Global Material Testing Market Size, Share, Trends & Growth Forecast Report – Segmented By Type (Universal Testing Machines, Servo-hydraulic Testing Machines, Hardness Test Equipment and Others), End-Use Industry, Material, Region, and Industry Analysis (2026 to 2034)

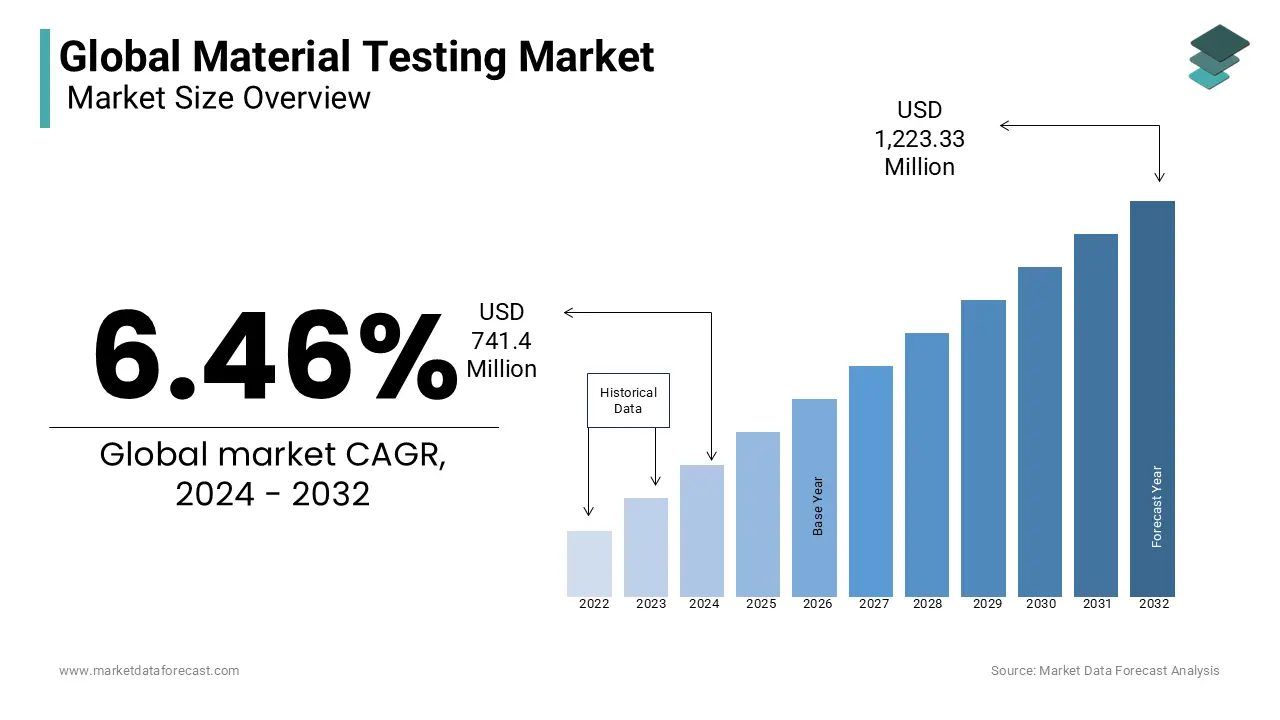

Market Size, 2025

$789.2 MnMarket Estimate, 2026

$840.2 MnMarket Forecast, 2034

$1386.4 MnCAGR, 2026–2034

6.46%Global Material Testing Market Size

The global material testing market size was valued at USD 789.28 million in 2025 and is expected to reach USD 1,386.47 million by 2034, growing from USD 840.27 million in 2026. The market is growing at a CAGR of 6.46%.

