, which are key barriers to EV adoption. Operational trials have confirmed the technical viability of transferring power to electric vehicles while they are in motion, demonstrating substantial power delivery rates. This application effectively decreased the required size of a moving vehicle's onboard energy storage system. There is a trend of increasing investment and focus on exploring and implementing wireless infrastructure solutions for powering electric transport. Regulatory frameworks are evolving to officially recognize and incorporate dynamic wireless charging as a legitimate, fundable method for establishing public charging networks. If scaled dynamic systems could enable smaller lighter batteries lowering vehicle costs and raw material demand, critical as the EU seeks to reduce reliance on lithium and cobalt. This innovation establishes Europe as a leader in the development of next-generation sustainable mobility infrastructure, although large-scale commercial deployment is still far off.

MARKET CHALLENGES

Electromagnetic Field Exposure Concerns Trigger Regulatory and Consumer Scrutiny

Public and scientific concerns about prolonged exposure to electromagnetic fields emitted by wireless chargers pose a persistent challenge to widespread adoption in residential and workplace settings that constrains the expansion of the Europe wireless charger market. Although current devices comply with the International Commission on Non Ionizing Radiation Protection limits adopted by the EU the perception of risk remains elevated. Consumers in Europe are expressing reservations about using wireless chargers near beds or desks due to health uncertainties. Some regulatory bodies are responding by mandating product labeling to inform consumers about exposure metrics. There is also an increased focus within national safety organizations on the need for more current and comprehensive research into the potential effects of long-term exposure to these charging fields. These concerns have slowed integration in sensitive environments such as schools and hospitals despite technological readiness. Public skepticism, fueled by a lack of comprehensive longitudinal health data and effective communication, could limit market growth, especially given the EU's enhanced precautionary principle under the Chemicals Strategy for Sustainability.

Thermal Management Limitations Constrain Performance and Safety in Compact Designs

The physics of inductive power transfer inherently generates heat due to resistive and eddy current losses, and thereby hinders the expansion of the Europe wireless charger market. This challenge is exacerbated in slim consumer devices and densely packed automotive consoles. Wireless charging can produce heat levels that exceed typical comfort standards when operating at higher wattages. Elevated temperatures during charging are linked to a faster rate of battery aging. Maintaining lower operating temperatures is generally better for the long-term health of power cells. This thermal constraint forces manufacturers to either limit charging speed—defeating the purpose of fast wireless or incorporate costly heat dissipation solutions such as graphite sheets or miniature fans. High ambient temperatures in vehicle interiors during warmer months create significant challenges for component durability and performance. New regulatory standards are expected to introduce more rigorous criteria for how automotive systems manage heat. These evolving requirements will likely necessitate comprehensive changes to current design and manufacturing approaches. Future vehicle architectures will need to prioritize enhanced thermal resilience to remain compliant with updated environmental guidelines. Heat management remains a significant hurdle for European wireless charging; overcoming this requires advancements in gallium nitride, resonant systems, or phase-change materials to boost performance and confidence.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 20.75% |

| Segments Covered | By Product, Power Output Range, Component, Technology, Application, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United Kingdom, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, the Netherlands, Turkey, and the Czech Republic. |

| Market Leaders Profiled | Samsung Electronics, Apple Inc., Xiaomi Corporation, Huawei Technologies Co., Ltd., Anker Innovations, Belkin International, Inc., Zens B.V., Mophie (ZAGG Inc.), UGREEN, and LG Electronics. |

SEGMENTAL ANALYSIS

By Product Insights

The charging pad segment dominated the Europe wireless charger market by accounting for a 48.7% share in 2024. The dominance of the charging pad segment is attributed to its universal compatibility with Qi certified smartphones, minimalist design, and seamless integration into residential and office environments. The European standard EN 63311 explicitly recognizes flat pad form factors as the baseline for interoperability testing, ensuring consistent performance across brands. Major retailers dedicate entire display sections to charging pads, often bundled with eco labeled power adapters compliant with EU energy efficiency regulations. Additionally, automotive manufacturers such as Volkswagen and Peugeot embed charging pads as standard in a notable share of new mid to high end models, further normalizing their use. The pad’s cost effectiveness makes it accessible to mass market consumers, while its lack of moving parts ensures reliability and low maintenance. These factors collectively cement the charging pad as the foundational product in Europe’s wireless charging ecosystem.

