Middle East Insurance Market Size, Share, Trends, Forecast, Research Report - Segmented By Type (General Insurance, Life Insurance), Distribution Channel, and Region (Brazil, Mexico, Argentina, Chile & Rest of Latin America) – Regional Industry 2025 to 2033

Middle East Insurance Market Size

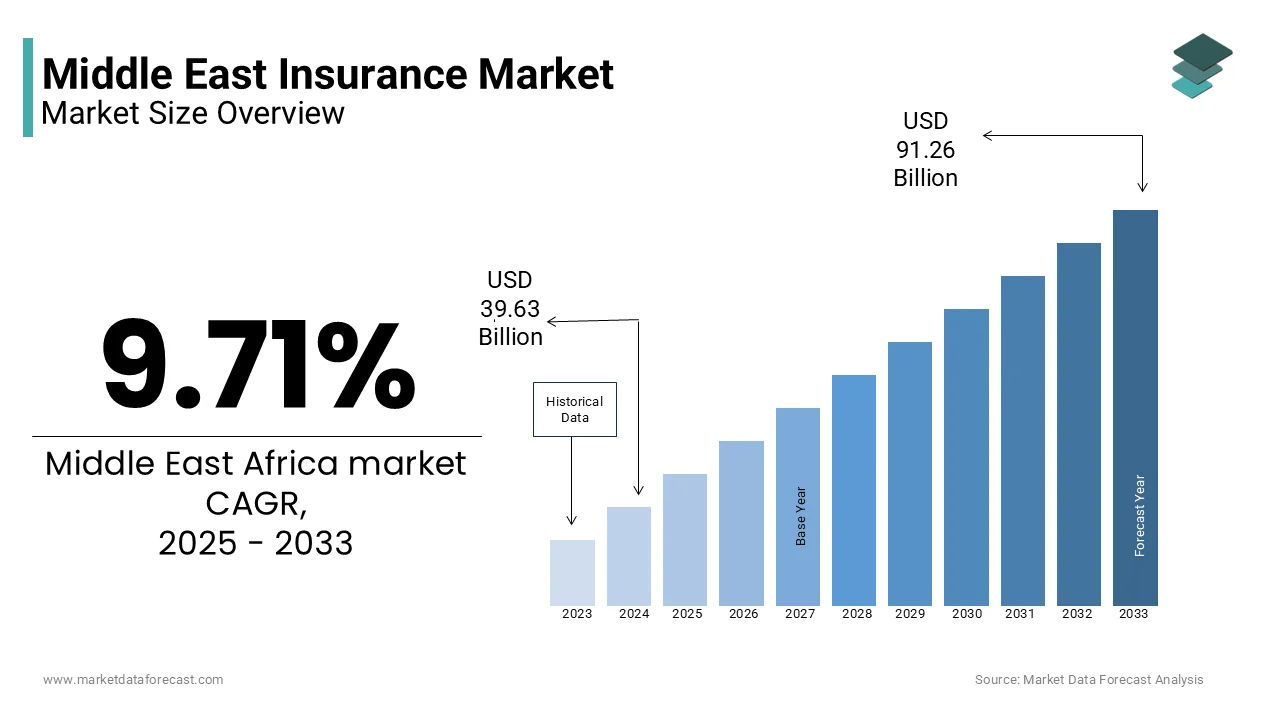

The Middle East Insurance market size was valued at USD 39.63 billion in 2024, and is expected to reach USD 91.26 billion by 2033 from USD 43.48 billion in 2025. With a growing CAGR of 9.71%.

The insurance is a risk management and financial protection services, including life, health, motor, property, and commercial insurance across countries such as Saudi Arabia, UAE, Kuwait, Qatar, Oman, Bahrain, and Iraq. This market has been undergoing transformation driven by regulatory reforms, economic diversification efforts, and increasing awareness of risk mitigation among individuals and businesses. According to the Gulf Insurance Federation (GIF), the insurance industry in the Gulf Cooperation Council (GCC) countries has seen a gradual shift from being commodity-driven to more customer-centric and digitally enabled. The region’s growing population, expanding middle class, and rising disposable incomes have contributed to the demand for personal insurance products.

