Latin America Agricultural Inoculants Market Size, Share, Growth, Trends, And Forecasts Research Report, Segmented By Type, Source, Application, Crop Type, And By Country (Brazil, Argentina, Mexico, Chile and Rest of Latin America) - Industry Analysis 2026 to 2034

Latin America Agricultural Inoculants Market Size

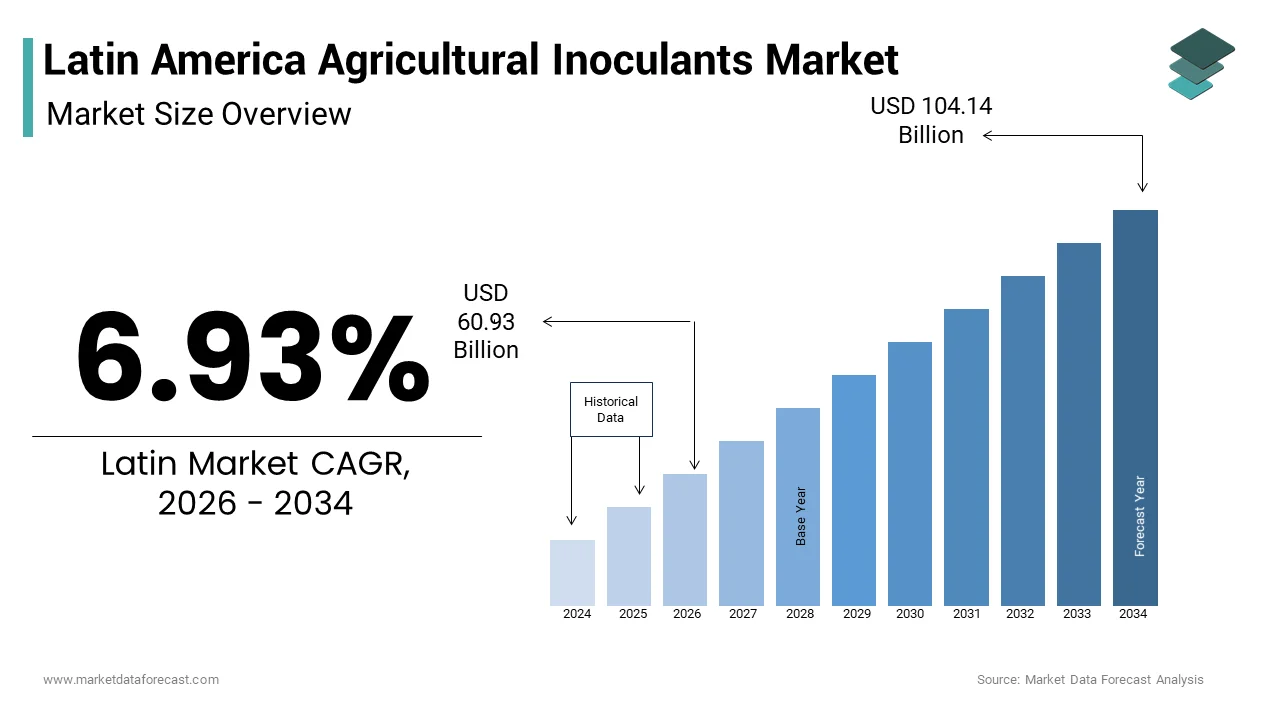

The Latin America agricultural inoculants market size was valued at USD 56.98 billion in 2025 and is anticipated to reach USD 60.93 billion in 2026 to reach USD 104.14 billion by 2034, growing at a CAGR of 6.93% during the forecast period from 2026 to 2034.

The Latin American agricultural inoculants market refers to the production and application of biological products that introduce beneficial microorganisms into the soil to enhance plant nutrient uptake, primarily through nitrogen fixation and phosphorus solubilization. These inoculants are widely used in leguminous crops such as soybeans, peanuts, and common beans, as well as increasingly in non-leguminous crops to reduce dependency on synthetic fertilizers. According to the International Center for Tropical Agriculture (CIAT), sustainable farming practices are gaining momentum across the region due to rising awareness of environmental degradation caused by chemical inputs. Governments and research institutions across the region are promoting biofertilizers as part of integrated nutrient management strategies, which aligns with global sustainability goals and reinforces the growing relevance of agricultural inoculants in Latin America.