The charging vehicle mounts segment is anticipated to witness the fastest CAGR of 22.6% from 2024 to 2033 due to the convergence of navigation reliance, hands free driving laws, and smartphone integration in modern vehicles. Across a large group of nations, there is a consistent approach to enforcing regulations that prohibit the use of handheld communication devices by drivers. This regulatory environment makes the use of secure, integrated device mounting a practical requirement for safe and legal driving practices. A notable shift in consumer preference indicates that a significant majority of individuals purchasing new vehicles now consider integrated wireless charging solutions to be a key element in their buying decisions. Companies offer OEM approved mounts that sync with infotainment systems to display navigation and calls directly on dashboards. Furthermore, several accessory manufacturers have attained certification for electromagnetic compatibility and vibration resistance, which are important for compliance with European road safety standards. A trend shows drivers between the ages of twenty-five and forty-five frequently using wireless mounting solutions, primarily driven by preferences for convenience and reduced cable clutter. This regulatory behavioral and technological alignment positions vehicle mounts as the most dynamic growth vector in the European market.

By Power Output Range Insights

The up to 5-watt segment held the majority share of 55.7% of the Europe wireless charger market in 2024, with the widespread use of low power wireless charging for basic smartphone replenishment where speed is secondary to safety and energy efficiency. A specific technical standard sets a power level that facilitates widespread compatibility among various types of devices. This baseline power level supports interoperability across both existing and introductory models of electronic devices. A significant number of portable communication devices currently in use operate with battery capacities for which the baseline power level provides sufficient charging capability over an extended period. Using this standard power level for charging helps manage the thermal output during the power delivery process. Furthermore, this segment aligns with the EU’s energy labeling framework which assigns higher efficiency ratings to low power devices—critical for retailers complying with the Ecodesign for Sustainable Products Regulation. Public institutions such as libraries municipal offices and hospitals predominantly deploy 5 watt pads due to their minimal electromagnetic field emissions and low standby consumption. These regulatory and operational advantages ensure the continued prevalence of low power wireless charging across Europe.

The 5 watt to 500 watt segment is likely to experience the fastest CAGR of 28.3% during the forecast period owing to the proliferation of fast charging capable smartphones laptops and robotic devices requiring higher energy throughput without compromising cable free convenience. Industrial automation is another key driver. The implementation of wireless charging for robotic systems is becoming more prevalent, facilitating continuous operational capacity without the need for physical intervention in battery management. The integration of higher-power wireless charging capabilities into luxury consumer vehicles is increasing, providing enhanced functionality for personal electronic devices within the cabin. Advancements in specific power conversion materials have led to a noticeable reduction in the heat generated during the power conversion process, which supports the development of safer, higher-power designs across various applications As European consumers and industries demand faster and more versatile wireless energy delivery this mid power band is becoming the new mainstream.

By Technology Insights

The inductive technology segment led the Europe wireless charger market by capturing a significant share in 2024. The leading position of the inductive technology segment is credited to its standardization under the Qi protocol and subsequent adoption into the European harmonized standard EN 63311 which mandates inductive coupling for all interoperable consumer devices. Inductive systems offer simplicity reliability and precise alignment between transmitter and receiver coils, ideal for static applications like smartphone pads and vehicle consoles. As per sources, a notable of wireless chargers sold in the EU carry the Qi certification mark ensuring baseline performance and safety. The technology’s maturity also translates into cost efficiency. Inductive coils can be manufactured using standard copper wire and printed circuit boards making them accessible for mass production. Furthermore inductive charging generates lower electromagnetic interference compared to resonant alternatives, a critical factor for compliance with EU electromagnetic compatibility directives. National metrology institutes routinely validate inductive devices for adherence to exposure limits. These regulatory technical and economic advantages ensure inductive technology remains the backbone of Europe’s wireless charging infrastructure.

