Middle East and Africa Industrial Lubricants Market Size, Share, Trends & Growth Forecast Report Segmented By Base Oil (Mineral Oil, Synthetic Oil, Bio-Oil), Product, End-User, And Country (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan and Rest of MEA), Industry Analysis from 2026 to 2034

Market Size, 2025

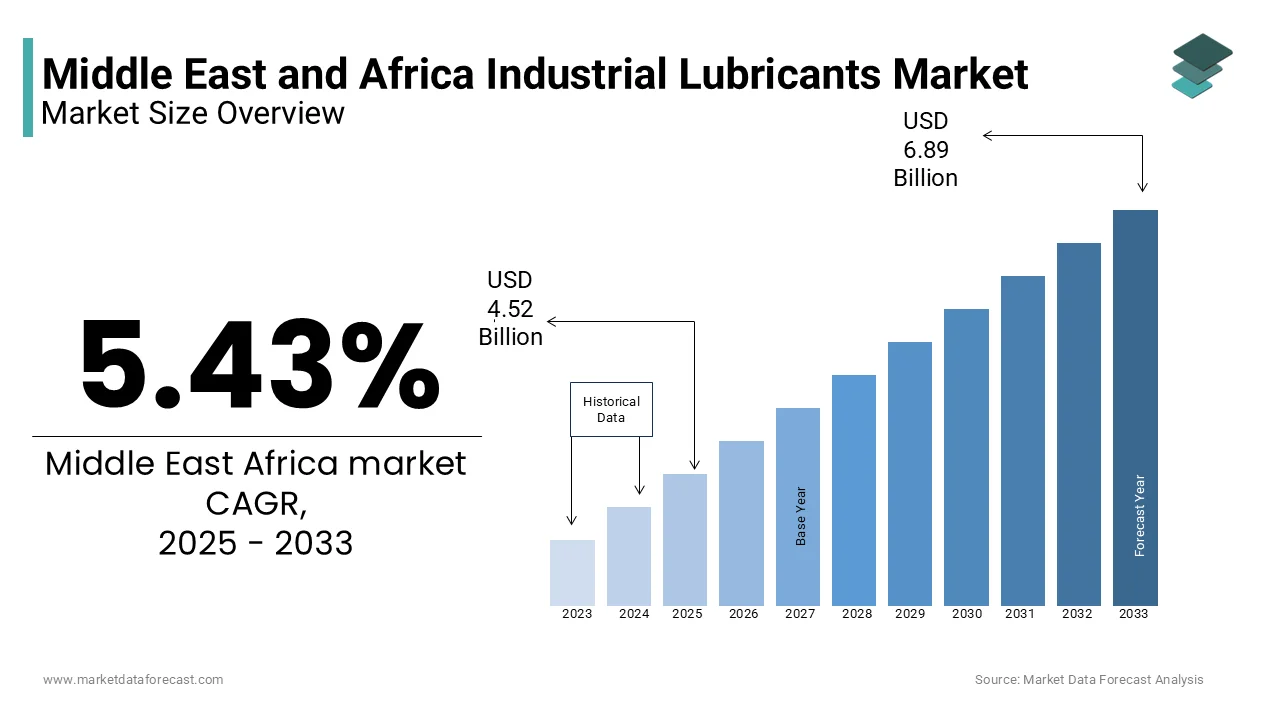

$4.52 BnMarket Estimate, 2026

$4.77 BnMarket Forecast, 2034

$7.28 BnCAGR, 2026–2034

5.43%Executive Summary: Middle East and Africa Industrial Lubricants Market

- Market Scope: Comprehensive Middle East and Africa industrial lubricants market analysis covering base oils, product segments, end-user industries, regional leadership frameworks, key market players, and emerging synthetic and bio-based lubricant trends.

- Market Valuation: Valued at USD 4.52 billion (2025), estimated at USD 4.77 billion (2026), and projected to reach USD 7.28 billion by 2034, registering a robust CAGR of 5.43% (2026–2034).

