Global Hybrid Aircraft Market Size, Share, Trends & Growth Forecast Report By Aircraft Type, By Lift Technology, By Propulsion Architecture, and By Region (North America, Europe, Asia Pacific, Latin America, Middle East & Africa) – Industry Analysis and Forecast, 2026 to 2034

Global Hybrid Aircraft Market Summary

Market Size & Growth

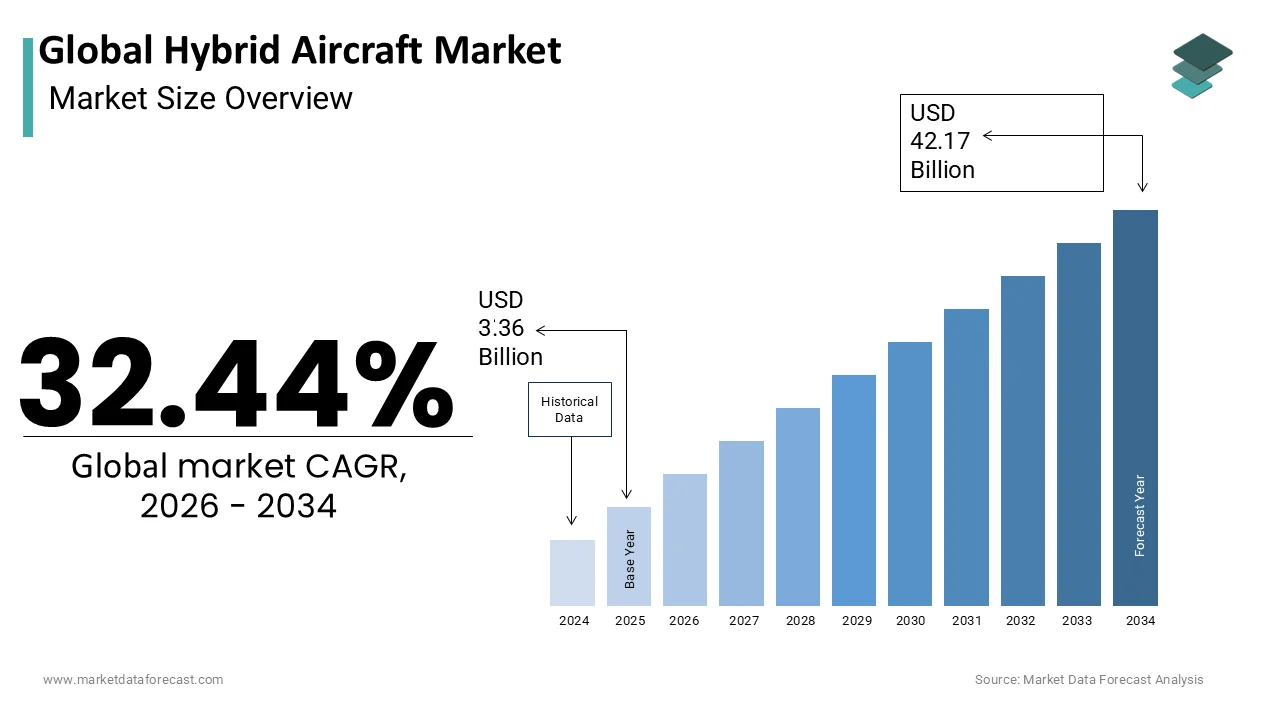

- The global hybrid aircraft market was valued at USD 3.36 billion in 2025.

- Expected to reach USD 4.46 billion in 2026 and USD 42.17 billion by 2034, growing at a CAGR of 32.44% from 2026 to 2034.

- North America led with a 40.1% share in 2025; Asia Pacific is the fastest-growing region.

