Global Industrial Robotics Market Size, Share, Trends, & Growth Forecast Report, Segmented By Type (Articulated, Cartesian, SCARA, Cylindrical, Others), By End-user Industry (Automotive, Electrical & Electronics, Chemical Rubber & Plastics, Machinery, Food & Beverages, Others), & Region, Industry Forecast From 2026 to 2034

Market Size, 2025

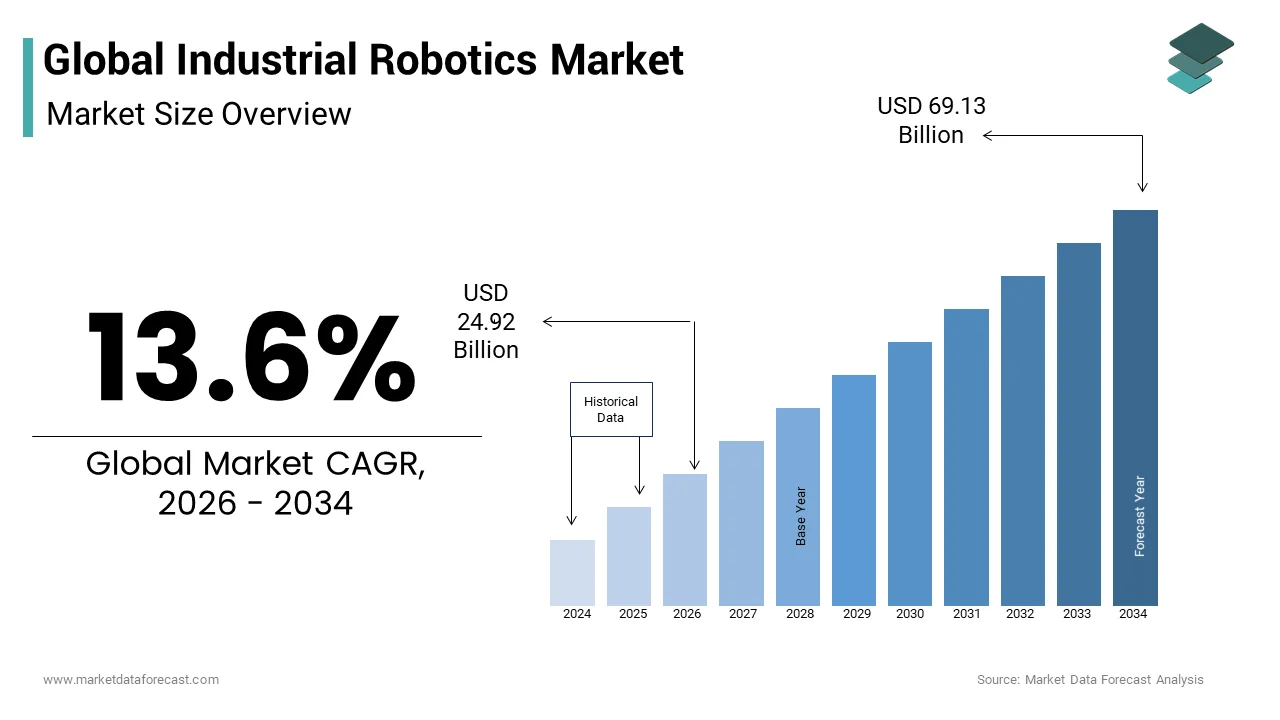

$21.94 BnMarket Estimate, 2026

$24.92 BnMarket Forecast, 2034

$69.13 BnCAGR, 2026–2034

13.6%Global Industrial Robotics Market Size

The global industrial robotics market size was valued at USD 21.94 billion in 2025 and is anticipated to reach USD 24.92 billion in 2026, and to reach USD 69.13 billion by 2034, growing at a CAGR of 13.6% during the forecast period from 2026 to 2034.