MARKET DRIVERS

Regulatory Reforms and Compulsory Insurance Mandates

The implementation of regulatory reforms and mandatory insurance requirements by national authorities is driving the growth of the Middle East insurance market. Governments across the region have introduced policies that make certain types of insurance compulsory, thereby boosting market growth and enhancing financial inclusion. In the UAE, for instance, mandatory motor insurance laws have significantly increased insurance penetration. According to the Insurance Authority of the UAE, all vehicle owners are required to carry at least third-party liability coverage, a regulation that has resulted in nearly 100% compliance in motor insurance. These regulatory measures not only ensure broader risk coverage for individuals and businesses but also create a more structured and sustainable insurance ecosystem in the region.

Economic Diversification and Growth of Non-Oil Sectors

The economic diversification initiatives across the Middle East have led to the expansion of non-oil sectors such as real estate, healthcare, tourism, and manufacturing, all of which contribute to the growth of the insurance market. According to the Qatar Financial Centre Regulatory Authority (QFCRA), the number of commercial insurance policies issued annually has grown by over 10%, driven by new construction projects and expanding private enterprises. Moreover, the development of free zones and special economic areas across the GCC has attracted foreign investors, many of whom are required to obtain comprehensive insurance coverage. These economic transformations are reshaping the insurance landscape, which is making it more dynamic and responsive to evolving business needs.

MARKET RESTRAINTS

Low Insurance Penetration and Awareness

The relatively low level of insurance penetration and consumer awareness in non-mandatory insurance segments is restraining the growth of the Middle East insurance market. In countries like Iraq and Yemen, where insurance infrastructure is underdeveloped, insurance penetration remains below 1%, according to the Arab Insurance Federation (ARABINFO). Cultural perceptions and a lack of trust in insurance products also contribute to low uptake. The lack of awareness regarding the benefits of insurance among younger demographics that hinders the expansion of personal insurance products. Additionally, in some countries, the insurance sector is viewed with skepticism due to past issues with claim settlements and lack of transparency. These challenges make it difficult for insurers to build trust and expand their customer base beyond mandatory insurance categories.

Regulatory Fragmentation and Compliance Complexity

The Middle East insurance market growth is hindered with the regulatory fragmentation across countries, which complicates compliance for multinational insurers and limits market integration. In the GCC, while there have been efforts toward harmonization, differences in regulatory approaches persist. According to the Gulf Insurance Federation (GIF), insurers operating in multiple GCC countries must navigate varying capital adequacy requirements, solvency standards, and product approval processes. In Saudi Arabia, for instance, SAMA has introduced stringent corporate governance and risk management standards that require insurers to maintain higher capital reserves and adopt advanced reporting systems. In Kuwait, regulatory restrictions on foreign ownership and investment in insurance companies have limited the inflow of international capital and innovation.

MARKET OPPORTUNITIES

Digital Transformation and Insurtech Adoption

The rapid adoption of digital technologies and the emergence of insurtech startups are greatly influencing the growth of the Middle East insurance market. The increasing use of smartphones, growing internet penetration, and the rise of e-government initiatives have created a conducive environment for digital insurance solutions. In the UAE, for example, the government’s Smart Dubai initiative has encouraged the digitization of financial services, including insurance. According to the Dubai Financial Services Authority (DFSA), the number of digital insurance platforms has grown by over 40% in the last three years, offering consumers instant policy issuance, digital claims processing, and AI-driven underwriting. Moreover, the integration of telematics in motor insurance, wearables in health insurance, and blockchain for fraud detection is enhancing efficiency and customer experience.

Growth of Takaful Insurance and Islamic Finance Integration

The expansion of takaful insurance is escalating the growth of the Middle East insurance market. Takaful operates on the principles of mutual cooperation and shared responsibility, aligning with Islamic finance guidelines and offering an ethical alternative to conventional insurance. Kuwait and Bahrain have also made significant strides in integrating takaful with broader Islamic finance frameworks, with regulators introducing standardized guidelines to enhance transparency and investor confidence.

