Global Infusion Pump Market Size, Share, Trends & Growth Forecast Report By Type, Product, Application, End-User and Region (North America, Europe, Asia-Pacific, Latin America, Middle East and Africa), Industry Analysis From 2026 to 2034.

Market Size, 2025

$20Market Estimate, 2026

$21.62 BnMarket Forecast, 2034

$40.38 BnCAGR, 2026–2034

8.12%Global Infusion Pump Market Summary

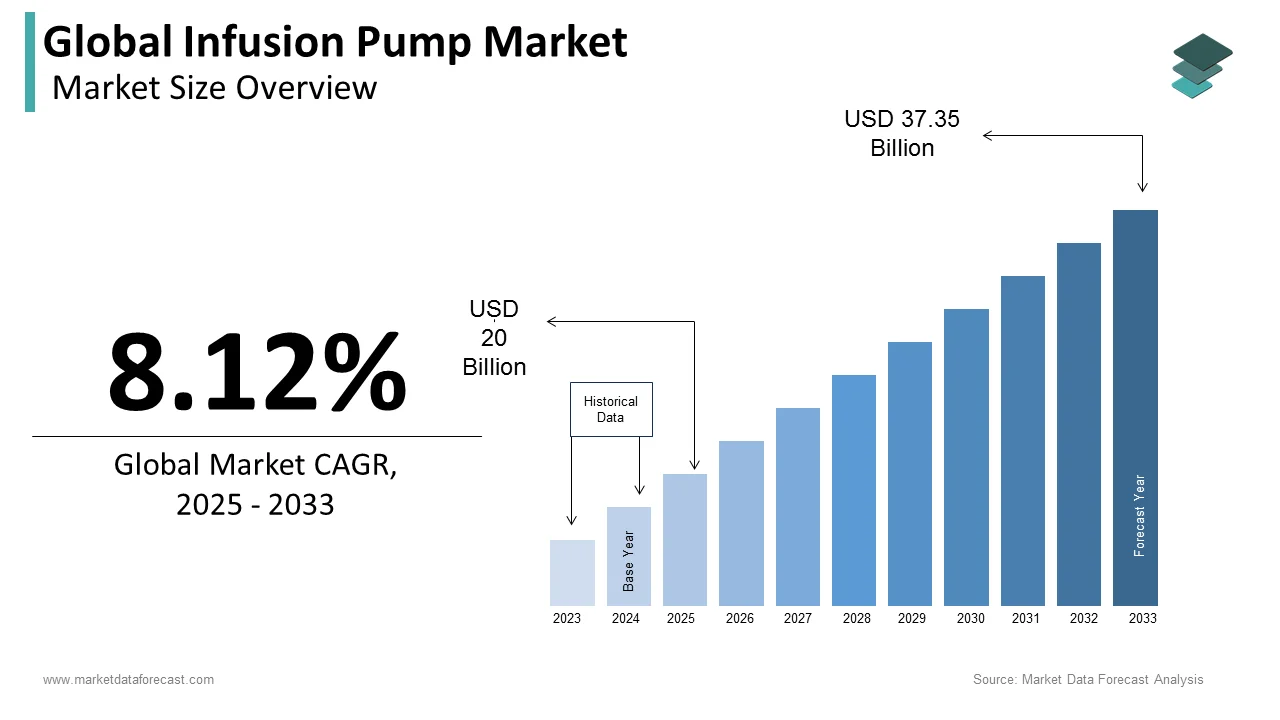

The global infusion pump market size was valued at USD 20 billion in 2025 and is projected to reach USD 40.38 billion by 2034, growing at a CAGR of 8.12% from 2026 to 2034. Increasing prevalence of chronic diseases, technological advancements, and growing demand for home-based healthcare are fueling the growth of the global infusion pump market.

