Middle East And Africa Liquid Fertilizers Market Size, Share, Growth, Trends Report, Segmented By Nutrient Type (Potassium, Micronutrients, Phosphate, Nitrogen), Form (Organic, Synthetic), Mode Of Application (Soil, Fertigation, Foliar, And Others), Crop Type (Oil Seeds, Fruits & Vegetables, Grains & Cereals, And Others), And By Country (KSA, UAE, Israel, Rest of the GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, Rest of MEA), Industry Analysis From 2024 to 2033

Middle East and Africa Liquid Fertilizers Market Size

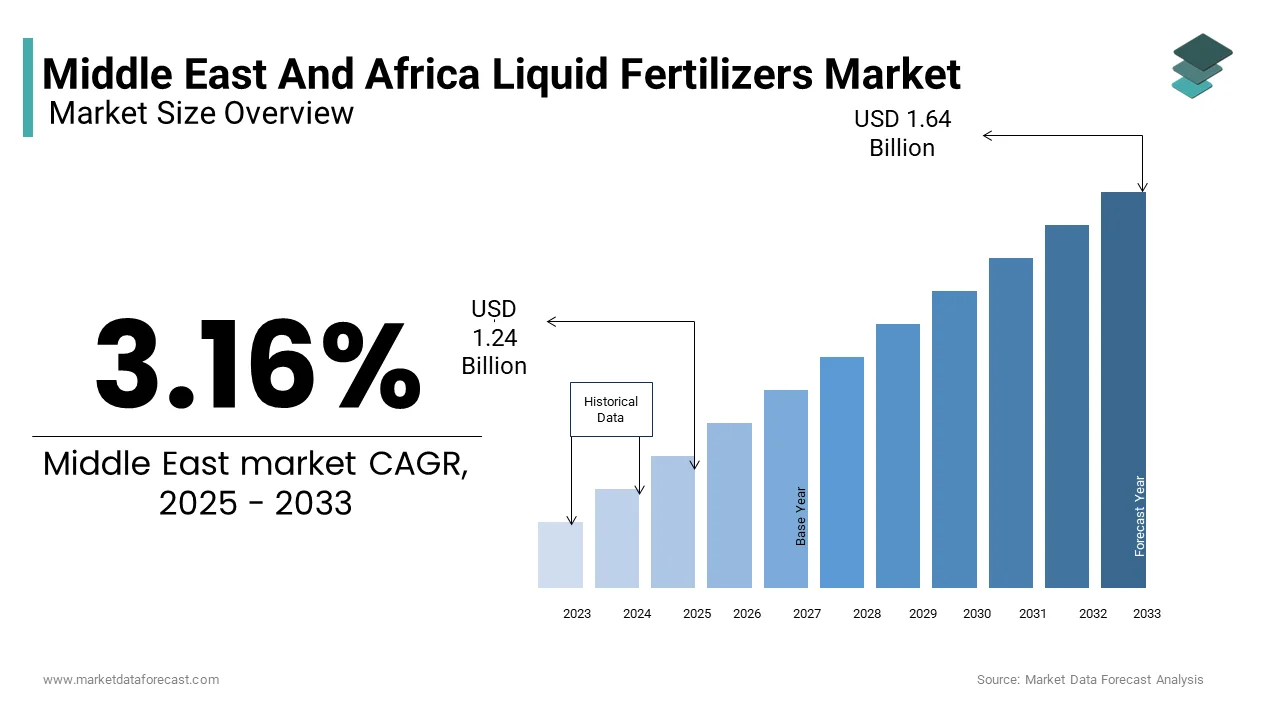

The Middle East And Africa Liquid Fertilizers market is anticipated to reach from USD 1.24 billion in 2024 to USD 1.64 billion by 2033, growing at a CAGR of 3.16%.

Liquid Fertilizers are a nutrient-rich liquid formulation used to enhance soil fertility and crop yield across diverse agricultural landscapes. Unlike traditional solid fertilizers, liquid variants offer greater ease of application through fertigation and foliar spraying systems, enabling precise nutrient delivery and faster absorption by plants. This market includes a wide array of products such as nitrogen-based solutions, phosphatic liquids, potassium-containing formulations, and specialty blends enriched with micronutrients.

Given the region’s arid climate and water-scarce conditions, particularly in the Middle East, liquid fertilizers are increasingly favored for their compatibility with precision irrigation technologies like drip and sprinkler systems. As per the Food and Agriculture Organization (FAO), over 65% of cultivated land in Gulf Cooperation Council (GCC) countries now utilizes some form of controlled irrigation, significantly boosting demand for compatible nutrient delivery methods.

