- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

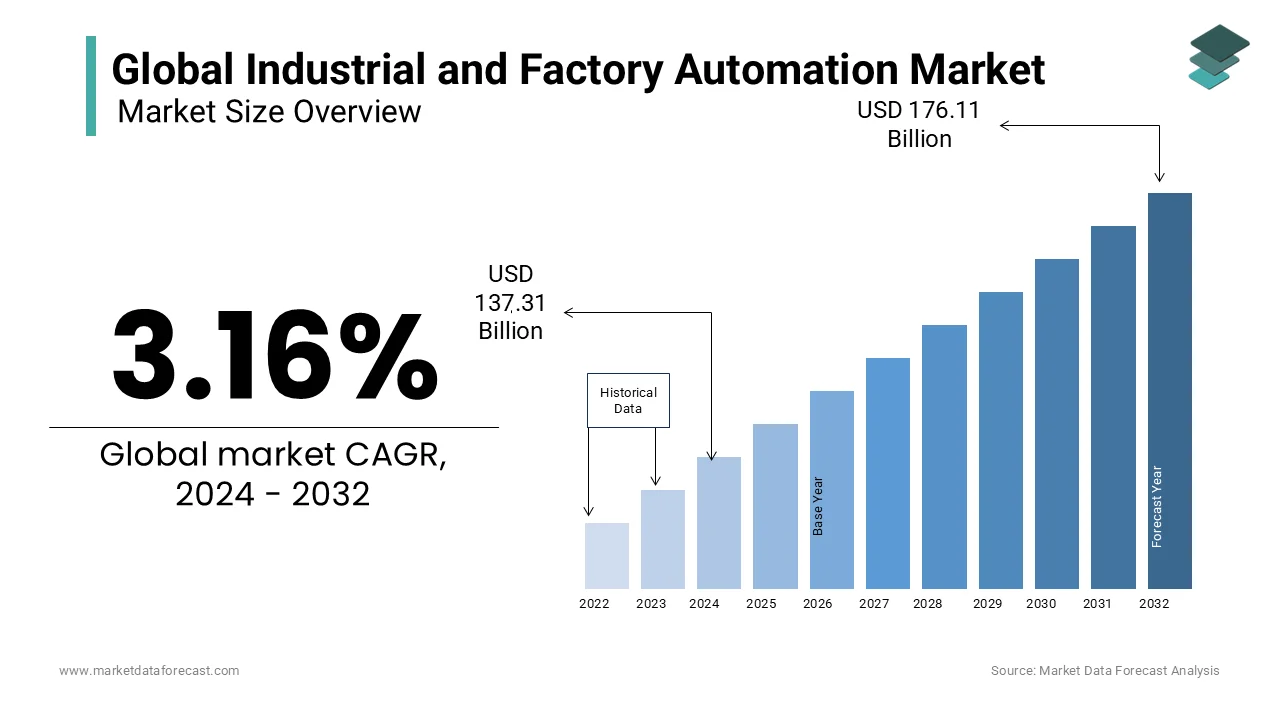

Market Size, 2025

$147.65 BnMarket Estimate, 2026

$152.32 BnMarket Forecast, 2034

$195.36 BnCAGR, 2026–2034

3.16%Global Industrial and Factory Automation Market Size

The global industrial and factory automation market was worth USD 147.65 billion in 2025 and is anticipated to reach USD 152.32 billion in 2026, and from USD 195.36 billion by 2034, growing at a CAGR of 3.16 % during the forecast period from 2026 to 2034.

Industrial And Factory Automation Market Overview

Industrial and factory automation involves using control systems, computers, and robots to operate machinery and processes automatically, reducing or eliminating the need for human intervention. This ecosystem integrates hardware such as sensors, actuators, and programmable logic controllers with software platforms for real time data analysis and decision making. The primary objective is to enhance operational efficiency, product quality, and workplace safety while reducing production costs. According to the International Federation of Robotics (IFR), the global stock of operational industrial robots reached 3.9 million units in 2022 (the 3.5 million milestone was reached in 2021). This proliferation is driven by the need for precision and consistency in high volume production lines. As per the United Nations Industrial Development Organization (UNIDO), the Asia and Oceania region (which includes major developing economies) recorded an MVA growth rate of 4.0%, while developing and emerging industrial economies (excluding China) saw a recovery of 5.9% in 2021 following a decline in 2020. UNIDO attributes this growth to broader industrial recovery and structural performance rather than exclusively to automation.The integration of cyber physical systems enables predictive maintenance, which the World Economic Forum estimates can reduce machine downtime notably. Furthermore, the rise of smart factories leverages Internet of Things connectivity to optimize energy consumption, addressing sustainability goals mandated by global regulatory bodies. The transition from traditional mechanization to intelligent automation marks a pivotal evolution in industrial history, enabling manufacturers to respond dynamically to market demands and supply chain disruptions. This technological paradigm shift is not merely about replacing labor but augmenting human capabilities through collaborative robotics and data driven insights, fundamentally reshaping the competitive landscape of global manufacturing.