Material Testing refers to the methodologies and technologies employed to evaluate the physical, mechanical, and chemical properties of materials used across industrial, engineering, and scientific applications. This domain includes tensile, compression, impact, hardness, fatigue, and non-destructive testing techniques, essential for ensuring structural integrity, safety compliance, and performance optimization in sectors such as aerospace, automotive, construction, and energy. As materials grow increasingly complex—ranging from advanced composites to high-performance alloys—the necessity for precise, repeatable, and standardized testing has intensified. Regulatory frameworks such as ISO 17025 and ASTM standards mandate rigorous material validation, reinforcing the role of testing in quality assurance. The expansion of smart manufacturing ecosystems in industrialized nations has further embedded material testing into product lifecycle management, transforming it from a compliance function into a strategic engineering tool.

MARKET DRIVERS

Expansion of Aerospace and Defense Manufacturing Requiring High-Integrity Material Validation

The aerospace and defense sector’s relentless pursuit of lightweight, high-strength materials has significantly amplified demand for advanced material testing protocols. As modern aircraft increasingly incorporate composite materials—constituting up to 50% of the structural mass in next-generation models such as the Boeing 787 and Airbus A350—the need for rigorous certification testing has become paramount. Also, every composite component used in commercial aircraft must undergo fatigue and environmental testing before certification. Hence, the cascading demand for material qualification testing is set to escalate, reinforcing the indispensability of sophisticated testing systems in ensuring flight safety and regulatory compliance.

Stringent Regulatory Mandates in the Automotive Industry for Crashworthiness and Emission Compliance

Automotive manufacturers are under increasing pressure to meet global safety and emissions regulations, driving the need for precise material characterization and durability testing. For instance, Advanced High-Strength Steels (AHSS) such as Ultra-High-Strength Steels (UHSS, ≥ 980 MPa) are commonly used in vehicle frames for crashworthiness. ASTM E8 is the standard for tensile testing. These regulatory frameworks transform material testing from a developmental step into a compliance-critical function, directly influencing market expansion.

MARKET RESTRAINTS

Shortage of Skilled Personnel in Advanced Testing Methodologies

The global deficit of qualified technicians and engineers proficient in advanced testing techniques is a critical impediment to the scalability of the material testing market. As testing technologies evolve toward digitalization, automation, and AI-driven analytics, the demand for personnel skilled in areas such as scanning electron microscopy, acoustic emission testing, and finite element analysis has surged. However, the American Society for Nondestructive Testing reports that over 30% of NDT technician positions in the United States remain unfilled due to a lack of certified professionals. The complexity of ISO 9712 certification, which requires a minimum of 400–1,200 hours of training depending on the method and level, exacerbates the talent gap. This shortage delays project timelines, increases operational costs, and compromises testing accuracy, particularly in emerging economies where industrial expansion outpaces workforce development. Without strategic investment in technical education and certification programs, the scarcity of skilled labor will continue to constrain the effective deployment of advanced material testing systems.

High Capital and Operational Costs of Precision Testing Equipment

The deployment of state-of-the-art material testing systems involves substantial financial investment, limiting accessibility for small and medium-sized enterprises (SMEs) and research institutions in developing regions. According to the U.S. Bureau of Economic Analysis, capital expenditures for industrial testing equipment was around $1.9 trillion in 2022, reflecting the significant outlay required for modernization. Maintenance and calibration costs further burden operations. In addition, compliance with ISO 17025 accreditation requires continuous investment in quality management systems, personnel training, and equipment traceability, adding operational overhead. In Southeast Asia, where SMEs constitute over 97% of manufacturing firms as per the ASEAN Secretariat, the cost barrier restricts in-house testing capabilities, forcing reliance on third-party laboratories and increasing lead times. Even in developed economies, budget constraints in public infrastructure projects limit investment in advanced testing. These economic constraints hinder the widespread adoption of cutting-edge testing technologies, slowing innovation and quality assurance across critical sectors.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Machine Learning in Predictive Material Behavior Modeling

The convergence of artificial intelligence (AI) with material testing presents a transformative opportunity to enhance predictive accuracy and reduce physical testing cycles. Machine learning algorithms are increasingly employed to analyze vast datasets from historical material performance, enabling the simulation of failure modes and lifespan predictions under variable stress conditions. Companies like Siemens and GE Additive utilize AI-powered digital twins to simulate thermal and mechanical stress on 3D-printed metal components, slashing validation time. The U.S. Department of Energy’s Materials Genome Initiative has accelerated this trend by funding several projects aimed at developing computational models that predict material properties before synthesis, effectively compressing R&D timelines. Furthermore, the integration of AI in non-destructive testing has enabled real-time defect recognition. Hence, the synergy between intelligent algorithms and material testing is poised to redefine quality assurance paradigms, enabling faster innovation cycles and reduced resource consumption in product development.

