- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$58.83 BnMarket Estimate, 2026

$63.29 BnMarket Forecast, 2034

$113.55 BnCAGR, 2026–2034

7.58%Executive Summary: Latin America Power Distribution Component Market

- Market Scope: Comprehensive regional Latin America power distribution component market analysis covering product categories, mounting configurations, voltage ratings, country-level leadership frameworks, and grid infrastructure metrics.

- Market Valuation: Valued at USD 58.83 billion (2025 base year), estimated at USD 63.29 billion (2026), and projected to reach USD 113.55 billion by 2034, registering a robust CAGR of 7.58% (2026–2034).

- Primary Growth Drivers: Rising electricity consumption, urban expansion, grid modernization, and renewable energy integration. Key energy, demographic, and infrastructure highlights include regional electricity consumption increasing by 4.7% year-over-year in 2023, Latin America’s urban population projected to reach 85% by 2030 (up from 81% in 2020), Brazil adding >15 million residential connections between 2020 and 2023, >75% of regional electricity distribution occurring below 11 kV, >40% of electrical distribution assets exceeding 30 years in age, Latin America adding >10 GW of renewable capacity in 2023, and Brazil targeting 120,000 EV charging stations by 2027.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product Segment | Switchgear (dominated product segment with 34.3% of total consumption in 2025) | Motor Control Panels (projected to grow at approximately 7.9% CAGR) |

| By Mounting Configuration | Fixed Mounting Configurations (accounted for 41.5% of installations in 2025) | Withdrawable Configurations (forecasted to expand at approximately 8.4% CAGR) |

| By Voltage Rating | ≤11 kV Segment (held 46.6% of consumption in 2025) | >33 kV to ≤66 kV Segment (projected to grow at approximately 7.1% CAGR) |

| By Country / Region | Brazil (led geographically with 37.7% of regional consumption in 2025) | Emerging Latin American Smart Grid & Renewable Integration Hubs |

Major Market Players & Market Structure

Market Structure: Highly competitive Latin American electrical equipment and power infrastructure landscape featuring major global and regional engineering enterprises competing intensely on smart grid integration, asset replacement for aging infrastructure, renewable energy interconnection, switchgear reliability, and localized manufacturing footprints.

Key Companies: ABB, Schneider Electric, Siemens, Mitsubishi Electric Corporation, Eaton, Alstom, GE Power, L&T, Powell Industries, Hitachi Group, and Cerisol.

Latin America Power Distribution Component Market Size

The Latin American power distribution component market size was valued at USD 58.83 billion in 2025, and is expected to reach USD 63.29 billion in 2026 and USD 113.55 billion by 2034, with a CAGR of 7.58% during the forecast period.

The Latin America power distribution component market encompasses a broad range of equipment essential for the safe and efficient transmission, transformation, and utilization of electrical energy across residential, commercial, industrial, and utility sectors. This includes components such as transformers, circuit breakers, switchgear, busbars, and protective relays that form the backbone of modern electrical networks. With rising electricity demand driven by urbanization and industrial expansion, the need for reliable and advanced power distribution infrastructure has grown significantly. According to the Economic Commission for Latin America and the Caribbean (ECLAC), regional electricity consumption increased by 4.7% year-on-year in 2023, reflecting stronger economic activity and greater electrification rates. In Brazil, the National Electric Energy Agency (ANEEL) reported that over 98% of the population now has access to electricity, necessitating upgrades to existing grid infrastructure to manage load balancing and reduce losses. Similarly, Mexico’s Ministry of Energy emphasized the importance of digitalizing distribution systems to support smart grid development and integrate renewable energy sources more effectively. Chile’s Ministry of Energy noted a surge in investments in medium-voltage switchgear due to the expansion of mining operations in remote regions.

MARKET DRIVERS

Urbanization and Expansion of Electrical Infrastructure

One of the primary drivers fueling the Latin America power distribution component market is the rapid pace of urbanization and the corresponding increase in demand for reliable electricity distribution. According to the United Nations Department of Economic and Social Affairs (UN DESA), Latin America’s urban population is expected to reach 85% by 2030, up from 81% in 2020. This demographic shift has placed immense pressure on existing electrical infrastructure, particularly in rapidly expanding metropolitan areas such as São Paulo, Bogotá, and Lima. The Brazilian National Electric Energy Agency (ANEEL) reported that over 15 million new residential connections were added between 2020 and 2023, requiring extensive deployment of low- and medium-voltage distribution equipment. Similarly, in Peru, the Ministry of Energy and Mines mandated the installation of intelligent protection devices in new housing developments to enhance grid stability and minimize outages. Additionally, Chile’s Ministry of Public Works highlighted the role of pad-mounted transformers and underground cable systems in supporting urban renewal projects in Santiago and Valparaíso.

