- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

Market Size, 2025

$93.05 BnMarket Estimate, 2026

$104.03 BnMarket Forecast, 2034

$253.92 BnCAGR, 2026–2034

11.8%Executive Summary: North America Biomarkers Market

- Market Scope: Regional North American biomarkers market analysis covering product categories, biomarker types, country leadership frameworks, and precision medicine adoption metrics.

- Market Valuation: Valued at USD 93.05 billion in 2025, estimated at USD 104.03 billion in 2026, and projected to reach USD 253.92 billion by 2034, registering a CAGR of 11.80% from 2026 to 2034.

- Primary Growth Drivers: Rising incidence of chronic diseases, expanding precision medicine initiatives, increasing adoption of companion diagnostics, advancements in genomics and proteomics, AI-enabled biomarker discovery, and growing investments in personalized healthcare.

Key Market Segment Metrics (2026–2034)

| Category | Leading Segment (2025 Position) | Fastest-Growing Segment |

|---|---|---|

| By Product | Consumables segment (held the largest market share of 45.4% in 2025 due to reagents, assay kits, and tools) | Software segment (projected to register the fastest growth with a CAGR of 15.7% due to AI, machine learning, and analytics) |

| By Biomarker Type | Efficacy biomarkers (accounted for the largest share of 39.9% in 2025 for personalized therapies) | Advanced companion diagnostic and prognostic biomarker variants |

| By Technology & Innovation | Genomics, proteomics, and standard clinical assays | AI-enabled biomarker discovery, liquid biopsy technologies, and digital health analytics platforms |

| By Region / Country | United States (dominates owing to advanced healthcare infrastructure and strong biotech ecosystem) | Canada (steady growth supported by expanding healthcare investments and biomarker research initiatives) |

Major Market Players & Market Structure

Market Structure: Competitive North American life sciences and diagnostics landscape characterized by investments in biomarker discovery, AI-enabled diagnostic platforms, companion diagnostics, strategic collaborations, and genomic research capabilities.

Key Companies: Bio-Rad Laboratories, Qiagen N.V., Enzo Biochem, and PerkinElmer, Inc.

North America Biomarkers Market Size

The North America Biomarkers Market is projected to grow from USD 93.05 billion in 2025 to USD 104.03 billion in 2026 and reach USD 253.92 billion by 2034, registering a CAGR of 11.80% from 2026 to 2034.

The biomarkers are biological indicators used in the detection, diagnosis, monitoring, and treatment of diseases. These biomarkers are integral to modern medicine, particularly in oncology, neurology, cardiology, and infectious disease management. Biomarkers are becoming important tools for enabling precision medicine, predictive analytics, and drug development in the US and Canada due to developments in genomics, proteomics, and digital diagnostics. According to the National Institutes of Health (NIH), over 150,000 research studies involving biomarkers were registered in the U.S. between 2020 and 2023. Biomarkers are essential for accurate diagnostic and prognostic tools, which are in high demand due to the rising prevalence of chronic illnesses including cancer, diabetes, and Alzheimer's.

MARKET DRIVERS

Rising Incidence of Chronic Diseases

The rising incidence of chronic illnesses including cancer, heart disease, and neurological disorders is one of the main factors driving the North America biomarkers market. According to the Centers for Disease Control and Prevention (CDC), chronic diseases account for approximately 70% of all deaths in the United States, with cancer alone affecting nearly 2 million Americans annually. Early and precise diagnosis is necessary due to the growing health burden, and biomarkers provide significant benefit in this area. For example, according to the American Cancer Society, more than 90% of patients with advanced-stage lung cancer do not live for more than five years, showing the critical need for early diagnosis using biomarker-based testing. In response, healthcare providers and researchers are increasingly adopting biomarkers to detect disease progression before symptoms manifest. In 2023, the FDA approved several new liquid biopsy tests designed to detect tumor-specific biomarkers through blood samples, providing a non-invasive alternative to traditional tissue biopsies.