Key Market Segments

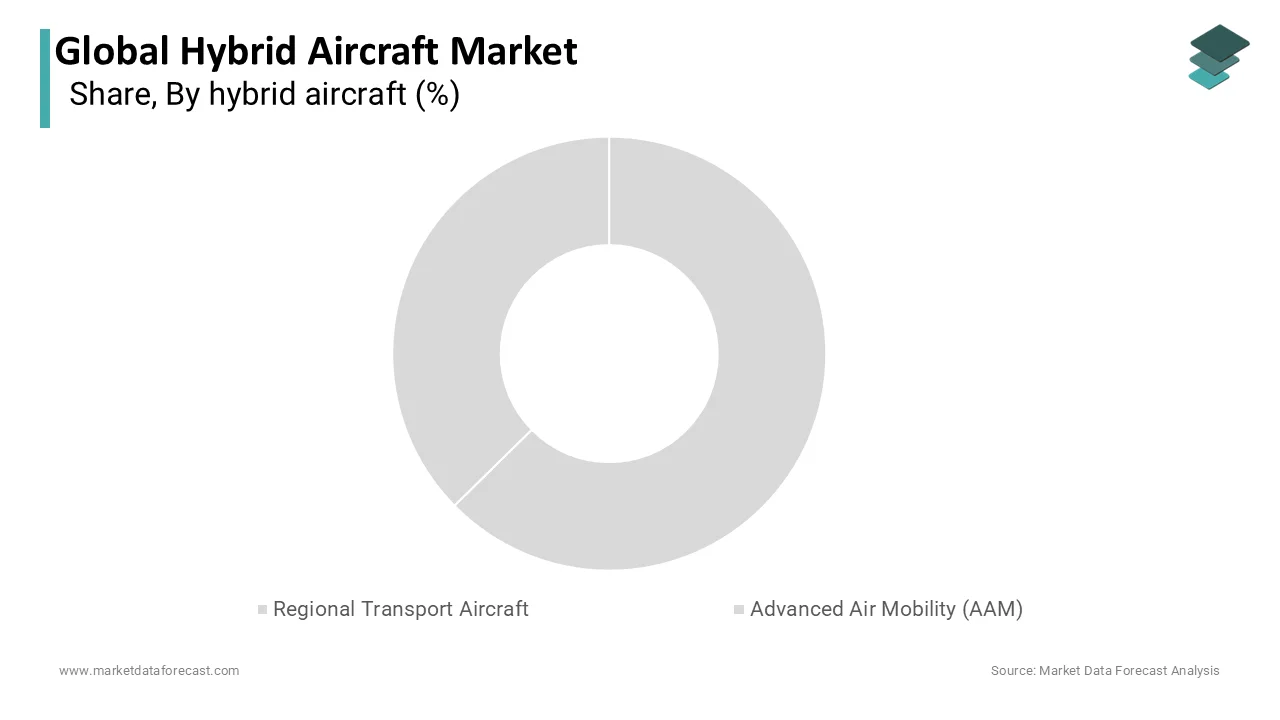

- By aircraft type: Regional Transport Aircraft (41.8% share, 2025), Advanced Air Mobility (39.6% CAGR, 2026–2034)

- By lift technology: Conventional Takeoff and Landing (53.9% share, 2025), Vertical Takeoff and Landing (39.2% CAGR, 2026–2034)

- By propulsion architecture: Parallel Hybrid (50.7% share, 2025), Series Hybrid (37.4% CAGR, 2026–2034)

Key Drivers

- Stringent environmental regulations, including the EU's Fit for 55 package targeting a 55% reduction in net greenhouse gas emissions by 2030 versus 1990 levels.

- Rising jet fuel costs, which account for 20–30% of airline operating costs, pushing carriers toward fuel-saving hybrid propulsion.

- Expansion of regional air mobility, with short-haul flights making up around 30% of global departures.

Key Players

Airbus SE, The Boeing Company, RTX Corporation (Pratt & Whitney), Rolls-Royce Holdings plc, Safran S.A., GE Aerospace, Embraer S.A., Textron Inc., Ampaire Inc., VoltAero S.A.S., Heart Aerospace AB, Pipistrel d.o.o. (Textron eAviation).

Global Hybrid Aircraft Market Size

The Global Hybrid Aircraft Market is projected to grow from USD 3.36 billion in 2025 to USD 4.46 billion in 2026 and reach USD 42.17 billion by 2034, registering a CAGR of 32.44% during the forecast period from 2026 to 2034.

A hybrid aircraft combines traditional fossil-fuel engines with electric motors to power flight. This dual power architecture aims to optimize fuel efficiency, reduce carbon emissions, and lower operational noise levels compared to traditional turbine-powered aircraft. As global aviation faces increasing pressure to meet sustainability targets, hybrid technology offers a pragmatic transitional solution before full electrification becomes viable for larger airframes. In 2021, the International Air Transport Association committed member airlines to achieving net-zero carbon emissions by 2050, identifying sustainable aviation fuels (SAF) as the primary mechanism for decarbonization. To support alternative aircraft development, the European Union Aviation Safety Agency established the Special Condition SC E-19 framework to standardize safety and airworthiness certifications for electric and hybrid propulsion architectures. As per the International Energy Agency, global aviation accounts for roughly 2.5% of energy-related carbon dioxide emissions, emphasizing the demand for low-carbon fuels and alternative engine designs. Hybrid aircraft are particularly suited for regional and short-haul flights, which constitute a significant portion of daily air traffic. The U.S. Government Accountability Office highlights that electric and hybrid-electric aircraft are ideally suited for short-to-medium-range flights, addressing a domestic market segment where roughly half of all routes span under 500 miles.

