Latin America Medical Device Technologies Market Research Report By Device Type, Technology and Country (Mexico, Brazil, Argentina, Chile and Rest of Latin America) – Analysis on Size, Share, Trends, and Growth Forecast from 2025 to 2033

Latin America Medical Device Technologies Market Summary

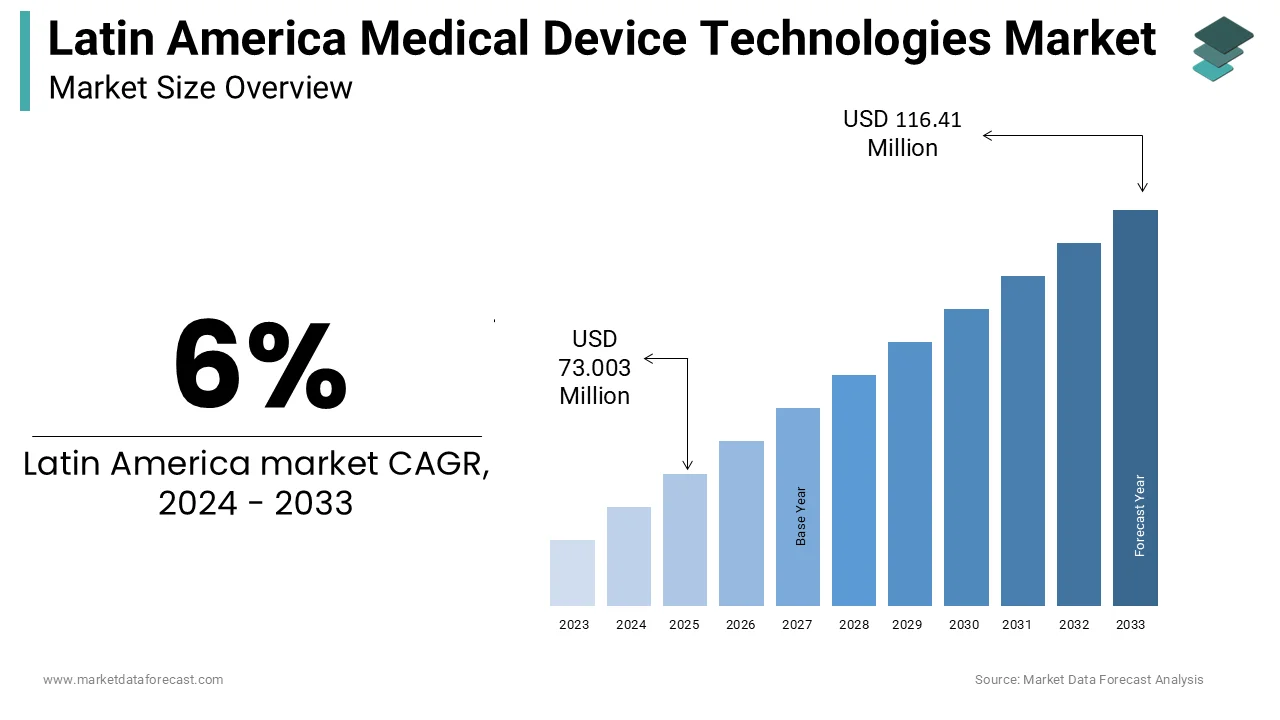

The Latin America Medical Device Technologies Market size was valued at USD 68.9 million in 2024 and is anticipated to reach USD 116.41 million by 2033, growing at a CAGR of 6% from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- Latin America dominated the global market with a largest share in 2024.

- Latin America is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 6%.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 68.9 million

- 2033 Projected Market Size: USD 116.41million

- CAGR (2024–2033): 6%

- Latin America: Largest market in 2024

- Latin America: Fastest-growing region

Latin America Medical Device Technologies Market Size

The Latin America medical device technologies market size was valued at USD 68.9 million in 2024 and is predicted to be worth USD 116.41 million by 2033 from USD 73.003 million in 2025, growing at a CAGR of 6% during the forecast period.

