Global Molded Plastics Market Research Report Segmented By Type (PE, PP, PVC, PET, PS, and PU), Application (Packaging, Automotive & Transportation, Construction & Infrastructure, Electronics & Electrical, Pharmaceutical and Agriculture) - And Region (North America, Europe, Asia Pacific, Latin America, Middle east and Africa), 2026 to 2034

Global Molded Plastics Market Size

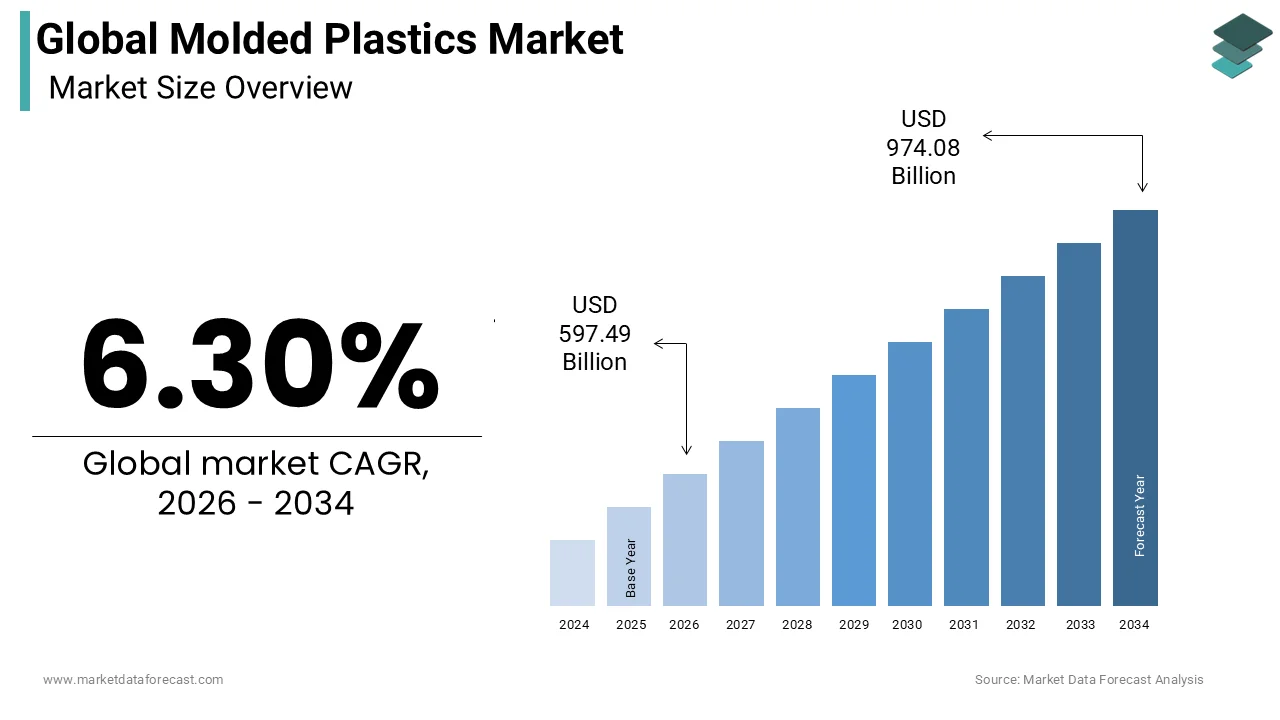

The global molded plastics market size was valued at USD 562.08 billion in 2025 and is predicted to be worth USD 974.08 billion by 2034, from USD 597.49 billion in 2026 and grow at a CAGR of 6.30% from 2026 to 2034.

