Global Marine Battery Market Size, Share, Trends, and Growth Analysis Report, Segmented by Application (Marine Starting Service, Deep Cycle Service, Dual Purpose Service), Ship Type (Commercial and Defense), & Region, Industry Forecast From 2025 to 2033

Global Marine Battery Market Size

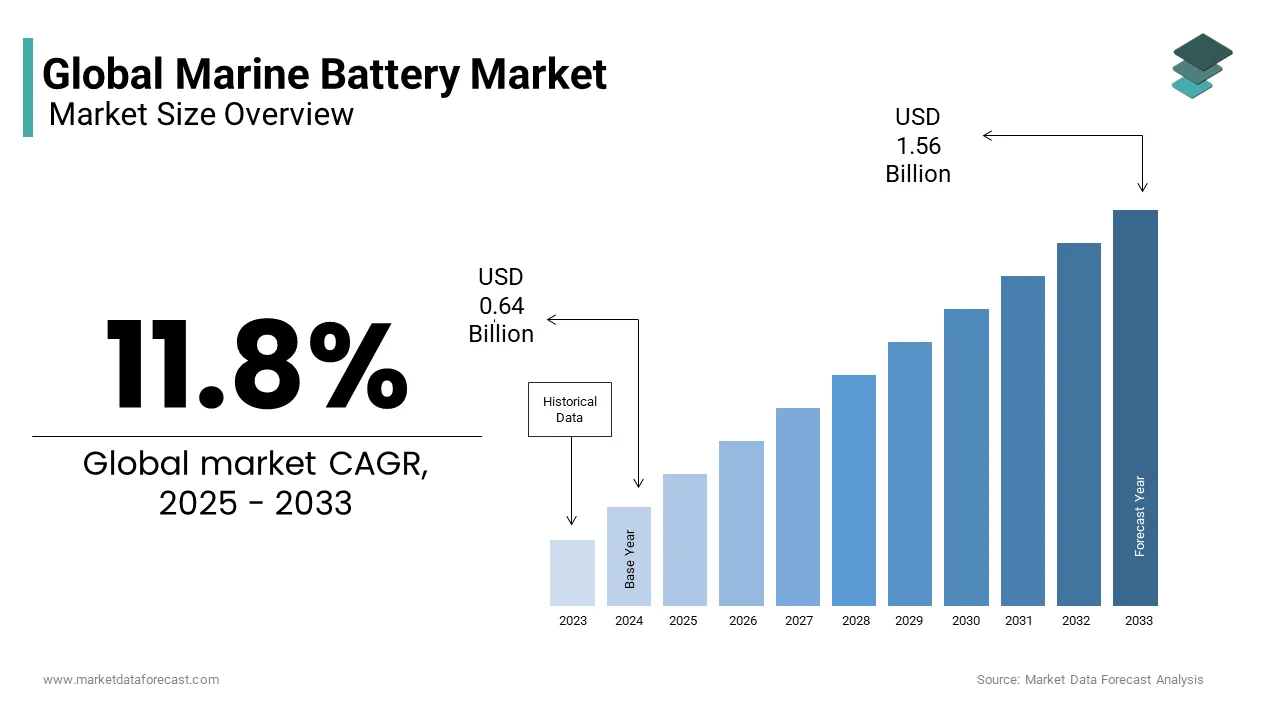

The global marine battery market was valued at USD 0.57 billion in 2024 and is anticipated to reach USD 0.64 billion in 2025 and USD 1.56 billion by 2033, growing at a CAGR of 11.8% during the forecast period from 2025 to 2033.

Marine battery refers to the electrochemical energy storage systems engineered specifically for maritime applications, including propulsion, auxiliary power, onboard electronics, and emergency backup across commercial, recreational, and naval vessels. These batteries must endure extreme environmental stressors such as saltwater corrosion, constant vibration, wide temperature fluctuations, and prolonged partial state of charge operation, conditions that render standard automotive or industrial batteries unsuitable. As per sources such as the International Chamber of Shipping (ICS) and the European Maritime Safety Agency (EMSA), approximately ninety percent of global trade by volume is transported by sea, and this logistical backbone is undergoing an energy transition. Regulatory mandates such as the IMO’s Carbon Intensity Indicator and the European Union’s FuelEU Maritime regulation are compelling vessel operators to reduce emissions, accelerating the adoption of hybrid and fully electric propulsion systems. According to DNV's Maritime Forecast to 2050, the share of the global merchant fleet requiring some form of battery integration (hybrid or fully electric) is projected to increase substantially. Beyond propulsion, safety-critical systems such as navigation, communication, and emergency lighting rely on uninterruptible battery power, governed by stringent classification society rules from Lloyd’s Register and Bureau Veritas. The marine battery is no longer a passive component but a strategic enabler of operational efficiency, regulatory compliance, and environmental stewardship in the global maritime domain.

