Latin America Medicated Feed Additives Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Type, Livestock, Mixture Type, And By Region (Brazil, Mexico, Argentina), Industry Analysis From (2025 to 2033)

Latin America Medicated Feed Additives Market Size

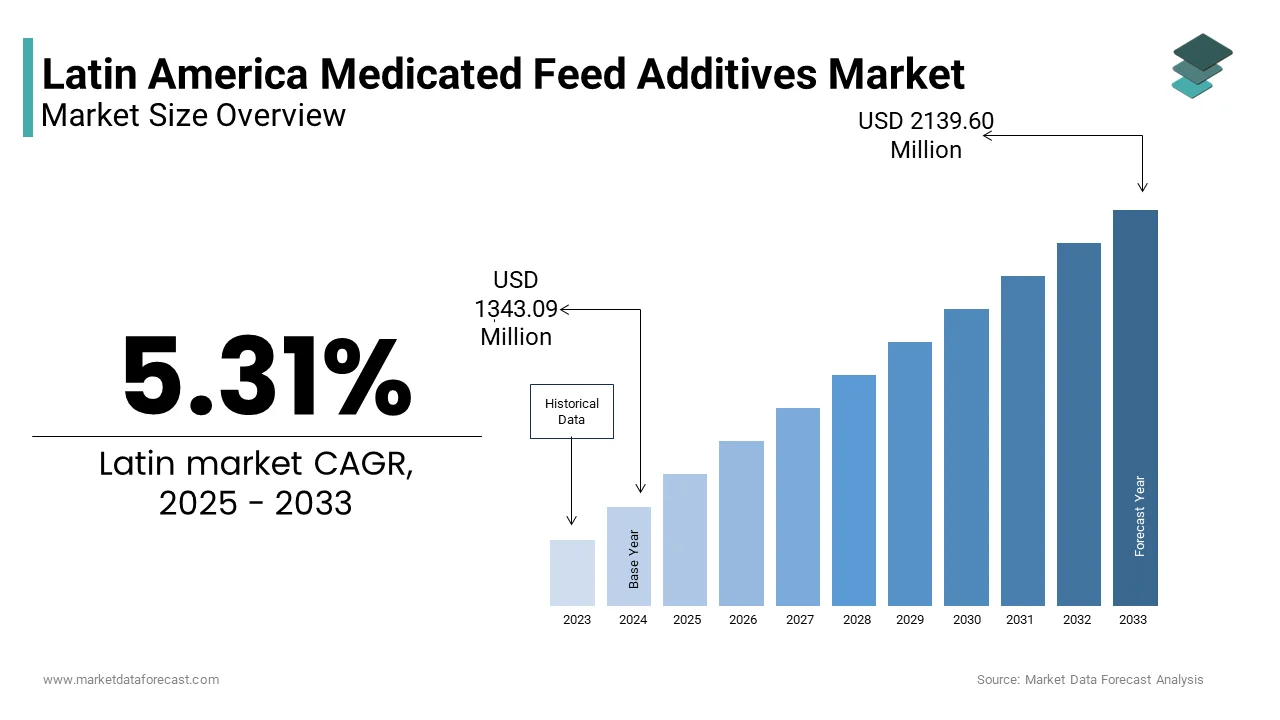

The Latin America medicated feed additives market size was valued at USD 1343.09 million in 2024 and is anticipated to reach USD 1414.41 million in 2025 and USD 2139.60 million by 2033, growing at a CAGR of 5.31% during the forecast period from 2025 to 2033.

Medicated feed additives are substances (vitamins, minerals, antibiotics, probiotics, etc.) mixed into animal feed to improve health, boost growth, and prevent/treat diseases in livestock (poultry, swine, cattle, aquaculture) on a large scale. These additives include antibiotics, anticoccidials, probiotics, enzymes, and other bioactive substances incorporated into animal feed formulations to optimize nutritional efficiency and combat pathogenic microorganisms. The integration of medicated feed additives has become essential for maintaining productivity standards in intensive farming operations across Brazil, Argentina, and Mexico, where commercial livestock operations increasingly adopt standardized feeding protocols. As per research, the strategic use of medicated feed additives can improve feed conversion ratios while reducing mortality rates in commercial poultry operations. The regulatory framework governing these additives varies significantly across Latin American countries, with Brazil's Ministry of Agriculture establishing comprehensive guidelines through its National Health Program for Animal Health Surveillance. The market's evolution reflects broader trends in agricultural modernization, where scientific approaches to animal nutrition replace traditional feeding practices, positioning medicated feed additives as indispensable tools for sustainable livestock production in the region.

MARKET DRIVERS

Expanding Livestock Production and Intensification of Farming Practices

The rapid expansion of livestock production across the region accelerates the growth of the Latin American medicated feed additives market. This is because commercial operations are increasingly adopting intensive farming methods to meet growing protein consumption demands. Latin America is experiencing growth in its meat production. One major country in the region has become a significant global beef exporter, while another is a key producer of pork. The intensification of meat production practices often involves the use of medicated feed additives to help prevent disease and support animal growth in confined operations. For example, the livestock sector in one large country manages a vast number of cattle in feedlot systems, where continuous treatment through medicated feed may be used to help prevent various health issues. In other regional countries, such as Argentina and Mexico, growth in livestock operations and poultry production correlates with the use of such feed additives. These additives are seen as playing a role in managing animal health and potentially reducing pathogen transmission concerns. Furthermore, the economic benefits of using medicated feed additives are substantial. This economic incentive, combined with increasing consumer demand for affordable protein sources, continues to drive the expansion of medicated feed additive usage throughout Latin America's growing livestock sector.

