Global LFP Cathode Powder Market Size, Share, Trends & Growth Forecast Report – Segmented By Product Type (Portable and Stationary), Application (Automotive, Power Generation, Industrial and Others), and Region (North America, Latin America, Europe, Asia Pacific, Middle East & Africa) - Industry Analysis (2026 to 2034)

Global LFP Cathode Powder Market Report Summary

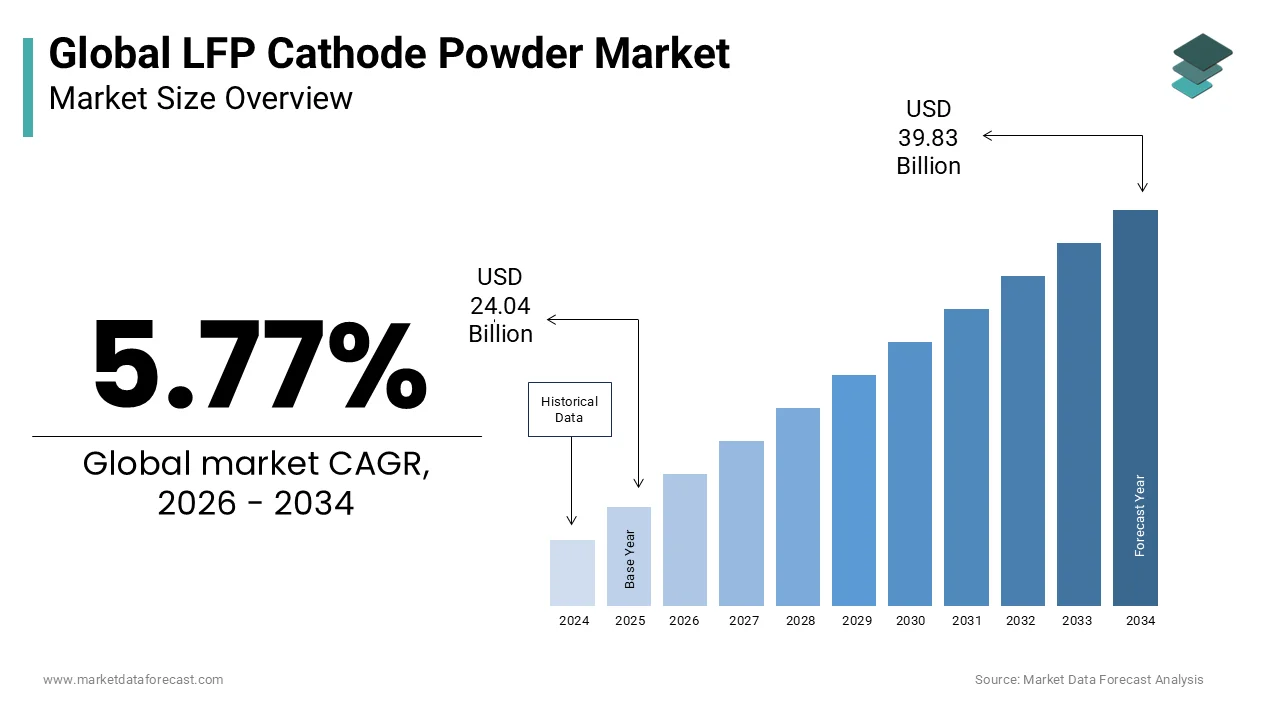

The global LFP cathode powder market was valued at USD 24.04 billion in 2025, is estimated to reach USD 25.43 billion in 2026, and is projected to reach USD 39.83 billion by 2034, growing at a CAGR of 5.77% during the forecast period. Market growth is driven by increasing demand for lithium iron phosphate batteries, rising adoption of electric vehicles, and growing investments in energy storage systems. LFP cathode materials are widely preferred due to their thermal stability, long cycle life, and safety advantages compared to other battery chemistries. The expansion of renewable energy integration and grid storage solutions is further supporting steady market growth globally.

Key Market Trends

- Rising adoption of electric vehicles is driving demand for LFP cathode materials.

- Increasing investments in energy storage systems are supporting market growth.

- Growing preference for safer and longer lasting battery chemistries is boosting adoption.

- Expansion of renewable energy integration is enhancing demand for battery storage solutions.

- Technological advancements in battery materials are improving performance and efficiency.