Medical Device Technologies are diagnostic, therapeutic, and monitoring equipment, ranging from imaging systems and cardiovascular implants to point-of-care testing devices and digital health platforms, integrated into clinical workflows across public and private healthcare institutions. This domain is transforming due to rising non-communicable disease burdens, incremental expansion of health infrastructure, and growing demand for precision interventions. According to the Pan American Health Organization, over 72% of deaths in Latin America are attributed to chronic conditions such as diabetes, cardiovascular disease, and cancer, necessitating advanced technological support for early diagnosis and management. As per the study, Brazil performs hundreds of thousands of surgeries requiring implantable devices annually, and the use of diagnostic imaging is increasing in Mexico. Despite disparities in access, technological adoption is accelerating in urban centers, driven by regulatory modernization and increasing physician reliance on data-driven tools for patient care.

MARKET DRIVERS

Expanding Burden of Cardiovascular and Metabolic Diseases

The escalating prevalence of cardiovascular and metabolic disorders is a primary catalyst for medical device demand across Latin America. As per the Latin American Society of Hypertension, hypertension affects nearly 35% of adults in the region, with control rates below 30% in countries like Argentina and Colombia. The Interheart Latin America Study found that over 80% of myocardial infarction cases are linked to modifiable risk factors, necessitating widespread use of diagnostic tools such as echocardiography, ambulatory blood pressure monitors, and cardiac stents. Diabetes further amplifies demand: the International Diabetes Federation points out that approximately 49 million adults in Latin America live with diabetes, a figure projected to rise to 62 million by 2030. This has spurred the adoption of glucose monitoring systems, insulin delivery devices, and vascular screening tools. In Brazil, a large number of glucometers are distributed through the national diabetes program. These epidemiological trends are compelling healthcare systems to invest in scalable, technologically advanced devices to manage long-term complications and reduce hospitalization burdens.

Increasing Adoption of Minimally Invasive Surgical Techniques

Minimally invasive surgery (MIS) is gaining traction across major hospitals in Latin America, significantly influencing the demand for laparoscopic instruments, robotic-assisted systems, and high-resolution visualization technologies. According to the research, Laparoscopic procedures have increased significantly in Brazil. As per the study, minimally invasive gynecological surgeries are increasing in Chile. Argentina has seen growing integration of robotic platforms in urological and oncological procedures, with several robotic surgeries conducted, as per the Argentine Association of Robotic Surgery. Public-private partnerships in Peru and Colombia are funding training programs for surgeons in MIS techniques, enhancing procedural capacity. The shift away from open surgery is not only improving clinical outcomes but also creating sustained demand for advanced surgical instrumentation, navigation systems, and integrated operating room technologies.

MARKET RESTRAINTS

Fragmented Regulatory Frameworks Across Countries

The lack of harmonized regulatory systems, leading to prolonged approval timelines and inconsistent product availability, is a critical restraint on the Latin American medical device market. While countries like Brazil and Argentina have well-established but complex regulatory bodies, ANVISA and ANMAT, respectively, others, such as Bolivia and Paraguay, lack dedicated medical device legislation, relying on ad hoc import approvals. According to the research, device registration in Brazil can take several months, compared to that in the United States or the European Union. As per a study, only a portion of Class III devices submitted in Peru received approval within a few months, largely due to documentation inconsistencies and inspector shortages. This regulatory fragmentation discourages multinational companies from launching innovative technologies in smaller markets and fosters reliance on outdated or second-hand equipment. The absence of a regional mutual recognition agreement further impedes equitable access and delays the diffusion of life-saving technologies across borders.

Limited Reimbursement Coverage and Public Funding Constraints

Public healthcare systems in Latin America face severe financial limitations, resulting in restricted reimbursement for advanced medical devices and uneven access across socioeconomic groups. As per the Inter-American Development Bank, public health expenditure averages only 3.8% of GDP in Latin America, well below the OECD average of 6.4%. Public insurance coverage for high-cost cardiovascular devices in Mexico is limited, according to the research. Colombia’s EPS system frequently denies coverage for high-cost devices such as drug-eluting stents or implantable cardioverter-defibrillators without prior authorization. Also, budget-related procurement delays occur in Chilean public hospitals. These fiscal constraints deter investment in new technologies and limit the adoption of next-generation devices, particularly in rural and underserved areas, where infrastructure and funding gaps are most pronounced.

