Middle East And Africa Specialty Feed Additives Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Type Of Feed (Vitamins, Antioxidants, Flavours And Sweeteners, Minerals, Binders, Acidifiers And Others), By Livestock (Aquatic Animals, Poultry, Swine, Ruminants And Others), By Type Of Feed (Liquid Feed And Dry Feed), By Function (Palatability Enhancement, Mycotoxin Management, Ingredient Preservation Digestive Performance Enhancement And Others) And By Region (KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, rest of MEA), Industry Analysis From 2025 to 2033

Middle East and Africa Specialty Feed Additives Market Summary

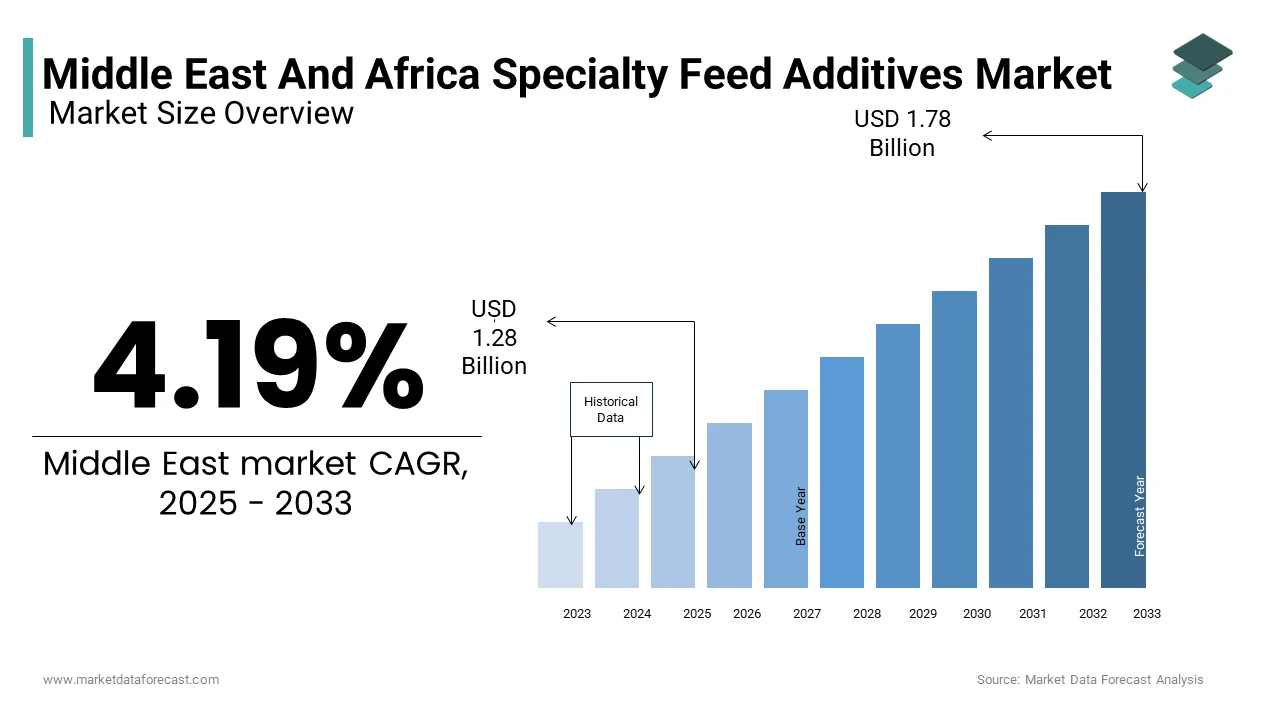

The Middle East And Africa specialty feed additives market was valued at USD 1.23 billion in 2024 and is anticipated to reach USD 1.28 billion in 2025 to USD 1.78 billion by 2033, growing at a CAGR of 4.19% during the forecast period from 2025 to 2033.

Key Market Trends & Insights

- Saudi Arabia led the Middle East And Africa Market in 2024

- Egypt is expected to showcase the strong growth throughout the forecast period.