In Sub-Saharan Africa, rising awareness among smallholder farmers about improved agricultural inputs has led to the gradual but steady adoption of liquid fertilizers. Countries like Kenya and Nigeria have seen increased government support for modern farming techniques, aligning with regional food security goals. Apart from these, growing investments in agri-tech startups and digital farming platforms are facilitating better access to advanced fertilizer products across rural areas, further shaping the evolving dynamics of the Middle East and Africa Liquid Fertilizers Market.

MARKET DRIVERS

Expansion of Precision Farming Techniques

The increasing adoption of precision farming practices, particularly in large-scale commercial agriculture is one of the primary drivers fueling the growth of the Middle East and Africa Liquid Fertilizers Market. Precision farming relies on efficient resource utilization—especially water and nutrients—to maximize yield while minimizing environmental impact. Given the widespread use of drip and sprinkler irrigation systems in arid regions such as Saudi Arabia, Israel, and Egypt, liquid fertilizers have become an essential component due to their solubility and compatibility with fertigation systems.

These systems allow farmers to apply precise quantities of nutrients in real time, reducing waste and improving plant uptake efficiency. In addition, governments across the GCC region have launched initiatives promoting sustainable agricultural practices, including subsidies for high-efficiency irrigation equipment and associated inputs.

Moreover, in North African countries like Morocco and Tunisia, where water scarcity remains a persistent challenge, the integration of liquid fertilizers into national agricultural strategies has been actively encouraged. As per the Moroccan Ministry of Agriculture, more than 40% of citrus and vegetable farms have shifted toward liquid-based nutrient applications to optimize productivity under constrained water availability. These developments are strengthening their strategic importance in the regional market.

Rising Government Support for Agricultural Modernization

Government-backed agricultural modernization programs are playing a crucial role in accelerating the adoption of liquid fertilizers across the Middle East and Africa. Many national ministries recognize the need to boost domestic food production amid growing populations and climate-induced challenges. As part of broader agricultural reforms, several governments have introduced policies and funding mechanisms aimed at promoting the use of advanced input materials, including liquid fertilizers.

In Saudi Arabia, Vision 2030 includes a dedicated agenda for agricultural sustainability, encouraging the transition from conventional to technologically enhanced farming methods. The Kingdom’s Ministry of Environment, Water, and Agriculture has allocated significant funds to support the procurement and distribution of liquid fertilizers to registered farm cooperatives. Similarly, in Egypt, the Ministry of Agriculture has partnered with international agribusiness firms to provide subsidized liquid nutrient packages to small and medium-scale farmers.

In Sub-Saharan Africa, countries such as Ethiopia and Ghana have implemented national fertilizer subsidy programs that now include provisions for liquid formulations, recognizing their efficacy in improving yields with reduced application rates. These policy-driven interventions are instrumental in reshaping farmer behavior and fostering sustained market expansion for liquid fertilizers in the region.

MARKET RESTRAINTS

Limited Awareness Among Smallholder Farmers

The limited awareness and understanding among smallholder farmers regarding their benefits and application techniques is a major constraint impeding the widespread adoption of liquid fertilizers in the Middle East and Africa. Despite growing government efforts to promote modern agricultural inputs, many rural farmers continue to rely on traditional solid fertilizers due to familiarity and perceived cost advantages. According to the Food and Agriculture Organization (FAO), over 60% of small-scale farmers in Sub-Saharan Africa lack formal training on best agronomic practices, including the proper use of liquid nutrient solutions.

This knowledge gap is exacerbated by inadequate extension services and poor dissemination of technical information at the grassroots level. In countries like Tanzania and Mali, where mobile internet penetration remains low, access to digital advisory tools that could educate farmers on liquid fertilizer usage is limited. Besides, misconceptions about the effectiveness and affordability of liquid fertilizers persist, especially in regions where extension officers have not actively promoted their integration into local farming systems.

Furthermore, language barriers and inconsistent messaging from local distributors contribute to confusion among farmers. As per a study conducted by the International Institute of Tropical Agriculture (IITA), less than 20% of surveyed farmers in West Africa had accurate knowledge of fertigation-compatible fertilizers.