MARKET DRIVERS

Stringent Global Emission Regulations Are Forcing Retrofit and Newbuild Adoption of Marine Battery Systems

International and regional maritime regulators are imposing progressively tighter emissions controls, which accelerates the growth of the global marine battery market. These regulations make battery hybridization not optional but mandatory for continued vessel operation. International regulations mandate that large vessels must significantly decrease their carbon intensity. New rules cap the greenhouse gas intensity of energy used on board ships in European Union waters, with penalties imposed for non-compliance. As per a study, the maritime transport sector is a notable contributor to transport-related CO2 emissions, increasing political and environmental pressure to transition towards electrification. Classification societies are responding. The number of certified battery-hybrid vessels is consistently increasing year over year, demonstrating growing industry adoption. Specific national requirements for zero-emission operations in sensitive marine areas have led to substantial reductions in local emissions through the use of battery technology. Shipowners are investing pre-emptively. Major shipping companies are now integrating large-scale battery systems into existing container vessels to optimize engine efficiency. Regulatory momentum is not slowing. The IMO’s revised strategy targets net zero emissions by or around 2050, which ensures battery demand will escalate as compliance deadlines approach.

Rapid Expansion of Short Sea Shipping and Electric Ferry Fleets Is Creating Structured Demand for High-Cycle-Life Marine Batteries

Coastal and inland waterway transport is undergoing electrification at an unprecedented pace, particularly in regions prioritizing urban air quality and noise reduction, which also contributed to the expansion of the global marine battery market. According to sources, hundreds of fully electric or hybrid ferries are now in commercial operation globally, with hundreds more on order. Norway leads this transition, operating a significant number of electric ferries that dramatically cut annual carbon emissions, as per research. China is rapidly scaling. Its use of electric water transport has recently deployed numerous electric cargo barges equipped with substantial battery systems designed for efficient charging cycles. A key region in North America has committed to a complete transition to an all-electric public ferry fleet within the next couple of decades, requiring a large capacity of marine-grade batteries. These vessels operate on fixed routes with predictable charging windows, making them ideal for high-cycle lithium-ion chemistries. Across busy European waters, these electric ferries run continuous daily routes, completing multiple charge and discharge cycles, which necessitate batteries with high durability and longevity ratings. This operational rhythm is creating a standardized, high-volume market segment that battery manufacturers are tailoring products for, including liquid-cooled packs and integrated battery management systems certified for marine safety.

MARKET RESTRAINTS

High Upfront Capital Costs Remain a Critical Barrier to Widespread Marine Battery Adoption

The steep upfront cost of marine battery technology often discourages vessel operators, even when substantial long-term savings are achievable, and degrades the growth of the global marine battery market. This restraint is particularly evident in price-sensitive segments such as small cargo, fishing, and regional passenger transport. The installed cost of a marine battery system varies significantly based on safety certifications and integration complexity. For midsize coastal ferries, this cost represents a substantial portion of the total conversion cost, posing a significant barrier without external financial support. A majority of shipowners delay electrification due to capital constraints. Safety mandates from classification societies for redundant cooling, fire suppression, and monitoring systems can increase system costs. Classification requirements add expense. Insurance premiums also remain elevated. Furthermore, insurance premiums for battery-equipped vessels are higher compared to conventional vessels because of perceived fire risk. Many operators will postpone adoption of green technology without scalable leasing models, government grants, or other incentives, despite regulatory and environmental pressures.

Lack of Standardized Global Safety Certification Frameworks Is Fragmenting Market Development and Delaying Deployment

Marine battery systems must satisfy overlapping and sometimes conflicting safety standards from classification societies, flag states, and port authorities, which ultimately obstructs the expansion of the global marine battery market. These varied requirements create regulatory uncertainty that slows procurement and installation. According to research, while technical specifications for land-based energy storage are harmonized, marine applications lack a unified global standard for fire containment, thermal runaway propagation, and crashworthy enclosures. Classification societies each maintain proprietary rules. DNV’s DNV ST 0387, Bureau Veritas’ NR 545, and Lloyd’s Register’s E20 do not fully align on cell-level testing, ventilation requirements, or emergency disconnect protocols. As per studies, a portion of shipowners delayed battery projects due to unclear or evolving certification pathways. This fragmentation increases engineering costs and time to market. The lack of a unified technical framework among global regulatory bodies is keeping marine battery deployment slower and more expensive than required.