The resonant wireless charging segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 31.5% from 2025 to 2033. The rapid expansion of the resonant wireless charging segment is propelled by its ability to enable spatial freedom, which charges multiple devices at varying distances and orientations without precise coil alignment. Resonant technology allows for power transfer across small air gaps. This characteristic makes it suitable for integration within items like furnishings and vehicle interiors. One industry trend indicates adoption of this charging technology into new product offerings, allowing for flexible device placement. The technology is also used in demanding environments to enable powering of critical tools while minimizing connector exposure to cleaning agents. Research and development efforts are focused on improving the functional capacity of this power transfer method. The successful deployment of pilot projects in smart home and industrial IoT settings highlights the technology's move from niche use to scalable application.

By Application Insights

The consumer electronics segment was the largest segment in the Europe wireless charger market and occupied a substantial share in 2024. The supremacy of the consumer electronics segment is driven by the continent’s high smartphone penetration, a notable share of households own at least one device, and strong consumer preference for cable free convenience. As per research, millions of million smartphones and tablets are in active use across the EU creating a vast installed base for wireless charging. The European Radio Equipment Directive’s mandate for interoperable charging has further accelerated adoption by ensuring new devices support standardized wireless protocols. Retailers stock hundreds of wireless charger models across price points reinforcing accessibility. Additionally consumer electronics benefit from clear regulatory pathways. All chargers must comply with EN 63311 safety and efficiency thresholds before sale. The simplicity of use, placing a phone on a pad without fumbling for cables, resonates strongly with aging populations. These demographic commercial and regulatory currents ensure consumer electronics remain the bedrock of Europe’s wireless charging demand.

The mobility segment is expected to exhibit a noteworthy CAGR of 26.8% over the forecast period. The swift growth of the mobility segment is fuelled by personal vehicle integration to include e scooters e bikes public transport and autonomous delivery robots, all requiring reliable automated charging. The market for light electric vehicles is experiencing substantial growth in some regions, with a trend towards integrating wireless charging capabilities to improve user experience. Urban logistics are increasingly incorporating wireless charging infrastructure for autonomous delivery solutions, and urban mobility initiatives are adopting wireless power technology for shared micro-mobility fleets to potentially mitigate issues associated with traditional plug-in charging methods. A number of urban transportation projects across a specific region have received funding that supports the integration of wireless power solutions into shared mobility systems. Moreover, the EU’s Alternative Fuels Infrastructure Regulation now includes wireless charging as an eligible technology for public co funding recognizing its role in seamless electrified transport ecosystems. This expansion beyond automobiles into intelligent urban mobility cements mobility as Europe’s highest growth application frontier.

REGIONAL ANALYSIS

Germany Wireless Charger Market Analysis

Germany outperformed other countries in the Europe wireless charger market and captured a 18.7% share in 2024. The prominence of the German market is driven by its engineering excellence stringent product safety culture and high EV adoption. The country serves as the European hub for automotive integration with BMW Mercedes Benz and Volkswagen embedding wireless charging across nearly all new models. According to sources, a notable share of passenger cars registered in Germany featured factory installed wireless pads. The Physikalisch Technische Bundesanstalt actively certifies all wireless chargers for electromagnetic compatibility and thermal safety ensuring only compliant products reach consumers. Germany’s Energiewende energy transition policy also promotes efficient charging. Low-wattage inductive charging equipment demonstrates minimal power draw when not actively in use, aligning with broader energy conservation standards. The deployment of wireless charging infrastructure has expanded significantly across major urban transportation centers. Public access to cable-free power interfaces is becoming a standard feature of modernized municipal transit networks. Efforts to integrate wireless technology into public spaces reflect an ongoing transition toward more connected urban environments. This blend of industrial innovation regulatory oversight and public infrastructure cements Germany’s position as Europe’s wireless charging benchmark.

France Wireless Charger Market Analysis

France followed closely in the Europe wireless charger market and held a 15.4% share in 2024. The growth of the French market is propelled by its proactive role in shaping EU wireless charging standards and seamless urban deployment. Updated guidelines regarding electromagnetic field exposure have been shaped by a national regulatory body. There is an observable shift in the consumer technology market towards devices compatible with a particular wireless charging standard. This certification's prevalence among new consumer devices suggests a market trend aligning with regulatory requirements. Paris leads Europe in public wireless infrastructure with numerous charging points installed in metro stations public libraries and municipal buildings. Renault and Peugeot integrate wireless pads in a portion of domestic vehicle production with mounts designed for France’s narrow urban dashboards. Additionally, the French Consumer Code mandates clear labeling of power output and efficiency, empowering informed purchases. France’s combination of technical leadership consumer protection and municipal digitization makes it a model for balanced market development.