Segmental Insights

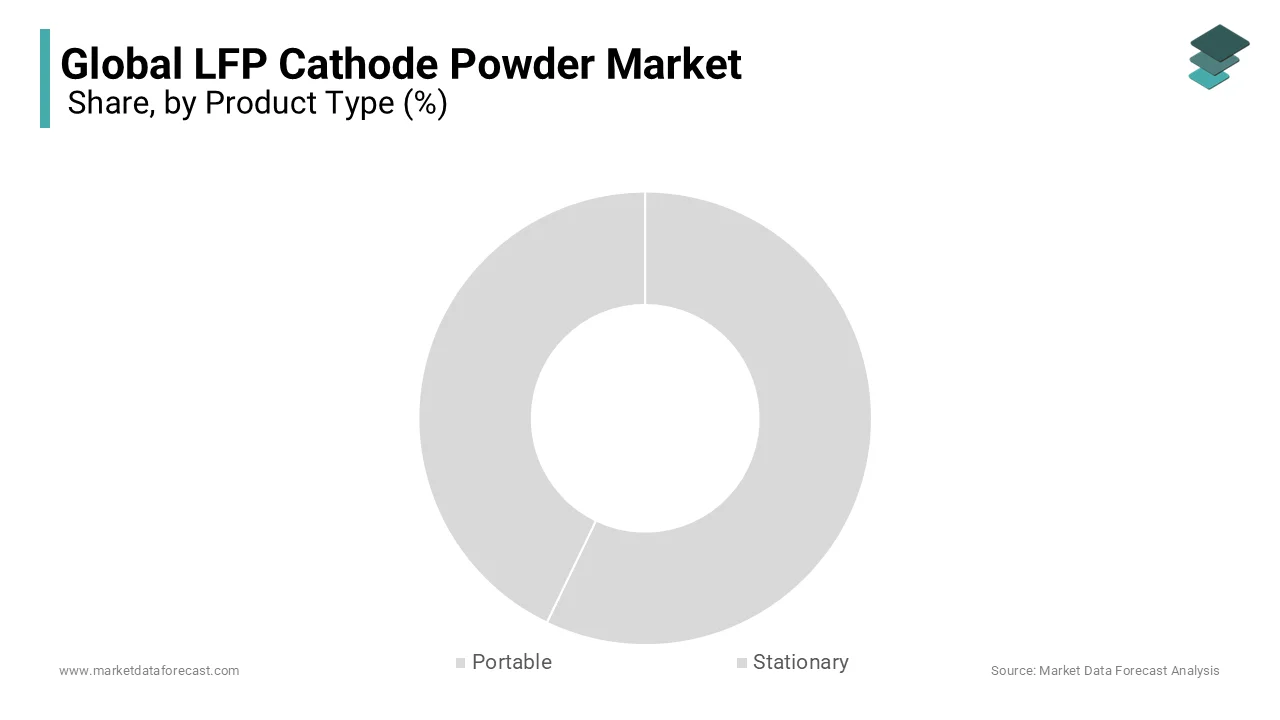

- Based on product type, the portable applications segment was the largest and held 61.2% of the global LFP cathode powder market share in 2025. This dominance is attributed to widespread use in consumer electronics such as smartphones, laptops, and portable devices.

- Based on application, the automotive segment accounted for 54.5% of the global LFP cathode powder market share in 2025. The segment’s growth is driven by increasing production and adoption of electric vehicles globally.

Regional Insights

- The global LFP cathode powder market is experiencing strong growth across regions, supported by increasing battery demand and industrial expansion.

- Asia Pacific was the leading region in 2025, driven by strong battery manufacturing capabilities, high electric vehicle adoption, and presence of major raw material suppliers and manufacturers.

Competitive Landscape

The global LFP cathode powder market is moderately competitive, with key players focusing on product innovation, capacity expansion, and strategic partnerships to strengthen their market position. Companies are investing in advanced battery technologies, supply chain optimization, and sustainable production methods. Prominent players in the global LFP cathode powder market include Targray, Pulead Technology Industry, Tesla, Novarials Corporation, Johnson Matthey, Aleees, Lithium Australia, Sumitomo Osaka Cement, BASF, Guizhou Anda Energy, and others.

Global LFP Cathode Powder Market Size

The global LFP cathode powder market size was valued at USD 24.04 billion in 2025 and is projected to reach USD 39.83 billion by 2034 from USD 25.43 billion in 2026, growing at a CAGR of 5.77%.