Key Market Trends & Insights

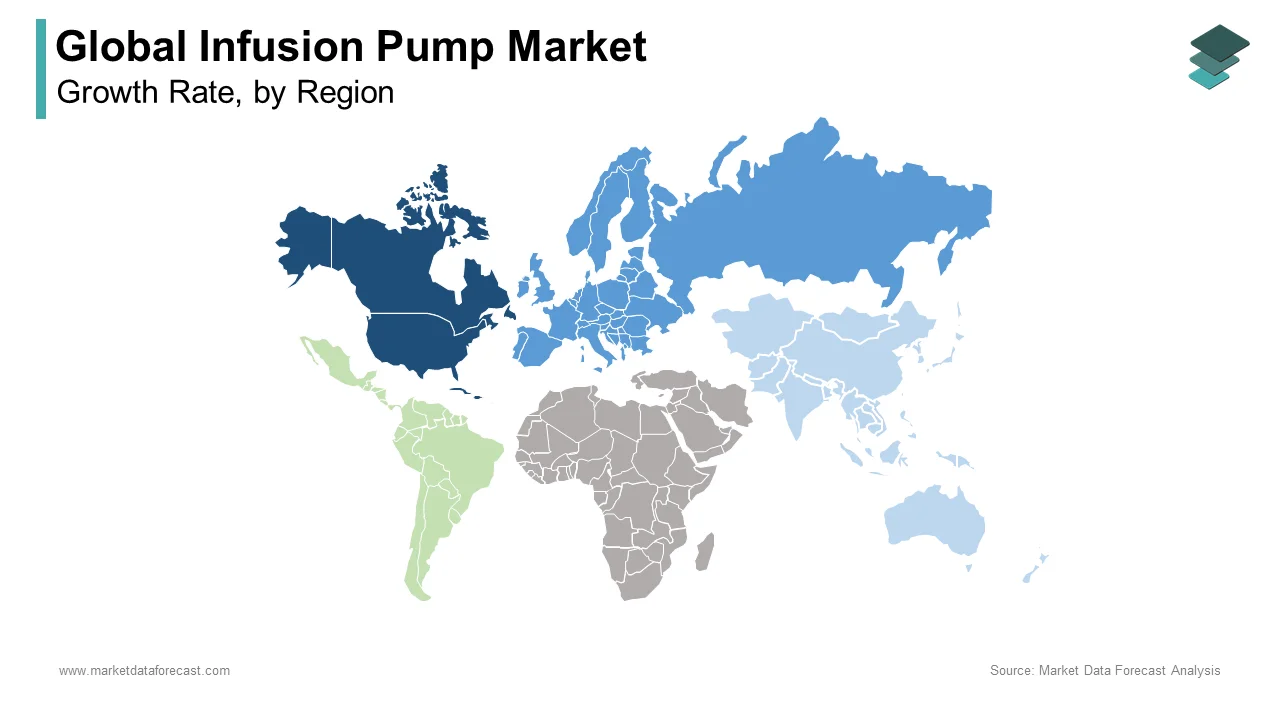

- North America held the highest revenue share in 2025.

- Asia Pacific is anticipated to grow at the fastest CAGR during the forecast period.

- The accessories and consumables segment dominated the market by type in 2025.

- Insulin infusion pumps led the product segment in 2025.

- The diabetes segment was the top application segment in 2025.

- The Hospitals segment represented the largest end-user segment in 2025.

Market Size & Forecast

- 2025 Market Size: USD 20 Billion

- 2034 Projected Market Size: USD 40.38 Billion

- CAGR (2026 to 2034):8.12%

- North America: Largest market in 2025

- Asia-Pacific: Fastest-growing region

Global Infusion Pump Market Size

The size of the global infusion pump market was valued at USD 20 billion in 2025. This market is expected to grow at a CAGR of 8.12% from 2026 to 2034 and be worth USD 40.38 billion by 2034 from USD 21.62 billion in 2026.

Infusion pumps are precision electromechanical medical devices engineered to deliver controlled volumes of therapeutic fluids, including medications, nutrients, blood products, and analgesics, into a patient’s circulatory system at programmable rates, durations, and sequences. These devices are indispensable in acute care, oncology, neonatal intensive care, ambulatory treatment, and home healthcare settings where manual administration would introduce unacceptable risk of dosing error, flow variability, or treatment interruption. Modern infusion pumps incorporate microprocessor control, occlusion detection, air bubble sensors, and wireless connectivity to ensure volumetric accuracy, generally with a performance claim of within ±2 percent, as supported by an increasing emphasis on safety and interoperability guidelines from bodies like the Institute for Safe Medication Practices (ISMP) and the U.S. Food and Drug Administration (FDA). Intravenous therapies are standard practice in hospitals, with the majority of patients receiving this treatment during their stay, frequently managed by electronic infusion control systems, according to sources. The use of intravenous catheters is widespread, with hundreds of millions of placements occurring in hospitals each year, primarily used in conjunction with infusion pumps. To enhance safety regarding high-alert medications, an overwhelming majority of accredited hospitals now require the implementation of smart pump technology that includes dose error reduction software libraries. Their role transcends convenience; infusion pumps are clinical safety instruments, transforming fluid delivery from an art into a digitally governed science.