Rising Awareness of Animal Health Management and Disease Prevention

Regional livestock producers are increasingly recognizing that the economic benefits of proactive animal health management have boosted the expansion of the Latin American medicated feed additives market. This growing recognition has significantly accelerated demand for medicated feed additives as preventive healthcare tools rather than reactive treatment measures. According to sources, veterinary consultation rates among commercial livestock producers in the region have increased over the years, indicating heightened awareness of professional animal health management practices. This shift in mindset has led to widespread adoption of medicated feed additives as routine components of feeding protocols, particularly in large-scale operations where disease outbreaks can result in catastrophic financial losses. A majority of commercial poultry producers have adopted continuous anticoccidial programs as a standard part of their feeding strategies. The use of antibiotics in meat production has decreased, a change observed after the introduction of strategic medicated feed additive programs designed to optimize drug delivery. Producers implementing comprehensive medicated feed additive programs have experienced lower mortality rates and better feed conversion efficiency compared to those who rely only on therapeutic interventions. The rise of producer education programs and extension services throughout the region has further accelerated this trend, with agricultural universities and government agencies promoting evidence-based animal health management practices. Additionally, the increasing availability of technical support from feed additive manufacturers has enabled smaller producers to access professional-grade health management solutions, democratizing the benefits of medicated feed additives across various operation scales and contributing to overall market growth.

MARKET RESTRAINTS

Stringent Regulatory Frameworks and Compliance Requirements

The implementation of increasingly stringent regulatory frameworks governing medicated feed additives across the regional countries are major operational barrier for market participants, which further restricts the growth of the Latin America medicated feed additives market. These frameworks also create financial challenges. Moreover, these frameworks create barriers to market entry and product registration that can delay commercialization by several years. Regulatory approval processes for new medicated feed additives in Brazil typically span a period of several months. Approval timelines in Argentina are influenced by the requirement for comprehensive environmental impact assessments. These regulatory complexities are compounded by varying standards across different countries within the region, forcing manufacturers to navigate multiple approval processes and maintain separate compliance documentation for each market. Mexico’s Federal Commission for the Protection against Sanitary Risk enforces manufacturing standards that require facility improvements for international companies entering the market. The Brazilian Ministry of Agriculture requires periodic re-evaluations of approved additives, which involve the submission of updated safety documentation. Regulatory compliance represents a portion of the total operational expenses for feed additive companies maintaining a presence in multiple Latin American countries. Additionally, the region's evolving antimicrobial resistance policies have introduced new restrictions on certain antibiotic classes, forcing manufacturers to reformulate existing products or develop alternative solutions. The European Union's influence on regional regulatory standards through trade agreements has further complicated compliance requirements.

Concerns Regarding Antimicrobial Resistance and Regulatory Pressure

Growing international concerns regarding antimicrobial resistance have prompted regional governments to implement restrictive policies on medicated feed additive usage, particularly antibiotics, which in turn obstructs the expansion of the Latin AAmericanmedicated feed additives market. These policies are creating significant market constraints that threaten traditional product categories and force costly reformulation efforts. Latin America exhibits high rates of antimicrobial resistance in food-producing animals, particularly within poultry production. Regulatory bodies have responded to resistance trends by banning specific antibiotics in animal feed and restricting others to therapeutic use. Regional health programs are implementing phased reductions of approved antibiotic feed additives. Veterinary antibiotic consumption in livestock feed is decreasing across the region due to regulatory shifts and evolving prescribing practices. Producers face increased operational costs when replacing traditional antibiotic additives with alternative growth promoters. Economic pressures associated with alternative additives may limit the adoption of new practices among smaller operations. International trade pressures, particularly from the European Union and the United States, have intensified these regulatory trends, with export-certified livestock operations required to demonstrate reduced antimicrobial usage through comprehensive monitoring programs. These developments force manufacturers to invest heavily in research and development of alternative solutions while navigating complex regulatory transitions that can impact market stability and profitability.

MARKET OPPORTUNITY

Development of Natural and Organic Feed Additive Alternatives

The growing consumer demand for antibiotic-free and naturally-produced animal protein products opens new growth opportunities for natural and organic feed additive alternatives, which is expected to drive forward the Latin America medicated feed additives market. This demand is driving innovation in plant-based antimicrobials, probiotics, and enzyme technologies. According to the Organic Trade Association, organic meat consumption in Latin America has increased over the years. This consumer trend has prompted major livestock producers to seek certified organic feed additive solutions that maintain production efficiency while meeting organic certification requirements. The organic poultry sector is expanding, creating a need for organic-approved feed additives to replace conventional antibiotic growth promoters. Plant-based feed additives that include essential oils and botanical extracts show effectiveness in managing common health challenges in organic poultry production. A range of natural feed additives is recognized for use in certified organic livestock production, establishing clear pathways for product acceptance in the market. Additionally, the premium pricing associated with organic and antibiotic-free meat products creates economic incentives for producers to adopt alternative feed additive technologies. Government support programs throughout the region, including subsidies for organic certification and technical assistance for alternative production methods, further accelerate market adoption of natural feed additive solutions.

