Global Industrial Starch Market Size, Share, Trends, & Growth Forecast Report, Segmented By Source (Corn, Wheat, Potato, Cassava), Type (Native Starch, Starch Derivatives & Sweeteners (Modified Starch, Other Derivatives & Sweeteners)), Application (Feed, Food & Beverages, Paper Industry), Form (Liquid, Dry), And Region (North America, Europe, APAC, Latin America, Middle East And Africa), Industry Analysis From 2026 To 2034

Market Size, 2025

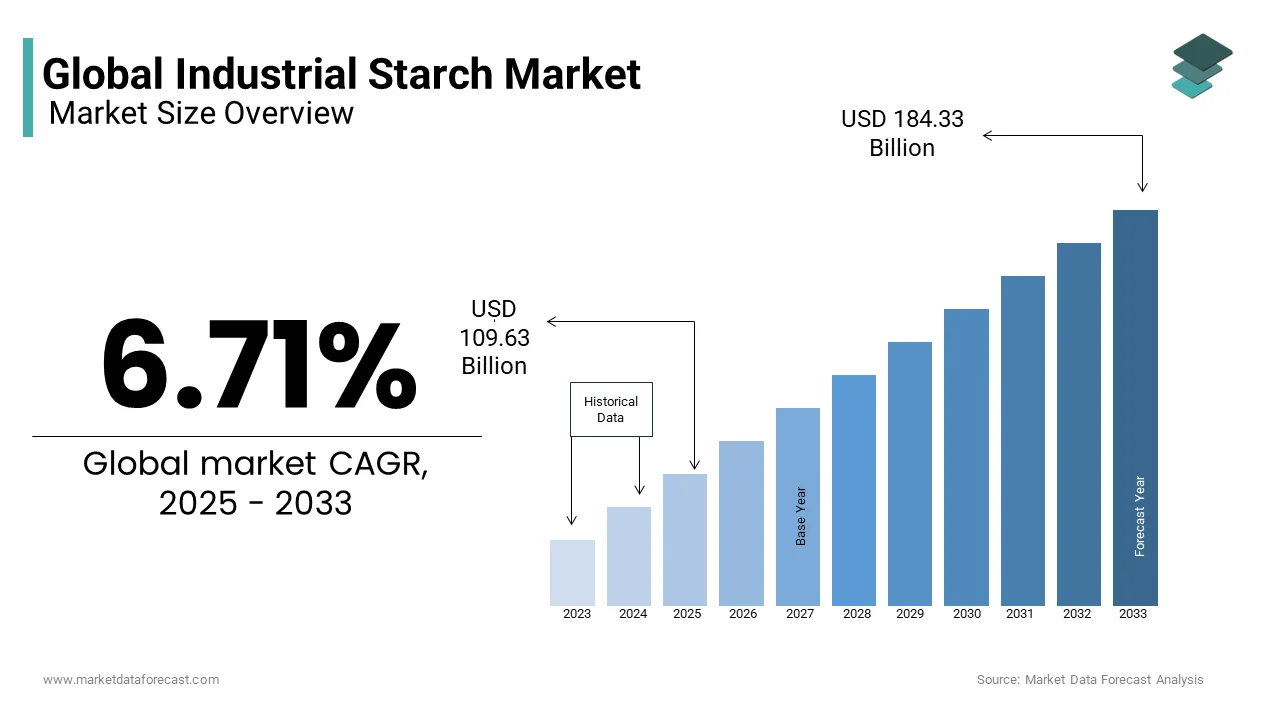

$109.63 BnMarket Estimate, 2026

$116.99 BnMarket Forecast, 2034

$196.69 BnCAGR, 2026–2034

6.71%Global Industrial Starch Market Size

The global industrial starch market size was valued at USD 109.63 billion in 2025 and is anticipated to reach USD 116.99 billion in 2026 to reach USD 196.69 billion by 2034, growing at a CAGR of 6.71% during the forecast period from 2026 to 2034.

Industrial starch is the production and commercial use of starch derived primarily from crops such as corn, wheat, cassava, and potatoes for non-food applications across various industries. Unlike food-grade starch, this is utilized in manufacturing processes that demand binding, thickening, adhesive, or gelling properties. It is crucial in sectors including paper and packaging, textiles, pharmaceuticals, construction, adhesives, and biofuels.

