Global Greenhouse Grow Light Market Size, Share, Trends, & Growth Forecast Report, Segmented By Spectrum (partial, Full), Installation (new, Retrofit), Technology (high-intensity Discharge, Fluorescent, LED, Others), Application (indoor Farming, Vertical Farming, Greenhouse, Others) And By Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034

Global Greenhouse Grow Light Market Size

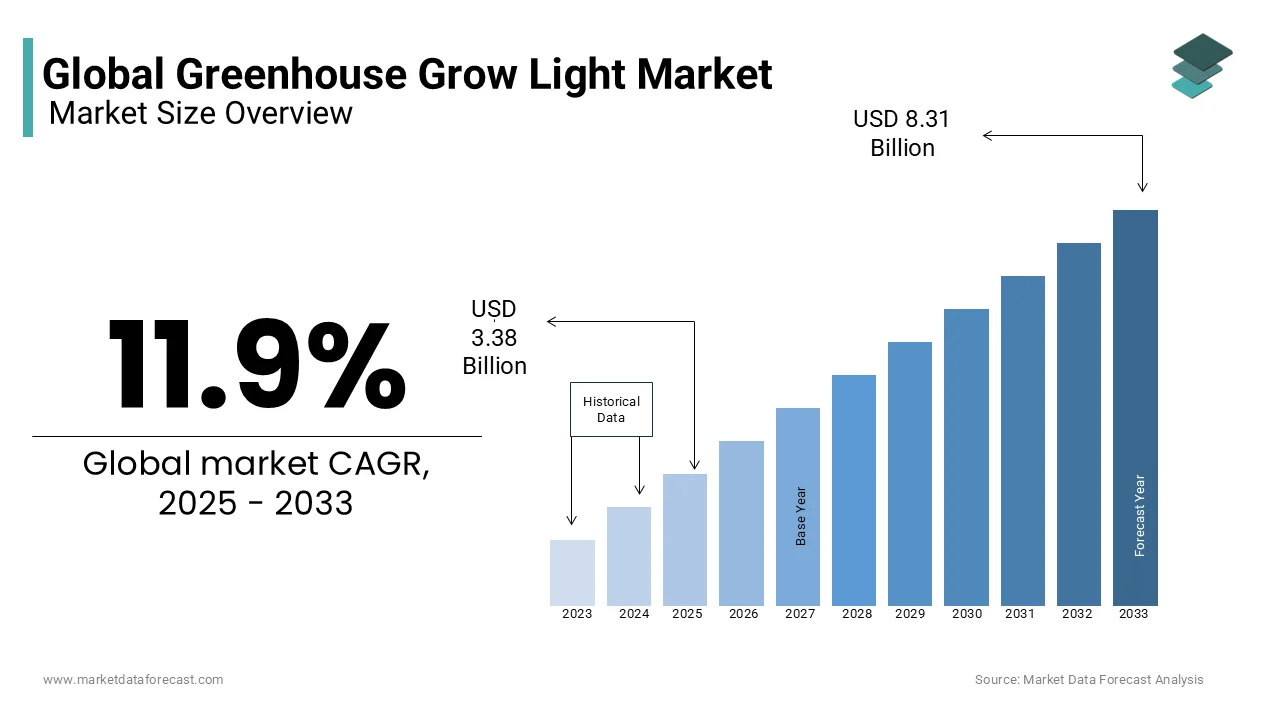

The global greenhouse-growth light market size was valued at USD 3.38 billion in 2025 and is anticipated to reach USD 3.78 billion in 2026 to reach USD 9.30 billion by 2034, growing at a CAGR of 11.9% during the forecast period from 2026 to 2034.

Greenhouse Grow Light is an agricultural technology that involves the deployment of artificial lighting systems within controlled environments to enhance plant growth, especially in regions with limited natural sunlight. These lighting systems, primarily based on LED, high-pressure sodium (HPS), and fluorescent technologies, are designed to replicate the spectrum of natural light essential for photosynthesis and crop development. As urbanization intensifies and arable land availability declines, greenhouse farming supported by grow lights is becoming a critical solution for sustainable food production.