LFP cathode powder represents a critical segment within the global lithium ion battery supply chain, focusing on Lithium-Iron Phosphate materials that serve as the positive electrode in energy storage systems. This market is characterized by the production of high purity powders through processes such as solid state reaction or hydrothermal synthesis, which are essential for manufacturing safe and durable batteries. Unlike nickel based chemistries, LFP offers superior thermal stability and longer cycle life, making it indispensable for applications where safety and longevity are paramount. According to the International Energy Agency, electric vehicle sales reached approximately 10 million units globally in 2022, with a significant portion utilizing LFP chemistry due to its cost effectiveness. As per the United States Department of Energy, the abundance of iron and phosphate in the Earth's crust ensures a more stable and ethical supply chain compared to cobalt dependent alternatives. The market is further driven by the rapid expansion of stationary energy storage systems required to support renewable energy integration. Regulatory frameworks in major economies are increasingly favoring batteries with lower environmental footprints and reduced reliance on conflict minerals. The technological evolution towards higher energy density LFP variants, through methods like manganese doping, is also reshaping the landscape. This sector plays a pivotal role in the transition to sustainable energy by providing reliable storage solutions for both mobility and grid applications. The strategic importance of securing domestic LFP production capabilities has become a priority for many nations, aiming to reduce dependency on single source suppliers.

MARKET DRIVERS

Surging Adoption of Electric Vehicles in Emerging Markets Drives Demand for Cost Effective Battery Solutions

The rapid proliferation of electric vehicles in emerging markets is propelling the growth of the global LFP cathode powder market as manufacturers seek affordable and reliable battery chemistries to meet mass market needs. Consumers in regions such as Southeast Asia, Latin America, and India are highly price sensitive, making the lower cost structure of LFP batteries particularly attractive compared to nickel manganese cobalt alternatives. According to the International Energy Agency, the share of LFP batteries in the global electric vehicle market rose to nearly 30% in 2022, driven largely by adoption in China and expanding into other developing economies. As per the World Bank, economic growth in these regions is increasing disposable incomes, yet affordability remains a key barrier to widespread electric vehicle adoption. LFP cathode powder enables the production of batteries that reduce the overall vehicle cost by eliminating expensive raw materials like cobalt and nickel. Major automakers are increasingly integrating LFP packs into entry level and mid-range models to broaden their customer base. The robust cycle life of LFP batteries also aligns with the high utilization rates of commercial fleets and ride sharing services prevalent in these markets. Government incentives promoting electric mobility further accelerate this trend, by subsidizing vehicles equipped with domestically produced or cost efficient batteries. This shift towards affordable electrification ensures sustained demand for LFP cathode powder as the backbone of accessible green transportation solutions.

Expansion of Stationary Energy Storage Systems Supports Grid Stability and Renewable Integration

The extensive deployment of stationary energy storage systems is a significant driver for the LFP cathode powder market owing to the material’s exceptional safety profile and long operational lifespan. As countries worldwide strive to integrate intermittent renewable energy sources, such as solar and wind, into their grids, the need for reliable large scale storage becomes critical. According to the International Renewable Energy Agency, global renewable power capacity is expected to grow by over 50% between 2023 and 2027, necessitating substantial investments in energy storage infrastructure. LFP batteries are preferred for these applications because they exhibit minimal risk of thermal runaway and can withstand thousands of charge discharge cycles without significant degradation. As per the United States Environmental Protection Agency, the transition to clean energy requires storage solutions that are both environmentally sustainable and economically viable over decades of operation. Utility scale projects increasingly specify LFP chemistry, due to its ability to maintain performance under rigorous daily cycling conditions. The declining cost of LFP cathode powder further enhances the economic feasibility of these storage installations. Governments are implementing policies that mandate storage capacity alongside new renewable projects, creating a steady demand pipeline. This structural shift towards decentralized and resilient energy grids positions LFP cathode powder as a fundamental component in the global energy transition.

MARKET RESTRAINTS

Lower Energy Density Compared to Nickel Based Chemistries Limits Application in Long Range Vehicles

The inherent lower energy density of Lithium Iron Phosphate compared to nickel rich chemistries is a major restraint on the LFP cathode powder market, particularly in the premium electric vehicle segment. While LFP offers safety and cost benefits, its volumetric and gravimetric energy density is approximately 20% to 30% lower than that of Nickel Manganese Cobalt or Nickel Cobalt Aluminum batteries. According to the Argonne National Laboratory, this limitation necessitates larger and heavier battery packs to achieve the same driving range, which can compromise vehicle design and efficiency. As per the Society of Automotive Engineers, consumers demanding long range capabilities exceeding 400 miles often prefer vehicles equipped with higher energy density batteries, despite the higher cost. This constraint restricts the use of LFP cathode powder primarily to standard range vehicles and commercial applications, where weight and space are less critical. Automakers aiming to compete in the luxury market may hesitate to adopt LFP technology due to perceived performance limitations. Although advancements in cell to pack technology are mitigating some of these issues, the fundamental chemical limitation remains a barrier. The trade-off between range and cost means that LFP cannot fully replace high performance chemistries in all segments. This technological ceiling caps the total addressable market for LFP cathode powder in high end automotive applications.