Molded plastics are a diverse array of components fabricated by forcing molten polymer resins into precisely engineered molds under controlled temperature and pressure conditions. Key processes include injection molding for high-precision parts, blow molding for hollow containers, compression molding for thermosets, and rotational molding for large seamless structures. These methods enable the replication of intricate designs at high volumes with minimal post-processing, making them foundational to modern industrial manufacturing across sectors ranging from medical devices to automotive interiors. The scale and impact of molded plastics are deeply intertwined with global resource use and waste challenges. As per the International Energy Agency, the plastics sector consumes roughly 6% of the world’s oil and could absorb up to 20% of global oil supply by 2050 if fossil-based production continues unabated. Compounding this pressure, the World Health Organization estimates that more than 11 million metric tons of plastic enter marine environments yearly, much of it originating from poorly managed post-consumer waste streams. These realities are driving a paradigm shift wherein molded plastics are increasingly evaluated not only for performance and cost but also for end-of-life recyclability, material origin, and compatibility with circular systems—prompting adoption of bio-based polymers designed for disassembly and integration with mechanical or chemical recycling infrastructure.

MARKET DRIVERS

Lightweighting in Automotive and Aerospace Industries to Meet Fuel Efficiency Standards

The demand for molded plastics is significantly propelled by the automotive and aerospace sectors’ strategic shift toward lightweight materials to comply with stringent fuel economy and emissions regulations. The lightweighting in the automotive and aerospace industries to meet fuel efficiency standards is a major factor prompting the growth of the molded plastics market. The new light-duty vehicles achieve an average fleet fuel economy of 49 miles per gallon by 2026, accelerating the adoption of injection-molded polyamides, polycarbons, and long-fiber reinforced thermoplastics for structural and semi-structural applications. In aerospace, the European Aviation Safety Agency reports that modern aircraft, such as the Airbus A350, utilize over 52% composite and high-performance molded plastic content by weight to lower operational emissions. A 2023 study by the Oak Ridge National Laboratory found that replacing metal brackets, ducts, and interior panels with molded thermoplastics reduced vehicle mass by up to 50% in targeted subsystems. Furthermore, the International Council on Clean Transportation estimates that global vehicle lightweighting efforts could avoid 1.2 billion metric tons of carbon dioxide emissions by 2035.

Rising Demand for Single-Use Medical Devices Requiring Precision and Sterility

The healthcare sector’s expanding reliance on disposable diagnostic and therapeutic devices is additionally prompting the growth of the molded plastics market. These applications demand extreme dimensional accuracy, biocompatibility, and compatibility with sterilization methods, including gamma radiation and ethylene oxide requirements that only advanced molding processes can consistently meet. As per the United States Food and Drug Administration, many of these items are classified as Class II medical devices, mandating strict validation of molding parameters to ensure patient safety. A 2023 report from the Centers for Disease Control and Prevention noted that single-use devices reduce hospital-acquired infection rates compared to reprocessed alternatives, reinforcing their clinical necessity. Additionally, the aging global population intensifies demand. The United Nations projects that by 2030, one in six people worldwide will be over 60 years old, driving the need for chronic disease management tools like insulin pens and inhalers, which rely on micro-molded plastic assemblies. Companies, such as Medtronic and Becton Dickinson, increasingly partner with specialized molders capable of clean room production and traceable lot control, underscoring how regulatory rigor and demographic trends converge to sustain robust demand for medical-grade molded plastics.

MARKET RESTRAINTS

Escalating Regulatory Pressure on Single-Use Plastics and Extended Producer Responsibility

The stringent global regulations targeting single-use plastics and mandating extended producer responsibility in packaging and disposable consumer goods are hampering the growth of the molded plastics market. The European Union’s Single Use Plastics Directive bans specific molded items, such as cutlery plates and stirrers, and requires producers to cover waste management and cleanup costs for others. According to the European Commission, this directive affects over 70% of marine litter items and has prompted member states to implement national levies on non-recyclable plastic packaging. In the United States, the Environmental Protection Agency launched the National Recycling Strategy in 2021, which includes design standards that discourage complex multi-material molded packaging. India’s Plastic Waste Management Amendment Rules 2022 prohibit 19 categories of single-use plastic products, including injection molded cups and trays, with enforcement beginning in 2023. As per the survey, 127 countries have now adopted some form of regulation on single-use plastics, with 66 imposing outright bans or restrictions. These measures directly reduce demand for conventional molded items and increase compliance costs for manufacturers who must redesign products for recyclability or shift to alternative materials.

