North America Medical Gas Equipment Market Research Report - Segmented By Product (Medical Gases, Medical Gas Mixtures, Medical Gas Equipment), Application, End-users & Country (the United States, Canada and Rest of North America) - Industry Analysis From 2026 to 2034

North America Medical Gas Equipment Market Summary

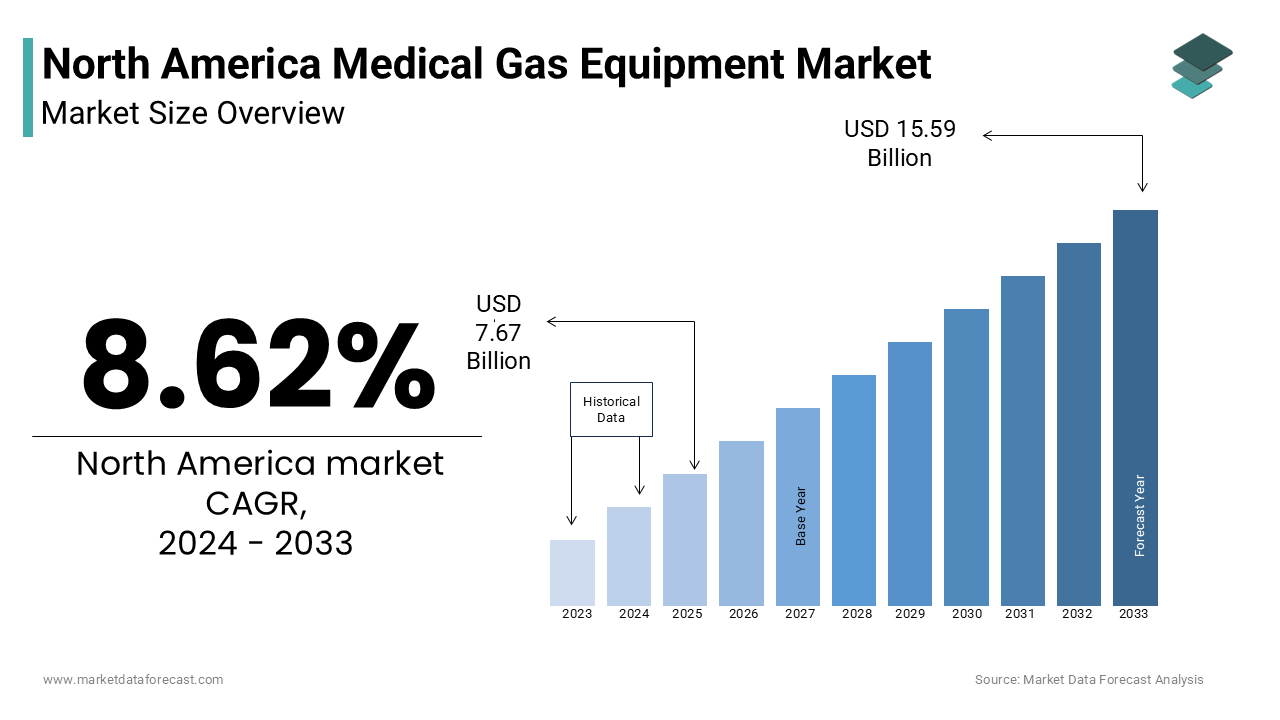

The North America medical gas equipment market was valued at USD 7.67 billion in 2024 and is projected to reach USD 15.59 billion by 2033, growing at a CAGR of 8.2%.

Medical gas systems are crucial for the safe storage, distribution, and delivery of oxygen, nitrous oxide, and other gases across hospitals, clinics, homecare, and emergency services. The market is driven by rising respiratory disease prevalence, aging populations, smart oxygen delivery solutions, and expanding home healthcare adoption.

Key Market Trends & Insights

-

United States led the market with 85.1% share in 2024, driven by robust healthcare infrastructure and regulatory frameworks (NFPA 99, FDA).