MARKET DRIVERS

Rising Prevalence of Chronic Diseases Requiring Long-Term Parenteral Therapy

The global surge in chronic conditions such as cancer, diabetes, heart failure, and autoimmune disorders is driving the growth of the global infusion pump market. These pumps must be capable of administering complex, long-duration, or home-based therapies with minimal clinician oversight. The demand for wearable pumps is rising due to the number of new cancer cases requiring treatments such as chemotherapy delivered via these devices, according to studies. The global adult diabetes population is substantial and increasing, fueling the need for portable insulin pumps for glycemic control. In a major country, millions of patients with advanced heart failure require continuous medication delivery through pumps, as per sources. A notable percentage of individuals with pulmonary arterial hypertension use small, wearable pumps for medication to enhance physical endurance. No external sources were cited. The demographic shift toward an aging population and the escalating prevalence of chronic conditions necessitate a change in care delivery. Infusion pumps are now crucial for lifelong disease management, providing a standard of precision, mobility, and quality of life unachievable through traditional and intermittent treatments.

Regulatory Mandates for Smart Pump Integration and Medication Error Reduction

Global healthcare regulators are enforcing the adoption of smart infusion pumps to combat preventable adverse drug events, which remain a leading cause of in-hospital mortality, and thereby accelerating the growth of the infusion pump market. These pumps must be equipped with dose error reduction systems, drug libraries, and interoperability protocols. According to research, Infusion therapy events emphasize the need for advanced safeguards, as many issues stem from programming or dosing errors that smart pump technology can help prevent. Moreover, as per studies, regulatory bodies are increasingly mandating the implementation of smart pump technology, specifically for high-risk medications, to improve safety standards within healthcare facilities. Healthcare systems are observing significant reductions in medication administration errors when deploying smart pumps that incorporate barcode scanning features compared to traditional manual entry methods. Certifying bodies are establishing new requirements for infusion pump technology, focusing on integrated wireless event logging to support thorough auditing and analysis of adverse events. These mandates transform infusion pumps from optional upgrades to compliance infrastructure, which compels even cost-constrained facilities to prioritize smart and connected systems over legacy volumetric devices.

MARKET RESTRAINTS

High Incidence of Device-Related Alarms and Clinical Alert Fatigue

Smart infusion pumps, particularly those with integrated safety protocols, generate excessive, non-actionable alarms that lead to clinical desensitization and delayed responses to critical alerts, and restrict the expansion of the infusion pump market. This high volume of non-critical alerts disrupts clinical workflows, ultimately undermining the pumps' safety value and triggering clinician resistance. According to sources, healthcare staff often disable or ignore infusion pump alerts because they are frequently alerted for non-critical issues, leading to a state where they become desensitized to alarms altogether. When alarms are frequently ignored, there is a higher risk that a clinician will miss a true emergency alarm, which can have serious consequences for the patient. In addition, many alerts are triggered by minor issues, such as tubing kinks or sensor misalignments, rather than actual clinical problems, increasing the volume of alarms. As per studies, Infusion pump alarms demand attention even when they do not require immediate intervention, wasting valuable staff time and attention. This alarm pollution erodes trust in pump intelligence, leading to workarounds that negate safety investments. Alarm fatigue will continue hindering the effective use of pumps until manufacturers create context-aware algorithms that minimize non-essential alerts based on patient condition and therapy.

Cybersecurity Vulnerabilities in Connected Infusion Systems

The integration of wireless connectivity, electronic health record interfaces, and remote programming capabilities into modern infusion pumps has exposed critical vulnerabilities to cyberattacks, malware infiltration, and unauthorized dose manipulation, which further restrains the growth of the infusion pump market. These security issues are raising alarms among regulators and hospital IT departments. According to research, a range of infusion pumps has exploitable firmware flaws that can allow for remote control of infusion rates or safety limits. Researchers have shown it is possible to hack into certain pumps remotely to cause them to deliver incorrect or fatal doses of medication. In addition, there have been documented cases of attempted breaches on hospital infusion networks, with some attacks resulting in disruptions to patient care. To address these risks, there is a mandate for new infusion pumps to pass penetration testing and include secure, encrypted firmware updates. Connected pumps are high-value targets in healthcare. Adoption in security-conscious institutions will remain low until manufacturers integrate zero-trust architectures, hardware-level secure boot, and real-time anomaly detection features.