Rising Demand for Sustainable and Recycled Materials Requiring Rigorous Qualification Testing

The global shift toward circular economy principles has catalyzed the use of recycled and bio-based materials, necessitating robust testing frameworks to ensure performance parity with virgin materials. Also, the automotive industry is adopting recycled aluminum, which must undergo tensile and corrosion testing to verify structural integrity. In packaging, bio-based polymers such as polylactic acid (PLA) are subject to ASTM D6400 biodegradability and mechanical strength testing before commercial use. Thus, the need to qualify secondary materials is driving investment in testing infrastructure. This transition positions material testing as a critical enabler of sustainability, opening new revenue streams for testing service providers and equipment manufacturers alike.

MARKET CHALLENGES

Inconsistencies in Global Testing Standards and Certification Protocols

A persistent challenge in the material testing market is the lack of harmonization across international testing standards, leading to compliance complexities and market access barriers. While organizations such as ASTM International and ISO develop widely adopted protocols, regional deviations persist; for example, China’s GB standards for steel tensile testing differ in specimen dimensions and strain rate from ASTM E8, requiring dual testing for export-oriented manufacturers. The CE marking in the EU requires products to meet essential requirements, often aligned with EN standards. In the U.S., the Federal Railroad Administration oversees railcar safety, and AAR M-101 is a standard for railcar materials. In emerging markets, the absence of standardized accreditation bodies exacerbates the issue. These discrepancies not only inflate compliance expenditures but also erode confidence in cross-border material certification, hindering global supply chain integration and technological interoperability.

Rapid Technological Obsolescence Due to Accelerated Innovation Cycles

The material testing sector faces mounting pressure from the accelerating pace of materials science innovation, rendering existing testing infrastructure obsolete before full return on investment is achieved. The emergence of metamaterials, self-healing polymers, and multi-functional composites demands testing systems capable of evaluating non-traditional properties such as shape-memory response or electrical conductivity under mechanical load. Equipment manufacturers like Instron and ZwickRoell face shrinking product lifespans. Furthermore, the integration of Industry 4.0 technologies such as IoT-enabled sensors and cloud-based data analytics requires continuous hardware and software upgrades, increasing total cost of ownership. In academic and government research facilities, budget cycles often lag behind technological change, resulting in capability gaps. This dynamic creates a perpetual upgrade burden, challenging the economic sustainability of testing operations and threatening the reliability of long-term material performance data.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.46% |

| Segments Covered | By Type, End-use, Material, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, Asia-Pacific, Latin America, Middle East & Africa |

| Market Leaders Profiled | Instron (US), Zwick Roell (Germany), MTS Systems (US), Shimadzu (Japan), Tinius Olsen (US), Ametek (US), Aimil Ltd., Humboldt Mfg. Co., CMT Equipment, Qualitest International Inc., Canopus Instruments, ELE International Controls S.p.A. and OLSON INSTRUMENTS INC. |

SEGMENTAL ANALYSIS

By Type Insights

The Universal Testing Machines (UTMs) segment dominated the global material testing market by accounting for a 34.2% of total revenue in 2025. These systems, capable of conducting tensile, compression, and flexural tests on a wide range of materials, serve as the foundational equipment in quality control laboratories across industries. The dominance of UTMs is primarily driven by their versatility and standardization in compliance testing. Nearly all international mechanical testing protocols, including ASTM E8, ISO 6892-1, and EN 10002, are designed around UTM-based methodologies, making them indispensable in regulated sectors. Furthermore, the widespread adoption of high-strength steels and advanced alloys in automotive and aerospace manufacturing has amplified demand for precision tensile testing. In addition, the integration of digital load cells and servo-controlled crossheads has enhanced accuracy. This combination of regulatory entrenchment, cross-industry applicability, and technological refinement ensures UTMs remain the cornerstone of material testing infrastructure.