High Import Dependency and Supply Chain Limitations

The heavy reliance on imported raw materials and finished products, coupled with weak supply chain infrastructure is another critical restraint affecting the Middle East and Africa Liquid Fertilizers Market. Unlike in more industrialized regions, local manufacturing capacity for liquid fertilizers remains limited, particularly in Sub-Saharan Africa. As a result, most countries depend on imports from Europe, Asia, and North America to meet domestic demand, exposing them to price volatility and logistical disruptions.

This dependency increases costs and limits accessibility, especially in remote and underserved regions. Moreover, inadequate transportation networks and storage facilities often lead to product degradation and delayed deliveries, discouraging consistent usage among farmers.

Moreover, import duties and regulatory hurdles in certain countries further inflate prices, making liquid fertilizers less competitive compared to cheaper, locally available alternatives. For instance, in Nigeria, tariffs on imported agricultural inputs remain relatively high, despite ongoing reform discussions.

MARKET OPPORTUNITY

Growth of Hydroponics and Controlled Environment Agriculture (CEA)

The rapid expansion of hydroponics and controlled environment agriculture (CEA), particularly in urban and arid regions is an emerging opportunity driving the Middle East and Africa Liquid Fertilizers Market. With traditional soil-based farming constrained by water scarcity and land degradation, hydroponic systems where plants are grown in nutrient-rich water solutions are gaining traction as a sustainable alternative. Liquid fertilizers play a central role in these systems by providing essential macro and micronutrients in a readily absorbable form.

Countries like the UAE and Qatar have heavily invested in vertical farming and greenhouse cultivation, where liquid fertilizers are integral to maintaining optimal plant nutrition.

Beyond the Middle East, African nations are also exploring hydroponics to address food insecurity. In South Africa and Kenya, urban farming startups are leveraging liquid fertilizers to grow vegetables in rooftop greenhouses and repurposed warehouses. As governments and private investors continue to back CEA initiatives, the demand for specialized liquid formulations tailored for hydroponic use is expected to rise significantly.

Rise of Digital Farming Platforms and E-Commerce Distribution

The proliferation of digital farming platforms and e-commerce channels presents a transformative opportunity for expanding the reach of liquid fertilizers across the Middle East and Africa. With increasing smartphone penetration and internet connectivity, farmers, particularly in rural areas, are gaining access to online marketplaces, mobile advisory services, and direct-to-consumer agri-input sales models. These digital tools are helping bridge the gap between manufacturers and end users, enhancing product visibility and affordability.

Startups such as Hello Tractor in Kenya and Thrive Agric in Nigeria have integrated liquid fertilizer suppliers into their mobile-based service offerings, allowing farmers to order and receive customized nutrient solutions with minimal intermediation.

In the Middle East, companies like Pure Harvest Smart Farms in the UAE utilize cloud-based agronomy management systems that recommend specific liquid fertilizer blends based on real-time crop data. Governments in the region are also supporting these innovations through smart agriculture initiatives.

MARKET CHALLENGES

High Cost Relative to Traditional Fertilizers

The relatively higher cost of liquid formulations compared to conventional solid fertilizers is one of the foremost challenges facing the Middle East and Africa Liquid Fertilizers Market. While liquid fertilizers offer superior efficiency and compatibility with modern application methods, their upfront pricing remains a deterrent for many smallholder and budget-conscious farmers. According to the African Fertilizer and Agribusiness Partnership (AFAP), liquid fertilizers can be up to 30% more expensive per unit of nutrient content than granular or powdered alternatives, limiting their adoption in price-sensitive markets.

This cost disparity is primarily attributed to formulation complexity, packaging requirements, and transportation expenses. Liquid fertilizers often require specialized containers and handling procedures to prevent leakage and contamination, adding to production and logistics costs. In regions where bulk purchasing and cooperative distribution models are underdeveloped, individual farmers face higher retail prices, further constraining market penetration.

Moreover, in many parts of Sub-Saharan Africa, where cash flow limitations are common, farmers prioritize immediate affordability over long-term yield benefits. Without sufficient financial incentives or subsidies, the economic viability of switching to liquid fertilizers remains questionable for a large segment of the agricultural community.

Lack of Standardization and Quality Control

The lack of standardized quality control measures and regulatory oversight across the region is a significant challenge impeding the growth of the Middle East and Africa Liquid Fertilizers Market. Unlike in developed agricultural markets, where stringent certification processes ensure product consistency and safety, many African and Middle Eastern countries struggle with fragmented regulatory frameworks and inconsistent enforcement.

Also, only a handful of African nations have established comprehensive standards for liquid fertilizer composition and labeling. This absence of uniformity allows substandard or misbranded products to enter the market, undermining consumer confidence and hindering legitimate market expansion. In some cases, counterfeit or diluted fertilizers are sold without proper testing, leading to poor performance and potential harm to crops.

