Global Flexible Plastic Packaging Market Size, Share, Trends & Growth Forecast Report – Segmented By Material (Polyethylene (PE), Polypropylene (PP), Polyethylene Terephthalate (PET), Polyvinyl Chloride (PVC), Others), Product Type, End-User and Region (North America, Europe, Asia Pacific, Latin America, and Middle East & Africa) - Industry Analysis From 2025 to 2033

Global Flexible Plastic Packaging Market Summary

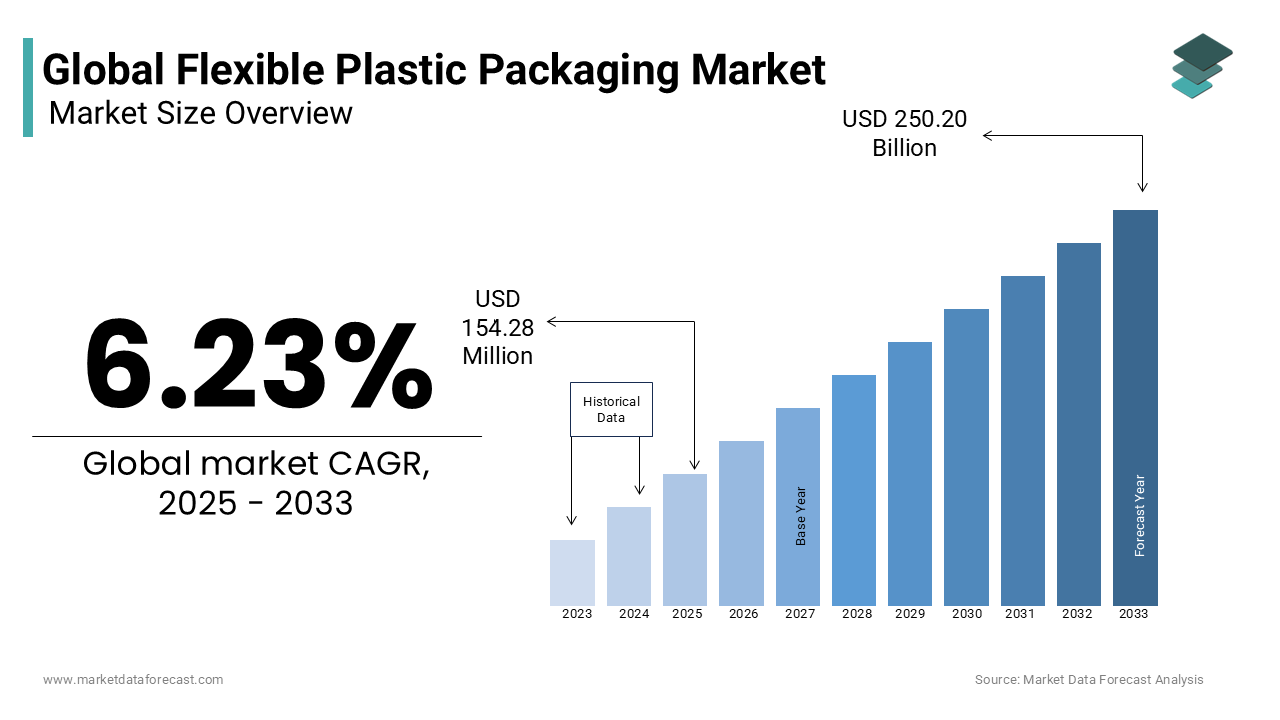

The global flexible plastic packaging market was valued at USD 145.23 billion in 2024, is estimated to reach USD 154.28 billion in 2025, and is projected to reach USD 250.20 billion by 2033, expanding at a CAGR of 6.23% from 2025 to 2033. Market growth is fueled by rising demand for lightweight, durable, and cost-effective packaging solutions, increasing consumption of packaged food & beverages, and growing adoption across healthcare, personal care, and e-commerce industries. Additionally, sustainability initiatives and innovations in recyclable and bio-based flexible plastics are supporting market expansion.

