Latin America Poultry Feed Market Size, Share, Growth, Trends, And Forecast Report Segmented By Animal, Ingredients, Supplements, And By Country (Brazil, Chile, Argentina, Mexico, and Colombia, etc), Industry Analysis From 2025 To 2033

Latin America Poultry Feed Market Size

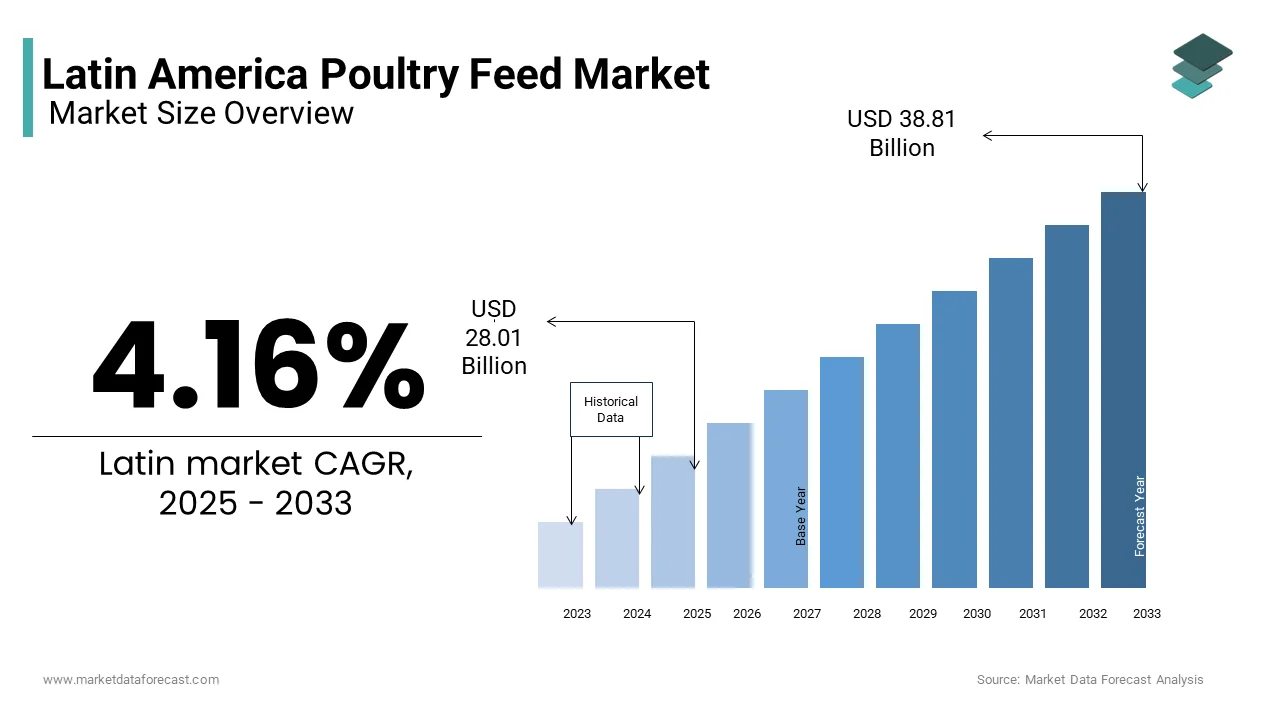

The Latin American poultry feed market was valued at USD 26.89 billion in 2024 and is anticipated to reach USD 28.01 billion in 2025 from USD 38.81 billion by 2033, growing at a CAGR of 4.16% during the forecast period from 2025 to 2033.

The Latin American poultry feed market refers to the production, distribution, and consumption of formulated feed designed to meet the nutritional requirements of poultry species such as broilers, layers, and turkeys. This sector is integral to the region’s agricultural economy, supporting both domestic consumption and international export of poultry meat and eggs. The market encompasses a wide range of ingredients, including corn, soybean meal, wheat, and various additives that enhance growth performance, immunity, and feed conversion ratios. According to the Food and Agriculture Organization (FAO), Latin America ranks among the top global contributors to poultry production, with Brazil being the second-largest exporter of chicken meat worldwide. As per data from the International Feed Industry Federation (IFIF), in 2023, approximately 65 million metric tons of compound feed were produced across Latin America, with poultry feed accounting for nearly 40% of this volume. Moreover, the increasing adoption of precision feeding techniques, biosecurity measures, and fortified feed formulations has enhanced productivity and disease resistance in poultry flocks.