MARKET DRIVERS

Acute Global Labor Shortages and Rising Wage Costs

The persistent global labor shortage and escalating wage costs fuel the growth of the industrial and factory automation market. Developed nations are experiencing demographic shifts characterized by aging populations and shrinking workforces, compelling manufacturers to seek alternative labor sources. According to the United Nations Department of Economic and Social Affairs, the proportion of the population aged 65 years or older is projected to double from 10 percent in 2022 to 20 percent by 2050, significantly reducing the available pool of manual laborers. In Germany, economic research institutes and employment tracking agencies report an acute shortage of skilled workers, with over 225,000 vocationally trained and technical vacancies remaining unfilled, forcing companies to automate routine tasks to maintain production levels. Similarly, in the United States, the Bureau of Labor Statistics indicates that manufacturing hourly compensation has increased by over 15% over a five-year period, compressing profit margins for labor-intensive operations. Automation offers a viable solution by providing consistent output without the constraints of shift limitations, breaks, or turnover rates. Research cited across international labor groups notes that industrial robot densification acts as a key driver of labor productivity and national competitiveness, offsetting initial capital investments through optimized task allocation. Furthermore, the risk of workplace injuries associated with repetitive strain jobs is mitigated through automation, reducing liability and insurance costs. The economic imperative to replace human labor with automated systems is becoming increasingly urgent as global labor markets tighten. Consequently, this shift drives sustained demand for robotics, automated guided vehicles, and smart control systems across diverse industrial verticals.

Demand for Operational Efficiency and Mass Customization

The growing demand for operational efficiency and the ability to deliver mass customized products is a significant driver propelling the Industrial and Factory Automation Market. Modern consumers increasingly expect personalized products with short lead times, a requirement that traditional rigid manufacturing lines cannot meet efficiently. Automation enables flexible manufacturing systems that can rapidly switch between product variants without extensive retooling. According to McKinsey and Company, companies that implement advanced automation and digital technologies can reduce production costs by up to 30 percent while improving throughput by 20 percent. In the automotive sector, the Society of Motor Manufacturers and Traders highlights that leading manufacturers now offer hundreds of customization options for vehicle models, made possible only through highly automated and interconnected assembly lines. These systems utilize real time data to adjust parameters instantly, ensuring precision and consistency across diverse product specifications. The World Economic Forum states that smart factories leveraging automation can achieve a 50 percent reduction in changeover times, allowing for smaller batch sizes and greater responsiveness to market trends. Additionally, automation minimizes material waste through precise control of processes, contributing to cost savings and sustainability goals. The European Commission reports that resource efficiency improvements driven by automation can save manufacturers up to 20 percent in raw material costs. Competition is intensifying and customer preferences are fragmenting. To stay competitive, companies must scale the production of high-quality customized goods by widely adopting flexible automation technologies.

MARKET RESTRAINTS

High Initial Capital Investment and Implementation Costs

The high cost of implementing these systems is a significant restraint to the industrial and factory automation market. This is especially true for small and medium-sized enterprises (SMEs) requiring substantial initial capital. Deploying comprehensive automation solutions involves not only the purchase of expensive hardware such as robots and sensors but also the integration of complex software platforms and infrastructure upgrades. ccording to industrial assembly integrators and the Association for Advancing Automation (A3), capital expenditures vary dramatically by scope, with entry-level robotic integrations scaling upward into millions of dollars for fully bespoke, high-volume production architectures. This financial barrier limits accessibility for smaller manufacturers who operate on tighter margins and lack access to affordable financing options. Data monitored by the World Bank Group indicates that real commercial lending rates regularly exceed 10% in developing markets, compounding financial strain on local small-to-medium enterprises trying to transition away from labor-intensive operations. Furthermore, the expense of manufacturing engineering goes beyond capital machinery; custom software licensing, system optimization, and labor retraining typically inflate initial equipment bills by 20% to 35%. The Asian Development Bank shows that many small businesses in Southeast Asia hesitate to automate due to uncertainty regarding long term profitability and technological obsolescence. Without clear financial incentives or government subsidies, the high entry cost remains a formidable obstacle. Additionally, the rapid pace of technological advancement means that invested systems may become outdated within a few years, posing a risk of stranded assets. High capital requirements will continue to restrict widespread automation adoption among smaller industrial players. This will remain true until financing models become more flexible and costs decrease.

Complexity of Integration with Legacy Systems

The complexity of integrating modern automation technologies with existing legacy systems is a major impediment to the expansion of the Industrial and Factory Automation Market. Many manufacturing facilities operate with machinery and control systems that were installed decades ago, lacking the connectivity and compatibility required for seamless integration with contemporary digital platforms. Global operational technology data highlights that a massive baseline of operating brownfield facilities, estimated near 70%, still run on legacy infrastructure entirely isolated from modern Internet Protocol (IP) networks. Retrofitting these legacy systems with sensors and communication modules often requires custom engineering solutions, which are time consuming and costly. Studies suggest that cross-network interoperability issues remain a major point of friction, with McKinsey Global Institute data noting that while automation potential is high (up to 60%), integration friction consistently blocks swift, on-time project execution. The technical friction between older proprietary fieldbus communication systems and next-generation cloud analytics is heavily documented in the International Society of Automation (ISA) InTech Journals. This lack of standardization forces manufacturers to rely on specialized vendors for integration services, increasing dependency and costs. Furthermore, the risk of system failures during integration can halt production, causing significant financial losses. Reports compiled by the European Factories of the Future Research Association (EFFRA) repeatedly warn that a deficit in internal cross-disciplinary engineering skills (the intersection of traditional operational technology and cloud IT) severely impairs legacy system modernization across European industrial sectors. Integration complexity will remain a major hurdle for automation adoption. This will continue until standardized interfaces and plug-and-play solutions become widely available.

