- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

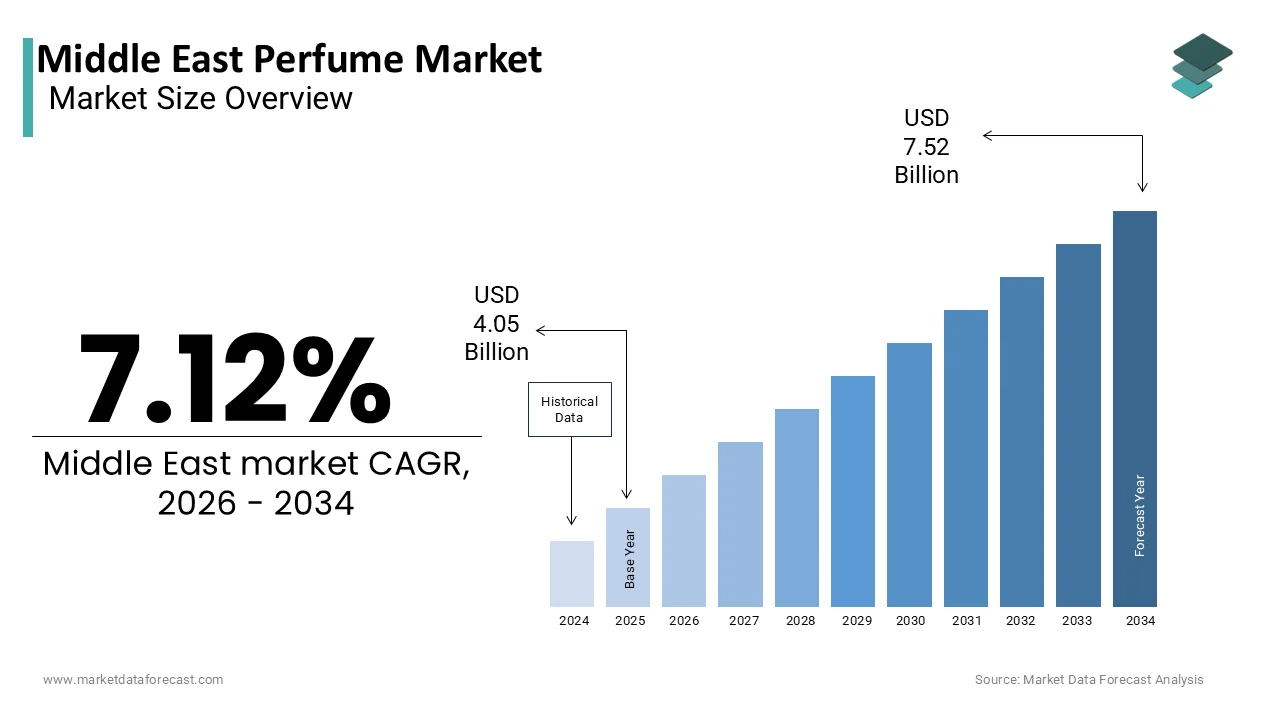

Market Size, 2025

$4.05 BnMarket Estimate, 2026

$4.34 BnMarket Forecast, 2034

$7.52 BnCAGR, 2026–2034

7.12%Middle East Perfume Market Size

The Middle East perfume market was valued at USD 4.05 billion in 2025, is estimated to reach USD 4.34 billion in 2026, and is projected to reach USD 7.52 billion by 2034, growing at a CAGR of 7.12% from 2026 to 2034.

MARKET DRIVERS

Cultural Significance and Deep-rooted Olfactory Traditions

The cultural significance of perfume in daily life and social customs is one of the primary factors driving the Middle East perfume market in the region. In many Middle Eastern societies, perfumes are not just luxury items but integral components of personal grooming, hospitality, and religious practices. Traditional attars (natural perfumes) and oud-based perfumes have been used for centuries, especially during prayers, weddings, and festive occasions. This deep-rooted tradition fuels consistent demand across generations. Additionally, the prominence of gifting perfumes during Ramadan, Eid, and other cultural celebrations contributes substantially to market growth. According to Euromonitor International data, about 35% of perfume sales were for gifts. The Middle East is one of the most loyal markets for both traditional and modern scent profiles due to the persistent influence of history and identity in perfume smells, which ensures steady growth even in the face of economic ups and downs.