In addition, the global adoption of greenhouse cultivation has surged due to rising concerns over climate variability and food security. For instance, the Netherlands, known as a global leader in horticulture, pointed out a 14% increase in greenhouse vegetable production compared to the previous decade, largely attributed to the optimized use of grow lighting systems. In Asia, countries like China and Japan have significantly expanded their vertical farming initiatives, integrating advanced grow lights to maximize yield per square meter.

Moreover, research from Wageningen University indicates that optimal light conditions can improve crop yields by up to 30%, reinforcing the strategic importance of grow lights in modern agriculture. This technological shift reflects an evolving paradigm where precision agriculture tools such as grow lights are no longer niche but integral components of future-ready farming strategies.

MARKET DRIVERS

Rising Demand for Year-Round Crop Production

The increasing demand for year-round crop production across diverse climatic zones is one of the primary drivers fueling the Greenhouse Grow Light Market. Traditional farming methods are highly susceptible to seasonal variations, which can disrupt food supply chains and affect market stability. Artificial grow lights provide a consistent light source, enabling farmers to maintain stable production cycles regardless of external weather conditions. In colder regions such as Canada and Northern Europe, where winter daylight hours are minimal, greenhouse operators rely heavily on grow lights to sustain commercial vegetable and herb cultivation.

This trend aligns with findings from the International Society for Horticultural Science, which estimates that optimized photoperiod control through artificial lighting can enhance annual harvest cycles by up to four times in certain crops.

Furthermore, as consumer preferences shift toward fresh, locally grown produce, retailers and distributors are increasingly sourcing from greenhouse farms equipped with grow lights. This ensures product consistency and reduces dependency on imported goods, particularly during off-season months. The ability to regulate flowering and fruiting phases using tailored light recipes also supports high-value crop cultivation, including cannabis and medicinal herbs, further expanding the market’s scope.

Expansion of Controlled Environment Agriculture (CEA)

Controlled Environment Agriculture (CEA) has emerged as a transformative approach in modern farming, driving significant growth in the Greenhouse Grow Light Market. CEA integrates advanced technologies—including climate control, hydroponics, and artificial lighting—to create optimal growing conditions independent of external environmental factors. As per the United Nations Food and Agriculture Organization (FAO), nearly 25% of global greenhouse operations now incorporate some form of CEA, with grow lights playing a pivotal role in ensuring efficient photosynthesis and resource utilization.

North America leads in CEA adoption, with the U.S. Department of Agriculture reporting that over 1,200 commercial indoor farms were operational in 2023, many of which utilize energy-efficient LED grow lights. In particular, states like Arizona and California have seen rapid expansion in vertical farming setups, where multi-tiered plant racks depend entirely on artificial lighting to maximize space efficiency. As per a study conducted by Cornell University, vertical farms using optimized grow light systems achieved a 40% reduction in water usage while doubling biomass output compared to conventional greenhouses. Apart from these, government support in several countries is accelerating CEA implementation.

MARKET RESTRAINTS

High Initial Investment and Operating Costs

The high initial investment and ongoing operating costs are one of the most significant restraints impeding widespread adoption. Setting up a fully functional greenhouse with advanced lighting infrastructure requires substantial capital expenditure, particularly when opting for high-efficiency LED systems.

Beyond installation, the continuous energy consumption required to operate these lighting systems remains a persistent challenge. Energy costs can account for up to 30% of total operational expenditures in commercial greenhouses, as per the U.S. Department of Energy. For instance, in Germany, where electricity prices have risen sharply in recent years, many small-scale growers have hesitated to adopt artificial lighting despite favorable government subsidies.

Moreover, maintenance and replacement costs further add to the economic burden. LEDs, although more durable than traditional HPS lamps, still require periodic servicing and eventual replacement. These cumulative financial pressures make it difficult for smaller agricultural enterprises to justify the long-term return on investment without substantial financial backing or subsidies.

Technical Complexity and Lack of Expertise

The technical complexity involved in selecting, installing, and managing appropriate lighting systems, coupled with a lack of skilled personnel capable of optimizing their performance, is another major restraint affecting the Greenhouse Grow Light Market. Unlike traditional horticultural practices, effective grow lighting requires a nuanced understanding of light spectra, intensity levels, photoperiods, and plant-specific requirements. As per a 2024 industry survey, nearly 60% of greenhouse operators reported difficulties in configuring lighting parameters to match crop needs, leading to suboptimal growth outcomes.