MARKET OPPORTUNITIES

Adoption of Artificial Intelligence and Predictive Maintenance

The integration of artificial intelligence (AI) and predictive maintenance technologies offers a substantial opportunity for the Industrial and Factory Automation Market. This helps to enhance reliability and reduce operational costs. AI algorithms can analyze vast amounts of data generated by sensors and machines to identify patterns indicative of potential failures before they occur. According to updated tech sector tracking from International Data Corporation (IDC), discrete manufacturing and process manufacturing consistently rank among the top vertical industries investing heavily in AI platforms to streamline supply chains and operations. Predictive maintenance can reduce machine downtime by up to 50 percent and extend equipment life by 20 percent, as per sources. In the aerospace industry, Boeing reports that using AI driven analytics for maintenance scheduling has saved millions of dollars in unplanned repair costs and improved flight safety. Furthermore, AI enables optimization of production parameters in real time, enhancing energy efficiency and product quality. The World Economic Forum highlights that smart factories utilizing AI can reduce energy consumption by 15 percent through optimized machine operation. Additionally, the ability to predict supply chain disruptions and adjust production schedules accordingly enhances resilience against external shocks. As computing power increases and AI models become more accessible, manufacturers of all sizes can leverage these technologies to gain competitive advantages. The shift from reactive to predictive maintenance transforms asset management, creating new revenue streams for automation providers through software as a service models and continuous monitoring services.

Expansion of Collaborative Robotics in SMEs

The proliferation of collaborative robots, or cobots, in small and medium sized enterprises (SMEs) unlocks potential for the Industrial and Factory Automation Market. Unlike traditional industrial robots that require safety cages and specialized programming, cobots are designed to work safely alongside human workers and are easy to deploy and reprogram. The International Federation of Robotics (IFR) reveals that industrial robot installations have sustained historically high volumes, with low-footprint, user-friendly collaborative robots steadily penetrating small and mid-sized enterprises due to simplified programming requirements. These robots are ideal for tasks such as assembly, packaging, and quality inspection, which are labor intensive and prone to errors. In Japan, the Ministry of Economy Trade and Industry promotes the adoption of cobots to address labor shortages in small manufacturing firms, providing subsidies for initial purchases. The ease of use allows workers with minimal technical training to program cobots using intuitive interfaces, reducing deployment time from weeks to hours. The Boston Consulting Group (BCG) stresses that cobots offer rapid adaptability for variable-run assembly, yielding substantial double-digit efficiency gains without requiring the rigid floor footprints of traditional safety-caged machinery. Furthermore, the lower cost of cobots compared to traditional robots makes them accessible to businesses with limited capital budgets. As awareness of their benefits grows and technology advances, cobots are becoming a staple in diverse industries including electronics, food and beverage, and pharmaceuticals. This democratization of automation empowers SMEs to compete with larger corporations, driving broader market penetration and innovation.

MARKET CHALLENGES

Cybersecurity Vulnerabilities in Connected Industrial Systems

The increasing connectivity of industrial systems exposes manufacturers to significant cybersecurity vulnerabilities, posing a major challenge to the Industrial and Factory Automation Market. As factories become more integrated with the Internet of Things and cloud platforms, the attack surface for cyber threats expands, risking operational disruption and data theft. According to the IBM X-Force Threat Intelligence Index, the manufacturing industry remains the most targeted sector for global cyberattacks, driven heavily by attackers exploiting web-facing applications and deploying ransomware against operational downtime vulnerabilities. Ransomware attacks can halt production lines for days, causing millions of dollars in losses and damaging brand reputation. The Colonial Pipeline incident demonstrated how cyber vulnerabilities in critical infrastructure can have widespread economic impacts. Cybersecurity agencies note that connected automotive smart factories are high-stakes targets for advanced persistent threat (APT) groups seeking industrial espionage and proprietary mechanical blueprints. Furthermore, the lack of standardized security protocols across different vendors complicates the implementation of robust defense mechanisms. The National Institute of Standards and Technology emphasizes that many legacy industrial devices lack basic security features, making them easy entry points for attackers. Protecting these systems requires continuous monitoring, regular software updates, and employee training, which add to operational costs. As reliance on digital technologies grows, ensuring cybersecurity becomes a critical challenge that manufacturers must address to maintain trust and operational continuity. Failure to do so can result in catastrophic failures and regulatory penalties.