The servo-hydraulic testing machines segment is projected to register the highest CAGR of 8.7% between 2026 and 2034. This accelerated growth is fueled by their unmatched capability in simulating real-world dynamic and fatigue conditions, particularly in high-performance engineering applications. One key driver is their critical role in aerospace and defense testing, where components must endure extreme cyclic loading. A further pivotal factor is their integration into seismic simulation for civil infrastructure. Additionally, the rise of electric vehicles has intensified demand for battery pack durability testing under vibration and impact conditions, with Tesla and BYD employing multi-axis servo-hydraulic shakers to simulate road profiles. These high-fidelity simulation requirements position servo-hydraulic machines as essential tools in next-generation product validation.

By End-Use Insights

The construction segment commanded the material testing market by capturing a 34.5% of global demand in 2025. This preeminence is due to the sector’s reliance on continuous quality assurance for structural materials such as concrete, steel, and masonry. With urbanization accelerating worldwide, the volume of construction activity necessitates rigorous on-site and laboratory testing to ensure compliance with safety codes. Additionally, the increasing use of high-performance concrete (HPC) with compressive strengths exceeding 100 MPa demands advanced testing protocols to verify durability under chloride exposure and freeze-thaw cycles. Moreover, post-disaster infrastructure assessments, such as those following the 2023 Turkey-Syria earthquakes, have intensified scrutiny on material integrity, prompting governments to enforce stricter testing regimes. These systemic requirements embed material testing into the core of construction workflows, solidifying its position as the market’s largest end-use segment.

The educational institutions segment is emerging as the fastest-growing end-use in the material testing market and is projected to expand at a CAGR of 9.3% from 2026 to 2034. This surge is driven by the integration of hands-on material science curricula in engineering programs worldwide. Universities and technical colleges are increasingly investing in testing equipment to provide students with experiential learning in mechanical behavior, failure analysis, and standards compliance. A further contributing factor is government funding for research infrastructure. Institutions such as the Technical University of Munich and Nanyang Technological University have established dedicated material characterization centers equipped with universal testers and hardness analyzers. This institutional push to align academic training with industrial standards is transforming educational facilities into significant demand centers for testing systems, fueling sustained market expansion.

By Material Insights

The metals segment led the material testing market by holding a 42.5% share in 2025. This dominance is rooted in the extensive use of metallic materials across critical industries such as aerospace, energy, and heavy manufacturing, where mechanical integrity is non-negotiable. The aerospace sector alone consumes a significant metric tons of titanium and nickel-based superalloys annually, each requiring exhaustive testing for tensile strength, creep resistance, and fatigue life. In the oil and gas industry, pipelines transporting high-pressure fluids must comply with API 5L standards, which mandate full-scale burst and tensile testing for every batch of line pipe. Additionally, the construction of nuclear reactors relies on stainless steel and zirconium alloys subjected to irradiation-assisted stress corrosion cracking tests. The rise of additive manufacturing in metal components has further intensified testing demands. Thus, the sheer volume of metallic material in circulation ensures that metal testing remains the most substantial segment in the market.

The composites segment is anticipated to grow at a CAGR of 10.2% during the forecast period. This rapid expansion is propelled by the increasing adoption of fiber-reinforced polymers in lightweight, high-performance applications. In the aerospace industry, composites are notably used in the structural weight in next-generation aircraft such as the Boeing 787 Dreamliner, necessitating specialized testing for interlaminar shear strength, delamination resistance, and moisture absorption. Each blade must be tested for torsional stiffness and fatigue resistance under simulated wind loads exceeding 50 years of operational stress. Additionally, the automotive industry is integrating carbon fiber composites into electric vehicle chassis to reduce weight and extend battery range. These rigorous validation requirements are driving investment in specialized testing equipment, positioning composites as the most dynamic segment in the material testing landscape.