Expansion of Precision Medicine Initiatives

Implementing precision medicine methods that personalize therapies to individual patient profiles is a major factor driving the North American biomarkers market. According to the National Institutes of Health's (NIH) All of Us Research Program, since its start in 2018, more than one million people have enrolled, providing genetic, environmental, and lifestyle information for the creation of tailored treatments. Precision medicine relies heavily on biomarkers to determine which therapies will be most effective for specific patients. For instance, according to a 2023 report by the U.S. Department of Health and Human Services, around 60% of newly approved cancer medications came with a companion diagnostic test based on biomarker analysis that guarantees personalized therapy delivery. Canada has also made significant strides in this domain. According to a Canadian Partnership Against Cancer (CPAC) study, over 70% of cancer patients in a few trial programs in British Columbia and Ontario had better results with personalized treatment plans that included biomarker testing. Moreover, major pharmaceutical firms like Roche, Merck, and AstraZeneca are integrating biomarker assessments into their drug development pipelines.

MARKET RESTRAINTS

High Cost of Biomarker Development and Validation

The high cost associated with biomarker discovery, development, and clinical validation is a significant challenge for the North America Biomarkers Market. The financial burden is particularly pronounced for small and mid-sized biotech firms that lack the resources of large pharmaceutical conglomerates. According to the Biotechnology Innovation Organization (BIO), only 15% of biomarker candidates identified in preclinical studies between 2020 and 2023 progressed to full clinical validation due to funding limitations. Moreover, the process involves multi-phase clinical trials, longitudinal studies, and extensive data analysis, all of which contribute to prolonged duration and increased costs. According to the Fred Hutchinson Cancer Research Center, these logistical and financial barriers prevent less than 10% of new biomarkers discovered in academic research from being commercially available. Additionally, reimbursement challenges persist despite technological advances. As per the Centers for Medicare & Medicaid Services (CMS) report, less than 30% of newly developed biomarker tests receive consistent coverage under insurance plans, which limits their adoption in clinical practice.

Regulatory Complexity and Standardization Challenges

The complex and evolving regulations governing biomarker-based diagnostics and therapeutics are another major challenge tothe North America Biomarkers Market. As per the U.S. Food and Drug Administration (FDA), the approval process for biomarker-integrated diagnostics involves multiple stages, including analytical validation, clinical validation, and demonstration of clinical utility, each requiring extensive documentation and evidence. This complexity often delays the commercialization of novel biomarkers, even when scientific data supports their effectiveness. According to the Association for Molecular Pathology (AMP), the average time required for regulatory review of a biomarker assay increased by 18% between 2020 and 2023, primarily due to heightened scrutiny of clinical relevance and reproducibility. Furthermore, inconsistencies in regulatory standards between federal agencies and state-level bodies create additional complications.s Stakeholders in Canada point out that approval processes are still uncertain even though Health Canada has modified its recommendations for biomarker-based diagnostics. As per the Canadian Medical Association Journal (CMAJ), delays in regulatory approvals have resulted in limited access to certain advanced biomarker tests in provinces outside major urban centers. These regulatory complexities and standardization gaps continue to pose substantial challenges for developers and healthcare providers aiming to integrate biomarkers into routine medical practice.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Big Data Analytics

The incorporation of big data analytics and artificial intelligence (AI) into biomarker discovery and interpretation offers an opportunity for the North America biomarkers market. AI enables researchers to analyse vast datasets from genomic sequencing, electronic health records (EHRs), and imaging modalities to uncover novel biomarkers that may have been previously overlooked. According to a 2023 study by the Dana-Farber Cancer Institute, machine learning models were able to more accurately identify novel immune-oncology biomarkers than conventional methods. Additionally, cloud-based analytics solutions are streamlining the processing and sharing of biomarker data among hospitals, laboratories, and pharmaceutical companies. Moreover, startups and tech firms are developing proprietary algorithms that can predict disease progression based on biomarker trends. Companies like Tempus and Freenome are leveraging AI to refine early cancer detection techniques, demonstrating the transformative potential of digital integration in the biomarker space.

