Global Marine Engine Monitoring System Market Size Share, Growth, Trends, and Forecast Research Report - Segmentation By Type, Engine Propulsion, End-User, And By Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa), - Industry Analysis From 2026 to 2034

Global Marine Engine Monitoring System Market Report Summary

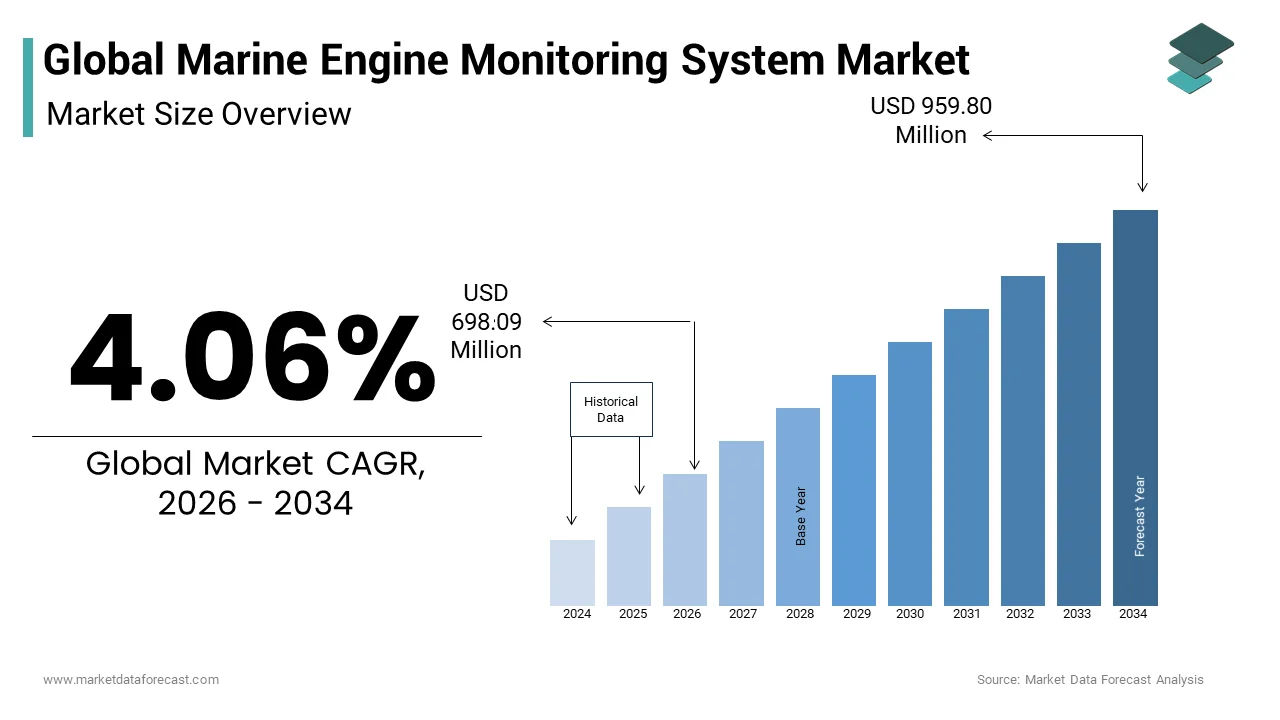

The global marine engine monitoring system market was valued at USD 670.85 million in 2025, is estimated to reach USD 698.09 million in 2026, and is projected to reach USD 959.80 million by 2034, expanding at a CAGR of 4.06% during the forecast period from 2026 to 2034. The global marine engine monitoring system market is experiencing steady growth as the maritime industry increasingly adopts intelligent monitoring technologies to improve vessel performance, operational safety, and fuel efficiency. Shipping companies are investing in advanced engine monitoring solutions to enable predictive maintenance, minimize unplanned downtime, and comply with stringent international environmental and emission regulations. The growing deployment of digital ship management systems, real-time engine diagnostics, and remote monitoring platforms is further accelerating market expansion. Rising global seaborne trade, fleet modernization initiatives, and increasing investments in smart shipping technologies are also creating significant opportunities for marine engine monitoring system providers worldwide.

Key Market Trends

- Shipping operators are increasingly adopting predictive maintenance solutions powered by real-time engine performance monitoring and advanced analytics.

- Integration of IoT, artificial intelligence, and cloud-based platforms is enabling remote vessel monitoring and more efficient fleet management.