MARKET OPPORTUNITIES

Emergence of Second Life Marine Battery Applications Is Unlocking Circular Economy Value Chains

Retired electric vehicle batteries, though no longer suitable for automotive use, are increasingly being repurposed for less demanding marine applications such as auxiliary power, hotel load support, and short-duration peak shaving, which opens new growth opportunities for the global marine battery market. These retired electric vehicle batteries retain seventy to eighty percent of their original capacity. Companies are partnering with maritime operators to validate marine reuse. Classification societies are adapting. The European Commission’s Battery Regulation now mandates extended producer responsibility, incentivizing manufacturers to design for reuse. This circular model not only reduces lifecycle emissions but also lowers entry barriers for smaller operators, democratizing access to marine electrification.

Integration of Smart Battery Management Systems With Vessel Digital Twins Is Enabling Predictive Performance Optimization

Advanced marine batteries are no longer standalone power sources but intelligent nodes within a vessel’s digital ecosystem, which communicate real-time data to optimize efficiency, extend lifespan, prevent failures, and provide fresh prospects for the expansion of the global marine battery market. Companies embed computing-capable battery management systems that analyze cell voltage, temperature gradients, and impedance trends to predict degradation and recommend charge protocols. In a trial conducted by Wärtsilä on the Norwegian offshore supply vessel Viking Princess, the hybrid system with batteries enabled fuel savings of approximately 30 percent and is expected to lead to significantly reduced maintenance costs due to lower engine running hours. Data from these systems feeds into vessel digital twins, allowing operators to simulate energy flows under different sea conditions and adjust power distribution preemptively. Classification societies are recognizing the safety value. This convergence of electrochemistry and artificial intelligence is transforming marine batteries from passive components into active, adaptive, and self-optimizing assets.

MARKET CHALLENGES

Marine Battery Fire Risk Perception Persists Despite Technological Mitigations, Constraining Insurance and Financing Availability

The perceived risk of catastrophic battery fires continues to influence insurance underwriting and lender risk assessment, which constrains the growth of the global marine battery market. This situation is despite significant advances in cell chemistry, thermal management, and containment design. According to the North P&I Club, marine battery-related incidents, though statistically rare, account for disproportionately high claims due to total vessel loss potential and complex salvage operations. Insurers require extensive safety documentation, third-party testing, and crew training before offering coverage, adding months to project timelines. Fires involving lithium-ion batteries on ferries receive extensive media coverage, which heightens public and regulatory anxiety, despite them being statistically infrequent. Classification societies mandate expensive countermeasures. Classification societies mandate strict safety requirements for battery installations, such as isolating battery rooms with highly fire-rated bulkheads and installing dedicated fire suppression systems, which substantially increases the overall cost of the battery system. Lenders remain cautious. Financial and legal obstacles will remain, despite technical capabilities, until large-scale incident data proves long-term safety and insurers create standard risk models.

Absence of Port Side Charging Infrastructure Is Creating Operational Bottlenecks for Electric and Hybrid Vessels

The lack of high-power, standardized, and geographically dispersed shore charging infrastructure limits their operational range and utility, even when vessels are equipped with advanced battery systems, thereby challenging the expansion of the global marine battery market. According to sources, the vast majority of major ports around the world currently lack the necessary infrastructure to provide large-scale charging solutions for commercial vessels. Specific regions have very few operational shore power systems that can support modern battery electric ferries. The situation is worse in developing economies. Ports in key developing regions do not yet possess the operational fast-charging stations required for cargo ships. This forces operators to rely on onboard generators, negating emissions benefits. Even where infrastructure exists, interoperability is lacking. The Baltic Sea region has different plug and communication standards, which require vessels to carry multiple adapters. The marine battery revolution will only scale globally if there is synchronized investment in grid capacity, connector harmonization, and smart load management; without these changes, it will be limited to short routes and subsidized projects.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 11.8% |

| Segments Covered | By Ship Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | East Penn Manufacturing Co. (US), EnerSys (US), EverExceed Industrial Co., Ltd (China), Exide Technologies (US), GS Yuasa (Japan), HBL Power Systems Limited (India), Korea Special Battery (South Korea), Manbat Ltd (UK), Saft Groupe SA (France), Systems Sunlight SA (Greece) and Zibo Torch Energy (China). |