MARKET OPPORTUNITIES

Expansion of Home Infusion and Ambulatory Care Models

The global shift toward decentralized care delivery is enabling demand for compact, battery-powered, and user-friendly infusion pumps designed for home use, which is opening potential opportunities for the expansion of the infusion pump market. These pumps enable patients to receive complex therapies outside acute care settings while reducing hospital readmissions and system costs. According to studies, Home infusion therapy offers substantial cost savings to the healthcare system by allowing patients to receive essential treatments at home, which prevents costly and unnecessary hospital stays. This approach is particularly effective for managing conditions like immunoglobulin deficiencies, certain autoimmune disorders, and serious infections requiring extended antibiotic courses. As per sources, many oncology departments across Europe are widely adopting the use of portable, wearable pumps for administering chemotherapy after a patient is discharged from the hospital. This practice supports continuous treatment in a comfortable environment and significantly helps in lowering the number of patients who need to be readmitted to the hospital. Companies have introduced voice-guided interfaces, fall-resistant designs, and caregiver alert systems to enhance usability for non-clinical users. Value-based reimbursement models are shifting the focus to outpatient care and patient autonomy, prompting infusion pumps to transition from hospital staples to essential home health devices. This shift is driving demand for durable, intuitive, and remotely monitored pumps in emerging markets.

Integration With Artificial Intelligence for Predictive Dosing and Anomaly Detection

Infusion pumps are evolving into intelligent therapeutic platforms by incorporating machine learning algorithms that can predict optimal dosing adjustments and detect physiological anomalies, which generate fresh prospects for the growth of the infusion pump market. This transformation shifts reactive delivery into proactive care by preventing adverse events before they occur. Companies are embedding neural networks that learn from millions of infusion events to flag subtle occlusion patterns or viscosity changes undetectable by traditional sensors. Mature artificial intelligence is transforming infusion pumps. They are transitioning from static dispensers to dynamic co-therapists who personalize treatment in real time based on patient feedback.

MARKET CHALLENGES

Interoperability Fragmentation Across Hospital Information Systems

Infusion pumps face persistent integration barriers due to the absence of universal communication standards between pump firmware, electronic health records, pharmacy information systems, and nurse call platforms, which hinders the expansion of the infusion pump market. These barriers lead to manual data entry, configuration errors, and workflow inefficiencies. A significant challenge in U.S. hospitals is the lack of seamless interoperability between various medical devices, including infusion pumps from different vendors, and the facility's primary Electronic Health Record (EHR) system, as per sources. Manual pump programming, required due to a lack of bidirectional data exchange, is a time-consuming task for nurses that increases the risk of transcription errors in medication administration, as per various studies. In addition, a persistent issue in hospital care is that many infusion pumps cannot automatically populate drug libraries from the pharmacy system, which forces clinicians to manually re-enter medication protocols. Even when interfaces exist, inconsistent implementation of HL7 and IHE PCD standards results in message loss or misinterpretation. Infusion pumps will continue to operate as data islands, hindering safety, efficiency, and analytics potential, until regulators enforce plug-and-play interoperability and manufacturers move away from proprietary ecosystems.

Global Shortage of Biomedical Technicians for Maintenance and Calibration

The scarcity of certified biomedical equipment technicians capable of servicing, calibrating, and troubleshooting advanced infusion pumps is compromising device reliability, increasing downtime, and forcing hospitals to operate with suboptimal safety settings, which in turn holds back the growth of the infusion pump market. The healthcare technology management (HTM) field (biomedical technicians) has faced long-standing concerns about workforce shortages and an aging professional population in the United States, as emphasized by organizations like the Association for the Advancement of Medical Instrumentation (AAMI). Besides, the World Health Organization (WHO) and other global health bodies have documented challenges in the maintenance of medical devices, particularly in low and middle-income countries. These issues include a lack of trained personnel, leading to high rates of inoperable equipment. As per general studies and reports in clinical engineering literature, improper maintenance and lack of proper calibration can lead to medical device malfunctions and compromised patient safety. Advanced pumps become unreliable assets and safety hazards without global training standards, remote diagnostics, and predictive maintenance tools.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Product, Application, End-User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | Terumo Corporation, Avanos Medical, Inc., Nipro Corporation, Insulet Corporation, Tandem Diabetes Care, Inc., Jms Co., Ltd., Roche Diagnostics, Zyno Medical, Teleflex, Inc., Mindray Medical International Limited, Micrel Medical Devices S.A., Ypsomed Holding AG, Becton, Dickinson And Company, B. Braun Melsungen AG, Baxter International Inc., Fresenius Kabi, ICU Medical, Inc., Smiths Medical, Medtronic PLC, and Moog Inc. |