Rising Disposable Incomes and Urbanization

A significant increase in disposable incomes and rapid urbanization of major nations like the United Arab Emirates, Qatar, and Kuwait are major factors driving the Middle East perfume market. These nations rank among the highest globally in per capita income by allowing consumers greater purchasing power to invest in premium and luxury goods,s including high-end perfumes. Financial capacity enables a broader segment of the population to afford niche and designer perfumes, which were once considered exclusive to elite classes. Additionally, the growth in modern retail infrastructure, re such as duty-free shops and luxury malls,lls has improved access to top global perfume brands. The growing presence of affluent millennials and Gen Z consumers, who prioritize self-expression through unique and premium scents, further amplifies the demand.

MARKET RESTRAINTS

Regulatory Challenges and Ingredient Restrictions

The strict regulations related to perfume ingredients and labeling requirementsae the significant barrier influencing the Middle East Perfume market. Several Gulf Cooperation Council (GCC) countries have implemented strict regulations on perfume formulations due to health and safety concerns, particularly around synthetic compounds and allergens. For instance, the Saudi Food and Drug Authority (SFDA) mandates compliance with specific perfume ingredient thresholds, which requires manufacturers to undergo rigorous testing and certification before products can be sold domestically. According to a report by SGS, a leading inspection and certification body, approximately 15% of imported perfumes were rejected in 2023 due to non-compliance with local chemical regulations. This creates additional costs and delays for international brands seeking market entry, discouraging smaller or independent perfume houses from operating in the region. Furthermore, the push for transparency in ingredient sourcing and environmental impact is reshaping product development strategies,s limiting the use of certain traditional elements like natural oud due to sustainability concerns.

Economic Volatility and Currency Fluctuations

Economic volatility and currency fluctuations represent a significant challenge for the Middle East perfume market in countries heavily reliant on oil exports. Many regional economies, including Saudi Arabia, Kuwait, and Bahrain, experience fluctuating shares based on global oil prices, which directly impact consumer spending power and import dynamics. According to the International Monetary Fund (IMF), the real GDP growth rate of the GCC region declined from 6.4% in 2022 to 2.3% in 2023 due to lower hydrocarbon output and global economic slowdowns. This downturn has led to cautious consumer behavior, especially regarding discretionary purchases such as premium perfumes. Additionally, currency devaluations in some Middle Eastern countries have increased the cost of imported perfumes, which make them less accessible to a broader customer base. For example, as reported by Bloomberg in early 2025, the availability of luxury items, especially perfumes, has been severely limited due to Lebanon's ongoing currency crisis.

MARKET OPPORTUNITIES

Expansion of E-commerce and Digital Perfume Retail

The fastest-growing e-commerce platforms and digital perfume retail offer the most promising opportunities for the Middle East perfume market. The region has witnessed a surge in online shopping, driven by high internet penetration, smartphone usage, and a tech-savvy youth demographic. The convenience of online shopping, coupled with personalized recommendations and virtual try-ons, has made digital platforms a preferred channel for perfume purchases, especially among millennials and Gen Z consumers. As per Euromonitor International, online perfume sales in the UAE alone grew by 22% in 2023, outpacing traditional retail channels. Moreover, local e-commerce giants such as Namshi, Ounass, and Shein have expanded their perfume offerings, and global players like Amazon and Sephora have strengthened their digital presence in the region. Social media marketing, influencer collaborations, and targeted advertising campaigns have further boosted brand visibility and consumer engagement. This digital transformation presents a significant avenue for both international and regional perfume brands to expand their reach, improve customer retention, and capitalize on the growing appetite for diverse and niche perfume options in the Middle East.

Rise of Niche and Artisanal Perfume Brands

The growing popularity of niche and artisanal perfume brands presents a substantial opportunity for the Middle East perfume market's growth. Consumers in the Gulf region, particularly in the UAE and Saudi Arabia, have shown a strong inclination toward limited-edition and bespoke perfumes, which are frequently bought from European and Middle Eastern independent perfumers. As per Euromonitor International, niche perfume sales in the Middle East grew by 14% in 2023, significantly outpacing mainstream perfume segments. The increasing number of luxury concept stores, pop-up boutiques, and curated online platforms offering niche perfumes has further fueled this trend. Additionally, the revival of traditional Middle Eastern perfumery techniques such as distillation of oud and bakhoor has attracted a new generation of perfume enthusiasts seeking authenticity and heritage-driven products.

