Latin America Industrial Dryers Market Size, Share, Growth, Trends, And Forecasts Report Segmented, By Type (Spray, Fluidized Bed, Rotary), Application (Pharmaceutical, Fertilizer, Food, Cement, Chemicals), By Product (Direct, Indirect, Specialty) And By Region (Brazil, Mexico, Chile, Argentina, Others), Industry Analysis From (2025 to 2033)

Latin America Industrial Dryers Market Size

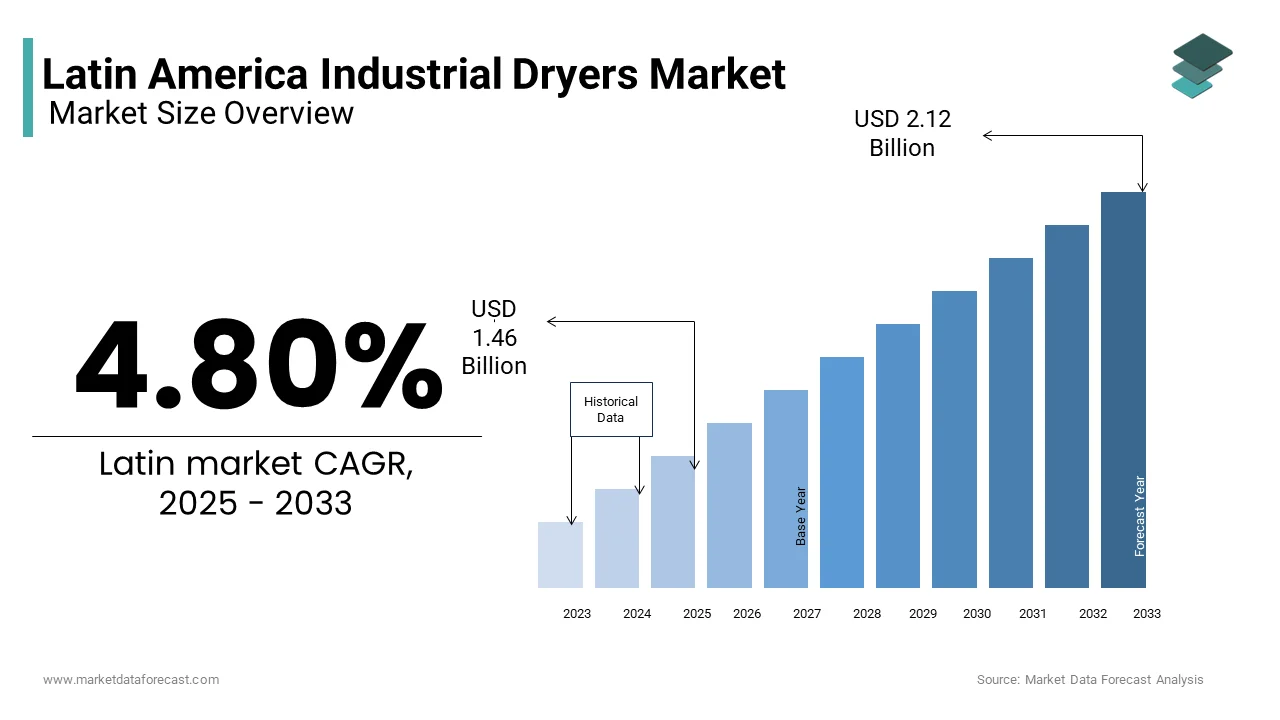

The Latin American industrial dryers market was valued at USD 1.39 billion in 2024 and is anticipated to reach USD 1.46 billion in 2025 from USD 2.12 billion by 2033, growing at a CAGR of 4.80% during the forecast period from 2025 to 2033.

The Latin American industrial dryers market involves a diverse range of drying technologies deployed across food processing, chemical manufacturing, pharmaceuticals, agriculture, and mineral extraction industries. These systems are essential for removing moisture from raw materials or end products, ensuring product stability, shelf life, and compliance with international quality standards. The market has seen steady development in recent years, driven by increasing industrialization and growing demand for processed goods across key economies such as Brazil, Mexico, Argentina, and Colombia.