This knowledge gap is particularly pronounced in emerging markets, where access to technical training and advisory services remains limited. In India, for instance, the National Horticulture Board found that less than 20% of greenhouse farmers had formal training in controlled environment agriculture, hindering the adoption of advanced lighting technologies. Even in developed economies, there exists a shortage of agronomists and engineers trained in both plant biology and electrical engineering—disciplines that must converge for optimal grow light utilization.

Furthermore, the integration of smart lighting systems with automated controls and data analytics platforms adds another layer of complexity. Many growers struggle with interpreting sensor-generated data or adjusting light settings dynamically based on real-time feedback. Without adequate training and support, the potential benefits of grow lights remain unrealized, limiting market expansion.

MARKET OPPORTUNITY

Integration of Smart Lighting Systems with IoT and AI

The integration of smart lighting systems with Internet of Things (IoT) and artificial intelligence (AI) technologies is one of the most promising opportunities shaping the future of the Greenhouse Grow Light Market. These advancements enable precise control over light intensity, spectrum, and duration, allowing growers to tailor illumination conditions to specific plant species and growth stages.

Smart grow lights equipped with embedded sensors and cloud connectivity can collect real-time data on environmental conditions such as temperature, humidity, and CO₂ levels. This information is then analyzed using AI algorithms to adjust lighting parameters automatically, optimizing photosynthetic efficiency and minimizing energy consumption.

Moreover, AI-powered predictive analytics allows for proactive adjustments in lighting schedules, preventing stress-induced growth anomalies and improving overall crop resilience. As per the research published by MIT’s Media Lab in 2023, AI-integrated grow light systems could reduce energy costs by up to 35% while maintaining or even enhancing biomass accumulation.

Growth of Urban and Vertical Farming Initiatives

Urbanization and the corresponding decline in available farmland have spurred the emergence of urban and vertical farming as viable alternatives to traditional agriculture, creating a robust opportunity for the Greenhouse Grow Light Market. Unlike open-field farming, vertical farms operate in stacked layers within controlled environments, making them entirely dependent on grow lights for photosynthesis.

Countries like Japan, Singapore, and the United Arab Emirates have pioneered large-scale vertical farming ventures, all of which integrate LED-based grow lighting systems. For example, in Tokyo, Spread Co.—one of the world’s largest vertical farming companies—uses proprietary LED lighting to cultivate over 30,000 heads of lettuce daily in a fully automated indoor facility. Their energy-efficient lighting setup, developed in partnership with Fuji Electric, contributes to a 98% reduction in water usage compared to conventional farming.

Similarly, in the Middle East, where extreme temperatures and arid conditions limit outdoor cultivation, governments are investing heavily in agtech innovations. As per the UAE Ministry of Climate Change and Environment, in 2024 that investments in vertical farming projects exceeded USD 1.2 billion since 2020, with grow lights accounting for nearly 40% of infrastructure costs.

MARKET CHALLENGES

Rapid Technological Obsolescence and Product Standardization Issues

The rapid pace of technological innovation, which often results in product obsolescence before full return on investment is realized, is a key challenge confronting the Greenhouse Grow Light Market. Manufacturers frequently introduce newer generations of LED lighting systems with improved efficiency, spectral tunability, and smart integration features, rendering older models less competitive in the marketplace.

This fast-evolving landscape creates uncertainty for growers, particularly small and mid-sized operations, who may hesitate to invest in cutting-edge systems, fearing premature replacement. Besides, the lack of standardized performance metrics across different lighting products complicates decision-making. The absence of universally accepted benchmarks for evaluating light efficacy, spectrum composition, and longevity makes it difficult for buyers to compare offerings from various vendors.

Regulatory bodies and industry consortia have attempted to address this issue, but progress remains fragmented. In the U.S., the DesignLights Consortium (DLC) has established a Qualified Products List for horticultural lighting; however, international adoption of such standards remains uneven. Consequently, many growers face challenges in identifying reliable, high-performing solutions, delaying broader market penetration, and limiting the full potential of grow light technologies in mainstream agriculture.