Expansion in Aquaculture Feed Additive Applications

The expansion of fish and shrimp farming in the region creates potential for the expansion of the Latin American medicated feed additives market. These additives are essential for managing unique aquatic pathogen challenges and improving production efficiency. Aquaculture production in Latin America has experienced substantial expansion, increasing the need for specific feed additives designed for aquatic environments. This growth includes some countries becoming major global producers of salmon and shrimp. The expansion of this sector has driven demand for medicated feed additives to manage common issues like bacterial infections, parasitic infestations, and nutritional deficiencies that occur in intensive farming systems. For example, Brazil's aquaculture sector, which yields over a million tons of fish annually, requires specialized feed additives capable of maintaining their therapeutic effectiveness through aquatic processing conditions. Medicated feed additive usage in Latin American aquaculture has generally increased, showing faster growth compared to its application in farming land-based livestock. The shrimp farming industry in Mexico is another example that depends on the use of medicated feed additives to help prevent serious aquatic diseases. The technical challenges associated with aquatic feed manufacturing, including water stability requirements and precise dosing capabilities, create opportunities for specialized manufacturers with expertise in marine applications. Additionally, the premium value of aquaculture products compared to traditional livestock creates willingness among producers to invest in advanced feed additive technologies that can improve survival rates and product quality, supporting sustained market growth.

MARKET CHALLENGES

Limited Technical Expertise and Veterinary Support Infrastructure

The inadequate availability of specialized technical expertise and veterinary support infrastructure throughout many Latin American regions creates significant operational challenges. This situation hinders effective medicated feed additive implementation, limits optimal product usage, and constrains market expansion in rural and remote production areas. Latin America experiences a shortage in its veterinary workforce, particularly within rural sectors. Specialized animal health professionals available toguiden medicated feed additive applications are limited in number. The deficiency of veterinary personnel is notably present in Central American countries and the Andean regions. The ratio of veterinarians to livestock units in these areas remains below international benchmarks. Inconsistent dosage and application timing of medicated feed additives contribute to treatment failures in small-scale operations. Improper application of these additives leads to regional economic losses. The limited continuing education opportunities for rural veterinarians further exacerbate knowledge gaps regarding new product developments and regulatory changes. Additionally, the absence of comprehensive diagnostic laboratory networks in many regions prevents accurate identification of pathogenic conditions, leading to inappropriate medicated feed additive selection and contributing to antimicrobial resistance development. The economic constraints faced by small producers limit their ability to access professional veterinary services, forcing reliance on informal advice networks that may provide suboptimal recommendations. These infrastructure limitations create market inefficiencies that require coordinated investment in education, training, and technical support systems to ensure proper product utilization and sustainable market development.

Economic Volatility and Currency Instability Impacting Market Access

The persistent economic volatility and currency instability experienced by many Latin American countries ccreatesignificant financial challenges for medicated feed additive manufacturers and end-users, which ultimately coconstrainhe expansion of the Latin AmeAmericandicated feed additives market. This affects pricing strategies, import capabilities, and long-term investment planning throughout the regional supply chain. The economic conditions directly impact the affordability of imported feed additives, as many active pharmaceutical ingredients and specialized manufacturing equipment must be sourced from international suppliers, creating cost pressures that can increase product prices. The volatility of local currencies forces manufacturers to frequently adjust pricing structures, creating uncertainty for producers who must plan annual feed additive purchases and budget accordingly. Credit availability for agricultural investments remains limited throughout the region, making long-term equipment investments and inventory purchases financially challenging for feed additive distributors. Additionally, import restrictions and foreign exchange controls implemented by several governments to stabilize economies have disrupted supply chains and created product availability issues that can impact animal health programs. These economic pressures force manufacturers to develop flexible pricing models and financing options while navigating complex regulatory environments that vary significantly across different economic conditions and policy frameworks.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 5.31% |

| Segments Covered | By Type, Livestock, Mixtures, By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | Brazil, Mexico, Argentina, Etc |

| Market Leaders Profiled | Cargill, Zoetis Inc., Archer Daniels Midland Company, Purina Animal Nutrition (Land O’ Lakes), CHS Inc., Adisseo France Sas, Biostadt India Limited, Alltech Inc. (Ridley), Hipro Animal Nutrition, Zagro. |