Energy consumption patterns also play a pivotal role in shaping the market landscape. While this growth supports increased adoption of industrial dryers, it also highlights the importance of transitioning toward more sustainable drying methods.

Despite these promising trends, challenges related to economic volatility, limited access to financing, and uneven technological adoption continue to influence market expansion across different sub-regions.

MARKET DRIVERS

Expansion of the Agro-Processing Industry

One of the primary drivers of the Latin American industrial dryers market is the rapid expansion of the agro-processing industry, particularly in countries with strong agricultural output such as Brazil, Argentina, and Mexico.

As per the Inter-American Development Bank (IDB), investments in agro-industrial infrastructure have risen by over 6% annually since 2021, with drying technology playing a central role in preserving perishable crops and enhancing export readiness.

Latin America is a major exporter of agricultural commodities, including coffee, cocoa, grains, and fruits. However, post-harvest losses remain a persistent challenge. According to the Food and Agriculture Organization (FAO), a notable share of harvested fruits and vegetables in the region is lost due to inadequate storage and processing facilities. Industrial dryers offer an effective solution by reducing moisture content, extending shelf life, and improving transportability.

In response to this need, governments and private investors are increasingly funding modern drying facilities. For instance, in Peru, as per the Ministry of Agriculture and Irrigation, an increase in investment in drying and dehydration units for export-oriented produce is expected between 2020 and 2023. Similarly, Brazilian cooperatives have adopted spray and fluidized bed dryers to process dairy powders and tropical fruit pulps for both domestic and international markets.

This trend underscores the growing integration of industrial dryers into the agro-processing value chain, positioning them as a vital component of regional food security and trade competitiveness.

Growth in the Chemical and Pharmaceutical Sectors

Another significant driver of the Latin American industrial dryers market is the expanding chemical and pharmaceutical industries, which require precision drying equipment to maintain product consistency and regulatory compliance. Countries such as Brazil, Mexico, and Colombia have been investing heavily in local drug production and specialty chemical manufacturing to reduce import dependency and meet rising domestic demand.

According to the Brazilian Association of the Chemical Industry (ABIQUIM), the country’s chemical sector grew by 5.2% in 2023, with a particular emphasis on polymers, coatings, and agrochemicals—all of which require industrial drying at various stages of production. Rotary and flash dryers are extensively used in the dehydration of resins, pigments, and fertilizers, supporting downstream applications in agriculture and construction.

Simultaneously, the pharmaceutical industry is gaining momentum. According to the Mexican Health Department, domestic pharmaceutical output increased by 6.4% in 2023, driven by government incentives aimed at boosting generic drug manufacturing. Drying plays a crucial role in active pharmaceutical ingredient (API) formulation, tablet granulation, and lyophilization processes, where moisture control is paramount.

This trajectory reflects broader industrial diversification efforts and underscores the strategic importance of drying technology in high-value manufacturing sectors.

MARKET RESTRAINTS

High Capital and Operational Costs

One of the most pressing constraints affecting the Latin American industrial dryers market is the high initial capital required for acquiring advanced drying systems, along with elevated operational costs. Many small and medium-sized enterprises (SMEs) in the region lack access to sufficient financing and often operate under tight budgetary constraints, making it difficult to adopt modern, energy-efficient drying technologies.

According to the World Bank, less than 40% of SMEs in Latin America have access to formal credit, severely limiting their ability to invest in capital-intensive equipment. Besides, energy prices in the region remain relatively high compared to global averages. According to the International Energy Agency (IEA), industrial electricity prices in countries like Argentina and Ecuador exceed USD 0.13 per kWh, h—higher than the global average of USD 0.10 per kWh, further escalating the cost of operating industrial dryers.

Even in larger economies such as Brazil and Mexico, where industrial infrastructure is more developed, the payback period for high-efficiency dryers can extend beyond five years.

These financial barriers hinder the widespread integration of modern drying technologies, especially in rural and semi-industrialized zones where infrastructure limitations already pose operational challenges.

Limited Technical Expertise and After-Sales Support

Another critical limitation restraining the industrial dryers market in Latin America is the scarcity of technical expertise and inadequate after-sales service networks. The operation and maintenance of advanced drying systems require skilled personnel, which remains a challenge in many parts of the region.