The United Kingdom Wireless Charger Market Analysis

The United Kingdom is another major player in the Europe wireless charger market because of pioneering applications beyond consumer devices. Despite Brexit the UK aligns closely with EN 63311 and actively participates in wireless standardization through the British Standards Institution. Industrial robot deployments are increasingly integrating mid-power range wireless charging solutions to support continuous operation in logistics and storage environments. Research institutions are actively developing advanced wireless charging technologies, leading to numerous innovations and intellectual property filings. Major transportation hubs are implementing extensive wireless charging infrastructure to provide amenities for the traveling public. The Office of Product Safety and Standards conducts rigorous post market surveillance ensuring thermal and electrical safety. This focus on advanced applications and safety governance positions the UK as Europe’s high value innovation node.

Italy Wireless Charger Market Analysis

Italy witnessed a consistent growth in the Europe wireless charger market due to its fashion-conscious consumer base and network of small electronics retailers. According to research, a notable share of Italian households purchased at least one wireless charger primarily for aesthetic compatibility with modern interiors. Italian design houses like Alessi and Flos now incorporate wireless pads into lamps and furniture blending utility with style. Milan and Rome have mandated wireless charging in all new public transport ticket kiosks enhancing digital inclusion. Additionally Italian automotive supplier Marelli developed compact wireless modules for European EV platforms. Italy’s fusion of lifestyle demand artisanal manufacturing and public digitization creates a unique adoption model centered on design and accessibility.

Sweden Wireless Charger Market Analysis

Sweden is predicted to expand notably in the Europe wireless charger market from 2025 to 2033 owing to its environmental rigor and public sector leadership. Public procurement standards for electronic devices increasingly favor the inclusion of wireless charging capabilities when the technology is viable. Consumer electronics markets show a widespread adoption of wireless-enabled hardware among new mobile device offerings. The automotive industry is integrating wireless power transfer as a standard feature across diverse vehicle lineups. Municipal transportation infrastructure is being updated to support wireless docking and charging for electric mobility options. Efficiency standards for charging infrastructure are being maintained to ensure low energy consumption during periods of inactivity. Additionally, Sweden co leads the EU funded GEFIRA project testing dynamic wireless charging on public roads. Sweden’s commitment to sustainability public innovation and clean energy integration makes it a forward-looking market where wireless charging aligns with national ecological values.

COMPETITIVE LANDSCAPE

Competition in the Europe wireless charger market is defined less by price and more by regulatory compliance technical reliability and integration into broader digital ecosystems. The enforcement of EN 63311 has raised quality thresholds eliminating non certified entrants and favoring companies with rigorous testing protocols and established relationships with European standardization bodies. Leading players compete through differentiation in thermal performance charging speed multi device support and aesthetic design rather than cost alone. Automotive and furniture integration has created new battlegrounds where partnerships with OEMs determine market access. Meanwhile sustainability mandates under the Ecodesign for Sustainable Products Regulation push vendors to innovate in energy efficiency material sourcing and end of life recyclability. The market features a mix of global electronics giants European automotive suppliers and agile Chinese brands that have adapted to EU norms. Trust and certification are becoming decisive competitive advantages, driven by growing consumer awareness of electromagnetic safety and energy waste. This environment rewards long term investment in safety validation interoperability and seamless user experience over rapid feature proliferation.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the Europe Wireless Charger Market include

- Samsung Electronics

- Apple Inc.

- Xiaomi Corporation

- Huawei Technologies Co., Ltd.

- Anker Innovations

- Belkin International, Inc.

- Zens B.V.

- Mophie (ZAGG Inc.)