Key Market Trends

- Increasing demand for single-serve and convenience packaging.

- Growth of sustainable and recyclable flexible plastics.

- Expanding usage in online retail and e-commerce packaging.

- Rising adoption of advanced laminates and barrier films.

- Strategic collaborations to develop eco-friendly packaging materials.

Segmental Insights

- Based on material, the polyethylene (PE) segment was the largest, accounting for 48.2% of the market share in 2024 due to its durability and versatility.

- Based on product type, the films and laminates segment dominated with 37.5% share in 2024, driven by food preservation and extended shelf life.

- Based on end-use industry, the food and beverage sector led the market, capturing 62.7% of global share in 2024, reflecting rising packaged and ready-to-eat product consumption.

Regional Insights

- Asia Pacific was the top-performing region in 2024 with 44.3% of the market share, supported by rapid growth in China, India, and Southeast Asia due to urbanization and increasing disposable incomes.

- North America remains a key market, driven by strong demand for frozen food, snacks, and pharmaceutical packaging.

- Europe is advancing due to strict sustainability regulations and adoption of eco-friendly packaging materials.

- Latin America and the Middle East & Africa show steady growth with rising investments in consumer goods and retail sectors.

Competitive Landscape

Leading companies in the global flexible plastic packaging market include Amcor Limited, Berry Global Inc., Mondi Group, Sealed Air Corporation, Sonoco Products Company, Huhtamäki Oyj, Coveris Holdings S.A., Constantia Flexibles, ProAmpac, Bemis Company Inc. (now part of Amcor), Winpak Ltd., Uflex Ltd., Clondalkin Group Holdings B.V., Novolex Holdings LLC, and Innovia Films. These players are focusing on R&D, recyclable material innovation, and strategic acquisitions to strengthen their market presence.

Global Flexible Plastic Packaging Market Size

The global flexible plastic packaging market was valued at USD 145.23 billion in 2024, is estimated to reach USD 154.28 billion in 2025, and is projected to reach USD 250.20 billion by 2033, growing at a CAGR of 6.23% from 2025 to 2033.

Flexible plastic is a malleable, lightweight containment system made from polymeric films, such as polyethylene, polypropylene, and polyester. It is engineered to protect and preserve a wide range of products, primarily in food, pharmaceuticals, and consumer goods. Unlike rigid packaging, it offers superior formability, reduced material use, and optimized transport efficiency. The sector is increasingly defined by performance-driven innovation, particularly in moisture, oxygen, and light barrier properties, which are important for extending shelf life and maintaining product integrity. According to the study, flexible plastics accounted for a portion of municipal plastic waste, emphasizing both their ubiquity and disposal complexity.

MARKET DRIVERS

Surge in E-Commerce and Direct-to-Consumer Logistics

The exponential growth of e-commerce is majorly propelling the growth of the flexible plastic packaging market. This surge has fundamentally altered packaging requirements by favoring lightweight, durable, and space-efficient flexible solutions. As per Amazon, switching to flexible mailers reduced packaging weight compared to rigid boxes, which significantly lowers shipping emissions. In China, JD.com implemented flexible plastic packaging for a portion of its beauty and household product shipments, citing a reduction in warehouse storage volume.

Demand for Extended Shelf Life in Perishable Food Segments

The need to minimize food waste while ensuring product safety is driving adoption of high-barrier flexible films in perishable goods which further drives the flexible plastic packaging market. As per research, a portion of global food is lost between harvest and retail, with spoilage due to moisture and oxygen exposure being a primary factor. Multilayer flexible laminates incorporating ethylene vinyl alcohol (EVOH) and metallized PET can reduce oxygen transmission rates, extending the shelf life of fresh meat and cheese, according to research. In Europe, the European Commission estimates that improved packaging could prevent millions of tons of food waste annually. Companies like Sealed Air have introduced CRYOVAC barrier films that maintain freshness in vacuum-packed proteins for several days.