According to UNESCO’s Institute for Statistics, only about 28% of tertiary graduates in Latin America specialize in science, technology, engineering, and mathematics (STEM) fields, contributing to a skills gap in industrial maintenance and automation. This shortage extends to specialized roles in process engineering, which are vital for optimizing dryer performance and ensuring system longevity.

Moreover, multinational dryer manufacturers often face logistical difficulties in providing timely support services across remote locations in South America. Like, delays in spare parts delivery and technician availability can lead to extended machine downtime, reducing return on investment for end-users.

In Mexico and Brazil, while there is better access to trained engineers, there remains a reliance on expatriate labor for complex technical tasks, increasing operational costs. Local workforce training programs remain underdeveloped, limiting the ability of indigenous firms to independently manage sophisticated drying equipment.

This lack of localized technical capacity continues to impede the effective deployment and maintenance of industrial dryers across the Latin American market.

MARKET OPPORTUNITY

Adoption of Renewable Energy for Sustainable Drying Solutions

The integration of renewable energy sources into industrial drying processes presents a compelling opportunity for the Latin American market. With abundant solar irradiation and increasing government focus on sustainability, the region is well-positioned to transition toward green drying technologies.

According to the International Renewable Energy Agency (IRENA), Latin America receives a high average of solar radiation, making solar-assisted drying systems highly viable. Countries such as Chile and Brazil have already made significant strides in harnessing solar power for industrial applications. Chile’s Atacama Desert hosts some of the world’s largest solar farms, enabling off-grid drying operations in remote agro-industrial settings.

Brazil has launched initiatives to promote clean energy projects, including solar-powered drying units in coffee and cassava processing plants. Similarly, in Colombia, the Ministry of Mines and Energy supports decentralized renewable energy projects that benefit small-scale food processors using industrial dryers.

As per a study conducted by the United Nations Industrial Development Organization (UNIDO), transitioning to solar-assisted drying systems could reduce energy costs by up to 40% in selected agro-processing applications across Latin America. This shift not only lowers operational expenses but also aligns with regional climate commitments under the Paris Agreement.

Increasing Demand for Processed Foods in Urban Centers

Urbanization trends in Latin America are driving a surge in demand for packaged and processed foods, presenting a lucrative opportunity for the industrial dryers market. As per the United Nations Department of Economic and Social Affairs (UN DESA), the urban population in Latin America is expected to reach over 650 million by 2030, representing nearly 85% of the total population. This demographic shift is reshaping consumer preferences toward convenience foods, requiring advanced drying technologies to ensure longer shelf life and enhanced food safety.

In cities such as São Paulo, Bogotá, and Mexico City, supermarkets and organized retail chains are expanding rapidly, increasing the need for standardized food processing. The Economic Commission for Latin America and the Caribbean (ECLAC) reports that packaged food sales in the region increased significantly between 2018 and 2023, outpacing overall GDP growth.

Dried fruits, instant noodles, powdered milk, and dehydrated spices are among the fastest-growing product categories, all of which rely heavily on industrial dryers during production. For example, in Argentina, where per capita dairy consumption has risen steadily, manufacturers are investing in spray drying systems to produce powdered milk efficiently.

Similarly, in Mexico, food import dependency has prompted local authorities to promote domestic food processing capabilities.

MARKET CHALLENGES

Inconsistent Power Supply and Infrastructure Deficits

An ongoing challenge in the Latin American industrial dryers market is the inconsistent power supply and underdeveloped infrastructure, particularly in rural and semi-urban areas. Industrial dryers, especially those used in large-scale operations, require stable and continuous energy inputs to function efficiently. However, frequent power outages and grid instability hinder consistent production cycles and increase maintenance costs.

According to the World Bank’s Enterprise Survey, a significant percentage of manufacturing firms in Latin America experience at least one power outage per month, leading to significant disruptions. In countries like Venezuela and Bolivia, unreliable electricity distribution forces many industries to rely on costly diesel generators, which escalate operational expenses and carbon footprint.