- Primary Growth Drivers: Rapid industrialization, expansive infrastructure development (such as Saudi Arabia’s Vision 2030), rising mining activities in Sub-Saharan Africa, reliance of manufacturing and energy sectors on high-performance machinery efficiency, and adoption of bio-based lubricants meeting environmental regulations.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Base Oil & Product | Mineral oil segment (dominated due to cost-effectiveness); Hydraulic fluids (held largest share in product category) | Synthetic oil segment (fastest CAGR via extreme operating demand); Turbine oils (fastest product growth) |

| By End-User | Power generation segment (led the market in 2025) | Construction segment (anticipated fastest expansion fueled by GCC and African infrastructure commitments) |

| By Region / Country | Saudi Arabia (held dominant 37.21% market share in 2025 as manufacturing/petrochemical hub) | Sub-Saharan African mining corridors and expanding industrial zones across the MEA region |

Major Market Players & Market Structure

Market Structure: Highly competitive regional and multinational industrial lubricants landscape featuring major energy and chemical enterprises competing on technical service center expansions, synthetic base oil investments, and biodegradable lubricant portfolios.

Key Companies: ExxonMobil Corporation, Royal Dutch Shell plc, BP plc, Chevron Corporation, TotalEnergies SE, LUKOIL Oil Company, PETRONAS Lubricants International, FUCHS Petrolub SE, Idemitsu Kosan Co., Ltd., Sinopec Limited, ENOC Group, Gulf Oil Middle East Ltd., Qalaa Holdings (ASCOM), ORYX Energies, Addinol Lube Oil GmbH, Oman Oil Marketing Company, ENGIE Africa, Oryx Oil Company Limited, and Master Lubricants Company (MLC).

Middle East and Africa Industrial Lubricants Market Size

The Middle East and Africa Industrial Lubricants market was valued at USD 4.52 billion in 2025 and is anticipated to reach USD 7.28 billion by 2034 from USD 4.77 billion in 2026, with a CAGR of 5.43% during the forecast period.

The region's industrial landscape is undergoing substantial transformation, with the African continent experiencing annual urbanization rates of 4.4% according to data published by the United Nations Department of Economic and Social Affairs, creating sustained demand for machinery and associated lubrication solutions. Population dynamics further reinforce this trajectory, as approximately 60% of Africa's population is under the age of 25 according to the United Nations, establishing a long-term workforce and consumption base that supports industrial expansion. In the Middle East, national development frameworks such as Saudi Arabia's Vision 2030 have mobilized significant capital commitments, directly stimulating equipment deployment and lubricant consumption across construction, petrochemical, and manufacturing sectors. Energy transition initiatives also shape market parameters, with the International Energy Agency indicating that oil and gas operations contribute approximately 5.1 gigatonnes of carbon dioxide equivalent annually, prompting industries to adopt high-performance lubricants that enhance energy efficiency and reduce emissions. These macroeconomic and demographic fundamentals establish a robust foundation for industrial lubricant demand beyond conventional market valuation metrics.

MARKET DRIVERS

Expanding Manufacturing and Infrastructure Development Across Gulf Cooperation Council Nations

Industrial lubricant consumption in the Middle East receives substantial impetus from accelerated manufacturing sector growth and large-scale infrastructure deployment, which is a key factor propelling the growth of the Middle East and African industrial lubricants market. Saudi Arabia Vision 2030 has catalyzed extensive infrastructure projects spanning transportation networks, industrial cities, and energy facilities, each requiring extensive machinery lubrication for construction equipment, processing units, and maintenance operations. The United Arab Emirates demonstrates parallel momentum, with the industrial sector contribution to gross domestic product reaching approximately 11% according to the United Arab Emirates Ministry of Industry and Advanced Technology, reflecting deliberate economic diversification away from hydrocarbon dependence. Qatar's industrial production index has expanded steadily, signaling robust activity in manufacturing, petrochemicals, and utilities that directly correlates with industrial lubricant demand. Manufacturing facilities require continuous lubrication for hydraulic systems, gearboxes, compressors, and turbine assemblies, with each operational hour consuming specialized formulations to prevent wear and maintain efficiency. Infrastructure projects similarly depend on heavy machinery lubricated with high-performance industrial oils to ensure reliability under extreme temperatures and load conditions prevalent across the region. This sustained capital expenditure cycle creates predictable, long-term demand for industrial lubricants that extends beyond cyclical commodity fluctuations, establishing manufacturing and infrastructure expansion as a foundational growth driver for the regional market.

