Latin America Energy Drinks Market Research Report - Segmented Based on Type, Packaging, and By Country (Brazil, Argentina, Chile and Rest of Latin America) - Industry Analysis on Size, Share, Trends & Growth Forecast (2026 to 2034)

Latin America Energy Drinks Market Report Summary

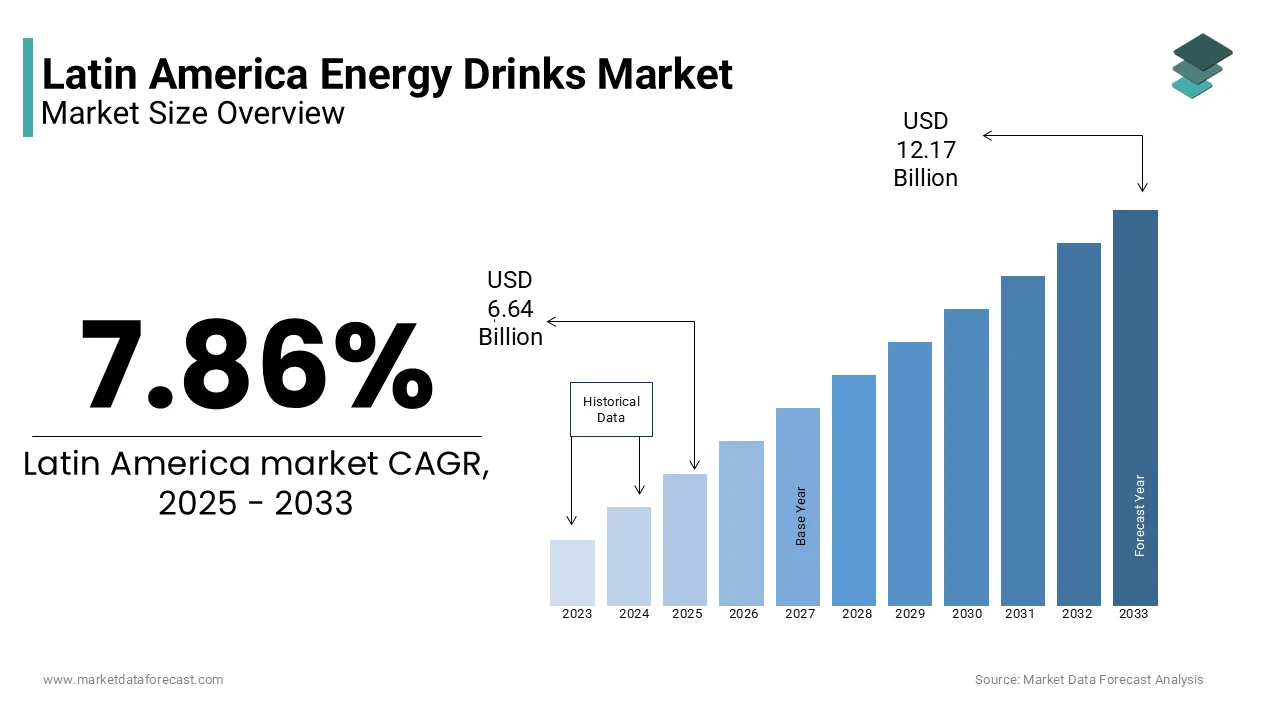

The Latin America energy drinks market was valued at USD 6.64 billion in 2025, is estimated to reach USD 7.16 billion in 2026, and is projected to reach USD 13.12 billion by 2034, growing at a CAGR of 7.86% during the forecast period. Market growth is driven by increasing demand for functional beverages, rising urbanization, and growing consumer preference for energy boosting drinks. Energy drinks are widely consumed for improved alertness, performance, and convenience. The expansion of fitness culture and busy lifestyles is further supporting steady market growth across Latin America.

Key Market Trends

- Rising demand for functional and performance enhancing beverages is driving market growth.

- Increasing urbanization and fast paced lifestyles are boosting consumption.

- Growing preference for convenient ready to drink beverages is supporting market expansion.

- Expansion of retail and distribution networks is improving product availability.

- Innovation in flavors and formulations is influencing consumer preferences.

Segmental Insights

- Based on type, the hypertonic energy drinks segment led the Latin America energy drinks market in 2025. This dominance is attributed to their effectiveness in replenishing energy and electrolytes.

- Based on ingredient type, the additives segment held a dominant share of the Latin America energy drinks market in 2025, driven by the inclusion of caffeine, vitamins, and other functional ingredients.

- Based on packaging, the cans segment held the majority share of the Latin America energy drinks market in 2025, supported by convenience, portability, and longer shelf life.