Even in more developed markets such as Brazil and Mexico, distribution inefficiencies persist. As reported by the Inter-American Development Bank (IDB), aging transmission infrastructure contributes to an average of 10% energy loss across the region, impacting industrial productivity.

Such infrastructural deficiencies deter foreign investment and slow down the adoption of automated drying systems. Manufacturers are hesitant to install high-capacity dryers without assurance of uninterrupted power supply, thereby stalling technological advancements in the sector.

Stringent Regulatory Compliance and Quality Standards

The enforcement of stringent regulatory requirements and evolving quality standards poses a significant challenge for manufacturers and users of industrial dryers in Latin America. As global trade expands and food safety regulations become more rigorous, local producers must align their drying processes with international benchmarks, adding complexity and cost to operations.

Similarly, in Mexico, the Federal Commission for the Protection against Sanitary Risk (COFEPRIS) enforces Good Manufacturing Practices (GMP) that apply to pharmaceutical and food-grade drying equipment. Meeting these evolving standards requires periodic audits, process modifications, and investment in compliant technologies.

According to a Deloitte white paper, compliance with these evolving standards has increased capital expenditure for small-scale processors, limiting their competitive edge. Furthermore, the lack of centralized regulatory bodies in some Andean nations leads to fragmented enforcement, complicating cross-border trade and standardization efforts.

Meeting these regulatory expectations demands continuous investment in compliant technologies and skilled oversight, challenging the scalability of industrial dryer adoption in Latin America.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.80% |

| Segments Covered | By Type, Application, Product, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | Brazil, Argentina, Chile, Mexico, Rest of Latin America, and Country |

| Market Leaders Profiled | ThyssenKrupp AG (Germany), Andritz AG (Austria), GEA Group (Germany), Metso Corporation (Finland), FLSmidth & Co. A/S (Denmark), Buhler Holding AG (Switzerland), ANIVI Ingeniería SA (Spain), Carrier Vibrating Equipment, Inc. (U.S.), COMESSA (France), and Mitchell Dryers Ltd. (U.K.), among others. |

SEGMENTAL ANALYSIS

By Type Insights

The Rotary Dryers segment held the largest market share, accounting for 36.3% of total revenue in 2024 in the Latin America industrial dryers market. This dominance is primarily attributed to their widespread use across bulk material processing industries such as mining, cement production, and chemical manufacturing—sectors that form a substantial part of the region’s industrial landscape.

One key driver behind the prominence of rotary dryers is their adaptability to high-volume operations. According to the Economic Commission for Latin America and the Caribbean (ECLAC), mineral extraction activities in countries like Chile and Peru have expanded at a significant annual rate since 2020, necessitating robust drying solutions for ores and concentrates. Rotary dryers are particularly suited for handling large quantities of materials with varying moisture content, making them ideal for such applications.

Another critical factor is cost-effectiveness in operation and maintenance. Unlike more complex systems, rotary dryers offer relatively straightforward mechanical designs that reduce downtime and repair costs.

Furthermore, in the cement industry, where raw materials must be dried before entering kilns, rotary dryers remain the preferred choice. These combined factors underscore why rotary dryers maintain a dominant position in the Latin American industrial dryers market.

The Fastest-growing segment in the Latin America industrial dryers market by type is the Fluidized Bed Dryers segment, projected to grow at a CAGR of 7.6%. This rapid expansion reflects growing demand for precision drying in sectors such as pharmaceuticals, food processing, and specialty chemicals, where uniform heat distribution and product integrity are crucial.

One of the primary growth drivers is the rising investment in the pharmaceutical industry, particularly in Brazil and Mexico. According to the National Health Surveillance Agency (ANVISA), domestic pharmaceutical production in Brazil increased by 6.7% in 2023, supported by government incentives aimed at reducing reliance on imports. Fluidized bed dryers are extensively used in API and tablet granulation processes due to their ability to provide controlled, gentle drying without compromising product quality.

Besides, the food processing industry's shift toward value-added products is fueling demand for fluidized bed technology. The United Nations Economic Commission for Latin America and the Caribbean (ECLAC) notes that packaged food sales in the region grew from 2018 to 2023, driven by urbanization and changing consumer habits. Fluidized bed dryers are widely employed in drying instant coffee, powdered milk, and dehydrated vegetables, aligning well with this trend.