Volatility in Lithium Raw Material Prices Impacts Production Costs and Supply Chain Stability

Fluctuations in the price of lithium carbonate and other raw materials is further hampering the expansion of the global LFP cathode powder market by creating uncertainty in production costs and supply chain planning. Although LFP does not use cobalt or nickel, it is still heavily dependent on lithium, which has experienced dramatic price swings in recent years. According to the London Metal Exchange, lithium carbonate prices surged by over 400% in 2022 before correcting sharply in 2023, reflecting market instability. As per the International Monetary Fund, such volatility makes it difficult for cathode manufacturers to maintain consistent pricing structures and profit margins. Sudden price spikes can erode the cost advantage of LFP batteries, making them less competitive against alternative chemistries during periods of low nickel prices. Supply chain disruptions caused by geopolitical tensions or export restrictions in key producing countries further exacerbate these challenges. Manufacturers must engage in complex hedging strategies or secure long term off take agreements to mitigate risks, which adds administrative burden and cost. The unpredictability of raw material availability can delay production schedules and hinder the ability to meet growing demand. Until lithium markets stabilize or alternative sourcing methods become commercially viable, price volatility will remain a persistent headwind for the LFP cathode powder industry.

MARKET OPPORTUNITIES

Development of Manganese Doped LFP Technologies Offers Enhanced Energy Density Opportunities

The innovation of manganese doped Lithium Iron Phosphate, which is known as LMFP presents a substantial opportunity for the LFP cathode powder market by addressing the energy density limitations of traditional LFP. By incorporating manganese into the crystal structure, LMFP increases the operating voltage from 3.4 volts to approximately 4.1 volts, resulting in a 15% to 20% improvement in energy density. According to the Journal of Power Sources, this enhancement allows LMFP batteries to approach the performance of nickel based chemistries while retaining the safety and cost benefits of LFP. As per the Chinese Ministry of Industry and Information Technology, several leading battery manufacturers have announced plans to commercialize LMFP cells for mainstream electric vehicles by 2025. This technological evolution opens new market segments for LFP cathode powder producers, who can upgrade their existing production lines with minimal capital expenditure. The ability to offer a drop in solution for current LFP manufacturing processes accelerates adoption rates. Automakers are increasingly interested in LMFP as a way to extend vehicle range without significantly increasing costs. The transition to LMFP also aligns with sustainability goals, by reducing the need for scarce nickel and cobalt resources. This innovation revitalizes the growth trajectory of the LFP market and expands its applicability to higher performance vehicles.

Recycling and Circular Economy Initiatives Create Sustainable Secondary Raw Material Streams

The emergence of robust recycling infrastructure and circular economy initiatives offers a significant opportunity for the LFP cathode powder market, by providing a sustainable source of raw materials. As the first generation of electric vehicles reaches end of life, the volume of recyclable LFP batteries is increasing rapidly. According to the European Commission, new regulations mandate higher recycling efficiency rates and material recovery targets for lithium ion batteries by 2030. As per the International Council on Clean Transportation, recovering lithium, iron, and phosphate from spent batteries can reduce dependency on virgin mining and lower the environmental footprint of cathode production. Advanced hydrometallurgical processes are being developed to efficiently extract high purity precursors from LFP waste streams. Cathode manufacturers can integrate these recycled materials into their supply chains to produce eco-friendly cathode powder with a lower carbon intensity. This approach appeals to environmentally conscious automakers and consumers who prioritize sustainability. Government subsidies and incentives for recycling facilities further support the development of this secondary market. By establishing closed loop systems, companies can mitigate raw material price volatility and enhance supply chain resilience. The growing emphasis on corporate social responsibility and environmental governance makes recycled LFP cathode powder an attractive value proposition for future growth.

MARKET CHALLENGES

Intense Competition from Alternative Battery Chemistries Threatens Market Share Retention

The significant competition from emerging battery technologies, such as solid state batteries and sodium ion batteries that promise superior performance or lower costs is primarily challenging the global LFP cathode powder market growth. Solid state batteries offer higher energy density and improved safety, potentially displacing LFP in premium automotive applications. According to the Toyota Research Institute, solid state technology is expected to reach commercial viability by the late 2020s, posing a long term threat to liquid electrolyte based systems. As per the Nature Energy journal, sodium ion batteries are gaining traction as a cost effective alternative for stationary storage and low speed vehicles due to the abundance of sodium. These alternatives could erode the market share of LFP cathode powder if they achieve scalable production and competitive pricing. Automakers are diversifying their battery portfolios to include multiple chemistries, reducing reliance on any single technology. The rapid pace of innovation in the battery sector requires LFP producers to continuously improve their products to remain relevant. Failure to adapt to changing technological landscapes could result in obsolescence. The threat of substitution is particularly acute in segments where cost and performance are critical decision factors. LFP manufacturers must invest in research and development to maintain their competitive edge against these disruptive technologies.

