Global Industrial Computed Tomography Market Size, Share, Trends, Impact & Growth Forecast Report by Offering (Equipment, Services); Application (Flaw Detection & Inspection, Failure Analysis, Assembly Analysis, Dimensioning & Tolerancing Analysis and Others); End-Use (Oil & Gas, Aerospace and Defense, Automotive, Electronics, and Others) and Regional - (2026 to 2034)

Market Size, 2025

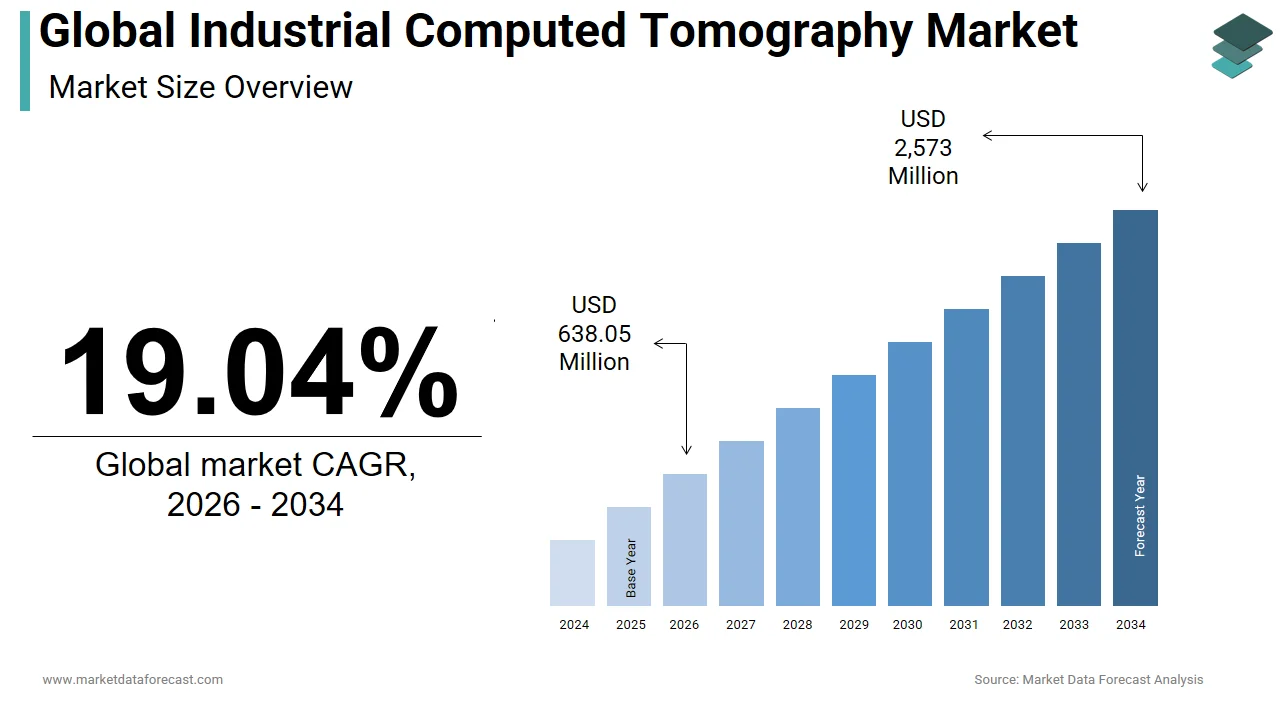

$536 MnMarket Estimate, 2026

$638.05 MnMarket Forecast, 2034

$2,573 MnCAGR, 2026–2034

19.04%Global Industrial Computed Tomography Market Size

The global industrial computed tomography (CT) market was worth USD 536 million in 2025. The global market is expected to reach USD 638.05 million in 2026 and USD 2,573 million by 2034, growing at a CAGR of 19.04% from 2026 to 2034.

Industrial computed tomography (CT) systems are used for dimensional measurement and defect inspection of manufactured parts, assemblies, and sub-assemblies on the outside and inside. The increased complexity in the design and manufacturing of components that use new processes, new materials, and precise geometries that necessitate improved quality control and assurance solutions is one element driving the demand for industrial CT systems. Due to the inability of traditional dimensional measurement methods (e.g., CMM) to achieve such requirements, CT has emerged as one of the most effective technologies.

MARKET DRIVERS

As the technology progresses from prototyping to production, the CT market is fueled by the increasing use of 3D printing techniques in many manufacturing processes. As a result, additive manufacturing of diverse items derived from 3D modeling has increased significantly. The necessity for radiographic testing techniques like CT to investigate the inside geometry of 3D-printed items has also grown.

To mitigate money and time, aircraft manufacturers are focused on CT technologies to inspect big components such as piston engines, turbines, and other apparatus in a single run. The aerospace industry has been pushed by increasing mandates for high precision and reliability requirements for analyzing complex parts under high temperatures. CT can also inspect smaller and medium-sized components, including aluminum castings, tube welds, turbine blades, and other small and medium-sized components.