Moreover, global starch production has seen a steady rise due to increasing industrialization and the need for sustainable raw materials. The shift toward biodegradable and renewable resources has further boosted its adoption, especially in regions prioritizing environmental sustainability. As per the European Starch Association, Europe remains a key hub for industrial starch utilization, particularly in the paper and textile industries.

Besides, the growing emphasis on green chemistry and bio-based alternatives to petrochemical-derived products has enhanced the relevance of industrial starch in chemical synthesis and polymer production. In North America and the Asia-Pacific, governments have been promoting bio-based inputs through subsidies and regulatory incentives, encouraging industries to incorporate starch-based solutions.

While corn remains the dominant source of industrial starch globally, regional variations in feedstock availability influence production patterns. Countries like China are expanding their cassava-based starch industries to meet rising domestic and export demands. The ongoing technological advancements are enhancing the functional properties of starch, so its role in industrial applications continues to evolve, which is making it a strategic component in sustainable manufacturing practices worldwide.

MARKET DRIVERS

Rising Demand for Sustainable and Biodegradable Materials

The growing demand for sustainable and biodegradable materials across multiple industries is one of the most significant drivers of the industrial starch market. Increasing awareness about plastic pollution and carbon emissions has prompted manufacturers to seek eco-friendly alternatives in packaging, textiles, and chemical production. Industrial starch, being a renewable and compostable resource, is increasingly used as a substitute for synthetic polymers in packaging films, coatings, and disposable products.

Moreover, regulatory support for reducing single-use plastics has accelerated this transition. Like, the European Commission has implemented directives banning certain single-use plastic items across the EU, including Germany, France, and Italy, which has led to a surge in starch-based bioplastics. Companies like Novamont have developed starch-composite materials that offer similar performance characteristics to conventional plastics but with significantly lower environmental impact.

In addition, the biofuels sector is leveraging industrial starch for ethanol production, aligning with global efforts to reduce fossil fuel dependency. As reported by the International Energy Agency (IEA), starch-based bioethanol is playing an expanding role in transportation fuels, particularly in the U.S. and Brazil. This shift is strongly reinforcing the growth trajectory of the industrial starch market.

Expansion of the Paper and Textile Industries in Emerging Economies

The rapid expansion of the paper and textile industries, particularly in emerging economies, is another major driver fueling the industrial starch market. For instance, the Indian paper industry alone expanded in 2023, driven by increased demand for packaging and writing paper, both of which utilize starch as a key binding agent. Further, in the textile sector, starch derivatives are extensively used for sizing cotton yarns, improving fabric strength, and enhancing dye absorption. The demand for processed paper and textiles is expected to remain strong, ensuring sustained growth in industrial starch consumption across these vital sectors.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

The volatility in raw material prices, primarily stemming from fluctuations in the agricultural commodity industry, is a major restraint affecting the industrial starch market. Starch is largely sourced from crops such as corn, wheat, cassava, and potatoes, all of which are subject to price swings influenced by weather conditions, geopolitical tensions, and trade policies. Like, global corn prices experienced an increase in 2023 due to supply chain bottlenecks and adverse climatic conditions in major producing regions.

These price fluctuations directly impact production costs for starch manufacturers, leading to inconsistent pricing structures for downstream industries. Small-scale starch processors were disproportionately affected, limiting their ability to compete with larger firms.

Furthermore, global supply chain disruptions, exacerbated by events such as the Red Sea shipping crisis and labor strikes at key ports, have delayed raw material deliveries and increased logistics expenses. These challenges are hindering the overall growth potential of the industrial starch market.

Regulatory Restrictions and Environmental Concerns Related to Starch Processing

Environmental concerns surrounding the processing of industrial starch pose a significant challenge to market expansion. The starch extraction and modification process generates wastewater containing organic residues. This has led to stricter discharge regulations in Europe and North America, compelling manufacturers to invest in costly wastewater treatment infrastructure. Moreover, certain chemical modifications used to enhance starch functionality, such as acid hydrolysis and cross-linking, have come under scrutiny for their environmental impact. According to the U.S. Environmental Protection Agency (EPA), some starch-processing plants have been required to adopt cleaner production methods or face penalties under updated industrial effluent standards. These compliance requirements increase capital expenditure and operational complexity, particularly for smaller players who lack the resources to implement large-scale environmental controls.