- Based on Type, The vitamins was the leading segment in 2024

- Based on Livestock, The Poultry segment was commanded the market in 2024.

- Based Function, The Digestive performance enhancement segment led the market in 2024

Market Size & Forecast

2024 Market Size: USD 1.23 Billion

2033 projected Market Size: USD 1.78 Billion

CAGR (2025 to 2033): 4.19%

Saudi Arabia: Largest Market in 2024

Egypt: Strongest Growth Region

Middle East and Africa Specialty Feed Additives Market Size

The Middle East and Africa specialty feed additives market was valued at USD 1.23 billion in 2024 and is anticipated to reach USD 1.28 billion in 2025 to USD 1.78 billion by 2033, growing at a CAGR of 4.19% during the forecast period from 2025 to 2033.

Specialty Feed Additives are advanced nutritional compounds engineered to enhance animal productivity, improve feed efficiency, and support health in livestock, poultry, and aquaculture systems across diverse agro-climatic zones. These additives, including enzymes, probiotics, organic acids, amino acids, and mycotoxin binders, are increasingly integrated into formulated feeds to address physiological stressors prevalent in tropical and arid environments.

With a large portion of feed ingredients in sub-Saharan Africa derived from maize, sorghum, and soybean meal, crops inherently deficient in digestible phosphorus and essential amino acids, the role of specialty additives has become critical in unlocking nutritional value.

Like, a high percentage of cereal grains stored under humid conditions in West Africa are contaminated with aflatoxins, necessitating widespread use of adsorbent technologies. In Saudi Arabia, where natural forage is scarce, intensive dairy farms in the Al-Jouf region rely on enzyme-supplemented total mixed rations to maintain milk yields often exceeding 35 liters per cow per day.

Besides, rising urbanization and income growth are shifting protein consumption patterns. Thus, specialty feed additives are transitioning from optional inputs to essential components of modern animal production systems owing to prioritization of food security and sustainable intensification.

MARKET DRIVERS

Expanding Commercial Dairy and Poultry Production Drives Demand for Performance Enhancers

The rapid expansion of commercial livestock operations, particularly in dairy and poultry sectors, where maximizing output per animal is crucial due to limited land and water resources, is a principal driver shaping the Middle East and Africa specialty feed additives market.

Broiler integrators in Nigeria’s Ogun State have adopted enzyme-supplemented diets to improve feed conversion ratios, with field trials conducted by the National Animal Production Research Institute showing an enhancement in weight gain when xylanase and protease are included in maize-soy rations. Similarly, in Saudi Arabia’s vast dairy complexes such as Sadaka and Al Safi Danone, operators utilize amino acid-balanced feeds to sustain high lactation performance under extreme heat stress. The King Abdulaziz City for Science and Technology confirms that supplementing lactating cows with rumen-protected methionine increases milk protein content by 0.3 percentage points, directly improving product quality and revenue.

Furthermore, in Kenya’s peri-urban poultry belts, small-scale commercial farmers are adopting probiotic blends to reduce mortality linked to Salmonella and coccidiosis.

Government-Led Initiatives to Phase Out Antibiotic Growth Promoters Accelerate Substitution

The growing regulatory push across several countries to restrict or eliminate antibiotic growth promoters (AGPs) in animal feed, in alignment with global antimicrobial resistance (AMR) mitigation efforts, is another major driver. As per the World Health Organization, AMR causes a notable number of deaths annually in Africa alone, with agricultural misuse contributing significantly to resistant bacterial strains.

The Gulf Standardization Organization has also harmonized regulations among GCC states, mandating veterinary oversight for all antimicrobial use and encouraging alternatives. With the Africa Centres for Disease Control and Prevention advocating for coordinated AMR action plans, the policy environment increasingly favors non-antibiotic health modulators, positioning specialty additives as indispensable tools in compliant, future-ready animal production systems.

