Global High End Greenhouse Market Size, Share, Trends, COVID-19 Impact And Growth Forecasts Report, Segmented By Covering Materials Type (Plastic, Solid Brush, And Others), Product Type (Tomatoes Greenhouse, Cucumber Greenhouse, Eggplant Greenhouse, Pepper Greenhouse, And Others), Component Type (HAVC System, Control System & Sensor, Valves & Pumps, And Irrigation System, Material Handeling, LED Grow Lights, And Others), Application Type (Residential and Commercial), And Region (North America, Europe, Asia-Pacific, Latin America, Middle East And Africa), Industry Analysis (2025 to 2033)

Global High-End Greenhouse Market Size

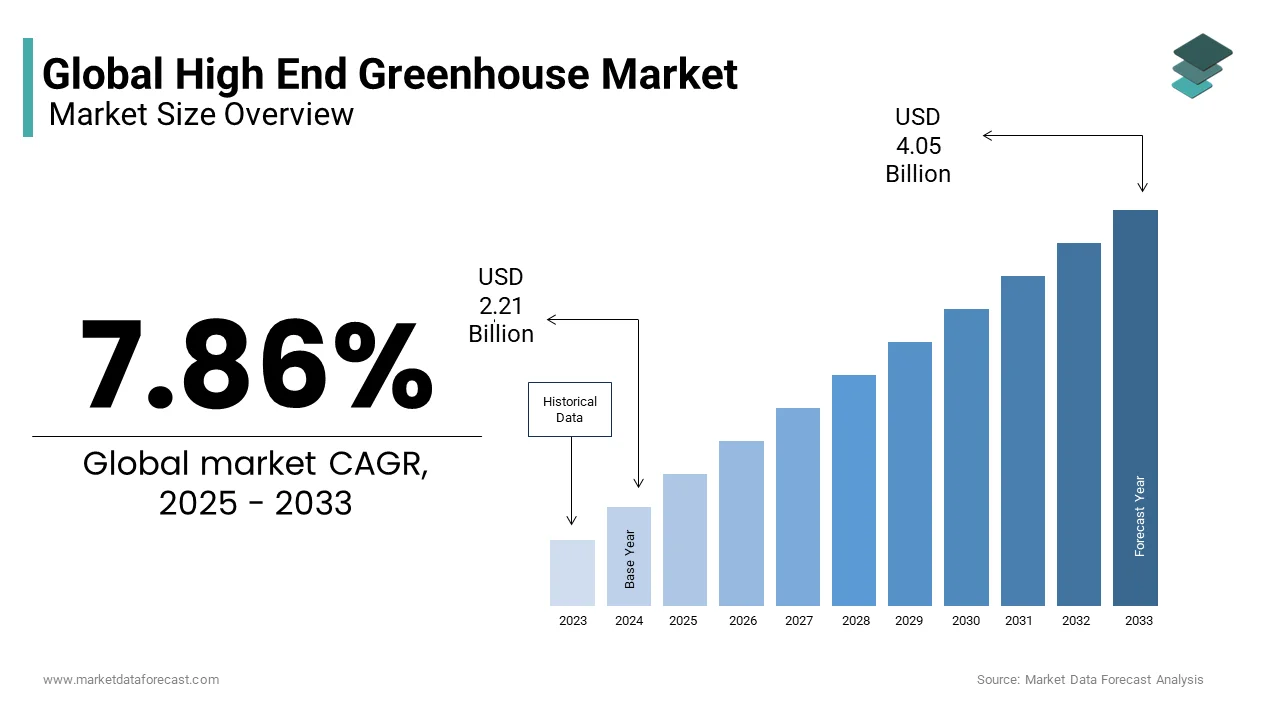

The global high-end greenhouse market size was valued at USD 2.05 billion in 2024 and is anticipated to reach USD 2.21 billion in 2025 to USD 4.05 billion by 2033, growing at a CAGR of 7.86% during the forecast period from 2025 to 2033.