Rising Mining and Energy Sector Activities Across Sub-Saharan Africa

Mining operations and energy extraction activities are further boosting the regional market expansion, particularly in resource-rich nations such as South Africa, Nigeria, and the Democratic Republic of Congo. The continent's mining sector consumes specialized lubricants for drilling equipment, haul trucks, crushers, and processing machinery that operate under extreme abrasion, dust, and temperature conditions. South Africa alone generated significant mining lubricants revenue during 2021, with projections indicating expansion through 2030. Energy sector activities further amplify demand, as oil and gas operations across Nigeria, Angola, and Mozambique require high-performance lubricants for drilling rigs, refinery compressors, and pipeline pumping stations that function continuously under high-pressure environments. Africa consumed a substantial volume of finished lubricants, with industrial applications accounting for a significant portion, driven by mining and energy infrastructure. Power generation represents the fastest-growing end-user segment, as nations expand electricity access through thermal, hydroelectric, and renewable facilities that all depend on turbine oils, transformer fluids, and hydraulic lubricants for reliable operation. The African Continental Free Trade Area, effective since 2021, is projected to increase real incomes by 7% or approximately $450 billion by 2035, according to the World Bank, stimulating industrial activity and associated lubricant demand across member states. These interconnected factors establish mining and energy sector expansion as a persistent, high-value driver for industrial lubricant consumption throughout the African continent.

MARKET RESTRAINTS

Volatility in Crude Oil and Base Stock Pricing Affects Production Economics

Fluctuating crude oil prices create significant uncertainty for industrial lubricant manufacturers across the Middle East and Africa, which directly impacts base stock costs that constitute 70% to 90% of finished lubricant production expenses. Base oil prices remain tightly correlated with crude benchmarks, and regional producers face exposure to global supply disruptions, geopolitical tensions, and OPEC production decisions that can trigger double-digit percentage price swings within single quarters. This volatility complicates long-term pricing strategies for lubricant formulators, who must balance input cost uncertainty against competitive market pressures and customer contract commitments. In Africa, where foreign exchange constraints frequently accompany commodity price instability, import-dependent lubricant blenders encounter compounded challenges as currency depreciation amplifies raw material cost increases. Manufacturers operating in Egypt, Nigeria, or Kenya must navigate complex import licensing, customs delays, and payment verification processes that extend lead times and increase working capital requirements during periods of price turbulence. Additionally, base stock quality variations from different regional refineries can affect finished product performance consistency, requiring additional quality control investments that further pressure margins. A single litre of lubricant can generate over 3.5 kilograms of carbon dioxide equivalent during production, meaning that cost-driven formulation compromises may also conflict with emerging environmental compliance requirements. These interconnected economic and operational constraints limit pricing flexibility and investment capacity for regional lubricant producers, restraining market expansion despite underlying demand growth.

Stringent Environmental Regulations and Compliance Complexity Across Diverse Jurisdictions

Industrial lubricant manufacturers operating across the Middle East and Africa face increasingly complex regulatory environments that impose significant compliance burdens and operational constraints. Environmental standards governing lubricant composition, biodegradability requirements, and end-of-life disposal protocols vary substantially between national jurisdictions, creating fragmentation that complicates regional product standardization. The United Arab Emirates Net Zero by 2050 strategic initiative and Saudi Arabia Circular Carbon Economy framework establish ambitious emissions reduction targets that influence lubricant formulation requirements, pushing manufacturers toward lower carbon footprint products that may carry higher production costs. Compliance with international standards such as European Union REACH regulations or United States Environmental Protection Agency guidelines becomes essential for exporters, yet meeting these specifications demands substantial research and development investment that smaller regional blenders may struggle to afford. Regulatory bodies across Africa are progressively adopting stricter chemical composition standards to reduce environmental impact, requiring manufacturers to reformulate products and revalidate performance characteristics. Additionally, waste lubricant management regulations impose collection, recycling, or proper disposal obligations that increase operational complexity and cost structures for industrial users. The absence of harmonized regional regulatory frameworks means that manufacturers must maintain multiple product variants and documentation systems, elevating administrative overhead and slowing time to market for new formulations. These regulatory dynamics create barriers to entry and expansion, particularly for small and medium enterprises, thereby restraining overall market growth potential despite favorable demand fundamentals.