Regional Insights

- The Latin America energy drinks market is experiencing strong growth across key countries, supported by rising consumption and lifestyle changes.

- Brazil was the largest contributor, accounting for 40.1% of the Latin America energy drinks market share in 2025, driven by large consumer base, strong demand for energy beverages, and expanding retail presence.

Competitive Landscape

The Latin America energy drinks market is highly competitive, with key players focusing on product innovation, branding, and expansion of distribution networks to strengthen their market position. Companies are investing in new product launches, marketing strategies, and regional expansion. Prominent players in the Latin America energy drinks market include Red Bull, Monster Beverage Corporation, Rockstar Inc., Coca Cola, PepsiCo, Arizona Beverage Company, National Beverage Corp, Dr Pepper Snapple Group, and Living Essentials.

Latin America Energy Drinks Market Size

The Latin America energy drinks market size was valued at USD 6.64 billion in 2025, and the market size is estimated to reach USD 13.12 billion in 2034 from USD 7.16 billion in 2026. The market is growing at a CAGR of 7.86%.

Energy drinks are a category of non-alcoholic beverages marketed to increase mental alertness and physical performance. These functional beverages typically contain stimulants such as caffeine taurine guarana and B vitamins designed to enhance mental alertness and physical endurance. The market definition encompasses traditional carbonated energy drinks as well as emerging natural and organic variants that cater to evolving health consciousness among consumers. According to the International Labour Organization the average working hours in several Latin American countries exceed 45 hours per week which is higher than the OECD average creating a substantial demand for products that sustain energy levels throughout extended shifts. This labor dynamic is particularly evident in major economies like Brazil and Mexico where the service and industrial sectors rely heavily on sustained productivity. As per the Pan American Health Organization the prevalence of obesity and diabetes in the region has prompted regulatory scrutiny on sugary beverages leading to significant reforms in product formulation and labeling. The cultural integration of energy drinks into nightlife sports and study routines further cements their position in daily consumption habits. Recent trends indicate a shift towards premiumization with consumers seeking brands that offer unique flavors and ethical sourcing. The market operates within a complex regulatory environment where taxation and health warnings vary significantly across borders influencing both production strategies and consumer behavior. This sector reflects a blend of traditional consumption patterns and modern health awareness driving innovation and competition among global and local manufacturers.

MARKET DRIVERS

Rapid Urbanization and Growth of the Informal Labor Sector

The rapid urbanization and the substantial size of the informal labor sector serve as primary drivers for the Latin America Energy Drinks Market. This creates a large demographic of workers who require affordable and accessible energy solutions. As millions of individuals migrate to urban centers in countries like Colombia Peru and Argentina they often engage in informal employment such as street vending transportation services and casual labor which demands long hours and physical stamina. According to the Economic Commission for Latin America and the Caribbean approximately 50 percent of the employed population in the region works in the informal sector lacking fixed schedules and benefits. This workforce relies on inexpensive and readily available stimulants to maintain productivity during irregular and extended workdays. Data from the World Bank and UN indicates that urban populations in Latin America, already exceeding 80%, are projected to reach approximately 86% to 90% by 2050. The accessibility of these products through extensive distribution networks ensures that even low income consumers can afford them. The cultural normalization of consuming energy drinks as a substitute for meals or coffee further drives volume sales. Manufacturers leverage this by offering small single serve packages that fit tight budgets. This structural economic reality ensures a consistent and growing consumer base for energy beverages across the region.

Strong Cultural Association with Sports and Nightlife Activities

Strong cultural associations with sports and nightlife activities significantly propel the Latin America energy drinks market. This growth occurs as consumers weave these products into the fabric of their daily recreation. Latin America has a vibrant culture of football dancing and social gatherings where energy drinks are often consumed to enhance endurance and enjoyment. Research indicates that these fans are a primary target for energy drink brands like Powerade, which maintain major sponsorships with the federation. A study indicates that the nightlife economy in major cities like São Paulo Buenos Aires and Mexico City contributes significantly to local GDP with bars and clubs serving as key distribution channels for energy beverages. The marketing strategies of major brands heavily emphasize sponsorship of music festivals sporting events and extreme sports aligning the product with youth culture and vitality. The psychological association between energy drinks and social confidence drives habitual purchase among young adults. Additionally the rise of fitness culture in urban areas has led to increased consumption of energy drinks pre workout. Brands collaborate with influencers and athletes to reinforce this lifestyle connection. This deep embeddedness in social and recreational contexts ensures robust demand regardless of economic fluctuations. The emotional appeal of these beverages as enhancers of fun and performance sustains their popularity.