SEGMENTAL ANALYSIS

By Type Insights

The antibiotics segment dominated the Latin America medicated feed additives market by accounting for a 45.5% share in 2024. The supremacy of the antibiotics segment is driven by the continued reliance on antimicrobial compounds for disease prevention and growth promotion in intensive livestock operations throughout the region. The prevalence of infectious diseases in concentrated animal feeding operations across Latin America necessitates continuous antibiotic prophylaxis to maintain herd health and production efficiency. Latin America experiences a shortage in its veterinary workforce, particularly within rural sectors. Specialized animal health professionals available to guide medicated feed additive applications are limited in number. The deficiency of veterinary personnel is notably present in Central American countries and the Andean regions. The ratio of veterinarians to livestock units in these areas remains below international benchmarks. Inconsistent dosage and application timing of medicated feed additives contribute to treatment failures in small-scale operations. Improper application of these additives leads to regional economic losses. The economic impact of disease prevention through medicated feed additives is substantial. These factors sustain strong demand for antibiotic feed additives despite growing regulatory restrictions and consumer concerns about antimicrobial resistance. Antibiotic feed additives continue to dominate market share due to their demonstrated cost-effectiveness and reliable performance benefits compared to alternative growth promoters, particularly in price-sensitive Latin American markets where production margins remain thin. According to sources, antibiotic growth promoters can improve feed conversion efficiency while reducing mortality rates in commercial livestock operations, translating to significant economic benefits for producers. The cost differential between traditional antibiotic additives and alternative solutions remains substantial, with natural growth promoters costing more while delivering comparable but not superior performance outcomes. Small and medium-scale producers often dedicate a modest percentage of their operating budgets to animal health management, which increases the appeal of more economical options for maintaining livestock health. In the swine industry, the use of feed additives helps producers meet targeted growth rates efficiently and at a lower operational expense compared to systems that do not use them. Similarly, poultry producers have noted that production systems without certain feed additives necessitate a higher volume of feed to reach the same weight gains, which substantially increases operational expenditure. Overall, the cost of producing meat without conventional additives can be considerably higher than traditional methods, creating economic obstacles to adopting alternative health management strategies. Additionally, the established supply chain infrastructure and technical knowledge base for antibiotic feed additives provide operational advantages that alternative solutions cannot match, ensuring continued market dominance despite regulatory pressures.

The probiotics segment is anticipated to witness the fastest CAGR of 12.8% due to increasing regulatory acceptance and producer adoption of biological alternatives to traditional antibiotic growth promoters. Government regulatory agencies throughout Latin America are actively promoting probiotic feed additives as viable alternatives to traditional antibiotics, creating favorable market conditions for biological growth promoters through policy support and reduced regulatory barriers. Many Latin American countries have established formal programs to decrease the use of antibiotics in animal feed. Regulatory authorities in the region are implementing expedited approval processes for probiotic additives to shorten registration timelines. The number of approved probiotic feed additive products has increased significantly in recent years compared to previous periods. Lower regulatory compliance costs for probiotic feed additives facilitate easier market entry for manufacturers compared to traditional antibiotic products. Government funding is being directed toward research and development projects to support innovation in the probiotic sector. Livestock industries are committing to antibiotic reduction goals, with the adoption of probiotics serving as a primary strategy for achieving these targets. The European Union's influence on regional trade standards has accelerated probiotic acceptance, with export-certified operations required to demonstrate reduced antimicrobial usage through biological alternatives. These regulatory developments create clear market pathways for probiotic feed additive expansion while establishing supportive policy frameworks that encourage investment and innovation in biological solutions. Advances in probiotic strain development and formulation technologies have significantly improved performance consistency and efficacy, building producer confidence and accelerating adoption rates across diverse livestock production systems throughout Latin America. Probiotic feed additives have shown effectiveness in preventing common health issues in young livestock during vulnerable periods. Operations using probiotics in poultry farming are achieving performance metrics that are closer to those seen in conventional systems while also supporting better overall animal health. The use of probiotic feed additives has notably increased across the animal protein sector over the past several years. Cattle operations incorporating probiotic supplements have observed improvements in growth rates and reduced expenses related to animal health management. The technical reliability of modern probiotic formulations has addressed previous concerns about environmental sensitivity and storage requirements, with new microencapsulation technologies extending shelf life and improving temperature stability. Besides, the premium pricing associated with antibiotic-free meat products creates economic incentives for producers to invest in proven probiotic solutions, with antibiotic-free chicken commanding higher market prices. These performance improvements and economic benefits have transformed probiotics from experimental alternatives to mainstream feed additive solutions, driving rapid market expansion throughout the region.

By Livestock Insights

The poultry segment led the Latin America medicated feed additives market by capturing a 38.8% share in 2024. The prominence of the poultry segment is credited to the region's status as a major global poultry producer and the intensive health management requirements of commercial poultry operations. Latin America's position as one of the world's largest poultry-producing regions creates enormous demand for medicated feed additives to support intensive production systems and maintain flock health across millions of birds. Latin America is a major producer of broiler chickens, with specific countries contributing substantially to regional volume. One country stands out as a top global exporter of poultry products. The poultry industry in another nation produces several million tons of chicken meat each year. Preventing common diseases is a significant concern within commercial operations across the region. Continuous health management programs are considered necessary to prevent diseases that could otherwise impact production. Commercial poultry operations often have high stocking densities, which necessitate systematic health management protocols to mitigate the risk of disease transmission. Large, integrated poultry companies manage extensive operations with substantial feed consumption. Another country's poultry sector also relies on ongoing health management programs to maintain production efficiency and prevent economic losses from common infections. Appropriate health management protocols help keep mortality rates significantly lower compared to operations without such measures. These massive production volumes and associated health risks create sustained demand for specialized poultry feed additives, establishing the segment as the largest consumer of medicated feed additive products throughout Latin America. The inherent susceptibility of commercial poultry to infectious diseases and the complexity of modern poultry health management create continuous demand for specialized medicated feed additives that address multiple pathogenic challenges simultaneously. Coccidiosis impacts a significant majority of commercial poultry flocks in Latin America when effective anticoccidial programs are not implemented, leading to substantial regional economic losses. Newcastle disease outbreaks within the poultry sector have risen, requiring more robust vaccination and medicated feed additive protocols to ensure flock immunity and production stability. Respiratory disease complexes in commercial broiler operations necessitate multi-modal treatment strategies that integrate antibiotics, anticoccidials, and immune modulators through medicated feed systems. The poultry industry experiences seasonal fluctuations in disease pressure that require adaptive medicated feed additive strategies, as warmer months are associated with a higher incidence of bacterial infections. The complexity of modern poultry nutrition, with specialized diets for different growth phases and production objectives, creates demand for phase-specific medicated feed additives that can be precisely formulated for optimal efficacy. The economic consequences of disease outbreaks in intensive poultry operations are severe, making preventive medicated feed additive programs essential risk management tools for commercial producers.