MARKET OPPORTUNITIES

Accelerated Adoption of Synthetic and Bio-Based Lubricants Supporting Sustainability Objectives

The transition toward synthetic and bio-based industrial lubricants presents substantial growth opportunities across the Middle East and Africa as industries prioritize energy efficiency and environmental compliance. Synthetic lubricants engineered from high-quality base oils and advanced additive packages deliver superior performance characteristics, including enhanced thermal stability, extended drain intervals, and reduced friction losses compared to conventional mineral oils. These attributes align with regional decarbonization commitments, as the International Energy Agency emphasizes that oil and gas operations must reduce emissions by over 60% by 2030 to remain on track for net-zero targets. Bio-based lubricants derived from renewable feedstocks such as vegetable oils or biomass-balanced additives offer biodegradability and lower carbon footprints while maintaining performance parity with fossil-derived alternatives, creating compelling value propositions for environmentally conscious industrial operators. Modern additive technologies have enabled lubricant change intervals to increase significantly in modern engines, reducing manufacturing, transportation, and disposal emissions across the product lifecycle. Regional governments are increasingly incentivizing sustainable industrial practices through tax benefits, green procurement policies, and technical assistance programs that favor high-performance, low environmental impact lubricants. Manufacturers who invest in synthetic and bio-based formulation capabilities can differentiate their offerings, command premium pricing, and secure long-term contracts with multinational industrial clients operating across the region. This sustainability-driven product evolution represents a high-value growth avenue that transcends conventional price competition and establishes technological leadership as a competitive advantage.

Integration of Digital Monitoring Technologies and Predictive Maintenance Solutions

The convergence of industrial lubricants with digital monitoring technologies and predictive maintenance platforms creates promising opportunities for value creation across the Middle East and Africa industrial landscape. Internet of Things sensors, real-time oil analysis systems, and artificial intelligence-driven condition monitoring enable industrial operators to optimize lubricant usage, extend equipment service intervals, and prevent unplanned downtime. Real-time oil monitoring installed across hydraulic systems can significantly reduce oil consumption and cut lubricant-related emissions by up to 80% through smarter maintenance protocols. These digital solutions generate continuous data streams that inform lubricant selection, application timing, and performance validation, transforming lubrication from a periodic maintenance task into an integrated component of asset management strategy. Industrial operators in mining, power generation, and manufacturing sectors increasingly recognize that predictive lubrication management delivers measurable returns through reduced equipment failures, lower inventory carrying costs, and enhanced operational reliability. Africa's industrial sector is expanding rapidly with automation adoption, creating fertile ground for digital lubrication solutions that improve efficiency and sustainability outcomes. Lubricant manufacturers who embed digital capabilities into their service offerings can transition from commodity suppliers to strategic technology partners, establishing recurring revenue streams through data analytics subscriptions and performance-based contracts. This digital transformation pathway enables premium positioning, deeper customer relationships, and defensible competitive advantages that support long-term market share expansion across the region.

MARKET CHALLENGES

Fragmented Distribution Networks and Supply Chain Complexity Across Diverse Geographic Markets

The Middle East and Africa industrial lubricants market confronts significant distribution challenges stemming from geographic fragmentation, infrastructure limitations, and heterogeneous market structures that impede efficient product delivery. Africa comprises 54 distinct national markets with varying import regulations, customs procedures, and logistical capabilities, creating a complex operational landscape that increases supply chain costs and delivery timelines. Frontier economies such as the Democratic Republic of Congo, Ethiopia, and Mozambique present particular difficulties due to underdeveloped road networks, limited warehousing infrastructure, and inconsistent energy access that complicate last-mile distribution to industrial end users. Traditional distributor-led models that historically dominated the African lubricant trade create structural dependencies where international brands struggle with limited visibility, inconsistent pricing, and diluted brand representation across multi-brand distributor portfolios. Counterfeit products further exacerbate these challenges, as informal markets in regions with weak regulatory enforcement introduce substandard lubricants that damage equipment and erode trust in legitimate brands. In the Middle East, while Gulf Cooperation Council nations offer more developed logistics ecosystems, cross-border trade with non-GCC countries still encounters customs delays, documentation requirements, and currency conversion complexities that increase transaction costs. Reaching industrial customers beyond major urban centers remains particularly challenging, as rural mining sites, remote power plants, and dispersed manufacturing facilities require specialized transportation arrangements and inventory management approaches. These distribution complexities constrain market penetration, elevate operational expenses, and limit the scalability of growth strategies for industrial lubricant suppliers operating across the region.