MARKET RESTRAINTS

Poor Cold Chain Infrastructure Compromises Viability of Microbial-Based Additives

The inadequate cold chain infrastructure, which severely impacts the stability and efficacy of live microbial products such as probiotics and fermented feed supplements, is one significant restraint affecting the specialty feed additives market in the Middle East and Africa. These temperature-sensitive additives require consistent refrigeration between 2°C and 8°C during storage and transport, a condition rarely met in rural distribution networks across sub-Saharan Africa.

Also, only a limited portion of pharmaceutical and biologic supply chains in East Africa maintain uninterrupted cold storage, and feed additives face even lower prioritization. In Tanzania, some probiotic samples collected from village-level agro-dealers showed zero viable colony-forming units after three weeks of ambient storage at 30–38°C. Similarly, in Sudan’s Kassala state, where summer temperatures exceed 45°C, enzyme activity in phytase powders declines within months of import.

The lack of climate-controlled warehouses and refrigerated trucks limits shelf life and undermines farmer confidence in premium products. Private distributors often resort to air-conditioned rooms or ice boxes, but these are neither scalable nor reliable. Without investment in temperature-regulated logistics, the performance gap between laboratory-tested efficacy and field outcomes will persist, constraining adoption despite proven benefits.

Prevalence of Informal Feed Mixing Limits Access to Precision Nutrition

The dominance of informal and on-farm feed mixing practices, particularly among smallholder producers, is another critical restraint. Most small-scale farmers blend maize bran, cottonseed cake, and kitchen waste manually, bypassing formulated feeds and thus excluding specialty additives entirely.

Like, in Uganda’s Central Region, a lesser percentage of poultry farmers purchase commercial rations, relying instead on inconsistent home-mixed feeds that lack balanced micronutrient profiles. This practice leads to deficiencies in vitamins A, D, and B12, resulting in poor feathering, skeletal deformities, and low egg production.

Moreover, extension services are sparse; only a few farmers receive regular technical advice on feed formulation. Even when commercial feeds are used, improper storage exposes them to moisture and pests, degrading additive potency.

MARKET OPPORTUNITY

Desert Agriculture Expansion Creates Demand for Heat-Stress Mitigation Additives

The proliferation of desert agriculture and enclosed livestock systems in Gulf Cooperation Council (GCC) countries, where extreme thermal stress necessitates advanced nutritional interventions, is an emerging opportunity for the market. In Saudi Arabia’s NEOM and Al-Kharj regions, vertically integrated poultry and dairy farms operate under controlled-environment housing, but animals still experience metabolic strain due to ambient temperatures exceeding 50°C. To counteract this, producers are incorporating betaine, vitamin C, and electrolyte complexes into rations to stabilize osmotic balance and maintain feed intake.

According to King Saud University’s College of Food and Agriculture Sciences, broilers supplemented with betaine during summer months exhibit higher daily weight gain and lower mortality.

With Kuwait and Bahrain investing in indoor aquaculture using recirculating systems, there is growing interest in immune-boosting nucleotides and omega-3 supplements to sustain fish health in closed-loop environments. These high-tech ventures represent a premium segment where performance certainty justifies investment in cutting-edge additives, opening a niche yet rapidly expanding frontier for specialty nutrition.

Rising Aquaculture Investments Drive Adoption of Functional Feeds in Coastal Economies

Increasing government-backed investments in aquaculture across coastal nations seeking to diversify protein sources and reduce import dependency is another transformative opportunity. The shift from capture fisheries to intensive tilapia and seabream farming requires formulated feeds enriched with enzymes, pigmentation agents, and immunostimulants. Also, astaxanthin-supplemented diets improve flesh coloration in market-ready tilapia, increasing consumer acceptance. As more countries develop regulatory frameworks for aquatic feed safety, the demand for certified specialty additives is set to accelerate, transforming aquaculture into a key growth vector for the regional market.

MARKET TECHNOLOGY

Counterfeit and Adulterated Products Undermine Trust in Premium Brands

The widespread circulation of counterfeit and substandard products, particularly in decentralized markets with weak enforcement mechanisms, is a primary challenge confronting the Middle East and Africa specialty feed additives market. Unregulated manufacturers replicate branded packaging and sell diluted or inactive formulations at lower prices, deceiving cost-sensitive farmers.