MARKET DRIVERS

Rising Demand for Sustainable Farming Practices

One of the primary drivers of the Latin American agricultural Inoculants Market is the increasing shift toward sustainable farming practices aimed at reducing reliance on synthetic fertilizers and mitigating environmental impact. As per the Food and Agriculture Organization (FAO), over 60% of arable land in Latin America is under cultivation, with excessive fertilizer use contributing to soil degradation and water contamination. Agricultural inoculants offer a natural alternative by enhancing nutrient availability through biological nitrogen fixation, particularly in legume crops like soybeans, which are major contributors to regional agricultural output. The International Center for Tropical Agriculture (CIAT) reports that Brazil alone uses inoculants on more than 70 million hectares of farmland annually, which is significantly lowering its dependence on synthetic nitrogen fertilizers. This trend has been reinforced by government policies promoting eco-friendly farming methods, including subsidies and technical support for farmers adopting biofertilizers. Moreover, organizations such as Embrapa in Brazil have conducted extensive field trials demonstrating the economic viability of inoculant use, encouraging widespread adoption.

Expansion of Legume Cultivation and Government Support

Another key driver fueling the growth of the Latin America Agricultural Inoculants Market is the expansion of legume cultivation, particularly soybeans, which naturally benefit from rhizobia-based inoculation to fix atmospheric nitrogen. According to the United States Department of Agriculture (USDA), Latin America accounts for nearly 45% of global soybean production, with Brazil and Argentina leading the way. These countries have adopted large-scale inoculant programs to optimize yields while minimizing input costs. Additionally, governments across the region are actively promoting bio-inputs through national agricultural policies.

MARKET RESTRAINTS

Limited Farmer Awareness and Technical Knowledge

A significant restraint affecting the Latin American agricultural Inoculants Market is the limited awareness and technical knowledge among smallholder farmers regarding the benefits and proper application of inoculants. Despite their proven efficacy in improving soil fertility and crop yield, many farmers continue to rely on conventional chemical fertilizers due to familiarity and perceived reliability. According to the International Fund for Agricultural Development (IFAD), over 60% of small-scale farmers in rural areas lack access to formal extension services, which is limiting exposure to modern agricultural technologies. Additionally, language barriers, insufficient training materials, and inconsistent dissemination of best practices hinder widespread adoption. While larger agribusinesses and cooperatives have embraced inoculant technology, smaller farms often remain underserved.

Supply Chain and Distribution Challenges

Another critical challenge impacting the Latin American agricultural Inoculants Market is the inefficiency in supply chain logistics and distribution networks, particularly in remote and rural regions. Inoculants require specific storage conditions, including refrigeration, to maintain microbial viability, yet cold-chain infrastructure remains inadequate in many parts of the region. Additionally, weak transportation networks, customs delays, and fragmented retail systems contribute to inconsistent availability of inoculants during planting seasons. In Brazil, despite having the most advanced inoculant market in the region, regional disparities persist, particularly in the North and Northeast, where distribution challenges limit access. To overcome these obstacles, manufacturers must invest in localized production hubs, partner with regional distributors, and implement digital inventory tracking systems.

MARKET OPPORTUNITIES

Integration with Digital Farming and Precision Agriculture

A significant opportunity for the Latin American agricultural Inoculants Market lies in the integration of microbial inputs with digital farming and precision agriculture technologies. As data-driven farming gains traction across the region, there is growing interest in leveraging real-time soil health analytics, satellite imaging, and AI-powered decision-making tools to optimize inoculant application. Companies such as Yara International and Bioceres have introduced digital platforms that recommend customized bio-input applications based on soil composition and crop requirements. Additionally, startups in Chile and Colombia are developing mobile apps that provide farmers with step-by-step guidance on inoculant use, enhancing adoption among tech-savvy growers. The Economic Commission for Latin America and the Caribbean (ECLAC) emphasizes that digital integration can significantly improve the efficiency and return on investment for biofertilizers, making them more attractive to commercial farmers.

