Global Military Communications Market Size, Share, Trends & Growth Forecast Report By Platform (Land, Naval, Airborne, Unmanned Vehicles), Application (Command and Control, Intelligence Surveillance and Reconnaissance, Routine Operations, Combat), System (Military Satcom System, Satellite on the Move, Satellite on the Pause, Military Radio System, Military Security System), Point of Sale (New Installation, Upgrade), and Region (North America, Europe, Asia Pacific, Latin America, Middle East and Africa) – Industry Analysis From 2025 to 2033.

Global Military Communications Market Size

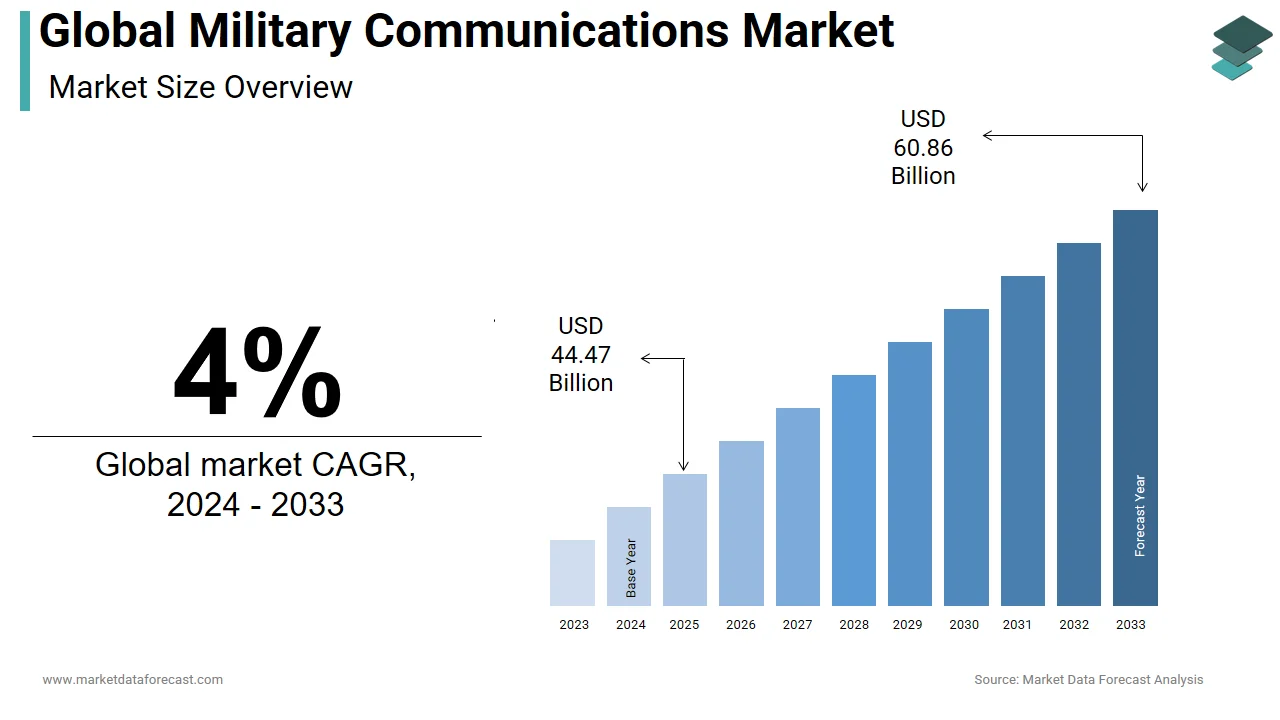

The global military communications market was worth USD 42.76 billion in 2024. The global market is expected to grow from USD 44.47 billion in 2025 to USD 60.86 billion by 2033, expanding at a compound annual growth rate of about 4% during the forecast period.

Military communication can be expressed as the transmission of information from reconnaissance units and other units in contact with the enemy. It involves the transmission of messages, orders and reports both on the ground and at sea and between headquarters and distant installations or vessels. It relates to all aspects associated with the communication of information and data by the armed forces for effective military operation, command and control. It generally depends on a large and complex network of communication equipment and protocols for transmitting information between people and regions. It plays a vital role in the security, economic and scientific capacities of several countries of the world.

The increase in the acquisition of military communication solutions due to the growing conflicts between the countries of the world, the ever-increasing concerns related to the security of military communications and the need to modernize and replace obsolete equipment are the main factors that lead the global military communications market.

MARKET DRIVERS

Growing concerns related to the security of communications is the main factor driving the global military communications market.

The growing volume of IP-based data, such as situational awareness video and remote sensor data, transmitted through standard interfaces, makes advanced data network security necessary. In addition, securing military satellites against cyber-attacks has become increasingly crucial, as terrestrial, air and space cyber resources are vulnerable to various threats. Since military communication data and network infrastructure are essential, security breaches can also jeopardize the safety of citizens. To avoid this, the defense sector adopts secure military communication solutions.

MARKET RESTRAINTS

The interoperability of communications and collaboration between different services or defense agencies is a critical problem.

