Latin America Farm Mechanization Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Product And By Country (Brazil, Mexico, Argentina, Chile and Rest of Latin America), Industry Analysis From (2025 to 2033)

Latin America Farm Mechanization Market Size

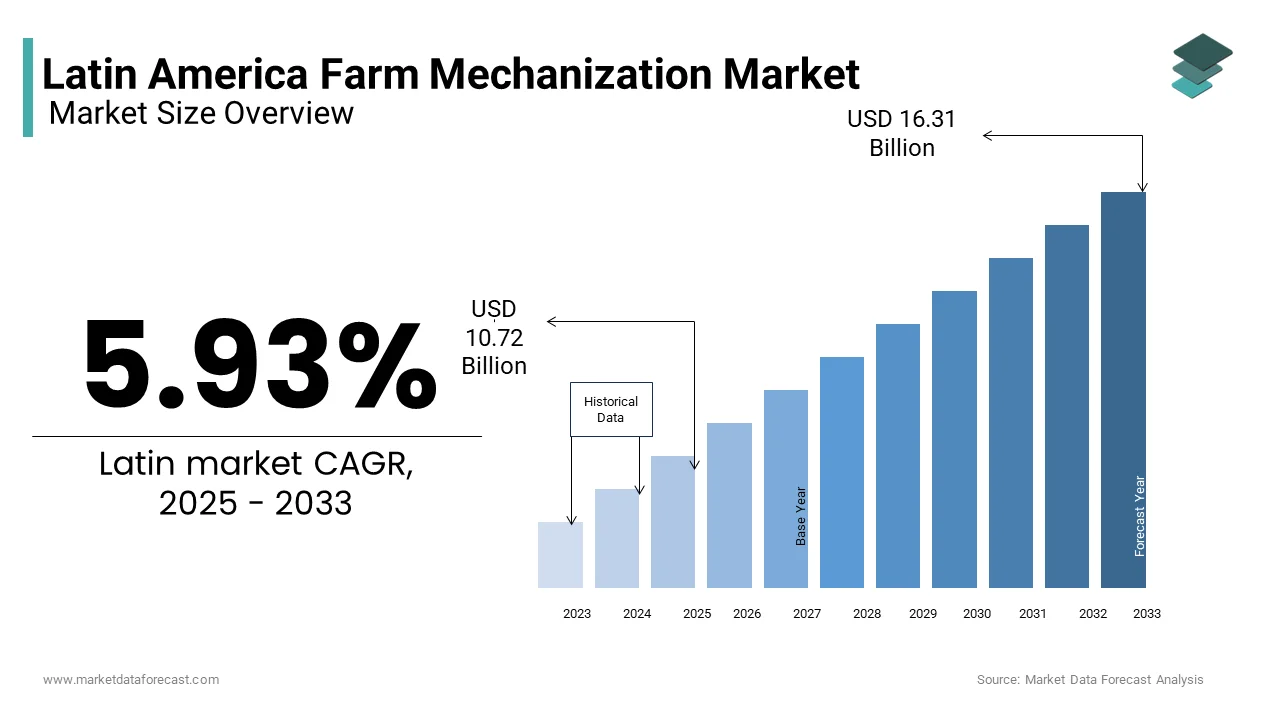

The Latin America farm mechanization market was valued at USD 10.17 billion in 2024, and is anticipated to reach USD 10.72 billion in 2025, to USD 16.31 billion by 2033, growing at a CAGR of 5.39% during the forecast period from 2025 to 2033.

Farm mechanization refers to the application of advanced machinery, automation technologies, and digital systems in agricultural operations to enhance productivity, reduce labor dependency, and improve sustainability. In Latin America, this sector is undergoing a transformation driven by rising demand for food security, increasing export-oriented agriculture, and growing awareness of precision farming practices.

According to the Food and Agriculture Organization (FAO), a large amount of arable land in Latin America is used for commercial agriculture, particularly in countries like Brazil, Argentina, and Paraguay. As per the Inter-American Development Bank (IDB), the region contributes nearly 25% of global soybean production, making it one of the world’s most important agricultural hubs. However, despite its vast potential, farm mechanization levels remain uneven across the region due to economic disparities and infrastructural limitations.