Regulatory and Environmental Compliance Pressures

As the Greenhouse Grow Light Market expands, regulatory scrutiny surrounding energy consumption and environmental impact is intensifying, presenting a notable challenge for manufacturers and users alike. Governments worldwide are enforcing stricter energy efficiency regulations to curb carbon emissions, compelling producers of grow lighting systems to comply with evolving standards.

While this transition promotes greener technologies, it also increases compliance costs for manufacturers, who must invest in research and development to meet stringent certification requirements. As per the U.S. Environmental Protection Agency (EPA), in 2023 that compliance-related expenses accounted for approximately 15% of total R&D budgets among leading grow light producers. Moreover, environmental assessments, including life cycle analyses and recyclability mandates, further complicate product design and distribution strategies.

From the consumer side, regulatory incentives and disincentives play a dual role. While some governments offer tax rebates and subsidies for adopting energy-efficient grow lights, others impose higher utility tariffs on excessive electricity consumption, particularly in regions experiencing power shortages. Such policies, while environmentally motivated, can deter adoption among cost-sensitive growers unless offset by sufficient financial support mechanisms.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 11.9% |

| Segments Covered | By Spectrum, Installation, Technology, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Royal Philips, General Electric Company, Osram Licht AG, Gavita Holland B.V., Lumigrow Inc., Heliospectra, Iwasaki Electric Co., Ltd., Illumitex Inc. |

SEGMENTAL ANALYSIS

By Spectrum Insights

Partial Spectrum Grow Lights

The partial spectrum segment holds a dominant share of 58% in the Greenhouse Grow Light Market in 2024. This segment primarily includes lighting systems that emit specific wavelengths tailored to particular growth stages, such as flowering or vegetative development. Its cost-effectiveness and targeted efficiency are largely driving the dominance of the partial spectrum segment. Many growers prefer using red and blue light spectrums for boosting photosynthesis without investing in full-spectrum solutions.

Further, partial spectrum lighting aligns well with traditional horticultural practices where light manipulation is used to control plant morphology and flowering times. Similarly, in the Netherlands, greenhouse tomato production relies heavily on supplemental lighting.

Moreover, energy savings play a pivotal role. As per a study published by the International Society for Horticultural Science, partial-spectrum LEDs can reduce energy consumption by up to 28% compared to full-spectrum alternatives while maintaining comparable biomass output. This makes them particularly attractive for large-scale operations aiming to cut operational overhead without compromising productivity.

Full Spectrum Grow Lights

The full spectrum segment is projected to grow at the fastest CAGR of 14.2% from 2025 to 2033, which is driven by increasing demand for holistic plant growth solutions that mimic natural sunlight. Unlike partial spectrum systems, full spectrum lights cover a broader range of wavelengths, including ultraviolet (UV) and far-red, which are essential for enhancing secondary metabolite production and improving plant resilience.

The rising adoption of vertical farming and indoor agriculture, where plants rely entirely on artificial lighting,g ionene a major driver behind this rapid growth.

Furthermore, advancements in LED technology have made full-spectrum systems more energy-efficient and affordable. Osram Opto Semiconductors pointed out in 2024 that the latest generation of full-spectrum LEDs offers up to 40% higher photon efficacy compared to earlier models, significantly lowering long-term operating costs.

Consumer preferences also influence this trend. Apart from these, research from Wageningen University indicates that full-spectrum lighting enhances anthocyanin production in strawberries by 18%, contributing to better coloration and nutritional value.

Government-backed agricultural innovation programs in countries like Japan and South Korea are further accelerating the shift toward full-spectrum systems. These initiatives support the integration of advanced grow lights into smart farming ecosystems, reinforcing the segment’s strong upward trajectory.

By Installation Insights

New Installation

The new installation segment accounted for 63.5% of the global Greenhouse Grow Light Market, which is driven by the expansion of controlled environment agriculture (CEA) and the construction of purpose-built greenhouse facilities equipped with integrated lighting systems. The growing preference among commercial growers to establish technologically advanced greenhouses rather than retrofit existing structures is propelling the growth of the new installation segment.