Expansion of Companion Diagnostics and Personalized Therapies

The growing significance of companion diagnostics in personalized treatment provides an opportunity for the North America biomarkers market. According to the Personalized Medicine Coalition (PMC), over 70% of newly approved targeted therapies in the U.S. now require a companion diagnostic test based on biomarker analysis to guide treatment decisions. Companion diagnostics enable physicians to identify patients who are most likely to benefit from specific drugs, thereby improving treatment efficacy and reducing adverse effects. According to the U.S. Food and Drug Administration (FDA), 14 novel companion diagnostic tests were authorized in 2023, indicating the increasing use of biomarker-guided medication selection. Pharmaceutical companies are increasingly co-developing biomarker tests alongside new drugs to ensure optimal patient stratification. For example, the collaboration between AstraZeneca and Qiagen on the development of EGFR mutation tests for lung cancer therapies has set a precedent for integrated drug-diagnostic development models. Moreover, the rise of liquid biopsy technology has enabled non-invasive biomarker testing, which enables real-time monitoring of treatment response. The implementation of companion diagnostics into clinical practice is anticipated to propel sustainable expansion in the North American biomarkers market, with growing support from payers, regulatory agencies, and healthcare providers.

MARKET CHALLENGES

Reimbursement and Coverage Limitations

The inconsistent reimbursement policies and limited insurance coverage for many biomarker-based diagnostic tests are the major challenges facing the North American biomarkers market. Although biomarker science has advanced, many tests are still not covered by conventional insurance plans or have restricted coverage requirements, which restricts patient access. According to the Centers for Medicare & Medicaid Services (CMS), only 28% of newly introduced biomarker assays received full coverage under Medicare in 2023, with many requiring prior authorization or restricted indications. This creates administrative burdens for healthcare providers and discourages widespread adoption. Private insurers also exhibit variability in their coverage policies. According to the American Society of Clinical Oncology (ASCO), over 40% of patients seeking biomarker-guided cancer treatments had to pay more than $1,000 out of pocket since their insurance covered just some of the costs. Moreover, the absence of standardized billing codes for some biomarker tests complicates claims processing and reimbursement. As per the Healthcare Common Procedure Coding System (HCPCS), only 15 new biomarker-related codes were added in 2023, lagging behind the pace of test development.

Data Privacy and Ethical Concerns in Biomarker Use

Data privacy and ethical concerns surrounding biomarker utilization present another significant challenge in the North America Biomarkers Market. The use of genetic and health data in biomarker research has raised concerns regarding patient confidentiality, data ownership, and permission. Ethical dilemmas also arise regarding the use of predictive biomarkers, particularly in employment and insurance contexts. According to the Presidential Commission for the Study of Bioethical Issues, people with predisposition biomarkers for illnesses like cancer or Alzheimer's may face discrimination or be refused coverage even in the absence of legal protections. Moreover, informed consent practices in biomarker research remain inconsistent. According to research by the National Institutes of Health (NIH), there are gaps in interaction and transparency,y as over 40% of biobank members were unsure of how their data would be utilized.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Type, Product Application, ion and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada, and Rest of North America |

| Market Leader Profiled | Bio-Rad Laboratories (U.S.), Qiagen N.V. (Netherlands), Enzo Biochem (U.S.), PerkinElmer, Inc. (U.S.) |