MARKET DRIVERS

Rising Demand for Poultry Meat and Eggs

One of the primary drivers of the Latin American poultry feed market is the increasing regional and global demand for poultry meat and eggs, which directly influences feed production volumes. As consumers shift toward affordable, high-quality protein sources, poultry remains a preferred choice over red meats due to its lower cost, shorter production cycle, and perceived health benefits. In Brazil alone, domestic chicken consumption rose to 47 kilograms per person, as reported by the Brazilian Animal Protein Association (ABPA). This trend has been reinforced by expanding retail networks, growing fast-food chains, and rising middle-class populations seeking convenient protein options. Besides, international exports have surged, particularly to Asia and the Middle East, further incentivizing poultry production and consequently boosting feed demand.

Expansion of Commercial Poultry Farming Operations

The expansion of commercial poultry farming across Latin America is another key driver fueling the growth of the poultry feed market. Large-scale, vertically integrated poultry operations are increasingly replacing traditional backyard farming methods, leading to higher demand for standardized, nutrient-dense feed formulations. This transition has been supported by government-backed rural development programs encouraging modernization and investment in agro-industrial infrastructure. In Brazil, where poultry farming is highly consolidated, companies like JBS S.A., BRF S.A., and Tyson Foods operate extensive supply chains that include dedicated feed mills supplying thousands of contracted farmers. Furthermore, foreign direct investment in poultry processing plants and breeding facilities has spurred feed demand, particularly in Colombia and Peru. As commercial operations continue to expand, the need for high-performance feed tailored to specific production stages will remain a strong catalyst for market growth.

MARKET RESTRAINTS

Volatility in Raw Material Prices

A significant restraint affecting the Latin American poultry feed market is the volatility in raw material prices, particularly for key commodities such as corn and soybeans, which constitute the majority of poultry feed formulations. Fluctuations in global commodity markets, influenced by climate conditions, trade policies, and currency exchange rates, directly impact feed production costs and profitability. In 2023, soybean prices experienced a major year-over-year increase due to reduced harvests in South America and increased demand from China. Similarly, corn prices saw sharp fluctuations following adverse weather patterns in Argentina and Brazil, as documented by the Buenos Aires Grain Exchange. These price swings place financial pressure on feed manufacturers and poultry producers, many of whom operate on thin margins. In response, some companies have resorted to using alternative ingredients such as sorghum or distillers’ dried grains with solubles (DDGS), but these substitutes often come with limitations in terms of availability and nutritional efficiency. Moreover, inflationary pressures in several Latin American economies have compounded the issue, making it difficult for smaller feed producers to absorb input cost increases without passing them on to end users.

Regulatory and Environmental Constraints

Regulatory and environmental constraints represent another major challenge for the Latin American poultry feed market, particularly as governments implement stricter sustainability mandates and land-use regulations. Concerns about deforestation, biodiversity loss, and greenhouse gas emissions linked to large-scale agriculture have prompted policy changes that affect feed crop production and supply chain logistics. According to the World Resources Institute (WRI), in 2023, Brazil intensified enforcement of the Forest Code, requiring soybean and corn producers to maintain legal reserves and restrict farming in ecologically sensitive areas. While these measures support environmental conservation, they have also limited available farmland and increased compliance costs for feed ingredient suppliers. Similarly, in Mexico, recent amendments to animal feed safety standards by the Federal Commission for the Protection against Sanitary Risk (COFEPRIS) have added complexity to formulation and import procedures.

MARKET OPPORTUNITY

Growth in Organic and Specialty Feed Ingredients

An emerging opportunity in the Latin American poultry feed market is the growing demand for organic and specialty feed ingredients, driven by consumer preferences for natural, antibiotic-free, and sustainably raised poultry products. As awareness of animal welfare and food safety increases, both domestic and international buyers are placing greater emphasis on clean-label poultry feed solutions. According to the Latin American Organic Products Network (Red Latinoamericana de Productos Orgánicos), the organic feed market in the region expanded considerably in 2023, with Brazil, Chile, and Uruguay leading the adoption of certified organic poultry feed. Consumers in North America and Europe, major importers of Latin American poultry, are increasingly favoring products derived from birds fed non-GMO and organic diets. This shift has encouraged feed manufacturers to develop alternative formulations incorporating ingredients such as organic soybeans, insect-based proteins, and functional additives like probiotics and prebiotics aimed at improving gut health and reducing reliance on antibiotics. Additionally, certification bodies such as Ecocert and IFOAM – Organics International have facilitated market access by providing recognized organic verification frameworks.