When farmers experience poor results, they often blame the technology rather than the source, eroding confidence in legitimate brands. Rebuilding trust requires robust authentication systems such as QR codes, blockchain traceability, and third-party certification—measures that increase costs and complexity for genuine suppliers operating in price-sensitive environments.

Limited Local Manufacturing Capacity Increases Import Dependency and Supply Volatility

A further critical challenge is the near-total reliance on imported specialty additives due to minimal local production capacity, exposing the region to currency fluctuations, trade disruptions, and logistical delays. A significant portion of amino acids, enzymes, and synthetic vitamins used in MEA are sourced from Europe, China, and India, as reported by the African Union’s Regional Economic Communities.

In Lebanon, where foreign exchange shortages persist, feed mills have faced months-long delays in securing lysine shipments, forcing temporary ration modifications. Similarly, during the Red Sea shipping crisis in 2024, Ethiopian poultry integrators experienced a spike in additive costs due to rerouted freight and insurance premiums. The absence of domestic synthesis facilities stems from high capital requirements, a lack of skilled labor, and insufficient R&D ecosystems. South Africa hosts the continent’s most advanced feed additive blending units, yet even it imports core actives. Until localized manufacturing emerges through public-private partnerships or industrial incentives, the market will remain vulnerable to external shocks, constraining scalability and long-term planning for both suppliers and end-users.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4.19% |

| Segments Covered | By Type, Livestock, Function, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, rest of GCC countries, South Africa, Ethiopia, Kenya, Egypt, Sudan, rest of MEA |

| Market Leaders Profiled | Novus International, BASF SE, Evonik Industries, Luca S.A., Chr. Hansen Holdings A/S, Biomin Holding GmbH, Invivo NSA, DSM, Akzo Nobel Surface Chemistry AB, Kemin Industries Inc., and Biomin Holding GmbH, Nutreco N.V |

SEGMENTAL ANALYSIS

By Type Insights

The vitamins segment was the prominent type in the Middle East and Africa specialty feed additives market by capturing 32.4% of total demand in 2024. The dominance of this segment is primarily driven by the physiological necessity of micronutrients in animal metabolism, particularly in regions where basal diets are nutritionally imbalanced. A further key factor behind its leadership is the widespread deficiency of essential vitamins, especially A, D, E, and B-complex, in cereal-based rations that form the backbone of livestock feeding across arid and semi-arid zones.

Like, in Egypt, where maize and wheat bran constitute a notable share of poultry feed, vitamin A deficiency affects several backyard flocks, leading to poor vision, reduced hatchability, and increased mortality. To counter this, commercial integrators like Al Watania Poultry have adopted fortified premixes, resulting in an improvement in egg production and chick viability.

Similarly, in Saudi Arabia, some intensive dairy farms, supplementation with vitamin E and selenium has been shown to reduce mastitis incidence. The region’s limited natural forage availability exacerbates deficiencies. Thus, vitamins remain non-negotiable components of modern animal nutrition, ensuring sustained segment supremacy is credited to governments promoting balanced ration programs and large-scale producers investing in flock health.

Acidifiers Emerge

The acidifiers segment is expanding at the fastest CAGR of 9.9% from 2025 to 2033, which is propelled by rising demand for antibiotic-free gut health management strategies in response to antimicrobial resistance (AMR) concerns and regulatory shifts. Organic acids such as formic, propionic, and butyric acid are increasingly used to lower gastrointestinal pH, inhibit pathogenic bacteria like Salmonella and E. coli, and improve protein digestibility in young animals.

As per South Africa’s Department of Agriculture, Land Reform and Rural Development, broiler farms adopting multi-acid blends in starter feeds recorded a reduction in necrotic enteritis cases, reducing reliance on therapeutic antibiotics. In Kenya’s some areas, layer operations using acidified drinking water observed a decline in Salmonella pullorum contamination. An additional critical driver is their preservative function; organic acids extend the shelf life of moist feed and prevent mold proliferation in tropical climates. Like, adding propionic acid to poultry mash in humid conditions reduces spoilage-related losses. With Gulf Cooperation Council states enforcing stricter controls on antibiotic use and African nations aligning with WHO AMR guidelines, acidifiers are transitioning from niche supplements to core components of modern feeding programs, fueling rapid market expansion.