Growing Demand for Organic and Regenerative Agriculture

The increasing consumer preference for organic and sustainably produced food is creating new opportunities for the Latin American Agricultural Inoculants Market. According to the Research Institute of Organic Agriculture (FiBL), Latin America accounts for nearly 30% of the world’s certified organic agricultural land, with Argentina, Brazil, and Mexico leading in organic crop production. In response, governments and private-sector stakeholders are promoting biofertilizers as essential tools for maintaining soil health and productivity without chemical inputs. The Brazilian Ministry of Agriculture supports organic farming through financial incentives and technical assistance programs, encouraging the adoption of microbial inoculants. Similarly, Peru and Ecuador have seen a surge in organic exports, driving investments in biological inputs.

MARKET CHALLENGES

Regulatory Heterogeneity Across Countries

One of the primary challenges facing the Latin American agricultural Inoculants Market is the lack of harmonized regulatory frameworks governing the approval, registration, and marketing of microbial inputs across different countries. Unlike the European Union or the United States, where centralized regulatory authorities streamline the process, Latin American nations operate under varying legal structures, complicating market entry for manufacturers. According to the Inter-American Institute for Cooperation on Agriculture (IICA), differences in labeling requirements, microbial strain specifications, and registration timelines create inconsistencies that delay product launches and increase compliance costs. For instance, while Brazil has a well-established regulatory system managed by MAPA (Ministry of Agriculture, Livestock, and Supply), other countries such as Guatemala and Honduras rely on less structured frameworks, leading to prolonged approval periods. Additionally, the absence of standardized quality control protocols hampers cross-border trade and limits the scalability of the inoculant product, as noted by the Economic Commission for Latin America and the Caribbean (ECLAC).

Price Volatility and Input Cost Sensitivity

Price volatility and sensitivity to input costs present a considerable challenge for the Latin American agricultural Inoculants Market among small and medium-sized farmers who operate on tight profit margins. Although inoculants offer long-term economic benefits by reducing the need for synthetic fertilizers, their initial procurement cost and perceived risk compared to traditional inputs make adoption hesitant. Additionally, currency fluctuations and import dependencies further complicate pricing stability for biofertilizers. In countries like Ecuador and Bolivia, where agricultural incomes are highly variable, farmers often opt for cheaper, immediate-impact solutions rather than investing in biological inputs with delayed returns.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.93% |

| Segments Covered | By Type, Source, Application, Crop Type, and Region. |

| Various Analyses Covered | Global, Regional and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Mexico, Chile, Argentina, the Rest of Latin America |

| Market Leaders Profiled | BASF SE, E.I. Du Pont de Nemours and Company, Bayer CropScience, Novozymes A/S, Brettyoung, Verdesian Life Sciences, Dow Chemical Company, Syngenta AG, Precision Laboratories, Xitebio Technologies. |

SEGMENTAL ANALYSIS

By Type Insights

The Plant Growth Promoting Microorganisms (PGPMs) segment was the largest and held 58.1% of the Latin America Agricultural Inoculants Market share in 2024. According to the Brazilian Agricultural Research Corporation (Embrapa), over 70 million hectares of farmland in Brazil alone utilize PGPM-based inoculants annually, which is significantly reducing dependency on synthetic nitrogen fertilizers. Governments across the region have also endorsed their adoption through policy incentives and extension programs aimed at promoting biological inputs over chemical fertilizers.

The plant-resistance stimulants segment is projected to grow with a projected CAGR of 10.4% in the coming years. This rapid expansion is driven by rising concerns over climate variability, pest outbreaks, and the need for enhanced crop resilience. Plant-resistance stimulants function by activating systemic acquired resistance (SAR) mechanisms within plants, enabling them to withstand biotic and abiotic stressors more effectively. According to the Inter-American Institute for Cooperation on Agriculture (IICA), climate change has increased the frequency of extreme weather events across Latin America, affecting crop yields and quality. In response, farmers are increasingly adopting bio-stimulant inoculants that enhance plant immunity without compromising environmental sustainability.

By Source Insights

The bacterial-based inoculants segment held da dominant share of the Latin America Agricultural Inoculants Market in 2024. These microbes form symbiotic relationships with host plants, converting atmospheric nitrogen into a usable form, thereby reducing the need for synthetic fertilizers. The Food and Agriculture Organization (FAO) reports that bacterial inoculants can reduce synthetic nitrogen fertilizer requirements by up to 70% in well-managed legume systems, making them an economically viable and environmentally beneficial solution. Additionally, regulatory support and farmer education initiatives led by national agricultural agencies have further strengthened the adoption of bacterial-based products.