High-end greenhouses are technologically advanced, climate-controlled agricultural structures that are engineered for precision cultivation, resource optimization, and year-round production of premium horticultural crops. These facilities integrate automated environmental control systems, hydroponic or aeroponic growing platforms, energy-efficient glazing materials, and data-driven monitoring via IoT sensors and AI analytics. Unlike traditional polytunnels or low-cost hoop houses, high-end greenhouses are capital-intensive installations designed for commercial-scale output, often exceeding five thousand square meters in footprint and featuring redundancy systems for temperature, humidity, CO2, and lighting. According to the Food and Agriculture Organization of the United Nations, controlled environment agriculture can increase crop yields by up to seven times per square meter compared to open field farming, while reducing water consumption by as much as ninety percent. As per the International Energy Agency, modern greenhouses equipped with thermal screens and heat recovery systems can lower energy intensity by forty percent compared to conventional heated structures. Adoption is accelerating among commercial growers in North America, Western Europe, and parts of Asia. This is driven by labor shortages, climate volatility, and rising demand for locally grown, as well as pesticide-free produce with consistent quality and extended shelf life.

MARKET DRIVERS

Demand for Year-Round Premium Produce Is Reshaping Investment in Controlled Environment Agriculture

Consumer preference for consistent availability of high-quality fruits, vegetables, and ornamentals regardless of season is driving the adoption of the high-end greenhouse market. According to the United States Department of Agriculture Economic Research Service, retail sales of greenhouse-grown tomatoes, peppers, and leafy greens in the United States increased by thirty-eight percent between two thousand twenty and two thousand twenty three, outpacing field-grown equivalents. Moreover, in the Netherlands, as per Wageningen University and Research, over ninety-five percent of commercial tomato production occurs in high-tech greenhouses, which enables twelve-month harvest cycles with Brix levels and flavor profiles superior to imported varieties. The global floral industry also relies on precision greenhouses. This convergence of retailer standards, consumer expectations, and agronomic performance is fueling capital expenditure in climate-controlled facilities.

Labor Shortages and Rising Wage Costs Are Accelerating Automation Adoption in Greenhouse Operations

A structural deficit in agricultural labor also accelerates the expansion of the high-end greenhouse market. This shortage is pushing commercial growers toward high-end greenhouses equipped with robotic systems and AI-driven management platforms. In Canada, according to Agriculture and Agri-Food Canada, over sixty percent of greenhouse operators cite labor scarcity as their top operational constraint, prompting investment in transplanting robots, autonomous harvesters, and computer vision-based grading systems. Companies like Priva and Ridder now offer integrated control systems that reduce manual intervention by up to seventy percent by enabling a single operator to manage over ten thousand square meters of cultivation space. The European Commission’s Farm to Fork Strategy also incentivizes automation through grants for labor-saving sustainable technologies. These macroeconomic and policy forces are transforming high-end greenhouses from luxury assets into essential infrastructure for economically viable specialty crop production.

MARKET RESTRAINTS

High Capital Expenditure and Financing Barriers Limit Adoption Among Mid-Sized and Independent Growers

The upfront investment required for high-end greenhouse systems remains prohibitive for many growers, particularly in developing economies and among family-owned farms, which degrades the growth rate of the high-end greenhouse market. According to Rabobank’s two thousand twenty three Global Greenhouse Monitor, the average cost to construct a fully automated glass greenhouse with hydroponics and climate control exceeds three hundred fifty dollars per square meter, with total project costs for a five-hectare facility exceeding seventeen million dollars. In India, the National Horticulture Board estimates that fewer than five percent of protected cultivation projects exceed one thousand square meters due to limited access to institutional credit and the absence of specialized agricultural infrastructure loans. Equipment import duties further inflate costs.

Regulatory Fragmentation and Permitting Delays Impede Timely Deployment of Advanced Facilities

The development of these greenhouses is frequently delayed or downsized due to inconsistent zoning laws, environmental permitting requirements, and utility interconnection policies that vary significantly across jurisdictions, thereby hindering the expansion of the high-end greenhouse market. These regulatory hurdles increase soft costs, deter foreign direct investment, and create uncertainty for equipment suppliers. Standardized national frameworks for controlled environment agriculture are lacking. This causes developers to face unpredictable timelines and compliance expenses that erode project economics and delay technology adoption.