Prevalence of Counterfeit Products and Quality Control Issues in Informal Market Segments

Fragmented retail networks and limited regulatory oversight in many African markets enable the circulation of substandard or adulterated lubricants that fail to meet performance specifications, which is causing premature equipment wear, increased maintenance costs, and operational downtime for industrial users and further challenging the regional market expansion. Counterfeit products often mimic established brand packaging while containing inferior base oils or inadequate additive packages, creating significant risks for machinery operating under demanding conditions in mining, energy, and manufacturing applications. Informal mechanics and small workshops frequently source lubricants based on price rather than technical specifications, creating demand channels that favor low-cost, low-quality products over performance-optimized formulations. This dynamic pressures legitimate manufacturers to compete on price rather than value, compressing margins and limiting investment capacity for research, development, and technical support services. Additionally, the absence of standardized testing protocols and certification mechanisms across many regional markets complicates quality verification for industrial purchasers, who may lack the technical expertise or laboratory resources to authenticate product specifications. Combating counterfeit lubricants requires coordinated efforts among manufacturers, regulators, and industry associations to strengthen intellectual property enforcement, enhance consumer education, and implement track and trace technologies that verify product authenticity throughout the supply chain. Until these systemic challenges are addressed, the prevalence of substandard products will continue to constrain market development, damage brand reputations, and impede the adoption of advanced lubrication technologies across the region.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 5.43% |

| Segments Covered | By Base Oil, Product, End User, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, South Africa, Ethiopia, Kenya, Egypt, And Sudan |

| Market Leaders Profiled | ExxonMobil Corporation, Royal Dutch Shell plc, BP plc, Chevron Corporation, TotalEnergies SE, LUKOIL Oil Company, PETRONAS Lubricants International, FUCHS Petrolub SE, Idemitsu Kosan Co., Ltd. M, Sinopec Limited, ENOC Group, Gulf Oil Middle East Ltd., Qalaa Holdings (ASCOM), ORYX Energies, Addinol Lube Oil GmbH, Oman Oil Marketing Company, ENGIE Africa, Oryx Oil Company Limited, Master Lubricants Company (MLC), and others. |

SEGMENTAL ANALYSIS

By Base Oil Insights

The mineral oil segment dominated the market by holding the highest share of the Middle East and Africa industrial lubricants market in 2025 due to abundant regional refining capacity and cost competitiveness that aligns with price-sensitive industrial procurement practices. Mineral-based formulations deliver reliable viscosity characteristics and oxidation stability at accessible price points, making them the preferred choice for machinery operating in manufacturing plants, mining sites, and power generation facilities throughout the region. The dominance is further reinforced by compatibility with legacy equipment specifications and widespread technical familiarity among maintenance personnel who trust conventional lubricant performance profiles. Regional refineries produce substantial volumes of mineral base oils that feed domestic blending operations, reducing import dependency and supporting competitive pricing structures. Additionally, mineral oils demonstrate adequate performance in moderate temperature and load conditions prevalent across many industrial settings in the region, reducing the immediate need for premium synthetic alternatives in non-critical applications. This combination of economic accessibility, supply chain maturity, and technical adequacy sustains mineral oil as the foundational base stock choice for industrial lubricant consumption across the Middle East and Africa.

On the other hand, the synthetic oil segment is projected to grow at the fastest CAGR in the regional market during the forecast period, owing to the escalating demand for high-performance lubricants capable of withstanding extreme operating conditions inherent to Middle Eastern and African industrial environments. The transition is accelerated by original equipment manufacturer recommendations that specify synthetic base stocks for new generation turbines, compressors, and hydraulic systems designed for maximum uptime in harsh climates. Regulatory frameworks promoting energy efficiency and emissions reduction further favor synthetic lubricants that minimize friction losses and support cleaner combustion in power generation applications. Technological advancements in polyalphaolefin and ester chemistry have improved synthetic oil compatibility with diverse additive packages, expanding application suitability across metalworking, gear lubrication, and compressor systems. Regional investments in synthetic base oil production capacity enhance supply security and price stability for end users. These converging factors position synthetic oil for sustained volume growth as industrial modernization initiatives prioritize performance optimization and sustainability outcomes throughout the forecast horizon.