The adoption of modern farming equipment such as tractors, harvesters, and automated planting systems has been steadily increasing, especially among large-scale agribusinesses. Moreover, governments in several Latin American countries have introduced subsidies and financing programs to encourage farmers to transition from manual labor to mechanized operations.

So, the Latin America Farm Mechanization Market is poised for significant evolution. However, challenges related to affordability, access to credit, and rural infrastructure continue to influence the pace of adoption.

MARKET DRIVERS

Expansion of Commercial Agriculture and Export Demand

Expansion of large-scale commercial farming and rising global demand for agricultural exports are one of the primary drivers of the Latin America Farm Mechanization Market. Countries like Brazil, Argentina, and Paraguay are among the world’s top producers and exporters of soybeans, corn, coffee, and sugarcane. According to the United States Department of Agriculture (USDA), Brazil alone accounts for more than 40% of global soybean exports, necessitating efficient and scalable farming methods.

As global demand increases, traditional labor-intensive farming practices are proving inadequate to meet production targets. This has led large agribusinesses to invest heavily in mechanized solutions such as high-horsepower tractors, autonomous planters, and combine harvesters. The need to maintain competitiveness in international markets has further accelerated the adoption of precision agriculture tools that optimize yield and resource efficiency.

Moreover, multinational corporations operating in the region are integrating mechanization into their supply chains to ensure consistent output quality and cost-effectiveness. These factors contribute to the growing demand for advanced farm equipment across Latin America.

Technological Advancements and Digital Agriculture Adoption

The rapid integration of digital technologies into agricultural practices, including drones, IoT sensors, and AI-powered analytics, is another major driver of the Latin America Farm Mechanization Market. Also, internet penetration in rural areas of Latin America increased significantly between 2020 and 2023, enabling greater access to smart farming tools.

Brazil, in particular, has emerged as a leader in adopting precision agriculture technologies. According to Embrapa, Brazil’s agricultural research corporation, over 3 million hectares of farmland are now managed using satellite-guided systems, allowing for precise input application and improved crop management. Companies like John Deere and AGCO have expanded their digital platforms in the region, offering cloud-based farm planning and real-time field monitoring services.

Besides, startups focused on agritech innovation are gaining traction, supported by both private investment and government-backed initiatives. The use of unmanned aerial vehicles (UAVs) for crop spraying and soil analysis has become increasingly common, particularly in soybean and sugarcane plantations. These technological advancements are not only improving productivity but also reshaping the future of mechanized farming in Latin America.

MARKET RESTRAINTS

Limited Access to Financing and High Equipment Costs

Limited access to affordable financing remains a major barrier in Latin America, particularly for small and medium-sized farmers. According to the World Bank, less than 30% of smallholder farmers in the region have access to formal credit, restricting their ability to invest in modern agricultural machinery.

High initial costs associated with farm equipment further exacerbate this issue. Even used machinery imports often come with high maintenance and operational expenses.

In response, some governments have launched subsidy programs to support mechanization. For instance, Brazil’s PRONAF (National Program for Strengthening Family Agriculture) provides low-interest loans for small farmers, though coverage remains limited. Hence, until financial accessibility improves significantly, the widespread adoption of farm mechanization will remain constrained across much of Latin America.

Underdeveloped Rural Infrastructure and Connectivity Gaps

Lack of robust rural infrastructure and inconsistent digital connectivity a critical constraints affecting the growth of the Latin America Farm Mechanization Market. Many farms, particularly in remote regions of Bolivia, Peru, and parts of Colombia, lack reliable road networks, electricity supply, and internet access—key enablers for deploying and maintaining modern agricultural equipment.

As per the Economic Commission for Latin America and the Caribbean (ECLAC), a significant portion of rural households in the region do not have stable access to electricity, limiting the feasibility of electric-powered or digitally integrated farm machinery. Apart from these, poor mobile network coverage hampers the functionality of GPS-guided tractors and drone-based monitoring systems, which rely on continuous data transmission.

This infrastructure deficit also affects after-sales service availability. Spare parts distribution centers and technical support teams are often concentrated in urban areas, making repairs and maintenance difficult for rural users.