Moreover, advancements in modular and compact fluidized bed dryer designs have made them increasingly accessible to small and mid-sized processors. Companies like Glatt and Hosokawa Micron have expanded their presence in Colombia and Argentina, offering tailored solutions that cater to local production needs.

With increasing regulatory emphasis on hygiene and efficiency, the fluidized bed dryers segment is poised for sustained growth across Latin America.

By Application Insights

Among the application segments, the Chemicals segment commanded the market, contributing 31% of total revenue in 2024. This dominance is primarily attributed to the expanding chemical manufacturing base in Brazil, Mexico, and Argentina, which rely heavily on industrial dryers for resin, polymer, and pigment production.

A major driver behind the chemicals segment’s leading position is the strategic diversification of economies away from oil dependency, particularly in Mexico and Brazil. Drying plays a crucial role in ensuring product consistency and reducing moisture content, especially in coatings, agrochemicals, and synthetic resins.

Another contributing factor is the increased production of polymers and specialty chemicals, which require precise drying conditions to maintain product stability.

Additionally, regional export ambitions are pushing manufacturers to adopt standardized drying methods to meet international quality benchmarks. These trends collectively underline the chemical application’s stronghold in the Latin American industrial dryers market.

The booming application segment in the Latin American industrial dryers market is the Pharmaceuticals segment, expected to expand at a CAGR of 8.3%. This accelerated growth is fueled by rising investments in drug manufacturing infrastructure and increasing demand for locally produced medicines, especially in response to public health challenges.

One of the key growth enablers is the expansion of domestic pharmaceutical production capacity, particularly in Brazil and Argentina. Drying plays a crucial role in the formulation of solid dosage forms, including tablets and capsules, where moisture control is essential for stability and efficacy.

In addition, the Pan American Health Organization (PAHO) has been advocating for regional self-sufficiency in healthcare, encouraging greater investment in compliant production facilities equipped with modern drying equipment. Regulatory bodies such as ANVISA and COFEPRIS are enforcing stricter Good Manufacturing Practice (GMP) standards, prompting pharmaceutical firms to upgrade their drying infrastructure.

Furthermore, global pharmaceutical companies are establishing partnerships with local firms to enhance production capabilities. For instance, Novartis and Sanofi have entered joint ventures in Brazil and Mexico, respectively, to develop cost-effective drug formulations tailored to regional health needs. These collaborations often include technology transfers involving fluidized bed and vacuum dryers.

By Product Insights

The Direct Dryers segment led the market, contributing approximately 41% of total market revenue in 2024. This dominance is primarily due to their widespread adoption in energy-intensive industries such as cement, minerals, and agro-processing, where direct contact between the drying medium and the product offers efficiency advantages.

One of the key reasons for the segment’s leadership is its cost-effectiveness and ease of integration in large-scale operations. Direct dryers typically utilize hot gases generated from combustion sources, making them highly suitable for industries requiring rapid evaporation of moisture.

Also, the agro-industrial sector in Latin America continues to rely heavily on direct dryers for processing commodities such as maize, cassava, and rice. Direct dryers, being relatively simple to operate and maintain, are favored in rural agro-processing hubs.

Moreover, in the mining industry, direct dryers are extensively used for dewatering and conditioning ores before transportation or refining. These factors collectively reinforce the dominant position of the Direct Dryers segment in the Latin American industrial dryers market.

The rapidly expanding product segment in the Latin American industrial dryers market is the Specialty Dryers segment, anticipated to grow at a CAGR of 9.5%. This segment includes freeze dryers, vacuum dryers, and microwave-assisted drying systems, which are gaining traction due to their ability to preserve product integrity and deliver superior drying performance in niche applications.

One of the primary growth drivers is the expansion of the pharmaceutical and biotechnology sectors, particularly in Brazil and Mexico. Specialty dryers play a crucial role in preserving heat-sensitive compounds during lyophilization and sterile processing.

Another contributing factor is the growing demand for premium food products such as freeze-dried fruits, instant soups, and functional ingredients.