Furthermore, the rising cost of jet fuel drives airlines to seek more economical propulsion options. Hybrid systems promise a reduction in fuel burn during specific flight phases such as takeoff and climb. This technological evolution aligns with broader industrial trends towards decarbonization and energy diversification, positioning hybrid aircraft as a critical component of future sustainable aviation infrastructure.

MARKET DRIVERS

Stringent Environmental Regulations and Carbon Reduction Mandates

Strict environmental regulations and global mandates for carbon reduction are primary drivers for the hybrid aircraft market. This compels manufacturers and operators to adopt cleaner propulsion technologies. Governments and international bodies are implementing aggressive policies to curb greenhouse gas emissions from the aviation sector,r which is historically difficult to decarbonize. According to the International Civil Aviation Organization, the CORSIA scheme requires airlines to offset carbon emissions exceeding 85% of 2019 baseline levels. The European Union has included aviation in its Emissions Trading System, em forcing carriers to purchase allowances for their carbon output, which significantly increases operating costs for conventional aircraft. As per the European Commission,sion the Fit for 55 package aims to reduce net greenhouse gas emissions by at least 55 percent by 2030 compared to 1990 levels, directly impacting aviation strategies. Hybrid aircraft offer a tangible pathway to compliance by reducing fuel consumption and associated emissions on regional routes. The Federal Aviation Administration in the United States has also established certification standards for emerging aircraft technologies,s encouraging innovation in hybrid electric propulsion. Airlines facing potential fines and restricted access to certain airports due to noise and emission limits are increasingly interested in hybrid solutions. These regulatory pressures create a compelling business case for investing in hybrid technology as it allows operators to maintain profitability while adhering to evolving environmental laws. The threat of stricter future regulations further accelerates research and development efforts, ensuring that hybrid aircraft remain a focal point for sustainable aviation growth.

Rising Fuel Costs and Operational Efficiency Demands

The continuous demand for operational efficiency and the volatility of jet fuel prices are accelerating the adoption of hybrid aircraft, which further contributes to the expansion of the global market. Thus, airlines are leveraging this technology to stabilize costs and increase profitability. Fuel represents one of the largest expense categories for airlines,s often accounting for 20 to 30 percent of total operating costs depending on market conditions. According to the International Air Transport Association, average jet fuel prices fluctuated significantly in recent years, with spikes exceeding 100 dollars per barrel, causing financial strain on carriers globally. Hybrid propulsion systems mitigate this risk by reducing fuel consumption through optimized energy management, where electric motors assist during high-power phases such as takeoff and climb. As per the United States Energy Information Administration, global crude oil prices remain susceptible to geopolitical tensions and supply chain disruptions, making long-term cost predictability difficult for traditional aircraft operations. Hybrid aircraft can achieve fuel savings on short-haul routes by utilizing electric power for taxiing and initial ascent t, thereby reducing reliance on expensive kerosene. Additionally, the reduced mechanical wear on combustion engines due to electric assistance lowers maintenance costs and extends component life cycles. The Federal Aviation Administration highlights that operational efficiency improvements are critical for airline sustainability in a competitive market. By lowering both fuel and maintenance expenses, hybrid aircraft offer a compelling economic advantage. This financial incentive motivates airlines to invest in hybrid fleets, particularly for high-frequency regional routes where cumulative savings are substantial. The desire for cost stability in an unpredictable energy market thus acts as a powerful catalyst for the commercialization of hybrid aviation technologies.

MARKET RESTRAINTS

Technological Immaturity and Battery Energy Density Limitations

The current immaturity of hybrid propulsion technology and limitations in battery energy density are major restraints to the hybrid aircraft market. While electric motors are well understood, the integration of high-capacity batteries that can deliver sufficient power for flight without adding excessive weight remains a significant engineering challenge. According to the National Aeronautics and Space Administration, current lithium-ion batteries have an energy density of approximately 250 watt-hours per kilogram,m which is far below the 800 to 1000 watt-hours per kilogram required for viable long-range hybrid flight. This disparity limits the payload capacity and range of hybrid aircraft, making them less competitive than traditional turboprops for many commercial routes. Furthermore, the thermal management of large battery packs during flight poses safety risks that require complex and heavy cooling systems. As per the Federal Aviation Administration, certification processes for novel propulsion systems are lengthy and rigorous due to the lack of established precedents and safety data. Manufacturers must demonstrate unprecedented levels of reliability and fail-safe mechanisms, which increase development time and costs. The rapid pace of battery technology evolution also creates uncertainty for investors who fear that early adopters may face obsolescence as newer, superior chemistries emerge. The performance constraints of current technology will limit the market appeal of hybrid aircraft to niche regional applications rather than broad commercial adoption. This restriction will persist until breakthroughs in solid-state batteries or other high-energy-density storage solutions occur.