- Stricter international maritime emission standards are encouraging shipowners to deploy advanced engine monitoring systems that optimize fuel consumption and reduce environmental impact.

- Digitalization of commercial shipping operations is accelerating demand for connected marine equipment and automated performance management solutions.

- Fleet modernization and the development of smart vessels are driving investments in integrated engine monitoring technologies across global maritime industries.

Segmental Insights

Based on type, the commercial cargo and container vessels segment accounted for a significant share of the global marine engine monitoring system market in 2025. The segment's leadership is attributed to the high operational intensity of cargo fleets, increasing demand for fuel-efficient vessel operations, and the growing need for continuous engine health monitoring to reduce maintenance costs and operational disruptions.

Based on end user, the commercial transport segment captured 44.6% of the global marine engine monitoring system market share in 2025. Commercial shipping companies continue to invest heavily in intelligent engine monitoring technologies to improve fleet reliability, maximize operational efficiency, enhance regulatory compliance, and optimize long-distance maritime transportation.

Regional Insights

Asia Pacific dominated the global marine engine monitoring system market by accounting for 40.3% of the market share in 2025. The region's leadership is supported by its large commercial shipbuilding industry, expanding maritime trade, major port infrastructure, and growing adoption of digital marine technologies across countries such as China, Japan, and South Korea. Europe secured the second-largest market share with 25.3% in 2025, driven by advanced maritime engineering capabilities, stringent environmental regulations, and continuous investments in smart shipping solutions. North America is expected to experience significant growth during the forecast period as commercial fleet operators accelerate digital transformation initiatives. Latin America is witnessing steady expansion through increasing trade activities and modernization of port infrastructure, while the Middle East and Africa are emerging as promising markets due to the presence of strategic shipping routes, expanding energy industries, and ongoing investments in maritime infrastructure.

Competitive Landscape

The global marine engine monitoring system market is characterized by strong competition among established marine technology providers, engine manufacturers, and industrial automation companies focused on delivering intelligent monitoring and predictive maintenance solutions. Leading market participants are investing in digital technologies, artificial intelligence, cloud connectivity, and advanced sensor integration to improve engine performance, operational reliability, and fuel efficiency. Strategic collaborations with shipbuilders, fleet operators, and maritime technology firms are strengthening product portfolios and expanding global market reach. Companies are also prioritizing software innovation, cybersecurity, remote diagnostics, and integrated fleet management platforms to support the maritime industry's transition toward smart shipping. As digitalization, sustainability, and regulatory compliance become increasingly important across global shipping operations, continuous technological innovation will remain the primary competitive differentiator in the marine engine monitoring system market.

Prominent players in the global marine engine monitoring system market include ABB Ltd., Cummins Inc., Caterpillar Inc., Kongsberg Maritime, Emerson Electric Co., Hyundai Heavy Industries Co., Ltd., MAN Energy Solutions SE, AST Group, CMR Group, Mitsubishi Heavy Industries Group, Noris Group, Rolls-Royce plc, and Wärtsilä Corporation.

Global Marine Engine Monitoring System Market Size

The global marine engine monitoring system market size was valued at USD 670.85 million in 2025 and is anticipated to reach USD 698.09 million in 2026 to reach USD 959.80 million by 2034, growing at a CAGR of 4.06% during the forecast period from 2026 to 2034.

Introduction to the Marine Engine Monitoring System Market

The marine engine monitoring system is advanced diagnostic and surveillance technology designed to track the performance, health, and operational parameters of propulsion systems in commercial, naval, and leisure vessels. These systems utilize a network of sensors, data acquisition units, and software algorithms to monitor metrics, such as temperature, pressure, vibration, and fuel consumption in real time. The primary objective is to enable predictive maintenance, enhance safety, and ensure regulatory compliance in an increasingly stringent environmental landscape. In Europe, the European Maritime Safety Agency emphasizes the importance of digitalization in enhancing maritime safety, noting that technical failures contribute significantly to maritime accidents. As vessels become more complex with hybrid and dual fuel engines, the integration of sophisticated monitoring solutions becomes indispensable. These systems facilitate remote diagnostics, allowing shore based teams to analyze data and provide immediate support, thereby reducing downtime and optimizing fleet management strategies in a highly competitive global logistics environment.