Shortage of Skilled Workforce for Advanced Technologies

The acute shortage of skilled workforce capable of operating and maintaining advanced automation technologies is a formidable hurdle for the Industrial and Factory Automation Market. While automation reduces the need for manual labor, it increases the demand for technicians, engineers, and data analysts with specialized skills in robotics, programming, and systems integration. According to the ManpowerGroup Talent Shortage Survey, 75 percent of employers globally report difficulty finding skilled talent, particularly in technology and engineering roles. In the United States, the National Association of Manufacturers estimates that 2.1 million manufacturing jobs could remain unfilled by 2030 due to the skills gap. This shortage hinders the effective deployment and utilization of automation systems, leading to suboptimal performance and increased downtime. In Europe, the European Centre for the Development of Vocational Training notes that vocational education systems are struggling to keep pace with the rapid evolution of industrial technologies, leaving many workers ill prepared for modern factory environments. Furthermore, the complexity of integrated systems requires cross functional expertise that is rare in the current labor market. Companies must invest heavily in training and upskilling programs, which are time consuming and costly. The World Economic Forum highlights that reskilling initiatives often fail to meet immediate operational needs, creating a bottleneck in automation adoption. Without a sufficient pipeline of qualified professionals, manufacturers face challenges in maximizing the benefits of automation, limiting market growth and innovation potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 3.16 % |

| Segments Covered | By Solution, By Component, By Industry, and by reason |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, the Middle East, and Africa |

| Market Leaders Profiled | General Electric, ABB Ltd., Emerson Electric Co., Rockwell Automation Inc., Siemens AG, Endress+Hauser Group, Schneider Electric, Yokogawa, Omron Corporation, Mitsubishi, Honeywell. |

SEGMENTAL ANALYSIS

By Solution Insights

Programmable Logic Controllers (PLC) (33.0%)

The Programmable Logic Controllers (PLC) segment dominated the Industrial and Factory Automation Market and accounted for a 33.7% share in 2025. This dominance of the segment was driven by its foundational role in discrete manufacturing and machinery control. PLCs are the backbone of automated production lines, offering robustness, reliability, and flexibility for controlling complex sequences of operations. Major suppliers confirms that while native robot controllers manage real-time axes movement, a vast majority of robotic cells interface with upstream PLCs to coordinate cell-level safety, external sensors, and factory-wide I/O logic. The versatility of PLCs allows them to be used in diverse applications ranging from automotive assembly lines to packaging machines. The German Machine Tool Builders' Association (VDW) highlight that the automotive and precision electromobility shift continues to fuel multi-billion euro investment cycles for automated hardware, anchoring PLCs as the dominant control hardware segment. Furthermore, the ease of programming and modification makes PLCs ideal for manufacturers who frequently update production processes. Historically, transitioning from complex hard-wired mechanical relays to modern micro-processor based PLCs drastically cut down on point-to-point wiring faults, providing integrated logic diagnostics that minimize baseline equipment troubleshooting from hours to minutes. Their ability to interface with various sensors, actuators, and human machine interfaces ensures seamless integration into existing factory infrastructures. As industries continue to prioritize operational efficiency and flexibility, the demand for PLCs remains steadfast. The widespread availability of skilled technicians familiar with PLC programming further supports their dominance. Additionally, the transition towards soft PLCs running on industrial PCs is expanding their applicability in data intensive environments, ensuring their continued leadership in the automation solutions landscape.

Furthermore, the dominance of Programmable Logic Controllers is further reinforced by extensive standardization and interoperability across various industrial sectors. International standards such as IEC 61131 3 define programming languages and communication protocols for PLCs, ensuring compatibility between devices from different manufacturers. The standardization facilitates easier maintenance and replacement of components, reducing lifecycle costs for end users. Furthermore, the development of open communication protocols such as OPC UA enables PLCs to communicate seamlessly with higher level systems like Supervisory Control and Data Acquisition and Manufacturing Execution Systems. The interoperability allows manufacturers to create heterogeneous automation systems that leverage the best components from various vendors. The ability of PLCs to integrate with legacy equipment while supporting modern digital technologies ensures their relevance in both brownfield and greenfield projects. Global supply chains are becoming increasingly interconnected. Consequently, this need for standardized and interoperable control solutions drives the sustained leadership of PLCs in the industrial automation market.

Manufacturing Execution Systems (MES)

The Manufacturing Execution Systems (MES) segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 12.5% from 2026 to 2034 due to its critical role in integrating physical production with digital information in Industry 4.0 environments. MES bridges the gap between enterprise resource planning and process control, providing real time visibility into production operations. Digital twins, which are virtual replicas of physical assets, rely on data from MES to simulate and optimize production processes. According to regional manufacturing research published by Zebra Technologies and Oxford Economics, the integration of digital tracking, advanced automation, and analytical models has generated a 20% average boost in operations productivity across Asian manufacturing hubs. Aviation manufacturing use-cases show that Boeing achieved a 25% reduction in wiring assembly times, while Lockheed Martin logged a 30% reduction in F-35 assembly times specifically by deploying augmented reality blueprints, as per the Whale Process Optimization Frameworks / IJICC Digital Evolution Analysis. Furthermore, MES facilitates predictive maintenance by analyzing machine data to identify potential failures before they occur. Research indicates that implementing an integrated predictive maintenance framework allows smart factories to lower maintenance costs by 25% to 30% and slash unplanned equipment downtime by up to 35% to 50%. As manufacturers strive for greater agility and transparency, the demand for MES solutions that offer advanced analytics and visualization capabilities is surging. The ability of MES to provide actionable insights for decision making transforms traditional manufacturing into smart, data driven operations, driving its rapid growth.