SEGMENTAL ANALYSIS

By Application Insights

In 2024, the deep-cycle service batteries segment dominated the marine battery market by capturing a 54.7% share. The dominance of the deep cycle service batteries segment is attributed to its important role in powering electric and hybrid propulsion systems, hotel loads, and onboard electronics that demand sustained energy discharge over hours rather than short bursts. According to research, a vast majority of new electric ferries and hybrid offshore supply vessels utilize advanced battery configurations, such as deep-cycle lithium-ion or advanced lead-acid systems. This preference is due to their proven capability to endure thousands of partial discharge cycles without notable performance degradation. In regions with significant fleets of battery-powered ferries, individual vessels cycle their deep-cycle battery banks multiple times a day. This operational requirement translates into a very high number of full equivalent cycles accumulated annually. Recreational boating is also shifting. Regulatory pressure further entrenches this segment. Their technical suitability for evolving vessel architectures ensures sustained market primacy.

The dual-purpose service segment is estimated to register the fastest CAGR of 22.1% from 2025 to 2033. The rapid expansion of the dual-purpose service segment is fueled by the proliferation of smaller commercial and recreational vessels that cannot accommodate separate battery banks due to space or cost constraints. Fishing boats, pilot vessels, and coastal patrol craft increasingly adopt dual-purpose systems to simplify maintenance and reduce weight. In the recreational segment, the trend toward compact electric outboards is driving demand. Technological advances are enabling this convergence. Companies have developed absorbed glass mat and lithium iron phosphate variants that meet cold cranking amp requirements while sustaining a substantial number of deep cycles. Classification societies are adapting too. Dual-purpose batteries are now standard for mass-market vessels as electrification moves beyond luxury yachts and ferries.

By Ship Insights

The commercial vessels segment held the leading share of the marine battery market in 2024. The supremacy of the commercial vessels segment is driven by the convergence of international emissions regulations, fuel cost volatility, and operational efficiency demands that make battery integration economically and legally unavoidable. According to sources, Vessels above five thousand gross tonnage are required to implement energy efficiency measures, and battery hybridization is becoming a leading solution for optimizing auxiliary loads. Container shipping leaders are responding. Ferry operators are even more aggressive. Most new ferries being ordered in Europe are specifying integrated battery systems to enable zero-emission operations while in port. Inland waterway transport is also transforming. Unlike defense applications, commercial adoption is volume-driven, standardized, and accelerated by return on investment calculations, making it the anchor of global market growth.

The defense vessels segment is estimated to register the fastest CAGR of 27.3% from 2025 to 2033. The swift growth of the defence vessels segment is credited to strategic imperatives for silent mobility, energy resilience, and reduced thermal signature in contested environments. Naval forces increasingly deploy battery systems not for emissions compliance but for tactical advantage. Unmanned surface and underwater vehicles are almost exclusively battery-powered. European navies are equally committed. Classification for defense is less constrained by civilian standards, allowing faster adoption of cutting-edge chemistries such as lithium titanate and solid-state. Budgetary prioritization also accelerates deployment. Naval doctrine is evolving toward distributed, low-observable operations, making battery systems mission-critical enablers rather than mere auxiliary components.

REGIONAL ANALYSIS

Europe Market Analysis

Europe led the global marine battery market by occupying a 43.6% share in 2025. The demand for marine batteries in Europe is driven by aggressive regulatory frameworks, concentrated short sea shipping corridors, and coordinated public-private investment in charging infrastructure. Norway alone accounts for a notable share of global electric ferry deployments, which typically use substantial installed battery capacity per vessel. New rules are mandating that all ships calling at major ports must reduce their emissions intensity starting in the near future. Germany and the Netherlands are expanding inland waterway electrification. A major European shipping corridor has seen a notable increase in the number of electric cargo barges entering service recently. Port infrastructure is advancing in parallel. Classification harmonization also aids adoption. Europe’s combination of policy enforcement, technical standardization, and infrastructure maturity makes it the global benchmark for marine battery deployment.