MARKET OPPORTUNITIES

Integration of Renewable Energy and Closed Loop Water Systems Offers Pathway to Carbon Neutral Cultivation

The incorporation of solar photovoltaic roofs, geothermal climate buffers, and zero-discharge hydroponic systems opens new opportunities for the growth of the high-end greenhouse market. High-end greenhouses are increasingly serving as testbeds for sustainable agriculture through this integration. According to the International Renewable Energy Agency, greenhouse facilities equipped with bifacial solar panels and battery storage can meet up to eighty-five percent of their electricity demand on site, with surplus energy sold back to the grid during peak pricing windows. In the Netherlands, as per the Greenport initiative, over sixty commercial greenhouses now operate on closed-loop water systems, which recycle over ninety-eight percent of irrigation runoff and reduce fertilizer leaching to near zero. Companies are offering net positive energy greenhouse designs that generate more power than they consume annually.

Urban and Peri-Urban Deployment Enables Hyper-Local Food Systems and Reduces Supply Chain Vulnerability

These greenhouses are being strategically deployed within or adjacent to metropolitan zones to shorten supply chains, reduce food miles, and respond dynamically to retail demand, which provides fresh opportunities for the expansion of the high-end greenhouse market. According to the World Urbanization Prospects published by the United Nations, fifty-six percent of the global population now resides in urban areas, which creates dense markets for fresh produce within twenty-five kilometers of consumption points. Also, as per the Rockefeller Foundation’s YieldWise Initiative, urban greenhouses reduce post-harvest loss by up to ninety percent compared to imported produce. Municipalities are incentivizing such installations through tax abatements and expedited permitting, recognizing their role in food security and job creation. This geographic repositioning transforms greenhouses from rural production assets into urban infrastructure critical for resilient and just-in-time food systems.

MARKET CHALLENGES

Interoperability Gaps Between Hardware and Software Platforms Undermine Operational Efficiency

Many such greenhouses suffer from fragmented technology ecosystems where climate controllers, irrigation systems, and data analytics platforms operate in silos, which challenges the growth of the high-end greenhouse market. These conditions require manual reconciliation and real-time responsiveness. Inconsistent API standards and proprietary communication protocols prevent seamless data flow between sensors and actuators, which limits the effectiveness of predictive algorithms. Companies have begun adopting the automation framework to improve compatibility, but adoption remains below thirty percent among mid-tier suppliers. The lack of universal data ontologies also hinders benchmarking and knowledge transfer across facilities. Interoperability standards have not been enforced across the industry. As a result, growers will continue to experience suboptimal yields and inflated labor costs despite their significant capital investment in hardware.

Skilled Workforce Shortage in Greenhouse Technology Management Constricts Scalability and ROI

The rapid evolution of greenhouse automation has outpaced the availability of trained personnel capable of managing integrated control systems, interpreting agronomic data, and maintaining robotic equipment, which remains a key obstruction to the high-end greenhouse market. According to sources, only a few accredited academic programs globally offer specialized degrees in controlled environment agriculture technology, which produces fewer graduates annually than the industry demand, exceeding twelve thousand positions. A concerted industry and academic effort is needed to build a pipeline of systems-literate horticultural technologists so that the full potential of high-end greenhouse investments is realized, thus avoiding delayed payback periods and discouraging further adoption.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 7.9% |

| Segments Covered | By covering material, Product Type, Component Type, Application, and Region. |

|

Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Texas Greenhouse Company Inc., Nexus Corporation, Certhon, Dutch Greenhouse, Conley's Manufacturing and Sales, Netafim, The Toro Company, Nelson Irrigation, LumiGrow, Poly-Tex, Inc., United Greenhouse Systems, Inc. |

SEGMENTAL ANALYSIS

By Covering Materials Insights

The solid glass segment was the largest in the high-end greenhouse market and accounted for a 63% share in 2024. The dominance of the solid glass segment is driven by superior optical clarity, structural longevity, and thermal performance essential for precision horticulture. Glass transmits up to ninety-five percent of photosynthetically active radiation according to Wageningen University and Research, enabling optimal plant morphology and accelerated growth cycles. Unlike plastic films that degrade under UV exposure, architectural-grade glass retains performance for over thirty years, reducing lifecycle replacement costs. Premium retailers mandate glass-grown produce for flavor consistency, which supports grower preference for this material despite a higher initial outlay.