MARKET RESTRAINTS

Stringent Regulatory Taxes and Sugar Content Restrictions

Stringent regulatory taxes and sugar content restrictions act as major restraints for the Latin America Energy Drinks Market. This increases production costs and alters consumer purchasing behavior. Several countries in the region have implemented excise taxes on sugary beverages to combat rising rates of obesity and diabetes. According to the Pan American Health Organization (PAHO), Mexico was the first country in the region to implement a comprehensive excise tax on sugary drinks in 2014, followed by Chile, Barbados, and others. A study published in Health Affairs shows that the introduction of a one peso per liter tax on sugary beverages in Mexico led to a 7.6 percent average decline in purchases over the first two years (2014–2015). These fiscal measures directly impact the affordability of energy drinks which are often high in sugar. As per the World Bank, while health taxes can be regressive, low-income consumers are often more price-responsive, leading to greater health gains through reduced consumption of taxed beverages. Manufacturers face pressure to reformulate products to lower sugar content which can alter taste profiles and alienate traditional consumers. The complexity of varying regulations across different countries complicates supply chain management and marketing strategies for multinational brands. Compliance with strict labeling requirements such as warning labels in Chile and Uruguay further discourages impulse purchases. These regulatory headwinds increase operational costs and limit market growth. The uncertainty regarding future tax hikes creates a challenging business environment. This regulatory landscape forces companies to innovate rapidly while managing margin pressures.

Growing Health Consciousness and Preference for Natural Alternatives

Growing health consciousness and a preference for natural alternatives are creating significant barriers for the Latin American energy drinks market. Consumers are increasingly shifting away from synthetic ingredients in favor of healthier beverage options. Modern consumers are increasingly aware of the potential negative effects of artificial additives preservatives and high levels of refined sugar found in traditional energy drinks. According to a survey, a notable portion of consumers in Brazil and Argentina actively try to reduce their intake of artificial ingredients in their diet. This trend is particularly strong among millennials and Gen Z who prioritize wellness and clean label products. The Global Wellness Institute indicates that the global wellness market is projected to grow at an average annual rate of 7.6 percent through 2029. The rise of functional waters herbal teas and coconut water offers competition by providing mild energy boosts without the jittery side effects associated with high caffeine intake. Consumers are also scrutinizing the source of caffeine preferring plant based options like guarana and yerba mate over synthetic caffeine. This shift in perception challenges the core value proposition of traditional energy drinks which are often viewed as unhealthy. Manufacturers face the challenge of reformulating products to meet these new expectations while maintaining taste and efficacy. The higher cost of natural ingredients can also make these alternatives less accessible to price sensitive consumers. This cultural shift towards holistic health limits the growth potential of conventional energy drinks.

MARKET OPPORTUNITIES

Expansion into Rural and Semi Urban Markets

The proliferation into rural and semi-urban landscapes offers a significant opportunity for the Latin American energy drinks market. This is because infrastructure improvements and rising disposable incomes are broadening the consumer base beyond major cities. Historically energy drink consumption was concentrated in metropolitan areas but improved distribution networks are making these products accessible to smaller towns and villages. According to the Inter American Development Bank investment in rural infrastructure has improved connectivity allowing for more efficient logistics and supply chain penetration. The World Bank indicates that rural household incomes for participants in specific programs like "Productive Alliances" in Colombia have seen a total increase of 22 percent. Energy drink manufacturers are adapting their strategies by introducing smaller affordable pack sizes that cater to price sensitive consumers in these regions. The aspirational value of global brands also drives trial among younger demographics in semi urban areas who emulate urban lifestyles. Digital marketing and mobile commerce platforms are playing a crucial role in reaching these dispersed populations. Localized marketing campaigns that highlight affordability and energy benefits for agricultural and manual labor workers can further drive adoption. The untapped potential in these markets offers significant volume growth opportunities for established players. By focusing on accessibility and affordability brands can establish early loyalty in emerging consumer segments. This geographic expansion diversifies revenue streams and reduces dependence on saturated urban markets.

Innovation in Plant Based and Organic Energy Formulations

The innovation in plant based and organic energy formulations provides a promising prospect for the Latin America Energy Drinks Market. This aligns with the growing demand for clean label and sustainable products. Consumers are increasingly seeking energy solutions that derive from natural sources such as guarana yerba mate green tea and fruit extracts rather than synthetic chemicals. According to research, the market for organic soft drinks in Latin America is projected to grow at a compound annual growth rate of approximately 12 percent from 2023 to 2030, driven by health-conscious consumer segments. Brands that introduce organic certified energy drinks can capture this premium segment by offering transparency and purity. This trend is supported by the rich biodiversity of Latin America which provides access to unique local ingredients like acai cupuacu and camu camu. Manufacturers can leverage these indigenous ingredients to create differentiated products that resonate with local tastes and cultural heritage. The use of sustainable sourcing practices also appeals to environmentally conscious consumers who value ethical production. Partnerships with local farmers and suppliers can enhance brand storytelling and community engagement. The development of low calorie and sugar free variants using natural sweeteners like stevia and monk fruit further expands the addressable market. This innovation pathway allows brands to position themselves as health partners rather than just stimulant providers. By embracing natural formulations companies can overcome health related reservations and attract a broader demographic.