In response, organizations such as the African Regional Organization for Standardization (ARSO) have initiated efforts to harmonize fertilizer regulations across member states. However, implementation remains slow due to limited institutional capacity and coordination challenges.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.16% |

| Segments Covered | By Nutrient, Form, Mode Of Application, Crop Type, and By Country |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, rest of MEA. |

| Market Leaders Profiled | Haifa Chemicals Ltd, Kugler Company, Yara International ASA, Israel Chemicals Ltd, Agrium Inc, Sociedad Quimica Y Minera SA (SQM). |

SEGMENTAL ANALYSIS

By Nutrient Type Insights

Nitrogen

The nitrogen-based liquid fertilizers segment commanded the Middle East and Africa Liquid Fertilizers Market by accounting for 36.7% of total revenue in 2024. The essential role nitrogen plays in promoting plant growth, particularly in staple crops such as maize, wheat, and rice, which are widely cultivated across the region, is primarily attributed to the dominance of the nitrogen-based liquid fertilizers segment.

According to the Food and Agriculture Organization (FAO), nitrogen deficiency remains a major constraint to agricultural productivity in many African soils, especially in countries like Nigeria and Ethiopia where continuous cropping without adequate nutrient replenishment has degraded soil fertility. As a result, farmers increasingly rely on liquid nitrogen formulations for rapid nutrient delivery and improved yield potential.

Moreover, the widespread adoption of fertigation systems in arid regions such as Saudi Arabia and the UAE has significantly boosted the demand for soluble nitrogen products that can be easily integrated into irrigation networks. The International Center for Biosaline Agriculture (ICBA) notes that over 60% of greenhouse farms in the Gulf Cooperation Council (GCC) countries utilize nitrogen-rich liquid blends due to their compatibility with precision farming techniques.

Further, government-backed fertilizer subsidy programs in Egypt and Morocco have prioritized nitrogen-based inputs, making them more accessible to smallholder farmers. These combined factors continue to strengthen nitrogen’s position as the leading nutrient type in the regional liquid fertilizers market.

Micronutrients

The micronutrient-based liquid fertilizers segment is projected to grow at the fastest compound annual growth rate (CAGR) of 12.5% over the forecast period, outpacing other nutrient types in the Middle East and Africa Liquid Fertilizers Market. The increasing awareness of the critical role micronutrients such as zinc, boron, iron, and manganese play in enhancing crop quality, yield, and resilience to environmental stress is propelling the surge of micronutrient-based liquid fertilizers segment.

According to the International Fertilizer Development Center (IFDC), nearly 50% of cultivated soils in Sub-Saharan Africa exhibit deficiencies in key micronutrients, directly affecting agricultural output and nutritional content of food crops. In response, governments and development agencies are promoting the use of micronutrient-enriched liquid fertilizers to address both food security and hidden hunger.

In Kenya, the Ministry of Agriculture reports that foliar application of micronutrient solutions has become a common practice among vegetable and fruit growers, who seek to improve produce appearance and shelf life for export markets. Similarly, in South Africa, commercial horticulture farms have adopted micronutrient liquid blends to enhance fruit coloration and sugar content.

Furthermore, advancements in chelated micronutrient formulations have improved bioavailability and efficiency, encouraging wider adoption among high-value crop producers.

By Form Insights

Synthetic

The synthetic liquid fertilizers segment dominated the Middle East and Africa Liquid Fertilizers Market by capturing a substantial portion of the total share in 2024. Their widespread availability, ease of formulation, and compatibility with large-scale agricultural operations that prioritize high-yield production are largely responsible for the strong presence of the synthetic liquid fertilizers segment.

These formulations offer predictable nutrient composition and immediate plant availability, making them ideal for intensive farming practices.

Moreover, the reliance on imported synthetic nutrients is particularly pronounced in countries like Egypt and Nigeria, where domestic agricultural expansion plans emphasize increased food production through conventional input usage.

Apart from these, multinational agrochemical companies have established strong supply chains for synthetic liquid fertilizers in the region, ensuring consistent product availability even in remote areas.

Organic

The organic liquid fertilizers segment is emerging as the fastest-growing segment in the Middle East and Africa Liquid Fertilizers Market and is projected to expand at a CAGR of 14.2% through 2033. Rising consumer preference for organic produce, increased awareness of sustainable farming practices, and supportive regulatory developments are driving the accelerated growth of the organic liquid fertilizers segment.