Countries like the Netherlands, Canada, and the United Arab Emirates are leading this trend, where modern greenhouse complexes are being developed with full automation and LED-based lighting infrastructure. In the UAE, for instance, as per the Ministry of Climate Change and Environment, in 2024 that 90% of newly built agricultural greenhouses included state-of-the-art grow lighting to ensure year-round production despite harsh climatic conditions.

The availability of government incentives aimed at promoting high-tech agricultural projects is another key factor.

Moreover, new installations allow for optimal system design and energy efficiency planning. As per a study by the U.S. Department of Energy, newly constructed greenhouses with pre-installed grow lights achieved 30% lower energy consumption compared to retrofitted setups, reinforcing the economic viability of this approach.

Retrofit Installation

The retrofit installation segment is experiencing the highest growth within the Greenhouse Grow Light Market and is expanding at a CAGR of 13.7% through 2033. This surge is fueled by the increasing need to upgrade aging greenhouse infrastructure with modern, energy-efficient lighting technologies without necessitating complete facility overhauls is fuelling the surge of the retrofit installation segment.

The push for sustainability and reduced operational costs is another driver. Older greenhouses, especially those relying on outdated high-pressure sodium (HPS) lamps, are being retrofitted with LED systems that offer significant energy savings.

Besides, retrofitting allows growers to adopt smart lighting systems without dismantling existing irrigation and climate control infrastructure.

As legacy greenhouses seek to remain competitive and sustainable, retrofit installation will continue to be a strategic avenue for market expansion.

By Technology Insights

LED Grow Lights

The LED grow light segments dominated the Greenhouse Grow Light Market with an estimated 59.5% share in 2024, attributed to their superior energy efficiency, longevity, and spectral tunability. Unlike older technologies such as high-intensity discharge (HID) and fluorescent lamps, LEDs provide customizable light spectra that optimize plant growth at various developmental stages.

An additional key factor driving LED adoption is their ability to deliver high photon efficacy while consuming less power. As per the U.S. Department of Energy’s 2024 Commercial Lighting Report, modern LED grow lights achieve photon efficacies exceeding 3.0 µmol/J, significantly outperforming HID lamps, which typically operate below 1.8 µmol/J.

Moreover, LED systems generate less heat, reducing the need for extensive cooling mechanisms and lowering overall energy costs. A case study published by Cornell University in 2023 demonstrated that switching from HPS to LED lighting in a commercial greenhouse reduced cooling expenses by 35%, contributing to a faster return on investment.

Moreover, LED technology aligns well with the rise of smart agriculture. Integration with IoT sensors and AI-based controls enables dynamic adjustments to light intensity and wavelength, enhancing photosynthetic efficiency. According to the Netherlands’ Wageningen University, in 2024 that LED-equipped greenhouses achieved a 20% increase in cucumber yield compared to conventional lighting setups.

Government policies and financial incentives further bolster LED adoption. In Japan, the Ministry of Agriculture, Forestry and Fisheries provided subsidies covering up to 50% of LED installation costs for domestic greenhouse operators, resulting in a 40% increase in adoption rates over two years.

With continuous technological improvements and supportive regulatory frameworks, LED remains the most preferred lighting technology in the greenhouse sector.

Others

The “Others” category, encompassing emerging technologies such as plasma lighting, laser diodes, and hybrid systems, is anticipated to register the highest growth rate in the Greenhouse Grow Light Market and is expanding at a CAGR of 12.9% from 2025 to 2033.

The increasing experimentation with novel lighting sources that offer unique advantages over conventional technologies is one of the primary reasons for this rapid expansion. For example, sulfur plasma lamps, known for their broad-spectrum emission and high intensity, are gaining traction in specialized horticulture applications. Similarly, laser-based grow lights are being explored for their directional efficiency and minimal thermal output.

Further, hybrid lighting systems that combine solar concentrators with artificial light augmentation are gaining interest in off-grid and remote agricultural settings. In India, the Indian Council of Agricultural Research piloted a solar-assisted hybrid grow light setup in 2024, achieving a 20% reduction in grid dependency while maintaining optimal plant growth.

These innovations, though still in early adoption phases, are attracting significant R&D investments.