Complex Manufacturing Processes and Quality Control Requirements Increase Operational Barriers

The intricate manufacturing processes and stringent quality control requirements associated with LFP cathode powder production present a major challenge to market entry and scalability. Achieving consistent particle size distribution, crystallinity, and purity is critical for battery performance but difficult to maintain at large scales. According to the Journal of Materials Chemistry A, variations in synthesis parameters, such as temperature and atmosphere, can significantly affect the electrochemical properties of the final product. As per the International Organization for Standardization, adherence to strict quality standards is necessary to meet automotive grade specifications which require zero defect tolerance. Establishing facilities that can consistently produce high quality LFP powder requires substantial capital investment in specialized equipment and skilled personnel. Small and medium sized enterprises often struggle to meet these rigorous standards, limiting their ability to compete with established players. Any deviation in quality can lead to battery failures, recalls, and reputational damage. The need for continuous monitoring and process optimization adds to operational complexity and cost. Furthermore, the handling of nano sized particles poses health and safety risks, requiring advanced containment systems. These technical and regulatory hurdles create high barriers to entry, constraining the number of qualified suppliers in the market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.77% |

| Segments Covered | By Product Type, Application, Region. |

| Various Analyses Covered | Global, Regional, and Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa. |

| Market Leaders Profiled | Targray, Pulead Technology Industry, Tesla, Novarials Corporation, Johnson Matthey, Aleees, Lithium Australia, Sumitomo Osaka Cement, BASF, Guizhou Anda Energy, and Others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The portable applications segment dominated the market by holding 61.2% of the global market share in 2025. The dominance of portable segment in the global market is driven by the massive adoption of electric vehicles and consumer electronics. Major automotive manufacturers are shifting towards LFP chemistry for standard range vehicles to reduce dependency on scarce metals like cobalt and nickel. According to the International Energy Agency, electric car sales reached 14 million globally in 2023, with a significant portion utilizing LFP battery packs due to their affordability. As per the China Association of Automobile Manufacturers, over 50% of new energy vehicles sold in China now feature LFP batteries, reflecting a strong regional preference that influences global trends. The lightweight nature of modern LFP formulations also makes them suitable for portable consumer electronics, such as laptops and power tools, where safety is paramount. The ability of LFP batteries to withstand frequent charging cycles without significant degradation aligns with the usage patterns of portable devices. Furthermore, government subsidies for electric mobility in key markets accelerate the deployment of LFP based vehicles. The supply chain for portable applications is well established, allowing for economies of scale that further lower costs. This widespread integration into high volume consumer products ensures that the portable segment remains the largest consumer of LFP cathode powder globally.

On the other side, the stationary energy storage segment is estimated to grow at a CAGR of 29.2% in the global market during the forecast period owing to the grid modernization and renewable energy integration. The urgent need to stabilize electrical grids amidst the increasing penetration of intermittent renewable energy sources, such as solar and wind is further contributing to the expansion of the stationary energy storage segment in the global market. LFP batteries are ideal for stationary applications due to their long cycle life and thermal stability, which are critical for large scale installations. According to the International Renewable Energy Agency, global renewable capacity additions reached approximately 473 gigawatts in 2023, necessitating substantial energy storage infrastructure. As per the United States Department of Energy, investments in grid scale battery storage have increased significantly in recent years, with LFP chemistry accounting for the majority of new projects. The declining cost of LFP cathode powder makes these systems economically viable for utilities and commercial entities seeking to optimize energy usage. Regulatory mandates in regions like Europe and North America require utilities to incorporate storage solutions to enhance grid resilience. Additionally, the rise of behind the meter storage systems for residential and commercial buildings drives demand for safe and durable LFP batteries. The ability of LFP batteries to operate efficiently over thousands of cycles reduces the levelized cost of storage. This combination of regulatory support, economic feasibility, and technical suitability positions stationary storage as the most dynamic growth engine in the market.