Furthermore, the adoption of green drying technologies is accelerating in response to sustainability mandates. As per a report by the United Nations Industrial Development Organization (UNIDO), transitioning to energy-efficient specialty dryers can reduce carbon emissions in selected food and pharma applications, aligning with regional climate goals.

With increasing investment in R&D and supportive regulatory frameworks, the Specialty Dryers segment is positioned for robust growth across Latin America.

COUNTRY ANALYSIS

Brazil

Brazil had a leading position in the Latin American industrial dryers market, accounting for 28.4% of regional market revenue in 2024. This dominance is primarily driven by the country’s robust industrial base and strategic economic initiatives aimed at enhancing manufacturing competitiveness.

One of the key contributors to Brazil’s market strength is the rapid expansion of its chemical and petrochemical industries. Industrial dryers are integral to polymer, resin, and fertilizer manufacturing processes, where moisture removal is essential for product consistency and quality.

Also, the pharmaceutical sector is witnessing significant investment. Drying technologies such as fluidized bed and vacuum dryers are increasingly adopted in API manufacturing and tablet formulation to meet international quality standards.

Moreover, the agro-processing industry remains a major user of industrial dryers, particularly in dairy, coffee, and fruit dehydration. With ongoing industrialization and government-backed infrastructure projects, Brazil remains a pivotal market for industrial dryers in Latin America.

Mexico

Mexico ranks among the top contributors to the Latin American industrial dryers market, holding an estimated 22% market share in 2024. Its strong industrial base, coupled with ambitious economic diversification strategies, positions it as a key player in the regional market.

One of the primary drivers of Mexico’s industrial dryers market is the expansion of its chemical and pharmaceutical manufacturing sectors. Industrial dryers play a vital role in ensuring product purity and consistency in polymer and fine chemical production.

Additionally, the Mexican pharmaceutical industry is growing rapidly. Fluidized bed and freeze dryers are increasingly deployed to enhance product stability and shelf life.

Moreover, the food processing industry is expanding rapidly, particularly in Guadalajara and Monterrey, where organized food parks and export-oriented production units are emerging. With continued support for industrial innovation and foreign investment, Mexico remains a key growth engine for the Latin American industrial dryers market.

Argentina

Argentina occupies a notable position in the Latin American industrial dryers market. Despite economic fluctuations, the country maintains a strong industrial foundation, particularly in agro-processing and chemical manufacturing, which drives consistent demand for drying solutions.

One of the major contributors to Argentina’s market standing is the expansion of its agro-industrial sector, especially in grain and oilseed processing. Spray and rotary dryers are extensively used in flour mills and biodiesel production plants.

Moreover, the chemical industry is undergoing modernization, supported by government incentives to boost domestic production. Moreover, the pharmaceutical sector is gaining traction, with increased investments in local drug manufacturing. Despite macroeconomic challenges, Argentina remains a key player in the Latin American industrial dryers market due to its strong agricultural and industrial foundations.

Chile

Chile represents a significant and growing segment of the Latin American industrial dryers market. The country’s industrial development, particularly in mining and food processing, supports steady demand for drying equipment.

One of the main drivers of Chile’s market growth is the expansion of the mining industry, especially copper and lithium extraction. Rotary and flash dryers are extensively used in ore beneficiation and concentrate preparation, reinforcing demand for industrial drying solutions.

Additionally, the agro-food sector is evolving, with increasing exports of dried fruits, wines, and seafood. Spray and belt dryers are commonly used in juice concentration and snack production.

Moreover, the government is promoting sustainable drying technologies, particularly in remote areas with abundant solar energy potential. With its strong mining and agro-export industries, Chile remains a key contributor to the Latin American industrial dryers market.

Rest of Latin America

The Rest of Latin America category, encompassing countries such as Colombia, Peru, Ecuador, and Central American nations, contributed a smaller share of total revenue in the Latin America industrial dryers market in 2024. While individually, these economies may not dominate the market, collectively, they represent a growing base for industrial expansion and technological adoption.

One of the key drivers in this segment is the ongoing industrial development in Colombia, particularly in the agrochemical and pharmaceutical sectors. Industrial dryers play a crucial role in ensuring product stability and compliance with international standards. These industries require rotary and flash dryers for dehydration and product conditioning, driving steady demand for drying equipment.