Volatility in Feedstock Prices Linked to Fossil Fuel Markets

The cost instability due to its heavy reliance on petroleum-derived resins, whose prices fluctuate with crude oil and natural gas, is additionally hampering the growth of the molded plastics market. According to the International Energy Agency, over 99% of primary plastic feedstocks are sourced from fossil fuels, making the sector highly vulnerable to geopolitical and macroeconomic shocks. This volatility complicates long-term pricing and procurement strategies for molders, especially small and medium enterprises that lack hedging capabilities. European processors cited raw material cost unpredictability as their top operational challenge. Although, bio-based alternatives exist, they account for less than 1% of total plastic production, where the United Nations and remain significantly more expensive.

MARKET OPPORTUNITIES

Integration of Recycled and Bio-Based Resins into High-Performance Molding Applications

The incorporation of certified recycled and bio-based polymers into technically demanding applications previously dominated by virgin fossil-based resins is significantly promoting new opportunities for the growth of the molded plastics market. Technological advances have enabled mechanical recycling streams to meet the stringent performance that recycled polypropylene now achieves, 90% of virgin material tensile strength, making it viable for under-the-hood automotive components. In parallel, bio-based polymers, such as polyethylene furanoate derived from plant sugars, are gaining traction with the United States Department of Agriculture certifying over 50 new bio-based plastic grades in 2023 alone. The International Energy Agency estimates that scaling advanced recycling and bio feedstocks could reduce the plastics sector’s carbon footprint by up to 50% by 2040.

Adoption of Digital Twin and AI-Driven Process Optimization in Molding Operations

The deployment of digital twin technology and artificial intelligence in molding facilities to enhance precision, reduce waste, and accelerate time is rapidly boosting the growth of the molded plastics market. Manufacturers can simulate material flow cooling rates and warpage before producing a single part, thereby minimizing trial runs and scrap by creating virtual replicas of physical molding systems. According to the Fraunhofer Institute for Production Technology, real-time AI algorithms analyzing cavity pressure, temperature, and cycle data have reduced defect rates by up to 35% in high-volume injection molding. Furthermore, cloud-based platforms now enable remote monitoring and parameter adjustment across global production sites, ensuring consistency in multi-location manufacturing. The digital molding workflows cut new product introduction timelines by 30% while improving material utilization by 12% through optimized gate and runner design. The equipment makers like Engel and KraussMaffei are embedding sensors and analytics directly into presses, creating closed-loop systems that self-correct for viscosity shifts or mold-wear. This emergence of data science and polymer processing not only boosts operational efficiency but also enables the production of micro precision components for electric vehicles and wearable medical devices, where tolerances are measured in microns and reliability is non-negotiable.

MARKET CHALLENGES

Complexity in Recycling Multi-Material and Additive-Laden Molded Components

The inherent difficulty in recycling products composed of multi-material structures or compounded with performance additives, which dominate high-value applications, is a challenge for the growth of the molded plastics market. Many molded parts, such as automotive dashboards or electronic housings, combine polymers with metals, glass, or dissimilar plastics bonded through overmolding or insert molding, making mechanical separation economically unviable. According to the Organisation for Economic Co-operation and Development, less than 9% of all plastic waste globally is effectively recycled, with multi-layer and composite items being primary contributors to this low rate. Furthermore, additives like flame retardants, colorants, and impact modifiers often degrade polymer quality during reprocessing. Over 4000 chemical substances are used in plastic formulations, many of which hinder recyclability or pose toxicity risks in secondary loops. A 2023 study found that only 22% of post-consumer engineering plastics from electronics could be mechanically recycled into equivalent-grade material due to additive contamination. Even advanced recycling methods like pyrolysis struggle with halogenated flame retardants, which generate corrosive byproducts.