By Application Insights

The automotive segment led the market by holding 54.5% of the global market share in 2025. The dominance of the automotive segment in the global market is driven by the aggressive electrification strategies adopted by major original equipment manufacturers worldwide, who are prioritizing LFP chemistry for its cost effectiveness and safety. The shift away from internal combustion engines has created an unprecedented demand for battery materials, with LFP emerging as a preferred choice for mass market vehicles. According to BloombergNEF, the average price of lithium iron phosphate battery packs fell below 100 dollars per kilowatt hour in 2023, making them competitive with traditional powertrains. As per the European Automobile Manufacturers Association, electric vehicle registrations in Europe have surged, with many entry level models adopting LFP batteries to meet affordability targets. The robust thermal stability of LFP reduces the risk of fire, enhancing consumer confidence in electric vehicles. Government incentives, such as tax credits and purchase subsidies, further stimulate demand for LFP equipped cars. Automakers are also forming strategic partnerships with cathode suppliers to secure long term material availability. The scalability of LFP production allows manufacturers to meet the high volume requirements of the automotive industry. This structural shift in vehicle propulsion technology ensures that the automotive segment remains the primary driver of LFP cathode powder consumption.

On the other side, the power generation segment is the fastest growing application segment and is predicted to record a promising CAGR of 31.1% over the forecast period owing to the global imperative to decarbonize energy systems and integrate renewable sources into the main grid. LFP batteries play a crucial role in smoothing out the variability of solar and wind power, by storing excess energy during peak production times and releasing it during demand spikes. According to the International Energy Agency, investment in clean energy technologies, including storage for power generation, is set to exceed 2 trillion dollars annually by 2030. As per the Global Wind Energy Council, offshore and onshore wind installations are expanding rapidly, requiring integrated storage solutions to ensure consistent power delivery. LFP cathode powder is essential for manufacturing the large format cells used in these utility scale storage systems. The long lifespan of LFP batteries reduces the frequency of replacements, lowering the total cost of ownership for power generators. Governments are implementing policies that mandate storage capacity for new renewable projects, further boosting demand. The ability of LFP batteries to operate safely in large clusters makes them the preferred choice for grid scale applications. This alignment with global sustainability goals and energy security initiatives drives the rapid expansion of the power generation segment.

REGIONAL ANALYSIS

Asia Pacific LFP Cathode Powder Market Analysis

Asia Pacific led the LFP cathode powder market in 2025 with the highest share of the global market in 2025. The dominance of Asia-pacific in the global market can be credited to the dominant manufacturing capabilities and robust electric vehicle adoption. Asia Pacific maintains its leadership position due to the presence of major battery manufacturers and cathode producers primarily in China, which controls a significant portion of the global supply chain. The region benefits from established infrastructure for raw material processing and battery cell assembly. According to the Chinese Ministry of Industry and Information Technology, China produced over 70% of the world's LFP cathode materials in 2023, supporting both domestic and international demand. As per the Japan Battery Association, neighboring countries are increasingly collaborating on technology development and supply chain integration to enhance regional competitiveness. The rapid urbanization and rising middle class in India and Southeast Asia are driving electric vehicle sales, further boosting local demand for LFP batteries. Government policies in countries like South Korea and Japan promote the development of advanced battery technologies, including LFP variants. The availability of skilled labor and competitive manufacturing costs attract foreign investment in production facilities. Additionally, the strong export orientation of Asian manufacturers ensures a steady flow of LFP cathode powder to global markets. This combination of production capacity, policy support, and market demand solidifies Asia Pacific's dominance in the global LFP landscape.

North America LFP Cathode Powder Market Analysis

North America represents a significant and rapidly growing market due to the legislative incentives and efforts to localize battery supply chains. North America is experiencing substantial growth in the LFP cathode powder market due to the Inflation Reduction Act, which provides tax credits for electric vehicles with batteries sourced from friendly nations or domestically. This legislation has spurred significant investment in local manufacturing facilities to reduce reliance on Asian suppliers. According to the United States Department of Energy, billions of dollars have been allocated to build a domestic battery ecosystem, including cathode production plants. As per the Canadian Mineral Processors, several projects in Canada and the United States are underway to process lithium and produce LFP cathode materials locally. Automakers in the region are actively securing supply agreements with emerging LFP producers to meet upcoming regulatory requirements. The growing consumer preference for sustainable transportation options further accelerates market expansion. State level initiatives in California and New York promote the adoption of electric vehicles and energy storage systems. The focus on energy security and supply chain resilience drives government support for domestic LFP production. These factors collectively position North America as a key growth region with increasing self-sufficiency in battery materials.