MARKET CHALLENGES

Intense Competition and Market Saturation

The increasing competition among a rising number of local and international brands seeking consumers' attention is one of the main challenges facing the Middle East perfume market. The region has become a battleground for global perfume giants such as Chanel, Dior, and Estée Lauder, alongside established Middle Eastern brands like Ajmal, Swiss Arabian, and Rasasi. According to Euromonitor International, the number of active perfume brands in the UAE alone increased by over 25% between 2020 and 2023, leading to market saturation and diminishing differentiation among products. This overcrowding forces companies to engage in aggressive pricing strategies and extensive promotional campaigns to maintain visibility and market share. Furthermore, brand equity and customer trust are at risk from the increasing number of false and grey-market perfumes. According to a Gulf Research Center analysis from 2023, fake scents undermine legal companies and regulatory initiatives by making up about 12% of all perfume sales in the area.

Changing Consumer Preferences Toward Sustainable and Clean Beauty

A growing focus on sustainability and clean beauty is presenting a significant challenge for the Middle East perfume market, particularly for traditional perfume brands reliant on synthetic ingredients and animal-derived extracts. Consumers, especially younger populatiom are becoming more conscious about the ethical and environmental implications of their purchases. This transition is prompting brands to reformulate their offerings, adopt sustainable sourcing practices,s and enhance transparency in ingredient labelling changes that come with increased production costs and supply chain complexities. However, traditional Middle Eastern perfumes often contain oud, musk, and ambergris ingredients that face scrutiny due to conservation concerns and regulatory restrictions. For instance, the Convention on International Trade in Endangered Species (CITES) limits the trade of certain natural musks and ambergris derivatives, compelling brands to seek synthetic alternatives that may alter the authenticity of classic perfume profiles. Balancing heritage with evolving consumer expectations remains a critical challenge for the region’s perfume market.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2025 to 2034 |

| Segments Covered | By Property Type, Nature, Sales Channel, and Region |

| Various Analyses Covered | Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC; PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | KSA, UAE, Israelthe restst of GCC countries, andthe restt of the Middle East. |

| Market Leaders Profiled | Ajmal Perfume, Guccio Gucci S.p.A., LVMH Moët Hennessy Louis Vuitton SE, AL Haramain Perfumes LLC, Giorgio Armani S.p.A., Abdul Samad Al Qurashi Company, The Fragrance Kitchen, Calvin Klein, Inc., Yas the Royal Name of Perfumes, ODICT, and HB USA Holdings, Inc, and others. |

SEGMENTAL ANALYSIS

By Product Type Insights

The Eau de Parfum (EdP) segment was the largest segment and held approximately 38.7% of Middle East Perfume market share in 2025. This dominance is primarily attributed to the region’s preference for long-lasting, concentrated perfumes that align with cultural and climatic conditions. As per Euromonitor International, EdP commands a significantly higher price point compared to other perfume types making it a key share driver despite its relatively smaller volume share. The hot and arid climate across much of the Middle East necessitates perfumes with strong sillage and longevity, which EdP delivers due to its high concentration of aromatic compounds typically between 15% and 20%.

The Eau Fraîche segment is predicted to witness a CAGR of 9.6% from 2025 to 2033. Eau Fraîche is ideal for younger customers looking for light, refreshing perfumes that are appropriate for everyday wear since it has a lower percentage of perfume oils (1–3%) and is frequently alcohol-free. Additionally, rising health consciousness and a shift toward clean beauty have made Eau Fraîche an attractive option for those avoiding heavy synthetic compositions. Brands such asL’Oréale and Jo Malone have introduced alcohol-free lines specifically tailored to the Middle Eastern market. Eau Fraîche is expected to continue growing in popularity among all genders and age groups as urbanization and fluctuations in temperature fuel the demand for adaptable perfume profiles.

By Nature Insights

The synthetic perfumes segment dominated the Middle East perfume market share in 2025. The widespread use of synthetic aroma chemicals allows manufacturers to create complex, cost-effective, and highly stable scent compositions that mimic natural ingredients such as oud, jasmine, and amber. Market brands like Calvin Klein, Hugo Boss, and Davidoff collectively made up more than 30% of perfume sales in the Gulf Cooperation Council (GCC) region last year. The affordability and consistency of synthetic formulations make them accessible to a broader consumer base, especially in economies where disposable incomes vary widely. Moreover, advancements in olfactory science have enabled the recreation of rare and expensive natural notes without regulatory constraints, further boosting synthetic perfumes' appeal. The growing presence of international perfume retailers such as Sephora and Marionnaud has also contributed to the mainstream adoption of synthetic-based offerings across the region.