In addition, stringent regulatory compliance and traceability requirements are significantly propelling the growth of the Manufacturing Execution Systems segment. Industries such as pharmaceuticals, medical devices, and food and beverage are subject to rigorous regulations that mandate detailed recording of production processes and quality control measures. MES systems automate data collection, reducing the risk of human error and ensuring accuracy in regulatory reporting. Furthermore, consumers are increasingly demanding transparency regarding the origin and production methods of goods, prompting manufacturers to adopt MES for end to end traceability. The ability of MES to provide comprehensive documentation and real-time monitoring is becoming indispensable as regulatory frameworks become increasingly complex and global. Consequently, this critical function is driving its accelerated adoption across regulated industries.

By Component Insights

Industrial Robots

The Industrial Robots led the Industrial and Factory Automation Market and captured a 38.3% share in 2025. This leading position of the segment was attributed to its extensive use in automotive and electronics manufacturing. These industries require high precision, speed, and consistency, which robotic systems deliver effectively. The electronics sector is another major contributor, with smartphone and computer production relies heavily on robotic arms for assembly, testing, and packaging. The precision required for handling small components makes industrial robots indispensable in this sector. Furthermore, the shift towards electric vehicles is driving new investments in automated battery production lines. The ability of industrial robots to operate continuously without fatigue ensures high throughput and consistent quality, which are critical for maintaining competitiveness in these fast paced industries. The reliance on industrial robots continues to solidify their market leadership in manufacturing. This is largely driven by increasing production volumes and rapidly shortening product life cycles.

Moreover, the dominance of the Industrial Robots segment is further strengthened by technological advancements in collaborative and mobile robotics, which expand their applicability beyond traditional caged environments. Collaborative robots, or cobots, are designed to work safely alongside humans, enabling flexible automation in small and medium sized enterprises. Autonomous Mobile Robots (AMRs) are also gaining traction in warehousing and logistics, where they optimize material handling and inventory management. These robots utilize advanced sensors and artificial intelligence to navigate dynamic environments, offering greater flexibility than traditional Automated Guided Vehicles. Furthermore, the integration of vision systems and force sensors allows industrial robots to perform delicate tasks such as picking irregular objects, expanding their use in food processing and agriculture. The versatility and safety features of modern robotic systems are breaking down barriers to adoption, making them accessible to a wider range of industries and applications, thereby reinforcing their leading position in the automation component market.

Fastest Growing Segment: Machine Vision

But the Machine Vision segment is expected to exhibit a noteworthy CAGR of 9.1% during the forecast period owing to the increasing need for precise quality control and defect detection in high speed production environments. Machine vision systems use cameras and image processing algorithms to inspect products for defects, measure dimensions, and verify assembly correctness. The complexity and miniaturization of electronic components make manual inspection impossible, necessitating automated vision systems. Furthermore, in the automotive sector, machine vision is used to check weld quality, paint finish, and part alignment. The ability of machine vision systems to operate at high speeds without compromising accuracy ensures that production lines maintain throughput while meeting stringent quality standards. Consumer expectations for product quality are rising and regulatory requirements are tightening. Consequently, the adoption of machine vision for real-time quality assurance is accelerating, which drives its rapid growth in the automation market.

In addition, the integration of artificial intelligence and deep learning technologies is significantly accelerating the growth of the Machine Vision segment. Traditional rule based vision systems struggle with variable lighting, complex backgrounds, and unpredictable defects, but AI powered systems can learn from data to identify anomalies with high accuracy. Deep learning algorithms enable these systems to improve over time, adapting to new product types and defect patterns without extensive reprogramming. Furthermore, in pharmaceuticals, AI vision is used to verify label accuracy and detect counterfeit products, enhancing supply chain security. The flexibility and intelligence of AI driven machine vision systems make them suitable for diverse applications, from reading optical character recognition on packages to detecting microscopic cracks in metal parts. The capabilities of machine vision systems are expanding as computing power increases and algorithms grow more sophisticated. Consequently, this drives the segment's fastest growth rate and creates new opportunities for automation.

By Industry Insights

Discrete Manufacturing

The discrete manufacturing segment held the majority share of 56.8% of the Industrial and Factory Automation Market in 2025. This supremacy of the segment was supported by the high volume production and increasing product complexity in sectors such as automotive and electronics. Discrete manufacturing involves the production of distinct items, such as cars, smartphones, and appliances, which require precise assembly of multiple components. According to the International Federation of Robotics, the automotive industry is the largest user of industrial robots, accounting for 35 percent of global installations, due to the need for welding, painting, and assembly automation. Similarly, the electronics sector relies on automation for the rapid assembly of printed circuit boards and tiny components. The complexity of these products demands advanced automation solutions such as computer numerical control machines, robotic arms, and automated guided vehicles to manage intricate assembly processes. Furthermore, the short product life cycles in electronics drive the need for flexible automation systems that can be quickly reconfigured for new models. The ability of discrete manufacturing automation to handle high mix and high volume production efficiently ensures its dominance. As consumer demand for customized and technologically advanced products grows, the reliance on sophisticated automation in discrete manufacturing continues to strengthen its market leadership.