Europe LFP Cathode Powder Market Analysis

Europe holds a prominent position in the market and the growth of the European market can be credited to the stringent environmental regulations and ambitious climate goals. Europe is a key market for LFP cathode powder driven by the European Green Deal, which aims for carbon neutrality by 2050 and mandates the phase out of internal combustion engines. The region is witnessing a surge in electric vehicle adoption and renewable energy projects that require reliable storage solutions. According to the European Commission, the EU Battery Regulation sets strict sustainability and performance standards, encouraging the use of safe and recyclable materials like LFP. As per the European Automobile Manufacturers Association, electric vehicle sales in Europe continue to rise, with many manufacturers introducing LFP based models to offer affordable options. Investments in gigafactories across Germany, France, and Hungary are increasing local production capacity for LFP batteries. The region strong focus on circular economy principles supports the development of recycling infrastructure for LFP materials. Government subsidies and grants facilitate the establishment of domestic cathode production facilities. The emphasis on reducing carbon footprints throughout the supply chain favors LFP chemistry, due to its lower environmental impact compared to nickel based alternatives. This regulatory and market environment ensures steady growth for the LFP cathode powder sector in Europe.

Latin America LFP Cathode Powder Market Analysis

Latin America is an emerging market with significant potential. The abundant raw material reserves and growing electric mobility initiatives are driving Latin American market expansion. Latin America is leveraging its rich lithium resources, particularly in Chile, Argentina, and Bolivia, to develop a local LFP cathode powder industry. The region is attracting international investment to establish processing facilities that can add value to raw lithium exports. According to the United Nations Economic Commission for Latin America and the Caribbean, initiatives to promote electric public transportation are gaining momentum in major cities, creating demand for LFP batteries. As per the Brazilian Automotive Vehicle Manufacturers Association, Brazil is implementing policies to incentivize the production and adoption of electric vehicles, including those with LFP batteries. The availability of low cost renewable energy in countries like Brazil and Chile supports sustainable battery manufacturing processes. Regional collaborations aim to create a integrated supply chain from mining to cathode production. Government efforts to diversify economies beyond traditional commodities drive support for the battery sector. The growing awareness of environmental issues among consumers and policymakers further encourages the shift towards clean energy solutions. These developments position Latin America as a promising emerging market, with unique advantages in raw material availability.

Middle East and Africa LFP Cathode Powder Market Analysis

The Middle East and Africa represent a nascent but strategically important market and is driven by economic diversification and energy transition goals. The Middle East and Africa are beginning to explore the LFP cathode powder market as part of broader strategies to diversify economies away from fossil fuels and invest in future technologies. Countries like Saudi Arabia and the United Arab Emirates are investing heavily in renewable energy projects and electric vehicle infrastructure. According to the Saudi Ministry of Investment, the kingdom aims to localize electric vehicle manufacturing, including battery production, as part of its Vision 2030 plan. As per the African Union, initiatives to improve energy access through off grid solar solutions are driving demand for stationary storage systems using LFP batteries. The region abundant solar resources make it ideal for renewable energy projects that require efficient storage. International partnerships are facilitating technology transfer and capacity building in battery manufacturing. The focus on sustainable urban development in major cities supports the adoption of electric public transport. Although the market is currently small, the strategic investments and policy commitments indicate significant long term potential. The region role in global energy dynamics ensures that it will become an increasingly important participant in the LFP value chain.

COMPETITIVE LANDSCAPE

The competition in the LFP Cathode Powder Market is intense and characterized by the presence of established chemical giants and specialized material producers. Major players compete on the basis of product quality cost efficiency and supply chain reliability to secure contracts with leading battery manufacturers. The market is moderately consolidated with a few dominant companies holding significant influence over pricing and availability. Competitive advantage is often derived from vertical integration which allows control over raw material sourcing and production costs. Technological innovation plays a crucial role as companies strive to improve the performance metrics of LFP materials. Regulatory compliance regarding environmental sustainability serves as a key differentiator in attracting environmentally conscious clients. New entrants face high barriers due to substantial capital requirements and technical expertise needed for production. Strategic alliances and joint ventures are common as firms seek to expand their geographic reach and technological capabilities. Overall the market rewards companies that can demonstrate consistent quality scalability and adherence to sustainability standards.