MARKET OPPORTUNITY

Increasing Use of Modified Starch in Bio-Based Packaging Solutions

The expanding use of modified starch in bio-based packaging solutions is a significant opportunity in the industrial starch market. Modified starch, particularly thermoplastic starch (TPS), offers a viable solution by enabling the production of compostable films and containers.

This trend is being reinforced by government mandates aimed at reducing plastic waste. In response, major packaging firms have integrated starch-based compounds into their product lines, targeting food and beverage, personal care, and pharmaceutical industries. Besides, innovations in starch modification techniques such as esterification and grafting have improved mechanical strength and moisture resistance, making starch-based packaging more commercially viable. Like, new bio-packaging launches contained starch-based components, indicating a strong upward trajectory. With environmental consciousness shaping purchasing decisions across global markets, the industrial starch sector is well-positioned to capitalize on the growing momentum of sustainable packaging solutions.

Growth in the Pharmaceutical and Nutraceutical Sectors

The pharmaceutical and nutraceutical industries present a promising growth avenue for the industrial starch market, driven by the increasing use of starch derivatives in drug formulation and dietary supplements. As per the International Pharmaceutical Excipients Council (IPEC), starch serves as a critical excipient in tablet manufacturing, acting as a disintegrant, binder, and filler due to its excellent compressibility and flow properties.

In the nutraceutical space, starch-based ingredients are being incorporated into encapsulation matrices and controlled-release formulations to enhance nutrient delivery and stability. Moreover, advancements in starch derivatization, such as hydroxypropylation and carboxymethylation, have broadened its application scope in pharmaceutical dosage forms, including orally disintegrating tablets and sustained-release capsules.

MARKET CHALLENGES

Competition from Synthetic and Alternative Biopolymers

The growing competition from synthetic and alternative biopolymer materials that offer superior performance characteristics in specific applications is one of the primary challenges facing the industrial starch market. As per the American Chemical Society (ACS), synthetic polymers such as polyvinyl alcohol (PVA) and polyacrylates continue to dominate industries requiring high tensile strength, moisture resistance, and thermal stability—attributes where native starches often fall short without extensive modification.

Besides, the emergence of alternative biopolymers like polylactic acid (PLA), polyhydroxyalkanoates (PHA), and cellulose derivatives has intensified competition in the bio-based materials segment. While starch can be chemically modified to improve functionality, the added processing steps increase production costs and complexity, making it less competitive in price-sensitive markets.

Limited Shelf Life and Storage Requirements of Starch-Based Products

The limited shelf life and specific storage requirements of starch-based products, which can affect usability and performance in downstream applications, are a persistent challenge in the industrial starch market. As per the Institute of Food Technologists (IFT), unmodified starch tends to retrograde over time, leading to gel hardening, texture degradation, and reduced viscosity—issues that are particularly problematic in food, pharmaceutical, and adhesive industries. Moreover, starch-based materials are highly hygroscopic, meaning they readily absorb moisture from the environment, which can compromise structural integrity and accelerate microbial spoilage. For instance, improper storage conditions can result in loss of functional properties. These storage constraints increase logistics and inventory management costs, particularly for manufacturers operating in tropical and humid climates where humidity levels are consistently high. So, widespread implementation remains a challenge due to associated costs and technical barriers.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.71% |

| Segments Covered | By Source, Type, Application, Form, and Region |

| Various Analyses Covered | Global, Regional and Country Level Analy, sis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Cargill, Archer Daniels Midland Company, Ingredion Incorporated, Tate & Lyle PLC, AGRANA Beteiligungs-AG, Grain Processing Company, Roquette Frères, The Tereos Group, Royal Cosun, and Altia Industrial Services. |

SEGMENTAL ANALYSIS

By Source Insights

The corn segment dominated the industrial starch market by accounting for 45.1% of total global production in 2025. The high starch content and efficient processing capabilities of corn, particularly in North America and China, are key drivers behind the growth of the corn segment. As per the U.S. Grains Council, corn contains about 72–73% starch by weight, making it more efficient than wheat or cassava in terms of yield per tonne. Apart from these, government support and well-established supply chains have reinforced corn’s position as the leading source. In China, government-backed initiatives promoting domestic starch production have led to the expansion of corn-based processing facilities, particularly in provinces like Jilin and Heilongjiang.