High Development Costs and Infrastructure Deficiencies

Substantial development costs and the lack of specialized infrastructure for charging and maintenance are significant impediments to the hybrid aircraft market. Designing and certifying a new aircraft platform with hybrid propulsion requires billions of dollars in investment, which poses a high financial barrier for manufacturers and startups alike. Airlines are hesitant to commit to unproven technologies without guaranteed returns,s especially when traditional aircraft remain readily available and financially predictable. An infrastructure assessment by the U.S. Government Accountability Office highlights that most commercial airports face severe electrical constraints, lacking the grid capacities and high-voltage megawatt chargers needed for alternative aircraft. Retrofitting airports to support hybrid aircraft requires significant capital expenditure and coordination with utility providers, rs which slows down deployment timelines. A regulatory review by the U.S. Government Accountability Office outlines that deploying high-voltage aircraft requires completely new ground-handling safety standards, specialized maintenance gear, and updated training protocols. Additionally,lly the supply chain for critical components such as rare earth magnets and advanced semiconductors is constrained,ined leading to potential delays and increased costs. The absence of standardized charging protocols and interoperability frameworks further complicates operations for airlines considering mixed fleets. Until the ecosystem matures and costs decrease through economies of scale, the financial and logistical hurdles will restrain the growth of the hybrid aircraft market, limiting its penetration to well-funded pilot programs and specialized operators.

MARKET OPPORTUNITIES

Expansion of Regional Air Mobility and Short Haul Connectivity

The growing emphasis on regional air mobility and the need for enhanced short-haul connectivity offer significant opportunities for the hybrid aircraft market. Many remote and underserved communities lack reliable air service due to the high operating costs of traditional aircraft on low-density routes. Hybrid aircraft with their lower fuel consumption and reduced noise profiles are ideally suited for these markets, enabling economically viable operations. Global tracking from the Air Transport Action Group shows that short-haul regional flights make up around 30% of global departures, highlighting a major sector positioned for alternative propulsion upgrades. Hybrid propulsion can reduce operating costs,s making it feasible to serve smaller airports with lower passenger volumes. The Federal Aviation Administration supports initiatives to improve regional connectivity through modernization programs that encourage the use of advanced air mobility solutions. The European Commission’s Single European Sky initiative seeks to reorganize European air traffic management, reducing flight delays and lowering overall fuel burn across all regional carriers. Governments in various countries are offering subsidies and grants for projects that enhance rural accessibility and reduce environmental impact. Hybrid aircraft can operate from shorter runways and produce less noise, allowing them to access airports closer to city centers, which improves convenience for travelers. This capability opens new market segments for airlines seeking to differentiate their services and capture demand in underserved areas. The ability to provide frequent, affordable, andeco-friendlyy connections between secondary cities and hubs positions hybrid aircraft as a key enabler of expanded regional networks, driving growth in this segment.

Integration with Renewable Energy and Sustainable Aviation Fuels

The potential for integrating hybrid aircraft with renewable energy sources and sustainable aviation fuels provides a clear path for enhancing environmental benefits and operational flexibility, which is anticipated to boost the expansion of the global market. Hybrid systems can be designed to utilize electricity generated from solar,r wind, or other renewable sources for charging,g reducing the overall carbon footprint of flight operations. According to the International Energy Agency,cy the global share of electricity from renewable sources reached 30 percent in 2,025 providing a cleaner energy mix for powering electric components of hybrid aircraft. This synergy allows airlines to market their services as genuinely green, thereby appealing to environmentally conscious consumers and corporate clients with strict sustainability mandates. As per the International Air Transport Association,ation the use of sustainable aviation fuels in the combustion engine portion of hybrid systems can further reduce lifecycle emissions by up to 80 percent compared to conventional jet fuel. The combination of electric propulsion and sustainable fuels creates a multi-layered approach to decarbonization that maximizes environmental benefits. Governments and regulatory bodies are increasingly supporting the production and distribution of sustainable aviation fuels through incentives and mandates. The Federal Aviation Administration encourages research into integrated energy systems that optimize the use of renewable electricity and biofuels. Hybrid aircraft serve as a flexible platform that can adapt to evolving energy landscapes, allowing operators to leverage the cheapest and cleanest energy sources available at any given time. This adaptability future-proofs investments and aligns with global trends towards circular economy principles. Manufacturers and airlines can unlock new value propositions by positioning hybrid aircraft within a broader sustainable energy ecosystem. Consequently, this ensures long-term competitiveness in a low-carbon economy.