By Product Insights

The hydraulic fluid segment held the largest share of the regional market in 2025. The dominance of the hydraulic fluid segment in the global market is attributed to the pervasive deployment across construction equipment, mining machinery, and industrial automation systems that rely on pressurized fluid power for precise motion control and heavy load handling. The growing adoption of advanced hydraulic technologies such as electrohydraulic controls and high-pressure systems in modern excavators, cranes, and material handling equipment further elevates fluid performance requirements and drives premium product adoption. Regional manufacturing growth in automotive assembly, metal fabrication, and food processing sectors amplifies demand for hydraulic fluids that meet stringent cleanliness and compatibility standards. Additionally, the expansion of mining operations across Sub-Saharan Africa increases the consumption of high viscosity index hydraulic oils designed for dust-laden environments and extreme temperature variations. Distributors and service providers increasingly offer fluid analysis and condition monitoring services that optimize hydraulic system maintenance schedules, reinforcing customer loyalty and repeat procurement patterns. These interconnected demand drivers sustain hydraulic fluid as the predominant product category within the regional industrial lubricants landscape.

However, the deployment of the specialty turbine lubrication segment is set to outpace other product variants over the next few years, corresponding directly with massive regional electrical grid modernizations. Turbine oil demonstrates the most rapid growth trajectory, fueled by accelerating investments in power generation infrastructure and the transition toward gas-fired and renewable energy facilities that depend on specialized lubrication for reliable turbine operation. The shift from aging coal-fired units to modern gas turbines in countries like Egypt, South Africa, and Kenya creates replacement demand for advanced lubricants capable of extended service intervals and reduced maintenance burden. Technological innovations in ester-enhanced and synthetic turbine oils enable operation at elevated temperatures while maintaining film strength and deposit control, supporting higher efficiency power generation cycles. Regulatory emphasis on environmental compliance favors biodegradable turbine fluid formulations for hydroelectric applications in ecologically sensitive regions, expanding market opportunities for sustainable product variants. Additionally, the integration of digital monitoring systems for turbine oil condition assessment creates value-added service opportunities that strengthen customer relationships and support premium pricing strategies. These dynamics position turbine oil for accelerated adoption as regional energy infrastructure modernization intensifies throughout the forecast period.

By End User Insights

The power generation segment held the leading share of the Middle East and Africa industrial lubricants market in 2025 due to critical reliance on specialized lubricants for maintaining reliable operation of turbines, generators, transformers, and auxiliary equipment that underpin regional energy security. The transition toward cleaner energy sources, including solar thermal and wind power, introduces novel lubrication requirements for heat transfer systems, gearboxes, and pitch control mechanisms that drive demand for specialized formulations. Regional initiatives to reduce carbon emissions and improve energy efficiency favor lubricants that minimize friction losses and extend equipment service life, aligning procurement decisions with sustainability objectives. Additionally, the growing prevalence of distributed generation and microgrid solutions in remote African communities creates opportunities for compact lubrication systems that support decentralized power infrastructure. Maintenance contractors and original equipment manufacturers increasingly specify premium lubricants backed by technical support services, reinforcing quality-focused procurement practices that benefit established suppliers. These converging factors sustain power generation as the most influential end-user segment shaping market dynamics across the region.

On the other hand, the construction segment is anticipated to showcase the most rapid expansion among end-user segments during the forecast period, propelled by unprecedented infrastructure development commitments across Gulf Cooperation Council nations and emerging African economies that collectively drive demand for heavy equipment lubrication solutions. Construction equipment operates under extreme conditions, including high ambient temperatures, abrasive dust environments, and variable load cycles that necessitate lubricants with superior anti-wear protection, thermal stability, and contamination tolerance. The growing adoption of advanced hydraulic systems and electrified construction machinery introduces new lubrication requirements that favor synthetic and semi-synthetic formulations capable of extended service intervals and reduced maintenance frequency. Regional manufacturing growth in cement production, steel fabrication, and building materials further amplifies demand for industrial lubricants that support continuous plant operation and equipment reliability. Additionally, the expansion of urban transportation networks, including metro systems, airports, and port facilities, creates sustained demand for construction lubricants throughout multiyear project lifecycles. Equipment rental companies and contractor networks increasingly prioritize total cost of ownership metrics that favor premium lubricants delivering measurable productivity gains, supporting market penetration for high-performance product variants. These dynamics position construction as the fastest-growing end-user segment within the regional industrial lubricants market.