By Application Insights

Greenhouse

The greenhouse application segment continued to lead the Greenhouse Grow Light Market with a share of 54% in 2024, which is driven by the widespread adoption of supplemental lighting in traditional greenhouse structures to enhance productivity and extend growing seasons. This segment benefits from the fact that greenhouses serve as the bridge between open-field agriculture and fully enclosed indoor farming. Countries like the Netherlands, Spain, and the U.S. have long-standing greenhouse cultivation traditions, where grow lights are increasingly deployed to maintain year-round production of vegetables, fruits, and ornamental plants.

The University of Florida’s IFAS Extension drew attention that LED supplementation boosted pepper yields by 22% in trial greenhouses, reinforcing the economic justification for grow light deployment.

Moreover, government-backed agricultural modernization programs are supporting this trend. As global food demand rises and climate variability impacts traditional farming, the continued reliance on greenhouses equipped with grow lights ensures this segment remains the largest in the market.

Vertical Farming

The vertical farming segment is projected to expand at the fastest CAGR of 15.3% within the Greenhouse Grow Light Market, driven by the increasing demand for space-efficient, high-yield agricultural solutions in urban centers.

Unlike conventional greenhouses, vertical farms utilize stacked layers of crops illuminated entirely by artificial lighting, making grow lights an indispensable component of their infrastructure.

Japan leads in vertical farming adoption, with companies like Spread Co. producing over 30,000 heads of lettuce daily in fully automated, vertically stacked grow chambers illuminated by proprietary LED systems. The Japanese Ministry of Economy, Trade and Industry recorded a 25% increase in vertical farm establishments in 2023, attributing much of this growth to government subsidies for energy-efficient grow lighting.

Similarly, in the Middle East, where arable land is scarce and water resources are limited, the UAE has invested heavily in vertical farming. In addition, with urbanization accelerating worldwide, the vertical farming segment is poised to drive substantial growth in the grow light market over the coming decade.

REGIONAL ANALYSIS

North America Market Analysis

North America held a commanding position in the global Greenhouse Grow Light Market, accounting for 28.5% of total revenue in 2024. The region’s leading position is attributed to the presence of advanced agricultural technologies, robust government support, and a growing emphasis on food security through controlled environment agriculture.

The U.S. dominates the regional market, with states like California, Arizona, and Colorado investing heavily in greenhouse and vertical farming projects. Also, over 1,500 commercial greenhouse farms were operational in 2023, many of which adopted LED-based grow lighting to enhance yield and reduce energy consumption.

Canada is another key player, particularly in cannabis cultivation, where artificial lighting plays a central role.

Moreover, the U.S. government has actively supported the sector through initiatives such as the USDA’s Smart Agriculture Program, including grow lighting systems. With ongoing technological advancements and favorable policy frameworks, North America is expected to maintain its market-leading status throughout the forecast period.

Europe Market Analysis

Europe commands a notable share of the global Greenhouse Grow Light Market, driven by stringent environmental regulations, high levels of agricultural automation, and a strong focus on sustainable food production.

The Netherlands stands at the forefront of this movement, recognized globally as a leader in greenhouse horticulture. The country's expertise in high-tech horticulture has enabled it to export a substantial amount of greenhouse-grown vegetables annually, supported by optimized lighting strategies that enhance yield and resource efficiency.

Germany follows closely. As per a report from the German Renewable Energy Federation, LED retrofits in existing greenhouses resulted in a reduction in electricity usage while maintaining or improving crop quality. With strong regulatory backing and a growing emphasis on circular agriculture, Europe remains a key hub for innovative grow light applications.

Asia-Pacific Market Analysis

Asia-Pacific accounts for a notable share of the global Greenhouse Grow Light Market, with growth accelerated by rapid urbanization, government-led agricultural modernization, and rising demand for fresh produce in densely populated cities.

China leads the regional market. The Chinese government has prioritized smart agriculture, launching initiatives such as the “Digital Greenhouse Plan,” which mandates the integration of LED grow lights in new agricultural developments. In Beijing, pilot projects involving AI-controlled lighting systems have improved vegetable yields by 25%, demonstrating the scalability of these technologies.

Japan ranks second in the region, with vertical farming and controlled-environment agriculture gaining traction in response to land scarcity.