Furthermore, the top position of this segment is further reinforced by the widespread adoption of flexible manufacturing systems (FMS) that allow for rapid changes in production lines. FMS enables manufacturers to produce a variety of products on the same line with minimal downtime, addressing the growing demand for customization. In the appliance industry, a study notes that manufacturers are using modular automation cells to produce different models of refrigerators and washing machines on shared lines. This flexibility reduces inventory costs and allows for faster response to market trends. Furthermore, the integration of digital twins and simulation software enables manufacturers to test and optimize production scenarios before physical implementation, reducing risks and costs. The ability to switch between products quickly and efficiently is crucial in competitive markets where consumer preferences change rapidly. As mass customization becomes the norm, the need for agile and adaptable automation systems in discrete manufacturing drives its continued leadership. The combination of high volume capability and flexible configuration ensures that discrete manufacturing remains the largest application area for industrial automation.

Fastest Growing Segment: Process Industry

But the process industry segment is predicted to witness the highest CAGR of 11.5% over the forecast period. This quick surge of the segment is propelled by digital transformation initiatives in oil and gas, chemical, and pharmaceutical sectors. Process industries involve the continuous production of goods through chemical, biological, or physical transformations, requiring precise control of parameters such as temperature, pressure, and flow. Sources indicate that global IT spending in the oil and gas market exceeds $33 billion, showing strong adoption of cloud architectures and advanced process control systems to optimize exploration and refining operations. Distributed Control Systems and Supervisory Control and Data Acquisition systems are being upgraded with Internet of Things sensors and artificial intelligence to enable real time monitoring and predictive maintenance. In the chemical industry, research highlights that automation is critical for managing hazardous materials and ensuring safety compliance. Advanced process control systems use machine learning to optimize reaction conditions, maximizing yield and minimizing waste. Furthermore, the push for sustainability is driving the adoption of automation to monitor emissions and energy consumption. As process industries seek to enhance safety, efficiency, and sustainability, the demand for advanced automation solutions is accelerating, driving the segment’s rapid growth.

Moreover, the expansion of pharmaceutical and biotechnology production is another key factor propelling the growth of the Process Industry segment. The global demand for vaccines, biologics, and personalized medicines is surging, requiring highly controlled and automated manufacturing environments. Biopharmaceutical production involves complex fermentation and purification processes that require precise automation to ensure product consistency and safety. Furthermore, regulatory agencies such as the Food and Drug Administration mandate strict process validation and data integrity, which are facilitated by automated Manufacturing Execution Systems. The adoption of continuous manufacturing, an automated approach that produces drugs in a steady stream rather than batches, is gaining traction. As the pharmaceutical industry shifts towards more complex and personalized therapies, the need for sophisticated automation to manage these intricate processes drives the fast growth of the process industry segment in the automation market.