The aquaculture segment is likely to experience the fastest CAGR of 14.2% over the forecast period, owing to the rapid expansion of fish and shrimp farming throughout the region and the specialized health management requirements of aquatic production systems. The dramatic expansion of aquaculture production throughout Latin America has created unprecedented demand for specialized medicated feed additives that address unique aquatic pathogen challenges and support intensive farming operations in marine and freshwater environments. Latin America's aquaculture output has shown significant expansion over an extended period. Specific nations within the region are prominent participants in global seafood markets. One country is a major global producer of salmon, contributing substantially to the overall supply. Another nation is a significant worldwide supplier of shrimp, holding a leading position in exports. A large South American nation has seen considerable expansion in its aquaculture sector. This growth creates a need for specialized products used in fish nutrition and health management. These products help address common health challenges found in dense fish farming environments. The use of such nutritional and health management products in regional aquaculture is increasing notably. This expansion in usage is proceeding at a faster pace compared to similar applications in land-based animal farming. Aquaculture is currently the most rapidly expanding part of the animal agriculture market for these types of products. A key national shrimp farming industry in North America relies heavily on these health products. These products are vital for preventing specific, highly destructive diseases that can impact entire farm populations. The technical challenges associated with aquatic feed manufacturing, including water stability requirements and precise dosing capabilities, create opportunities for specialized manufacturers with expertise in marine applications. The premium value of aquaculture products compared to traditional livestock creates willingness among producers to invest in advanced feed additive technologies that can improve survival rates and product quality, supporting sustained market growth and technological innovation. Aquaculture operations face unique pathogenic challenges that require specialized medicated feed additive solutions not applicable to terrestrial livestock, creating distinct market opportunities for manufacturers with aquatic-specific expertise and formulation capabilities. Aquatic animal diseases can lead to substantial economic losses in Latin America. Bacterial infections represent a significant portion of reported cases, suggesting a need for specific feed additive interventions. Viral diseases observed in salmon farming have encouraged the development of immunostimulant feed additives. These additives are designed to potentially enhance fish immune responses and reduce their susceptibility to illness. Additionally, parasitic infections in shrimp farming may necessitate the use of specialized anthelmintic feed additives. Such treatments must be effective within aquatic environments and provide characteristics crucial for the successful management of these conditions. The complexity of aquatic ecosystems creates additional challenges for medicated feed additive delivery, as water quality parameters such as pH, temperature, and salinity can affect product stability and bioavailability. The regulatory approval processes for aquatic feed additives differ significantly from terrestrial applications, requiring specialized safety and efficacy data that create barriers to market entry but also establish competitive advantages for companies with established aquatic product portfolios. These specialized requirements and technical challenges position aquaculture as a high-value growth segment with limited competition and substantial profit margins for manufacturers with appropriate expertise and regulatory approvals.

By Mixture Insights

The premix feeds segment held the leading share of 42.4% of the Latin America medicated feed additives market in 2024. The leading position of the premix feeds segment is attributed to the convenience and precision that premix formulations offer to livestock producers seeking consistent medicated feed additive delivery across diverse production systems. Premix feeds provide significant operational advantages through standardized formulation and precise dosage delivery, making them the preferred choice for large-scale livestock operations throughout Latin America that require consistent health management protocols across multiple production sites. Premix feed adoption generally reduces the likelihood of formulation errors compared to mixing individual additives on-farm, which can lead to improved treatment consistency and help minimize economic losses from under-dosing or overdosing. Using premix formulations can often lead to improved feed conversion efficiency for poultry companies when compared to manual additive incorporation methods. Research suggests that premix feeds are better at maintaining the stability of active ingredients than individual additive mixing, which helps ensure consistent therapeutic efficacy throughout storage and distribution. The swine industry often relies on premix feeds to standardize antibiotic delivery across commercial operations, which helps achieve uniform treatment protocols that can support various certification requirements. The operational complexity of managing multiple feed additive products creates significant administrative and logistical challenges for producers. The precision and consistency offered by premix formulations address critical quality control requirements in modern livestock operations, establishing this segment as the preferred delivery method for medicated feed additives throughout the region. Premix feeds offer significant regulatory compliance advantages and quality assurance benefits that make them essential for export-oriented livestock operations and producers seeking certification under international food safety standards throughout Latin America. Premix feed manufacturers adhere to Good Manufacturing Practices certification to maintain consistent product quality and traceability for regulatory compliance. Poultry exporters utilize premix feeds to satisfy international residue monitoring requirements and antimicrobial usage restrictions. Certification of premix feeds assists in reducing regulatory audit findings and minimizing the risks associated with shipment rejections or facility closures. Beef exporters require premix feed documentation to demonstrate alignment with international veterinary standards and medicated additive usage requirements. The traceability requirements imposed by international food safety standards create substantial documentation burdens for producers, with premix feed manufacturers providing comprehensive batch records and quality certificates that simplify compliance procedures. The legal liability protection offered by certified premix feed suppliers provides additional economic security for producers operating in regulated markets, making premix feeds essential tools for risk management in commercial livestock operations.