MARKET OPPORTUNITIES

Integration of Telemedicine and Remote Monitoring Devices

The rapid expansion of telehealth infrastructure is creating a fertile ground for remote diagnostic and monitoring devices, particularly in geographically dispersed regions. Following the pandemic, telemedicine consultations in Latin America increased notably between 2020 and 2023, as per the study. This shift has accelerated demand for connected devices such as Bluetooth-enabled blood pressure cuffs, ECG patches, and portable ultrasound systems. In Brazil, it has expanded remote monitoring into its SUS Digital initiative, deploying several telehealth kits to primary care units. Besides, Colombia is advancing telemonitoring via Ruta Digital. Companies have launched region-specific tele-ultrasound carts for maternal and cardiac screening in rural clinics. These developments are enabling real-time diagnostics in remote communities, reducing referral burdens, and expanding the utility of medical device technologies beyond urban hospitals.

Growth of Medical Tourism and Private Healthcare Hubs

Several Latin American countries are positioning themselves as regional centers for advanced medical care, attracting patients from within and outside the continent and driving investment in cutting-edge medical technologies. According to the research, Latin America receives hundreds of thousands of medical tourists, with common procedures including cardiac, orthopedic, and bariatric care. Costa Rica and Mexico are leading destinations, with private hospitals in Guadalajara and San José equipped with hybrid operating rooms, intraoperative MRI, and robotic surgery systems. As per the study, accredited facilities in the country invested a substantial amount in new medical equipment between 2021 and 2023. Similarly, Bogotá and Medellín in Colombia have developed specialized health parks integrating diagnostics, surgery, and rehabilitation under one ecosystem. These high-end facilities procure premium devices from global manufacturers, creating a niche but influential segment that accelerates technology diffusion and sets new standards for clinical excellence across the region.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Import Dependence

Most Latin American countries rely heavily on imported medical devices, making them susceptible to global supply disruptions, currency fluctuations, and logistical bottlenecks. As per the study, many high-complexity devices used in the region are imported from the United States, Germany, and China. During the pandemic, shipment delays led to critical shortages of ventilators and infusion pumps, and device imports in Peru were affected. Argentina experienced an increase in device procurement costs due to peso depreciation against the dollar, limiting purchasing power. Additionally, inadequate cold chains and last-mile distribution networks hinder the deployment of sensitive technologies in remote areas. These systemic vulnerabilities compromise continuity of care and deter long-term planning, particularly in public procurement, where budget cycles and import licensing delays compound logistical inefficiencies.

Workforce Shortages in Clinical Engineering and Technical Support

A persistent shortage of trained biomedical engineers and technical service personnel impedes the effective deployment and maintenance of advanced medical devices. According to the research, there is a shortage of clinical engineers in Latin America. In Ecuador, a portion of imaging equipment in public hospitals was non-functional due to a lack of maintenance. Brazil points out a deficit of qualified technicians nationwide. This gap results in prolonged downtime, improper calibration, and increased risk of device-related errors. Training programs are limited and often concentrated in urban centers, leaving rural facilities underserved. Without a robust technical workforce, even the most sophisticated technologies cannot achieve optimal performance, undermining return on investment and constraining the scalability of modern medical device integration across the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6 % |

| Segments Analysed | By Device Type, Technology, and Country |

| Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Countries Analysed | Mexico, Brazil, Argentina, Chile, Peruu anthe d the Rest of Latin America |

| Market Leaders Profiled | Abbott Laboratories, Inc., Becton, Dickinson and Company, GE Healthcare, Novartis Diagnostics |

SEGMENTAL ANALYSIS

By Device Type Insights

The Diagnostic Imaging Devices segment held the largest share of the Latin America medical device market at 23.3% of total revenue in 2024. This dominance is primarily driven by the escalating demand for early and accurate disease detection amid rising burdens of cancer, cardiovascular conditions, and neurological disorders. According to research, there has been a high number of cancer cases diagnosed, necessitating widespread use of CT, MRI, and ultrasound for staging and treatment planning. As per the study, public hospitals in Buenos Aires perform thousands of imaging procedures per month, with an annual increase in demand over the past five years. Additionally, technological modernization in public health systems has prioritized the procurement of digital radiography and mobile imaging units for rural areas. The integration of AI-powered image analysis tools in private clinics further enhances diagnostic precision, reinforcing investment in advanced imaging infrastructure across major urban centers.