MARKET OPPORTUNITY

Government Initiatives and Subsidy Programs for Agricultural Modernization

The increasing number of government-led initiatives aimed at promoting agricultural modernization and mechanization presents a significant opportunity for the Latin American Farm Mechanization Market. Several countries have introduced policies and funding mechanisms designed to assist farmers in acquiring advanced machinery and adopting sustainable farming practices.

For example, Brazil’s PRONAF (National Program for Strengthening Family Agriculture) offers subsidized loans with favorable interest rates to small and mid-sized farmers seeking to purchase tractors, planters, and irrigation systems.

In addition, regional development banks such as the Inter-American Development Bank (IDB) have funded multiple projects supporting mechanization through grants and soft loans. These initiatives have contributed to a notable increase in machinery adoption in rural cooperatives and family-owned farms.

Growth of Agritech Startups and Local Manufacturing Hubs

The emergence of agritech startups and the development of localized manufacturing facilities are other promising opportunities for the Latin America Farm Mechanization Market. Over the past few years, there has been a surge in entrepreneurial activity focused on developing affordable, adaptable mechanized solutions tailored to the region’s diverse agricultural conditions.

Countries like Brazil and Mexico have seen a rise in domestic manufacturing units producing tractors, seeders, and post-harvest equipment, reducing reliance on expensive imports. According to the Latin American Agribusiness Development Corporation (LAAD), local production helps cut transportation costs and enables quicker delivery and after-sales service.

Simultaneously, agritech startups are introducing innovative products such as compact autonomous robots for weeding and spraying, mobile-based farm advisory apps, and drone-assisted crop monitoring. These companies are attracting venture capital investments and forming strategic partnerships with global machinery manufacturers to scale up operations.

This growing ecosystem of innovation and localization is expected to drive broader mechanization adoption across Latin America, particularly in smaller farms that were previously excluded due to cost barriers.

MARKET CHALLENGES

Fragmentation of Land Ownership and Diverse Farming Conditions

The fragmented nature of land ownership and highly variable farming conditions across the region are one of the key challenges facing the Latin America Farm Mechanization Market. Unlike North America and Europe, where large-scale commercial farms dominate, Latin America features a mix of vast agribusiness estates and numerous smallholder plots, each requiring different mechanization strategies.

According to the Food and Agriculture Organization (FAO), over 80% of farms in Latin America are classified as smallholding, covering less than five hectares of land. These farms often operate under diverse climatic, topographic, and soil conditions, making standardized mechanization solutions inefficient or impractical.

Furthermore, fragmented land holdings limit economies of scale, discouraging investment in high-cost machinery. Customized equipment that can function efficiently in small, irregularly shaped fields is still underdeveloped, posing a challenge for manufacturers aiming to cater to all segments of the agricultural sector.

Limited Technical Expertise and Training for Advanced Farming Equipment

The lack of technical expertise and training required to operate and maintain advanced agricultural equipment is another pressing challenge impacting the Latin American Farm Mechanization Market. While larger agribusinesses can afford specialized technicians, small and mid-sized farms often struggle with knowledge gaps related to digital farming tools, GPS-guided systems, and automated machinery.

This shortage of skilled labor results in lower efficiency and higher downtime, discouraging farmers from investing in mechanized solutions.

Further, equipment manufacturers face difficulties in establishing comprehensive after-sales support networks due to the region’s vast geographical spread and logistical complexities. Without adequate training and service infrastructure, even when farmers acquire new machinery, they may not be able to maximize its benefits.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.39% |

| Segments Covered | By Product, And By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Mexico, Argentina, Chile, Rest of Latin America |

| Market Leaders Profiled | John Deere, CNH Global, AGCO, Alamo Group, Kubota, International Harvester, TAFE, CLAAS, Mitsubishi. |

SEGMENTAL ANALYSIS

By Product Insights

The tractor segment dominated the market by accounting for 35.2% of total revenue in 2024. The expanding use of tractors in large-scale commercial farming operations, particularly in Brazil and Argentina, which are among the world’s top agricultural producers, is one key factor behind this dominance of the tractor segment. The adoption of high-horsepower tractors equipped with GPS-guided systems has further reinforced demand. Tractors serve as the backbone of mechanized agriculture across the region due to their versatility in performing multiple tasks such as plowing, planting, spraying, and hauling.