MARKET CHALLENGES

Volatility in Raw Material Prices and Currency Fluctuations

Volatility in raw material prices and currency fluctuations challenge the growth of the Latin America Energy Drinks Market. This affects production costs and profit margins. Key ingredients such as sugar caffeine aluminum for cans and plastic for bottles are subject to global commodity price fluctuations which can impact profitability. According to the Food and Agriculture Organization, global sugar prices experienced a 13.2 percent decrease in 2024, as larger-than-expected production in Brazil and improved prospects in Thailand offset earlier weather-related supply concerns. This cost inflation forces manufacturers to either absorb the losses or pass them on to consumers potentially reducing demand. Data from the International Monetary Fund indicates that currency volatility in countries like Argentina and Turkey has severely impacted import costs for packaging materials and equipment. As per the Aluminum Association prices for aluminum used in canning have remained volatile impacting the packaging costs for beverage companies. The reliance on imported ingredients such as specific flavorings or additives adds another layer of complexity and risk. Currency devaluation in key markets reduces the purchasing power of consumers making premium products less affordable. Manufacturers must invest in hedging strategies and diversified sourcing to mitigate these risks but this adds to operational complexity. Small and medium sized enterprises are particularly vulnerable to these shocks as they lack the bargaining power of larger players. The unpredictability of input costs makes long term planning difficult and can lead to inconsistent product quality or availability. This economic instability tests the resilience of market participants and requires agile management responses.

Counterfeit Products and Brand Imitation in Emerging Markets

Counterfeit products and brand imitation remain a serious hurdle for the Latin America Energy Drinks Market. This erodes brand equity and poses safety risks to consumers. In many emerging markets across the region weak intellectual property enforcement allows counterfeiters to produce and distribute fake energy drinks that mimic popular brands. According to the OECD Latin America is one of the regions most affected by trademark infringement in the food and beverage sector. These counterfeit products often contain unsafe levels of caffeine unlisted ingredients or contaminants that can harm consumers and damage the reputation of legitimate brands. Legitimate manufacturers must invest heavily in anti counterfeiting technologies such as holographic labels QR codes and blockchain tracking to verify authenticity. However these measures add to production costs and may not be fully effective against sophisticated counterfeiters. The presence of cheap imitations also creates unfair price competition forcing genuine brands to lower prices or lose market share. Consumer education is necessary to help buyers identify genuine products but this requires sustained effort and resources. The legal framework in some countries lacks the rigor to prosecute offenders effectively. This persistent threat diverts resources from innovation and marketing to security and legal defense. It creates an uneven playing field where unethical operators gain market share through deception and low prices.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.86% |

| Segments Covered | By Type, Packaging, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Argentina, Chile and Rest of Latin America |

| Market Leaders Profiled | Red Bull, Monster Beverage Corporation, Rockstar Inc, Coca Cola, PepsiCo, Arizona Beverage Company, National Beverage Corp, Dr.Pepper Snapple Group, Living Essentials |

SEGMENTAL ANALYSIS

By Type Insights

The hypertonic energy drinks segment led the Latin America Energy Drinks Market in 2025. This leading position of the segment is attributed to its high concentration of carbohydrates and electrolytes which provide sustained energy release essential for the region's active workforce and sports enthusiasts. These beverages are particularly favored by individuals engaged in prolonged physical activities such as football manual labor and endurance sports where immediate spikes in energy are less desirable than sustained stamina. The dominance of hypertonic energy drinks is primarily driven by their formulation which contains a higher concentration of solutes than human blood allowing for a slow and steady release of energy over extended periods. This characteristic makes them ideal for individuals engaged in prolonged physical activities such as marathon running cycling or manual labor where immediate spikes in energy are less desirable than sustained stamina. In the Latin America region where outdoor sports and physically demanding jobs are prevalent the demand for such functional benefits is substantial. The ability of these drinks to serve dual purposes of hydration and fueling enhances their value proposition. Manufacturers often fortify these drinks with B vitamins and taurine to further enhance metabolic efficiency. The cultural acceptance of sweet beverages in many Latin American countries also supports the popularity of high sugar content formulations. This alignment with physiological needs and local taste preferences ensures the continued leadership of the hypertonic segment. The strong preference for hypertonic energy drinks among professional athletes and manual laborers significantly contributes to their market leadership in the Latin America region. As the fitness industry expands across major cities in Brazil Mexico and Chile there is a growing cohort of consumers who prioritize performance optimization through specialized nutrition. Professional sports leagues particularly football and rugby frequently partner with hypertonic beverage brands for official hydration status enhancing brand visibility and credibility. The scientific backing behind hypertonic formulations appeals to educated consumers who seek evidence based solutions for their fitness goals. Brands leverage endorsements from famous athletes to reinforce the association between their products and peak performance. The availability of these drinks in gyms sports clubs and health food stores further facilitates access. This targeted marketing and product efficacy solidify the position of hypertonic drinks as the preferred choice for serious athletes and active individuals.