According to the Research Institute of Organic Agriculture (FiBL), the number of certified organic farms in Africa has grown by over 10% annually in recent years, particularly in countries like Uganda, Tanzania, and Kenya. These nations have seen a corresponding rise in demand for organic-compliant nutrient sources, including seaweed extracts, compost teas, and fish emulsions.

In the Middle East, the United Arab Emirates has launched several initiatives promoting organic agriculture, including certification frameworks and subsidies for eco-friendly inputs. The UAE Ministry of Climate Change and Environment notes that the organic farming area has expanded by nearly 25% since 2020, directly boosting the uptake of organic liquid fertilizers.

Besides, digital farming platforms and agri-tech startups are playing a crucial role in educating farmers about the benefits of organic nutrient solutions.

By Mode of Application Insights

Fertigation

The fertigation segment was the highest-performing mode of application within the Middle East and Africa Liquid Fertilizers Ma, commanding 41.6% of the total share in 2024. The region's heavy reliance on drip and sprinkler irrigation systems, particularly in arid and water-scarce environments where efficient nutrient and water management is critical, is largely associated with the dominance of the fertigation segment.

This method allows for precise control of nutrient delivery, reducing waste and enhancing absorption rates, which is especially beneficial in saline or low-fertility soils.

Similarly, in Saudi Arabia and Egypt, national agricultural modernization programs encourage the adoption of fertigation-compatible nutrient solutions to support sustainable food production.

Moreover, government-backed initiatives in Sub-Saharan Africa, such as Ghana’s Planting for Food and Jobs program, are promoting the use of liquid fertilizers through subsidized irrigation equipment packages.

Foliar

The foliar application segment is anticipated to grow at the fastest CAGR of 13.8% in the Middle East and Africa Liquid Fertilizers Market owing to its effectiveness in delivering nutrients directly to plant leaves for rapid absorption. This method is particularly advantageous in correcting micronutrient deficiencies and enhancing plant health during critical growth stages.

According to the International Fertilizer Association (IFA), foliar feeding is gaining popularity among fruit and vegetable growers in Kenya, South Africa, and Morocco due to its ability to improve crop aesthetics, increase resistance to pests and diseases, and boost overall yield. Smallholder farmers are increasingly adopting this technique as part of integrated nutrient management strategies.

In the UAE, where soil salinity poses challenges to root nutrient uptake, agronomists recommend foliar sprays containing chelated micronutrients to ensure optimal plant development. The Abu Dhabi Agricultural and Forestry Investment Company (IMAC) highlights that foliar applications have become standard practice in date palm and citrus orchards to address specific nutrient gaps.

Moreover, advancements in nano-fertilizer and biostimulant formulations have enhanced the efficacy of foliar sprays, making them more attractive to commercial growers seeking cost-effective and environmentally friendly solutions.

By Crop Type Insights

Fruits & Vegetables

The fruits & vegetables segment represents the biggest crop type in the Middle East and Africa Liquid Fertilizers Market by contributing 35.7% of total revenue in 2024. The lead position of this segment is attributed to the high economic value of these crops, the need for consistent quality, and the intensive nutrient management required to maintain productivity in diverse climatic conditions.

According to the Food and Agriculture Organization (FAO), fruits and vegetables account for a rapidly expanding portion of agricultural exports in countries like Egypt, Kenya, and Morocco. To meet both domestic and international market demands, farmers increasingly rely on liquid fertilizers to enhance yield, color, size, and shelf life—key attributes that determine marketability.

In the Middle East, particularly in the UAE and Israel, hydroponic and greenhouse farming of tomatoes, cucumbers, and peppers heavily depend on liquid nutrient solutions for optimal growth. The Israeli Ministry of Agriculture reports that over 90% of commercial vegetable farms utilize liquid fertilizers in combination with fertigation systems to ensure year-round production.

Moreover, in Sub-Saharan Africa, smallholder farmers engaged in contract farming for supermarket chains and export-oriented cooperatives are adopting liquid fertilizers to meet stringent quality standards.

Oilseeds

The Oilseeds segment, including soybean, sunflower, and sesame, is witnessing the fastest growth in the Middle East and Africa Liquid Fertilizers Market and is projected to expand at a CAGR of 12.7% over the next decade. The rising domestic and global demand for edible oils, coupled with efforts to reduce dependence on imports and enhance local production, is fuelling the upward trajectory of the oilseeds segment.