MARKET CHALLENGES

Regulatory Uncertainty and Certification Complexities

Regulatory uncertainty and the complex certification process for novel hybrid propulsion systems are major challenges to the hybrid aircraft market. Authorities are struggling to establish standardized safety frameworks. Unlike conventional aircraft, which have decades of operational data and established certification pathways,s hybrid aircraft introduce new risks related to high-voltage systems, battery thermal runaway and software-controlled power management. According to the Federal Aviation Administration, the certification of hybrid electric aircraft requires extensive testing and validation to ensure safety under all flight conditions,s which prolongs the time to market. The lack of harmonized global standards means that manufacturers may face different requirements in different jurisdictions, increasing development costs and complexity. The regulatory gap creates ambiguity for manufacturers and insurers who must assess risks without clear guidelines. The International Civil Aviation Organization is working towards global standards,s but the process is slow due to the rapid pace of technological change. Airlines are reluctant to invest in aircraft that may face regulatory hurdles or restrictions in key markets.

Furthermore, the liability issues surrounding battery failures and software glitches remain unresolved, creating legal uncertainties. Comprehensive and internationally recognized certification standards are not yet established. As a result, the regulatory landscape remains a significant challenge, slowing down the commercialization and adoption of hybrid aircraft technologies across the global aviation industry.

Supply Chain Vulnerabilities for Critical Components

Vulnerabilities in the supply chain for critical components, such as batteries, semiconductors, and rare earth materials, are a significant hurdle for the hybrid aircraft market. The production of high-performance batteries relies heavily on materials like lithium cobalt and nickel, which are subject to geopolitical tensions and supply constraints. In addition, the United Nations Conference on Trade and Development projects global lithium demand to increase dramatically over the next two decades, introducing supply risks for battery-reliant industries. The semiconductor shortage that affected various industries also impacts the availability of power electronics and control systems essential for hybrid propulsion. As per the International Trade Administration, trade restrictions and export controls on critical minerals can disrupt supply chains and increase lead times for manufacturers. The concentration of battery production in a few countries creates dependency risks that can affect the stability of the hybrid aircraft industry. The Aerospace Industries Association highlights that diversifying the supply chain is crucial but requires significant time and investment to develop alternative sources and processing capabilities. Additionally,lly the recycling infrastructure for aviation-grade batteries is not yet mature, raising concerns about long-term sustainability and material recovery. Manufacturers must navigate these complexities while ensuring consistent quality and reliability of components. Any disruption in the supply of critical materials can delay production schedules and increase costs, undermining the economic viability of hybrid aircraft. Addressing these supply chain challenges requires strategic partnerships and investment in domestic manufacturing capabilities to ensure resilience and continuity in the face of global market fluctuations.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Aircraft Type, Lift Technology, Propulsion Architecture, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | North America Europe Asia-Pacific Latin America Middle East & Africa |

| Market Leaders Profiled | Airbus SE, The Boeing Company, RTX Corporation (Pratt & Whitney), Rolls-Royce Holdings plc, Safran S.A., GE Aerospace, Embraer S.A., Textron Inc., Ampaire Inc., VoltAero S.A.S., Heart Aerospace AB, Pipistrel d.o.o. (Textron eAviation). |

SEGMENTAL ANALYSIS

By Aircraft Type Insights

The regional transport aircraft segment dominated the hybrid aircraft market and accounted for a 41.8% share in 2025. This dominance of the segment was driven by the ability of manufacturers to retrofit existing turboprop designs with hybrid electric systems,s which significantly reduce certification timelines and development costs for airlines operating sub-150000 km routes. The established infrastructure at secondary airports allows these aircraft to operate efficiently without requiring new vertiports or extensive ground support modifications. In May 2025, Deutsche Aircraft rolled out its first D328eco test aircraft at its Oberpfaffenhofen facility, establishing a manufacturing timeline aimed at commercial entry into service by 2027. Airlines prioritize these platforms because they offer immediate fuel savings and lower operational expenses compared to conventional turboprops while maintaining payload capacity and range requirements for regional connectivity. The maturity of the supply chain for regional airframes further supports this segment leadership as maintenance providers can adapt existing procedures quickly to handle hybrid components. This practical approach to decarbonization appeals to fleet managers who seek to meet environmental regulations without disrupting their current route networks or incurring prohibitive capital expenditures for entirely new aircraft types.