In contrast, the Diabetes Care Devices segment is the fastest-growing and is projected to expand at a CAGR of 14.7% from 2025 to 2033. This surge is fueled by the explosive rise in diabetes prevalence and the shift toward patient-centric, self-managed care models. As per the Latin American IDF Atlas, over 50 million adults in the region live with diabetes, with undiagnosed cases exceeding 30% in countries like Peru and Bolivia. Like, Brazil conducts large-scale distribution of diabetes monitoring supplies. Continuous glucose monitoring (CGM) adoption is accelerating in private healthcare: a study found that CGM use among type 1 patients in São Paulo increased since 2020. Furthermore, Chile and Colombia are expanding coverage and telehealth integration. These factors, combined with rising obesity rates and urban sedentary lifestyles, are driving sustained demand for next-generation glucose monitors, insulin pumps, and connected diabetes management systems.

By Technology Insights

The Biomarkers segment led by representing 38.7% of the technology-based medical device market in Latin America in 2024. This position is due to the increasing integration of biomarker-driven diagnostics in oncology, cardiology, and autoimmune disease management. Cardiac biomarkers such as troponin and BNP are routinely used in emergency departments to rule in or out myocardial infarction. Point-of-care cardiac biomarker testing is widespread in Brazilian tertiary hospitals. In oncology, HER2, PD-L1, and BRCA testing guide targeted therapies, particularly in breast and ovarian cancers. Argentina’s National Administration of Drugs, Foods, and Medical Devices (ANMAT) approved many biomarker-based companion diagnostics between 2020 and 2023, reflecting regulatory recognition. Additionally, the expansion of centralized laboratories like Grupo Leforte in Brazil and Clínica Alemana in Chile has enabled high-throughput biomarker analysis, improving turnaround times. The clinical utility of biomarkers in risk stratification, treatment selection, and monitoring makes them a foundational component of modern precision medicine infrastructure across the region.

Conversely, the Molecular Diagnostics segment is the fastest-growing technology and is anticipated to grow at a CAGR of 16.3% through 2033. This rapid expansion is driven by the post-pandemic institutionalization of PCR and next-generation sequencing (NGS) platforms in public health systems. Brazil greatly expanded molecular labs during the pandemic. Colombia has a molecular network for infectious diseases. In cancer care, NGS panels are increasingly used in academic centers like Mexico’s Instituto Nacional de Cancerología to identify actionable mutations in lung and colorectal cancers. Chile has integrated liquid biopsy-based molecular testing into its national lung cancer guidelines, enabling non-invasive EGFR monitoring. With sustained investment in genomic surveillance and antimicrobial resistance tracking, molecular diagnostics is transitioning from emergency response to routine clinical utility, catalyzing long-term market growth.

COUNTRY LEVEL ANALYSIS

Brazil Medical Device Technologies Market Insights

Brazil held the largest share of the regional medical device market at 41.6% in 2024. The country’s position is anchored in its expansive public health system (SUS), large population, and growing private healthcare sector. SUS covers Brazil’s entire population (around 213 million in 2023), and central procurement mechanisms for medical devices are standard practice. It allocatea d substantial amount for equipment procurement, with significant investments in imaging, dialysis, and surgical technologies. ANVISA has streamlined regulatory pathways for high-risk devices, reducing approval times. Private hospitals in São Paulo and Rio de Janeiro are adopting robotic surgery and hybrid operating rooms, often serving as regional training hubs. Additionally, MedTech innovation is rising in technology parks like Campinas and Belo Horizonte, supported by FINEP and BNDES funding. Despite fiscal constraints, Brazil remains the primary entry point for multinational device manufacturers due to its scale and institutional infrastructure.