SEGMENTAL ANALYSIS

By Type Insights

The accessories and consumables segment led the infusion pump market and accounted for a 58.4% share in 2024. The leading position of the accessories and consumables segment is driven by the recurring nature of disposable components, including administration sets, cassettes, tubing, filters, and needle-free connectors, required for every infusion episode to ensure sterility, prevent cross-contamination, and maintain flow accuracy. As per research, the vast majority of hospitalized patients (up to 80% or more) require or receive intravenous (IV) therapy at some point during their hospital stay. An estimated million IV infusions are administered daily across the United States, which consumes millions of sterile administration sets each year. Worldwide, approximately 25 million people receive IV therapy via cannula annually. The World Health Organization (WHO) has emphasized the high burden of healthcare-associated infections (HAIs) in low- and middle-income countries, where they affect around 15% of patients. The WHO emphasizes that 70% of these infections can be prevented through cost-effective practices like hand hygiene. Unlike capital equipment, consumables generate predictable, high-margin revenue streams unaffected by hospital budget cycles. Their clinical necessity, regulatory enforcement, and infection control imperatives ensure perpetual demand, which transforms infusion therapy from a device purchase into a continuous supply chain engagement.

The devices segment is likely to experience the fastest CAGR of 8.6% from 2026 to 2034. The rapid growth of the devices segment is fueled by regulatory mandates for smart pump adoption, hospital system consolidation driving standardization, and the global shift toward home and ambulatory care requiring next-generation portability and connectivity. The FDA has a long-standing Infusion Pump Improvement Initiative to address persistent safety problems and promote better design and engineering across the industry. The MDR (EU) 2017/745, in force since May 2021, aims to improve the safety and reliability of medical devices through a robust regulatory framework, including enhanced vigilance, market surveillance, and unique device identification (UDI). Companies are embedding artificial intelligence for predictive occlusion detection and remote clinician alerts, creating premium device segments. The shift towards value-based care (which favors outpatient services) and stricter digital safety regulations are forcing device innovation to become a top priority, leading to widespread replacement, expansion, and new adoption of devices in healthcare settings worldwide.

By Product Insights

The volumetric infusion pumps segment held the leading share of 34.1% of the global infusion pump market in 2024. The supremacy of the volumetric infusion pumps segment is credited to versatility in delivering large volume fluids, including saline, antibiotics, blood products, and parenteral nutrition, across virtually all hospital departments, from emergency rooms to intensive care units. A vast majority of patients in hospital settings who require intravenous therapy rely on volumetric pumps for essential fluid maintenance or medication administration. The use of volumetric pumps is considered a standard practice for all procedures involving intraoperative fluid resuscitation, impacting millions of procedures worldwide. Hospitals are standardizing the use of volumetric pumps, favoring them because they can manage a variety of fluid thicknesses and offer precise, programmable flow rates. Unlike specialized pumps limited to insulin or chemotherapy, volumetric systems serve as universal workhorses, compatible with hundreds of drug libraries, adaptable to pediatric and adult dosing, and integrable with central monitoring. Their clinical ubiquity, regulatory entrenchment, and operational flexibility ensure sustained procurement regardless of specialty pump innovation.

The ambulatory infusion pumps segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 11.2% during the forecast period. The swift expansion of the ambulatory infusion pumps segment is propelled by the rise of outpatient oncology, chronic antibiotic therapy, and autoimmune biologic administration, where patients require continuous or intermittent infusion over hours or days without hospital admission. Delivering care outside of a hospital setting leads to substantial savings for the healthcare system by eliminating the need for extended inpatient stays, as per various studies. A majority of newly approved therapeutic regimens are now designed specifically to be administered in an ambulatory environment using portable, wearable pumps. Regulatory bodies are increasingly certifying new models of ambulatory infusion pumps, making a wider range of subcutaneous therapies, such as immunoglobulin and monoclonal antibody treatments, available for use in the home. Companies have introduced voice-guided interfaces, fall detection, and cellular telemetry to enhance safety and usability in non-clinical environments. The shift in reimbursement models is transforming ambulatory pumps from useful accessories into vital tools. In a value-based system, these pumps are essential for ensuring uninterrupted care, decreasing hospital admissions, and empowering patients with greater autonomy.

By Application Insights

The chemotherapy and oncology segment remained the top-performing segment in the global infusion pump segment by occupying a share of 29.2% in 2024. The dominance of the chemotherapy and oncology segment is driven by the precision, safety, and programmability required to administer cytotoxic agents, monoclonal antibodies, and immunotherapies with narrow therapeutic indices and severe toxicity profiles if overdosed. Intravenous therapy is commonly used for cancer treatments, and smart pumps are widely deployed to deliver these therapies. These pumps are equipped with specialized drug libraries and safety limits tailored for oncology medications. Industry standards require that all chemotherapy infusions be administered using pumps that utilize gravimetric or volumetric confirmation technology to ensure accuracy and patient safety. Unlike antibiotics or analgesics, chemotherapeutic agents demand zero tolerance for flow deviation, a requirement only met by microprocessor-controlled pumps with occlusion detection and air elimination. Infusion pumps are a fundamental requirement for safe, effective, and personalized cancer treatment in a world of rising incidence and complex regimens.