The isotonic segment is likely to experience the fastest CAGR of 8.2% from 2026 to 2034 due to its balanced formulation that matches the body’s natural fluid levels facilitating rapid absorption and hydration. This segment appeals to a broader audience including casual exercisers and office workers seeking quick refreshment without the heaviness of hypertonic drinks. The rapid growth of the isotonic segment is also fueled by its ability to provide quick hydration without causing gastrointestinal distress making it suitable for a wide range of activities and consumer groups. Isotonic drinks have similar osmotic pressure to body fluids allowing for efficient absorption of water and electrolytes. The versatility appeals to the growing number of casual fitness enthusiasts in urban Latin America who engage in activities like jogging yoga and team sports. Also, the lower sugar content compared to hypertonic drinks aligns with increasing health consciousness among consumers who want to avoid excessive calorie intake. Manufacturers are innovating with natural electrolytes from coconut water and fruit extracts to enhance appeal. The convenience of ready to drink formats supports on the go consumption. This combination of scientific efficacy and lifestyle compatibility drives robust expansion in the isotonic segment. The expansion of isotonic energy drinks into corporate and everyday consumption contexts significantly accelerates their growth as consumers seek healthy alternatives to sugary sodas and coffee. Office workers and students increasingly consume isotonic beverages to maintain focus and hydration during long hours of mental work. The mild flavor profile of isotonic drinks makes them palatable for frequent consumption unlike stronger stimulant based energy drinks. Brands are marketing these products as lifestyle beverages rather than just sports supplements broadening their appeal. Retailers are placing isotonic drinks in mainstream beverage aisles alongside water and juices increasing visibility. The trend towards preventive health and wellness encourages regular hydration as a habit. This shift in usage occasion from purely athletic to general well being drives sustained growth in the isotonic segment.

By Ingredient Type Insights

The additives segment dominated the Latin America Energy Drinks Market in 2025. This dominance of the segment is driven by the essential role of stimulants and functional compounds in delivering the promised energy boost and mental alertness. They contain the primary energizing elements, including B vitamins and caffeine, that characterize the segment. Consumers primarily purchase energy drinks for these specific active ingredients which provide the desired physiological effects. Caffeine remains the primary active ingredient in most energy drinks due to its proven efficacy in reducing fatigue and improving concentration. Taurine an amino acid commonly found in energy drinks is believed to support cardiovascular function and muscle performance. The synergy between these additives creates a potent effect that appeals to students professionals and drivers. Manufacturers invest heavily in sourcing high quality additives to ensure consistent potency and safety. The regulatory approval of these ingredients in major markets like Brazil and Mexico facilitates their widespread use. Consumer awareness of the benefits of B vitamins for energy metabolism further supports demand. This reliance on specific functional ingredients ensures that additives remain the core value driver in the market. The strong consumer demand for enhanced performance and focus significantly propels the additives segment as users seek tangible benefits from their beverage choices. In competitive academic and professional environments in countries like Brazil and Chile energy drinks are viewed as tools for gaining an edge. The inclusion of nootropics such as ginseng and guarana in premium formulations appeals to those seeking mental clarity. The marketing narrative around additives emphasizes productivity and efficiency resonating with ambitious demographics. Brands collaborate with esports teams and tech companies to reinforce this positioning. The perceived effectiveness of these ingredients drives repeat purchases and brand loyalty. Consumers are willing to pay a premium for formulations with verified ingredient profiles. This demand for performance enhancement sustains the leadership of the additives segment.