Mexico Medical Device Technologies Market Insights

Mexico ranks second with a significant market share. The country has emerged as a strategic manufacturing and distribution hub, hostingseveralf medical device production facilities, primarily in Baja California and Jalisco, as per the study. Its proximity to the U.S. and participation in USMCA facilitate export-oriented production, while domestic demand is driven by rising chronic disease prevalence and medical tourism. The federal government’s Instituto de Salud para el Bienestar (INSABI) and IMSS-Bienestar have expanded access to diagnostics and implants in rural areas, procuring a large number of pieces of medical equipment. Private hospitals in Monterrey and Mexico City are integrating AI-driven diagnostics and tele-ultrasound, enhancing service differentiation. With regulatory convergence efforts underway with the U.S. FDA, Mexico is positioning itself as a technologically advanced and operationally resilient market.

KEY MARKET PLAYERS

Companies that play a noteworthy role in the Latin America medical device technologies market profiled in the report are Abbott Laboratories, Inc., Becton, Dickinson and Company, GE Healthcare, Novartis Diagnostics, bioMerieux, Inc., Biomerica, Inc., Johnson and Johnson Diagnostics, Inc., Olympus Corporation, Qiagen N.V., Siemens AG, Thermo Fischer Scientific, Inc., and Zenith Healthcare Ltd.

TOP LEADING PLAYERS IN THE MARKET

Medtronic

Medtronic maintains a substantial presence in the Latin America Medical Device Technologies Market through its comprehensive portfolio of cardiovascular, diabetes, and surgical technologies. The company has deepened its regional integration by establishing clinical training centers in Mexico City, São Paulo, and Bogotá, where physicians receive hands-on instruction on minimally invasive devices and implantable systems. It also launched its Hugo robotic-assisted surgery system in Chile and Colombia, positioning itself at the forefront of surgical automation. Through localized service networks and Spanish- and Portuguese-language digital support platforms, Medtronic ensures post-deployment reliability. Additionally, the company collaborates with academic institutions on real-world evidence studies, reinforcing clinical trust and facilitating regulatory acceptance of next-generation technologies across diverse healthcare settings.

GE Healthcare

GE Healthcare plays a pivotal role in advancing diagnostic imaging and digital infrastructure across Latin America, with a strong footprint in hospitals, imaging centers, and primary care networks. The company has tailored its Edison AI-powered imaging platforms for regional use, integrating them into public health systems in Peru and Argentina to improve radiology workflow efficiency. It also launched its APM (Asset Performance Management) platform in Brazil, enabling predictive maintenance for MRI and CT scanners, reducing downtime in under-resourced facilities. The company collaborates with local governments on equipment modernization initiatives and supports training for biomedical technicians through its Edison Academy. By combining hardware innovation with data-driven service models, GE Healthcare is strengthening healthcare system resilience and enabling scalable, sustainable technology adoption across the region.

Siemens Healthineers

Siemens Healthineers has solidified its influence in Latin America through strategic investments in high-end imaging, laboratory diagnostics, and integrated digital health ecosystems. The company’s Magnetom MRI and Somatom CT systems are widely installed in leading hospitals across Argentina, Chile, and Colombia, supported by a regional network of service engineers and remote diagnostics. It also expanded its Atellica VACS automated lab solutions in Mexico, enhancing throughput for blood tests and biomarker analysis. The company actively engages in public-private partnerships, such as its collaboration with Peru’s Ministry of Health to modernize oncology diagnostics in regional cancer centers. By emphasizing operational efficiency, precision diagnostics, and long-term service contracts, Siemens Healthineers is shaping the evolution of technologically advanced, data-integrated care delivery in Latin America.