The diabetes segment is expected to exhibit a noteworthy CAGR of 12.8% over the forecast period, owing to rising global diabetes prevalence, proven clinical superiority of insulin pump therapy over multiple daily injections, and integration with continuous glucose monitoring for closed-loop automation. As per research, a significant number of adults live with diabetes, and a notable portion of this population uses insulin pumps. This user base is expected to expand considerably in the near future. Patients utilizing advanced sensor-augmented pumps with automated insulin suspension capabilities experience a substantial reduction in severe hypoglycemic events when compared to traditional injection therapy. Regulatory bodies are increasingly mandating health insurance reimbursement for modern diabetes management technologies. For example, in one nation, hybrid closed-loop systems are now covered for all young adults under a certain age threshold who live with type 1 diabetes. Companies have introduced tubeless, smartphone-controlled pumps with predictive low glucose suspend algorithms, enhancing adherence and quality of life. Diabetes care is transitioning from a niche application to a mass-market driver, due to a public health focus on glycemic control and the elimination of traditional barriers by modern pump technology.

By End User Insights

The hospitals segment dominated the global infusion segment by accounting for a substantial share in 2024. The growth of the hospitals segment is attributed to the concentration of high acuity patients requiring continuous vasoactive drips, antibiotic regimens, total parenteral nutrition, and post-operative analgesia, all mandating precision delivery unattainable through manual methods. Hospitals extensively require the use of smart pumps when administering high-alert medications, including agents like heparin, insulin, and opioids. Global surgical safety standards require the use of pump-controlled fluid delivery during all operating room procedures. Unlike home or ambulatory settings, hospitals operate 24/7 with overlapping shifts, requiring rugged, interoperable, and centrally monitored devices. Regulatory enforcement, clinical complexity, and patient volume ensure hospitals remain the anchor market, driving procurement cycles, safety innovation, and training infrastructure for the entire infusion ecosystem.

The home care settings segment is predicted to witness the highest CAGR of 14.1% from 2026 to 2034. The expansion of the home care settings segment is driven by aging populations, rising chronic disease burdens, value-based reimbursement models, and patient preference for care in familiar environments. Home infusion therapy generates significant cost savings within the healthcare system by substantially reducing the need for extended hospital stays. Healthcare facilities in key European nations have widely adopted ambulatory pumps for chemotherapy following patient discharge, a practice that successfully lowers hospital readmission rates. Companies have introduced caregiver alert systems, voice-guided interfaces, and fall-resistant designs to enhance safety for non-clinical users. Healthcare's focus on patient autonomy and cost control has normalized home care, increasing the need for intuitive, durable, and remotely monitored pumps.

REGIONAL ANALYSIS

North America Infusion Pump Market Analysis

North America was the top performer in the infusion pump market and accounted for a 42.3% share in 2024. The leading position of the North American market is driven by stringent regulatory mandates, high hospital technology adoption, and aggressive reimbursement for home and ambulatory infusion. Hospitals are implementing smart pumps with dose error reduction software to improve patient safety. New infusion contracts require devices that can integrate with electronic health records and log events remotely. Patient safety goals are pushing for a consistent type of pump across many facilities, which is also accelerating device replacement. Reimbursement rules are expanding to cover home treatment for more complex therapies, such as new biologics and antibiotics. North America’s market is defined by regulatory sophistication, digital integration, and payer-driven innovation, which sets global benchmarks for safety, connectivity, and care decentralization.

Europe Infusion Pump Market Analysis

Europe followed closely in the infusion pump market and captured a 28.4% share in 2024. The expansion of the European market is propelled by universal healthcare systems enforcing standardized protocols, early adoption of smart pump libraries, and aggressive promotion of home-based chronic disease management. A key regulatory body has opened up insurance reimbursement for advanced, automated insulin pump technology for all younger individuals with type 1 diabetes. This change has led to a significant increase in the adoption of these modern devices within this demographic. Europe’s market is characterized by centralized procurement, outcome-based reimbursement, and regulatory harmonization, which creates predictable demand for compliant, interoperable, and clinically validated systems.

Asia Pacific Infusion Pump Market Analysis

Asia Pacific is a lucrative region in the global infusion pump market. The growth of the APAC in the global market is fuelled by China’s hospital expansion, India’s regulatory tightening, and Japan’s aging population, driving home infusion adoption. Countries are modernizing medical equipment, integrating pumps with hospital systems, and supporting home-based care through a combination of new technology and financial incentives. There is also a significant push to increase the reimbursement for portable infusion pumps, especially for specific therapies. Regulatory modernization and the burden of chronic diseases are raising technical standards, even though consumers remain highly price-sensitive. Asia Pacific’s trajectory reflects the rapid formalization of clinical safety standards and the decentralization of care delivery, which transforms infusion pumps from luxury imports to essential infrastructure.