The cassava segment is emerging as the fastest-growing source of industrial starch and is projected to expand at a CAGR of 6.2% between 2025 and 2033. The availability of large-scale cassava cultivation in tropical climates, particularly in Thailand, Indonesia, and Nigeria, is a primary factor driving the surge of the cassava segment. Its growth rate significantly outpaces that of other sources due to increasing adoption in the Asia-Pacific and Africa. Like, Thailand remains the world's largest exporter of cassava products, supplying over 10 million tonnes of starch and starch derivatives annually. The crop thrives in poor soil conditions with minimal water input, making it an economically viable option for smallholder farmers. Moreover, the growing demand for gluten-free and allergen-free starch alternatives in food and pharmaceutical applications has boosted cassava’s appeal.

By Type Insights

The modified starch segment commanded the industrial starch market by capturing 42.4% of total revenue in 2024. The superior performance characteristics achieved through chemical, physical, or enzymatic modifications are one of the main reasons for the dominance of the modified starch segment. As per the American Association of Cereal Chemists (AACC), modified starches offer improved stability, viscosity, freeze-thaw resistance, and moisture retention—qualities essential in food processing, pharmaceutical tablets, and paper coatings. These attributes make them indispensable in high-performance applications where native starch would otherwise fail. Also, the growing demand for convenience foods and processed products has increased reliance on modified starches. Its use in instant soups, ready-to-eat meals, and frozen desserts ensures product consistency and extended shelf life. Furthermore, advancements in clean-label modification techniques such as hydroxypropylation and cross-linking are enabling manufacturers to meet consumer demands for enhanced functionality without compromising transparency.

The native starch segment is experiencing the highest growth rate in the industrial starch market and is likely to expand at a CAGR of 5.8% in the coming years. The increasing demand for clean-label and organic products in the food and beverage sector is one key driver of the native starch segment. This shift is particularly strong in baby food, dairy, and health-conscious snacks, where ingredient simplicity is a major selling point. Its growth trajectory is accelerating due to shifting consumer preferences toward natural and minimally processed ingredients. In addition, regulatory pressures against synthetic food additives are pushing industry players to explore native starch alternatives. Beyond food, native starch is gaining traction in eco-friendly adhesives, animal feed, and biodegradable packaging films.

By Application Insights

The paper industry segment constituted the prominent application in the industrial starch market by representing 36.7% of total demand in 2024. The essential role of starch in enhancing paper strength, printability, and smoothness is a major reason for the prominence of the paper industry segment. As per the Confederation of European Paper Industries (CEPI), starch improves fiber bonding and reduces dusting during printing processes, making it a critical additive in both board and fine paper manufacturing. In particular, modified starches such as oxidized and cationic variants are extensively used for improving runnability on high-speed paper machines. Also, the growth of the corrugated packaging industry has further bolstered starch consumption. Starch-based adhesives play a crucial role in box assembly, offering environmental advantages over synthetic glues.

The feed industry segment is the fastest-growing application area for industrial starch and is projected to expand at a CAGR of 6.4%. The use of starch as an energy source in compound animal feed formulations is one of the primary drivers of the industry segment. As per the Food and Agriculture Organization (FAO), global meat and dairy consumption has risen steadily, prompting feed manufacturers to enhance the nutritional density and digestibility of feedstocks. Industrial starch serves as a cost-effective binder and energy booster in poultry, swine, and cattle feed. Besides, advancements in feed processing technologies have expanded the use of gelatinized and pregelatinized starches in pelleted and extruded feeds. Moreover, the shift toward plant-based feed ingredients amid concerns over antibiotic overuse has encouraged the incorporation of starch-based binders and bulking agents.

REGIONAL ANALYSIS

North America Market Analysis

North America held the top position in the industrial starch market by contributing 27.3% of total revenue in 2024. A key factor behind this leadership is the large-scale corn cultivation and starch extraction capacity in the United States, particularly in the Midwest Corn Belt. As per the U.S. Department of Agriculture (USDA), the U.S. produces over 360 million metric tons of corn annually, a significant portion of which is converted into starch for use in food, pharmaceuticals, and industrial applications. In addition, strong regulatory frameworks supporting bio-based materials have reinforced starch usage in packaging and adhesives.