TOP STRATEGIES USED BY THE KEY MARKET PARTICIPANTS

Key players in the Latin America Medical Device Technologies Market are leveraging localized regulatory navigation, public sector engagement, service ecosystem development, technology adaptation for resource-limited settings, and strategic partnerships with healthcare providers to consolidate their presence. Companies are investing in regional regulatory teams to expedite ANVISA, ANMAT, and COFEPRIS approvals, reducing time-to-market. Expanding clinical training programs and biomedical support networks ensures device usability and longevity, particularly in remote areas. Firms are also adapting high-end technologies—such as portable imaging and AI-enabled diagnostics—for decentralized care models. Collaborations with ministries of health and social security institutions facilitate large-scale procurement and integration into public systems. Additionally, digital platforms for remote monitoring, predictive maintenance, and data analytics are being deployed to enhance value beyond hardware, differentiating offerings in a competitive and cost-sensitive environment.

COMPETITION OVERVIEW

The competition in the Latin America Medical Device Technologies Market is intensifying as global leaders and regional players navigate a complex landscape marked by economic volatility, regulatory diversity, and uneven healthcare access. Multinational corporations dominate high-complexity segments such as imaging, cardiovascular implants, and robotic surgery, leveraging brand trust, clinical evidence, and service infrastructure. However, local distributors and emerging manufacturers are gaining ground in mid-tier devices by offering cost-optimized solutions and faster technical response times. The market is increasingly shaped by procurement models, with public tenders favoring price competitiveness while private hospitals prioritize innovation and integration. Digital health capabilities, post-sales support, and training programs have become critical differentiators. As countries modernize health infrastructure and expand insurance coverage, the competitive edge lies in balancing technological sophistication with affordability, adaptability, and long-term system integration across fragmented healthcare ecosystems.

MARKET SEGMENTATION

This research report on the Latin America medical device technologies market has been segmented and sub-segmented into the following categories.

By Device Type

- Electromedical Equipment

- Irradiation Apparatus

- Dental Apparatus

- In Vitro Diagnostics (IVD) Devices

- Kidney/Dialysis Devices

- Diagnostic Imaging Devices

- Ophthalmology Devices

- Orthopedic Devices

- Endoscopy Devices

- Diabetes Care Devices

- Anesthesia & Respiratory Care Devices

- Wound Management Devices

By Technology

- Biomarkers

- Bio Implants

- Molecular Diagnostics

By Country

- Mexico

- Brazil

- Argentina

- Chile

- Rest of Latin America

Frequently Asked Questions

1. Which countries in Latin America are the largest markets for medical devices?

The top markets are: Brazil (largest) Mexico Argentina Colombia Chile

2. Is there a trend toward local manufacturing in Latin America?

Yes. Governments are encouraging local production to reduce dependence on imports, particularly in Brazil and Mexico, through tax incentives and partnerships.

3. What role do international companies play in the Latin American market?

Multinational corporations dominate, particularly in high-end device categories. They often partner with local distributors or establish local subsidiaries to navigate regulations and logistics.

4. What role does telemedicine play in the Latin America Medical Device Technologies Market?

Telemedicine has accelerated care access, especially remote diagnostics and monitoring, within the Latin America Medical Device Technologies Market.

5. What device types have the highest demand in the Latin America Medical Device Technologies Market?

Diagnostic imaging, wearable monitors, and surgical tools dominate demand in the Latin America Medical Device Technologies Market for better chronic disease management.

6. How is artificial intelligence used in the Latin America Medical Device Technologies Market?

Artificial intelligence enhances diagnostics, automates workflows, and improves clinical outcomes in the Latin America Medical Device Technologies Market.

7. What are the biggest challenges facing the Latin America Medical Device Technologies Market?

Regulatory complexity, digital infrastructure gaps, and high device costs are critical challenges in the Latin America Medical Device Technologies Market

8. How has COVID-19 impacted the Latin America Medical Device Technologies Market?

The pandemic increased demand for remote monitoring and digital health in the Latin America Medical Device Technologies Market but also revealed supply and logistics challenges.

9. What trends are shaping future demand in the Latin America Medical Device Technologies Market?

Key trends include expansion of telehealth, focus on affordable innovation, and rising investment in digital health across the Latin America Medical Device Technologies Market.

10. Are local manufacturers significant in the Latin America Medical Device Technologies Market?

Local manufacturers are growing in importance, backed by government incentives and partnerships in the Latin America Medical Device Technologies Market.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com