-

Medical Gas Equipment dominated by product, with 56.2% market share due to hospital infrastructure needs.

-

Therapeutic applications accounted for 48.1% share in 2024; home healthcare is the fastest-growing segment (CAGR: 12.1%).

-

Medical Gas Mixtures segment is growing at a CAGR of 10.8%, especially in anesthesia and respiratory therapies.

Market Size & Forecast

-

2024 Market Size: USD 7.67 Billion

-

2033 Projected Market Size: USD 15.59 Billion

-

CAGR (2024–2033): 8.2%

-

United States: Largest market (85.1% share)

-

Canada & Mexico: Emerging focus on home-based care and infrastructure modernization

North America Medical Gas Equipment Market Size

The medical gas equipment market size in North America is projected to grow from USD 7.67 billion in 2024 to USD 15.59 billion by 2033, at a CAGR of 8.2%.

The North America medical gas equipment market encompasses a wide range of specialized systems and devices used for the safe storage, distribution, and administration of medical gases such as oxygen, nitrous oxide, carbon dioxide, and medical air in healthcare settings. These gases are essential for patient care in hospitals, clinics, ambulatory surgical centers, and home healthcare environments. The market includes bulk gas storage units, manifold systems, pressure regulators, anesthesia machines, oxygen concentrators, and associated delivery accessories.

North America leads in the adoption of advanced medical gas technologies due to its well-established healthcare infrastructure, stringent safety regulations, and high demand for critical care services.

Besides, the aging population and rising prevalence of chronic respiratory diseases have significantly increased the need for medical oxygen and related equipment, especially in home healthcare settings. As per the Centers for Disease Control and Prevention, chronic lower respiratory diseases remain among the leading causes of death in the U.S., further driving demand for portable oxygen concentrators and related delivery systems.

Moreover, regulatory frameworks such as NFPA 99 and CSA Z7396 in the U.S. and Canada respectively mandate strict compliance with medical gas system design and maintenance standards. This emphasis on patient safety and operational reliability ensures continuous innovation and investment in medical gas equipment across North America.

MARKET DRIVERS

Increasing Prevalence of Respiratory Diseases

One of the primary drivers of the North America medical gas equipment market is the increasing prevalence of chronic respiratory conditions such as chronic obstructive pulmonary disease (COPD), asthma, cystic fibrosis, and sleep apnea. These conditions necessitate long-term or intermittent use of medical oxygen and other therapeutic gases, particularly among the aging population.

According to the American Lung Association, more than 16 million Americans have been diagnosed with COPD, though the actual number may be higher due to undiagnosed cases.

This trend has spurred demand for both institutional and home-based oxygen delivery systems. Home oxygen therapy usage has surged, driven by advancements in portable oxygen concentrators and favorable reimbursement policies from Medicare and private insurers. As per the National Home Infusion Association, home oxygen therapy services accounted for a significant portion of outpatient respiratory care in 2023, reinforcing the role of medical gas equipment in decentralized healthcare models.

With respiratory illnesses continuing to rise due to environmental factors, smoking habits, and an aging demographic, the need for efficient and reliable medical gas delivery systems remains a strong growth catalyst.

Expansion of Critical Care Infrastructure and Emergency Preparedness

Another key driver fueling the North America medical gas equipment market is the expansion of critical care infrastructure and heightened focus on emergency preparedness following recent public health crises. Hospitals and government agencies have prioritized investments in ICU beds, ventilators, and centralized medical gas systems to ensure readiness for surges in critical care demand.

According to U.S. Department of Health and Human Services, between 2020 and 2023, federal funding for hospital infrastructure modernization exceeded $15 billion, with a significant portion allocated to upgrading medical gas pipelines, bulk oxygen storage, and emergency backup systems. These upgrades were prompted by lessons learned during the peak of the pandemic when shortages of medical oxygen led to supply chain vulnerabilities and highlighted the need for resilient gas delivery networks.