Europe Market Analysis

Europe commanded a significant share of the global industrial starch market. A key growth driver is the EU’s emphasis on reducing plastic dependency through biodegradable alternatives. As per the European Commission, directives banning single-use plastics have prompted the widespread adoption of starch-based films and coatings in food packaging. Countries like Germany, France, and the Netherlands have led the transition, integrating thermoplastic starch into compostable packaging formats. In addition, the paper industry remains a dominant consumer of starch derivatives, particularly in Finland and Sweden, where pulp and paper manufacturing is a core economic activity. According to CEPI, European paper mills utilize over 1.5 million tonnes of starch annually for surface sizing and adhesive applications.

Asia-Pacific Market Analysis

Asia-Pacific is rapidly expanding in the industrial starch market, with China and India leading in terms of production and consumption. A key factor supporting this growth is the rising demand for starch-based sweeteners and modified starches in food and beverage manufacturing. Besides, India’s cassava-based starch industry is witnessing strong growth, particularly in Tamil Nadu and Kerala. So, Asia-Pacific is positioned for continued expansion in industrial starch consumption, particularly in bio-packaging and nutraceutical applications.

Latin America Market Analysis

Latin America is emerging in the global industrial starch market. A major growth driver is the large-scale cassava and maize cultivation in Brazil, which supports both domestic starch production and export markets. Also, Brazil produces around 20 million tonnes of cassava annually, a significant portion of which is processed into starch for food, feed, and industrial uses. Also, Argentina’s corn starch industry is expanding due to favorable climatic conditions and government incentives.

Middle East and Africa Market Analysis

The Middle East and Africa collectively account for a notable share of the industrial starch market. A key factor supporting this presence is the expansion of the food processing and bakery industries, particularly in the Gulf Cooperation Council (GCC) countries. Like, starch consumption in Saudi Arabia and the UAE has grown due to rising demand for convenience foods and processed bakery items. Moreover, South Africa’s starch-based ethanol industry plays a minor but notable role in fuel blending initiatives.

COMPETITIVE LANDSCAPE

- The industrial starch market is highly competitive, characterized by the presence of well-established multinational corporations alongside numerous regional and local producers. Leading players such as Cargill, Ingredion, and Roquette dominate due to their extensive R&D capabilities, global distribution networks, and strong brand recognition. These firms continuously innovate to improve product performance and expand application areas, particularly in bio-based packaging and clean-label food formulations.

- At the same time, regional starch processors are gaining traction by offering cost-effective alternatives tailored to local industry needs. In countries like China, India, Brazil, and Thailand, domestic companies leverage abundant raw material availability and lower production costs to compete effectively in both domestic and export markets.

- Competition is further intensified by the increasing integration of starch derivatives into high-value applications such as pharmaceutical excipients and biodegradable polymers. As sustainability becomes a central theme across industries, players are differentiating themselves through eco-friendly sourcing, traceability, and specialized product offerings. This dynamic environment fosters continuous innovation, strategic expansion, and operational efficiency among market participants seeking to maintain or enhance their market positions.

KEY MARKET PLAYERS

The key market players of the Global Industrial Starch Market are

- Cargill

- Archer Daniels Midland Company

- Ingredion Incorporated

- Tate & Lyle PLC

- AGRANA Beteiligungs-AG

- Grain Processing Company

- Roquette Frères

- The Tereos Group

- Royal Cosun

- Altia Industrial Services.

Top Players In The Market

- Cargill is a global leader in agricultural and food ingredient solutions, with a strong presence in the industrial starch market. The company offers a wide range of starches and starch derivatives for use in food, pharmaceuticals, paper, and bioplastics. Known for its vertically integrated supply chain, Cargill ensures consistent quality and availability of raw materials, making it a trusted partner for large-scale manufacturers across the globe.

- Ingredion specializes in starch-based ingredients and biomaterials, catering to diverse industries including food, beverage, paper, and packaging. With a focus on innovation and sustainability, the company develops customized starch solutions that meet evolving consumer and regulatory demands. Ingredion’s expertise in starch modification and functional properties has positioned it as a key player in both North American and international markets.