KEY MARKET PLAYERS

The major key players of the global LFP cathode powder market are

- Targray

- Pulead Technology Industry

- Tesla

- Novarials Corporation

- Johnson Matthey

- Aleees

- Lithium Australia

- Sumitomo Osaka Cement

- BASF

- Guizhou Anda Energy

- Others

Top Players in the Market

- Hunan Yuneng is a leading global supplier of lithium iron phosphate cathode materials with extensive production capabilities. The company contributes to the global market by providing high performance LFP powder to major battery manufacturers worldwide. Hunan Yuneng has recently expanded its production capacity through new facilities in China to meet surging demand from electric vehicle makers. They focus on technological innovation to improve energy density and cycle life of their products. The company also emphasizes sustainable manufacturing practices to align with global environmental standards. By securing long term supply agreements with key industry players Hunan Yuneng strengthens its market position. Their commitment to quality and scalability ensures they remain a critical partner in the global battery supply chain supporting the transition to clean energy mobility solutions effectively.

- Dynanonic is a prominent player in the LFP cathode powder market known for its advanced material science and manufacturing expertise. The company supplies high quality LFP materials to battery producers across Asia and Europe. Dynanonic contributes to the global market by continuously improving the electrochemical performance of its cathode powders. Recently the company has invested in research and development to create next generation LFP variants with enhanced conductivity. They have also established strategic partnerships with raw material suppliers to ensure stable input costs. Dynanonic focuses on expanding its international footprint by setting up distribution centers in key markets. These actions help the company maintain competitiveness and respond quickly to customer needs. Their dedication to innovation and customer service solidifies their reputation as a reliable supplier in the rapidly evolving battery industry.

- Tianqi Lithium is a major integrated lithium producer that has vertically expanded into LFP cathode powder manufacturing. The company leverages its access to lithium resources to produce cost competitive cathode materials for the global market. Tianqi contributes by ensuring a secure supply chain from raw material extraction to final product delivery. Recently the company has announced plans to build large scale LFP production bases to capture growing market opportunities. They are collaborating with technology partners to optimize production processes and reduce environmental impact. Tianqi also engages in joint ventures with battery manufacturers to develop customized solutions. These strategic moves enhance their value proposition and strengthen their position in the supply chain. By integrating upstream and downstream operations Tianqi ensures consistency and reliability in delivering high quality LFP cathode powder to global customers.

Top Strategies Used by the Key Market Participants

Key players in the LFP Cathode Powder Market primarily focus on vertical integration to secure raw material supplies and reduce production costs. Companies invest heavily in expanding manufacturing capacity to meet the escalating demand from electric vehicle and energy storage sectors. Strategic partnerships with battery manufacturers and automakers ensure long term off take agreements and market stability. Innovation in product formulation aims to enhance energy density and charging speed while maintaining safety standards. Sustainability initiatives such as green manufacturing and recycling programs are increasingly adopted to comply with regulatory requirements. Geographic expansion into emerging markets allows firms to diversify revenue streams and mitigate regional risks. Continuous research and development efforts drive technological advancements that differentiate products in a competitive landscape. These strategies collectively enable participants to maintain leadership and adapt to dynamic market conditions effectively.

MARKET SEGMENTATION

This research report on the global LFP cathode powder market has been segmented and sub-segmented based on product type, application, and region.

By Product Type

- Portable

- Stationary

By Application

- Automotive

- Power Generation

- Industrial

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1.What is LFP cathode powder?

LFP cathode powder is a lithium iron phosphate material used as the cathode in lithium ion batteries, valued for its high safety, long cycle life, and thermal stability.

2.What are the key applications of LFP cathode powder?

It is widely used in electric vehicles, stationary energy storage systems, consumer electronics, and industrial equipment.

3.What factors are driving the LFP cathode powder market?

Key growth drivers include rising electric vehicle adoption, increasing renewable energy integration, and demand for cost effective and safe battery chemistries.

4.What are the advantages of LFP cathode powder?

LFP offers excellent thermal stability, long lifespan, low cost, and enhanced safety compared to other cathode materials.

5.How does LFP compare with NMC and NCA cathodes?

LFP provides better safety and longer cycle life, while NMC and NCA offer higher energy density but at higher cost and lower thermal stability.

6.What are the different types of LFP cathode powder?

The market includes nano structured and micro structured LFP powders, designed for different performance and cost requirements.

7.Which region leads the LFP cathode powder market?

Asia Pacific dominates due to large scale battery manufacturing and strong electric vehicle demand, especially in China.

8.What challenges does the LFP cathode powder market face?

Challenges include lower energy density compared to alternatives, raw material supply constraints, and evolving battery technologies.

9.What is the future outlook for the LFP cathode powder market?

The market is expected to grow steadily with increasing investments in battery manufacturing and expansion of energy storage projects.

10.How is technology improving LFP cathode performance?

Advancements focus on improving conductivity, energy density, and charging speed through material coating and nano engineering techniques.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com