India, though still in the early stages of adoption, is witnessing a surge in greenhouse farming, particularly in states like Maharashtra and Punjab.

As governments in the Asia-Pacific region continue to invest in sustainable food systems, the grow light market is expected to experience sustained momentum.

Latin America Market Analysis

Latin America contributes a notable share to the global Greenhouse Grow Light Market, with Mexico, Colombia, and Brazil emerging as key markets driven by increasing investment in agribusiness and controlled-environment agriculture.

Mexico leads the regional market, benefiting from proximity to the U.S. and a strong export-oriented greenhouse industry. As per the Mexican Ministry of Agriculture (SADER), in 2024 that over 15,000 hectares of greenhouse space were dedicated to tomato and chili production, with more than 50% of new installations incorporating LED grow lights to improve yield consistency.

Brazil is also gaining momentum, with the Brazilian Agricultural Research Corporation (EMBRAPA) promoting the use of artificial lighting in tropical greenhouse cultivation.

Colombia, leveraging its equatorial climate for year-round production, has seen a rise in greenhouse investments. Despite challenges related to infrastructure and financing, Latin America presents considerable opportunities for growth as regional governments prioritize modernization and food security.

Middle East and Africa Market Analysis

The Middle East and Africa account for a smaller share of the global Greenhouse Grow Light Market, with the UAE, Saudi Arabia, and Israel leading the charge in adopting controlled-environment agriculture to combat extreme climatic conditions and water scarcity.

The UAE has emerged as a regional powerhouse, with the Ministry of Climate Change and Environment (MOCCAE) investing heavily in agtech innovations.

Israel, known for its agricultural technology expertise, has pioneered the use of smart lighting in greenhouse settings. The Israeli Ministry of Agriculture and Rural Development collaborated with local tech firms to develop AI-integrated grow light systems that adjust illumination based on real-time plant feedback. Saudi Arabia is also ramping up efforts under its Vision 2030 initiative, with the Ministry of Environment, Water, and Agriculture allocating USD 500 million toward greenhouse modernization. As water constraints intensify and food self-sufficiency becomes a priority, the Middle East and Africa are expected to see continued expansion in grow light adoption.

COMPETITIVE LANDSCAPE

The competition in the Greenhouse Grow Light Market is intensifying as both established lighting manufacturers and emerging agtech startups vie for market share. The industry is characterized by rapid technological advancements, increasing customization, and a strong push toward sustainable agricultural practices. Companies are not only competing on product performance but also on system intelligence, energy efficiency, and integration with smart farming ecosystems. This has led to a dynamic landscape where differentiation through innovation plays a crucial role. Apart from these, the convergence of lighting, data analytics, and automation is reshaping competitive strategies, compelling firms to invest heavily in R&D and digital capabilities. As demand for food security and climate-resilient farming grows, market participants are under pressure to offer scalable and adaptable solutions. Regional expansion, strategic acquisitions, and partnerships are becoming common tactics to strengthen presence and respond to evolving customer needs. While a few dominant players hold significant influence, niche innovators continue to challenge the status quo, ensuring a competitive and forward-looking market environment.

KEY MARKET PLAYERS

The major players operating in the Global Greenhouse Grow Light industry include

- Royal Philips

- General Electric Company

- Osram Licht AG

- Signify N.V. (Philips GreenPower)

- Gavita Hollan B.V.

- Lumigrow Inc.

- Heliospectra AAB

- Iwasaki Electric Co., Ltd.

- Illumitex Inc.

- Hortilux Schreder B.V.

- Sunlight Supply Inc.

Top Players In The Market

- Signify, through its Philips GreenPower brand, is a global leader in horticultural lighting solutions. The company offers a comprehensive range of LED grow lights tailored for greenhouses and vertical farms. Known for innovation and sustainability, Signify has been instrumental in advancing light recipes that optimize plant growth across various crops. Its collaboration with research institutions and growers worldwide has enabled data-driven lighting strategies that enhance productivity while reducing energy consumption.