An industrial robot is a mechanical device that is programmed to execute activities connected to industrial production automatically. These robots can be reprogrammed, and the program may be altered as many times as needed, depending on the application. Industrial robots aid in improving productivity while lowering costs and generating high-quality goods in automation applications. Drive, end-effector, robotic manipulators, sensors, and controls make up the majority of industrial robots. The robotic controller is the robot's brain that assists in issuing commands. Microphones and cameras in robot sensors keep the robot aware of the industrial surroundings. The robotic manipulator is the robot's arm that assists it in moving and positioning, while the end effectors assist in interacting with the workpieces. Collaborative, cartesian, SCARA, cylindrical, and articulated robots are five types of robots used in industry. The degree of freedom of movement, size requirements, and payload capacity all influence the type of robot chosen. Industrial robots aid in the optimization of production processes for a healthy and efficient outcome. These features further increase the Industrial Robotics Market growth.

MARKET DRIVERS

The primary driver fueling the global industrial robotics market is government initiatives and public–private partnerships to lessen the impact of COVID-19. The Advanced Robotics for Manufacturing (ARM) Institute is a public-private collaboration that aims to boost American manufacturers' competitiveness by cooperating and creating new robotics solutions.

It is funded by the US Department of Defense. The institution has requested speedy and high-impact robotics projects to provide the quick response required for the COVID-19 pandemic. The Indian government has granted a Rs 1.45 trillion incentive package by extending the production-linked incentive (PLI) plan to eleven industrial sectors, with a particular focus on the car and vehicle component industries. As part of its China exit program, the Japanese government has set aside USD 221 million in subsidies for Japanese enterprises to relocate to India and other locations. The French government has provided financial assistance to businesses by guaranteeing the repayment of certain qualifying loans up to USD 358 billion under its State Guarantee scheme. To combat the consequences of the COVID-19 outbreak, Indonesia launched two stimulus packages. The first package, worth $725 million, was announced in February 2020, while the second, at $8 billion, was announced in March 2020. The second stimulus package was introduced to safeguard the economy and small and medium-sized businesses (SMEs), notably in the manufacturing sector. The increased use of automation in the automobile production process, as well as the integration of AI and digitalization, is driving up demand for industrial robots in the industry.

MARKET RESTRAINTS

A robotic automation project can be challenging, particularly for companies that have never completed one before. Not only is a large financial investment necessary for the robot itself, but also for its integration, programming, and maintenance. A bespoke integration may be necessary in some circumstances, which will increase the total expenses. Due to a shortage of space and infrastructure, robot deployment may not always be practicable. Because SMEs are often involved in low-volume production, obtaining a return on investment (ROI) can be challenging.

The difficulty is demonstrated by the presence of enterprises with seasonal or variable production schedules. Fast-changing consumer tastes will necessitate regular robot retraining since items are changed on average once a year. Over-automation can sometimes be problematic. Compared to its Japanese competitors, the US automobile industry began with a higher level of mechanization. Cost overruns arose when product lines and consumer demand altered over time, and many robots became obsolete or obsolete. A company's operating costs may not always be reduced by replacing human personnel.

A collaborative robot system can range in price from $3,000 to $100,000. A commercial robotic system might cost anything from $15,000 to $150,000. Automation is an expensive investment for SMEs, especially when they are involved in low-volume manufacturing, due to the cost of industrial robots, integration fees, and peripherals such as end-effectors and vision systems. Therefore, these factors further decrease the global Industrial Robotics Market size.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.6% |

| Segments Covered | By Type, End-user Industry, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Ericsson, Kuka AG, Kawasaki Heavy Industries Ltd, Fanuc Corporation, ABB Ltd, Denso Corporation, Mitsubishi Electric Corporation, Rockwell Automation, Inc, Bosch GmbH, Yaskawa Electric Corporation, Toshiba Corporation |

SEGMENTAL ANALYSIS

By Type Insights

The articulated segment led the Industrial Robotics Market in terms of revenue in 2020. However, the cylindrical segment is predicted to develop at the fastest CAGR throughout the forecast period. The electrical and electronics category led the market in 2020, according to the industry, while the food and drinks segment is predicted to grow at the fastest rate shortly. In terms of revenue, the materials handling category dominated the market in 2020; however, the painting & dispensing sector is expected to grow at the fastest rate during the forecast period. Asia-Pacific generated the most revenue in 2020, while LAMEA is expected to grow at the fastest rate over the projection period.