Skilled Labor Shortage and Knowledge Gaps in Advanced Molding Technologies

The molded plastics industry is increasingly constrained by a shortage of skilled technicians and engineers capable of operating and optimizing next-generation molding systems. Modern injection and blow molding machines integrate robotics in mold sensing, closed-loop control, and real-time analytics, requiring cross-disciplinary expertise in polymer science, automation, and data interpretation. A 2023 survey by the Society of Plastics Engineers revealed that 68% of North American molders cite difficulty in hiring personnel qualified to manage micro molding or multi-component systems. In Germany, the Federal Institute for Vocational Education and Training estimates a shortfall of over 15000 skilled plastics technicians by 2026 as digitalization outpaces curriculum development. This gap impedes the adoption of high-precision technologies needed for medical and electronics applications, where tolerances below 10 microns are standard. Moreover, the complexity of processing new materials such as bio-based resins or recycled blends demands a deep understanding of rheology and thermal degradation behavior.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 6.30% |

| Segments Covered | By Type, Application, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | China Petroleum Corporation, Solvay S.A., Eastman Chemical Company, Formosa Plastics Group (FPG), Chevron Corporation, Versalis, BASF SE, Hanwha Group, Reliance Industries, Westlake Chemical, Haldia Petrochemicals, AGC Chemicals, Chemours Company |

SEGMENTAL ANALYSIS

By Type Insights

The polypropylene segment was the largest by holding 29.3% of the molded plastics market share in 2025, with its exceptional balance of mechanical strength, chemical resistance, thermal stability, and cost efficiency, which makes it suitable for an expansive range of applications from automotive bumpers and battery cases to medical syringes and food containers. The United States Food and Drug Administration has long approved polypropylene for direct food contact and repeated sterilization cycles, enabling its widespread use in reusable and single-use healthcare products. Furthermore, its compatibility with both injection and blow molding processes allows manufacturers to produce everything from thin-walled caps to large structural panels on the same resin platform.

The polyurethane segment is likely to grow at the fastest CAGR of 6.8% from 2026 to 2034, with its unmatched versatility in formulation, which enables the production of rigid foams for insulation, flexible foams for seating, and high-density solid parts for industrial wheels and medical devices through reaction injection molding. In the automotive industry, polyurethane molded components are critical for electric vehicle battery enclosures due to their impact absorption, flame retardancy, and dimensional stability under thermal cycling, as validated by the Society of Automotive Engineers. Additionally, the healthcare sector increasingly relies on cast polyurethane for catheter wound dressings and prosthetic liners owing to its biocompatibility and abrasion resistance. A 2023 study confirmed that bio-based polyols now constitute over 20% of new polyurethane formulations in Europe, reducing reliance on petrochemical feedstocks.

By Application Insights

The packaging segment was the largest by occupying 36.4% of the molded plastics market share in 2025, with the global reliance on molded plastic containers, closures, trays, and blister packs for food, beverage, pharmaceutical, and consumer goods due to their lightweight nature, barrier properties, and cost-effective mass production. Injection-molded polypropylene caps and polyethylene terephthalate bottles dominate beverage packaging, with the latter accounting for over 500 billion units produced annually worldwide. The United Nations Food and Agriculture Organization estimates that proper plastic packaging reduces food spoilage by up to 20% in developed economies by extending shelf life and preventing contamination. Additionally, the rise of e-commerce has intensified demand for protective molded inserts and cushioning components, with the World Bank noting that global parcel volumes exceeded 131 billion in 2022, requiring durable yet lightweight solutions.

The electronics and electrical segment is expected to grow at the fastest CAGR of 7.4% from 2026 to 2034, with the proliferation of consumer electronics, electric vehicles, and renewable energy infrastructure, all of which require high-performance molded components with precise electrical insulation, thermal management, and flame retardancy. The global production of smartphones alone exceeded 1.2 billion units in 2023, with each device containing dozens of injection-molded parts, including connectors, housing, and antenna brackets made from liquid crystal polymer or polybutylene terephthalate. In the electric vehicle sector, the International Energy Agency reports that many EVs were sold in 2023, necessitating molded battery housings, busbars, and charging components that withstand high voltage and thermal stress. Furthermore, the rollout of 5G networks and data centers demands low dielectric loss polymers for waveguides and server components.