These developments have created sustained demand for medical gas equipment, not only in acute care hospitals but also in rehabilitation centers, urgent care clinics, and mobile healthcare units, reinforcing the sector’s long-term growth trajectory.

MARKET RESTRAINTS

High Installation and Maintenance Costs

A major restraint affecting the North America medical gas equipment market is the high cost associated with installation, commissioning, and ongoing maintenance of medical gas systems. Unlike standard HVAC or industrial gas setups, medical gas infrastructure must adhere to stringent regulatory requirements set forth by standards such as NFPA 99 and CSA Z7396, which mandate extensive testing, certification, and periodic inspections.

According to the Joint Commission, which accredits healthcare organizations in the U.S., non-compliance with medical gas system standards is one of the top reasons for facility citations during routine audits. This has forced hospitals and clinics to invest in regular maintenance contracts, leak detection systems, and certified technicians, adding to the overall operational burden.

Furthermore, the installation of centralized medical gas systems in new healthcare facilities can cost millions of dollars, depending on the scale and complexity of the piping network. While these costs are justified by long-term benefits and regulatory necessity, they pose financial challenges, particularly for smaller healthcare providers and rural hospitals with limited budgets. Until financing models improve and modular, scalable solutions become more widely available, cost barriers will continue to hinder broader market penetration.

Regulatory Compliance and Standardization Challenges

An additional significant constraint impacting the North America medical gas equipment market is the complex regulatory landscape governing the design, installation, and operation of medical gas systems. Both the United States and Canada enforce rigorous compliance protocols to ensure patient safety, equipment reliability, and system integrity, often requiring multiple certifications and third-party inspections.

In the U.S., compliance with NFPA 99 – Health Care Facilities Code – is mandatory for all healthcare institutions utilizing medical gas systems. Moreover, in Canada, adherence to CSA Z7396 – Piping Systems for Medical Gases and Vacuum – is required for all new and renovated healthcare facilities.

However, interpreting and implementing these standards consistently across different states and provinces remains a challenge. Variations in local building codes, inspector interpretations, and enforcement mechanisms create uncertainty for manufacturers and installers alike.

In addition, evolving standards and updates to existing codes—such as the 2023 revisions to NFPA 99—require ongoing training and system modifications, further complicating compliance efforts. As a result, some healthcare providers delay upgrades or expansions, limiting the pace of medical gas equipment adoption in certain regions. Until harmonization of regulatory practices improves across North America, compliance complexity will remain a persistent hurdle for market participants.

MARKET OPPORTUNITIES

Growth in Home Healthcare and Portable Oxygen Therapy

An emerging opportunity in the North America medical gas equipment market is the rapid expansion of home healthcare services, particularly in the domain of portable oxygen therapy. With rising preference for home-based treatment options, patients suffering from chronic respiratory conditions increasingly rely on lightweight, battery-powered oxygen concentrators and nasal cannulas that offer mobility and convenience without compromising therapeutic efficacy.

According to the Centers for Medicare & Medicaid Services, expenditures on home oxygen therapy grew significantly between 2020 and 2023, reflecting increased utilization and improved insurance coverage. Private insurers and managed care organizations have also expanded their reimbursement policies, encouraging wider adoption of home-based oxygen delivery systems.

Manufacturers are responding to this shift by developing compact, energy-efficient, and user-friendly oxygen concentrators tailored for domestic use. Companies like Philips Respironics, Inogen, and Invacare have introduced next-generation models equipped with smart sensors, remote monitoring capabilities, and integrated alarms, enhancing patient safety and caregiver oversight.

Also, telehealth platforms are integrating remote oxygen saturation tracking into chronic disease management programs, further reinforcing the role of medical gas equipment beyond traditional clinical settings. As the trend toward decentralized care continues to accelerate, the home healthcare segment presents a compelling avenue for sustained growth and innovation in the North America medical gas equipment market.