The water segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 6.5% over the forecast period owing to the rising popularity of hydrated energy formulations and clean label trends. Consumers are increasingly seeking lighter healthier options that provide energy without heavy synthetic loads. The swift growth of the water segment is also supported by the emergence of hydration focused energy beverages that combine the benefits of water with mild stimulants for a balanced boost. These products appeal to health conscious consumers who want to avoid the high sugar and artificial ingredient content of traditional energy drinks. Energy water products often use natural caffeine from green tea or coffee cherry extract appealing to clean label advocates. The light and refreshing nature of these drinks makes them suitable for all day consumption. Brands are leveraging the purity of water as a selling point emphasizing zero calories and natural sourcing. The convenience of single serve bottles supports on the go lifestyles. This trend towards lighter functional beverages drives significant expansion in the water segment. The preference for natural and clean label ingredients significantly accelerates the growth of the water segment as consumers reject artificial additives in favor of wholesome options. Modern shoppers scrutinize labels for synthetic colors preservatives and sweeteners driving demand for transparent formulations. Energy waters often feature organic certifications and non GMO claims which resonate with environmentally and health conscious buyers. The use of spring or mineral water as a base enhances the premium perception of these products. Marketing campaigns highlight the purity and simplicity of the ingredients appealing to wellness oriented demographics. The alignment with global clean label trends ensures sustained growth. This shift in consumer values positions water based energy drinks as a viable and growing alternative in the market.

By Packaging Insights

The cans segment held the majority share of the Latin America Energy Drinks Market in 2025 because of its superior protection against light and oxygen which preserves flavor and potency along with their convenience and recyclability. Aluminum cans are the preferred packaging format for major brands and consumers alike especially in warm climates. The dominance of cans is primarily driven by their ability to protect the contents from light and oxygen ensuring that the sensitive ingredients in energy drinks remain stable and effective. This preservation quality is crucial for maintaining the taste and efficacy of caffeine and other additives in the warm climates prevalent in much of Latin America. This environmental benefit appeals to eco conscious consumers. The compact size and lightweight nature of cans make them ideal for vending machines convenience stores and outdoor activities. The iconic shape and branding potential of cans also enhance shelf appeal. Manufacturers benefit from efficient logistics and storage due to the stackable design. This combination of functional and environmental advantages ensures the continued leadership of cans. The strong brand identity associated with cans and their extensive presence in vending machines significantly contribute to their market leadership in Latin America. Major energy drink brands have built iconic visual identities around their can designs which are instantly recognizable to consumers. The tactile experience of holding a cold can enhances consumption satisfaction particularly in hot weather. Brands invest heavily in limited edition can designs to create collectibility and buzz. The standardization of can sizes simplifies inventory management for retailers. This widespread availability and strong brand presence solidify the position of cans as the primary packaging format.

The bottles segment is expected to exhibit a noteworthy CAGR of 7.5% between 2026 and 2034. This quick surge of the segment is credited to the demand for resealable larger volume formats and premium plastic innovations. Bottles offer convenience for on the go consumption and multiple sittings. The rapid growth of the bottles segment is fueled by consumer preference for resealable containers that allow for gradual consumption and larger volumes that offer better value. Unlike cans bottles can be closed and reopened making them suitable for long commutes or work sessions. The transparency of plastic bottles allows consumers to see the product color which can influence purchasing decisions. Manufacturers are introducing ergonomic designs that fit cup holders and bags enhancing convenience. The ability to print detailed nutritional information and branding on labels adds marketing value. This functional versatility drives robust expansion in the bottle segment. The innovation in sustainable and premium plastic materials significantly accelerates the growth of the bottles segment as brands address environmental concerns while enhancing aesthetic appeal. Companies are adopting recycled PET rPET and bio based plastics to reduce their carbon footprint. The improved clarity and strength of new plastic technologies enhance product presentation. Brands leverage sustainability credentials in marketing to attract conscious buyers. Regulatory pressures to reduce virgin plastic use also drive adoption of recycled materials. This combination of environmental responsibility and premium aesthetics drives sustained growth in the bottle segment.

REGIONAL ANALYSIS

Brazil Snack Product Market Analysis

Brazil was the top performer in the Latin America Energy Drinks Market and accounted for a 40.1% share in 2025. This supremacy of the segment is driven by a large population vibrant youth culture and strong sports heritage. The country is the largest consumer of energy drinks in the region. Also, the Brazilian market is characterized by high consumption rates driven by the popularity of football nightlife and a growing fitness culture. According to the Brazilian Institute of Geography and Statistics the urban population exceeds 85 percent creating a vast customer base for convenience beverages. The rise of the gig economy with millions of delivery drivers and ride share operators has significantly boosted demand for affordable energy solutions. The government’s health regulations require clear labeling of caffeine content which influences consumer choices. As per sources, premium and imported brands are gaining traction among middle class consumers in major cities like São Paulo and Rio de Janeiro. The strong presence of local brands competing on price ensures wide accessibility. The cultural affinity for social gatherings and parties drives weekend sales spikes. Retail expansion into smaller towns offers new growth opportunities. These factors collectively sustain Brazil’s leadership in the regional market.