REGIONAL ANALYSIS

North America Material Testing Market Analysis

North America held a 26.3% share of the global material testing market and is positioned as a leader in technological innovation and regulatory enforcement. The region’s dominance is anchored in its advanced manufacturing base and stringent quality standards across aerospace, defense, and medical device industries. The United States, in particular, operates under a robust framework of material certification mandates enforced by agencies such as the FAA, FDA, and OSHA. The presence of leading testing equipment manufacturers such as Instron and MTS Systems further strengthens the ecosystem. Canada complements this landscape with its focus on infrastructure resilience. Hence, North America remains a hub of high-precision testing and methodological leadership.

Europe Material Testing Market Analysis

Europe commands a significant share of the global material testing market and is distinguished by its harmonized regulatory environment and leadership in sustainable material qualification. The European Union’s CE marking framework requires that all construction, automotive, and machinery products undergo material testing in accordance with EN standards, creating a unified compliance landscape across 27 member states. Germany, as the industrial core, operates a large number of accredited testing laboratories, the highest in Europe. The country’s automotive sector, led by Volkswagen and BMW, conducts substantial material tests annually for crashworthiness and emissions compliance. Additionally, the EU’s Green Deal has spurred demand for testing recycled materials. France and Italy are investing in digital testing platforms. This blend of regulatory rigor, industrial density, and sustainability focus solidifies Europe’s position as a testing innovation leader.

Asia Pacific Material Testing Market Analysis

The Asia Pacific is another key player in the market which is propelled by rapid industrialization and massive infrastructure development, as stated by the Asian Development Bank. China alone contributes a significant share of global construction output. The country’s Belt and Road Initiative has spurred the construction of railways and highways in partner nations, all subject to Chinese material standards. Japan maintains a high-precision testing culture, particularly in automotive and electronics. South Korea’s focus on semiconductor manufacturing has increased demand for ceramic and wafer material testing. With ASEAN nations investing heavily in smart cities and renewable energy, the region’s material testing demand is poised for sustained expansion.

Latin America Material Testing Market Analysis

Latin America holds a notable share of the global material testing market, with growth increasingly driven by public infrastructure projects and regulatory modernization. Brazil leads the region. Mexico hosts numerous automotive assembly plants, particularly in states like Guanajuato, Coahuila, and Puebla. Quality control is crucial in the automotive industry, and many Mexican auto parts undergo tensile and hardness testing before export. Chile's mining industry, particularly copper mining, involves extensive use of machinery exposed to harsh conditions. Despite challenges in standardization, countries like Colombia and Peru are establishing national accreditation bodies, signaling a shift toward formalized testing ecosystems. Hence, Latin America is evolving into a significant testing market.

Middle East and Africa Material Testing Market Analysis

The Middle East and Africa collectively hold a small share of the global material testing market, with growth concentrated in large-scale construction and hydrocarbon industries, as reported by the African Development Bank. In Saudi Arabia, a significant share of construction materials in Vision 2030 projects undergo third-party testing for durability in extreme climates. In the UAE, the Dubai Municipality emphasizes that high-rise buildings use concrete tested for chloride resistance and thermal expansion. The oil and gas sector remains a critical driver. In Africa, South Africa operates the continent’s most advanced testing infrastructure. With increasing investment in power plants and transportation networks, the region is gradually building a structured material testing ecosystem.

COMPETITIVE LANDSCAPE

The competition in the material testing market is characterized by technological differentiation, regional service expansion, and strategic innovation rather than price dominance. Leading firms distinguish themselves through advanced instrumentation, software integration, and compliance with international standards. The market features a mix of established global players and niche regional providers, creating a tiered competitive landscape. Companies invest heavily in R&D to introduce high-precision, automated, and digitally connected testing systems that cater to aerospace, automotive, and construction sectors. Differentiation is evident in the development of AI-powered analytics, real-time monitoring, and predictive maintenance capabilities. Geographic expansion, particularly in Asia Pacific, is a key battleground, with players establishing local service hubs and training centers. Strategic collaborations with regulatory bodies and research institutions enhance credibility and market access. The rise of smart manufacturing and sustainable materials has intensified demand for adaptable testing platforms, pushing competitors to innovate rapidly. While a few global leaders dominate in technology and reach, regional players are gaining ground by offering cost-effective, localized solutions. This dynamic fosters continuous innovation, ensuring the market remains highly competitive and responsive to evolving industrial and regulatory demands.