Integration of Smart Monitoring and IoT-Enabled Gas Delivery Systems

A transformative opportunity shaping the North America medical gas equipment market is the integration of smart monitoring and Internet of Things (IoT)-enabled gas delivery systems. As digital transformation gains momentum in healthcare, hospitals and home care providers are increasingly adopting connected medical devices that enable real-time data tracking, predictive maintenance, and remote diagnostics.

Smart medical gas systems equipped with pressure sensors, flow meters, and cloud-connected analytics platforms allow healthcare professionals to monitor gas consumption patterns, detect anomalies, and optimize resource allocation. Several leading manufacturers have launched intelligent oxygen concentrators and centralized gas management systems that integrate with hospital building automation and electronic health record (EHR) platforms. These innovations enhance clinical decision-making while improving compliance with regulatory reporting requirements.

Beyond institutional settings, smart home oxygen concentrators with app-based interfaces are gaining traction, allowing caregivers and family members to remotely monitor device performance and refill schedules. This connectivity enhances patient adherence to prescribed therapy regimens and reduces the risk of service interruptions. With continued advancements in AI-driven analytics and wireless communication protocols, smart and connected medical gas equipment is poised to redefine efficiency, safety, and responsiveness across North American healthcare environments.

MARKET CHALLENGES

Supply Chain Disruptions and Raw Material Shortages

A significant challenge facing the North America medical gas equipment market is the ongoing volatility in global supply chains and raw material availability. The manufacturing of medical gas equipment involves precision components, specialty metals, and polymer-based tubing and valves, many of which are sourced from international suppliers.

Also, according to the U.S. Department of Commerce, supply chain bottlenecks caused by geopolitical tensions, freight delays, and semiconductor shortages have led to extended lead times for critical parts used in gas regulators, compressors, and monitoring devices. These disruptions have affected production timelines and inventory availability, particularly for smaller manufacturers with limited procurement flexibility.

Apart from these, fluctuations in commodity prices—especially for stainless steel, aluminum, and copper—have added upward pressure on production costs. As per the Industrial Distribution Group in 2023, material price increases contributed to double-digit cost escalations for certain medical gas system components, forcing some companies to raise end-user prices or absorb losses.

These supply-side constraints complicate pricing strategies and profitability, especially for firms operating in highly regulated markets where product specifications and quality control measures leave little room for substitution. Until supply chain stability improves and localized sourcing expands, these logistical and cost-related challenges will continue to impact the growth and scalability of the North America medical gas equipment industry.

Skilled Labor Shortage and Technical Expertise Gap

An escalating challenge for the North America medical gas equipment market is the shortage of skilled labor and technical expertise required for proper installation, servicing, and compliance auditing of medical gas systems. The complexity of these systems demands trained personnel who understand gas purity requirements, pressure regulation, leak testing procedures, and code compliance standards.

According to the American Society of Safety Professionals (ASSP), there has been a growing gap between industry demand for certified medical gas installers and the current workforce capacity. Many vocational schools and trade programs have not kept pace with the evolving technical requirements of modern medical gas infrastructure, resulting in a shortage of qualified technicians.

This skills gap has led to inconsistencies in system performance and increased instances of non-compliance during regulatory inspections. As per the Joint Commission in 2023, deficiencies related to medical gas system maintenance and technician qualifications were among the most frequently cited issues during hospital accreditation reviews.

To address this challenge, industry associations such as ASSE International and the Compressed Gas Association are expanding certification programs and partnering with healthcare institutions to develop standardized training modules. However, until workforce development efforts catch up with market needs, the lack of skilled professionals will remain a pressing obstacle to the seamless deployment and maintenance of medical gas equipment across North America.