Industrialization and Growth of Manufacturing Sectors

The sustained growth of the manufacturing and industrial sector across Latin America is another significant driver of the power distribution component market. Governments in the region have been actively promoting industrial expansion through investment incentives and infrastructure development programs, leading to higher demand for robust electrical systems. Argentina’s Ministry of Productive Innovation emphasized the role of high-efficiency transformers in reducing energy losses within food processing and automotive assembly plants. With ongoing industrial modernization efforts and rising energy-intensive operations, the demand for advanced power distribution components continues to grow across Latin America.

MARKET RESTRAINTS

Volatility in Raw Material Prices

A major restraint affecting the Latin America power distribution component market is the volatility in raw material prices, particularly for copper, aluminum, steel, and silicon-based insulating materials. These metals are critical inputs for manufacturing transformers, switchgear, and circuit breakers, yet their costs fluctuate based on global commodity markets and geopolitical factors. According to the U.S. Geological Survey (USGS), copper prices averaged USD 8,200 per metric ton in 2023, a 14% increase compared to the previous year, directly impacting transformer and cable manufacturing costs. These fluctuations make long-term forecasting difficult and reduce profit margins, constraining market expansion despite rising end-use demand and infrastructure modernization initiatives.

Regulatory Uncertainty and Policy Instability

Regulatory Uncertainty and Policy Instability

Regulatory uncertainty and policy instability pose ongoing challenges for the Latin America power distribution component market, as inconsistent government directives and shifting energy policies disrupt investment planning and procurement activities. In several countries, frequent revisions to import tariffs and technical standards create confusion among stakeholders. For instance, in Argentina, the Central Bank imposed multiple foreign exchange controls in 2023, complicating the import of critical components such as molded-case circuit breakers and digital protection relays. According to the International Trade Centre (ITC), Argentina’s import licensing system for electrical equipment underwent three major revisions between 2021 and 2023, adding administrative complexity. Similarly, in Mexico, recent amendments to energy legislation have affected private sector participation in distribution projects, increasing regulatory scrutiny for foreign suppliers. In addition, political transitions in countries like Peru and Ecuador have resulted in abrupt shifts in energy infrastructure priorities, delaying approvals for new distribution projects.

MARKET OPPORTUNITIES

Smart Grid Investments and Digitalization of Distribution Networks

The increasing adoption of smart grid technologies presents a substantial opportunity for the Latin America power distribution component market. Governments and utility providers across the region are investing in digitalized electrical networks to improve grid reliability, optimize energy usage, and integrate renewable energy sources more efficiently. According to the International Renewable Energy Agency (IRENA), Latin America added over 10 GW of renewable energy capacity in 2023, necessitating intelligent distribution infrastructure to manage variable power flows. In Brazil, the National Electric Energy Agency (ANEEL) launched the “Smart Cities” initiative, allocating BRL 2.5 billion (USD 500 million) for smart metering and automated grid monitoring systems, boosting demand for intelligent electronic devices (IEDs) and communication-enabled circuit breakers. Chile’s Ministry of Energy endorsed the use of smart transformers and reclosers to enhance fault detection and self-healing capabilities in the national grid.

Electrification of Transportation and Charging Infrastructure

The rapid electrification of transportation is opening new avenues for the Latin America power distribution component market, particularly in the development of electric vehicle (EV) charging infrastructure. Governments across the region are implementing policies to promote EV adoption, necessitating significant upgrades to local distribution networks to accommodate increased electricity demand. According to the International Energy Agency (IEA), EV sales in Latin America increased significantly in 2023, with Chile and Colombia leading adoption efforts. In Brazil, the Ministry of Mines and Energy launched the "Recharge Brazil" initiative, aiming to install 120,000 public and private EV charging stations nationwide by 2027, requiring dedicated transformers, load-break switches, and smart meters. Similarly, in Mexico, the National Commission for the Efficient Use of Energy (CONUEE) mandated the integration of ultra-fast DC charging stations along federal highways, compelling electrical equipment manufacturers to develop specialized power conversion units. Chile’s Ministry of Transport emphasized the importance of grid-tied charging hubs powered by solar inverters and battery energy storage systems, reinforcing the need for compatible power distribution infrastructure.