Moreover, government-backed financing programs have made tractor purchases more accessible to small and medium-sized farmers. These factors ensure that the tractor segment remains the largest and most influential within the Latin American farm mechanization landscape.

Power Tiller Market

The power tiller segment is projected to grow at the fastest rate and is likely to expand at a CAGR of 7.4% between 2025 and 2033. Increasing demand from smallholder farms, which constitute the majority of agricultural holdings across the region, is primarily driving the rapid growth of the power tiller segment. Power tillers offer an affordable and efficient alternative to traditional plowing methods, especially in countries like Colombia, Peru, and Ecuador, where small farms account for a majority of total agricultural units, as per the International Fund for Agricultural Development (IFAD) in 2023. These compact machines provide greater maneuverability in smaller plots and require less maintenance compared to larger tractors, making them highly suitable for fragmented land structures.

Moreover, rising investments in sustainable farming practices and government support through subsidies are accelerating adoption. In Mexico, for example, the SADER (Secretariat of Agriculture and Rural Development) introduced financial incentives for farmers purchasing eco-friendly power tillers, leading to a notable increase in sales.

COUNTRY ANALYSIS

Brazil

Brazil spearheaded the Latin American Farm Mechanization Market by contributing 45.5% of the total regional revenue in 2024. As one of the world’s top agricultural producers, Brazil manages over 60 million hectares of soybean cultivation alone, according to Embrapa, the country’s agricultural research corporation. This vast agricultural output necessitates advanced mechanization strategies to sustain efficiency and global competitiveness. A major driver behind Brazil’s strong market position is the widespread adoption of precision agriculture technologies supported by national initiatives such as the ABC Program (Low Carbon Agriculture) and PRONAF, which provides subsidized credit for small and mid-sized farmers. Also, over 60% of large-scale farms now use GPS-guided tractors and automated planting systems, enabling real-time decision-making and resource optimization. Besides, foreign investment in Brazilian agribusiness has surged, with companies like John Deere and AGCO expanding their local manufacturing and digital service offerings.

Mexico

Mexico is a significant player in the Latin American Farm Mechanization Market. As a key player in North American agricultural trade, Mexico produces significant volumes of corn, avocados, tomatoes, and chili peppers, cultivating over 23 million hectares of farmland, according to the Secretariat of Agriculture and Rural Development (SADER). A primary driver of mechanization in Mexico is the increasing need for labor-saving technologies due to urban migration and rising wages in rural areas. Apart from these, the USMCA trade agreement has encouraged higher export standards, pushing farmers toward automation to improve quality and consistency.

Moreover, government-backed modernization programs under SADER have facilitated access to financing for purchasing new machinery. The National Agricultural Modernization Program has provided low-interest loans and tax incentives for acquiring tractors, power tillers, and irrigation systems. These developments indicate a growing shift toward mechanized farming across Mexico’s diverse agricultural landscape.

Argentina

Argentina contributes a notable share to the Latin American Farm Machinery Market. Known for its vast production of soybeans, corn, wheat, and beef, Argentina manages over 35 million hectares of cultivated land, according to the Ministry of Agriculture, Livestock, and Fisheries. This extensive farmland requires efficient mechanization strategies to maintain high yields and meet international export demands.

A key driver behind Argentina’s growing mechanization trend is the expansion of large-scale agribusinesses that rely on high-efficiency machinery to optimize production. Further, labor shortages in rural areas have intensified the shift toward mechanization, particularly in Pampas provinceswheree seasonal worker availability has declined.

Furthermore, the government has introduced policies encouraging sustainable farming practices, including subsidies for eco-friendly machinery under the National Plan for Sustainable Agriculture. With increasing focus on climate resilience and productivity, Argentina continues to strengthen its role in the regional farm mechanization landscape.