MARKET CHALLENGES

Geopolitical Risks and Political Instability

The geopolitical risks and political instability is posing significant challenge for the Middle East insurance market players. In countries such as Iraq, Yemen, and Syria, ongoing conflicts have severely disrupted insurance operations, with many insurers withdrawing from these markets due to high risk and limited profitability. According to the Arab Insurance Federation (ARABINFO), war risk insurance remains the only viable product in conflict-affected regions, limiting market diversification. For example, maritime insurance premiums spiked during the 2019 Gulf tanker attacks, as underwriters reassessed risk exposure in the region. The Insurance Authority of the UAE reported a 20% increase in marine insurance premiums following the incident. Moreover, sanctions imposed on certain countries in the region affect cross-border insurance transactions and reinsurance flows. Insurers based in the GCC face challenges in reinsuring risks associated with sanctioned entities, which is leading to higher costs and reduced coverage options.

Claims Fraud and Underwriting Complexity

The claims fraud and underwriting complexity is also hindering the growth of the Middle East insurance market. The lack of centralized fraud detection systems and inconsistent enforcement of anti-fraud measures have made it easier for fraudulent claims to go undetected. In Saudi Arabia, the Saudi Arabian Insurance Federation (SAIF) has reported rising cases of health insurance fraud, including unnecessary medical treatments and duplicate claims. Additionally, underwriting complexity is heightened by the lack of standardized data across sectors. In commercial insurance, for instance, the absence of comprehensive risk databases makes it difficult for insurers to assess creditworthiness and exposure accurately.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 9.71% |

| Segments Covered | By Type, Distribution Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israel, Rest of GCC countries and Rest of Middle East. |

| Market Leaders Profiled | Qatar Insurance Company, Sukoon Insurance, Gig Gulf, Bupa Arabia, Abu Dhabi National Insurance Company (ADNIC), Tawuniya, Orient Insurance, Oman Insurance Company, MedGulf, International Insurers/ Reinsurers Presen, and others. |