The supplements segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 11.5% from 2025 to 2033. The rapid growth of the supplements segment is fuelled by increasing producer interest in functional feed additives that enhance animal performance beyond basic disease prevention. The growing emphasis on productivity optimization and performance enhancement in Latin American livestock operations has created substantial demand for specialized supplement formulations that improve growth rates, feed efficiency, and overall animal health beyond traditional disease prevention applications. Livestock producers throughout Latin America are increasingly adopting precision nutrition approaches that incorporate performance-enhancing supplements to maximize return on investment from intensive production systems. Strategic supplement usage by the poultry industry in Brazil has documented improvements in daily weight gain and feed conversion ratios. Amino acid and enzyme supplement combinations can improve protein utilization efficiency in commercial swine operations, reducing feed costs while maintaining growth performance standards. Mexico's dairy sector relies on specialized mineral and vitamin supplement formulations to optimize reproductive performance and milk production efficiency. The economic benefits of performance-enhancing supplements are particularly attractive to producers operating in competitive commodity markets where small efficiency improvements can significantly impact profitability. The integration of supplement technologies with digital monitoring systems enables precision feeding approaches that maximize supplement efficacy while minimizing waste, creating additional value for producers investing in advanced nutrition solutions. Growing consumer awareness regarding animal welfare and sustainable production practices has accelerated demand for supplement-based feed additive solutions that support natural growth promotion and reduce reliance on traditional antibiotics throughout Latin American livestock industries. Organic meat consumption is growing across Latin America, with Brazil serving as the region's largest market. The expansion of the organic sector necessitates the use of certified supplement alternatives to replace conventional medicated additives. A significant portion of regional consumers shows a preference for meat products from animals raised without routine antibiotics. Consumer interest in antibiotic-free production is encouraging the development of supplement-based health management programs. Poultry producers in Mexico are decreasing their reliance on antibiotics by adopting strategic supplement programs. The transition to supplement-based systems allows producers to maintain performance outcomes while meeting the demand for responsibly produced protein. The European Union's influence on regional trade standards has intensified consumer preference trends, with export-certified operations required to demonstrate reduced antimicrobial usage through supplement-based alternatives that maintain production efficiency. The premium pricing associated with welfare-enhanced and antibiotic-free meat products creates economic incentives for producers to invest in proven supplement solutions, with antibiotic-free chicken commanding higher market prices and supporting sustained supplement market growth.

COUNTRY ANALYSIS

Brazil Medicated Feed Additives Market Analysis

Brazil was the top performer in the Latin America medicated feed additives market and accounted for a 45.1% in 2024. The supremacy of the Brazilian market is driven by its position as the world's largest beef exporter and second-largest poultry producer, creating massive demand for advanced animal health management solutions. Brazil's medicated feed additives market demonstrates robust expansion driven by the country's massive livestock production capacity and increasing regulatory sophistication governing animal health products. The Brazilian cattle industry manages a large number of cattle in intensive feeding systems, where continuous treatment through medicated feed additives is applied to prevent common health issues. Poultry production facilities use a significant portion of the country's medicated feed additives to maintain flock health and support growth performance in operations. Regulatory frameworks have been implemented to ensure product safety and efficacy, while also supporting innovation in alternative feed additive technologies. The swine industry represents another major consumption segment, with production companies investing in precision feeding technologies that optimize the delivery of medicated feed additives. The country's position as a major agricultural technology adopter creates demand for advanced formulation technologies and customized solutions that address specific regional pathogen challenges. Additionally, Brazil's export orientation necessitates compliance with international food safety standards, driving demand for certified medicated feed additive products that meet stringent residue monitoring requirements. The Brazilian government's support for agricultural innovation through research funding and tax incentives creates favorable conditions for market expansion and technological advancement.

Mexico Medicated Feed Additives Market Analysis

Mexico followed closely in the Latin American medicated feed additives market and captured a 22.1% share in 2024. The country's strong agricultural export orientation and diversified livestock production create substantial demand for advanced feed additive solutions. Mexico's medicated feed additives market benefits from the country's position as a major meat exporter and its integration with North American agricultural supply chains, creating demand for high-quality animal health solutions that meet international standards. Mexico's poultry industry requires continuous anticoccidial and antibiotic programs to maintain flock health. Preventing economic losses from common diseases remains a priority for commercial poultry operations. The country's swine industry relies on medicated feed additives to achieve target growth rates. Maintaining export certification for international pork shipments depends on specific animal health protocols. Progressive regulatory frameworks in the country balance animal health requirements with antimicrobial stewardship goals. These regulatory changes are creating demand for alternative feed additive solutions. Moreover, the beef export industry requires comprehensive medicated feed additive programs to meet specific international veterinary standards. These standards often mandate detailed records of all antimicrobial usage and residue monitoring protocols. The country's strategic position in North American trade relationships creates opportunities for technology transfer and market access that support advanced feed additive adoption. Additionally, Mexico's growing middle class drives consumer demand for safe, high-quality protein products, creating market incentives for producers to invest in proven health management solutions that ensure product safety and quality consistency.