REGIONAL ANALYSIS

Asia Pacific Molded Plastics Market Analysis

Asia Pacific was the largest contributor in the global molded plastics market by capturing 38.3% of the market share in 2025. China was the dominant share of the world’s foremost manufacturing hub, producing over 31% of global plastic goods, with injection-molded components integral to its electronics, automotive, and packaging sectors. Meanwhile, Southeast Asia, like Vietnam and Thailand, has become a preferred destination for automotive and appliance assembly, with Thailand producing over 1.8 million vehicles annually. Urbanization further amplifies demand. The United Nations projects that Asia’s urban population will grow by 600 million by 2035, increasing the consumption of packaged foods and disposable medical devices.

North America Molded Plastics Market Analysis

North America was positioned second by holding 24.3% of the global molded plastics market share in 2025, with the United States serving as the primary contributor through its advanced automotive, aerospace, and medical device industries. The United States produced over 10 million motor vehicles in 2023, according to the Bureau of Transportation Statistics, with each containing an average of 151 kilograms of plastic components, many of them injection molded under the hood or in interiors. Regulatory evolution is also shaping the landscape. The Environmental Protection Agency’s 2025 National Recycling Strategy mandates design for recyclability, pushing brand owners like Procter and Gamble and Johnson and Johnson to adopt mono-material molded packaging.

Europe Molded Plastics Market Analysis

Europe's molded plastics market was ranked second by capturing 28.3% of the market share in 2025, with a strong emphasis on regulatory compliance, material traceability, and circular design. The European Union’s REACH and RoHS directives strictly govern additives in molded components, ensuring safety in electronics and children’s products. Simultaneously, the Ecodesign for Sustainable Products Regulation, set to take full effect in 2027, will require all molded plastic goods placed on the EU market to be recyclable and contain a minimum recycled content. France and the Netherlands are pioneering digital product passports that track resin origin and molding parameters across supply chains.

Latin America Molded Plastics Market Analysis

Latin America's molded plastics market growth is likely to grow, with Brazil and Mexico driving demand through automotive manufacturing and agricultural packaging. Brazil and Mexico are prompting new opportunities for the growth of the molded plastics market. However, recycling infrastructure remains limited. The World Bank estimates that only 12% of plastic waste in the region is formally collected.

Middle East and Africa Molded Plastics Market Analysis

The Middle East and Africa molded plastics market growth is likely to grow with activity concentrated in South Africa, Saudi Arabia, and Egypt. South Africa leads sub-Saharan Africa with a mature plastics processing sector producing over 1.8 million metric tons of molded goods annually. Saudi Arabia is aggressively diversifying beyond oil through its Vision 2030 program, which includes 1.2 billion US dollars allocated to petrochemical downstream industries, including high-value molding for medical and construction applications. Nevertheless, strategic investments are emerging. The United Arab Emirates launched a circular economy policy in 2021, mandating recyclable design for all packaging by 2026, while Nigeria’s National Plastic Action Partnership is piloting collection hubs near major cities.

COMPETITION OVERVIEW

The competition in the molded plastics market is highly dynamic, featuring a mix of integrated petrochemical giants, specialty compounders, and regional resin producers. Global players leverage scale, technology, and sustainability credentials to dominate high-value segments such as automotive and medical, while regional firms compete on cost and proximity in packaging and construction. Differentiation increasingly hinges on material innovation, particularly in circular polymers and high-performance engineering plastics. Intense rivalry exists in qualifying resins for electric vehicle and electronics applications, where thermal, electrical, and flame-retardant properties are critical. Regulatory pressures on single-use plastics have intensified focus on design for recyclability, pushing suppliers to co-develop mono-material solutions with converters. The market also sees vertical integration as compounders acquire recycling assets and molders invest in material science capabilities.

KEY MARKET PLAYERS

A few major players of the global molded plastics market include

- China Petroleum Corporation (China)

- Solvay S.A. (Belgium)

- Eastman Chemical Company (U.S.)

- Formosa Plastics Group (FPG)

- Chevron Corporation (U.S.)