SEGMENTAL ANALYSIS

By Product Insights

Medical gas equipment spearheaded the North America medical gas equipment market, capturing an estimated 56.2% of total revenue in 2024. This dominance is attributed to the extensive infrastructure required for the safe storage, distribution, and administration of medical gases across healthcare settings.

A primary driver behind this segment’s leadership is the critical need for centralized gas pipeline systems, pressure regulators, flow meters, and manifold assemblies in hospitals and surgical centers. According to the American Hospital Association, there are over 6,000 registered hospitals in the U.S., each requiring robust medical gas delivery systems that comply with NFPA 99 standards. The installation and maintenance of these systems represent a significant portion of capital expenditures in healthcare infrastructure.

In addition, demand for portable oxygen concentrators has surged due to the growing home healthcare sector. As per the National Home Infusion Association, more than 1.5 million Americans receive home oxygen therapy annually, necessitating reliable and user-friendly gas delivery equipment.

Moreover, emergency services and ambulatory care centers rely heavily on compact oxygen cylinders, nasal cannulas, and transportable gas units, further reinforcing the importance of medical gas equipment in both institutional and mobile healthcare environments. With continuous advancements in smart monitoring and IoT-enabled devices, the medical gas equipment segment remains at the core of the industry’s growth trajectory in North America.

Medical gas mixtures are emerging as the fastest-growing segment in the North America medical gas equipment market, projected to expand at a CAGR of 10.8%. This rapid expansion is driven by increasing use of specialized gas blends in anesthesia, respiratory therapy, and diagnostic procedures.

One of the key factors fueling this growth is the rising number of surgeries and interventional procedures that require precise gas combinations such as oxygen-nitrous oxide and helium-oxygen (heliox). In addition, the adoption of heliox mixtures for treating obstructive lung diseases like asthma and COPD has gained traction in both hospital and outpatient settings. Pharmaceutical and biotechnology companies are also utilizing medical gas mixtures in drug development and testing processes. With ongoing clinical research into hyperbaric oxygen therapy and neonatal care applications, the demand for customized gas compositions continues to rise, making this segment one of the most dynamic areas of the market.

By Application Insights

Therapeutic applications held the dominant position in the North America medical gas equipment market, accounting for 48.1% of total share in 2024. This strong presence is primarily driven by the widespread use of medical oxygen, nitrous oxide, and heliox mixtures in treating respiratory conditions, pain management, and critical care interventions.

One of the major drivers behind this segment’s leadership is the high prevalence of chronic respiratory diseases such as COPD, asthma, and cystic fibrosis. According to the Centers for Disease Control and Prevention, chronic lower respiratory diseases remain among the leading causes of death in the U.S., underscoring the reliance on oxygen therapy and inhalation-based treatments.

Furthermore, the aging population in North America has intensified the demand for long-term oxygen support. As per the data by Medicare, over 1.7 million beneficiaries received home oxygen therapy in 2023, highlighting the role of therapeutic gas usage beyond acute care settings.

Hospitals and rehabilitation centers increasingly utilize oxygen-enriched air and controlled gas mixtures for post-operative recovery, wound healing, and sleep apnea treatment. With continued investment in respiratory disease management and patient-centered care models, the therapeutic application segment remains central to the growth and stability of the North America medical gas equipment market.

Diagnostic applications are the booming area in the North America medical gas equipment market, expected to grow at a CAGR of 11.4%. This surge is largely fueled by the expanding use of medical gases in pulmonary function testing, imaging diagnostics, and contrast-enhanced ultrasound procedures.

A major factor driving this growth is the increasing incidence of respiratory disorders that require early and accurate diagnosis. Pulmonary function tests (PFTs), which often involve the use of nitrogen, helium, and oxygen mixtures, are essential for assessing lung capacity and identifying conditions such as asthma, emphysema, and bronchitis.