Chile

Chile holds a notable share of the Latin American Farm Mechanization Market. Despite its relatively modest size compared to other regional markets, Chile plays a crucial role in global fruit exports, producing over 3 million tons of grapes, cherries, apples, and berries annually, according to the Agricultural Study Center (ODEPA). This high-value agricultural sector requires efficient and precise farming techniques to remain competitive. A primary driver of mechanization in Chile is the growing adoption of specialized equipment in vineyards and orchards, where manual labor is becoming harder to source. Moreover, water scarcity issues have led to increased deployment of mechanized drip irrigation and soil monitoring tools.

Moreover, the Chilean government supports innovation in agriculture through funding programs like CORFO’s AgriTech Initiative, which encourages startups and manufacturers to develop tailored mechanization solutions.

Rest of Latin America

The Rest of Latin America, which includes Colombia, Peru, Bolivia, Ecuador, and Central American nations, holds a considerable share of the regional farm mechanization market. While traditionally lagging behind larger economies like Brazil and Argentina, this segment is experiencing steady growth due to increasing awareness of mechanized farming benefits and supportive government policies.

Colombia and Peru, in particular, have seen a rise in mechanization adoption in coffee, cocoa, and banana production. As per FAO, over 90% of farms in these countries are classified as small-scale, requiring demand for cost-effective, easy-to-operate machinery.

Besides, regional trade agreements and foreign direct investment are facilitating easier access to imported agricultural equipment . Countries like Guatemala and Honduras are benefiting from cross-border partnerships that reduce import tariffs and expand distribution networks.

Top Players In The Market

John Deere

John Deere holds a dominant position in the Latin American farm Mechanization Market due to its strong brand reputation, extensive product range, and commitment to innovation. The company offers advanced tractors, harvesters, and precision agriculture tools tailored for large-scale commercial farms and smallholders alike. Its focus on digital integration, sustainability, and customer support has reinforced its leadership in the region. Globally, John Deere continues to set industry benchmarks by integrating AI, automation, and IoT into agricultural equipment, influencing mechanization trends worldwide.

CNH Industrial

CNH Industrial is a major player in Latin America through its well-established brands like Case IH and New Holland Agriculture. The company provides a wide array of farm machinery suited to diverse crops and field conditions across the region. CNH Industrial emphasizes technological advancement and after-sales service, ensuring high reliability and performance. Its global presence allows it to leverage economies of scale while adapting solutions to local farming needs, making it a key contributor to the expansion of mechanized agriculture in emerging markets.

AGCO Corporation

AGCO Corporation plays a strategic role in the Latin American market with its localized manufacturing units and partnerships aimed at improving accessibility for farmers. Through brands such as Fendt and Massey Ferguson, AGCO delivers high-performance machinery integrated with precision farming technologies. The company’s emphasis on sustainable agriculture and digital farming platforms strengthens its global influence and positions it as a forward-looking leader in the evolving farm mechanization landscape.

Top Strategies Used By Key Market Participants

Localization of Production and Distribution Networks

To better serve the diverse agricultural landscape of Latin America, leading players are establishing regional manufacturing hubs and expanding their dealer networks. This strategy enables faster delivery, cost-effective maintenance, and more responsive customer support tailored to local needs.

Investment in Digital Farming Solutions

Major companies are integrating digital technologies such as GPS guidance, telematics, and data analytics into their equipment. These innovations enhance productivity and resource efficiency, positioning firms at the forefront of smart and sustainable agriculture.

Strategic Partnerships with Local Institutions and Governments

Key players are forming alliances with research institutions, agritech startups, and national agricultural agencies to develop customized mechanization solutions. Collaborative efforts also include training programs and financing initiatives that facilitate wider adoption among small and mid-sized farmers.

COMPETITION OVERVIEW

The competition in the Latin American Farm Mechanization Market is shaped by a combination of global manufacturers, regional players, and emerging agritech firms. Established multinational corporations dominate the high-end segment with advanced machinery and digital solutions, while local brands and smaller manufacturers focus on affordability and adaptability to regional farming conditions. The market is highly fragmented due to the diversity of farm sizes, crop types, and economic conditions across countries.

Product differentiation is a key battleground, with companies investing in technology-driven features such as autonomous operation, fuel efficiency, and precision agriculture capabilities. Customer engagement strategies, including after-sales service, digital support, and farmer education programs, play a crucial role in building brand loyalty and trust.