SEGMENTAL ANALYSIS

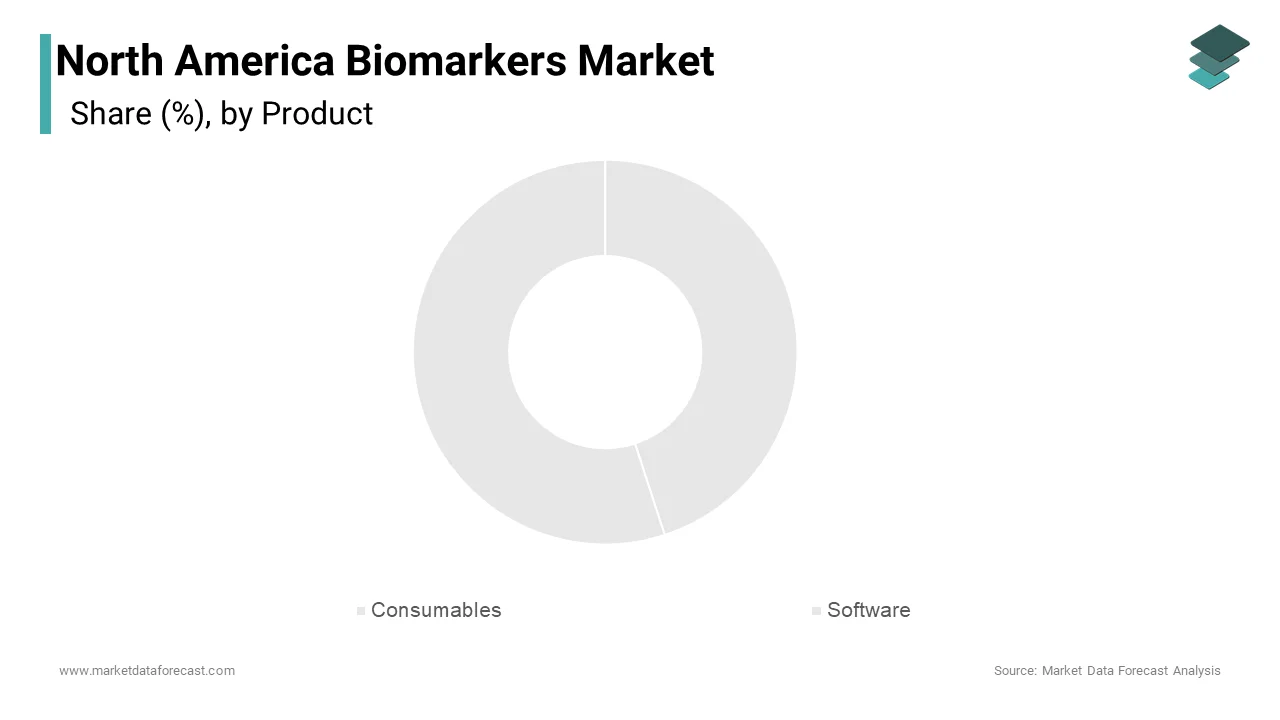

By Product Insights

The consumables segment dominated the North America biomarkers market by capturing 45.4% ofthe share in 2025. The growth of the segment is driven by the high-volume demand for reagents, assay kits, and sample preparation tools used in biomarker research, diagnostics, and drug development. One of the key drivers behind this segment’s leadership is the extensive use of consumables in clinical trials and academic research. Additionally, the expansion of diagnostic infrastructure in both the U.S. and Canada has increased the reliance on disposable and single-use consumables to ensure sterility and accuracy. According to the American Association for Clinical Chemistry (AACC), the number of biomarker-based laboratory tests conducted in U.S. hospitals increased by 28% over that time, which shows the necessity of a steady supply of consumables.

The software segment is estimated to register the fastest CAGR of 15.7% from 2025 to 2033. This rapid expansion is driven by the increasing integration of artificial intelligence (AI), machine learning, and cloud-based analytics into biomarker data interpretation and management. One of the primary factors fueling this growth is the adoption of digital health systems that enable real-time biomarker monitoring and predictive modeling. Furthermore, the rise in telemedicine and remote diagnostics has created a demand for software solutions that can process and store large volumes of patient biomarker data securely.

By Type Insights

The efficacy biomarkers segment led the North America biomarkers market with a 39.9% share in 2025. These biomarkers are extensively used to assess the effectiveness of therapeutic interventions, particularly in oncology, autoimmune diseases, and neurodegenerative disorders. A major factor behind this segment’s dominance is the growing focus on personalized medicine, where efficacy biomarkers play a crucial role in tailoring treatment strategies based on individual patient profiles. According to the American Society of Clinical Oncology (ASCO), over 75% of cancer treatment protocols in the U.S. now incorporate biomarker-driven efficacy assessments, leading to improved patient outcomes. In addition, pharmaceutical companies in North America are increasingly adopting efficacy biomarkers in clinical trials to enhance drug development efficiency. Moreover, regulatory bodies such as the U.S. Food and Drug Administration (FDA) and Health Canada have updated their approval guidelines to encourage the inclusion of efficacy biomarkers in trial designs.