Also, carbon dioxide is widely used in endoscopic procedures such as laparoscopy to insufflate body cavities, enabling better visualization during minimally invasive surgeries. Moreover, hyperpolarized noble gases like xenon and helium-3 are gaining attention in MRI imaging for lung visualization, offering non-invasive alternatives to traditional radiographic methods. As diagnostic modalities evolve, so too does the demand for specialized medical gas equipment tailored to precision medicine and advanced imaging technologies.

By End-users Insights

Hospitals accounted for the largest end-user segment in the North America medical gas equipment market, holding 63.3% of total share in 2024. This overwhelming dominance stems from the indispensable role medical gases play in emergency care, surgery, intensive care units, and neonatal wards.

A primary driver behind this segment’s leadership is the sheer scale of medical gas consumption within hospital facilities. According to the Joint Commission, every major hospital in the U.S. must maintain a fully compliant medical gas system capable of supplying oxygen, nitrous oxide, and medical air to multiple departments simultaneously.

Also, the expansion of ICU beds and surgical centers has intensified demand for reliable gas delivery infrastructure. Furthermore, federal mandates such as NFPA 99 and CSA Z7396 ensure that hospitals maintain strict compliance with gas purity, pressure regulation, and safety protocols. These requirements reinforce the need for regular equipment upgrades and preventive maintenance, ensuring sustained investment in medical gas infrastructure.

As healthcare institutions continue to modernize and expand their capabilities, hospitals will remain the cornerstone of the North America medical gas equipment market.

Home healthcare is the booming end-user segment in the North America medical gas equipment market, projected to expand at a CAGR of 12.1%. This rapid expansion is driven by shifting healthcare preferences toward decentralized treatment models, particularly for patients with chronic respiratory conditions.

One of the primary factors fueling this trend is the rising number of patients opting for home-based oxygen therapy. Moreover, advancements in lightweight, battery-powered oxygen concentrators have made it easier for patients to manage chronic conditions outside of hospital settings. Companies like Inogen and Philips Respironics have introduced compact, FAA-approved devices that allow users to travel while maintaining continuous oxygen therapy.

The shift toward value-based care models is also contributing to this growth. Health systems are incentivized to reduce hospital readmissions and promote outpatient care, which in turn increases reliance on home medical gas equipment. Telehealth integration is further enhancing the appeal of home-based solutions, allowing caregivers to remotely monitor oxygen saturation levels and device performance. As consumer awareness and insurance coverage improve, the home healthcare segment is poised for sustained high-growth momentum in the coming years.

REGIONAL ANALYSIS

United States Medical Gas Equipment Market Insights

The United States held the dominant position in the North America medical gas equipment market, capturing an estimated 85.1% of total market share in 2024. As the global leader in healthcare innovation and infrastructure, the U.S. benefits from a vast network of hospitals, clinics, and home healthcare providers that rely on consistent and regulated medical gas supply systems.

This position is reinforced by stringent regulatory frameworks such as NFPA 99 and FDA guidelines governing medical gas purity and system integrity. In addition, federal programs such as Medicare and Medicaid provide reimbursement for home oxygen therapy, significantly expanding access to portable oxygen concentrators. The U.S. also leads in research and development initiatives, with academic institutions and pharmaceutical companies leveraging medical gases for clinical trials, hyperbaric therapy, and pulmonology studies. As digital health platforms integrate remote oxygen monitoring into chronic disease management, the U.S. remains at the forefront of technological advancement and market expansion in the region.

Canada Medical Gas Equipment Market Insights

Canada is a significant player in the North America medical gas equipment market. While smaller than the U.S. market, Canada's healthcare system ensures broad access to medical gas equipment through universal health coverage and well-established hospital networks.

A key driver behind Canada’s market position is the country’s commitment to upgrading healthcare infrastructure. Also, the Canadian healthcare landscape emphasizes home-based care, supported by provincial funding mechanisms that cover durable medical equipment for chronic disease management. Provincial governments, including Ontario and Quebec, have implemented policies promoting the adoption of energy-efficient and technologically advanced medical gas equipment in public hospitals. Moreover, the Canadian Standards Association (CSA) enforces rigorous compliance standards under CSA Z7396, ensuring that medical gas systems meet the highest safety benchmarks.