SEGMENTAL ANALYSIS

By Type Insights

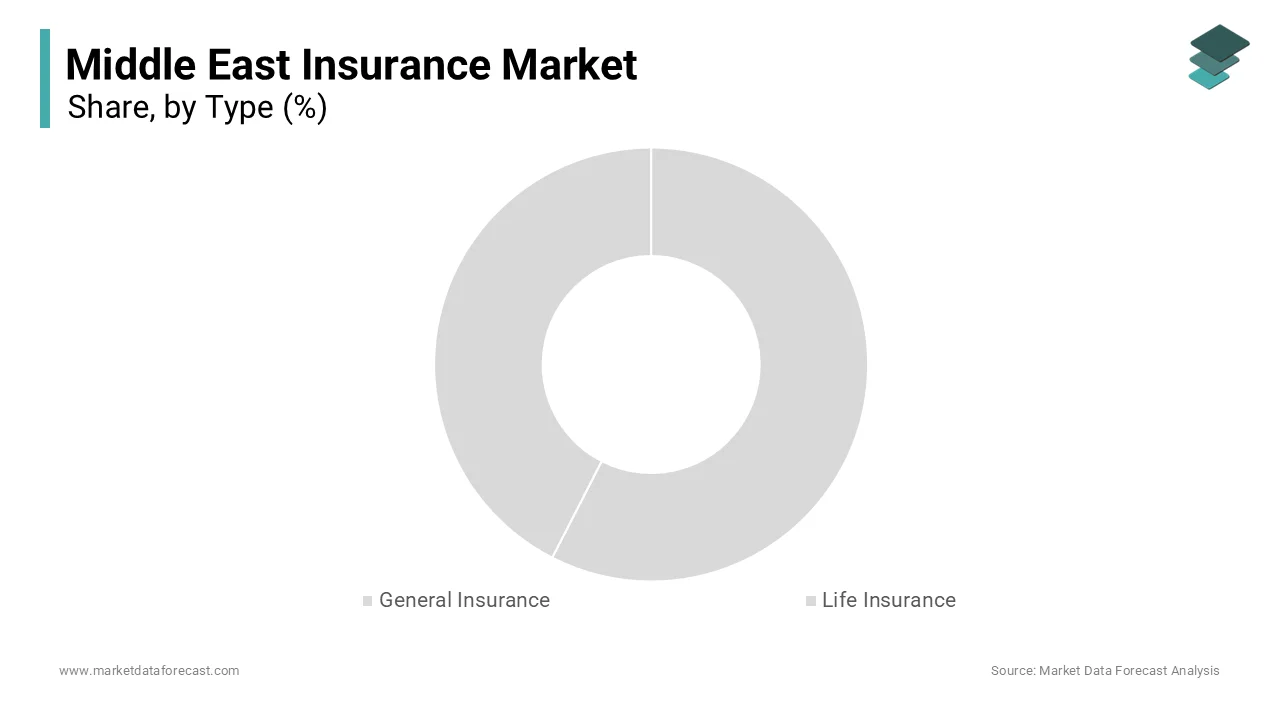

The general insurance segment was accounted in holding 58.4% of the Middle East insurance market share in 2024, with the widespread presence of mandatory insurance requirements across several categories such as motor, health, and property insurance, which are enforced by regulatory authorities in key markets like the UAE, Saudi Arabia, and Kuwait.

The legal requirement for motor insurance in most Gulf Cooperation Council (GCC) countries is additionally fuelling the growth of the segment. In the UAE, for example, the Insurance Authority mandates that all vehicle owners carry at least third-party liability coverage, ensuring near-universal adoption. Additionally, the expansion of mandatory health insurance policies has significantly boosted the general insurance segment. Moreover, the increasing number of infrastructure and industrial projects across the region has led to a rise in demand for commercial general insurance products such as property, liability, and construction insurance, further strengthening the segment’s dominance.

The Life Insurance segment is projected to grow with a CAGR of 9.2% from 2025 to 2033. In Saudi Arabia, for instance, the push under Vision 2030 to diversify the economy and promote private sector participation has led to greater emphasis on long-term savings and investment products, including life insurance. In the UAE, the growing expatriate population, which constitutes over 85% of the population in cities like Dubai, has increased demand for life insurance as part of employment and residency requirements. Additionally, the integration of takaful (Islamic insurance) models has played a key role in expanding life insurance adoption in Muslim-majority countries.

By Distribution Channel Insights

The insurers segment was accounted in holding 45.3% of the Middle East insurance market share in 2024 with the preference of consumers for direct interaction with insurance providers, particularly for mandatory insurance products such as motor and health insurance. Additionally, the rise of digital insurance platforms has empowered insurers to reach a broader customer base without relying heavily on intermediaries. In Saudi Arabia, SAMA has encouraged insurers to develop mobile apps and online portals, enabling policyholders to purchase, renew, and manage policies seamlessly. Moreover, large insurance companies in the region have invested in customer relationship management systems and AI-driven underwriting tools, enhancing the efficiency of direct sales and improving customer retention rates.

The insurance brokers and agencies segment is anticipated to register a CAGR of 8.7% from 2025 to 2033 with the increasing demand for personalized insurance solutions, growing complexity of insurance products, and the need for expert advice in risk assessment and policy selection. Additionally, the introduction of regulatory frameworks that support broker licensing and professional development has enhanced the credibility of the segment. According to the Arab Insurance Federation (ARABINFO), the number of licensed insurance brokers in the GCC has increased by 10% annually over the past five years, which is indicating a structural shift toward professionalized insurance distribution.