The safety biomarkers segment is likely to experience the fastest CAGR of 16.2% from 2025 to 2033. The growth of the segment can be attributed to the rising focus on drug safety profiling and early detection of adverse effects during preclinical and clinical phases of drug development. Regulatory authorities across North America are increasingly mandating the use of safety biomarkers to minimize drug-related complications and improve patient safety. As per the U.S. Food and Drug Administration (FDA), adverse drug reactions contribute to over 100,000 annual deaths in the U.S., prompting stricter pharmacovigilance requirements. Pharmaceutical companies are also integrating safety biomarkers into their pipelines to streamline regulatory submissions and reduce late-stage trial failures. Furthermore, the establishment of specialized toxicogenomics labs in the U.S. and Canada is facilitating the discovery and validation of new safety biomarkers.

By Application Insights

The drug discovery and development segment was the largest and accounted for 41.2% of North America's biomarkers market share in 202,5 with the integral role biomarkers play in accelerating pharmaceutical R&D processes and improving success rates in clinical trials. One of the main drivers is the growing participation of North American institutions in global clinical trials, particularly in oncology and rare diseases. According to the U.S. National Library of Medicine, over 120,000 biomarker-integrated clinical trials were registered in the U.S. between 2020 and 2023, many of which focused on novel drug candidates. Moreover, regulatory agencies such as the FDA have introduced policies encouraging the use of biomarkers in drug development frameworks. According to the FDA's Biomarker Qualification Program, there was a rise in industry participation in 2023, as seen by the acceptance of 25 additional biomarker submissions for assessment. Additionally, collaborations between multinational pharma companies and local research institutions are fueling innovation in this space.

The Personalized medicine segment is anticipated to witness the fastest CAGR of 16.8% between 2025 and 2033 owing to the increasing awareness of precision medicine and its potential to improve treatment outcomes through targeted therapies. A key factor propelling this segment is the expansion of genomic medicine programs across the region. According to the NIH-led All of Us Research Program, by mid-2023, more than one million people had provided genetic and health data, much of which involved the selection of therapies based on biomarkers. Public health institutions are also adopting personalized approaches in chronic disease management. Additionally, the public is becoming increasingly able to receive personalized medicine due to the growth of direct-to-consumer genetic testing services like those provided by 23andMe and Color Genomics.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North America biomarkers market with a 78.4% share in 2025. Positioned as the dominant force in the region, the U.S. benefits from a highly developed healthcare system, robust R&D funding, and a thriving biopharmaceutical industry. One of the key drivers is the country’s leadership in genomics and precision medicine. Additionally, the presence of leading research institutions such as the Mayo Clinic, Memorial Sloan Kettering, and Stanford University has fostered a strong ecosystem for biomarker discovery and validation. Moreover, the U.S. regulatory environment is conducive to rapid innovation. The FDA’s expedited approval pathways for companion diagnostics and biomarker assays have significantly reduced time-to-market for novel diagnostics and strengthened the nation's position as a leader in the world of biomarkers.

Canada was ranked second in the North America Biomarkers Market by capturing 17.6% of the share in 2025. Canada maintains a strong foothold due to its well-funded public health system, active government support for life sciences, and growing partnerships between academia and industry. A major growth enabler is the country’s commitment to precision medicine and genomics research. Moreover, Canada’s regulatory framework supports the development and adoption of innovative diagnostics. Health Canada approved 12 new biomarker-based tests in 2023, including several companion diagnostics for targeted cancer therapies, showing a progressive approach to market access. Additionally, the country has seen an uptick in biotech startups specializing in biomarker technologies. According to the Ontario Institute for Cancer Research, seven new companies specializing in liquid biopsy and proteomic biomarkers appeared in 2023, indicating an encouraging business climate that supports market growth.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

A few of the noteworthy companies operating in the North American biomarkers market profiled in this report are Bio-Rad Laboratories (U.S.), Qiagen N.V. (Netherlands), Enzo Biochem (U.S.), PerkinElmer, Inc. (U.S.), Merck & Co, Inc. (U.S.), EKF Diagnostics Holdings plc. (U.S.), Meso Scale Diagnostics, LLC (U.S.), Singulex, Inc. (U.S.), BioSims Technologies (France), Cisbio Bioassays (France), and Signosis, Inc. (U.S.).