By Livestock Insights

Poultry

The poultry segment commanded the Middle East and Africa specialty feed additives market by accounting for 34.2% of total consumption in 2024. The lead position of this segment is due to the region’s massive scale of chicken production, particularly in Egypt, Nigeria, and Saudi Arabia, where poultry serves as the primary source of affordable animal protein.

Also, Africa’s broiler meat output grew between 2015 and 2022, outpacing population growth, driven by urbanization and income gains. In Egypt, per capita poultry consumption increased, placing immense pressure on producers to maximize efficiency. Commercial integrators like Haramain Poultry in Saudi Arabia and CHICOCO in Côte d’Ivoire rely heavily on phytase and xylanase enzymes to extract energy from maize-soy diets, improving feed conversion ratios.

Additionally, vaccination failures due to immunosuppressive diseases like infectious bursal disease have increased reliance on immune-modulating additives. With governments promoting self-sufficiency in protein supply, the poultry sector continues to attract investment in advanced nutrition, making it the most additive-intensive livestock category in the region.

Ruminants

The ruminants segment is experiencing the fastest growth in specialty feed additive demand and is registering a CAGR of 9.4% from 2025 to 2033, and is fueled by the expansion of intensive dairy farming in water-scarce environments. In Gulf countries such as Saudi Arabia, UAE, and Oman, where natural pasture is virtually nonexistent, dairy production relies entirely on imported forage and formulated total mixed rations (TMR), necessitating high levels of nutritional intervention.

Rumen-protected amino acids like methionine and lysine are routinely included to optimize milk protein synthesis, with field data from Al Safi Danone showing an increase in protein content upon supplementation. In North Africa, Morocco supports modernization of smallholder herds through subsidized feed additives, including mineral-vitamin premixes and mycotoxin binders.

By Function Insights

Digestive Performance Enhancement

The digestive performance enhancement segment led the Middle East and Africa specialty feed additives market by commanding 35.1% of total demand in 2024. The dominance of this segment is rooted in the need to maximize nutrient utilization from low-cost, plant-based feedstuffs that dominate regional formulations. Diets rich in maize, sorghum, and cottonseed meal contain anti-nutritional factors such as phytic acid and non-starch polysaccharides, which impair mineral absorption and energy extraction.

Like, a notable share of phosphorus in unprocessed cereals is bound in phytate, rendering it unavailable to monogastric animals. To address this, phytase enzymes are now routinely included in broiler and swine rations across Egypt, Nigeria, and Saudi Arabia.

In addition, phytase supplementation increases phosphorus availability, reducing inorganic phosphate supplementation and lowering manure phosphorus runoff. Xylanase and glucanase are similarly used to break down arabinoxylans in wheat and barley, improving metabolizable energy. Moreover, protease enzymes help mitigate heat-damaged proteins in locally processed meals, particularly in feed mills lacking temperature control.

Mycotoxin Management

The mycotoxin management segment is growing at the fastest rate of 10.1% CAGR in the coming years and is driven by escalating contamination of staple feed grains due to climate change, poor storage infrastructure, and high humidity. Mycotoxins such as aflatoxin B1, deoxynivalenol (DON), and fumonisins are toxic fungal metabolites produced by Aspergillus and Fusarium species, which thrive in warm, damp conditions prevalent across sub-Saharan Africa.

According to the World Health Organization, aflatoxin exposure contributes to liver cancer and immune suppression in both humans and animals. Also, mycotoxin binders containing hydrated sodium calcium aluminosilicate (HSCAS) and yeast cell wall derivatives are now standard in commercial rations. Field trials showed that toxin adsorbents reduced liver lesions and improved weight gain.