On the other hand, the advanced air mobility segment is expected to exhibit a noteworthy CAGR of 39.6% between 2026 and 2034. This rapid expansion of the segment is propelled by increasing urbanization and the urgent need for sustainable short-distance transportation solutions in congested metropolitan areas. Vertical Aerospace secured 90 million USD in fresh equity funding in January 2025 to accelerate certification flights for its VX4 model at Cotswold Airport, which demonstrates strong investor confidence in this emerging sector. Municipalities are actively commissioning test hubs and vertiports to support these operations, with Rotterdam Port opening Europe's first commercial vertiport ahead of schedule to validate passenger handling procedures. Cargo operators are also evaluating lift-plus-cruise configurations for middle-mile logistics, which creates additional demand before passenger services fully mature. The flexibility of vertical takeoff capabilities allows these aircraft to bypass traditional runway constraints and access densely populated urban centers directly. Government backing through pilot projects and favorable regulatory frameworks further accelerates commercialization efforts as cities seek to reduce traffic congestion and lower emissions from ground transportation.

By Lift Technology Insights

The conventional takeoff and landing technology segment led the hybrid aircraft market and captured a 53.9% share in 2025. This leading position of the segment was mainly attributed to the compatibility of CTOL aircraft with existing airport infrastructure,e which eliminates the need for costly new construction projects. Operators can utilize current runway slots and maintenance facilities, thereby reducing entry barriers and operational disruptions during the transition to hybrid propulsion. Airlines favor CTOL platforms because they align with current pilot training programs and air traffic control procedures,s which simplifies integration into existing fleets. The proven reliability of fixed-wing aerodynamics combined with hybrid electric propulsion offers a balanced solution for regional carriers seeking to improve sustainability metrics while maintaining operational familiarity and safety standards recognized by global aviation authorities.

However, the vertical takeoff and landing technology segment is predicted to witness the highest CAGR of 39.2% during the forecast period. This swift growth of the segment is fueled by the rising demand for urban air mobility solutions that can operate in space-constrained environments where traditional runways are unavailable. Beta Technologies doubled its charging station network across the eastern seaboard of the United States, which de-risks cross-country ferry flights during certification phases and supports broader adoption. The ability of VTOL aircraft to access rooftop landing pads and small urban clearings makes them ideal for point-to-point transportation in densely populated cities. Municipal governments are increasingly allocating funds for vertiport development as they recognize the potential of these aircraft to alleviate ground traffic congestion and provide rapid emergency response capabilities. The modular design of many VTOL platforms allows for scalable production and easier maintenance, which appeals tostart-upp operators entering the market. As battery energy density improves and noise reduction technologies advance, public acceptance of VTOL operations continues to rise,e creating a favorable environment for widespread deployment in both passenger and cargo applications.

By Propulsion Architecture Insights

In 2025, the parallel hybrid propulsion architecture segment held the majority share of 50.7% of the hybrid aircraft market because of the technical simplicity of integrating electric motors alongside existing combustion engines, es which allows for incremental improvements in fuel efficiency without radical redesigns of aircraft structures. GE Aerospace partnered with NASA to embed electric motor generators into commercial turbofan cores, res which provides airlines with redundancy and performance benefits while leveraging familiar maintenance protocols. The parallel configuration enables simultaneous use of fuel and electric power, ower which optimizes energy consumption during different flight phases such as takeoff and cruise. Airlines favor this architecture because it minimizes weight penalties associated with dual propulsion systems and allows for smoother transitions between power sources. The availability of established supply chains for both combustion and electric components reduces manufacturing costs and accelerates time to market for new hybrid models. This pragmatic approach appeals to risk-averse operators who seek proven technology paths rather than unproven experimental systems, ensuring reliable service delivery and predictable operational costs throughout the aircraft lifecycle.

But the series hybrid propulsion segment is anticipated to witness the fastest CAGR of 37.4% between 2026 and 2034 due to advancements in smart grid control systems that reduce energy conversion losses and improve overall efficiency. Safran Electrical and Power released the ENGINeUS family of motors scaling from 100 kW to 1 M, W which complements GENeUS generators suited for distributed power sources. The series architecture allows for greater flexibility in component placement since the combustion engine does not need to be mechanically linked to the propellers, rs enabling optimized aerodynamic designs. Turbo electric concepts exploring boundary layer ingestion further enhance cruise efficiency by reducing drag. The decoupling of power generation from thrust production enables innovative aircraft configurations that were previously impossible with traditional mechanical linkages. This architectural freedom attracts designers seeking to maximize performance and sustainability metrics through novel airframe and propulsion integrations that leverage the full potential of electric drive systems.