According to the United Nations Conference on Trade and Development (UNCTAD), African countries collectively spend over USD 15 billion annually on edible oil imports, prompting governments to invest in oilseed cultivation as part of broader self-sufficiency strategies. Countries like Nigeria, Ethiopia, and Sudan are actively promoting the use of liquid fertilizers to improve oilseed yields under varying soil and climate conditions.

In Nigeria, the Federal Ministry of Agriculture reports that soybean production has increased by over 20% in the past five years, supported by extension services promoting liquid nutrient blends tailored for leguminous crops. Similarly, In Nigeria, the Federal Ministry of Agriculture reports that soybean production has increased by over 20% in the past five years, supported by extension services promoting liquid nutrient blends tailored for leguminous crops.

Further, private-sector investments in agri-processing infrastructure have created stronger market linkages for oilseed farmers, incentivizing the adoption of yield-enhancing inputs. As policy support and market incentives align, the oilseeds segment is poised to drive significant growth in liquid fertilizer consumption across the region.

COUNTRY-LEVEL ANALYSIS

Saudi Arabia

Saudi Arabia maintained the largest share of the Middle East and Africa Liquid Fertilizers Market, contributing 22.6% of total regional revenue. The country's strategic push toward agricultural self-sufficiency, despite its harsh desert environment, has led to the widespread adoption of precision irrigation and nutrient delivery systems that favor liquid fertilizers.

According to the Saudi Ministry of Environment, Water and Agriculture, the Kingdom allocates over USD 2 billion annually to agricultural development, with a strong emphasis on water-efficient farming techniques. Over 70% of greenhouse farms and vertical agriculture projects in the country integrate liquid nutrient solutions into their fertigation systems to maximize productivity while minimizing water usage.

Apart from these, the Vision 2030 initiative includes targets for expanding domestic food production, prompting large-scale investments in hydroponics and controlled environment agriculture. Companies such as SABIC Agri-Nutrients and Ma'aden Phosphate are actively developing customized liquid fertilizer blends suited for local crops and soil conditions.

Egypt

Egypt is a significant player in the Middle East and Africa Liquid Fertilizers Market. The country's extensive agricultural base, coupled with government-led modernization programs, has created a conducive environment for the adoption of liquid fertilizers, particularly in high-value and staple crops. Furthermore, the Nile Delta and Upper Egypt regions have seen increased implementation of drip irrigation systems, which inherently require compatible liquid nutrient formulations. Private agribusiness firms such as AkzoNobel and Yara International have expanded their distribution networks in the country to meet growing demand from both smallholders and commercial farms. With ongoing investments in smart agriculture and digital advisory platforms, Egypt is well-positioned to maintain its strong foothold in the regional liquid fertilizers market, supporting both food security and export-oriented agriculture.

South Africa

South Africa is positioning itself as a key player due to its well-developed agricultural sector and progressive adoption of modern farming technologies. The country’s structured commercial farming landscape, particularly in fruit, wine, and grain production, supports a steady demand for high-efficiency nutrient solutions. Besides, the country’s strong agri-tech ecosystem, including digital platforms and farm advisory services, has played a pivotal role in promoting liquid fertilizer usage among both large-scale and emerging farmers. Organizations such as AgriSETA provide training programs on best practices in nutrient management, strengthening the importance of liquid formulations in sustainable agriculture. With an increasing focus on water conservation and yield optimization, South Africa is expected to sustain its influential role in shaping the regional liquid fertilizers market dynamics.

United Arab Emirates

The United Arab Emirates is distinguished by its advanced agricultural infrastructure and aggressive pursuit of food security goals. Despite limited arable land, the UAE has emerged as a leader in innovative farming technologies, including vertical farming, hydroponics, and greenhouse cultivation—all of which rely heavily on liquid nutrient solutions. According to the Ministry of Climate Change and Environment (MOCCAE), the UAE has invested over USD 1.5 billion in smart agriculture initiatives since 2020, with a particular emphasis on controlled-environment farming. Moreover, the National Food Security Strategy 2051 aims to elevate the UAE to the top 10 globally in food security, necessitating the widespread use of precision nutrient management tools. Local and international players such as UPL Limited and Netafim have expanded their presence in the UAE to cater to the growing demand for customized liquid fertilizers tailored to desert agriculture.

Nigeria

Nigeria represents one of the fastest-emerging markets in the Middle East and Africa Liquid Fertilizers Market. Driven by a burgeoning population, increasing government support for agriculture, and the rise of agri-tech innovations, the country is witnessing gradual but meaningful adoption of liquid fertilizers, particularly among smallholder and commercial farmers.