The fungal-based inoculants segment is expected to grow with a CAGR of 9.8% during the forecast period. This growth is fueled by increasing interest in arbuscular mycorrhizal fungi (AMF) and Trichoderma species, which enhance phosphorus uptake, improve soil structure, and boost plant resistance against pathogens. According to the International Center for Tropical Agriculture (CIAT), fungal inoculants are gaining popularity in non-leguminous crops such as corn, wheat, and sugarcane, where phosphorus availability is a limiting factor for productivity. In Mexico and Colombia, government-backed pilot projects are promoting mycorrhizal applications in coffee and banana plantations to improve yield stability under low-input conditions. The Economic Commission for Latin America and the Caribbean (ECLAC) notes that fungal inoculant research and commercialization efforts have intensified in recent years, supported by collaborations between universities and agritech firms.

By Application Insights

The seed inoculation segment held a prominent share of the Latin America Agricultural Inoculants Market in 2024, with the widespread practice of applying microbial inoculants directly onto seeds before planting, ensuring early establishment of beneficial microbial associations in the rhizosphere. Countries such as Brazil and Argentina have long embraced seed inoculation for soybeans, where Rhizobium and Bradyrhizobium strains play a critical role in nitrogen fixation. The Brazilian Ministry of Agriculture emphasizes that seed inoculation provides cost-effective, scalable solutions for large-scale commercial farms, making it the preferred method among agribusinesses. Additionally, the smallholder farmers in Paraguay and Bolivia are increasingly adopting seed treatment technologies due to improved accessibility and ease of use.

The soil inoculation segment is expected to witness a CAGR of 9.3% in the coming years. Soil inoculation allows for targeted delivery of beneficial microorganisms directly into the root zone, supporting crops that do not naturally engage in symbiotic nitrogen fixation. According to the Inter-American Institute for Cooperation on Agriculture (IICA), soil drenching and granular formulations are gaining traction in specialty crops such as coffee, bananas, and tomatoes in Central America and the Andean region. Additionally, the Economic Commission for Latin America and the Caribbean (ECLAC) notes that organic farming initiatives in Peru and Ecuador are encouraging the use of soil-applied biofertilizers to restore degraded lands and maintain long-term productivity.

By Crop Type Insights

The oilseeds and pulses segment was the largest by occupying 45.2% of the Latin America Agricultural Inoculants Market share in 2024 due to the extensive cultivation of leguminous crops such as soybeans, common beans, and peanuts, which rely heavily on rhizobia-based inoculants for nitrogen fixation.

The fruits and vegetables segment is expected to grow with an estimated CAGR of 10.7% in the coming years. This rapid expansion is driven by increasing investments in horticultural production, particularly in export-oriented crops such as avocados, berries, citrus fruits, and tomatoes. Unlike traditional legumes, these crops benefit from microbial inoculants that enhance phosphorus uptake, improve disease resistance, and promote overall plant health. The International Trade Centre (ITC) notes that Latin American fruit and vegetable exports grew by over 12% in recent years, which is reinforcing the need for sustainable nutrient management solutions.

COUNTRY ANALYSIS

Brazil Agricultural Inoculants Market Analysis

Brazil was the top performer in the Latin American Agricultural Inoculants Market by holding 42.3% of the share in 2024. Positioned as the world’s largest soybean producer, Brazil has been a pioneer in adopting microbial inoculants, particularly rhizobia-based products, to replace synthetic nitrogen fertilizers. According to Embrapa, over 70 million hectares of soybean fields in Brazil use inoculants annually, which is saving the country billions of dollars in fertilizer imports while maintaining high yields. The Brazilian Ministry of Agriculture supports this transition through policies promoting biological inputs as part of national sustainability goals.

Argentina Agricultural Inoculants Market Analysis

Argentina was positioned second with 18.2% of the Latin American Agricultural Inoculants Market share in 2024. The country’s no-till farming system has further boosted demand for biological inputs that enhance soil microbiology and fertility. The International Center for Tropical Agriculture (CIAT) notes that Argentina’s inoculant market is evolving beyond soybeans to include wheat and pastureland applications, which indicates broader adoption potential.