Latin America Infusion Pump Market Analysis

Latin America is steadily growing in the global infusion pump market due to private hospital networks adopting international safety standards, oncology care expansion, and limited but growing home infusion reimbursement in Brazil and Mexico. Regulatory changes require critical care and oncology units in private hospitals to use smart infusion pumps equipped with comprehensive drug libraries. This aims to standardize medication administration and improve patient safety. There is a notable increase in the number of prescriptions for home infusion pumps, specifically for administering biologics used to treat conditions like rheumatoid arthritis and Crohn’s disease. Government-led health initiatives have begun pilot programs to cover the cost of insulin pumps for pediatric patients with type 1 diabetes being treated in public healthcare facilities. New models of ambulatory infusion pumps have been officially certified for use in outpatient settings, broadening the options available for therapies such as outpatient antibiotic treatment. Private investment and a rise in specialty care are creating structured demand, even though the public sector's reach is still limited. Latin America’s market is defined by dual-speed adoption, with advanced private facilities driving innovation while public systems lag, which creates pockets of high specification demand amid broader access challenges.

Middle East and Africa Infusion Pump Market Analysis

The Middle East and Africa region is likely to expand in the global infusion pump market between 2025 and 2033. Deployment is concentrated in Gulf Cooperation Council hospital modernization projects, South African oncology centers, and donor-funded programs in Nigeria and Kenya targeting maternal and pediatric care. New mega hospitals in major urban centers are integrating smart pump technology into their core infrastructure to modernize patient care delivery. There is an observable rise in private healthcare reimbursement policies that support the use of portable infusion technology for outpatient treatments like chemotherapy, encouraging care outside traditional hospital walls. Health ministries are actively deploying specialized infusion pumps to critical care areas, such as neonatal units, to improve outcomes for vulnerable patient populations. Governments are prioritizing human capital development by initiating specialized training programs for local technicians, ensuring effective long-term maintenance and operation of medical equipment fleets in public hospitals. Limited overall market penetration is being addressed through strategic investments in flagship locations and specialized disease programs, which are serving as anchor points for future growth. The region’s trajectory is donor and policy-driven, where global health partnerships and national prestige projects override pure market forces to establish foundational clinical infrastructure.

COMPETITIVE LANDSCAPE

The gasoline fuel additives market is fiercely contested among multinational chemical corporations, specialty formulators, and regional blenders, each vying for dominance through technological differentiation, regulatory compliance, and supply chain agility. Competition centers on performance validation under evolving engine architectures, particularly turbocharged gasoline direct injection systems, where deposit control and octane retention are paramount. Regulatory fragmentation across jurisdictions forces players to maintain parallel product portfolios, increasing R&D and certification costs. Strategic acquisitions of niche additive developers are common, enabling rapid entry into high-growth segments such as biofuel stabilizers or low-sulfur detergent packages. Price competition is tempered by long-term contracts with refiners and OEMs, where technical service and reliability outweigh cost. Innovation cycles are accelerating as electrification pressures compel additive makers to demonstrate tangible fuel economy and emission benefits. Collaborative development with automotive manufacturers shapes next-generation formulations aligned with hybrid engine requirements and carbon intensity scoring. Market leadership is determined not by volume but by technical credibility and regulatory foresight.

KEY MARKET PLAYERS

The leading companies operating in the global infusion pump market include:

- Terumo Corporation

- Avanos Medical, Inc.

- Nipro Corporation

- Insulet Corporation

- Tandem Diabetes Care, Inc.

- JMS Co., Ltd.

- Roche Diagnostics

- Zyno Medical

- Teleflex, Inc.

- Mindray Medical International Limited

- Micrel Medical Devices S.A.

- Ypsomed Holding AG

- Becton, Dickinson and Company

- Braun Melsungen AG

- Baxter International Inc.

- Fresenius Kabi

- ICU Medical, Inc.

- Smiths Medical

- Medtronic PLC

- Moog Inc.

TOP PLAYERS IN THE MARKET

- Becton Dickinson is a global leader in smart infusion systems, delivering integrated platforms that combine volumetric, syringe, and ambulatory pumps with interoperable software for hospital-wide medication safety and workflow optimization. The company’s Alaris and Sapphire platforms dominate acute care settings through seamless EHR integration and comprehensive drug libraries. It also introduced predictive occlusion detection algorithms using machine learning to alert clinicians before flow interruption occurs. These innovations reinforce BD’s position as the central nervous system of hospital infusion safety and efficiency.