REGIONAL ANALYSIS

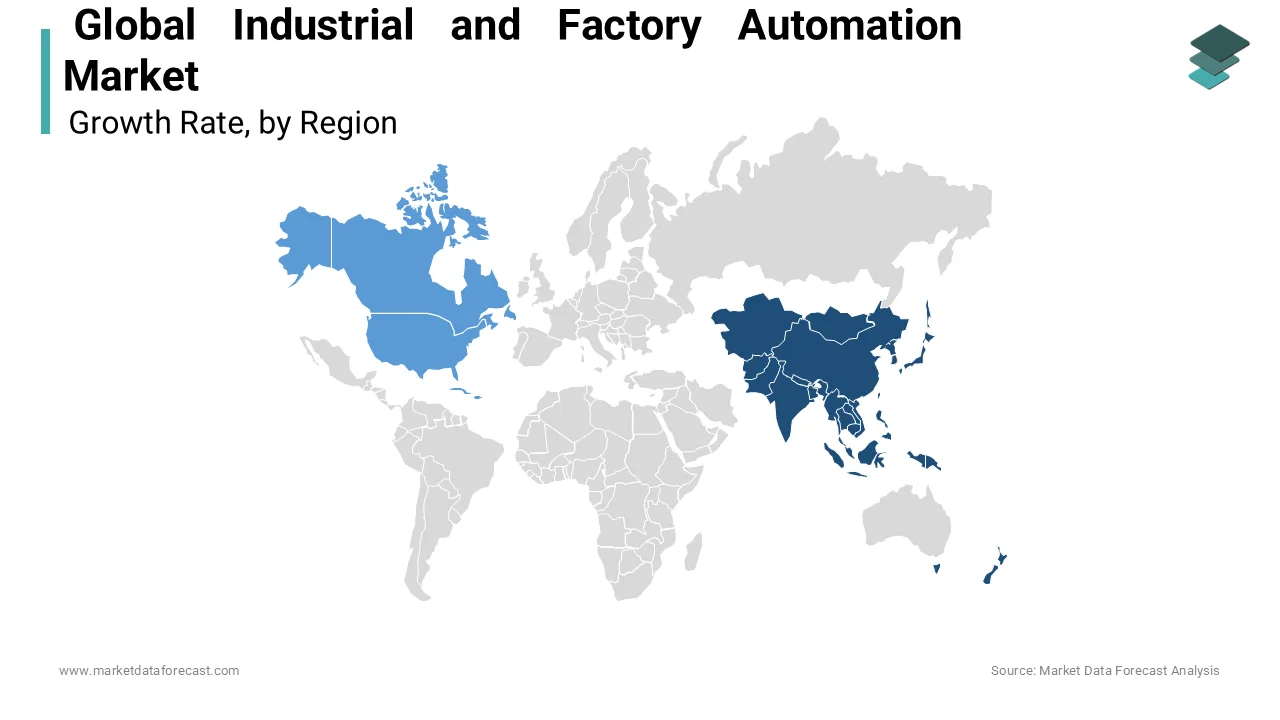

North America Market Analysis

North America plays a key role in the global Industrial and Factory Automation Market because of advanced technological infrastructure and strong investment in research and development. The United States is a leader in adopting Industry 4.0 technologies, driven by the need to reshore manufacturing and enhance competitiveness. According to the National Association of Manufacturers, the US manufacturing sector contributes 2.3 trillion dollars to the economy, with automation playing a key role in productivity growth. The presence of major automation vendors and technology companies in the region fosters innovation and early adoption of smart factory solutions. Furthermore, the labor shortage in the US is accelerating the adoption of robotics and collaborative systems to maintain production levels. Canada is also emerging as a hub for automation in the natural resources sector, with mining and oil and gas companies investing in autonomous equipment. Government initiatives such as the Superclusters Program in Canada support the development of advanced manufacturing technologies. As North America continues to lead in digital innovation and address labor challenges, the demand for industrial automation solutions remains robust, sustaining its prominent market position.

Europe Market Analysis

Europe followed closely behind in the global Industrial and Factory Automation Market and captured a 31.7% share in 2025. This position of the European market was supported by strong manufacturing bases in Germany, Italy, and France. The region is a pioneer in Industry 4.0, with Germany’s Plattform Industrie 4.0 initiative setting global standards for smart manufacturing. According to Eurostat, the manufacturing sector in the European Union accounts for 15 percent of GDP, with high levels of automation in automotive and machinery industries. The European Commission’s Green Deal is driving the adoption of energy efficient automation technologies to reduce carbon emissions. A study reports that European industries are investing heavily in smart meters and energy management systems to comply with sustainability targets. Furthermore, the region’s focus on high quality precision engineering sustains demand for advanced robotics and control systems. Labor shortages and aging populations in countries like Italy and Spain are also prompting increased automation uptake. Strict safety and environmental regulations further drive the adoption of automated systems that ensure compliance and reduce risks. As Europe continues to innovate in sustainable and smart manufacturing, it remains a key driver of technological advancement in the global automation market.

Asia Pacific Market Analysis

Asia Pacific holds the largest and fastest-growing share of the global Industrial and Factory Automation Market. This growth is fueled by rapid industrialization and massive manufacturing output in China, Japan, and South Korea. China is the world’s largest market for industrial robots, driven by its status as the global factory. According to the International Federation of Robotics, China accounted for 52 percent of global robot installations in 2022, supported by government policies such as Made in China 2025. Japan is a leader in robotics technology, with companies like Fanuc and Yaskawa dominating the global supply chain. The Japanese Ministry of Economy Trade and Industry promotes automation to address severe labor shortages caused by an aging population. South Korea has the highest robot density in the world, particularly in the electronics and automotive sectors. Emerging economies like India and Vietnam are also increasing automation investments to boost manufacturing competitiveness. The Indian Ministry of Commerce and Industry notes that production linked incentive schemes are encouraging automation in electronics and pharmaceuticals. As Asia Pacific continues to expand its manufacturing base and adopt advanced technologies, it remains the central engine of growth for the global industrial automation market.

Latin America Market Analysis

Latin America is moving ahead steadfastly in the global Industrial and Factory Automation Market, with growth driven primarily by the automotive, mining, and food and beverage sectors. Brazil and Mexico are the largest markets in the region, benefiting from their integration into global supply chains. Regional trade trackers from ECLAC indicate that while structural constraints affected broader regional averages, a sharp rise in strategic foreign direct investment (FDI) fueled robust localized automation pipelines across automotive and appliance manufacturing hubs in Mexico and Brazil. In Brazil, the automotive industry is a major adopter of robotics, with significant investments in modernizing assembly lines. Mexico’s proximity to the United States has led to a boom in nearshoring, with many manufacturers establishing automated facilities to serve the North American market. The Mexican Ministry of Economy indicates that automotive exports reached record highs, driving demand for automation equipment. The mining sector in Chile and Peru is also adopting autonomous vehicles and drilling systems to improve safety and efficiency. However, economic volatility and infrastructure challenges can hinder widespread adoption. Despite these hurdles, ongoing investments in key industries and the need for productivity improvements are creating opportunities for automation suppliers. As Latin America continues to industrialize and integrate with global markets, the demand for industrial automation solutions is expected to grow steadily.

Middle East and Africa Market Analysis

The Middle East and Africa region is likely to expand significantly in the global Industrial and Factory Automation Market from 2026 and 2034 owing to the oil and gas, petrochemical, and mining sectors. Countries in the Gulf Cooperation Council are investing heavily in automation to diversify their economies and enhance efficiency in energy production. According to the Organization of the Petroleum Exporting Countries, the Middle East accounts for over 30 percent of global oil production, sustaining demand for advanced process control systems. Saudi Arabia’s Vision 2030 initiative includes plans to develop new industrial cities and upgrade existing facilities with smart technologies. In the United Arab Emirates, the Dubai Industrial Strategy aims to boost the contribution of the industrial sector to the economy, promoting automation in food processing and logistics. Africa’s mining sector in countries like South Africa and Nigeria is also adopting automation to improve safety and productivity. However, limited infrastructure and skilled labor shortages pose challenges to broader adoption. Despite these constraints, strategic investments in energy and mining, coupled with economic diversification efforts, are creating gradual growth opportunities for the industrial automation market in the region.