Mexico Agricultural Inoculants Market Analysis

Mexican agricultural inoculants market is expected to grow with the fastest CAGR in the coming years. According to the International Maize and Wheat Improvement Center (CIMMYT), inoculant use in maize and wheat systems is increasing due to rising input costs and environmental concerns associated with synthetic fertilizers. Government-backed initiatives promoting organic farming and sustainable nutrient management have further supported inoculant adoption.

COMPETITIVE LANDSCAPE

The competition in the Latin American agricultural Inoculants Market is marked by a dynamic mix of global agrochemical giants, specialized biotech firms, and emerging local players striving to capture market share. While multinational corporations bring extensive R&D capabilities, brand recognition, and established distribution networks, regional and domestic companies leverage their understanding of local farming practices, regulatory landscapes, and cost structures to remain competitive. The market landscape reflects a balance between innovation-driven prominence and agile, customer-focused strategies aimed at addressing the unique needs of diverse agricultural ecosystems across the continent. Additionally, evolving regulatory frameworks, fluctuating input prices, and increasing emphasis on organic certification further shape competitive positioning.

KEY MARKET PLAYERS

Some of the key players in this market include

- BASF SE,

- E.I. Du Pont de Nemours and Company

- Bayer CropScience

- Koppert Biological Systems

- Novozymes A/S

- UPL Limited

- Brettyoung

- Verdesian Life Sciences

- Dow Chemical Company

- Syngenta AG

- Precision Laboratories

- Xitebio Technologies.

Top Players In The Market

- BASF is a global leader in agricultural solutions and plays a pivotal role in the Latin American agricultural Inoculants Market through its advanced microbial technologies. The company offers a wide range of bio-stimulant and nitrogen-fixing products tailored for soybean, corn, and other key crops in the region. BASF’s focus on innovation and sustainability has made it a trusted partner among farmers and agribusinesses seeking to reduce chemical input usage while maintaining productivity. Its strong R&D capabilities have led to the development of high-performance inoculant formulations that enhance soil health and crop resilience.

- Koppert is a leading provider of sustainable agricultural solutions, which is specializing in biological crop protection and soil health management. In the Latin American market, Koppert contributes significantly by offering natural inoculant-based products that promote nutrient availability and plant immunity. The company's integrated approach combines microbial technology with precision agriculture tools, enabling farmers to optimize yields while minimizing environmental impact. Koppert actively engages in knowledge transfer programs, training farmers and agronomists on best practices for using biological inputs effectively.

- UPL is a major player in the global bio-inputs space and has been instrumental in expanding access to affordable and effective agricultural inoculants across Latin America. The company provides a comprehensive portfolio of microbial products designed to enhance nutrient uptake, improve soil fertility, and support sustainable farming systems. UPL’s strategy focuses on integrating biologicals into conventional agricultural practices, making them accessible to both large-scale and smallholder farmers. Through strategic partnerships and localized distribution networks, UPL ensures reliable supply chains and technical support for farmers adopting biofertilizers.

Top Strategies Used By Key Market Participants

One of the primary strategies employed by key players in the Latin American agricultural Inoculants Market is investing in localized research and development to tailor microbial solutions to regional soil and climate conditions. Companies are partnering with national agricultural institutes and universities to develop strains that perform optimally in tropical and subtropical environments by ensuring higher efficacy and adoption rates.

Another crucial approach is expanding distribution networks and strengthening collaborations with local agro-input suppliers and cooperatives, which enables companies to reach remote farming communities more efficiently. This strategy enhances accessibility, improves after-sales support, and fosters trust among farmers who may be unfamiliar with biological alternatives to synthetic fertilizers.

The companies are increasingly focusing on farmer education and awareness campaigns to demonstrate the economic and environmental benefits of inoculants. Through field trials, demonstration plots, and digital outreach, manufacturers are building confidence in microbial inputs, encouraging greater adoption across both commercial and smallholder farming sectors in Latin America.

RECENT MARKET NEWS

- In February 2024, BASF launched a new line of rhizobia-based inoculants specifically formulated for tropical soybean varieties in Brazil, aiming to improve nitrogen fixation efficiency and support large-scale farmers in reducing synthetic fertilizer dependency.