REGIONAL ANALYSIS

Saudi Arabia

Saudi Arabia was the top performer of the MEA insurance market by accounting for 28.3% of share in 2024 with the expansion of mandatory insurance requirements in health and motor insurance. The Council of Cooperative Health Insurance (CCHI) reports that health insurance coverage has expanded to over 90% of expatriates, with gradual inclusion of citizens. Additionally, the Saudi Arabian Monetary Authority (SAMA) has introduced regulatory reforms to improve transparency and governance in the insurance industry. Moreover, the rise of digital insurance platforms and the integration of takaful models have contributed to increased insurance adoption across both personal and commercial segments.

United Arab

United Arab Emirates was positioned second by capturing 22.3% of the MEA insurance market share in 2024. The UAE has a well-developed insurance ecosystem, supported by a strong regulatory framework, high disposable incomes, and a large expatriate population that drives demand for life and health insurance. According to the UAE Insurance Authority, mandatory motor and health insurance policies have significantly boosted insurance penetration, particularly in Dubai and Abu Dhabi. Additionally, the UAE government’s Smart Dubai initiative has encouraged the digitization of insurance services, with many insurers offering mobile-first platforms and AI-driven underwriting tools.

Israel

Israel insurance market growth is likely to be driven by the high penetration rates, advanced risk management practices, and a strong regulatory environment. Israel’s insurance market growth is likely to grow with the mandatory health and motor insurance requirements, which ensure broad coverage across the population. The Ministry of Finance reports that nearly 100% of vehicle owners have motor insurance, while the National Health Insurance Law mandates universal health coverage.

Additionally, Israel’s thriving technology sector has led to the emergence of insurance technology (insurtech) startups that are reshaping traditional insurance models. According to the Israeli Insurance Association, over 25 insurtech firms have launched in the past five years, which is offering digital insurance platforms, parametric insurance, and AI-based fraud detection systems. Moreover, the integration of telematics in motor insurance and wearable devices in health insurance has enhanced risk assessment and personalized coverage options.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Qatar Insurance Company, Sukoon Insurance, Gig Gulf, Bupa Arabia, Abu Dhabi National Insurance Company (ADNIC), Tawuniya, Orient Insurance, Oman Insurance Company, MedGulf, International Insurers/ Reinsurers Presen are the key players in the Middle East insurance market.

The Middle East insurance market is highly competitive, shaped by a mix of domestic insurers, international players, and specialized takaful providers. The market is evolving rapidly due to regulatory reforms, digital transformation, and increasing demand for risk management solutions. Domestic insurers have a strong foothold due to their understanding of local regulations and customer preferences, while global insurers bring in advanced underwriting techniques, risk modeling, and reinsurance expertise.

Competition is intensifying as insurers strive to differentiate themselves through product innovation, digital customer engagement, and superior claims management. The rise of insurtech startups is further disrupting traditional insurance models, which is pushing established players to adopt new technologies and improve service delivery. Additionally, the growing emphasis on financial inclusion and mandatory insurance policies is expanding the customer base and driving market growth.

TOP PLAYERS IN THE MARKET

Majid Al Futtaim Insurance (MAFI)

Majid Al Futtaim Insurance is a leading player in the Middle East insurance market, offering a wide range of life and general insurance products across the Gulf Cooperation Council (GCC) countries. The company has built a strong reputation for customer-centric solutions, digital innovation, and strategic partnerships with global reinsurers. MAFI plays a significant role in shaping the regional insurance landscape by integrating advanced technologies and promoting financial inclusion. Its operations contribute to the broader insurance ecosystem by setting benchmarks for service quality and digital transformation in the sector.

Saudi Insurance Company (SAICO)

Saudi Insurance Company is one of the largest and most established insurers in Saudi Arabia, providing a comprehensive portfolio of life and non-life insurance products. SAICO has been instrumental in supporting the Kingdom’s Vision 2030 initiative by expanding insurance coverage and enhancing risk awareness among individuals and businesses. The company's strong underwriting capabilities, commitment to Sharia-compliant insurance solutions, and investment in digital platforms have reinforced its dominant position. Its influence extends beyond Saudi Arabia, contributing to the development of takaful-based insurance models across the Islamic finance sector globally.