The plastic segment is predicted to witness the highest CAGR of 11.9% from 2025 to 2033. The rapid growth of the plastic segment is fueled by advancements in multi-layer co-extruded films embedded with anti-drip, anti-fog, and UV-stabilizing additives that extend functional life to seven years. Manufacturers like RKW Group and Plastika Kritis have introduced infrared reflective films that reduce nocturnal heat loss by up to thirty percent, which narrows the energy efficiency gap with glass. In sub-tropical regions, plastic’s lighter weight and wind load tolerance make it preferable for hurricane-resistant designs. Plastic is gaining traction without compromising agronomic outcomes as material science improves and emerging markets prioritize affordability.

By Product Insights

The tomatoes segment dominated the high-end greenhouse market by capturing 41.5% share in 2024. Factors such as year-round consumer demand, premium pricing for vine-ripened varieties, and proven scalability in controlled environments are driving the growth of the tomatoes segment. Some retailers prioritize greenhouse tomatoes for consistent size, color, and brix levels. Breeding programs by companies like Rijk Zwaan and Syngenta have developed disease-resistant cultivars tailored for hydroponic systems, reducing pesticide use by over ninety percent. The convergence of agronomic efficiency, market premium, and supply chain reliability solidifies tomatoes as the anchor crop for commercial greenhouse operators globally.

The pepper segment is estimated to register the fastest CAGR of 13.6% during the forecast period, owing to rising global consumption of specialty peppers, including mini sweets, shishitos, and colored bells, which command up to four times the price of commodity bell peppers. The United States Department of Agriculture reports that per capita pepper consumption in North America grew twenty-two percent between two thousand twenty and two thousand twenty-three, outpacing all other vegetables. High-end greenhouses enable precise control of capsaicin levels and fruit wall thickness, which allows growers to tailor heat profiles and texture for niche markets. Some retailers feature flavor-curated pepper medleys sourced exclusively from climate-controlled facilities. Greenhouse peppers are capturing premium shelf space and restaurant menus as culinary trends embrace global heat profiles and color diversity.

By Component Insights

The control systems and sensors segment led the high-end greenhouse market by occupying 34.7% share in 2024. The prominence of the control systems and sensors segment is because of their role as the central nervous system of high-end greenhouses, integrating data from hundreds of environmental and crop sensors to automate climate, irrigation, and nutrient delivery. These systems also generate audit trails, which are required by a portion of supermarket chains. The convergence of regulatory compliance, labor reduction, and yield optimization cements control systems as the highest value component segment.

The LED grow lights segment is anticipated to witness the fastest CAGR of 18.3% from 2025 to 2033, owing to dramatic improvements in photon efficiency and spectral tuning capabilities that enable crop-specific light recipes. According to Signify’s two thousand twenty four horticulture lighting report, modern LED fixtures now deliver three point two micromoles per joule, up from one point eight in two thousand eighteen, cutting electricity costs by over forty percent. In vertical greenhouse installations in Japan and Singapore, where natural light is limited, LED supplementation increases yields of leafy greens by up to two hundred percent. The California Energy Commission now offers rebates covering up to fifty percent of LED retrofit costs for commercial greenhouses that reduce grid load during peak hours. As per the research from the University of Arizona’s Controlled Environment Agriculture Center, far red and UV-A supplementation via LEDs can increase terpene concentration in culinary herbs by up to 60 percent.

By Application Insights

In 2024, the commercial segment held a substantial share of the high-end greenhouse market. The dominant commercial segment is driven by economies of scale, retailer procurement mandates, and institutional investment in food security infrastructure. According to Rabobank, the average commercial greenhouse project exceeds five thousand square meters and requires over eight million dollars in capital, placing it beyond the reach of individual consumers. Supermarket chains, including Aldi and Carrefour, source over thirty percent of their leafy greens and tomatoes from contracted greenhouse growers, which demand GlobalG.A.P. and SMETA compliance as prerequisites. In the Netherlands, commercial greenhouses generate over seven billion euros in annual export revenue, as per Statistics Netherlands. Labor automation and data-driven yield optimization further widen the efficiency gap between commercial and residential scales, which ensures sustained dominance of institutional operators.