Moreover, in smaller economies such as Guatemala and Costa Rica, the agro-processing sector is gaining traction. With improving infrastructure and industrial policy reforms, the "Rest of Latin America" segment is steadily emerging as a meaningful contributor to the regional industrial dryers market.

KEY MARKET PLAYERS

Some of the major players in the Industrial Dryers market are ThyssenKrupp AG (Germany), Andritz AG (Austria), GEA Group (Germany), Metso Corporation (Finland), FLSmidth & Co. A/S (Denmark), Buhler Holding AG (Switzerland), ANIVI Ingeniería SA (Spain), Carrier Vibrating Equipment, Inc. (U.S.), COMESSA (France), and Mitchell Dryers Ltd. (U.K.), among others. Are the market players that are dominating the Latin American industrial dryers market?.

Top Players in the Market

One of the leading players in the Latin American industrial dryers market is GEA Group, a Germany-based engineering company specializing in process technology across food, pharmaceuticals, and chemicals. The company has a strong global presence and offers a wide range of drying solutions, including spray, fluidized bed, and vacuum dryers. In Latin America, GEA is recognized for its customized systems that cater to local industries such as dairy processing, mineral extraction, and pharmaceutical manufacturing. Its emphasis on energy efficiency, automation, and sustainability makes it a preferred partner for large-scale industrial clients seeking reliable drying technologies.

Another major player is Bühler AG, a Swiss multinational known for its innovative solutions in food processing and advanced materials. Bühler plays a crucial role in supplying industrial dryers tailored to agricultural commodities, particularly in Latin American countries where grain and legume drying are essential for reducing post-harvest losses. The company’s integration of digital monitoring and precision drying techniques enhances performance and product quality. In Mexico and Brazil, Bühler supports the petrochemical and cement industries with robust rotary and flash drying systems, reinforcing its strategic position in the regional market.

Glatt GmbH, a German leader in fluid bed and spouted bed drying technologies, is another key participant shaping the Latin American industrial dryers landscape. With expertise in pharmaceutical, food, and chemical applications, Glatt delivers high-precision drying systems that ensure product consistency and compliance with international standards. The company’s expansion into emerging markets includes partnerships and localized support services aimed at improving accessibility for Latin American manufacturers. Glatt's commitment to innovation and sustainable processing aligns well with evolving industry demands, strengthening its foothold in the region.

Top Strategies Used by Key Market Participants

Key players in the Latin American industrial dryers market employ several strategies to strengthen their competitive edge. One major approach is strategic partnerships and collaborations with local distributors and engineering firms, which help global manufacturers better understand regional needs and streamline after-sales service. These alliances facilitate technology transfer and improve customer support networks across remote locations.

Another critical strategy is product customization and localization, where companies design drying solutions tailored to the specific requirements of Latin American industries. This includes adapting equipment for local raw materials, climatic conditions, and regulatory standards, thereby enhancing adoption among small and medium enterprises.

Lastly, expanding digital integration and after-sales service capabilities allows key players to differentiate themselves in a fragmented market. By offering predictive maintenance tools, remote diagnostics, and training programs, companies ensure long-term customer engagement and operational reliability, reinforcing their market positions.

COMPETITION OVERVIEW

The competition in the Latin American industrial dryers market is characterized by a mix of global leaders and regional players striving to meet diverse industrial needs. Multinational corporations dominate due to their technological expertise, extensive product portfolios, and established distribution networks. However, increasing demand from emerging economies has led to the rise of local manufacturers who offer cost-effective and simplified drying solutions tailored to small and medium-sized enterprises. These domestic players are gradually gaining traction by addressing gaps in affordability and after-sales support, especially in rural and semi-industrialized regions.