KEY MARKET PLAYERS

Instron (US), Zwick Roell (Germany), MTS Systems (US), Shimadzu (Japan), Tinius Olsen (US), Ametek (US), Aimil Ltd., Humboldt Mfg. Co., CMT Equipment, Qualitest International Inc., Canopus Instruments, ELE International Controls S.p.A. and Olson Instruments Inc. are the key players in the material testing market.

TOP PLAYERS IN THE MARKET

- Instron has long been a cornerstone in material testing, renowned for its precision universal testing machines and advanced software integration. In the Asia Pacific region, the company has deepened its footprint through localized support centers in China, India, and Japan, enabling rapid service deployment and technical training. In 2023, Instron launched its Bluehill Universal software with expanded compliance features for ISO and ASTM standards, tailored to meet regulatory demands in automotive and aerospace sectors across South Korea and Thailand. The company also collaborated with the Indian Institute of Technology Madras to establish a joint testing laboratory focused on advanced materials for electric vehicles. By integrating IoT-enabled data acquisition systems into its latest electromechanical testers, Instron has enhanced real-time monitoring capabilities, catering to smart manufacturing trends. Its participation in industry expos such as Chinaplas and India Metallurgy has further solidified brand visibility. With dedicated R&D units in Yokohama and Shanghai, Instron continues to refine testing solutions that align with regional industrial growth, particularly in infrastructure and renewable energy applications.

- ZwickRoell has established a formidable presence in the Asia Pacific material testing landscape through its high-precision testing systems and strong emphasis on automation and digitalization. The company has strategically expanded its service network across major industrial hubs, including Singapore, Melbourne, and Pune, ensuring prompt calibration and maintenance support. In 2022, ZwickRoell introduced its roboTest series in Japan and Germany, later deploying it across automotive OEMs in Vietnam and Indonesia for robotic tensile testing, significantly improving throughput and repeatability. The company also partnered with the National Metrology Centre of Singapore to validate test data traceability for aerospace clients. In 2023, ZwickRoell launched a cloud-based data management platform, allowing manufacturers in India and Australia to centralize test results across multiple facilities. Its investment in local training academies has enhanced workforce competency in hardness and fatigue testing. By aligning its product roadmap with Industry 4.0 requirements—such as integrating AI-driven failure prediction in test software—ZwickRoell has positioned itself as a forward-thinking innovator. Its focus on sustainable testing, including energy-efficient servo motors and recyclable test fixtures, resonates with ESG-conscious enterprises in the region.

- MTS Systems Corporation is a leader in high-performance testing solutions, particularly in dynamic and fatigue testing for aerospace, automotive, and civil engineering applications. In the Asia Pacific market, MTS has strengthened its influence through strategic collaborations with national research institutions and industrial conglomerates. In 2023, the company inaugurated a new application support center in Shanghai, dedicated to serving wind energy and rail transportation clients requiring multi-axis servo-hydraulic testing. MTS also deployed its FlexTest controllers across battery testing labs in South Korea, supporting EV manufacturers in validating structural integrity under thermal and mechanical stress. The company’s partnership with the Japan Railway Technical Research Institute enabled the development of customized rail component durability tests. In India, MTS worked with Tata Motors to implement real-time load simulation systems for chassis validation. By incorporating digital twin technology into its testing platforms, MTS has enabled predictive maintenance and virtual prototyping for clients in Australia and Malaysia. Its recent integration with Ametek’s global service infrastructure has enhanced spare parts availability and remote diagnostics, improving uptime for critical testing operations across the region.