MARKET RESTRAINTS

Low Recyclability Due to Multi-Material Lamination

The constructed from multi-layer laminates combining polymers, aluminum, and adhesives, rendering them incompatible with conventional recycling streams, which hampers the expansion of flexible plastic packaging market. The lesser share of post-consumer flexible packaging in North America is mechanically recycled due to separation challenges. The presence of polyethylene bonded with polyamide or aluminum foil prevents efficient sorting and reprocessing, which leads to landfilling or incineration. These limitations have prompted regulatory scrutiny are forcing brands to reconsider material design and invest in mono-material alternatives.

Regulatory Burden on Single-Use Plastics

Governments worldwide are enacting stringent regulations to curb single-use plastic consumption, impacts the rise of flexible plastic packaging market. Many countries have implemented some form of plastic bag or film restriction, including India’s ban on specific categories of single-use plastics. The European Union’s Single-Use Plastics Directive mandates a 90% collection target for plastic bottles by 2029 and extends extended producer responsibility (EPR) to flexible films.

MARKET OPPORTUNITIES

Development of Mono-Material Recyclable Films

The emergence of mono-material flexible films is likely to showcase new opportunities for the growth of the flexible plastic packaging market. It offers new avenues for recyclability without sacrificing performance. As per Dow Chemical Company, its RETAIN PE-based sealant technology enables fully recyclable laminates that meet the APR Design for Recyclability protocol, with brands adopting it. The UK’s RECOUP agency reports that trials of mono-material pouches in supermarket chains increased recycling yield. Apart from these, companies like Amcor and Berry Global have commercialized recyclable stand-up pouches for snacks and pet food.

Integration of Active and Intelligent Packaging Features

Increased incorporation of active and intelligent functionalities to enhance product safety and consumer engagement is fuelling new opportunities for the flexible plastic packaging market. Oxygen scavengers, moisture absorbers, and antimicrobial layers are now embedded into film structures to prolong freshness. Intelligent features such as time-temperature indicators (TTIs) and QR codes are gaining traction. According to study, a portion of premium food brands in Germany now use printed sensors on flexible films to monitor spoilage. These advancements transform packaging from passive containment to dynamic communication and preservation tools, which create premiumization opportunities and strengthen brand loyalty in competitive retail environments.

MARKET CHALLENGES

Feedstock Price Volatility and Petrochemical Dependency

Dependence of fassil-derived feedstocks such as naphtha and natural gas liquids stands as an impediment to the flexible plastic packaging market. This exposes it to hydrocarbon price fluctuations. According to the study, ethylene prices, a primary precursor for polyethylene, spiked in 2022 due to supply disruptions, directly impacting film production costs. This volatility compresses margins for converters, particularly small and medium enterprises lacking hedging capabilities. A portion of plastic resins is still derived from petroleum, which is limiting short-term alternatives. While bio-based films like PLA and PHA exist, their production accounted for a smaller share of total flexible packaging volume, according to a study. The sector is vulnerable to geopolitical and energy market shocks until scalable, and cost-competitive renewable feedstocks emerge.

Consumer Perception and Brand Reputation Risks

The growing consumer awareness due to its association with environmental pollution and microplastic dispersion is a major factor challenging the expansion of flexible plastic packaging market. In response, Unilever and Nestlé have committed to phasing out hard-to-recycle laminates, which is signaling a shift in corporate packaging policy. According to the study, microplastics from degraded flexible packaging have been detected in a portion of bottled water samples globally, raising health concerns. These reputational risks compel brands to invest in redesign, labeling transparency, and take-back programs, which adds complexity to packaging innovation and marketing strategies.