The residential segment is likely to experience the fastest CAGR of 22.6% from 2025 to 2033. Factors like rising interest in hyper-local food production, wellness gardening, and smart home integration are boosting the expansion of the residential segment. Manufacturers like Planta Greenhouses and Soliculture now offer modular, app-controlled greenhouse kits under ten thousand dollars, with built-in irrigation and climate monitoring. Urban rooftop installations in cities are supported by municipal grants for food resilience. Social media platforms such as Instagram and TikTok have amplified visibility, with the hashtag #smartgreenhouse generating notable posts. Technology is miniaturizing, and consumer horticulture is evolving into a lifestyle investment, and residential adoption is accelerating beyond hobbyist niches.

REGIONAL ANALYSIS

North America Market Analysis

North America outperformed other regions in the global high-end greenhouse market by occupying a 38.4% share in 2024. Institutional capital deployment, retailer-driven supply chain mandates, and advanced automation adoption have significantly contributed to the growth of North America. According to sources, commercial-scale greenhouse development is expanding rapidly across the United States. As per studies, major companies are securing long-term supply agreements with leading retailers for crops like peppers and vine produce. According to research, greenhouse-grown vegetables represent a significant portion of fresh produce sales in key Canadian provinces. Venture capital funding is targeting technological upgrades and renewable energy improvements. Government programs and tax incentives are strengthening North America’s position in sustainable agriculture.

Europe Market Analysis

Europe followed closely in the high-end greenhouse market by capturing 35.1% share in 2024. Technological innovation, stringent food safety standards, and cohesive policy frameworks supporting decarbonization are the factors attributed to the rise of Europe in the global market. The Netherlands alone operates over ten thousand hectares of high-tech glasshouses, producing over sixty percent of Europe’s greenhouse tomatoes and peppers. Some retailers require blockchain traceability for all greenhouse-sourced items, which pushes growers toward digital integration. Strong vocational training pipelines and cooperative grower associations ensure knowledge transfer and operational consistency across thousands of facilities.

Asia Pacific Market Analysis

Asia Pacific is expected to be the most lucrative region in the high-end greenhouse market as the growth is concentrated in China, Japan, and increasingly India, where urbanization and food safety concerns are reshaping agricultural investment. Rising middle-class demand for pesticide-free produce and government-backed food resilience initiatives are accelerating adoption, with controlled environment agriculture now recognized as critical infrastructure in national food security plans.

Latin America Market Analysis

Latin America is moving ahead steadfastly in the high-end greenhouse market. Mexico and Brazil are primary growth enablers and are driven by export contracts with North American retailers, and climate volatility is forcing a transition from open field production. Supermarket chains allocate shelf space for controlled environment-grown labels, with consumer surveys indicating willingness to pay more. Government incentives for water-efficient agriculture and foreign direct investment in agtech are accelerating scale, which positions Latin America as a strategic sourcing hub for counter-seasonal production.

Middle East And Africa Market Analysis

Middle East and Africa are predicted to grow in the high-end greenhouse market during the forecast period, owing to the United Arab Emirates, Saudi Arabia, and South Africa, where water scarcity and food import dependency are driving investment in enclosed-loop cultivation. According to sources, the United Arab Emirates is expanding its greenhouse infrastructure through national initiatives aimed at improving local food production. As per studies, Saudi Arabia is investing heavily in high-tech greenhouse projects that utilize advanced cooling and irrigation systems. As per research, greenhouse farming in South Africa is helping ensure a more reliable supply of fresh produce in regions affected by drought. Though nascent, the region’s focus on sovereign food production and technology transfer partnerships is laying the foundations for strategic and high-margin expansion in arid climate zones.