MARKET DRIVERS

Stringent Environmental Regulations Driving Compliance Needs

The imposition of strict environmental regulations by international and regional bodies is solely propelling the growth of the marine engine monitoring system market. Governments and regulatory agencies are enforcing tighter limits on sulfur oxide, nitrogen oxide, and carbon dioxide emissions to combat climate change and marine pollution. According to the International Maritime Organization, the implementation of the IMO 2020 sulfur cap reduced the allowable sulfur content in fuel oil from 3.5% to 0.5%, necessitating precise monitoring of fuel quality and exhaust emissions. Vessels must continuously track their emissions data to prove compliance during port state controls and avoid substantial fines or detention. The European Union’s inclusion of maritime transport in its Emissions Trading System further compels shipowners to accurately measure and report carbon footprints. Monitoring systems provide the granular data required for these reports by ensuring transparency and accountability. Additionally, the Energy Efficiency Existing Ship Index requires older vessels to improve their energy efficiency, which can only be achieved through continuous performance monitoring and optimization.

Rising Operational Costs and Need for Fuel Efficiency

The escalating cost of marine fuels and the imperative to optimize operational expenses is additionally fuelling the growth of the marine engine monitoring systems market. Fuel represents the largest single operating cost for shipping companies, often accounting for 50 to 60% of total voyage expenses. The fluctuations in bunker fuel prices can significantly impact profitability by making fuel efficiency a competitive advantage. Monitoring systems enable captains and shore-based managers to track specific fuel consumption in real time, identifying deviations from optimal performance curves. Furthermore, these systems detect early signs of engine degradation, such as injector fouling or turbocharger inefficiency by allowing for timely maintenance that restores peak performance. Preventive maintenance avoids catastrophic failures that lead to expensive off hire periods and emergency repairs.

MARKET RESTRAINTS

High Initial Installation and Integration Costs

The substantial upfront capital expenditure required for installing and integrating advanced systems, particularly for small and medium sized shipping operators is impeding the growth of the marine engine monitoring system market. Retrofitting existing vessels with modern sensor networks and data processing units involves complex engineering work, dry docking time, and specialized labor, all of which contribute to high initial costs. For operators managing older fleets with tight cash flows, this investment presents a formidable barrier to entry. Additionally, the lack of standardization among different engine manufacturers means that custom integration is often required, further driving up expenses. Small coastal traders and fishing vessels, which operate on lower margins, may find the return on investment period too long to justify the expenditure. The economic volatility in the shipping sector, characterized by fluctuating freight rates, makes capital allocation for non-revenue generating technology risky. While larger conglomerates can absorb these costs, smaller entities may delay upgrades or opt for basic manual monitoring methods.

Cybersecurity Vulnerabilities and Data Privacy Concerns

The increasing connectivity of marine engine monitoring systems introduces significant cybersecurity risks that is restricting the growth of the marine engine monitoring system market. As these systems transmit sensitive operational data via satellite or cellular networks to shore based servers, they become potential targets for cyberattacks, including ransomware, data theft, and remote hijacking. A successful breach could allow malicious actors to manipulate engine parameters by leading to mechanical failure, safety hazards, or environmental disasters. The classification society DNV warns that many legacy monitoring systems were not designed with modern cybersecurity protocols, making them vulnerable to exploitation. Shipowners face the additional burden of implementing robust firewalls, encryption, and regular security audits, which add to operational complexity and cost. Furthermore, concerns regarding data privacy and ownership arise when third party service providers manage the data infrastructure. Operators fear that proprietary performance data could be leaked to competitors or used against them in insurance claims. The lack of universal cybersecurity standards for maritime IoT devices creates uncertainty, causing some companies to hesitate in fully integrating connected monitoring solutions.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence for Predictive Maintenance

The integration of artificial intelligence and machine learning to shift from reactive to predictive maintenance models is likely to foster prominent opportunities for the expansion of the marine engine monitoring systems market. AI algorithms can analyze vast historical and real time data sets to identify subtle patterns and anomalies that precede equipment failure by enabling interventions before breakdowns occur. By accurately predicting component lifespans, operators can optimize spare parts inventory and schedule repairs during planned port calls rather than facing emergency situations at sea. This capability is particularly valuable for autonomous and semi-autonomous vessels, where remote diagnostic accuracy is critical for safe operation. The development of digital twins, virtual replicas of physical engines that allows for simulation and testing of various operating scenarios to optimize performance without risking actual hardware. As computing power increases and costs decrease, AI driven monitoring becomes accessible to a wider range of vessels. Classification societies are beginning to recognize AI based condition monitoring as a valid alternative to traditional scheduled surveys, potentially reducing inspection frequencies and costs. This technological evolution opens new revenue streams for software developers and service providers, positioning AI enhanced monitoring as a cornerstone of next generation smart shipping solutions.