COUNTRY LEVEL ANALYSIS

North America Hybrid Aircraft Market Analysis

North America remained the largest regional market and occupied a 40.1% share in 2025. The regional market was driven by a robust aerospace ecosystem supported by significant government funding and advanced research initiatives such as the NASA Electrified Powertrain Flight Demonstration program. American Airlines signed a conditional agreement for 100 hydrogen-electric engines from ZeroAvia, while United Airlines backed JetZero with a provisional order for up to 200 fuel-efficient blended-wing-body aircraft. State-level support further strengthens the supply chain. In June 2025, JetZero selected Greensboro, North Carolina, for its major production facility, projected to generate over 500 manufacturing jobs to support its blended-wing-body fleet. The Federal Aviation Administration continues to refine certification frameworksthat provides clarity for manufacturers and accelerate commercialization timelines. The presence of major industry players like GE Aerospace and RTX Corporation ensures continuous innovation and investment in hybrid technologies. The combination of regulatory support, corporate commitment,t and technological leadership establishes North America as the primary driver of global hybrid aircraft adoption and market expansion.

Europe Hybrid Aircraft Market Analysis

Europe followed closely behind in the global market through substantial public finance instruments and collaborative research programs. The European Innovation Council granted €17.5 million to AURA Aero, complementing institutional backing from the EU’s HECATE consortium to develop high-voltage hybrid-electric distribution systems. Airbus, Daher, and Safran completed the EcoPulse flight campaign in December 2024, logging 100 flight hours that validated six motor distributed propulsion technologies. VoltAero opened a final assembly hall for the Cassio family in Nouvelle-Aquitaine, signaling Europe's readiness to shift from prototypes to serial production. The inclusion of aviation activities in the EU Taxonomy Regulation provides transparent criteria for directing sustainable private capital toward low-emission transport infrastructure. These coordinated efforts across member states create a supportive environment for innovation and ensure that European companies remain competitive in the evolving global landscape of sustainable aviation technologies.

Asia Pacific Hybrid Aircraft Market Analysis

Asia Pacific is quickly growing in the global market. China drives this expansion. The country is expanding its low-altitude ecosystem, with state planning targeting a market value of 2 trillion CNY by 2030 through the deployment of autonomous eVTOLs and regional hybrid aircraft. The Civil Aviation Administration of China granted EHang the world’s first Type Certificate for a pilotless passenger eVTOL aircraft. Battery developer CATL aims to release an 8-ton civil electric airliner by 2027–2028, leveraging high-density condensed matter battery technology. Australia contributed to regional growth by allocating grants to Dovetail Electric Aviation for regional aircraft retrofits targeting the Pacific market. Increasing air travel demand and government-supported aerospace programs in Japan, India, and South Korea further accelerate market expansion. The convergence of manufacturing capabilities, es policy support, and rising passenger traffic positions Asia Pacific as a critical growth engine for the global hybrid aircraft industry in the coming decade.

Latin America Hybrid Aircraft Market Analysis

Latin America shows gradual expansion in the hybrid aircraft market due to the need for cost-efficient regional connectivity and environmental sustainability. Brazil leads the regional market with investments in infrastructure and research initiatives aimed at reducing aviation emissions. The region benefits from growing awareness of green transportation solutions among passengers and regulators who encourage airlines to explore hybrid options for short-haul routes. Although current market share remains modest compared to North America and Europe, ongoing partnerships with global manufacturers and local startups foster innovation. The vast geographical diversity and presence of remote communities create unique opportunities for hybrid aircraft to provide essential services where traditional infrastructure is limited. As economic conditions improve and regulatory frameworks evolve,e Latin America is poised to increase its participation in the global hybrid aircraft market through targeted investments and strategic collaborations.

Middle East and Africa Hybrid Aircraft Market Analysis

The Middle East and Africa region is predicted to grow notably in the hybrid aircraft market over the forecast period, od supported by investments in sustainable aviation infrastructure. The United Arab Emirates leads regional efforts with initiatives aimed at reducing carbon footprints and enhancing air transport efficiency. Saudi Arabia also contributes through a vision for economic diversification, which includes modernizing the aviation sector and eco-friendly technologies. While the current market size is small, the region's growth potential is significant due to increasing air travel demand and government commitments to environmental goals. Partnerships with international aerospace companies facilitate technology transfer and capacity building, enabling local operators to adopt hybrid solutions. As awareness of climate change impacts grows and fuel prices fluctuate,e the Middle East and Africa are expected to play an increasingly important role in the global adoption of hybrid aircraft technologies for both passenger and cargo operations.