Adoption of Precision Feeding Technologies

The adoption of precision feeding technologies represents a transformative opportunity for the Latin American poultry feed market, offering improved efficiency, cost savings, and environmental sustainability. Precision feeding involves the use of digital tools, automated dispensing systems, and real-time data analytics to optimize feed formulation and delivery based on individual flock requirements. According to the International Livestock Research Institute (ILRI), in 2023, over 20% of large-scale poultry farms in Brazil and Mexico had implemented some form of automated feeding system, allowing for precise control over nutrient intake and minimizing waste. Academic institutions such as the University of São Paulo and Universidad Nacional Autónoma de México have collaborated with agri-tech startups to develop AI-driven monitoring platforms that analyze bird behavior, weight gain, and feed consumption patterns, enabling dynamic adjustments to feeding regimens. Moreover, multinational agribusiness firms are investing in smart barn technologies that integrate IoT sensors and cloud-based analytics to enhance overall farm productivity.

MARKET CHALLENGES

Limited Access to Credit and Financing for Small Producers

A major challenge confronting the Latin American poultry feed market is the limited access to credit and financing options for small and medium-sized feed producers and poultry farmers. Many independent operators struggle to secure loans or investment capital required to upgrade equipment, adopt advanced formulations, or scale production in line with market demands. According to the Inter-American Development Bank (IDB), in 2023, only 35% of small agribusinesses in the region had access to formal financial services, significantly constraining their ability to modernize operations or respond to fluctuating input costs. Traditional lenders often perceive poultry farming and feed production as high-risk sectors due to exposure to commodity price volatility and seasonal demand variations. In countries like Ecuador and Bolivia, where informal poultry operations dominate, lack of collateral and inadequate financial literacy further hinder access to institutional funding. The Pan-American Agricultural Credit Union (CAPS) reports that even when credit is available, interest rates tend to be prohibitively high, discouraging investment in feed technology and infrastructure improvements.

Logistical and Distribution Bottlenecks

Logistical and distribution bottlenecks pose a persistent challenge for the Latin American poultry feed market, particularly in remote and rural regions where transportation infrastructure is underdeveloped. Inefficiencies in freight movement, inconsistent road conditions, and port congestion contribute to delays in feed delivery, disrupting supply chains and increasing operational costs. As reported by the World Bank in its Logistics Performance Index (LPI) 2023, several Latin American countries, including Venezuela, Paraguay, and parts of Central America, ranked below global averages in terms of transport reliability and customs efficiency. Delays in importing essential feed ingredients such as amino acids, vitamins, and mineral supplements further exacerbate supply constraints. Inland distribution challenges are particularly acute in Brazil, where vast distances and seasonal weather disruptions affect the timely delivery of feed to poultry farms. The Brazilian Confederation of Agriculture and Livestock (CNA) notes that in 2023, transportation costs accounted for up to 25% of total feed production expenses in certain regions. To mitigate these issues, some feed manufacturers are exploring decentralized production models and local sourcing partnerships.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.16% |

| Segments Covered | By Animal, Ingredients, Supplements, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Chile, Argentina, Mexico, and Colombia, etc |

| Market Leaders Profiled | Cargill, Incorporated, Alltech, ADM, Land O Lakes Inc., Nutreco, InVivo, Charoen Pokphand Group, Kent Nutrition Group, CCPA Group |

SEGMENTAL ANALYSIS

By Animal Insights

The broilers dominated the Latin American poultry feed market by capturing 52.8% of the total market share in 2024. This leading position is primarily attributed to the region's strong preference for chicken meat as a cost-effective protein source, coupled with robust export demand from international markets. According to the Brazilian Animal Protein Association (ABPA), broiler production in Brazil reached over 14 million metric tons in 2023, making it the second-largest exporter globally. The country’s integrated poultry farming model ensures consistent feed demand, as large-scale processors operate vertically integrated supply chains that include dedicated feed mills. In Mexico, domestic consumption continues to rise, driven by fast-food expansion and changing dietary patterns. Like, local broiler meat consumption increased significantly between 2020 and 2023, directly influencing feed production volumes. Apart from this, Argentina has seen a revival in its poultry sector, with government incentives supporting investment in broiler farms and hatcheries. Also, Argentina’s broiler output rose significantly in 2023, further reinforcing the dominance of this segment in the regional poultry feed market.