Expansion into Offshore Renewable Energy Sector

The rapid growth of the offshore renewable energy sector, particularly wind farms, is also to propel the growth of the marine engine monitoring system market. Service operation vessels and crew transfer vessels used in offshore wind projects operate in harsh environments and require high reliability to minimize downtime and ensure worker safety. According to the Global Wind Energy Council, global offshore wind capacity is expected to reach 380 gigawatts by 2030, driving demand for specialized support vessels equipped with advanced monitoring technologies. These vessels often utilize hybrid or dual fuel engines to meet strict environmental standards in protected marine areas, requiring sophisticated monitoring to manage complex power trains. Monitoring systems ensure that engines operate efficiently during dynamic positioning and transit, reducing fuel consumption and emissions. Furthermore, the remote location of offshore installations makes real time remote diagnostics essential, as sending technicians for minor issues is prohibitively expensive and time consuming. Manufacturers of monitoring systems can tailor solutions to the specific needs of the offshore sector, such as corrosion resistance and enhanced vibration analysis for rough sea conditions. Partnerships with wind farm operators and vessel builders can create long term service contracts, providing stable revenue streams.

MARKET CHALLENGES

Legacy Infrastructure and Compatibility Issues

The prevalence of legacy infrastructure and older vessels to the widespread implementation of modern systems is a big barrier for the growth of the marine engine monitoring system market. A large portion of the global fleet consists of ships built decades ago, equipped with analog instruments and mechanical engines that lack the digital interfaces required for modern sensor integration. Retrofitting these older systems with digital monitoring capabilities is technically challenging and often requires extensive modification of existing wiring and control systems. The lack of standardized communication protocols among different engine manufacturers and generations of equipment complicates data aggregation and analysis. Interoperability issues mean that data from various subsystems may not seamlessly integrate into a unified monitoring platform, leading to data silos and incomplete insights. Shipowners may struggle to find compatible sensors and software that work reliably with aged infrastructure, increasing the risk of system errors and false alarms. Additionally, the physical space constraints on older vessels can make the installation of new hardware difficult. Overcoming these compatibility barriers requires significant engineering effort and custom solutions, which increases costs and deployment time.

Shortage of Skilled Personnel for Data Interpretation

The shortage of skilled personnel capable of interpreting complex data is also to limit the growth of the marine engine monitoring system market. While modern systems generate vast amounts of data, extracting actionable insights requires specialized knowledge in data analytics, marine engineering, and IT systems. The maritime industry faces a significant shortage of officers and engineers with digital literacy and data analysis skills. Traditional marine training programs have focused on mechanical and navigational competencies by leaving a gap in digital expertise. Shore based support teams also struggle to keep pace with the volume of data generated by connected fleets, leading to information overload and delayed decision making. The rapid evolution of monitoring technologies outpaces the ability of educational institutions to update curricula, resulting in a workforce that is ill prepared for digital operations. Recruiting and retaining talent with hybrid skills in engineering and data science is difficult due to competition from the tech sector. This human capital deficit limits the realization of the full potential of monitoring systems, as organizations cannot effectively leverage the data they collect.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.06% |

| Segments Covered | By Type, Engine Propulsion, End-User, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | ABB Ltd., Cummins Inc., Caterpillar Inc., Kongsberg Maritime, Emersion Electric Co., Hyundai Heavy Industries Co., Ltd., MAN Energy Solutions SE, AST Group, CMR Group, Mitsubishi Heavy Industries Group, Noris Group, Rolls-Royce plc, Wartsila Corporation. |

SEGMENTAL ANALYSIS

By Type Insights

The commercial cargo and container vessels segment held a significant share of the marine engine monitoring system market in 2025 due to their role in global trade and the high operational costs associated with their propulsion systems. According to the research, maritime transport handles over 80% of global merchandise trade by volume, with container ships representing a significant portion of this traffic. These vessels operate on tight schedules across long distances, making unplanned downtime financially devastating. Engine monitoring systems provide real time data on fuel consumption, engine load, and component health, allowing operators to optimize performance and prevent catastrophic failures. The International Maritime Organization’s stringent regulations on sulfur emissions and energy efficiency further compel container ship operators to adopt advanced monitoring technologies to ensure compliance. Additionally, the complexity of modern dual fuel engines used in these vessels requires sophisticated diagnostic tools that only advanced monitoring systems can provide by ensuring safe and efficient operations in an increasingly regulated environment.