According to the Federal Ministry of Agriculture and Rural Development (FMARD), Nigeria’s agricultural sector contributes over 25% of the country’s GDP, with a strong focus on staple crops such as maize, cassava, and rice. Recent initiatives, including the Anchor Borrowers’ Programme and e-wallet fertilizer distribution system, have begun incorporating liquid fertilizer options to improve nutrient efficiency and yield outcomes. Moreover, Nigerian agri-tech startups like Thrive Agric and Hello Tractor are leveraging digital platforms to educate farmers on the benefits of liquid fertilizers and facilitate direct access to affordable products. The International Institute of Tropical Agriculture (IITA) reports that liquid fertilizer trials conducted in collaboration with local cooperatives have demonstrated up to a 30% yield increase in selected crops. As rural connectivity improves and financial inclusion expands, Nigeria’s liquid fertilizers market is poised for accelerated growth, making it a key growth engine in the region.

KEY MARKET PLAYERS

Haifa Chemicals Ltd, Kugler Company, Yara International ASA, Israel Chemicals Ltd, Agrium Inc, Sociedad Quimica Y Minera SA (SQM). Are the market players that are dominating the Middle East and Africa Liquid Fertilizers Market?

Top Players In The Market

One of the leading players in the Middle East and Africa Liquid Fertilizers Market is Yara International, a global leader in crop nutrition solutions. Yara has a strong presence across both regions, offering a wide range of liquid fertilizers tailored for diverse agricultural conditions. The company plays a crucial role in promoting sustainable farming through its nutrient-efficient products and digital advisory services.

Another key player is SABIC Agri-Nutrients, a major contributor to the Middle Eastern market, particularly in Saudi Arabia and neighboring Gulf countries. SABIC specializes in producing high-quality liquid nitrogen-based fertilizers that support large-scale commercial farming and greenhouse agriculture. Its strategic partnerships with regional governments enhance its market influence.

UPL Limited, a prominent agrochemical company, also holds significant relevance in the MEA region. UPL provides cost-effective and eco-friendly liquid fertilizer formulations, supporting smallholder and commercial farmers alike. Through its integrated supply chain and local distribution networks, UPL strengthens accessibility and adoption of advanced nutrient management practices across the region.

Top Strategies Used By Key Market Participants

Key players in the Middle East and Africa Liquid Fertilizers Market are increasingly focusing on product innovation and formulation customization to meet specific regional soil and crop requirements. Companies are developing specialized blends that address micronutrient deficiencies and enhance yield performance in arid and semi-arid environments.

Another dominant strategy is expanding local partnerships and strengthening distribution networks, especially in rural and underserved areas. By collaborating with government agencies, cooperatives, and agri-tech platforms, firms ensure broader reach and improved accessibility for smallholder farmers.

Lastly, leveraging digital technologies and precision agriculture tools has become essential for enhancing customer engagement and optimizing fertilizer applications. Integrating mobile-based advisory services, soil testing apps, and e-commerce platforms to offer end-to-end nutrient management solutions that improve farmer adoption and loyalty.

COMPETITION OVERVIEW

The competition in the Middle East and Africa Liquid Fertilizers Market is characterized by a mix of multinational agrochemical companies and regional manufacturers vying for market share through product differentiation, localized strategies, and technological integration. While global players such as Yara International and SABIC dominate due to their extensive R&D capabilities and established supply chains, regional firms and emerging startups are leveraging affordability and proximity to capture niche segments. In the Middle East, where large-scale commercial farming and controlled-environment agriculture prevail, competition centers around technical expertise, efficiency, and compatibility with precision irrigation systems. In contrast, in Sub-Saharan Africa, where smallholder farming dominates, companies compete based on accessibility, ease of use, and affordability. Strategic initiatives such as partnerships with government bodies, digital extension services, and direct-to-farmer distribution models are reshaping industry dynamics. Further, sustainability trends and regulatory shifts toward organic and bio-based fertilizers are influencing competitive positioning. As awareness of liquid fertilizers grows and adoption expands, competition is expected to intensify further, with innovation and market education playing pivotal roles in shaping future growth trajectories.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, Yara International launched a new line of customized liquid fertilizers specifically designed for date palm cultivation in the Gulf region, aiming to improve yield and fruit quality while reducing environmental impact.

- In March 2024, SABIC Agri-Nutrients expanded its distribution network in Egypt by partnering with local cooperatives to facilitate easier access to liquid fertilizers for smallholder farmers engaged in rice and wheat production.