- OSRAM is a major player recognized for its high-performance lighting technologies designed specifically for controlled-environment agriculture. The company's focus on spectral tuning and energy-efficient LED systems has positioned it as a preferred supplier for greenhouse operators seeking precision and durability. OSRAM’s integration of smart lighting controls allows growers to adapt illumination conditions dynamically, supporting improved crop quality and resource efficiency.

- Heliospectra specializes in intelligent LED lighting systems that deliver customizable light spectra for commercial greenhouse applications. With an emphasis on research-backed solutions, the company enables growers to fine-tune light environments for optimal plant development. Heliospectra’s commitment to scalability and automation makes it a key contributor to the advancement of smart farming technologies globally.

Top Strategies Used By Key Market Participants

Product Innovation and Customization

Leading companies are continuously developing advanced grow light systems tailored to specific plant needs. These innovations include tunable spectrum LEDs, adaptive control systems, and integration with AI-driven analytics to enhance performance and efficiency.

Strategic Collaborations and Partnerships

To strengthen their market foothold, key players engage in strategic alliances with agricultural technology firms, research institutions, and government bodies. These partnerships facilitate knowledge exchange, accelerate product development, and expand market reach across diverse regions.

Expansion into Emerging Markets

Major players are actively expanding into new geographic territories, particularly in Asia-Pacific and Latin America. By establishing local distribution networks and adapting products to regional agricultural practices, companies aim to capture growing demand driven by urban farming and greenhouse modernization initiatives.

RECENT MARKET NEWS

- In January 2024, Signify launched a new line of full-spectrum LED grow lights designed specifically for vertical farming applications, enhancing crop yield and quality while improving energy efficiency.

- In March 2024, OSRAM partnered with a leading agritech firm to integrate its LED lighting systems with real-time plant monitoring software, enabling dynamic light adjustments based on plant response.

- In June 2024, Heliospectra introduced an AI-powered lighting control platform that allows greenhouse operators to remotely manage and optimize light settings for different growth stages across multiple locations.

- In September 2024, LumiGrow expanded its distribution network into Southeast Asia by forming a joint venture with a local agricultural technology provider to support growing demand for smart greenhouse lighting.

- In November 2024, Ushio America announced the launch of a hybrid grow light solution combining LED and UV technologies aimed at boosting secondary metabolite production in medicinal and specialty crops.

MARKET SEGMENTATION

This research report on the global greenhouse grow light market is segmented and sub-segmented into the following categories.

By Spectrum

- Partial

- Spectrum

- Full-spectrum

By Installation

- New installations

- Retrofit

By Technology

- High-intensity discharge

- Fluorescent lighting

- LED and others

By Application

- Indoor farming

- Vertical farming

- Commercial greenhouse

- TURF and landscaping research

- Other applications

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle-East & Africa

Frequently Asked Questions

What is driving the growth of the greenhouse grow light market?

Increasing adoption of controlled-environment agriculture, year-round crop production, and demand for higher crop yields are driving market growth.

What does the greenhouse grow light market include?

The market includes lighting systems used in greenhouses to supplement or replace natural sunlight for plant growth.

Which lighting technology dominates the greenhouse grow light market?

LED grow lights dominate the market due to their energy efficiency, longer lifespan, and ability to optimize plant growth.

Why are greenhouse operators investing in grow light solutions?

Grow lights help improve crop productivity, support off-season cultivation, and enhance crop quality in controlled environments.

Who are the major end users in the greenhouse grow light market?

Commercial greenhouse operators, indoor farming companies, horticulture producers, and research institutions are the major end users.

How do grow lights improve greenhouse crop production?

They provide the optimal light spectrum for photosynthesis, promote healthy plant development, and increase harvest yields.

What trends are accelerating demand for greenhouse grow lights?

The expansion of vertical farming, increasing adoption of smart agriculture, and demand for locally grown produce are accelerating demand.

What challenges are affecting the greenhouse grow light market?

High initial installation costs, energy consumption concerns, and maintenance expenses can impact market growth.

How is technology transforming the greenhouse grow light industry?

Smart lighting controls, spectrum-adjustable LEDs, and IoT-enabled monitoring systems are improving energy efficiency and crop performance.

What is the future outlook for the greenhouse grow light market?

The market is expected to witness strong growth with rising investments in greenhouse farming, urban agriculture, and sustainable food production.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com