The offshore support and specialized vessels segment is esteemed to register a fastest CAGR of 9.2% throughout the forecast period with the expansion of the offshore renewable energy sector, particularly wind farms, which require reliable service operation vessels and crew transfer boats. These vessels operate in harsh environments and often utilize hybrid or dynamic positioning systems that place unique stresses on engines, necessitating continuous monitoring to prevent failures. The remote nature of offshore installations makes predictive maintenance essential, as emergency repairs are logistically difficult and expensive. Monitoring systems enable shore-based teams to diagnose issues remotely, ensuring minimal disruption to wind farm operations. Furthermore, strict environmental regulations in protected marine areas mandate low emission operations, which hybrid propulsion systems achieve but require complex monitoring to manage effectively. The increasing adoption of autonomous features in offshore support vessels also drives demand for integrated monitoring solutions that provide real time data for remote control centers.

By End User Insights

The commercial transport segment was accounted in holding 44.6% of the marine engine monitoring system market share in 2025 with the intense competitive pressure to reduce operational costs and maintain schedule reliability. Engine monitoring systems allow these companies to track performance metrics across their entire fleet, identifying underperforming vessels and optimizing maintenance schedules to minimize off hire time. The implementation of digital twins and predictive analytics enables transport companies to anticipate mechanical issues before they cause delays, ensuring adherence to just in time delivery commitments. Regulatory compliance is another key driver, as transport companies must report emissions data to various international bodies to avoid penalties. The ability to demonstrate sustainable operations through accurate monitoring also enhances corporate reputation and meets customer demands for green logistics.

The naval and defense sector is esteemed to grow at a fastest CAGR of 8.5% during the forecast period due to increasing geopolitical tensions and modernization initiatives. The global military expenditure reached record highs in recent years, with significant portions allocated to naval modernization and technology upgrades. Modern warships rely on complex propulsion systems, including gas turbines and hybrid electric drives, which require sophisticated monitoring to ensure silent running and rapid response capabilities. Engine monitoring systems provide critical data on vibration and acoustic signatures, helping naval engineers minimize noise detection by adversaries. Additionally, the shift toward unmanned surface vessels and autonomous underwater vehicles in defense applications necessitates robust remote monitoring solutions that can operate without onboard crew intervention. Predictive maintenance is vital in military contexts to ensure mission success and reduce logistical burdens during deployments. Governments are investing heavily in cyber secure monitoring platforms to protect sensitive operational data from espionage and sabotage.

REGIONAL ANALYSIS

Asia Pacific Market Analysis

Asia Pacific was the largest contributor by capturing 40.3% of the marine engine monitoring system market share in 2025 with its status as the world’s manufacturing and shipping hub. The region’s market status is characterized by the presence of major shipbuilding nations, such as China, South Korea, and Japan, which integrate advanced monitoring systems into new vessels during construction. China’s Belt and Road Initiative has expanded maritime trade routes, increasing the demand for efficient and compliant shipping operations. South Korean shipyards are leaders in building smart ships equipped with integrated digital platforms by setting global standards for connectivity. Japan’s focus on technological innovation drives the development of AI based monitoring solutions for aging fleets. Local manufacturers are increasingly partnering with global tech firms to develop cost effective solutions tailored to regional needs.

Europe Market Analysis

Europe marine engine monitoring system market was positioned second by holding 25.3% of the share in 2025 with the stringent environmental policies and technological leadership. Europe leads in implementing digital reporting requirements and emission tracking systems, compelling shipowners to adopt advanced monitoring technologies. Norway and Germany are key countries, with Norway focusing on electric and hybrid ferry operations that require precise battery and engine monitoring. Germany’s strong engineering sector supports the development of high precision sensors and analytics software. The inclusion of shipping in the EU Emissions Trading System creates a financial imperative for accurate carbon footprint measurement, driving demand for certified monitoring solutions. European classification societies are at the forefront of defining standards for cyber security and data integrity in marine systems. The region’s emphasis on sustainability and innovation ensures that European shipowners are early adopters of next generation monitoring technologies.