Market participants are focusing on differentiation through innovation, service excellence, and environmental sustainability. As industries across the region evolve, there is a growing emphasis on energy-efficient and digitally integrated drying systems. Companies are also investing in capacity-building initiatives, technical training, and localized service centers to enhance customer retention. Despite the dominance of global firms, the market remains dynamic, with opportunities for both international and regional players willing to adapt to the unique challenges and opportunities present across Latin American countries.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, GEA Group launched a dedicated regional service hub in São Paulo to provide enhanced technical support and maintenance solutions for its industrial dryer customers across Brazil and neighboring countries, aiming to improve response times and strengthen after-sales service delivery.

- In June 2024, Bühler AG partnered with an Argentine agro-processing firm to deploy an integrated drying and storage system for soybean production, supporting efforts to reduce post-harvest losses and improve export quality in South America.

- In October 2023, Glatt GmbH signed a collaboration agreement with a Mexican pharmaceutical manufacturer to supply a state-of-the-art fluidized bed drying system, ensuring compliance with international drug production standards and boosting domestic API manufacturing capabilities.

- In February 2024, Thermopac Industrie, a Brazilian industrial dryer manufacturer, expanded its production facility in Curitiba to meet rising demand from the food and chemical sectors, emphasizing localized production and faster delivery cycles.

- In August 2023, ANDRITZ GROUP entered into a joint venture with a Chilean mining company to install high-capacity rotary dryers, enhancing mineral dewatering and processing efficiency in copper and lithium operations across South America.

MARKET SEGMENTATION

This research report on the Latin American industrial dryers market is segmented and sub-segmented into the following categories.

By Product

- Direct

- Indirect

- Specialty dryers

By Application

- Pharmaceutical

- Fertilizer

- Food

- Cement

- Chemicals

By Type

- Spray

- Fluidized beds

- Rotary dryers

By Country

- Brazil

- Chile

- Argentina

- Mexico

- Others

Frequently Asked Questions

What is the projected CAGR of the Latin America Industrial Dryers Market from 2024 to 2033?

The Latin American industrial dryers market is expected to grow at a CAGR of 4.80% from 2024 to 2033, driven by rising demand from agro-processing, chemical, and mineral processing industries across the region.

Which country leads in industrial dryer consumption within Latin America?

Brazil accounts for over 40% of total dryer demand, particularly in sectors like sugar & ethanol production, soybean processing, and mining, where large-scale drying operations are essential.

How many industrial dryers were installed across key manufacturing sectors in LATAM in 2023?

Approximately 2,700 new industrial dryers were installed in major sectors including food processing, chemicals, and minerals across Latin America in 2023, according to the Latin American Association of Process Equipment (ALAPE).

Which industry sector uses the most industrial dryers in Latin America?

The agro-industrial sector leads, especially in sugar mills, coffee drying plants, and grain storage facilities, accounting for over 52% of all industrial dryer applications in the region.

What percentage of industrial dryers in LATAM use biomass or renewable energy sources?

Over 28% of newly installed dryers in Brazil and Colombia utilize biomass, biogas, or waste heat recovery systems, reflecting a growing shift toward sustainable thermal energy solutions in food and fiber processing.

How did inflation and currency volatility impact dryer imports in LATAM in 2023?

Currency depreciation in Argentina and Peru caused a 12–15% drop in imported dryer purchases, pushing local manufacturers and users to explore cost-effective domestic alternatives and retrofit older units.

Which cities in Latin America have seen the fastest growth in dryer installations?

Industrial hubs such as São Paulo (Brazil), Medellín (Colombia), and Guadalajara (Mexico) reported the highest increase in dryer installations in 2023, largely due to expansion in packaged food and beverage production.

What types of dryers dominate the Latin American market: Rotary, Fluid Bed, or Flash?

Rotary dryers lead the market , especially in mineral drying and fertilizer production, with over 60% of industrial dryer sales in Chile and Peru attributed to this type due to its robustness and high throughput.

How much has the aftermarket services segment for industrial dryers grown since 2021?

Aftermarket services — including maintenance, retrofitting, and spare parts — grew by over 22% since 2021, driven by aging equipment in Argentina and Mexico and increased focus on operational efficiency.

What role do digital controls and IoT play in modern dryer installations in LATAM?

In 2023, nearly 35% of new dryer installations in Brazil and Chile included IoT-enabled monitoring systems, allowing real-time control of temperature, moisture levels, and energy consumption for improved process optimization.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com