The turkey poultry feed represented the fastest-growing segment within the Latin American poultry feed market, recording a CAGR of 5.1% between 2025 and 2033. This is fueled by increasing consumer demand for lean, protein-rich meats, particularly during festive seasons and special occasions. In Brazil, turkey production significantly increased year-over-year, supported by rising urban middle-class incomes and a shift toward healthier protein alternatives. In Mexico, where turkey is a traditional part of national cuisine, especially during holidays like Christmas and Día de la Virgen de Guadalupe, demand remains consistently high. Furthermore, turkey producers are adopting more efficient feeding strategies, including specialized feed formulations that enhance weight gain and disease resistance.

By Ingredients Insights

The cereals constituted the biggest ingredient segment in the Latin American poultry feed market by accounting for 47.5% of the total market share in 2024. Corn remains the dominant cereal used due to its high energy content, palatability, and availability across the region. According to the United States Department of Agriculture (USDA), Brazil harvested over 115 million metric tons of corn in 2023, with nearly 60% allocated for livestock and poultry feed. The country benefits from extensive arable land and advanced agricultural production systems, ensuring a stable supply chain for feed manufacturers. Argentina also plays a key role in cereal-based feed production, leveraging its status as one of the world’s top soybean and corn exporters. The Buenos Aires Grain Exchange highlights that in 2023, Argentina exported over 30 million metric tons of corn, with a significant portion processed into poultry feed domestically before reaching livestock operations.

The oilseed meal, particularly soybean meal, is the quickest advancing ingredient segment in the Latin American poultry feed market, registering a CAGR of 6.3%. This is driven by the high protein content of oilseed meals, which are essential for muscle development, feed efficiency, and overall poultry health. Brazil, the world’s largest soybean producer and exporter, produced over 150 million metric tons of soybeans in 2023, according to data from Conab, the country’s agricultural agency. A significant portion of this harvest was processed into soybean meal for domestic poultry feed use, while surplus supplies were exported to support global animal protein production. Like, soybean processing infrastructure in Argentina is well established, the National Institute of Agricultural Technology (INTA) reported that soybean meal exports increased significantly in 2023 compared to the previous year, reflecting stronger integration between feed manufacturing and poultry farming sectors. Moreover, growing awareness among farmers about optimal feed formulation practices has led to increased inclusion rates of oilseed meal in broiler and layer diets.

By Supplements Insights

The vitamins represented the top-performing supplement segment in the Latin American poultry feed market by capturing 28.5% of the total market share in 2024. Their widespread use in poultry nutrition is driven by their critical role in maintaining immune function, enhancing metabolic efficiency, and improving overall bird performance. According to the Latin American Feed Industry Association (ALIFE), a large majority of industrially manufactured poultry feed in the region includes vitamin premixes tailored to different life stages of birds. In Brazil, where poultry production is highly integrated, companies have standardized vitamin supplementation protocols to ensure consistency in meat and egg quality. The Pan-American Health Organization (PAHO) emphasizes that vitamin A, D, E, and the B-complex are particularly vital for poultry health, helping prevent deficiencies that can lead to poor growth, reduced eggshell quality, and heightened disease susceptibility. In Mexico, vitamin-fortified feeds have become a standard in broiler operations, contributing to improved feed conversion ratios and reduced mortality rates.

On the contrary, the probiotics and prebiotics are emerging as the booming supplement category in the Latin American poultry feed market, exhibiting a CAGR of 7.2%. This surge is attributed to growing awareness of gut health management and the need to reduce antibiotic usage in response to global calls for antimicrobial stewardship. According to the International Livestock Research Institute (ILRI), Latin American poultry producers have increasingly adopted probiotic-enriched feed to enhance digestion, improve immunity, and promote sustainable poultry farming practices. Mexico has also witnessed a shift toward natural feed additives, with several poultry integrators incorporating prebiotics such as fructooligosaccharides (FOS) and mannan-oligosaccharides (MOS) to support beneficial gut flora. Moreover, consumer concern over antibiotic residues in meat has prompted regulatory changes favoring alternative supplements.

COUNTRY-LEVEL ANALYSIS

Brazil led the Latin American poultry feed market with a commanding 38.6% share in 2024. As one of the world's top poultry producers and exporters, Brazil benefits from vast agricultural resources, a well-established feed manufacturing industry, and strong integration between feed production and poultry farming. According to the Brazilian Animal Protein Association (ABPA), the country produced over 14 million metric tons of chicken meat in 2023, requiring nearly 40 million metric tons of poultry feed annually. This high level of production is supported by the domestic availability of corn and soybean meal, two primary components of poultry diets. Government agencies such as Embrapa and MAPA continuously drive innovation in feed formulation and animal nutrition, ensuring efficient production cycles and compliance with international food safety standards. Also, Brazil's environmental policies encourage sustainable sourcing of feed ingredients, aligning with global market expectations.