North America Market Analysis

North America marine engine monitoring system market growth is likely to have a prominent opportunity in coming years with the robust domestic shipping activities, naval modernization, and strict environmental regulations. The investments in port infrastructure and short sea shipping are increasing, creating demand for efficient vessel operations. Canada’s extensive coastline and reliance on marine transport for remote communities drive demand for reliable monitoring solutions that ensure safety in harsh conditions. The adoption of liquefied natural gas fueled vessels in North America requires specialized monitoring for methane slip and engine performance, creating niche opportunities. Tech companies in Silicon Valley and other hubs are collaborating with maritime firms to develop cloud-based analytics platforms, fostering innovation. The region’s focus on supply chain resilience post pandemic has led to increased investment in digital tools for fleet management.

Latin America Market Analysis

Latin America marine engine monitoring system market growth is driven by growing trade volumes and modernization of port infrastructure. The intra-regional trade and exports to Asia are increasing, prompting shipping companies to improve operational efficiency. Brazil and Chile are leading markets, with Brazil’s offshore oil and gas sector driving demand for monitoring systems on support vessels. Chile’s copper exports require reliable shipping services, encouraging fleet operators to invest in predictive maintenance to avoid disruptions. The region faces challenges related to funding and technical expertise, but international partnerships and foreign investment are helping to bridge these gaps. Environmental regulations are gradually becoming stricter, particularly in port areas, encouraging the adoption of monitoring technologies to reduce local pollution.

Middle East and Africa Market Analysis

The Middle East and Africa marine engine monitoring system market growth is likely to driven by the strategic maritime hubs and growing energy sectors. The United Arab Emirates and Saudi Arabia are investing heavily in smart port initiatives and fleet modernization to maintain their status, as global logistics hubs. These projects, include the integration of advanced monitoring systems to enhance operational efficiency and comply with international environmental standards. In Africa, countries like South Africa and Nigeria are upgrading their naval and commercial fleets by creating opportunities for monitoring technology providers. The harsh operating conditions in the region, including high temperatures and sand, require robust and durable monitoring equipment. International shipping lines operating in the region are also driving adoption by implementing global standards for fleet management.

COMPETITIVE LANDSCAPE

The competition in the marine engine monitoring system market is characterized by intense rivalry among established industrial conglomerates and specialized technology providers. Major players compete on system accuracy reliability and the ability to integrate with diverse propulsion technologies, including dual fuel and hybrid engines. The shift toward digitalization and autonomous shipping has intensified the need for advanced data analytics and remote connectivity features creating barriers to entry for smaller firms. Price competition is moderate as value is derived from long term operational savings and regulatory compliance rather than initial hardware costs. Cyber security concerns act as a significant differentiator favoring companies with robust protection frameworks and certified protocols. Collaborations between hardware manufacturers and software developers are common to create holistic solutions that address both mechanical and digital aspects of vessel management. Customer retention relies heavily on after sales support and continuous software updates.

KEY MARKET PLAYERS

A powerful dominating market players that are in the global marine engine monitoring system market are

- ABB Ltd.

- Cummins Inc.

- Caterpillar Inc.

- Kongsberg Maritime

- Emersion Electric Co.

- Hyundai Heavy Industries Co., Ltd.

- MAN Energy Solutions SE

- AST Group

- CMR Group

- Mitsubishi Heavy Industries Group

- Noris Group

- Rolls-Royce plc

- Wartsila Corporation

Top Players In The Market

- Wartsila Corporation is a global leader in marine technologies providing advanced engine monitoring and digital solutions for the shipping industry. The company integrates its Smart Marine ecosystem with real time data analytics to optimize vessel performance and fuel efficiency. Recent actions, include expanding its predictive maintenance capabilities through artificial intelligence algorithms that detect anomalies before failures occur. Wartsila collaborates with major shipowners to implement remote diagnostic services that reduce downtime and operational costs. By focusing on lifecycle support and sustainability, the company strengthens its position as a trusted partner for decarbonization efforts. Their continuous investment in software development ensures compatibility with diverse engine types and regulatory requirements globally.