- In May 2024, Koppert Biological Systems expanded its technical support team in Argentina to provide on-the-ground training and advisory services for soybean and corn growers adopting microbial inoculation techniques in no-till farming systems.

- In September 2024, UPL Limited partnered with a Mexican agro-input distributor to enhance market access for phosphate-solubilizing inoculants in maize and wheat production zones, targeting both commercial and smallholder farmers.

- In January 2025, Syngenta introduced a digital platform in Colombia that connects farmers with agronomic advisors and provides real-time recommendations for optimal inoculant use based on soil analysis and weather data.

- In April 2025, Bioceres Crop Solutions Corp. acquired a Chilean biofertilizer startup to strengthen its portfolio of plant-resistance stimulant products and accelerate expansion into high-value fruit and vegetable export markets.

MARKET SEGMENTATION

This research report on the Latin American Agricultural Inoculants Market is segmented and sub-segmented into the following categories.

By Type

- Plant Growth Promoting Micro-organisms

- Bio-control agents

- Plant-resistance Stimulants

By Source

- Bacterial

- Fungal

- Others

By Application

- Seed inoculation

- Soil inoculation

- Others

By Crop Type

- Cereals & grains

- Oilseeds & pulses

- Fruits & vegetables

- Others

By Country

- Mexico

- Argentina

- Brazil

- Chile

Frequently Asked Questions

What is the projected CAGR of the Latin America Agricultural Inoculants Market from 2024 to 2033?

The Latin American agricultural inoculants market is expected to grow at a CAGR of 6.93% from 2024 to 2033, driven by increasing adoption in soybean, maize, and legume crops, along with government incentives for biological inputs in Brazil, Argentina, and Colombia.

Which country leads in agricultural inoculant usage in Latin America?

Brazil accounts for over 58% of total inoculant use, particularly in soybean farming, where Bradyrhizobium-based products are applied on over 36 million hectares annually, according to Embrapa (Brazilian Agricultural Research Corporation).

How many hectares of farmland in Latin America are treated with inoculants annually?

As of 2024, approximately 52 million hectares across Latin America—mainly in Brazil, Argentina, and Paraguay—are treated with microbial inoculants, especially nitrogen-fixing bacteria, significantly reducing synthetic fertilizer dependency.

Which type of inoculant dominates the Latin American market?

Rhizobia-based inoculants lead the market, used primarily in leguminous crops like soybeans and common beans. In Brazil alone, over 70% of soybean seeds are pre-treated with Bradyrhizobium strains, contributing to an average 15–20% increase in yield.

What percentage of pastureland in Brazil uses inoculants for forage crops?

Over 25% of Brazil’s pasturelands now apply Azospirillum-based inoculants to enhance nitrogen fixation in grasses like Brachiaria, improving cattle weight gain and reducing the need for synthetic fertilizers, per the Ministry of Agriculture.

How has government policy in Brazil influenced inoculant demand?

Brazil’s ABC+ Program (Low Carbon Agriculture) has incentivized microbial input use, leading to a 22% annual increase in inoculant adoption since 2021 , especially among large-scale soy and corn producers aiming to meet carbon credit targets.

Which application method is most common for inoculants in Latin America?

Seed treatment remains the dominant method , covering over 65% of all applications , especially among smallholder farmers who rely on cost-effective delivery systems and cooperative extension programs.

How does soil degradation affect inoculant demand in Latin America?

In countries like Colombia and Ecuador, where over 30% of farmland suffers from nutrient depletion, farmers are increasingly using inoculants to restore soil fertility and improve root development in cash crops.

Which universities or research institutions are driving inoculant innovation in the region?

Embrapa (Brazil), INTA (Argentina), and CIAT (International Center for Tropical Agriculture, Colombia) are leading R&D efforts, developing heat- and drought-tolerant strains suited to tropical and subtropical growing conditions.

How much has e-commerce contributed to inoculant sales growth in Latin America?

Online B2B sales of inoculants grew by over 35% annually since 2022 , especially in Brazil and Chile, where digital platforms offer farmer education modules, regional usage guides, and compatibility checks with other biologicals.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com