Mexico is another key player in the market. The country’s strong domestic demand for poultry products, bolstered by an expanding middle class and fast-food sector, drives continuous growth in feed production. According to the Mexican Ministry of Agriculture (SADER), in 2023, domestic poultry meat consumption reached 3.2 million metric tons, necessitating significant quantities of formulated feed to meet both commercial and backyard farm needs. Major poultry companies such as Bachoco and Tyson Foods operate large-scale integrated systems with dedicated feed mills supplying thousands of contracted producers. Moreover, Mexico serves as a key supplier to Central American markets, further boosting feed demand.

Argentina is growing at a moderate rate in the market and is driven by recent improvements in its poultry and agribusiness sectors. Despite historical economic fluctuations, the country has made strides in rebuilding its livestock industry through policy reforms and private-sector investment. This growth trajectory has been supported by public-private initiatives aimed at enhancing feed affordability and accessibility for small and medium-sized producers. Also, Argentina's abundant soybean and corn production provides a reliable base for formulating high-quality poultry feed, reducing dependency on imported inputs. Additionally, efforts to integrate feed suppliers with poultry integrators have improved supply chain efficiency and reduced costs.

Chile contributed a key share of the Latin American poultry feed market, supported by a well-developed agro-industrial infrastructure and strong domestic consumption patterns. The country benefits from a stable regulatory environment and efficient logistics networks that facilitate the timely distribution of feed across poultry farms. Domestic feed manufacturers have responded by optimizing formulations to meet export-oriented production standards. Chilean universities and agricultural research institutes have collaborated with feed producers to develop fortified feed solutions that enhance bird immunity and reduce reliance on antibiotics.

Colombia is benefiting from a growing population, rising disposable incomes, and supportive government policies encouraging livestock development. The poultry sector has expanded steadily over the past decade, stimulating corresponding increases in feed production. As per the Colombian Federation of Poultry Farmers (FEDEAVES), in 2023, the country produced over 1.3 million metric tons of poultry meat, representing a key increase compared to the previous year. This upward trend has been mirrored in the feed industry, where manufacturers are investing in new facilities and upgrading existing ones to meet evolving demand. Additionally, Colombia has taken proactive steps to reduce dependence on imported feed ingredients by promoting local soybean and corn cultivation.

KEY MARKET PLAYERS

Cargill, Incorporated, Alltech, ADM, Land O Lakes Inc., Nutreco, InVivo, Charoen Pokphand Group, Kent Nutrition Group, CCPA Group. These are the market players that are dominating the Latin American poultry feed market.

Top Players in the Market

Cargill Animal Nutrition

Cargill is a global leader in animal nutrition and plays a pivotal role in the Latin American poultry feed market. The company operates an extensive network of feed mills, research centers, and distribution channels across Brazil, Mexico, and Argentina. Cargill’s focus on sustainable sourcing, nutritional innovation, and integrated supply chain solutions has made it a preferred partner for large-scale poultry producers. Its commitment to developing region-specific feed formulations supports improved productivity and disease resistance, contributing significantly to the growth of the Latin American poultry industry.

JBS S.A. – Moy Park (Feed Division)

JBS, through its subsidiary Moy Park, is a major player in the Latin American poultry feed sector, particularly in Brazil and Mexico. As one of the world's largest meat processors, JBS integrates feed production with poultry farming operations to ensure quality control and cost efficiency. The company invests heavily in vertical integration strategies, biosecurity protocols, and advanced feed technologies that enhance performance and sustainability, reinforcing its influence in both regional and global markets.

Bunge Limited

Bunge is a key contributor to the Latin American poultry feed market, leveraging its expertise in agribusiness and grain processing to supply high-quality feed ingredients. With a strong presence in Brazil and Argentina, Bunge provides essential raw materials such as soybean meal and corn to feed manufacturers across the region. The company’s investment in sustainable agricultural practices and logistics infrastructure supports efficient feed production and strengthens the overall poultry value chain in Latin America.

Top Strategies Used by Key Market Participants

One of the primary strategies adopted by leading players in the Latin American poultry feed market is vertical integration, where companies control multiple stages of the supply chain—from feed ingredient sourcing to final poultry product distribution. This approach ensures consistent quality, cost control, and resilience against commodity price fluctuations.