The natural perfumes segment is anticipated to witness the fastest CAGR of 11.3% from 2025 to 2033. This surge is largely driven by shifting consumer preferences toward organic, sustainable, and ethically sourced ingredients. Local brands such as Arabian Oud and Nabeel Perfumes have capitalized on this trend by offering pure attars, bakhoor, and oil-based perfumes derived from plant extracts and resins. Additionally, government-backed initiatives promoting halal-certified beauty products have reinforced consumer trust in natural perfume offerings. The increasing number of eco-conscious retail platforms and wellness-focused perfume boutiques further supports the rapid ascent of this segment in the Middle East.

By Sales Channel Insights

The specialty stores segment dominated the Middle East perfume market by capturing 34.5% ofthe marke share in 2025. These dedicated perfume retailers offer curated selections of both luxury and niche perfumes, providing customers with immersive shopping experiences and expert guidance. According to Euromonitor International, specialty stores continue to outperform other offline channels due to their ability to cater to discerning consumers seeking premium and exclusive products. High-end malls in cities like Dubai, Riyadh, and Doha house flagship stores of renowned brands such as Guerlain, Tom Ford, and Amouage, drawing affluent shoppers who value personalization and brand heritage. Additionally, these outlets often feature private perfume consultations, sampling stations, and limited-edition launches, reinforcing customer loyalty.

The online retailers’ segment is expected to grow with an expected CAGR of 14.2% from 2025 to 2033. The digital transformation of perfume commerce has been fueled by rising internet penetration, smartphone usage, and the convenience of doorstep delivery. In orTor to a wide range of consumer preferences, platfplatforms such ashi, Ounass, and Amazon.ae have increased the variety of perfumes in their collections to include both local craft perfumes and worldwide designer brands. As per Euromonitor International, mobile commerce now represents over 60% of all online perfume purchases in the Middle East, driven by Gen Z and millennial buyers who rely on social media influencers and virtual try-on tools before making purchases. Introduction of subscription-based perfume services and AI-powered scent recommendations has further enhanced the digital shopping experience.

REGIONAL ANALYSIS

United Arab Emirates (UAE)

The UAE outperformed other countries in the Middle East and Africa (MEA) perfume market by accounting for 28.3% of the market share in 2025. The nation's tax-free status encourages luxury spending, and seasonal increases in perfume sales are driven by major events like the Dubai Shopping Festival and Ramadan sales. Innovation and market diversity are further fueled by the rising influence of Emirati youth, who are attracted to unique and personalized smell profiles.

Saudi Arabia (KSA)

Saudi Arabia was positioned second in the MEA perfume market with a share of 24.8% in 2025, which reflects the kingdom’s deep-rooted tradition of perfume usage in both daily life and religious practices. The rise of e-commerce platforms such as Noon and Ajmal’s own digital storefronts has broadened access to premium perfumes among young urban professionals. Government support for halal and sustainable beauty products has also encouraged domestic brands to innovate while preserving heritage.

Egypt

Egypt

The Egyptian perfume market is likely to grow in the coming years. Cairo and Alexandria serve as key retail hubs, where both global and local brands compete for market share. Additionally, the revival of ancient Egyptian perfumery traditions using natural ingredients like myrrh and frankincense has attracted niche perfume enthusiasts.

Israel

Israel's perfume market growth is anticipated to drive with a technologically advanced and design-oriented player in the perfume market. The country’s well-educated, fashion-conscious population drives demand for innovative and unconventional scent profiles, which are frequently purchased from independent European and local brands. Israel’s thriving startup ecosystem has also given rise to homegrown perfume brands that leverage sustainability, gender-neutral scents, and ethical sourcing as core selling propositions. According to a report by Start-Up Nation Central, over 15 new perfume tech startups emerged in the past two years, with a focus on AI-driven scent creation and biotech-based aroma molecules. Israel continues to evolve as a unique and influential perfume market within the MEA region, with a rising focus on wellness and self-expression.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the Middle East perfume market include

Ajmal Perfume, Guccio Gucci S.p.A., LVMH Moët Hennessy Louis Vuitton SE, AL Haramain Perfumes LLC, Giorgio Armani S.p.A., Abdul Samad Al Qurashi Company, The Fragrance Kitchen, Calvin Klein, Inc., Yas the Royal Name of Perfumes, ODICT, and HB USA Holdings, Inc. (Kayali).