Mexico Snack Product Market Analysis

Mexico was the second largest player in the Latin America Energy Drinks Market and captured a 25.7% share in 2025. This growth of the Mexican market is supported by proximity to the United States strong manufacturing capabilities and a young demographic. The country is a key production hub for global brands. Moreover, the Mexican market is distinguished by a high density of convenience stores and vending machines that provide 24 hour access to energy drinks. According to the National Institute of Statistics and Geography the youth population constitutes a large portion of the consumer base driving demand for trendy and energetic beverages. The implementation of sugar taxes has prompted manufacturers to reformulate products with lower sugar content and alternative sweeteners. According to Euromonitor International, while health and wellness trends are shaping the market, regular (full-sugar) energy drinks still lead sales and growth in Mexico. Research note that energy drinks are increasingly available in convenience stores and small local grocers (the leading channel), with growth fueled by intense competition and marketing efforts that link these drinks to social and high-energy occasions. The presence of major global brands ensures wide availability and competitive pricing. The cross border trade with the United States introduces new trends and products quickly. The strong manufacturing base supports efficient distribution. These structural and cultural factors maintain Mexico’s strong position in the regional market.

Argentina Snack Product Market Analysis

Argentina is expected to be the most lucrative region in the Latin America Energy Drinks Market due to a strong European influence on coffee and beverage culture and a resilient consumer base. The market is characterized by premium preferences despite economic volatility. In addition, the Argentine market is influenced by a sophisticated consumer base that values quality and brand reputation. Studies indicate that demand for premium energy drinks remains stable or resilient among higher income groups. The strong cafe culture complements the consumption of energy drinks as alternatives for socializing. Research indicates that imported brands hold a significant share due to perceived higher quality. The government’s economic policies affect import costs leading to local production by multinational companies. The youth demographic in Buenos Aires drives trends in flavors and packaging. Retailers focus on premium placements in supermarkets and specialty stores. These dynamics position Argentina as a key market for premium and innovative products.

Chile Snack Product Market Analysis

Chile is moving ahead steadfastly in the Latin America Energy Drinks Market owing to high health consciousness strict regulatory frameworks and a strong outdoor sports culture. The market focuses on natural and functional products. Also, the Chilean market is characterized by informed consumers who prioritize natural ingredients and low sugar content. According to the Ministry of Health Chile implemented strict front of pack labeling laws which have influenced product formulation and consumer choices. The strong participation in outdoor sports such as hiking and skiing drives demand for performance oriented beverages. Research indicates that sales of organic and natural energy drinks grew by approximately 7–10 percent in 2024 as consumers shifted toward healthier alternatives. The high disposable income allows for premium product adoption. Retailers emphasize sustainability and ethical sourcing. The small but affluent population supports niche and specialized products. These factors sustain Chile’s stable and quality focused market position.

COMPETITIVE LANDSCAPE

The competition in the Europe snack product market is intense and characterized by the presence of established multinational corporations alongside emerging artisanal brands. Major players leverage their extensive distribution networks and strong brand recognition to maintain dominance while smaller competitors focus on niche segments such as organic gluten free or vegan options. Innovation serves as a key differentiator with companies continuously launching new flavors and healthier formulations to attract health conscious consumers. Price competition remains significant particularly in the mass market segment where private label products from major retailers pose a substantial threat to branded items. Sustainability has become a critical competitive factor as consumers increasingly prefer brands with transparent and ethical supply chains. Regulatory pressures regarding sugar content and labeling further shape competitive dynamics forcing companies to reformulate products. Digital marketing and e commerce capabilities are essential for reaching broader audiences and enhancing customer engagement. The market sees frequent strategic alliances and acquisitions as firms seek to expand their portfolios and geographic reach. This dynamic environment requires constant adaptation and investment in technology and sustainability to sustain competitive advantage and meet evolving consumer demands effectively.

Key Market Players

Some of the key players in Latin America energy drinks market are

- Red Bull

- Monster Beverage Corporation

- Rockstar Inc.

- Coca Cola

- PepsiCo

- Arizona Beverage Company

- National Beverage Corp

- Dr Pepper Snapple Group

- Living Essentials

Top Players in the Market

- Red Bull GmbH maintains a dominant presence in the global energy drinks sector with significant influence in Latin America through aggressive marketing and event sponsorship. The company is renowned for linking its brand to extreme sports music and cultural festivals across the region. Red Bull recently expanded its distribution networks in rural areas of Brazil and Mexico to enhance accessibility. It continues to invest in digital platforms to engage younger consumers through interactive content. The corporation focuses on premium positioning and maintains strict quality control standards. Red Bull also introduces limited edition flavors tailored to local tastes such as tropical fruits. These actions reinforce its brand equity and ensure sustained relevance in diverse markets while driving global recognition and loyalty among active lifestyles.