Another major strategy involves product innovation and formulation customization, allowing feed manufacturers to cater to the specific nutritional needs of broilers, layers, and other poultry types. Companies are increasingly incorporating functional additives like probiotics, enzymes, and prebiotics to improve bird health and performance while aligning with global trends toward antibiotic reduction.

Lastly, strategic partnerships and local collaborations play a crucial role in strengthening market position. Leading firms are partnering with local cooperatives, research institutions, and government bodies to develop region-specific feed solutions, enhance distribution networks, and support smallholder farmers in adopting modern feeding practices tailored to their operational realities.

COMPETITION OVERVIEW

The competition in the Latin American poultry feed market is marked by a blend of multinational agribusiness giants and well-established regional players, all vying to meet the rising demand for poultry products amid evolving consumer preferences and regulatory landscapes. Large corporations leverage economies of scale, technological advancements, and integrated supply chains to maintain dominance, while mid-sized and local feed manufacturers focus on niche markets, customized formulations, and proximity to poultry producers.

Market leaders such as Cargill, JBS, and Bunge continue to expand their presence through strategic investments in feed technology, sustainability initiatives, and logistics optimization. These firms also benefit from strong relationships with poultry integrators, enabling them to offer tailored feed solutions that enhance productivity and food safety.

At the same time, growing awareness about animal nutrition, gut health, and sustainable farming is pushing companies to innovate beyond traditional formulations. Startups and specialty feed additive providers are emerging as competitive forces, offering niche supplements and biotechnological solutions aimed at improving feed efficiency and reducing environmental impact.

Additionally, fluctuating raw material prices, logistical challenges, and financial constraints faced by smaller operators create barriers to entry and scalability. However, increasing collaboration between the public and private sectors is helping to level the playing field, ensuring a dynamic and evolving competitive landscape across Latin America.

RECENT HAPPENINGS IN THE MARKET

In February 2024, Cargill launched a new feed mill in São Paulo, Brazil, designed to increase local production capacity and improve supply chain efficiency for poultry integrators operating in the region.

In June 2024, JBS announced a strategic partnership with a Brazilian biotech firm specializing in feed additives, aiming to incorporate natural probiotics into poultry feed formulations to enhance digestive health and reduce antibiotic dependency.

In October 2024, Bunge expanded its soybean processing facility in Argentina to boost the availability of high-protein soybean meal, directly supporting the growing demand for premium poultry feed in South America.

In December 2024, Nutreco acquired a controlling stake in a Mexican feed premix supplier, strengthening its foothold in Central America and enhancing its ability to provide customized vitamin and mineral blends to poultry producers.

In March 2025, DSM partnered with Colombian poultry associations to introduce a fortified feed program focused on improving nutrient absorption and immune response in broiler chickens, reinforcing its leadership in feed supplementation and animal health innovation.

MARKET SEGMENTATION

This research report on the Latin American poultry feed market is segmented and sub-segmented into the following categories.

By Animal Type

- Layer

- Broiler

- Turkey

- Other Animal Types

By Ingredients

- Cereal

- Oilseed Meal

- Oil

- Molasses

- Other Ingredients

By Supplement

- Vitamins

- Amino Acids

- Antibiotics

- Enzymes

- Antioxidants

- Acidifiers

- Probiotics and Prebiotics

- Other Supplements

By Country

- Brazil

- Chile

- Argentina

- Mexico

- Colombia

- Others

Frequently Asked Questions

What’s fueling the growth of poultry feed demand in Latin America?

Rising domestic and export-driven poultry meat production—especially in Brazil and Mexico—is increasing demand for high-performance, cost-effective feed formulations.

Which ingredients dominate poultry feed production in the region?

Corn and soybean meal are the primary components, driven by abundant local supply. Enzymes and amino acids are increasingly added to boost digestibility and feed efficiency.

How do regional challenges impact poultry feed quality?

Issues like climate variability, storage infrastructure gaps, and mycotoxin contamination push producers to invest in feed stabilizers and toxin binders to maintain flock health.

How are sustainability trends influencing poultry feed strategies?

There's a growing shift toward plant-based additives, reduced antibiotic use, and circular feed practices (like using agri-byproducts), driven by consumer pressure and global export standards.

What role does technology play in modernizing poultry feed production in Latin America?

Precision nutrition tools, automated mixing systems, and real-time data tracking are helping large producers optimize feed conversion ratios and reduce waste.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com