Apart from these, regulatory influences and government policies significantly impact market dynamics, particularly in terms of subsidies, import tariffs, and environmental compliance. As demand for efficient and sustainable farming grows, competition is intensifying not only in terms of product innovation but also in financial accessibility and rural outreach, shaping the future trajectory of the Latin American farm mechanization sector.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, John Deere launched an updated version of its My John Deere platform tailored for Latin American farmers, offering real-time field monitoring, predictive maintenance alerts, and remote diagnostics to improve equipment uptime and operational efficiency.

- In May 2024, CNH Industrial announced a joint venture with a Brazilian agritech startup to develop AI-powered planting and harvesting solutions specifically designed for tropical climates and medium-sized farms across South America.

- In July 2024, G CO Corporation expanded its distribution network in Mexico by opening three new regional service centers aimed at enhancing after-sales support and reducing equipment downtime for farmers in key agricultural zones.

- In September 2024, Kubota Corporation introduced a new line of compact, fuel-efficient tractors in Argentina, targeting smallholder farmers and aligning with regional sustainability goals by incorporating low-emission engine technology.

- In November 2024, eere & Company partnered with a Brazilian renewable energy firm to power its manufacturing facility in Sorocaba using clean energy, reinforcing its sustainability commitments while strengthening its market presence in one of Latin America’s largest agricultural economies.

MARKET SEGMENTATION

This research report on the Latin America Farm Mechanization Market is segmented and sub-segmented into the following categories.

By Product

- Combine Harvester

- Tractor

- Rice Transplanter

- Power Tiller

- Land leveler

By Country

- Brazil

- Argentina

- Mexico

- Rest of Latin America

Frequently Asked Questions

What is farm mechanization?

Farm mechanization refers to the use of machinery and equipment to perform agricultural tasks such as planting, harvesting, irrigation, and soil preparation, reducing reliance on manual labor. It helps improve productivity, efficiency, and crop yields across different farm sizes.

Why is farm mechanization growing in Latin America?

The region is seeing increased adoption due to rising labor shortages, especially in rural areas, and a push toward more efficient and scalable farming practices. Additionally, government support and access to financing are helping farmers invest in modern equipment.

Which countries are leading the farm mechanization trend in Latin America?

Brazil and Argentina are at the forefront due to their large-scale commercial agriculture and well-established agribusiness sectors. Mexico and Colombia are also showing strong growth as small and medium-sized farms begin adopting mechanized solutions.

What types of machinery are most commonly used?

Tractors, harvesters, planters, and sprayers are among the most widely adopted machines in the region. There's also growing interest in precision agriculture tools like GPS-guided systems and drones for monitoring crop health.

How does farm mechanization benefit smallholder farmers?

Mechanization allows small-scale farmers to reduce physical labor, save time, and increase production capacity, helping them compete more effectively in local and international markets. It also supports better resource management and reduces post-harvest losses.

Are there challenges to adopting farm mechanization in the region?

Yes, high upfront costs, limited access to credit, and lack of technical knowledge can prevent many farmers from investing in new equipment. In some areas, poor infrastructure and difficult terrain also limit the use of large machinery.

How is technology influencing farm mechanization in Latin America?

Digital tools like IoT-enabled sensors, automated irrigation systems, and mobile-based farm management apps are being integrated with traditional machinery to enhance efficiency and decision-making. Startups and agtech firms are increasingly offering affordable digital solutions tailored for local farmers.

What role do government policies play in promoting farm mechanization?

Governments in countries like Brazil and Argentina offer subsidies, low-interest loans, and training programs to encourage farmers to adopt modern technologies. These initiatives aim to boost food production and make agriculture more sustainable and competitive globally.

Is there a shift toward sustainable and eco-friendly farm equipment?

Yes, there’s growing interest in energy-efficient and low-emission machinery, including electric tractors and solar-powered irrigation systems. Farmers and policymakers are becoming more aware of environmental impacts, driving innovation and investment in greener alternatives.

What is the future outlook for the Latin America farm mechanization market?

The market is expected to grow steadily over the next decade, supported by technological advancements, increasing demand for food, and expanding access to financing and training. Analysts project a moderate but consistent rise in adoption, particularly among mid-sized farms.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com