- Monster Beverage Corporation is a key player in the global energy drinks market leveraging its extensive distribution network and diverse product portfolio. In Latin America the company has strengthened its position through strategic partnerships with local bottlers like Coca Cola FEMSA. Monster recently launched new variants featuring natural ingredients and lower sugar content to address health concerns in the region. The brand actively sponsors major esports tournaments and music festivals across Latin America to engage younger demographics. Monster also invests in innovative packaging solutions including recyclable cans and bottles. Its focus on variety allows it to cater to different consumer preferences from high performance to lifestyle oriented drinks. These initiatives enhance its competitive edge and expand its reach in emerging markets throughout the continent.

- The Coca Cola Company contributes significantly to the Latin America Energy Drinks Market through its Burn and Speed brands alongside its vast distribution infrastructure. The company leverages its established relationships with retailers to ensure widespread availability of its energy products. Coca Cola recently reformulated several energy drink lines to reduce sugar content complying with regional health regulations. It utilizes its robust logistics network to reach remote areas where competitors struggle to operate. The corporation invests in localized marketing campaigns that resonate with cultural traditions and social habits. Strategic acquisitions of local brands have further diversified its portfolio. These efforts enable Coca Cola to maintain a strong foothold in the competitive landscape by combining global brand power with local market insights and operational efficiency.

Top Strategies Used by the Key Market Participants

Key players in the Europe Snack Product Market primarily employ product innovation and premiumization strategies to differentiate their offerings. Companies invest heavily in research and development to create unique flavors and healthier formulations such as reduced sugar or organic variants. Sustainability initiatives form another core strategy with firms focusing on ethical sourcing of cocoa and eco friendly packaging solutions to meet regulatory standards and consumer expectations. Digital transformation is crucial as brands enhance their e commerce presence and utilize data analytics for personalized marketing. Strategic partnerships and collaborations with retailers ensure optimal shelf placement and visibility. Mergers and acquisitions allow companies to expand their portfolios and enter new niche segments. Brands also leverage influencer marketing and social media campaigns to engage younger demographics and build brand loyalty. These multifaceted approaches help participants navigate competitive pressures and adapt to evolving consumer preferences while maintaining profitability and market relevance in the dynamic European landscape.

MARKET SEGMENTATION

This research report on the Latin America energy drinks market is segmented and sub-segmented into the following categories

By Type

- Isotonic

- Hypotonic

- Hypertonic Energy Drinks

By Ingredient Type

- Water

- Additives

- Flavours

- Acidulants

By Packaging

- Bottles

- Cans

By Country

- Brazil

- Argentina

- Mexico

Frequently Asked Questions

1.What is the Latin America energy drinks market?

The Latin America energy drinks market refers to the industry focused on the production, distribution, and consumption of caffeinated and functional beverages designed to enhance energy, alertness, and physical performance across the region.

2.What factors are driving the growth of the Latin America energy drinks market?

Growth is driven by rising urbanization, increasing youth population, expanding fitness culture, growing demand for functional beverages, and aggressive marketing strategies by major brands.

3.Which countries are leading the Latin America energy drinks market?

Brazil and Mexico are leading markets due to their large consumer base, strong retail networks, and high consumption of functional and convenience beverages.

4.What are the common ingredients found in energy drinks?

Energy drinks typically contain caffeine, taurine, B vitamins, sugar or artificial sweeteners, guarana, ginseng, and other performance enhancing ingredients.

5.How is consumer preference evolving in the Latin America energy drinks market?

Consumers are increasingly seeking low sugar, sugar free, natural ingredient based, and plant derived energy drink options with added functional benefits.

6.What distribution channels dominate the market?

Supermarkets and hypermarkets, convenience stores, specialty beverage stores, and online retail platforms are the primary distribution channels in the region.

7.How does the fitness and sports culture influence demand?

The growing popularity of gyms, sports events, and active lifestyles has significantly boosted demand for energy drinks among young adults and athletes.

8.What challenges are affecting the Latin America energy drinks market?

Challenges include regulatory scrutiny over caffeine content, health concerns related to excessive consumption, price sensitivity, and competition from other functional beverages.

9.What role does branding and marketing play in market growth?

Strong branding, sponsorship of sports and music events, influencer marketing, and youth oriented campaigns play a crucial role in expanding market reach.

10.Who are the key players operating in the Latin America energy drinks market?

Major companies include Red Bull GmbH, Monster Beverage Corporation, PepsiCo Inc., The Coca Cola Company, and regional beverage manufacturers competing in the energy drink segment.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com