COUNTRY-LEVEL ANALYSIS

Saudi Arabia

Saudi Arabia occupied the foremost position in the Middle East and Africa specialty feed additives market by holding 27.4% of regional demand in 202,4 and is driven by its status as a regional leader in vertically integrated livestock production. The country hosts some of the world’s largest dairy and poultry complexes, including Sadaka, Almarai, and Al Watania, all operating under controlled-environment systems that require scientifically formulated rations. Additionally, the government’s Vision 2030 includes ambitious food security targets, prompting investments in desert agriculture and enclosed livestock systems. The NEOM agritech hub incorporates AI-driven feeding protocols with real-time additive adjustments based on animal performance data.

Egypt

Egypt is another key player in the MEA specialty feed additives market and is fueled by state-backed efforts to achieve poultry and fish self-sufficiency amid growing population pressures. The country is Africa’s largest poultry producer. Additionally, aflatoxin contamination in domestic maize has prompted widespread adoption of mycotoxin binders. With the government subsidizing feed additive imports and supporting private-sector integrators, Egypt’s transition toward science-based animal nutrition is creating robust momentum for market expansion.

South Africa

South Africa is distinguished by its well-developed agricultural infrastructure and alignment with international food safety standards. The country hosts the continent’s most sophisticated feed milling industry. In dairy, rumen-protected choline is widely used to prevent fatty liver syndrome in high-yielding cows. With strong veterinary oversight, technical extension services, and adherence to OIE guidelines, South Africa serves as a model for regulated, high-integrity animal production in Africa.

United Arab Emirates

The United Arab Emirates captures a significant portion of the MEA specialty feed additives markmarketwhich is supported by its focus on technological innovation and food security in extreme climatic conditions. Despite minimal arable land, the UAE has developed some of the world’s most advanced enclosed livestock facilities, including indoor dairy farms in Abu Dhabi and vertical poultry units in Dubai. Additionally, the UAE’s ban on antibiotic growth promoters hasacceleratedd the adoption of probiotics and organic acids. With free-trade zones facilitating rapid import of cutting-edge additives and strong government backing for agri-tech, the UAE functions as a high-value testbed for next-generation animal nutrition solutions.

Kenya

Kenya holds an emerging place in the Middle East and Africa specialty feed additives market in 2024, driven by the rapid formalization of poultry farming and emerging aquaculture initiatives around Lake Victoria. The country produces significant metric tons of broiler meat annually, with commercial operations expanding in Nakuru, Kiambu, and Eldoret. In aquaculture, cage farming of Nile perch and tilapia has increased demand for immune-boosting additives. The government’s Livestock Productivity Enhancement Project supports smallholders in adopting balanced rations, while private players like Unga Group expand feed mill coverage. With rising urban protein demand and increasing technical capacity, Kenya represents one of the most dynamic and scalable markets for specialty additives in East Africa.

KEY MARKET PLAYERS

Novus International, BASF SE, Evonik Industries, Luca S.A., Chr. Hansen Holdings A/S, Biomin Holding GmbH, Invivo NSA, DSM, Akzo Nobel Surface Chemistry AB, Kemin Industries Inc., and Biomin Holding GmbH, Nutreco N.V. are market players that dominate the global specialty feed additives market.

Top Players In The Market

Cargill Animal Nutrition

Cargill Animal Nutrition is a dominant force in the Middle East and Africa specialty feed additives landscape, leveraging its global scientific expertise to address regional challenges in animal productivity and nutrition security. The company delivers tailored solutions that integrate advanced additive technologies with on-the-ground technical support, particularly in poultry, dairy, and aquaculture sectors across Egypt, Saudi Arabia, and South Africa. Cargill emphasizes holistic nutrition programs, combining amino acids, enzymes, and gut health modulators to optimize feed efficiency under extreme climatic and logistical constraints. Its collaboration with local integrators and government agencies supports the transition from traditional feeding practices to science-based formulations. Through digital tools and farmer education initiatives, Cargill enhances adoption and demonstrates measurable performance improvements. With a strong distribution network and commitment to sustainable intensification, the company plays a pivotal role in advancing modern animal production systems in emerging markets.