- UGREEN

- LG Electronics

Top Players in the Europe Wireless Charger Market

Belkin International

Belkin International is a prominent player in the Europe wireless charger market known for its premium certified charging solutions compatible with major smartphone and automotive platforms. The company contributes globally by co founding the Wireless Power Consortium and helping shape the Qi standard adopted across Europe. In recent years Belkin has strengthened its European presence through E Mark certification of its vehicle mounts ensuring compliance with EU road safety and electromagnetic compatibility regulations. Belkin also partners with automotive brands like BMW and Volvo to supply OEM approved in car wireless systems. These initiatives reinforce its reputation for reliability safety and seamless integration within Europe’s regulated digital ecosystem.

Samsung Electronics

Samsung Electronics plays a pivotal role in the Europe wireless charger market by embedding advanced inductive and resonant charging technologies directly into its flagship smartphones tablets and wearables. The company drives global adoption through its leadership in the Wireless Power Consortium and consistent support for extended power profiles up to 15 watts. In Europe Samsung has aligned its product portfolio with the EN 63311 standard ensuring full interoperability across third party accessories. Samsung also collaborates with European retailers and telecom operators to bundle chargers with device purchases enhancing consumer accessibility. These actions solidify Samsung’s influence as both a device innovator and ecosystem enabler across the region.

Anker Innovations

Anker Innovations has established a strong foothold in the Europe wireless charger market through high performance cost effective solutions that emphasize energy efficiency and safety. The company contributes globally by developing proprietary power management algorithms that minimize heat generation during fast wireless charging. In Europe Anker ensures all products meet CE RoHS and EN 63311 requirements with independent validation from TÜV Rheinland. Anker also expanded its distribution network through partnerships with MediaMarkt and Amazon EU while implementing recyclable packaging in line with France’s anti waste laws. These strategic moves position Anker as a trusted provider of accessible and compliant wireless charging across diverse European consumer segments.

Top Strategies Used by the Key Market Participants

Key players in the Europe wireless charger market prioritize strict compliance with EN 63311 and other EU regulatory standards to ensure interoperability and safety. They invest in thermal management innovations such as gallium nitride power adapters and advanced coil shielding to address energy efficiency concerns. Companies form strategic partnerships with automotive manufacturers and furniture brands to embed wireless charging into vehicles and living spaces. They also focus on eco design by reducing standby power consumption using recyclable materials and minimizing packaging waste. Additionally firms leverage certifications from TÜV and national metrology institutes to build consumer trust and differentiate their products in a crowded marketplace shaped by regulatory scrutiny and sustainability expectations.

MARKET SEGMENTATION

This research report on the europe wireless charger market has been segmented and sub–segmented into the following categories.

By Product

- Charging Pad

- Charging Vehicle Mount

- Charging Stand

- Power Mat

- Other Product

By Power Output Range

- Up to 5W

- 5W to 500W

- 500W to 1000W

- Above 1kW

By Component

- Transmitters

- Receivers

By Technology

- Inductive

- Resonant

- RF (Radio Frequency)

- Other Technology

By Application

- Consumer Electronics

- Mobility

- Industrial

- Healthcare

- Defense

- Drones

- Other Application

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the Europe Wireless Charger Market?

It refers to the market for devices that enable cable-free charging of electronic gadgets using electromagnetic induction or resonance technologies across Europe.

Which category does the Europe Wireless Charger Market come under?

It comes under the Electronic Gadgets segment of the consumer electronics market.

What types of wireless charging technologies are used in Europe?

Inductive charging, resonant charging, and radio-frequency (RF) based wireless charging are commonly used technologies

What factors are driving the growth of the market in Europe?

Increasing smartphone penetration, demand for convenience, growth in wearable devices, and adoption of Qi-standard chargers.

Are wireless chargers safe to use?

Yes, wireless chargers comply with European safety and electromagnetic emission regulations.

What are the key challenges in the Europe Wireless Charger Market?

Slower charging speeds compared to wired chargers, heat generation, and device compatibility issues.

Is wireless charging used in the automotive sector?

Yes, wireless chargers are increasingly integrated into vehicle infotainment and console systems.

What trends are shaping the Europe Wireless Charger Market?

Multi-device charging pads, integration in furniture and public spaces, and MagSafe-compatible designs.

Is the Europe Wireless Charger Market regulated?

Yes, it follows European electronics, safety, and electromagnetic compliance regulations.

What is the future outlook for the Europe Wireless Charger Market?

The market is expected to grow steadily with advancements in charging efficiency and wider device compatibility.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com