Asia Pacific Market Analysis

Asia Pacific secured the second position in the global marine battery hierarchy by capturing a share of 31.4% in 2024. The expansion of the APAC market is attributed to domestic manufacturing and coastal electrification. China dominates this segment, manufacturing a significant share of the world’s marine-grade lithium-ion cells and deploying them domestically at an unprecedented scale. India is emerging as a secondary hub. Japan and South Korea are advancing high-tech naval and commercial applications. Domestic battery supply chains reduce costs. Government subsidies further accelerate adoption. Asia Pacific’s growth is not just consumption-driven but innovation and production-led, positioning it as the manufacturing engine of the global marine battery transition.

North America Market Analysis

North America is also a noteworthy region in the global marine battery market. The region leads Europe in defense and recreational innovation, despite lagging in commercial applications. Recreational boating is also transforming. Regulatory catalysts are emerging. Private investment is accelerating. Companies are scaling production of all-electric recreational boats with integrated battery management. North America’s strength lies not in volume but in high-value, high-technology applications that set global benchmarks for performance and safety.

Latin America Market Analysis

Latin America is rapidly expanding in the global marine battery market because of riverine and coastal transport, where diesel dependency imposes high economic and environmental costs. Brazil leads deployment on the Amazon River. Colombia is electrifying its Magdalena River corridor. Chile is pioneering coastal applications. Financing mechanisms are evolving. Climate vulnerability also drives urgency. Latin America’s approach is pragmatic, localized, and economically grounded, focusing on routes where batteries deliver immediate operational ROI.

Middle East and Africa Market Analysis

The Middle East and Africa region is predicted to expand in the global marine battery market between 2025 and 2033. Its growth is nascent but strategically focused on port efficiency and naval capability. The United Arab Emirates leads regional investment. Egypt is integrating batteries into Suez Canal support vessels. Naval modernization is another driver. South Africa is piloting inland applications. Transnet installed battery electric workboats in Durban Harbor to reduce diesel particulate emissions in enclosed basins. Challenges remain. However, donor-funded initiatives are emerging. Though small today, the region is laying institutional and infrastructural groundwork for accelerated adoption post 2027.

COMPETITIVE LANDSCAPE

The gasoline fuel additives market features intense rivalry among multinational chemical producers, specialty formulators, and regional innovators competing on performance efficacy, regulatory compliance, and pricing agility. Major participants differentiate through proprietary detergent, octane booster, and corrosion inhibitor blends tailored to regional fuel specifications and engine technologies. Strategic acquisitions of niche additive developers have expanded product portfolios and accelerated entry into emerging markets. Long-term supply agreements with refiners and fuel retailers secure volume commitments but compress margins, prompting innovation in high-value niche segments such as ethanol compatibility and deposit control for direct injection engines. Volatility in raw material prices, particularly for polyisobutylene and polyetheramines, forces players to hedge procurement and optimize formulations dynamically. Environmental regulations in North America and Europe drive investment toward bio-based and low-toxicity additives. Asia Pacific witnesses aggressive competition through localized manufacturing and price undercutting, while Latin America sees consolidation as multinationals acquire domestic blenders to strengthen distribution networks and regulatory influence.

KEY MARKET PLAYERS

A few of the notable players in the global marine battery market are

- East Penn Manufacturing Co. (US)

- EnerSys (US)

- Leclanché SA

- Corvus Energy

- EverExceed Industrial Co., Ltd (China)

- Exide Technologies (US)

- GS Yuasa (Japan)

- HBL Power Systems Limited (India)

- Korea Special Battery (South Korea)

- Manbat Ltd (UK)

- Saft Groupe SA (France)

- Systems Sunlight SA (Greece)

- Zibo Torch Energy (China).

Top Players In The Market

Corvus Energy is a global pioneer in maritime energy storage systems, supplying lithium-ion battery solutions for ferries, offshore vessels, and naval platforms. The company designs modular, scalable systems certified by all major classification societies for safety and performance under harsh marine conditions. It also launched an AI-driven predictive battery analytics platform that extends cell life by twenty-five percent through adaptive charging algorithms. Corvus continues to expand manufacturing in Canada and Norway to meet surging global demand while maintaining stringent quality control.

EnerSys provides advanced lead acid and lithium ion marine batteries tailored for engine starting, deep cycle, and dual purpose applications across commercial and defense fleets. Its Odyssey and Thin Plate Pure Lead product lines are widely specified for their vibration resistance and reliability in extreme environments. The company also opened a dedicated marine battery validation center in South Carolina to accelerate certification and customer testing. EnerSys invests heavily in ruggedized enclosures and thermal management to ensure operational continuity in mission-critical maritime settings.