TOP STRATEGIES USED BY THE KEY MARKET PLAYERS

Key players in the material testing market are deploying strategic initiatives to consolidate their global and regional influence. Major strategies include product innovation, geographic expansion, strategic partnerships, digital integration, and acquisitions. Companies are intensifying R&D efforts to develop smart testing systems embedded with IoT, AI, and cloud analytics to meet Industry 4.0 demands. Expanding service networks in emerging economies, particularly across Asia Pacific, enables faster deployment and technical support. Collaborations with academic and research institutions enhance credibility and foster next-generation testing methodologies. Integration of digital platforms allows centralized data management, improving compliance and traceability. Some firms are also focusing on sustainability by designing energy-efficient machines and recyclable components. These strategies collectively strengthen competitive positioning, improve customer retention, and enable adaptation to evolving regulatory and industrial requirements across critical sectors.

RECENT HAPPENINGS IN THE MARKET

- In March 2022, ZwickRoell launched its fully automated roboTest F series in Japan, integrating robotic specimen handling with high-load universal testing machines to enhance efficiency in automotive production lines, significantly reducing cycle times and improving data consistency across high-volume testing environments.

- In August 2022, Instron opened a new technical competence center in Pune, India, offering localized training, calibration, and application support for manufacturers in aerospace, automotive, and construction, strengthening its service delivery and customer engagement across South Asia.

- In January 2023, MTS Systems Corporation partnered with the Japan Railway Technical Research Institute to develop customized durability testing protocols for high-speed rail components, enabling advanced fatigue and vibration simulations that meet stringent Shinkansen safety standards.

- In May 2023, Instron introduced Bluehill Universal 5.0 software with expanded multilingual support and enhanced compliance modules for ISO 7500-1 and ASTM E4, specifically tailored for regulatory requirements in China, South Korea, and Southeast Asia, improving test traceability and audit readiness.

- In November 2023, ZwickRoell collaborated with the National Metrology Centre of Singapore to validate data traceability and measurement accuracy for aerospace testing systems, reinforcing confidence in certification processes and supporting regional manufacturers in meeting FAA and EASA compliance standards.

MARKET SEGMENTATION

This research report on the global material testing market has been segmented and sub-segmented based on type, end-use, material, and region.

By Type

- Hardness Test Equipment

- Universal Testing Machines

- Servo hydraulic Testing Machines

By End-use

- Construction

- Automotive

- Educational Institutions

By Material

- Metal

- Plastics

- Rubber

- Elastomer

- Ceramics and Composites

By Region

- North America

- The United States

- Canada

- Rest of North America

- Europe

- The United Kingdom

- Spain

- Germany

- Italy

- France

- Rest of Europe

- The Asia Pacific

- India

- Japan

- China

- Australia

- Singapore

- Malaysia

- South Korea

- New Zealand

- Southeast Asia

- Latin America

- Brazil

- Argentina

- Mexico

- Rest of LATAM

- The Middle East and Africa

- Saudi Arabia

- UAE

- Lebanon

- Jordan

- Cyprus

Frequently Asked Questions

1. What is the projected size of the global material testing market by 2034?

The global material testing market is expected to reach USD 1,386.47 million by 2034.

2. What trends are currently shaping the global material testing market?

Key trends include increased adoption of automated testing systems, non-destructive testing methods, and digital data integration.

3. What factors are driving growth in the global material testing market?

Growth is driven by rising demand for quality assurance, stricter regulatory standards, and expanding manufacturing sectors.

4. How is the construction industry influencing the global material testing market?

The need for reliable and durable building materials is boosting demand for testing services in infrastructure projects.

5. How does innovation impact the global material testing market?

Advancements in testing equipment, such as AI-powered analysis and robotic testing systems, are enhancing accuracy and efficiency.

6. What challenges are faced by the global material testing market?

Challenges include high equipment costs, skilled labor shortages, and complexity in testing composite or advanced materials.

7. How are end-use industries affecting the global material testing market?

Aerospace, automotive, and medical device industries are significantly increasing demand for precise and standards-compliant testing.

8. How is the global shift toward sustainability affecting the material testing market?

Sustainable material development requires rigorous testing, driving growth in eco-friendly and recyclable material evaluations.

9. Which regions are leading the global material testing market growth?

Asia-Pacific leads due to rapid industrialization, while North America and Europe remain strong in innovation and compliance testing.

10. What is the competitive outlook for the global material testing market?

The market is competitive, with key players investing in R&D, equipment upgrades, and global service expansion.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com