The competition in the North America Biomarkers Market is highly dynamic, driven by rapid technological advancements, increasing investment in precision medicine, and growing demand for predictive and personalized healthcare solutions. An increasingly competitive environment is a result of the coexistence of multinational corporations with an expanding number of creative startups and academic spin-offs. Established players maintain dominance through extensive R&D capabilities, strong regulatory expertise, and well-established distribution channels. However, emerging firms are gaining traction by introducing niche technologies and specialized biomarker assays tailored for specific therapeutic areas. The market is also witnessing intensified collaboration between industry leaders and healthcare institutions to develop integrated diagnostic platforms that combine biomarker testing with real-time data analytics. Businesses are always improving strategies in order to gain market dominance while meeting unmet clinical requirements as regulatory frameworks and reimbursement models change.

Top Players in the Market

F. Hoffmann-La Roche Ltd.

Roche is a dominant player in the North America Biomarkers Market by utilizing its expertise in diagnostics and pharmaceuticals to advance biomarker-driven healthcare. The company develops companion diagnostics that enable personalized treatment strategie,s particularly in oncology and chronic disease management. Roche'globally leadership in precision medicine is further strengthened by its partnerships with top research institutes and regulatory agencies that integrate biomarkers into clinical practice and drug development.

Thermo Fisher Scientific Inc.

Thermo Fisher plays a critical role in supplying high-quality biomarker-related products including analytical instruments, reagents, and laboratory services across North America. The company supports academic and clinical research by offering advanced tools for biomarker discovery, validation, and application. Its strategic partnerships and comprehensive portfolio make it a key enabler of innovation in life sciences and diagnostic sectors throughout the region.

Qiagen N.V.

Qiagen is a leader in sample preparation and molecular diagnostics, offering a wide range of solutions tailored for biomarker research and clinical applications. In North America, Qiagen provides integrated platforms for genomic analysis, enabling early disease detection and targeted therapies. The company works closely with biotech firms, hospitals, and research centers to enhance the utility and accessibility of biomarkers in precision medicine and drug development.

Top Strategies Used by Key Players

A primary strategy employed by key players in the North America Biomarkers Market is forming strategic collaborations with academic institutions, research organizations, and biotech firms. These partnerships facilitate access to novel biomarker discoveries and accelerate their translation into clinical applications.

Another major approach involves expanding product portfolios through acquisitions and internal innovation. Companies are investing in next-generation sequencing, digital pathology, and AI-powered analytics to enhance biomarker identification and interpretation capabilities by ensuring they remain at the forefront of technological advancements.

Additionally, market leaders are strengthening their commercial presence through enhanced distribution networks and localized support services. Businesses increase the accessibility and use of biomarker-based diagnostics in a variety of clinical settings by setting up regional service centers and engaging directly with healthcare providers.

RECENT HAPPENINGS IN THE MARKET

In February 2024, Roche launched a new companion diagnostic test in partnership with the Memorial Sloan Kettering Cancer Center ,which is designed to identify patients eligible for a recently approved immunotherapy drug.

In June 2023, Thermo Fisher Scientific expanded its North American footprint by opening a state-of-the-art biomarker research facility in Massachusetts. This research facility aims to accelerate the development of next-generation diagnostic assays and support pharmaceutical clients in clinical trial design.

In October 2023, Qiagen introduced a fully integrated digital biomarker platform that combines assay data with AI-driven interpretation tools, which helps in enhancing decision-making for clinicians and researchers across the U.S. healthcare system.

In March 2024, LabCorp announced a strategic alliance with a leading AI health tech firm to incorporate machine learning into its biomarker analytics pipeline, which improves early disease detection and patient stratification for clinical trials.

In August 2023, Exact Sciences acquired a biotech startup specializing in liquid biopsy-based cancer biomarkers, which strengthens its portfolio of non-invasive diagnostic solutions andexpandsg its reach in precision oncology within North America.

MARKET SEGMENTATION

This research report on the North American Biomarkers Market has been segmented and sub-segmented into the following categories.

By Product

- Consumables

- Software

By Type

- Safety Biomarkers

- Efficacy Biomarkers

- Validation Biomarkers

By Application

- Drug Discovery & Developments

- Personalized Medicine

By Country

- The United States

- Canada

- Rest of North America