Argentina Medicated Feed Additives Market Analysis

Argentina is another key player in the LatinAmericana medicated feed additives market. Its extensive cattle industry and growing agricultural exports create significant opportunities for feed additive market expansion. Argentina's medicated feed additives market demonstrates steady growth supported by the country's position as a major beef producer and exporter. The National Service for Agri-Food Health has implemented progressive regulatory standards that support innovation in alternative feed additive technologies while maintaining access to essential therapeutic compounds for disease prevention. Argentina's position as a major agricultural exporter creates demand for certified medicated feed additive products that meet international food safety standards and residue monitoring requirements for shipments to European and North American markets. The country's extensive agricultural research infrastructure supports technology adoption and product development initiatives that enhance feed additive efficacy and application efficiency. Additionally, Argentina's commitment to sustainable agricultural practices creates market opportunities for biological and natural feed additive solutions that support environmental stewardship goals while maintaining production efficiency.

Chile Medicated Feed Additives Market Analysis

Chile is an emerging country in the Latin American medicated feed additives market. Its specialized aquaculture industry creates unique opportunities for feed additive market expansion. Chile's medicated feed additives market shows promising growth potential driven by the country's position as the world's second-largest salmon producer and its advanced aquaculture technology infrastructure. Chile's regulatory environment, managed by the Subsecretariat of Fisheries and Aquaculture, has implemented progressive standards that balance disease prevention requirements with environmental protection goals, creating demand for targeted feed additive solutions that minimize environmental impact while maintaining production efficiency. The country's export orientation necessitates compliance with international food safety standards, driving demand for certified medicated feed additive products that meet stringent residue monitoring requirements for shipments to European, North American, and Asian markets. Chile's position as a technology adopter in aquaculture creates opportunities for advanced feed additive formulations and delivery systems that optimize therapeutic efficacy in marine environments. Additionally, Chile's commitment to sustainable aquaculture practices creates market opportunities for biological and natural feed additive solutions that support environmental stewardship goals while maintaining production efficiency and disease prevention capabilities.

COMPETITIVE LANDSCAPE

The Latin America medicated feed additives market exhibits moderate to high competition characterized by the presence of global multinational corporations, regional specialists, and emerging local manufacturers vying for market share across diverse production sectors. The competitive landscape is shaped by technological innovation, regulatory compliance capabilities, and distribution network efficiency, with established players leveraging their research capabilities and brand recognition to maintain dominant positions. Market dynamics are influenced by evolving regulatory frameworks that favor companies with strong compliance infrastructures and alternative solution portfolios that address antimicrobial reduction initiatives. The presence of both direct competition among feed additive specialists and indirect competition from integrated animal nutrition companies creates a complex competitive environment where differentiation through product performance and service quality becomes critical. Geographic competition varies significantly across different countries, with Brazil and Mexico dominated by global players while smaller markets show increasing participation from regional manufacturers offering cost-competitive solutions. Market consolidation through strategic acquisitions and partnerships is common as companies seek to expand technological capabilities and geographic reach. Intellectual property protection and regulatory expertise play crucial roles in maintaining competitive advantages, with companies investing heavily in patent portfolios and regulatory affairs capabilities. Customer relationships and technical support services increasingly differentiate market players, particularly in commercial livestock operations where reliability and performance consistency are essential factors for producer success.

KEY MARKET PLAYERS

The major companies dominating the market share include

- Cargill

- Zoetis Inc.

- Archer Daniels Midland Company

- Purina Animal Nutrition (Land O’ Lakes)

- CHS Inc.

- Adisseo FranceSASs

- Biostadt India Limited

- Alltech Inc. (Ridley)

- Hipro Animal Nutrition

- Zagro.

Top Players In The Market

- Cargill Incorporatedstands as a dominant force in the Latin America medicated feed additives market through its comprehensive animal nutrition division and extensive regional manufacturing footprint. The company's contribution to the global market encompasses innovative feed additive formulations specifically designed for tropical and subtropical production conditions prevalent throughout Latin America. Their research and development initiatives focus on creating climate-adapted solutions that maintain efficacy under high humidity and temperature variations characteristic of the region. Cargill's integrated approach combines traditional feed additive expertise with advanced biotechnology applications, offering producers customized health management programs that address specific pathogen challenges and nutritional requirements. The company's strong distribution network and technical support services ensure consistent product availability and optimal application guidance across diverse production systems. Their commitment to sustainable agriculture practices has led to significant investments in natural and organic feed additive alternatives that meet growing consumer demand for responsibly-produced animal protein. Cargill's collaborative partnerships with regional universities and research institutions facilitate continuous innovation and technology transfer that enhance product performance and market relevance.

- ADM (Archer Daniels Midland Company) emerges as a significant player in the Latin America medicated feed additives market through its specialized animal nutrition business and strategic regional investments. The company's contribution to the global market centers on developing advanced feed additive technologies that enhance animal health and performance while supporting sustainable production practices throughout Latin America. Their comprehensive product portfolio includes traditional antibiotic growth promoters, alternative biological solutions, and specialized nutritional supplements designed for the region's diverse livestock production systems. ADM's research facilities in Brazil and Mexico focus on creating formulations that address specific regional disease challenges and climatic conditions, ensuring optimal product performance across varied production environments. The company's commitment to innovation drives the continuous development of next-generation feed additives that reduce antimicrobial dependency while maintaining production efficiency. Their technical service teams provide extensive support to producers through on-farm consultations and customized health management programs that optimize feed additive usage and maximize economic returns. ADM's strategic partnerships with local distributors and veterinary networks enhance market penetration and ensure consistent product availability throughout the region.