COMPETITIVE LANDSCAPE

The gasoline fuel additives market is characterized by intense rivalry among multinational chemical manufacturers competing on performance efficacy, regulatory compliance, and supply chain reliability. Players differentiate through proprietary formulations that enhance octane rating, inhibit deposit formation, and reduce tailpipe emissions. Innovation cycles are rapid, driven by evolving fuel standards such as Euro 7 and Tier 3. Regional competitors focus on cost leadership and localized distribution, while global leaders leverage R and D scale and long-term contracts with refiners. Mergers and acquisitions are common as firms consolidate intellectual property and expand geographic reach. Technical service teams play a vital role in maintaining customer loyalty through on-site diagnostics and customized additive packages. Regulatory pressures around sustainability are accelerating investment in bio-based and low-toxicity chemistries, which reshape competitive dynamics.

KEY MARKET PLAYERS

A few of the market players in the global high-end greenhouse market include

- Texas Greenhouse Company Inc.

- Nexus Corporation

- Priva Holding B V

- Ridder Group

- Certhon

- Dutch Greenhouse

- Conley's Manufacturing and Sales

- Netafim

- The Toro Company

- Nelson Irrigation

- LumiGrow

- Poly-Tex, Inc.

- United Greenhouse Systems, Inc

Top Players In The Market

- Certhon Group, a Netherlands-based engineering firm, specializes in designing and constructing fully automated high-end greenhouses for global clients in horticulture and vertical farming. These innovations reinforce Certhon’s reputation for sustainable, future-ready greenhouse infrastructure and expand its footprint in North America and the Middle East within the high-end greenhouse market.

- Priva Holding B.V., headquartered in the Netherlands, is a global leader in climate control and process automation systems for high-tech greenhouses. These advancements enhance operational efficiency for commercial growers and solidify Priva’s role as the central nervous system provider within the high-end greenhouse market.

- Ridder Group, a Dutch innovator in greenhouse automation, delivers integrated hardware and software solutions for climate, energy, and crop management. These developments strengthen Ridder’s value proposition for institutional growers seeking scalable, labor-efficient operations within the high-end greenhouse market.

Top Strategies Used By The Key Market Participants

Leading players in the high-end greenhouse market prioritize full system integration by developing interoperable platforms that unify climate, irrigation, and lighting controls under a single dashboard. They invest heavily in renewable energy retrofits such as geothermal buffering and rooftop photovoltaics to achieve carbon neutrality and reduce operational costs. Strategic academic partnerships accelerate agronomic innovation, particularly in spectral lighting and CO2 optimization. Modular and scalable designs enable deployment across diverse geographies and facility sizes. Companies also offer performance-based financing and yield guarantee programs to de-risk adoption for growers. Digital twin technology and predictive analytics are increasingly embedded to enable remote diagnostics and preemptive maintenance, which enhances uptime and ROI.

RECENT MARKET NEWS

In April 2024, DynaTouch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen its greenhouse market presence.

MARKET SEGMENTATION

This research report on the global high-end greenhouse market is segmented and sub-segmented into the following categories.

By Covering Materials

- Plastic

- Solid Brush Cleaners

- Others

By Product Type

- Tomatoes Greenhouse

- Cucumber Greenhouse

- Eggplant Greenhouse

- Pepper Greenhouse

- Others

By Component Type

- HVAC Systems

- Control Systems & Sensors

- Valves & Pumps

- Irrigation System

- Material Handling

- LED Grow Lights

- Others

By Application

- Residential

- Commercial

By Region

- North America

- Asia Pacific

- Europe

- Latin America

- Middle East & Africa

Frequently Asked Questions

what is the current market size of the global end-greenhouse market?

The global high-end greenhouse market size is expected to reach USD 2436.24 million in 2024.

what segments are covered in the global end-greenhouse market?

It is segmented by covering material, product type, component type, and application are covered n the global end-greenhouse market.

what are the market drivers that are driving the end-greenhouse market?

The benefits of the adoption of this farming technique are leveraging the scope to increase the production rate of the crop, which is propelling the growth rate of the market.

which is the leading region in this market?

The US and Canada are highly developed countries where modern technology is booming in farming practices.

who are the key market players involved in this industry?

Texas Greenhouse Company Inc., Nexus Corporation, Certhon, Dutch Greenhouse, Conley's Manufacturing and Sales Netafim, etc...

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com