- Roquette is a French manufacturer renowned for its plant-based ingredients, including starches derived from potatoes, corn, and peas. The company emphasizes clean-label and sustainable processing methods, aligning with global trends toward natural and eco-friendly products. Roquette’s commitment to research and development has led to the creation of advanced starch formulations used in pharmaceuticals, food processing, and biodegradable packaging, reinforcing its competitive edge in the industrial starch sector.

Top Strategies Used By Key Market Participants

One of the primary strategies employed by leading players in the industrial starch market is product innovation through advanced starch modification technologies. Companies are investing heavily in R&D to develop modified starches with enhanced functionalities such as improved viscosity, thermal stability, and moisture resistance, catering to specific industry needs in food, packaging, and pharmaceuticals.

Another major strategy is expanding into emerging markets with growing industrial and food processing sectors. Major players like Cargill and Ingredion are strengthening their regional presence through new production facilities, joint ventures, and partnerships in Asia-Pacific, Latin America, and Africa, where demand for starch-based products is rising due to urbanization and dietary shifts.

Lastly, adopting sustainable sourcing and green manufacturing practices is a key trend among industry leaders. As environmental regulations tighten and consumer preferences shift toward eco-friendly products, companies are integrating responsible farming, water-efficient processing, and biodegradable starch applications into their operations to enhance brand reputation and comply with global sustainability standards.

RECENT MARKET NEWS

- In January 2024, Cargill announced the launch of a new line of enzyme-modified starches designed specifically for clean-label bakery applications, aiming to meet rising consumer demand for natural ingredients without compromising texture or shelf life.

- In March 2024, Ingredion expanded its production facility in Paraguay to increase the output of native and modified starches for the Latin American food and beverage industry, reinforcing its supply chain resilience and regional market presence.

- In June 2024, Roquette inaugurated a state-of-the-art research center in France focused on developing next-generation plant-based starches for pharmaceutical and packaging applications, enhancing its innovation pipeline and technical leadership.

- In September 2024, Tate & Lyle entered a strategic partnership with a European bioplastics firm to co-develop thermoplastic starch compounds for compostable packaging, aligning with global sustainability goals and expanding its industrial starch footprint.

- In November 2024, KMC (Korea Maize Starch Co.) launched a new line of gluten-free modified starches targeted at the Asian food processing sector, capitalizing on growing health-conscious consumer trends and regulatory shifts favoring transparency in food labeling.

MARKET SEGMENTATION

This research report on the global industrial starch market has been segmented and sub-segmented based on source, type, application, form, and region.

By Source

- Corn

- Wheat

- Potato

- Cassava.

- Corn acco

By Type

- Native Starch

- Starch Derivatives & Sweeteners

By Application

- Feed, Food & Beverages

- Paper Industry.

By Form

- Liquid form

- Dry form

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What is industrial starch?

Industrial starch is a carbohydrate extracted from crops like corn, wheat, potato, and cassava, used in non-food industries for binding, thickening, and adhesive properties.

What drives the growth of the global industrial starch market?

Rising demand from paper, textile, adhesives, and biodegradable packaging industries drives market growth.

What are the major sources of industrial starch?

Corn, potato, wheat, and cassava are the primary raw material sources.

Which industries use industrial starch?

Paper & packaging, textile, pharmaceuticals, construction, and food processing industries utilize industrial starch.

How is industrial starch used in paper production?

It improves strength, surface finish, and printability of paper and paperboard products.

What role does industrial starch play in textiles?

Starch is used as a sizing and finishing agent to enhance yarn strength and fabric quality.

Which regions lead the industrial starch market?

Asia-Pacific leads due to strong manufacturing growth; Europe and North America follow with high industrial demand.

Are bio-based starch products gaining traction?

Yes, demand for biodegradable and eco-friendly alternatives in packaging and plastics supports starch usage.

What are key challenges in the industrial starch market?

Price fluctuations of raw materials, climate impacts on crop yields, and competition from synthetic polymers are major challenges.

What is the future outlook for the global industrial starch market?

The market is expected to grow steadily with rising industrialization, sustainable product demand, and expansion in end-use sectors.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com