The competition in the Middle East perfume market is intense and multifaceted, which is shaped by the coexistence of global luxury houses and deeply rooted regional perfume brands. International players such as LVMH, Estée Lauder, and Coty leverage their brand equity, innovative formulations, and global supply chains to capture premium segments, while local champions like Ajmal, Rasasi, and Swiss Arabian maintain strong consumer loyalty through cultural relevance and traditional craftsmanship. The market is further fragmented by the emergence of niche and independent perfume houses that cater to evolving consumer preferences for exclusivity and authenticity. Retailers and distributors play a critical role in shaping brand visibility since they often create multi-brand portfolios that create additional layers of competition. The rise of e-commerce and digital engagement has intensified competition by compelling brands to continuously innovate in product development, packaging, and customer experience to stand out in a saturated marketplace.

TOP PLAYERS IN THE MARKET

LVMH (Louis Vuitton Moët Hennessy)

LVMH, a global luxury conglomerate, plays a dominant role in the Middle East perfume market through its prestigious perfume brands such as Christian Dior, Givenchy, and Maison Francis Kurkdjian. The company’s presence is amplified by its ability to blend French perfumery heritage with modern innovation, appealing to both traditional and contemporary Middle Eastern consumers. Its boutiques across Dubai, Riyadh, and Doha offer exclusive collections that cater to the region's demand for opulence and exclusivity. LVMH consistently invests in its legacy and storyline to sustain its position as a leader in high-end perfumes.

Estée Lauder Companies

Estée Lauder has established a strong foothold in the Middle East through its diverse portfolio of perfume brands, including Jo Malone London, Tom Ford Beauty, and Clinique. The company excels at adapting its product lines to suit regional scent preferences while maintaining a high standard of quality and packaging excellence. Estée Lauder continues to influence consumer behavior and shape purchasing trends across the Gulf with flagship stores in key urban centers and a growing digital footprint. Estée LauderCompanies's strategic collaborations with local retailers enhance its accessibility and brand recall.

Ajmal Perfumes

Ajmal Perfumeisre a homegrown Middle Eastern bran that holds significant sway in the regional perfume market due to its deep-rooted connection with Arabic olfactory traditions. Ajmal is known for its expertise in oud-based perfumes and natural attars that combines craftsmanship with modern retail strategies to maintain relevance among both older and younger generations. The brand operates an extensive network of retail outlets across the GCC and has expanded its reach internationally. Ajmal’s commitment to authenticity and cultural resonance makes it a formidable player in the Middle East perfume landscape.

TOP STRATEGIES USED BY KEY MARKET PLAYERS

One major strategy employed by key players in the Middle East perfume market is product localization, where international brands tailor their perfume compositions to align with regional scent preferences. This includes incorporating notes like oud, amber, and rose to appeal to local tastes while maintaining global brand identity.

Another approach is expanding through experiential retail,w herein companies establish luxury perfume counters, concept stores, and pop-ups that offer immersive sensory experiences. These spaces not only showcase products but also reinforce brand prestige and consumer engagement.

A third strategic focus is leveraging digital transformation, particularly through e-commerce expansion, social media marketing, and virtual try-on technologies. Brands are investing heavily in online platforms and influencer collaborations to connect with tech-savvy consumers and drive direct-to-consumer sales in a highly competitive market.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Maison Francis Kurkdjian opened its first standalone boutique in Riyadh to increase its regional presence and offer customers a curated selection of luxury perfumes in an immersive setting.

- In May 2025, Ajmal Perfumes launched a new line of sustainably sourced oud-based perfumes in accordance with consumers' increased interest in environmental responsibility and ethical sourcing.

- In July 2025, Sephora Middle East introduced an AI-powered perfume recommendation system on its mobile app by allowing users to discover personalized scent profiles based on mood, occasion, and preference.

- In September 2025, Estée Lauder partnered with a leading Emirati fashion influencer to develop a limited-edition perfume that blends modern design with traditional Arab perfumes.

- In November 2025, Rasasi Perfumes expanded its distribution network across Egypt and Jordan by strengthening its regional footprint and increasing accessibility to a broader consumer base.

MARKET SEGMENTATION

This research report on the Middle East perfume market is segmented and sub-segmented into the following categories.

By Product Type

- Eau de Perfume

- Eau de toilette

- Eau de Cologne

- Eau Fraiche

By Nature

- Natural

- Synthetic

By Sales Channels

- Wholesalers/Distributors

- Hypermarkets/Supermarkets

- Specialty Stores

- Multi-Brand Stores

- Independent Drug Stores

- Online Retailers

- Others

By Country

- KSA

- UAE

- Israel

- The rest of GCC countries and the rest of the Middle East