REGIONAL ANALYSIS

Saudi Arabia held 37.21% regional market share in 2025. The Kingdom of Saudi Arabia's domestic construction and industrial sectors are anticipated to demonstrate unrivaled growth over the next few years, cementing its status as the regional hub for heavy industrial manufacturing. Saudi Arabia maintains a preeminent position within the Middle East and Africa Industrial Lubricants Market, driven by its expansive industrial base, abundant hydrocarbon resources, and ambitious economic diversification programs that collectively stimulate sustained lubricant consumption across multiple sectors. The Kingdom benefits from integrated refining and blending infrastructure that supplies domestic industrial users while supporting export-oriented lubricant production for regional markets. Vision 2030 initiatives, including NEOM, Red Sea Project, and Qiddiya entertainment city, mobilize substantial capital expenditure on construction equipment, manufacturing facilities, and energy infrastructure that elevate demand for hydraulic fluids, turbine oils, and metalworking lubricants. The petrochemical sector expansion through massive corporate joint ventures creates specialized lubrication requirements for high-temperature compressors, polymer processing equipment, and catalyst handling systems that favor premium synthetic formulations. Regional manufacturing growth in automotive assembly, metal fabrication, and food processing further diversifies end-user demand and supports market resilience against sector-specific volatility. Additionally, Saudi Aramco domestic content mandates encourage local lubricant blending operations.

COMPETITION OVERVIEW

The Middle East and Africa Industrial Lubricants Market exhibits consolidated competitive dynamics characterized by established multinational corporations leveraging technical expertise, brand recognition, and integrated supply chains to maintain leadership positions across premium industrial lubricant segments. Regional players compete through localized manufacturing capabilities, cost-efficient distribution networks, and customized formulations that address specific operational requirements of African and Middle Eastern industrial environments. Market competition intensifies around technological differentiation as companies invest in synthetic chemistry, additive innovation, and digital lubrication management platforms to deliver measurable performance advantages for industrial customers. Price competition remains relevant in commodity lubricant segments where mineral oil-based products serve price-sensitive applications, yet value-based competition dominates premium segments where total cost of ownership metrics favor high-performance formulations. Strategic partnerships between international technology providers and regional blenders create hybrid competitive models that combine global innovation with local market knowledge to capture growth opportunities across diverse industrial end-user segments. The competitive landscape continues evolving as sustainability mandates, energy transition initiatives, and digital transformation trends reshape customer priorities and create new avenues for differentiation beyond traditional product performance parameters.

KEY MARKET PLAYERS

A few major players of the Middle East and Africa Industrial Lubricants Market include

- ExxonMobil

- Corporation

- Royal Dutch Shell plc

- BP plc

- Chevron Corporation

- TotalEnergies SE

- LUKOIL Oil Company

- PETRONAS Lubricants International

- FUCHS Petrolub SE

- Idemitsu Kosan Co., Ltd

- M, Sinopec Limited

- ENOC Group

- Gulf Oil Middle East Ltd

- Qalaa Holdings (ASCOM)

- ORYX Energies

- Addinol Lube Oil GmbH

- Oman Oil Marketing Company

- ENGIE Africa

- Oryx Oil Company Limited

- Master Lubricants Company (MLC)

- Others

Top Strategies Used By Key Market Participants

Key market participants employ product innovation strategies focusing on synthetic and bio-based formulations that deliver superior performance and environmental compliance to differentiate offerings in competitive industrial lubricant segments. Companies pursue geographic expansion through strategic partnerships with regional blenders and distributors that enhance market access while reducing logistics costs and import dependencies across diverse African and Middle Eastern markets. Technical service investments, including mobile laboratories, digital monitoring platforms, and application engineering support, strengthen customer relationships and create value-added revenue streams beyond commodity lubricant sales. Sustainability integration strategies align product development with circular economy principles and regulatory requirements to capture growing demand for environmentally responsible industrial lubricants across energy transition and infrastructure modernization projects. Vertical integration initiatives spanning base oil production, additive formulation, and finished product blending enhance supply chain control and margin protection against raw material price volatility in dynamic regional markets.

Leading Players in the Market

- Exxon Mobil Corporation maintains an influential position within the Middle East and Africa Industrial Lubricants Market through its comprehensive product portfolio, technical expertise, and strategic partnerships that support diverse industrial applications across the region. The company leverages its global research and development capabilities to deliver advanced lubricant formulations that meet stringent performance requirements for energy extraction, manufacturing, and transportation sectors. Exxon Mobil's recent initiatives include expanding technical service centers in Saudi Arabia and South Africa to provide application engineering support and fluid analysis services that enhance customer value and strengthen brand loyalty. The company's commitment to sustainability drives the development of bio-based and low-emission lubricant variants that align with regional environmental regulations and corporate responsibility objectives. Exxon Mobil's distribution network partnerships with regional blenders and distributors, ensures reliable product availability across remote industrial locations while maintaining quality standards consistent with global specifications. These strategic capabilities position Exxon Mobil as a trusted technology partner for industrial operators seeking performance optimization and operational efficiency throughout the Middle East and Africa.