- Versalis (Italy)

- BASF SE (Germany)

- Hanwha Group (South Korea)

- Reliance Industries (India)

- Westlake Chemical (Texas)

- Haldia Petrochemicals (India)

- AGC Chemicals (Exton)

- Chemours Company (U.S.)

Top Strategies Used by the Key Market Participants

Key players in the molded plastics market prioritize the development of sustainable polymer grades, including mechanically recycled and bio-based resins, to align with global circular economy mandates. They invest in application engineering support to help molders optimize processing parameters for new materials. Strategic collaborations with brand owners and recyclers ensure closed-loop feedstock availability. Companies also expand production capacity in high-growth regions such as Asia and North America to serve local manufacturing clusters. Additionally, they enhance digital tools for material selection simulation and traceability to accelerate product development and compliance.

Leading Players in the Market

LyondellBasell

LyondellBasell is a global leader in polymer production and a key enabler of the molded plastics market through its extensive portfolio of polyolefins, including advanced grades of polypropylene and polyethylene tailored for injection and blow molding. The company supplies resins to automotive packaging and healthcare sectors worldwide. Recently, LyondellBasell expanded its Circulen portfolio of circular and bio-based polymers and launched certified recycled polypropylene grades compatible with high precision molding processes to meet growing demand for sustainable materials in Europe and North America.

SABIC

SABIC plays a pivotal role in the molded plastics ecosystem by developing high-performance engineering thermoplastics such as polycarbonate, polyamide, and polyetherimide used in electronics, automotive, and medical applications. Its LNP and ULTEM brands are widely specified for flame-retardant and heat-resistant components. In recent years, SABIC has accelerated its circular initiatives by scaling certified renewable and mechanically recycled resins and collaborating with molders to validate processing parameters for closed-loop applications in electric vehicles and consumer electronics.

BASF

BASF contributes significantly through its Ultramid polyamide and Ultrason polysulfone families, which are engineered for demanding molded parts requiring strength, thermal stability, and chemical resistance. The company serves aerospace, industrial, and healthcare markets with specialty compounds that meet stringent regulatory standards. BASF has recently enhanced its ChemCycling project to convert plastic waste into pyrolysis oil feedstock for new molding resins and partnered with injection molding machine makers to optimize the processing of these circular materials in high-tolerance applications.

MARKET SEGMENTATION

This research report on the global molded plastics market has been segmented and sub-segmented based on type, application, and region.

By Type

- PE

- PP

- PVC

- PET

- PS

- PU

By Application

- Packaging

- Automotive & Transportation

- Construction & Infrastructure

- Electronics & Electrical

- Pharmaceutical

- Agriculture

By Region

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

Frequently Asked Questions

1. What factors are driving the growth of the molded plastics market?

Increasing demand from automotive, packaging, construction, healthcare, and consumer goods industries is driving market growth.

2. What are the major types of molded plastics?

Major types include injection molded plastics, blow molded plastics, compression molded plastics, and rotational molded plastics.

3. Who are the key players in the molded plastics market?

Leading companies include Berry Global, BASF, Dow, and LyondellBasell.

4. Why is injection molding widely used in the plastics industry?

Injection molding offers high production efficiency, precision, low waste generation, and cost-effective manufacturing for large-scale production.

5. How does the automotive industry influence the molded plastics market?

Automotive manufacturers use molded plastics to reduce vehicle weight, improve fuel efficiency, and enhance design flexibility.

6. What role does the packaging industry play in market growth?

The packaging sector extensively uses molded plastics for bottles, containers, caps, and flexible packaging solutions.

7. What are the major challenges in the molded plastics market?

Environmental concerns, plastic waste regulations, fluctuating raw material prices, and recycling challenges are major issues.

8. Which applications dominate the molded plastics market?

Packaging, automotive, electronics, healthcare, construction, and consumer goods are major application segments.

9. How is technology improving molded plastics manufacturing?

Advanced automation, 3D printing integration, and precision molding technologies improve production efficiency and product quality.

10. What are the future opportunities in the molded plastics market?

Growth opportunities include bio-based plastics, lightweight automotive components, smart packaging, and advanced medical applications.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com