MARKET CHALLENGES

Supply Chain Disruptions and Logistics Constraints

Supply chain inefficiencies and logistical bottlenecks present a persistent challenge for the Latin America power distribution component market. The region's reliance on imported electrical equipment and raw materials exposes it to delays caused by port congestion, inadequate transport infrastructure, and trade policy uncertainties. According to the World Bank Logistics Performance Index (LPI), several Latin American countries rank below global averages in terms of customs efficiency and infrastructure reliability. Brazil faces additional complexities, with EPE (Empresa de Pesquisa Energética) estimating that logistics costs account for up to 30% of final equipment prices in remote regions. These constraints not only inflate capital expenditures but also create inconsistencies in supply, making it difficult for utilities and industrial consumers to maintain steady procurement and execution schedules for power distribution projects.

Aging Grid Infrastructure and High Maintenance Costs

Aging grid infrastructure poses a significant challenge to the Latin America power distribution component market, as many countries operate legacy systems that require frequent upgrades and maintenance. According to the Inter-American Development Bank (IDB), over 40% of electrical distribution assets in Latin America are older than 30 years, contributing to inefficiencies, outages, and safety risks. Similarly, in Mexico, the Federal Electricity Commission (CFE) identified over 25,000 kilometers of deteriorating distribution lines that required immediate replacement, increasing demand for high-efficiency transformers and smart reclosers. As governments seek to enhance grid resilience and reduce operational expenditures, the transition toward modern power distribution components remains a complex and costly endeavor, limiting widespread adoption in economically constrained environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.58% |

| Segments Covered | By Product, Configuration, Voltage Rating, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Latin America include Brazil, Argentina, Mexico, and the Rest of Latin America |

| Market Leaders Profiled | ABB (Switzerland), Schneider Electric (France), Siemens (Germany), Mitsubishi Electric Corporation (Japan), Eaton (Ireland), Alstom (France), GE Power (U.S.), L&T (India), Powell Industries (U.S.), Hitachi Group (Japan), Cerisol (Brazil), and others. |