- Kongsberg Maritime specializes in high technology systems for the marine industry including comprehensive engine monitoring and control solutions. The company leverages its expertise in automation and robotics to deliver precise data acquisition and analysis tools for commercial and naval vessels. Recent initiatives involve enhancing its Kognitif digital platform to provide actionable insights for fleet operators regarding engine health and emissions. Kongsberg focuses on integrating cyber security measures into its monitoring systems to protect sensitive operational data from threats. By offering scalable solutions that adapt to various vessel sizes and complexities, the company maintains a strong competitive edge. Their commitment to innovation drives the adoption of smart shipping technologies across global markets.

- ABB Ltd is a prominent provider of electrification and automation technologies offering robust marine engine monitoring and power management systems. The company combines hardware sensors with cloud-based software to enable real time visibility into vessel operations and energy consumption. Recent actions include launching new digital services that facilitate remote assistance and predictive maintenance for complex propulsion systems. ABB partners with classification societies to ensure its monitoring solutions meet stringent international safety and environmental standards. The company emphasizes interoperability allowing seamless integration with third party equipment and existing ship infrastructure. Through strategic acquisitions and organic growth, ABB continues to expand its portfolio of smart marine solutions supporting the industry transition toward sustainable and efficient operations.

Top Strategies Used By Key Market Participants

Key players in the marine engine monitoring system market primarily focus on digital integration and artificial intelligence to enhance predictive capabilities and operational efficiency. Companies invest heavily in developing cloud based platforms that aggregate data from multiple sources for comprehensive fleet analysis. Strategic partnerships with classification societies and regulatory bodies ensure compliance with evolving environmental standards and certification requirements. Manufacturers prioritize cyber security features to protect sensitive vessel data from increasing digital threats in connected maritime environments. Product diversification includes offering modular solutions that can be retrofitted onto older vessels as well as integrated into new builds. Expansion into emerging markets through local collaborations helps firms address regional specific needs and infrastructure constraints. These strategies collectively strengthen market position by delivering reliable secure and scalable monitoring solutions that support the global maritime industry sustainability goals.

MARKET SEGMENTATION

This research report on the global marine engine monitoring system market is segmented and sub-segmented into the following categories.

By Type

- Vessel

- Container

- Passenger

- Others

By Engine Propulsion Type

- Diesel

- Gas Turbine

- Others

By End User

- Passenger Vessels

- Cruise Ships

- Tankers

- Others

By Region

- North America

- Europe

- Asia Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

Why is the global marine engine monitoring system market experiencing steady growth?

The market is expanding due to increasing maritime digitalization, rising demand for predictive maintenance, stricter emission regulations, and growing investments in fleet efficiency.

What is a marine engine monitoring system and how does it work?

A marine engine monitoring system is a digital solution that uses sensors, software, and analytics to continuously monitor engine performance, fuel consumption, temperature, pressure, and other critical operating parameters.

Which vessel segment accounts for the largest share of the global marine engine monitoring system market?

Commercial cargo and container vessels account for the largest market share due to their extensive engine monitoring requirements and large global fleet size.

How do marine engine monitoring systems improve vessel performance?

They enable real-time engine diagnostics, optimize fuel consumption, reduce maintenance costs, prevent unexpected failures, and improve operational reliability.

What factors are driving the growth of the global marine engine monitoring system market?

Growing international seaborne trade, increasing adoption of smart shipping technologies, rising demand for fuel-efficient operations, and stringent environmental regulations are driving market growth.

Which industries generate the highest demand for marine engine monitoring systems?

Commercial shipping, offshore oil and gas, naval defense, cruise operators, fishing fleets, ferry services, and marine logistics companies are the primary end users.

What technologies are shaping the future of the global marine engine monitoring system market?

Artificial intelligence, IoT-enabled sensors, cloud-based fleet management, digital twins, predictive analytics, remote diagnostics, and edge computing are driving innovation.

How is predictive maintenance transforming the marine engine monitoring system market?

Predictive maintenance helps identify engine issues before failures occur, reducing downtime, extending engine life, lowering maintenance costs, and improving fleet availability.

What challenges could affect the growth of the global marine engine monitoring system market?

High implementation costs, cybersecurity risks, integration with legacy vessels, data management complexities, and skilled workforce shortages could affect market growth.

Which regions are expected to lead the global marine engine monitoring system market?

Europe leads the market due to advanced maritime technologies and strict environmental standards, while Asia Pacific is witnessing rapid growth through shipbuilding expansion and increasing commercial shipping activities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com