REGIONAL ANALYSIS

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| Segments Covered | By Material, Product Type, End-User and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East, and Africa |

| Key Market Players | Amcor Limited, Berry Global Inc., Mondi Group, Sealed Air Corporation, Sonoco Products Company, Huhtamäki Oyj, Coveris Holdings S.A., Constantia Flexibles, ProAmpac, Bemis Company, Inc., Winpak Ltd., Uflex Ltd., Clondalkin Group Holdings B.V., Novolex Holdings, LLC, and Innovia Films. |

SEGMENTAL ANALYSIS

By Material Insights

The polyethylene (PE) segment was the largest and held 48.2% of the flexible plastic packaging market share in 2024. PE’s versatility, moisture resistance, and ease of processing across diverse applications are primarily driving the growth of the polyethylene (PE) segment. Low-density polyethylene (LDPE) and linear low-density polyethylene (LLDPE) are extensively used in food wraps, pouches, and shrink films due to their excellent sealability and toughness. According to the research, global LDPE production reached millions of metric tons, with a portion directed toward flexible packaging.

The polypropylene (PP) segment is predicted to witness the highest CAGR of 6.9% from 2025 to 2033. The rapid growth of the polypropylene (PP) segment is propelled by rising demand for high-clarity, heat-resistant films in microwaveable and retort applications. Biaxially oriented polypropylene (BOPP) films, which constitute a portion of PP-based flexible packaging, are favored for snack wrappers, confectionery, and labeling due to their optical clarity and printability.

By Product Type Insights

The films and laminates segment became the prominent segment in the flexible plastic packaging market by accounting for 37.5% of the market share in 2024. Their foundational role as substrates in high-performance packaging systems, particularly in food and pharmaceutical applications, is largely contributing to the expansion of films and laminates segment. Multilayer films combining PE, PP, EVOH, and metallized PET provide important barrier properties against oxygen, moisture, and light, essential for preserving perishable goods. According to a study, notable tons of laminated films were consumed globally, primarily in vacuum-sealed meats, cheese, and ready-to-eat meals. The rise of modified atmosphere packaging (MAP) has further amplified demand. Furthermore, advancements in adhesive lamination and extrusion coating have enabled thinner as well as stronger structures, which reduces material use while maintaining integrity.

The pouches and sachets segment is expected to lead the market with a CAGR of 7.4% during the forecast period owing to shifting consumer preferences for convenience, portion control, and premium presentation. Stand-up pouches, resealable zippers, and spouted pouches are increasingly replacing rigid containers in coffee, detergents, and baby food. According to research, a portion of U.S. consumers prefer stand-up pouches for pantry staples due to space efficiency and ease of use. In Asia, single-serve sachets remain vital for affordability. The rise of e-commerce has also boosted demand.

By End-use Industry Insights

The food and beverage segment led the flexible plastic packaging market by occupying 62.7% share of the global market in 2024. The material’s ability to preserve freshness, extend shelf life, and reduce food waste is fuelling the prominence of food and beverage segment in the global market. Flexible films are integral to vacuum packaging, modified atmosphere packaging (MAP), and retort pouches, which collectively prevent spoilage in meats, dairy, and ready-to-eat meals. According to research, up to one-third of all food produced globally is lost or wasted, and advanced flexible packaging can reduce this in perishable categories. In Europe, the European Commission estimates that MAP technologies save millions of tons of food annually. The rise of on-the-go consumption has further accelerated adoption.

The e-commerce segment is predicted to witness the highest CAGR of 10.2% from 2025 to 2033 due to the structural shift toward online retail, where packaging must withstand complex logistics, including multiple handling points and variable storage conditions. Flexible mailers, padded pouches, and inflatable air cushions made from PE and PP are replacing corrugated boxes due to their lower weight and volume. Furthermore, brands are leveraging e-commerce pouches for direct-to-consumer models in cosmetics and supplements by combining functionality with branding through high-definition printing and QR codes, which further amplifies demand.