SEGMENTAL ANALYSIS

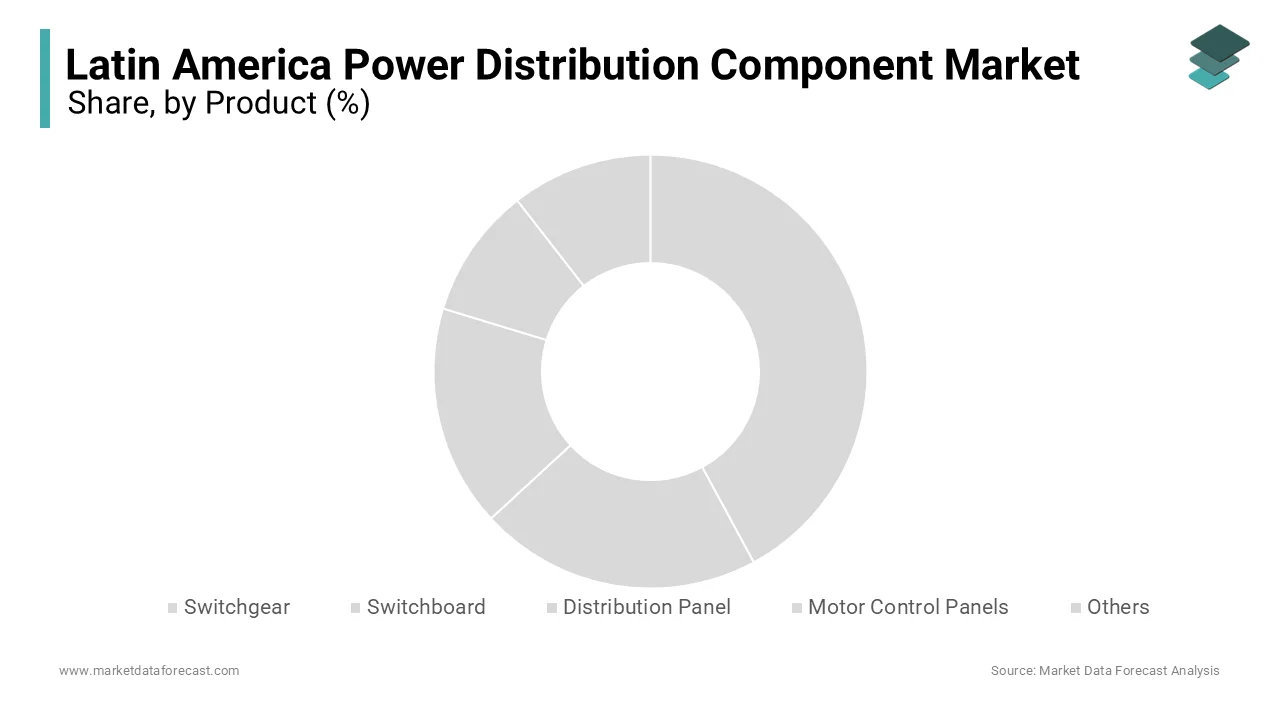

By Product Insights

The switchgear held the dominant position in the Latin America power distribution component market by capturing a 34.3% of total consumption in 2025. This segment's position is mainly attributed to its widespread use across utility, industrial, and commercial applications for circuit protection, isolation, and load management. Similarly, in Mexico, the Federal Electricity Commission (CFE) mandated the installation of IEC 62271-compliant switchgear in new substations to ensure compatibility with smart grid initiatives.

Motor control panels are emerging as the fastest-growing segment in the Latin America power distribution component market, projected to expand at a CAGR of approximately 7.9% from 2026 to 2034. This rapid expansion is propelled by increasing automation in industrial facilities and rising demand for energy-efficient motor drives in manufacturing and process industries. Additionally, renewable energy facilities such as wind farms and solar parks increasingly rely on motor control panels to manage pump stations, cooling systems, and tracking mechanisms.

By Configuration Insights

Fixed mounting configuration commanded the Latin America power distribution component market by accounting for a 41.5% of total installations in 2025. This is due to its cost-effectiveness, mechanical stability, and suitability for permanent electrical setups in industrial and utility settings. Some countries in the region also supported the deployment of fixed busbar systems in high-rise residential buildings due to their superior current-carrying capacity and thermal resistance. Also, fixed mounting components accounted for a large share of all low- and medium-voltage installations in Latin America, underscoring their pivotal role in regional power infrastructure development.

Withdrawable configuration is witnessing the highest growth within the Latin America power distribution component market, expanding at a CAGR of approximately 8.4%. This development is fueled by increasing demand for modular and easily maintainable electrical systems in data centers, hospitals, and critical manufacturing facilities. Moreover, withdrawable switchgear and circuit breaker designs are being prioritized in new hospital construction projects due to their ability to allow safe and fast equipment replacement without shutting down the entire power system. With ongoing advancements in plug-and-play design and predictive maintenance integration, withdrawable configurations are gaining momentum across Latin America’s mission-critical power environments.

By Voltage Rating Insights

The ≤ 11 kV voltage rating segment held the largest share of the Latin America power distribution component market i.e. 46.6% of total consumption in 2025. This dominance is primarily driven by its extensive use in urban and rural low-voltage networks that serve residential, commercial, and small-to-medium industrial consumers. According to the Inter-American Development Bank (IDB), over 75% of electricity distribution in Latin America occurs at voltages below 11 kV, making it the backbone of last-mile connectivity. Nations also emphasized the role of ≤ 11 kV systems in powering decentralized renewable energy microgrids, particularly in arid and remote areas. So, this segment benefits from strong government backing for electrification programs and localized generation sources, reinforcing its leading position in the regional market.

The > 33 kV to ≤ 66 kV voltage rating segment is witnessing the highest growth within the Latin America power distribution component market, expanding at a CAGR of approximately 7.1%. This growth is driven by increased investments in industrial clusters, renewable energy transmission corridors, and electric mobility infrastructure requiring higher-capacity distribution systems. According to the International Renewable Energy Agency (IRENA), Latin America added over 10 GW of wind and solar capacity in 2023, necessitating robust interconnection infrastructure to transmit generated power efficiently. Similarly, in Peru, the Ministry of Energy and Mines promoted 66 kV substations for copper extraction sites located in mountainous regions where long-distance power delivery is essential.