Interoperability improves the ability of the forces of different nations to work effectively in a synchronized manner. Spectrum allocation, rapidly evolving technologies, the changing nature of operations and inadequate financing add to the interoperability problems in military communications. The use of similar communication equipment on a global scale may be a solution, but it is not feasible. Ongoing operations in military communications must be scalable to meet the growing demand for communications services. This is achieved through adaptive communication that ensures that the changing requirements of various operating environments are encountered. For end-to-end secure communications, secure communication interoperability protocols (SCIPs) are the next-generation standard for interoperability. Many IP-based network interoperability solutions have also been introduced, and their adoption is expected to increase during the forecast period.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 4% |

| Segments Covered | By Platform, Application, System, Point of Sale, and Region |

|

Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

|

Market Leaders Profiled | Aselsan (Turkey), BAE Systems (United Kingdom), Cobham (United Kingdom), Elbit Systems (Israel), General Dynamics (United States), Harris (United States), Inmarsat (United United), Iridium Communications (United States), Israel Aerospace Industries (Israel), Kongsberg (Norway), L3 Technologies (United States), Leonardo (Italy), Lockheed Martin (United States), Northrop Grumman (United States), Raytheon (United States), Rheinmetall (Germany) , Rockwell Collins (United States), Rolta India (India), Saab (Sweden), Systematic (Denmark), Thales (France), Viasat (United States), EID (Portugal), Kratos Defense & Security Solutions (United States) and Rohde & Schwarz (Germany) and Others. |

REGIONAL ANALYSIS

Geographically, the Asia Pacific military communications market is estimated to record the highest CAGR during the projection period, attributing to the rise in terrorist activities in countries like India, China, Pakistan, etc., along with the increased investments and adoption of new technologies in the military sector.

KEY MARKET PLAYERS

The main players in the military communications market are Aselsan (Turkey), BAE Systems (United Kingdom), Cobham (United Kingdom), Elbit Systems (Israel), General Dynamics (United States), Harris (United States), Inmarsat (United United), Iridium Communications (United States), Israel Aerospace Industries (Israel), Kongsberg (Norway), L3 Technologies (United States), Leonardo (Italy), Lockheed Martin (United States), Northrop Grumman (United States), Raytheon (United States), Rheinmetall (Germany) , Rockwell Collins (United States), Rolta India (India), Saab (Sweden), Systematic (Denmark), Thales (France), Viasat (United States), EID (Portugal), Kratos Defense & Security Solutions (United States) and Rohde & Schwarz (Germany).

RECENT MARKET HAPPENINGS

- In 2024, the U.S. Air Force announced a USD 624 million contract with Raytheon Technologies to manufacture satellite communication terminals that are resilient to nuclear effects.

MARKET SEGMENTATION

This research report on the global military communications market has been segmented and sub-segmented into the following categories.

By Platform

-

Land

-

Command and Control / Ground Stations

-

Armored Vehicles

-

Combat Vehicles

-

Combat Support Vehicles

-

Soldiers

-

-

Naval

-

Ships

-

Destroyers

-

Frigates

-

Corvettes

-

Amphibious Vehicles

-

Survey Vessels

-

Patrol & Mine Countermeasure Vessels

-

Offshore Support Vessels (OSVs)

-

Submarines

-

-

Airborne

-

Fixed Wing

-

Fighter Aircraft

-

Transport Aircraft

-

Special Mission Aircraft

-

-

Rotary Wing

-

Attack Helicopters

-

Maritime Helicopters

-

Multirole Helicopters

-

-

-

Unmanned Vehicles

-

Unmanned Aerial Vehicles (UAVs)

-

Unmanned Ground Vehicles (UGVs)

-

Unmanned Underwater Vehicles (UUVs)

-

By Application

- Command and Control

- Intelligence, Surveillance, and Reconnaissance (ISR)

- Routine Operations

- Combat

By System

-

Military Satcom System

-

Satellite on the Move

-

Satellite on the Pause

-

Military Radio System

-

Analog Radio System

-

Digital Radio System

-

-

Military Security System

-

Data Encryption System

-

Communication Management System

-

By Point of Sale

- New Installation

- Upgrade

By Region

- North America

- Europe

- APAC

- Middle East and Africa

- Latin America

Frequently Asked Questions

What role does satellite communication play in the global military communications market?

Satellite communication is pivotal in the military communications landscape, offering wide coverage, mobility, and resilience against disruptions. It enables secure and real-time data transmission for various military applications such as command and control, intelligence, surveillance, and reconnaissance (ISR).

How does the integration of Artificial Intelligence (AI) impact military communication systems?

The integration of AI technologies enhances military communication systems by enabling intelligent data analysis, predictive maintenance, automated decision-making, and adaptive networking capabilities. This leads to improved operational efficiency, reduced response times, and enhanced situational awareness on the battlefield.

How does the adoption of 5G technology impact military communication capabilities?

The adoption of 5G technology enhances military communication capabilities by offering higher data rates, lower latency, increased network capacity, and support for a massive number of connected devices. It enables the deployment of bandwidth-intensive applications and facilitates the implementation of network-centric warfare concepts.

How does the growing emphasis on network-centric warfare influence the demand for advanced military communication solutions?

The shift towards network-centric warfare emphasizes the need for interconnected and information-sharing military platforms, driving the demand for advanced communication solutions that can support seamless connectivity, data fusion, and collaborative decision-making among diverse military assets and units.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com