REGIONAL ANALYSIS

Asia Pacific Flexible Plastic Packaging Market Insights

Asia Pacific was the top performer of the flexible plastic packaging market with 44.3% of the market share in 2024. China, India, and Southeast Asia are the primary engines of growth, which is driven by rapid urbanization, rising disposable incomes, and expanding food processing industries. China produced millions of metric tons of plastic packaging, according to study, with flexible formats accounting for a portion of total output. India’s flexible packaging business grew, fueled by government initiatives and the expansion of organized retail. The region is also at the forefront of innovation in sachet-based distribution. However, regulatory pressure is mounting. Like, India’s 2022 EPR rules mandate 70% collection of plastic waste, which pushes companies toward recyclable mono-material films and alternative delivery models.

North America Flexible Plastic Packaging Market Insights

North America flexible plastic packaging market held 23.5% of the share in 2024, with the United States functioning as the technological and regulatory benchmark for the industry. The U.S. consumes a significant million tons of plastic packaging annually, with flexible formats a portion of the total, as per research. The food and beverage sector drives demand, particularly for stand-up pouches and vacuum-sealed films in ready meals and snacks. According to the Grocery Manufacturers Association, a portion of new product launches featured flexible packaging due to its lightweight and resealable features. Regulatory dynamics are reshaping the landscape.

Europe Flexible Plastic Packaging Market Insights

Europe grew steadily in the flexible plastic packaging market by operating under one of the world’s most stringent regulatory frameworks. Germany, France, and Italy are the largest consumers, with food packaging constituting a portion of flexible plastic use. The European Commission’s Circular Economy Action Plan mandates that all packaging be reusable or recyclable by 2030, pushing manufacturers toward design-for-recycling principles. According to study, notable tons of flexible packaging entered the EU market, with only a share mechanically recycled, emphasizing the urgency for innovation. Countries like the Netherlands and Sweden are leading in chemical recycling pilot projects.

Latin America Flexible Plastic Packaging Market Insights

Latin America is predicted to thrive in the global market with Brazil dominating regional demand due to its large agricultural and consumer goods sectors. Brazil consumed a large amount of metric tons of plastic packaging, with flexible formats growing annually, as per research. The country’s food processing industry, particularly in meat, coffee, and dairy, relies heavily on vacuum and modified atmosphere packaging to meet export standards. According to a study, a percentage of exported beef is packaged in flexible laminates to ensure freshness during transit. However, recycling infrastructure remains underdeveloped.

Middle East and Africa Flexible Plastic Packaging Market Insights

The Middle East and Africa are likely to expand in the flexible plastic packaging market in over the forecast period with the Gulf Cooperation Council (GCC) countries leading in production and South Africa in regional distribution. Saudi Arabia and the UAE are expanding petrochemical integration, with SABIC producing over a million metric tons of polyolefins annually for export-driven packaging manufacturing. However, infrastructure gaps persist. Like, according to research, a smaller share of flexible plastics is collected in sub-Saharan Africa.

COMPETETIVE LANDSCAPE

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the global flexible plastic packaging market include

- Amcor Limited

- Berry Global Inc.

- Mondi Group

- Sealed Air Corporation

- Sonoco Products Company

- Huhtamäki Oyj

- Coveris Holdings S.A.

- Constantia Flexibles

- ProAmpac

- Bemis Company, Inc. (now part of Amcor)

- Winpak Ltd.

- Uflex Ltd.

- Clondalkin Group Holdings B.V.

- Novolex Holdings, LLC

- Innovia Films

The competition in the flexible plastic packaging market is intensifying as companies navigate the dual imperatives of functional performance and environmental accountability. Innovation-driven firms are redefining value through material science digital integration and circular economy models even as traditional converters dominate volume-based supply. The landscape is fragmented across regions, with Asia-Pacific serving as a battleground for cost and scale, while Europe leads in regulatory adaptation and sustainable design. Differentiation is increasingly achieved through proprietary resin formulations, recyclable architecture, and end-to-end lifecycle management. Large petrochemical integrators like Dow and SABIC compete with packaging specialists such as Amcor and Mondi by offering upstream material advantages.