- In June 2024, UPL Limited introduced a mobile-based agronomy advisory service in Kenya, enabling farmers to receive real-time recommendations on liquid fertilizer applications based on soil health assessments and crop needs.

- In August 2024, Netafim, in collaboration with an Israeli research institute, developed a new chelated micronutrient liquid formula optimized for fertigation in saline soils, targeting markets in Saudi Arabia and the UAE.

- In October 2024, OCP Group, a major phosphate producer based in Morocco, initiated a pilot program distributing subsidized liquid fertilizer kits to cooperative farms in Senegal and Ghana to promote efficient nutrient management among African growers.

MARKET SEGMENTATION

This research report on the Middle East and Africa Liquid Fertilizers Market is segmented and sub-segmented into the following categories.

By Nutrient Type

- Potassium

- Micronutrients

- Phosphate

- Nitrogen

By Form

- Organic

- Synthetic

By Mode of Application

- Soil

- Fertigation

- Foliar

- Others

By Crop Type

- Oilseeds

- Fruits & Vegetables

- Grains & Cereals

- Others

By Country

- KSA

- UAE

- Israel

- The rest of the GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- Rest of MEA

Frequently Asked Questions

What are liquid fertilizers?

Liquid fertilizers are nutrient-rich solutions applied to crops to enhance plant growth and soil fertility. They contain essential nutrients like nitrogen, phosphorus, potassium, and micronutrients in a dissolved or suspended form, making them easy to apply through irrigation systems or foliar sprays.

Why is there growing interest in liquid fertilizers in the Middle East and Africa?

The demand for liquid fertilizers is rising due to increasing awareness of efficient nutrient management, water scarcity challenges, and the need for sustainable farming practices. Liquid fertilizers offer better solubility, faster absorption by plants, and compatibility with drip and fertigation systems, making them ideal for arid and semi-arid regions common across the Middle East and parts of Africa.

How do climatic conditions influence the use of liquid fertilizers in the region?

The hot and dry climate in much of the Middle East and parts of Africa makes traditional solid fertilizers less effective due to rapid evaporation and runoff. Liquid fertilizers can be mixed directly into irrigation systems, ensuring more precise application and better nutrient uptake by plants even under harsh weather conditions.

Are there government initiatives supporting the use of liquid fertilizers?

Yes, several governments are promoting modern agricultural technologies, including precision farming and fertigation, through subsidies and training programs. For example, Egypt and Morocco have launched national programs to encourage farmers to adopt efficient nutrient delivery methods, including the use of liquid fertilizers.

What role does irrigation infrastructure play in the growth of the liquid fertilizers market?

Since liquid fertilizers are often applied through irrigation systems, the expansion of drip and sprinkler irrigation networks significantly supports their adoption. Countries investing in smart agriculture and water-saving techniques are seeing higher integration of liquid fertilizers into mainstream farming.

Who are the major players in the Middle East and Africa liquid fertilizers market?

While international companies such as Yara International, Haifa Chemicals, and The Mosaic Company operate in the region, local producers and distributors are gaining traction. Companies based in North Africa and the Gulf Cooperation Council (GCC) nations are increasingly manufacturing and supplying cost-effective liquid fertilizer formulations tailored to regional soil and crop needs.

How is e-commerce impacting the distribution of liquid fertilizers?

E-commerce platforms and digital farming services are making it easier for small and medium-scale farmers to access quality liquid fertilizers. In countries like Kenya and Nigeria, mobile-based agri-tech startups are connecting farmers with suppliers, offering advice on usage, and delivering products directly to farms.

What are the environmental benefits of using liquid fertilizers?

Liquid fertilizers generally allow for more controlled and targeted application, reducing nutrient wastage and minimizing environmental pollution. When used correctly, they help prevent over-application and leaching of chemicals into groundwater—critical concerns in water-scarce regions.

How is technology influencing the development of liquid fertilizers in the region?

Innovations such as nano-fertilizers, slow-release formulations, and sensor-based application tools are being tested and adopted. Some companies are also integrating IoT-enabled devices that monitor soil nutrient levels and automatically adjust liquid fertilizer dosages for optimal crop yield.

What is the projected growth of the Middle East and Africa liquid fertilizers market?

The market is expected to grow steadily over the next five to seven years, driven by increasing investments in agriculture modernization, population growth, and food security concerns. Analysts estimate a CAGR (Compound Annual Growth Rate) of around 6–8% during this period.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com