COMPETITIVE LANDSCAPE

The competition in the global Industrial and Factory Automation Market is characterized by the presence of established multinational corporations and specialized regional players, creating a moderately consolidated landscape. Leading companies compete on the basis of technological innovation, product reliability, and comprehensive service offerings. The market sees intense rivalry in terms of developing integrated digital platforms that combine hardware and software for seamless Industry 4.0 implementation. Price competition remains significant in standard component segments, particularly from manufacturers in Asia Pacific who offer cost effective alternatives. However, differentiation through specialized industry expertise and custom engineering services is becoming increasingly important for premium positioning. Strategic mergers and acquisitions are common as firms seek to expand their software capabilities and geographic reach. Regulatory compliance and cybersecurity standards also influence competitive dynamics, favoring companies with robust quality assurance systems. The entry of technology giants into the industrial space further intensifies competition. Overall, the market is evolving towards greater ecosystem collaboration and digital sophistication as demand for efficient and connected manufacturing solutions grows across diverse industries worldwide.

KEY MARKET PLAYERS

Major Key Players in the Global Industrial & Factory Automation Market are

- General Electric

- ABB Ltd,

- Emerson Electric, Inc

- Rockwell Automation Inc

- Siemens AG

- Endress+Hauser Group

- Schneider Electric

- Yokogawa

- Omron Corporation

- Mitsubish

- Honeywell.

Top Players In The Market

- Siemens AG is a global leader in industrial automation, providing comprehensive digitalization solutions for manufacturing and process industries. The company offers a wide portfolio including programmable logic controllers, human machine interfaces, and industrial software platforms. Siemens actively drives the adoption of Industry 4.0 through its Digital Enterprise suite, which integrates physical and digital worlds. Recent actions include expanding its Xcelerator open digital business platform to facilitate easier integration of hardware and software components. The company invests heavily in artificial intelligence and edge computing technologies to enhance predictive maintenance capabilities. By fostering ecosystems with partners and customers, Siemens strengthens its position as a key enabler of smart factories. Its focus on sustainability and energy efficiency further aligns with global regulatory trends, ensuring long term relevance and leadership in the evolving automation landscape.

- Rockwell Automation Inc. is a prominent player specializing in industrial automation and information solutions, particularly strong in North America. The company provides integrated control systems, sensors, and software that help manufacturers improve productivity and sustainability. Rockwell focuses on connecting people, processes, and technology through its FactoryTalk innovation suite. Recent initiatives involve strategic partnerships with cloud providers like Microsoft and Amazon to enhance industrial Internet of Things capabilities. The company has also acquired niche software firms to bolster its cybersecurity and supply chain management offerings. By emphasizing connected enterprise solutions, Rockwell enables real time data visibility and decision making for clients. Its commitment to worker safety and operational excellence drives continuous innovation in collaborative robotics and smart sensing technologies, reinforcing its competitive stance in the global market.

- Schneider Electric SE is a major contributor to the global industrial automation market, focusing on energy management and automation digital solutions. The company serves diverse sectors including infrastructure, data centers, and manufacturing with its EcoStruxure architecture. Schneider Electric emphasizes sustainability by integrating energy efficiency into automation systems. Recent actions include the expansion of its software portfolio through acquisitions of companies specializing in industrial software and cyber security. The company actively promotes open interoperability standards to ensure seamless integration of third party devices. By leveraging artificial intelligence and advanced analytics, Schneider Electric helps customers optimize energy usage and reduce carbon footprints. Its strong presence in emerging markets and commitment to digital transformation enable it to capture growth opportunities in smart manufacturing and sustainable industrial operations globally.

Top Strategies Used By Key Market Participants

Key players in the Industrial and Factory Automation Market primarily employ strategies focused on digital integration and strategic acquisitions to strengthen their competitive position. Companies are increasingly investing in software development to create unified platforms that connect operational technology with information technology. Collaborations with cloud computing providers enable the deployment of scalable Internet of Things solutions for real time data analytics. Expansion into emerging markets through local manufacturing and partnerships is another critical strategy to capture growth opportunities. Additionally, market participants focus on sustainability by developing energy efficient automation systems that comply with environmental regulations. These approaches help companies differentiate their offerings and address evolving customer needs for flexibility and transparency. Key players are aligning with Industry 4.0 trends to enhance their relevance. Consequently, they are driving the widespread adoption of smart factory technologies across various industrial sectors worldwide.

MARKET SEGMENTATION

This research report on the global Industrial and Factory Automation market has been segmented and sub-segmented based on solution, component, industry, and region.

By Solution

- SCADA (Supervisory Control and Data Acquisition)

- PLC (Programmable Logic Controller)

- DCS (Distributed Control System)

- MES (Manufacturing Execution System)

- Industrial Safety

- PAM (Plant Asset Management)

By Component

- Sensors

- Industrial Robots

- Machine Vision

- Control valves

- Industrial PC

- Control devices

By Industry

- Process Industry

- Discrete Industry

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East & Africa