REGIONAL ANALYSIS

Brazil secured the dominant position in the Latin America power distribution component market by contributing a 37.7% of total regional consumption in 2025. As the continent’s largest economy and most populous nation, Brazil’s extensive electrical infrastructure and ongoing modernization efforts drive significant demand for distribution equipment. According to the National Electric Energy Agency (ANEEL), over 98% of the population now has access to electricity, requiring continuous expansion and upgrading of low- and medium-voltage distribution networks. Additionally, Petrobras integrated advanced 66 kV-rated transformers into offshore oil platforms to support deep-sea exploration activities. Despite raw material price fluctuations and supply chain disruptions, Brazil remains the core market for power distribution components in Latin America, supported by sustained public and private sector investments in electrification and industrial automation.

Mexico continues to be a key player in the Latin America power distribution component market. The country benefits from a structured national energy policy and a strong industrial base that requires reliable electrical infrastructure. In addition, there is need for resilient power distribution infrastructure to support ultra-fast EV charging stations along federal highways. Despite regulatory shifts affecting private sector participation in energy projects, Mexico maintains a strong presence in the Latin American market, supported by ongoing investments in electrification, manufacturing, and smart grid technologies.

Argentina adds majorly to the Latin America power distribution component market, driven by targeted investments in industrial electrification and grid rehabilitation. Also, the country experienced significant annual grid maintenance costs due to outdated infrastructure, prompting a nationwide modernization program. The Buenos Aires Metro System expanded its fleet of electric trains, requiring upgraded substation transformers and protective relays to support high-frequency operations. Moreover, industrial zones have adopted arc-resistant switchgear to enhance workplace safety and reduce unplanned outages. Additionally, the authorities also encouraged the deployment of dry-type transformers in food processing and pharmaceutical facilities to meet fire safety and environmental compliance standards. Despite economic volatility, Argentina maintains a stable presence in the Latin American power distribution component market, supported by policy-driven infrastructure upgrades and industrial electrification mandates.

Chile saw steady growth in the Latin America power distribution component market, driven by strategic investments in mining, renewable energy, and urban electrification. According to the Chilean Ministry of Energy, the Atacama and Antofagasta regions require high-efficiency power distribution systems to support copper extraction operations that account for nearly one-third of global production. In Santiago and Valparaíso, municipal authorities integrated smart distribution panels and digital protection relays in new residential and commercial developments to enhance grid resilience.

The remaining Latin American countries are playing pivotal roles in shaping demand patterns. Colombia stands out as a key market, with mandating the use of intelligent electronic devices (IEDs) in new distribution nodes to improve fault detection and self-healing grid capabilities. Collectively, these nations contribute significantly to the broader Latin American power distribution component landscape.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

ABB (Switzerland), Schneider Electric (France), Siemens (Germany), Mitsubishi Electric Corporation (Japan), Eaton (Ireland), Alstom (France), GE Power (U.S.), L&T (India), Powell Industries (U.S.), Hitachi Group (Japan), and Cerisol (Brazil) are the key players in the Latin America power distribution component market.

The Latin America power distribution component market features a highly competitive landscape shaped by the coexistence of global multinationals and emerging regional specialists, each striving to gain a stronger foothold through differentiated offerings and strategic initiatives. Global leaders such as Siemens, Schneider Electric, and ABB dominate due to their extensive product portfolios, technological expertise, and established project execution capabilities. However, smaller regional players and local manufacturers are gaining traction by offering cost-effective, modular solutions tailored to specific municipal and industrial needs. The competition intensifies in countries like Brazil and Mexico, where government funding and regulatory mandates drive consistent demand for modernized electrical infrastructure. Product differentiation remains a key battleground, with companies striving to develop more energy-efficient, digitally integrated, and resilient distribution components that align with evolving sustainability goals and operational demands. Additionally, after-sales service, financing models, and turnkey project delivery play crucial roles in setting market participants apart. As demand diversifies across utility, industrial, and commercial applications, companies must continuously adapt to shifting dynamics, ensuring agility in technology development, customer engagement, and operational efficiency to maintain and expand their market presence. Regulatory pressures, supply chain volatility, and financial constraints further shape competitive behavior, compelling firms to innovate and invest strategically in resilient and adaptable business models.