Adisseo

Adisseo has established a strategic footprint in the Middle East and Africa by focusing on metabolic efficiency and animal resilience through innovative amino acid and gut health solutions. The company’s expertise in rumen-protected methionine and B-vitamins supports high-yielding dairy operations in arid regions such as the Gulf and North Africa, where maximizing output per animal is critical. Adisseo places strong emphasis on biological efficacy, developing heat-stable formulations that maintain potency in tropical supply chains. Its technical teams work closely with feed mills and veterinarians to implement antibiotic-free feeding strategies using olfactory stimulants and digestive enhancers. By investing in regional research partnerships and launching targeted educational campaigns, Adisseo builds trust among producers navigating regulatory shifts and disease pressures. The company’s focus on functional nutrition—rather than mere supplementation—positions it as a knowledge-driven partner in the evolution of commercial livestock systems across the region.

Evonik Industries AG

Evonik Animal Nutrition is a leader in precision amino acid technology, playing a transformative role in improving protein utilization and reducing environmental impact across Middle Eastern and African livestock operations. The company specializes in synthetic amino acids such as methionine, lysine, and threonine, which enable low-protein diets while maintaining growth performance—a crucial advantage in regions facing feed cost volatility and nitrogen pollution concerns. Evonik’s solutions are widely adopted in Saudi Arabia’s intensive dairy farms and Egypt’s integrated poultry complexes, where optimal nutrient balance directly influences profitability and compliance with food safety standards. Through its technical service centers and digital platforms like AMINODat, Evonik empowers formulators to tailor rations for local ingredients and species-specific needs. The company also advances sustainability by minimizing nitrogen excretion and supporting circular feed concepts. With a focus on innovation, regulatory alignment, and long-term customer engagement, Evonik reinforces its reputation as a trusted enabler of efficient, responsible animal production.

Top Strategies Used By Key Market Participants

A primary strategy employed by leading players is localized formulation development through a regional application center, allowing them to design additive blends that respond to specific climatic conditions, prevalent feedstuffs, and disease profiles across diverse agro-ecological zones. Companies are establishing technical hubs in key countries to conduct in vivo trials, validate efficacy, and adapt delivery mechanisms for high-temperature stability and extended shelf life.

Another key approach is direct technical engagement with large-scale integrators and government extension services, enabling knowledge transfer, demonstration of return on investment, and integration of additives into national agricultural development programs. This advisory model strengthens credibility and accelerates adoption beyond trial phases into mainstream production systems.

A third strategic imperative is investment in supply chain resilience and product authentication, ncluding temperature-resistant packaging, blockchain-enabled traceability, and anti-counterfeiting technologies. Given the prevalence of fake products and poor cold chain infrastructure, these measures protect brand integrity, ensure consistent performance, and build long-term trust among discerning commercial producers operating in complex, high-risk environments.

COMPETITION OVERVIEW

The competitive dynamics of the Middle East and Africa specialty feed additives market are shaped by a blend of technological sophistication, regulatory adaptation, and deep agronomic understanding. While multinational corporations lead through scientific authority and global R&D infrastructure, their success hinges not only on product quality but on the ability to navigate fragmented markets, variable logistics, and diverse farming systems. Differentiation arises from technical service depth, formulation relevance, and trust-building in environments where counterfeit products have eroded confidence in premium inputs. Regional players and importers compete on price, but struggle to match the consistency and support offered by global leaders. The phase-out of antibiotic growth promoters across multiple jurisdictions has intensified rivalry, with companies racing to offer validated alternatives such as organic acids, probiotics, and mycotoxin binders. However, true competitiveness requires more than portfolio breadth—it demands localized insight, educational outreach, and resilient distribution networks capable of preserving product integrity in extreme climates. As governments prioritize food security and sustainable intensification, the market increasingly favors those who combine chemistry with context, delivering solutions that perform reliably under real-world constraints. Ultimately, leadership in this region is determined not just by innovation, but by executional excellence across science, supply, and stakeholder engagement.