Leclanché SA delivers high-performance marine battery systems with a focus on sustainability, utilizing recyclable materials and second-life integration strategies. Its lithium titanate and lithium iron phosphate chemistries are engineered for ultra-long cycle life and rapid charging, ideal for short sea shipping and port operations. The company also introduced its Marine Rack System with integrated liquid cooling and cloud-connected diagnostics for real-time health monitoring. Leclanché collaborates closely with shipyards and classification bodies to ensure seamless integration and compliance with evolving safety standards worldwide.

Top Strategies Used by Key Market Participants

Leading players in the marine battery market prioritize strategic partnerships with shipbuilders and classification societies to co-engineer systems that meet exacting safety and performance criteria from the design phase. They invest in localized manufacturing and assembly hubs near key maritime corridors to reduce logistics costs and delivery timelines. Companies increasingly embed digital intelligence into battery packs, enabling predictive maintenance and remote diagnostics to enhance vessel uptime. Vertical integration of cell production and pack assembly ensures supply chain control amid global material shortages. Product portfolios are diversified to serve bothhigh-endd defense applications and cost-sensitive commercial segments through modular architecture. Regulatory alignment is proactive; firms engage early with maritime authorities to shape emerging standards. Training programs for ship crews and service technicians build operational confidence and reduce warranty claims. These strategies collectively reinforce technical leadership, geographic reach, and lifecycle value in a rapidly evolving market.

MARKET SEGMENTATION

This research report on the global marine battery market has been segmented and sub-segmented based on the ship type, application, and region.

By Ship Type

- Commercial

- Defense

By Application

- Marine Starting Service

- Deep Cycle Service

- Dual Purpose Service

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

What are marine batteries, and why is demand surging globally?

Marine batteries store and supply electrical power for propulsion, auxiliary systems, and onboard equipment on vessels. Demand is accelerating due to electrification of ferries, port operations, and inland waterway transport—driven by IMO decarbonization targets and zero-emission port mandates.

Which vessel types are leading battery adoption?

Short-sea shipping, hybrid/electric ferries (e.g., Norway’s MF Hydra), cruise ship hotel-load systems, and harbor craft dominate early adoption—where predictable routes and frequent docking enable feasible charging and ROI.

What battery chemistries dominate the marine sector?

Lithium-ion (NMC and LFP) prevails for high energy/power density and cycle life; LFP is gaining preference for enhanced safety and thermal stability. Emerging interest exists in sodium-ion and solid-state for future deep-sea applications.

How do classification societies influence battery system design?

DNV, ABS, LR, and Bureau Veritas enforce rigorous standards (e.g., DNV-RU-SHIP Pt.5 Ch.7) for fire safety, containment, monitoring, and redundancy—making certified, modular, and intrinsically safe battery systems a prerequisite for newbuilds and retrofits.

Which regions are at the forefront of marine electrification?

Europe leads—especially Norway, the Netherlands, and Germany—with strong policy support and hydrogen/electric ferry deployments. Asia-Pacific (China, Japan, Singapore) is scaling rapidly in port equipment and inland vessels, while North America focuses on ferries and short-haul tugs.

Who are the key battery and system integrators?

Leading suppliers include Corvus Energy (Canada), Ampelmann (Netherlands), Leclanché (Switzerland), CATL (China), and BYD—offering containerized Energy Storage Systems (ESS) with integrated BMS, cooling, and remote diagnostics tailored for marine environments.

How are charging infrastructures evolving?

Megawatt-scale shore power (cold ironing), automated connection systems (e.g., ABB’s Azipod® with battery hybrid), and battery-as-a-service (BaaS) models are emerging to overcome port grid limitations and reduce upfront CAPEX.

What challenges hinder wider adoption?

High upfront costs, space/weight constraints on retrofits, regulatory fragmentation across flag states, and fire-risk concerns—especially for large-scale installations—remain key barriers to deep-sea commercial deployment.

How does the IMO’s GHG strategy impact the market?

The 2023 IMO Revised Strategy (net-zero “by or around 2050”) and upcoming CII/EEXI compliance are pushing shipowners toward hybridization as a near-term decarbonization lever—making batteries a strategic bridge technology.

What’s the market outlook for 2025–2030?

The global marine battery market is projected to grow at a strong CAGR, fueled by ferry electrification, port decarbonization, and hybrid retrofits—though long-term scalability will depend on advances in energy density, safety certification harmonization, and green hydrogen integration for deep-sea shipping.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com