MARKET RESTRAINTS

One of the most challenging aspects of industrial computed tomography is the risk of data artifacts. Some machines also generate noise interruptions, which corrupts the inspection part's information or data. This can result in erroneous results, which limits the use of computed tomography methods in the industry.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 19.04% |

| Segments Covered | By Offering, Application, End Use, and Region. |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Nikon (Japan), Omron (Japan), Rigaku (Japan), Shimadzu (Japan), Hitachi (Japan), Baker Hughes (US), YXLON (Germany), Zeiss (Germany), Werth Inc (US), North Star Imaging (US) and Others. |

SEGMENTAL ANALYSIS

By Offering Insights

In 2020, the equipment category had the biggest revenue share of more than 58%, accounting for more than 58% of global market revenue. Due to confidentiality difficulties with the product design process, corporations previously preferred to buy CT scanners, including line and cone-beam scanners, which is the crucial reason for the high share of the equipment sector in the market. However, the high equipment cost prevents some small and medium-sized businesses from investing in product acquisitions, limiting the equipment segment's growth.

From 2025 to 2029, the services segment is expected to grow quickly, with a CAGR of approximately 8.5 %. The substantial growth of the services segment in the market has been facilitated by the capital-intensive nature of industrial CT scanners. Because of the low cost, companies increasingly outsource CT services to third-party providers.

By Application Insights

In 2020, the flaw detection and inspection segment had the most significant revenue share of more than 26%. The significant share of this category is due to the growing requirement for product inspection to detect any flaws, cracks, damage, or deviation from the planned product.

Over the projection period, the assembly analysis segment is predicted to increase rapidly. Assembly analysis is becoming more popular in industries like automotive, aerospace, and electronics, where inspecting and analyzing built goods to learn about the placement and condition of smaller/minor internal components is required without disassembling or destroying the product.

By End-User Insights

In 2020, the automobile category had the highest revenue share of over 34%. The automotive industry uses industrial CT systems at many stages of the manufacturing process, including pre-production inspection, production inspection, parts sorting, and failure investigation. The scanners produce exact metrology data, allowing users to verify that the parts comply with the original CAD designs and enhance overall product quality. In addition, the dimensioning and tolerance analysis of the generated parts are performed at regular intervals during the manufacturing process.

From 2025 to 2029, the electronics segment is expected to grow quickly, with a CAGR of more than 8.5%. CT scanning is rapidly being utilized in the electronics sector as a non-destructive testing tool for inspection to analyze interior parts and assemblies, molded circuits, and verify the proper functioning of electronic components.

REGIONAL ANALYSIS

In 2024, North America dominated the industrial CT market, accounting for more than 31% of the total revenue. The regional market is projected to develop as leading industry players increase their investments in adopting new and advanced technologies. The region's thriving automotive and electronics sectors and the presence of major market players are expected to fuel market expansion in the coming years.

The Asia Pacific region remains the fastest-growing regional market. The increased acceptance of industrial CT systems for testing and inspection purposes among numerous industries, such as electronics, automotive, aerospace, and defense, might be ascribed to this growth. The region is identified as a manufacturing hub for automotive and electronics firms. The APAC area is also home to the world's most significant oil and gas production volume.

KEY MARKET PARTICIPANTS

The major companies operating in the industrial computed tomography (CT) market include Nikon (Japan), Omron (Japan), Rigaku (Japan), Shimadzu (Japan), Hitachi (Japan), Baker Hughes (US), YXLON (Germany), Zeiss (Germany), Werth Inc (US), North Star Imaging (US).

RECENT MARKET HAPPENINGS

-

In a cash transaction valued at USD 1.45 billion, General Electric Company GE announced the completion of the acquisition of Boston and Copenhagen-based BK Medical. Altaris Capital Partners was the transaction's seller.

-

Doctor Anywhere (DA), a Singapore-based telehealth firm, has partnered with Omron Healthcare, a Japanese health monitoring and therapeutic equipment manufacturer, to deliver telehealth services throughout Southeast Asia. Omron will link its health monitoring devices with DA's digital platform as part of the cooperation, allowing doctors and patients to easily share health data such as heart rates and blood pressure. Omron's blood pressure monitoring devices will be included as part of this.

-

Samsung C&T Corporation has awarded Hitachi Energy a significant contract to connect ADNOC's offshore activities to the Abu Dhabi National Energy Company PJSC's onshore power infrastructure in the United Arab Emirates (TAQA). HVDC Light® technology and the MACHTM digital control platform1 from Hitachi Energy will transfer cleaner, more efficient power from the mainland to ADNOC's offshore production operations, decreasing the company's carbon footprint by more than 30%.

MARKET SEGMENTATION

This research report on the global industrial computed tomography (CT) market has been segmented and sub-segmented based on the offering, application, end user, and region.

By Offering

- Equipment

- Services

By Application

- Flaw Detection & Inspection

- Failure Analysis

- Assembly Analysis

- Dimensioning & Tolerancing Analysis

- Others

By End-User

- Oil & Gas

- Aerospace and Defense

- Automotive

- Electronics

- Others

By Region

- North America

- Europe

- Latin America

- Middle East & Africa

- Asia Pacific

Frequently Asked Questions

What are the key trends shaping the Industrial CT market globally?

Some notable trends include the increasing demand for non-destructive testing, advancements in CT technology for improved resolution and speed, and the integration of artificial intelligence for more accurate analysis in industrial applications.

What industries are the primary consumers of Industrial CT technology?

Industries such as automotive, aerospace, electronics, and healthcare are among the major consumers of Industrial CT technology, utilizing it for quality assurance, product development, and failure analysis.

How is the Industrial CT market contributing to sustainability initiatives in manufacturing?

Industrial CT plays a crucial role in sustainability by reducing material waste through precise quality control, optimizing manufacturing processes, and enhancing overall efficiency in production.

What role does government support play in the growth of the Industrial CT market?

Government initiatives and investments in research and development, particularly in countries like Germany and the United States, are instrumental in fostering innovation and driving the adoption of Industrial CT technology.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com