- TotalEnergies SE demonstrates a strong market presence within the Middle East and Africa Industrial Lubricants Market through integrated value chain capabilities spanning base oil production, additive formulation, and finished product blending that support competitive positioning across diverse industrial segments. The company's recent investments in synthetic base oil capacity and specialty additive technologies enable delivery of high-performance lubricants that extend equipment life and reduce maintenance costs for energy-intensive industrial applications. TotalEnergies strategic partnerships with regional industrial operators include joint development programs for customized lubricant solutions that address specific operational challenges in mining, power generation, and manufacturing environments. The company's sustainability commitments drive innovation in biodegradable and recyclable lubricant formulations that support circular economy principles and regulatory compliance across environmentally sensitive applications. TotalEnergies technical support infrastructure, including mobile laboratories and digital monitoring platforms, enhances customer engagement and reinforces brand differentiation through value-added services that optimize lubrication management practices. These integrated capabilities position TotalEnergies as a solutions-oriented partner for industrial operators pursuing operational excellence and environmental stewardship throughout the region.

- Shell PLC maintains a prominent position within the Middle East and Africa Industrial Lubricants Market through its extensive brand portfolio, technical innovation leadership, and localized manufacturing presence that support reliable supply and application expertise across diverse industrial sectors. The company's recent introduction of PANOLIN biodegradable lubricant range in the Middle East demonstrates a commitment to environmental sustainability while meeting performance requirements for sensitive applications in marine, mining, and hydropower sectors. Shell's strategic collaborations with regional equipment manufacturers and maintenance service providers enable co-development of lubricant specifications that optimize machinery performance and extend service intervals under challenging operating conditions. The company's digital lubrication management platforms, including condition monitoring sensors and predictive analytics tools, enhance customer value by reducing unplanned downtime and optimizing maintenance scheduling across industrial asset portfolios. Shell's investment in local blending facilities and technical training programs strengthens supply chain resilience and builds long-term customer relationships through knowledge transfer and capability development initiatives. These strategic advantages position Shell as a trusted innovation partner for industrial operators seeking performance reliability and sustainability leadership throughout the Middle East and Africa region.

MARKET SEGMENTATION

This research report on the Middle East and Africa Industrial Lubricants Market has been segmented and sub-segmented based on the following categories.

By Base Oil

- Mineral oil

- Synthetic oil

- Bio-oil

By Product

- Engine oil

- Metalworking fluid

- Hydraulic fluid

- Turbine oil

- Grease

- Gear

- Compressor

By End-User

- Automotive

- Construction

- Power generation

- Metal

- cement

- manufacturing

- food

By Country

- KSA

- UAE

- Isarel

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

Frequently Asked Questions

1. What is driving the growth of the Middle East and Africa industrial lubricants market?

Market growth is mainly driven by rapid industrialization, infrastructure development, expansion of manufacturing activities, and increasing investments in mining and energy exploration sectors.

2. Which base oil segment dominates the market?

Mineral oil dominates the market due to its cost-effectiveness and widespread availability for industrial applications

3. Which product segment holds a significant share in the market?

Process oils account for a significant share due to their extensive use in rubber processing, textiles, and chemical industries.

4. What are the major applications of industrial lubricants?

Industrial lubricants are widely used in hydraulic systems, compressors, turbines, gears, and metalworking equipment in manufacturing plants.

5. Which countries contribute significantly to market growth?

Saudi Arabia, the United Arab Emirates, Egypt, South Africa, and Nigeria are among the key contributors to the MEA industrial lubricants market growth.

6. What trends are shaping the Middle East and Africa industrial lubricants market?

Key trends include increasing demand for synthetic lubricants, technological advancements in lubricant formulations, and rising adoption of eco-friendly lubricant solutions.

8. Which distribution channel dominates the market?

Direct industrial procurement channels dominate due to large-scale consumption of lubricants by manufacturing industries.

9. How are technological advancements influencing the market?

Innovations in additive technologies and synthetic lubricants are enhancing machinery efficiency and extending equipment life

10. What is the future outlook of the Middle East and Africa industrial lubricants market?

The market is expected to witness steady growth due to increasing industrial activities and technological innovations in lubricant production.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com