AXA Gulf

AXA Gulf is a prominent international insurer with a strong presence in the Middle East, offering a wide array of insurance products tailored to the region’s regulatory and cultural landscape. The company has been at the forefront of introducing innovative insurance solutions, including digital insurance platforms, parametric insurance, and Sharia-compliant products. AXA Gulf plays a vital role in bridging global best practices with regional market needs, enhancing the overall insurance ecosystem in the Middle East. Its strategic investments in risk management and sustainability further support the evolution of the regional insurance industry.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

Expansion of Digital Insurance Platforms

A key strategy employed by major insurers in the Middle East is the development of digital insurance platforms that offer seamless policy issuance, claims processing, and customer engagement. Companies are investing in AI-driven underwriting, mobile-first insurance apps, and chatbots to enhance user experience and improve operational efficiency.

Integration of Takaful and Islamic Insurance Models

Insurers are strengthening their takaful offerings to align with regional religious and legal frameworks. This includes the development of Sharia-compliant life and general insurance products that cater to Muslim-majority populations and support the growth of Islamic finance across the region.

Strategic Partnerships and Bancassurance Models

Insurers are forming strategic alliances with banks and financial institutions to expand their distribution networks. Bancassurance models are being leveraged to reach new customer segments, particularly in life insurance and investment-linked policies by enhancing market penetration and product diversification.

RECENT HAPPENINGS IN THE MARKET

- In February 2023, Majid Al Futtaim Insurance launched a fully digital insurance platform that allows customers to purchase, manage, and renew policies online. This initiative was aimed at enhancing customer experience and expanding digital insurance adoption in the UAE and other GCC markets.

- In July 2023, Saudi Insurance Company (SAICO) partnered with a leading fintech firm to integrate AI-driven underwriting tools into its insurance operations. This move was designed to streamline policy issuance to improve risk assessment accuracy, and reduce operational costs.

- In November 2023, AXA Gulf expanded its takaful insurance offerings by introducing a new range of Sharia-compliant life insurance products tailored for the GCC market. The launch was part of a broader strategy to strengthen its presence in the Islamic insurance segment.

- In March 2024, a major insurer in the UAE formed a strategic bancassurance alliance with a national bank to distribute insurance products through its branch network and digital banking channels. This partnership aimed to increase insurance penetration among retail and corporate customers.

- In August 2024, a leading regional insurance group acquired a local insurtech startup specializing in parametric insurance solutions. The acquisition was intended to enhance product innovation and expand digital insurance capabilities across the Middle East.

MARKET SEGMENTATION

This research report on the Middle East insurance market is segmented and sub-segmented into the following categories.

By Type

- General Insurance

- Life Insurance

By Distribution Channel

- Insurers

- Insurance Brokers and Agencies

- Banks

- Others

By Country

- KSA

- UAE

- Israel

- Rest of GCC countries and Rest of Middle East

Frequently Asked Questions

1. What are the major segments in the Middle East insurance market?

The market is mainly divided into life insurance and non-life insurance, with non-life taking the larger share.

2. Which countries dominate the Middle East insurance market?

Saudi Arabia and the UAE dominate the market, accounting for nearly 75% of total premiums.

3. What is the share of non-life insurance in the Middle East?

Non-life insurance accounts for nearly 89% of total insurance premiums in the Middle East.

4. What factors are driving insurance market growth in the Middle East?

Growth is driven by government mandates, rising health awareness, and digital adoption.

5. Is health insurance mandatory in Middle Eastern countries?

Yes, health insurance is mandatory in many countries like the UAE and Saudi Arabia.

6. Which sector holds the largest share in non-life insurance?

Motor and health insurance lead the non-life segment in terms of premium volume.

7. What role does Takaful play in the Middle East insurance market?

Takaful, or Islamic insurance, is gaining popularity, especially in GCC countries.

8. What challenges does the Middle East insurance market face?

Key challenges include low penetration in life insurance and regulatory variation across countries.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 1600

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com