RECENT HAPPENINGS IN THE MARKET

- In March 2024, Cargill launched a regional technical training center in Cairo dedicated to optimizing feed additive use in poultry and aquaculture operations across North Africa and the Levant.

- In July 2023, Evonik expanded its partnership with a major Saudi Arabian dairy cooperative to implement customized amino acid balancing protocols aimed at improving milk protein yield in heat-stressed herds.

- In November 2024, Adisseo introduced a new line of thermo-stable vitamin premixes specifically engineered for tropical storage conditions, enhancing shelf life in West African feed mills without refrigeration.

- In January 2023, Cargill collaborated with Kenya’s Ministry of Agriculture to pilot a smallholder poultry nutrition program incorporating enzyme-supplemented feeds in peri-urban farming clusters.

- In October 2024, Evonik initiated a field validation study in Morocco’s aquaculture sector to assess the efficacy of nucleotide-enriched diets in improving survival rates of seabream fry under high-density hatchery conditions.

MARKET SEGMENTATION

The Middle East and Africa Specialty Feed Additives Market is segmented and sub-segmented into the following categories.

By Type of feed

- Vitamins

- Antioxidants

- Flavors and Sweeteners

- Minerals

- Binders

- Acidifiers

- others

By Livestock

- Aquatic animals

- Poultry

- Swine

- Ruminants

- others

By the Form of feed

- Liquid Feed

- Dry feed

By Function

- Palatability enhancement

- Mycotoxin Management

- Ingredient Preservation Digestive performance enhancement

- others

By Country

- KSA

- UAE

- Israel

- Rest of GCC countries

- South Africa

- Ethiopia

- Kenya

- Egypt

- Sudan

- rest of MEA

Frequently Asked Questions

What are specialty feed additives?

Specialty feed additives are high-value compounds added to animal feed to improve health, growth, digestion, and productivity in livestock, poultry, and aquaculture. Unlike basic nutrients, they serve targeted functions such as boosting immunity or enhancing feed efficiency.

Why is demand growing in the Middle East and Africa?

Rising meat and dairy consumption, coupled with the shift toward intensive farming, is driving the need for advanced animal nutrition solutions. Farmers are turning to additives to maximize output from limited resources and reduce disease-related losses.

What types of additives are most commonly used?

Key categories include amino acids, enzymes, probiotics, prebiotics, organic acids, and mycotoxin binders. Enzymes and probiotics are gaining popularity for improving gut health and reducing reliance on antibiotics.

How do feed additives support animal health in harsh climates?

In hot and arid regions, animals face heat stress and poor-quality forage, which affects digestion and immunity. Specialty additives help maintain nutrient absorption, balance gut flora, and strengthen resistance to environmental and disease pressures.

Are there concerns about antibiotic use in animal feed?

Yes, growing awareness of antimicrobial resistance has led to reduced reliance on antibiotic growth promoters. Many countries and producers are switching to natural alternatives like essential oils, phytogenics, and microbial supplements.

Who are the main users of specialty feed additives?

Large-scale poultry and dairy farms, commercial pig operations, and aquaculture ventures are the primary adopters. Feed mills and integrators also blend additives into commercial feed formulations for broader distribution.

How is the market affected by feed availability and cost?

Fluctuations in raw material prices—especially protein sources—make additives like synthetic amino acids more attractive, as they allow formulators to reduce overall protein content without sacrificing animal performance.

Are there regulatory frameworks for feed additives in the region?

Regulation varies widely—some countries have clear approval processes, while others lack standardized oversight. This creates challenges for quality control, but also opportunities for trusted international and regional suppliers.

What role do import and local production play?

Most specialty additives are imported from Europe, China, or the U.S., due to limited local manufacturing capacity. However, a few countries like South Africa and Egypt are beginning to develop domestic blending and packaging facilities.

What’s the future of this market in the region?

The market is expected to grow steadily, driven by population growth, urbanization, and rising demand for animal protein. Innovation, education, and better supply chains will be key to expanding access beyond large commercial farms.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com