COMPETITIVE LANDSCAPE

The competitive landscape of the hybrid aircraft market is characterized by intense rivalry between established aerospace giants and innovative start-ups seeking to disrupt traditional aviation models. Major incumbents leverage their extensive manufacturing capabilities and global supply chains to develop hybrid solutions that integrate seamlessly with existing fleet operations. Meanwhile, emerging companies focus on novel architectures such as distributed propulsion and vertical takeoff capabilities to address specific niche markets like urban air mobility and regional connectivity. Competition is further intensified by rapid technological advancements in battery chemistry and electric motor efficiency, which constantly redefine performance benchmarks and cost structures. Regulatory pressures and environmental mandates drive all participants to accelerate their development timelines and secure early mover advantages in key geographic regions. Strategic alliances between aircraft manufacturers and technology providers have become common as firms recognize the complexity of developing safe and efficient hybrid systems. Intellectual property protection plays a crucial role as companies vie for patents related to power management software and thermal control systems. The race to achieve certification first creates a dynamic environment where speed to market often determines long-term success and brand recognition among airline customers who are increasingly prioritizing sustainability in their procurement decisions today.

KEY MARKET PLAYERS

Some of the companies that are playing a dominant role in the Global Hybrid Aircraft Market include

- Airbus SE

- The Boeing Company

- RTX Corporation (Pratt & Whitney)

- Rolls-Royce Holdings plc

- Safran S.A.

- GE Aerospace

- Embraer S.A.

- Textron Inc.

- Ampaire Inc.

- VoltAero S.A.S.

- Heart Aerospace AB

- Pipistrel d.o.o. (Textron eAviation)

TOP LEADING PLAYERS IN THE MARKET

- Airbus leads innovation through its ZeroE initiative, ve which focuses on hydrogen and hybrid electric propulsion technologies for future aircraft. The company actively collaborates with engine manufacturers and research institutions to develop scalable solutions for regional short-haul flights. Airbus recently completed extensive flight testing of its EcoPulse demonstrator, which validated distributed propulsion concepts and provided critical data for certification processes. This commitment to sustainable aviation ensures that Airbus remains at the forefront of technological advancements while addressing environmental concerns raised by regulators and passengers globally.

- Boeing strengthens its position by investing heavily in autonomous flight systems and hybrid electric architectures through its subsidiary Wisk Aero. The company leverages its extensive aerospace expertise to integrate advanced battery technologies with traditional propulsion systems for improved efficiency. Boeing recently partnered with NASA to explore turbo-electric concepts that promise significant fuel savings for narrow-body aircraft. These strategic initiatives enable Boeing to offer competitive solutions that meet evolving regulatory standards and customer demands for quieter and cleaner air travel options worldwide.

- Heart Aerospace drives market growth with its ES 30 hybrid electric regional aircraft designed for sustainable short-distance operations. The company secured substantial orders from major airlines, including United Airlines and Air Canada, which validates its design approach and commercial viability. Heart Aerospace focuses on optimizing battery usage during takeoff and landing while relying on sustainable aviation fuel for cruise phases. This balanced strategy allows operators to reduce emissions immediately without waiting for full electric infrastructure development,nt thereby accelerating the adoption of hybrid technologies in the global aviation sector significantly.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the hybrid aircraft market primarily focus on strategic partnerships and collaborations to accelerate technology development and reduce financial risks. Companies frequently engage in joint ventures with battery manufacturers and software developers to create integrated propulsion systems that meet stringent safety standards. Investment in research and development remains a central strategy as firms seek to improve energy density and reduce weight penalties associated with hybrid components. Manufacturers also prioritize regulatory engagement to shape certification frameworks that facilitate faster market entry for new aircraft designs. Additionally,lly many participants adopt a phased commercialization approach starting with smaller regional aircraft before scaling up to larger platforms. This method allows them to validate technologies in real-world operations while building customer confidence and supply chain resilience. Licensing agreements and technology sharing further enable companies to leverage complementary strengths and expand their geographic reach without excessive capital expenditure on new facilities or production lines independently.

GLOBAL HYBRID AIRCRAFT MARKET NEWS

In January 2025, Vertical Aerospace secured 90 million USD in fresh equity funding to accelerate certification flights for its VX4 model and strengthen the Hybrid aircraft market presence.

In December 2024, Airbus, Daher, and Safran completed the EcoPulse flight campaign, logging 100 flight hours to validate distributed propulsion technologies and strengthen the Hybrid aircraft market presence.

MARKET SEGMENTATION

This research report on the global hybrid aircraft market is segmented and sub-segmented into the following categories.

By Aircraft Type

- Regional Transport Aircraft

- Advanced Air Mobility (AAM)

By Lift Technology

- Conventional Takeoff and Landing (CTOL)

- Vertical Takeoff and Landing (VTOL)

By Propulsion Architecture

- Parallel Hybrid

- Series Hybrid

By Country

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com