Top Players in the Flexible Plastic Packaging Market

Amcor is a global leader in developing high-performance, sustainable flexible packaging solutions, with a robust and expanding presence across the Asia-Pacific region. The company operates advanced manufacturing facilities in China, India, Thailand, and Australia, serving major food, healthcare, and consumer goods brands. Its collaboration with the CEFLEX consortium has also influenced sustainable design practices across Southeast Asian supply chains, which supports its role as a technology and sustainability pioneer in the region.

Sealed Air Corporation plays a pivotal role in Asia-Pacific through its specialized protective and food preservation packaging technologies. The company’s BreatheWay® modified atmosphere packaging and CRYOVAC® vacuum skin packaging are widely used in seafood, meat, and ready-to-eat meals across Japan, South Korea, and Australia.

Dow Chemical Company is a key enabler of innovation in flexible plastic packaging through its polymer and resin technologies, particularly in polyethylene and adhesive solutions tailored for Asia-Pacific applications. Dow supplies performance resins to major converters in India, Vietnam, and Indonesia, supporting the production of high-seal-strength, thin-gauge films for snacks, dairy, and personal care products. Dow is shaping the next generation of sustainable and high-functionality flexible packaging across the Asia-Pacific value chain by combining material science with regional co-development initiatives.

Top Strategies Used by Key Market Participants

Key players in the flexible plastic packaging market are deploying a multi-pronged approach centered on material innovation, sustainability transformation, and vertical integration. Companies are investing heavily in mono-material structures that align with recyclability standards and extended producer responsibility regulations. Strategic collaborations with brand owners, recyclers, and governments are enabling closed-loop system development. Digitalization is being leveraged through blockchain traceability, smart labeling, and AI-driven design optimization to enhance transparency and performance. Expansion into high-growth regions like Asia-Pacific is being accelerated through localized R&D centers and regional manufacturing hubs. Furthermore, firms are pursuing mergers and acquisitions to gain access to specialty technologies such as active packaging and chemical recycling. Decarbonization initiatives, including the use of bio-based feedstocks and renewable energy in production, are becoming central to corporate strategy.

MARKET SEGMENTATION

The research report on the flexible plastic packaging market has been segmented and sub-segmented based on categories.

By Material

- Polyethylene (PE)

- Polypropylene (PP)

- Polyethylene Terephthalate (PET)

- Polyvinyl Chloride (PVC)

- Others

By Product Type

- Bags

- Pouches & Sachets

- Films & Laminates

- Tapes & Labels

- Tubes

- Others

By End-use Industry

- Food & Beverage

- Healthcare

- Home Care

- Personal Care

- Agriculture

- E-commerce

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is flexible plastic packaging?

Flexible plastic packaging refers to packages made from flexible materials such as films, foils, and plastics that can easily change shape without breaking, used for protecting and preserving products.

What are the main applications of flexible plastic packaging?

It is widely used in food & beverages, healthcare & pharmaceuticals, personal care, household products, and industrial goods.

What are the key drivers of the flexible plastic packaging market?

Rising demand for lightweight, durable, and cost-effective packaging, increased e-commerce, and growing need for extended shelf life of products.

Which regions dominate the flexible plastic packaging market?

Asia-Pacific is the largest market, followed by North America and Europe, due to high consumption in food & beverage and personal care sectors.

Who are the major players in the market?

Leading players include Amcor Limited, Berry Global Inc., Mondi Group, Sealed Air Corporation, Sonoco Products Company, Huhtamäki Oyj, and Coveris Holdings S.A.

What is the future outlook of the flexible plastic packaging market?

The market is expected to grow steadily with innovations in sustainable packaging, recycling technologies, and increasing demand across end-use industries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com