- Novus International Inc. Novus International establishes itself as a leading innovator in the Latin America medicated feed additives market through its specialized focus on performance minerals and precision nutrition solutions. The company's contribution to the global market emphasizes scientific research and evidence-based product development that addresses specific nutritional deficiencies and health challenges common in Latin American livestock operations. Their proprietary microencapsulation technologies enhance mineral bioavailability and reduce interactions with other feed components, delivering superior performance compared to traditional supplement formulations. Novus's commitment to sustainable agriculture practices has resulted in significant investments in natural feed additive alternatives and biological solutions that support antibiotic reduction initiatives throughout the region. The company's technical expertise in mineral nutrition has led to the development of specialized products that optimize rumen function in cattle and enhance bone development in poultry and swine operations. Their collaborative approach with regional producers and veterinary professionals ensures that feed additive solutions are tailored to specific production conditions and performance objectives. Novus's continuous investment in research and development facilities throughout Latin America supports ongoing innovation and product adaptation that maintain competitive advantages in rapidly evolving market conditions.

Top Strategies Used By Key Market Participants

- Strategic Regional Manufacturing and Distribution Network Development. Leading medicated feed additive manufacturers focus on establishing comprehensive regional manufacturing capabilities and distribution networks to ensure product availability and reduce logistical costs throughout Latin America. This strategy involves constructing specialized production facilities in key market locations such as Brazil, Mexico, and Argentina to address specific regional requirements and regulatory standards. Companies invest heavily in cold chain logistics and quality control infrastructure to maintain product stability and efficacy during transportation and storage in tropical climates. Strategic partnerships with local distributors and veterinary supply chains enhance market penetration and provide technical support services essential for proper product application. Regional manufacturing also enables rapid response to disease outbreaks and emergency health management situations that require immediate product deployment. This localized approach reduces import dependencies and currency exchange risks while ensuring compliance with varying national regulatory requirements across different Latin American countries.

- Product Innovation and Alternative Solution Development. Key market participants prioritize continuous research and development investments to create innovative feed additive solutions that address evolving regulatory requirements and consumer preferences throughout Latin America. This strategy focuses on developing biological alternatives to traditional antibiotic growth promoters, including probiotics, prebiotics, and plant-based antimicrobial compounds that maintain production efficiency while supporting antimicrobial stewardship goals. Companies invest in advanced formulation technologies such as microencapsulation and targeted delivery systems that enhance product stability and bioavailability under challenging environmental conditions. Research initiatives also concentrate on creating climate-adapted formulations that maintain efficacy in high humidity and temperature variations characteristic of tropical production environments. Collaboration with regional universities and research institutions accelerates innovation and ensures that new products address specific pathogen challenges and nutritional requirements prevalent in Latin American livestock operations. This innovation focus helps manufacturers maintain competitive advantages while supporting industry sustainability objectives.

- Technical Support and Educational Service Provision Market leaders emphasize comprehensive technical support services and educational programs to build strong customer relationships and ensure optimal product performance throughout diverse Latin American production systems. This strategy involves deploying specialized technical service teams that provide on-farm consultations, customized health management program development, and training programs for producers and veterinary professionals. Companies invest in digital platforms and mobile applications that enable remote monitoring and real-time technical support for producers managing large-scale operations across multiple locations. Educational initiatives include producer workshops, veterinary training programs, and research collaboration projects that enhance understanding of proper feed additive application and health management practices. Technical support services also encompass regulatory compliance assistance, helping producers navigate complex approval processes and documentation requirements for export certification. This service-oriented approach builds customer loyalty and creates barriers to competitive entry while supporting long-term market expansion and technology adoption.

MARKET SEGMENTATION

This research report on the Latin America market is segmented and sub-segmented into the following categories.

By Type:

- Antioxidants

- Antibiotics

- Probiotics

- Prebiotics

- Enzymes

- Amino Acids

- Others

By Livestock:

- Poultry

- Swine

- Cattle

- Pet Foods

- Aquaculture

- Others

By Mixture Types

- Supplements

- Premix Feeds

- Concentrates

- Base Mixes

By Country

- Brazil

- Mexico

- Argentina

Frequently Asked Questions

What are medicated feed additives?

Medicated feed additives are nutritional feed components with drugs or medications to prevent or treat disease in livestock.

What is driving the Latin America medicated feed additives market?

Growth is driven by rising livestock production, demand for animal protein, and need for enhanced animal health and productivity.

Which animals benefit most from medicated feed additives?

Poultry, swine, and cattle are major livestock segments using medicated feed additives.

What role do medicated additives play in animal health?

They help prevent and control infections, improve growth rates, and support immune function.

How do regulations impact the Latin America market?

Strict drug residue limits and veterinary regulations influence product approvals and usage practices.

What are common types of medicated feed additives?

Antibiotics, antiparasitics, coccidiostats, and growth promoters.

Which countries lead the Latin America market?

Brazil and Mexico are key markets due to large livestock sectors and expanding meat production.

What are the main challenges in this market?

Rising regulatory scrutiny, antibiotic resistance concerns, and supply chain complexities.

Are alternatives to medicated feed additives gaining traction?

Yes, probiotics, prebiotics, and phytogenics are increasingly used due to health and regulatory trends.

What is the future outlook of the Latin America medicated feed additives market?

Slower antibiotic use and growth of alternative health solutions will shape long-term market evolution with steady demand for safe and effective additives.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com