- ICU Medical specializes in high acuity infusion therapy, offering precision pumps for oncology, critical care, and anesthesia with advanced cybersecurity and dose error reduction capabilities. The company’s Plum and LifeCare platforms are certified for use in over 90 countries, with particular strength in chemotherapy and vasoactive drug delivery. It also partnered with major cancer centers to co-develop oncology-specific smart pump libraries with dynamic dose capping based on body surface area. By embedding clinical intelligence and cyber resilience, ICU Medical ensures its systems remain indispensable in high-risk therapeutic environments.

- Moog Inc. is a pioneer in ambulatory and home infusion technology, serving oncology, immunology, and chronic disease patients with wearable, connected pumps designed for non-clinical environments. The company’s ambIT and CADD legacy platforms are widely adopted for chemotherapy, antibiotics, and pain management outside hospitals. It also launched a caregiver mobile application enabling real-time dose confirmation and low battery notifications. Through human-centered design and remote care enablement, Moog empowers patients to safely manage complex therapies at home, reducing hospital burden and improving quality of life.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Leading manufacturers embed artificial intelligence for predictive occlusion and dosing anomaly detection to preempt adverse events before they occur. They develop universal interoperability engines enabling bidirectional data exchange with all major electronic health record and pharmacy information systems. Companies pursue regulatory certification for cybersecurity resilience, including encrypted firmware and zero-trust architectures to prevent remote manipulation. Partnerships with specialty care centers co-create disease-specific drug libraries with dynamic dosing limits based on patient parameters. Voice-guided interfaces and caregiver mobile applications enhance usability in home and ambulatory settings. Gravimetric and air bubble detection sensors are integrated to meet global safety mandates. Training academies for biomedical technicians ensure long-term device reliability in low-resource settings. Remote monitoring platforms enable real-time clinician oversight of home infusion patients. Modular pump architectures allow field upgrades without full system replacement. Companies offer subscription-based consumables and maintenance to ensure recurring revenue and clinical compliance.

MARKET SEGMENTATION

This market research report on the global insulin pump market has been segmented and sub-segmented based on type, product, application, end-user, and region.

By Type

- Accessories and Consumables

- Devices

By Product

- Volumetric infusion pumps

- Insulin infusion pumps

- Enteral infusion pumps

- Ambulatory infusion pumps

- Syringe infusion pumps

- Patient-controlled analgesia (PCA) pumps

- Implantable infusion pumps

By Application

- Chemotherapy/Oncology

- Diabetes

- Gastroenterology

- Analgesia/pain management

- Pediatrics/neonatology

- Hematology

- Other applications

By End-User

- Hospitals

- Home care settings

- Ambulatory care settings

- Academic and research institutes

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- The Middle East and Africa

Frequently Asked Questions

1. What is the global infusion pump market?

The global infusion pump market involves medical devices that deliver precise medication doses intravenously for various therapies in hospitals and homecare settings

2. What drives growth in the global infusion pump market?

Growth is fueled by rising chronic diseases, technological advances in smart pumps, increasing home healthcare, and demand for precise drug delivery systems worldwide

3. Which types of infusion pumps are common in the global infusion pump market?

Types include volumetric, syringe, ambulatory, implantable, and insulin pumps, catering to different medical needs and care settings in the global infusion pump market

4. How do smart infusion pumps impact the global infusion pump market?

Smart pumps enhance dosing accuracy, safety, and data integration, reducing medication errors and boosting demand in the global infusion pump market

5. Who are major players in the global infusion pump market?

Leading companies include Baxter, Becton Dickinson, ICU Medical, Medtronic, and Smiths Medical driving innovation in the global infusion pump market

6. What applications use infusion pumps in the global infusion pump market?

Applications include oncology, diabetes, pain management, nutrition therapy, and critical care in diverse healthcare environments globally

7. How does home healthcare affect the global infusion pump market?

Growth in homecare boosts demand for portable, user-friendly infusion pumps in the global infusion pump market for chronic and outpatient therapy

8. What are the challenges in the global infusion pump market?

High device costs, regulatory hurdles, and device malfunctions challenge expansion in the global infusion pump market

9. How is technology advancing the global infusion pump market?

Integration with electronic health records, wireless features, closed-loop insulin pumps, and digital monitoring shape the evolving global infusion pump market

10. What safety features are essential in the global infusion pump market?

Features like dose error reduction, occlusion alerts, air bubble detection, and alarm systems ensure patient safety in the global infusion pump market

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com