TOP PLAYERS IN THE MARKET

Siemens Energy

Siemens Energy is a leading global supplier of power distribution components and holds a strong presence in the Latin America market. The company offers a comprehensive portfolio of switchgear, transformers, and digital grid solutions tailored for utility, industrial, and commercial applications. In Latin America, Siemens emphasizes innovation and sustainability, developing advanced products that meet evolving regulatory and performance demands. Its regional technical centers support customer-specific solutions, particularly in smart grid development and substation automation. Siemens’ extensive distribution network and strategic partnerships with local engineering firms enable efficient project execution. By leveraging its global expertise and localized capabilities, Siemens maintains a competitive edge and contributes to global advancements in electrical infrastructure.

Schneider Electric

Schneider Electric plays a pivotal role in shaping the Latin America power distribution component market by providing high-performance equipment such as motor control centers, smart panels, and energy-efficient switchboards. The company has strategically expanded its footprint through collaborations with regional utilities and industrial clients, ensuring reliable access to customized power solutions. In Latin America, Schneider emphasizes digitalization, offering IoT-enabled monitoring systems that enhance operational efficiency and reduce downtime. Its commitment to research and development supports long-term growth, particularly in markets adopting smart grid technologies. With a strong brand reputation and focus on application-specific innovation, Schneider strengthens its position as a technology-driven leader in the region.

ABB Ltd.

ABB is a major contributor to the Latin America power distribution component market, known for its innovative switchgear, circuit breakers, and digital protection relays used across utilities and industries. The company integrates advanced materials science with practical engineering, enabling performance improvements in grid reliability and energy efficiency. In Latin America, ABB emphasizes customization, adapting solutions to meet regional climatic conditions and infrastructure needs. Its robust brand reputation and long-standing partnerships with local distributors enhance market penetration. By focusing on sustainable production and technical collaboration, ABB strengthens its position as a key player in the region. The company’s ability to align with global trends while addressing localized distribution challenges makes it a significant force in the Latin American power sector.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

One of the primary strategies adopted by leading players in the Latin America power distribution component market is technology localization and product adaptation . Companies are investing in R&D to develop equipment that caters specifically to regional conditions such as variable load demands, extreme weather, and aging grid infrastructure. This enables better performance, longer asset life, and improved safety compliance.

Another critical strategy involves expanding local partnerships and service networks . By forming alliances with engineering firms, construction companies, and public utilities, manufacturers can improve installation support and after-sales maintenance services. These collaborations also facilitate faster deployment and greater trust among public and private sector clients.

Lastly, firms are increasingly engaging in integrated solution offerings , where power distribution components are bundled with digital monitoring tools, predictive analytics, and remote diagnostics. This approach enhances system efficiency and provides added value to customers seeking smart, data-driven grid management solutions. Such comprehensive offerings help reinforce market leadership and customer retention in competitive environments.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, Siemens launched a new line of compact gas-insulated switchgear specifically designed for urban substations in Latin America, responding to increasing demand for space-saving and high-reliability distribution solutions in densely populated cities like São Paulo and Bogotá.

- In May 2023, Schneider Electric opened a new technical service center in Guadalajara, Mexico, aimed at enhancing local engineering support and accelerating project implementation for smart distribution panels and motor control centers in industrial and commercial sectors.

- In September 2023, Eaton Corporation partnered with a Chilean energy firm to distribute its SF6-free medium-voltage switchgear across South America, aligning with regional decarbonization goals and offering an environmentally responsible alternative to traditional insulation technologies.

- In February 2025, ABB entered into a joint venture with a Colombian electrical equipment distributor to strengthen its supply chain for arc-resistant switchgear and digital protection relays, targeting mining and renewable energy clients in the Andean region.

- In June 2025, General Electric acquired a Peruvian power systems integrator specializing in substation automation, allowing for localized production and faster deployment of digital distribution components across Andean and Amazonian markets.

MARKET SEGMENTATION

This research report on the Latin America power distribution component market is segmented and sub-segmented into the following categories.

By Product

- Switchgear

- Switchboard

- Distribution Panel

- Motor Control Panels

- Others

By Configuration

- Fixed Mounting

- Plug-in

- Withdrawable

By Voltage Rating

- ≤ 11 kV

- > 11 kV to ≤ 33 kV

- > 33 kV to ≤ 66 kV

- > 66 kV to ≤ 132 kV

By Country

- Brazil

- Argentina

- Mexico

- Rest of Latin America