By End-user Industry Insights

The fastest-growing category is electrical and electronics, with growth expected to accelerate throughout the evaluation period in the Industrial Robotics Market. Furthermore, the automobile sector has been vying to become the largest end-user of Industrial Robots. The hardware sector has embraced the use of mechanical robots since quality and accuracy are two of the most important aspects of an electronic production facility. The rising range of activities that robots can accomplish, notably in the assembly of electronic equipment and components, is one of the main reasons why electrical and electronic is the largest market for Industrial Robots.

REGIONAL ANALYSIS

The Industrial Robotics market was dominated by the Asia Pacific, followed by Europe and North America. Market development is likely to be fueled by high and early adoption of breakthrough technologies in countries like India and China. Because of its strong financial position, it can make major expenditures in cutting-edge equipment and technology to maintain smooth company operations. The Chinese government's "Made in China 2025" plan aims to increase the competitiveness of Chinese businesses through automation.

North America is anticipated to hold a steady CAGR in the global industrial robotics market during the forecast period because of the introduction of Industry 4.0. On the other hand, Europe is trying to exhibit significant growth in the global industrial robotics market, owing to the manufacturers who are working on collaborative robots.

KEY MARKET PLAYERS

Major Key Players in the Global Industrial Robotics Market are

- Kuka AG

- Kawasaki Heavy Industries Ltd

- Fanuc Corporation

- ABB Ltd

- Denso Corporation

- Mitsubishi Electric Corporation

- Rockwell Automation, Inc.

- Bosch GmbH

- Yaskawa Electric Corporation

- Toshiba Corporation

RECENT MARKET NEWS

- Yaskawa Electric Corporation purchased more shares of Doolim-Yaskawa Co., Ltd. in January 2022 to expand its sealing system and robotic painting businesses.

- ABB announced the purchase of ASTI Mobile Robotics Group (ASTI) in July 2021, expanding its robotics and automation capabilities and becoming the first to offer a comprehensive profile for the next generation of flexible automation.

MARKET SEGMENTATION

This research report on the global industrial robotics market has been segmented and sub-segmented based on type, end-user industry, and region.

By Type

- Articulated

- Cartesian

- SCARA

- Cylindrical

- Others

By End-user Industry

- Automotive

- Electrical & Electronics

- Chemical Rubber & Plastics

- Machinery

- Food & Beverages

- Others

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

Why is the industrial robotics market experiencing unprecedented growth worldwide?

The market is growing rapidly due to increasing factory automation, labor shortages, rising demand for operational efficiency, and the adoption of Industry 4.0 technologies across manufacturing sectors.

What are industrial robots and how are they transforming modern manufacturing?

Industrial robots are programmable automated machines designed to perform tasks such as welding, assembly, material handling, packaging, inspection, and painting with high precision and consistency.

Which industries are driving the highest demand for industrial robotics solutions?

Automotive, electronics, metal fabrication, food and beverage, pharmaceuticals, logistics, and consumer goods industries are driving the highest demand.

How do industrial robots improve manufacturing productivity and efficiency?

They increase production speed, improve product quality, reduce operational errors, minimize downtime, and enable continuous production processes.

What types of industrial robots are most widely used in manufacturing facilities?

Articulated robots, SCARA robots, Cartesian robots, collaborative robots (cobots), and delta robots are among the most widely used industrial robotic systems.

Why are manufacturers investing heavily in industrial automation and robotics?

Manufacturers are investing to reduce labor costs, improve workplace safety, enhance production flexibility, and maintain competitiveness in global markets.

How is artificial intelligence influencing the future of industrial robotics?

AI enables robots to perform adaptive learning, predictive maintenance, machine vision inspection, intelligent decision-making, and autonomous operations.

What challenges could impact the growth of the industrial robotics market?

High initial investment costs, integration complexities, cybersecurity concerns, workforce skill gaps, and maintenance requirements could affect market growth.

Which regions are expected to dominate the industrial robotics market?

Asia Pacific leads the market due to strong manufacturing activity, while Europe and North America continue to drive innovation through advanced automation technologies.

How are collaborative robots changing industrial automation strategies?

Collaborative robots enable safe human-robot interaction, improve workplace flexibility, reduce deployment costs, and support automation in small and medium-sized enterprises.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com