With a strong emphasis on patient safety, regulatory oversight, and home healthcare expansion, Canada continues to strengthen its role in the regional medical gas equipment market.

Rest of North America Medical Gas Equipment Market Insights

The Rest of North America, comprising Mexico and select Caribbean economies, accounted for smaller share of the regional medical gas equipment market in 2024. Though currently a minor player compared to the U.S. and Canada, this sub-region is witnessing gradual growth driven by healthcare modernization efforts and cross-border collaboration with North American suppliers.

Mexico is showing increasing interest in adopting medical gas equipment in private hospitals, rehabilitation centers, and specialty clinics. In the Caribbean, islands such as Puerto Rico and Jamaica are exploring partnerships with U.S.-based medical gas distributors to enhance emergency preparedness and improve access to oxygen therapy in remote communities. While still in the early stages of adoption, these developments indicate potential for expanded utilization of medical gas equipment beyond traditional markets in North America.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a dominant role in the North America Medical Gas Equipment Market profiled in this report are Air Products and Chemicals, Inc., The Linde Group, Air Liquide, Praxair, Inc., Taiyo Nippon Sanso Corp., SOL-SpA, Airgas, Inc., Atlas Copco, Messer Group, GCE Holding AB, Beacon Medaes, Medical Gas Solutions Ltd., Matheson Tri-Gas, Taiya Nippon Sanso and Atlas Copco.

The competition in the North America medical gas equipment market is marked by a blend of multinational corporations and specialized regional firms vying for dominance through product differentiation, service excellence, and strategic expansion. Established players such as Linde, Air Liquide, and Chart Industries maintain strong positions due to their extensive distribution networks, deep technical expertise, and robust compliance capabilities.

However, the market is becoming increasingly competitive with the emergence of niche manufacturers focusing on home oxygen therapy, portable delivery systems, and IoT-enabled monitoring solutions. These companies are leveraging digital health trends and telemedicine integration to capture segments traditionally dominated by larger firms.

Additionally, the demand for cost-effective, scalable, and user-friendly medical gas equipment is encouraging new entrants and startups to innovate in areas such as compact oxygen concentrators, disposable nasal cannulas, and mobile gas delivery units. This growing diversity fosters a dynamic competitive environment where agility and customer-centric design play pivotal roles.

Regulatory compliance remains a key differentiator, with only a few companies possessing the resources to navigate complex certification processes and maintain nationwide service infrastructures. As healthcare continues to evolve toward decentralized care models, the market is expected to witness intensified competition, particularly in home-based therapeutic applications and smart medical gas technologies.

Top Players in the North America Medical Gas Equipment Market

One of the leading players in the North America medical gas equipment market is Linde plc, a global leader in industrial and medical gases. The company plays a crucial role in supplying high-purity medical oxygen, nitrous oxide, and specialized gas mixtures to hospitals, clinics, and home healthcare providers across the region. Linde’s advanced gas generation and distribution technologies ensure reliable and safe delivery of medical gases, supporting both emergency and long-term patient care.

Another key player is Air Liquide Healthcare, a division of Air Liquide Group, which specializes in respiratory therapy solutions and home oxygen therapy services. The company offers a wide range of portable oxygen concentrators, stationary oxygen systems, and related accessories tailored for chronic disease management outside hospital settings. Its focus on patient-centric innovation and comprehensive service support has strengthened its presence in the North American home healthcare sector.

Chart Industries is also a major contributor to the North America medical gas equipment market. Known for its cryogenic and gas processing technologies, Chart produces essential equipment such as medical liquid oxygen storage tanks, pressure regulators, and manifold systems used in hospitals and ambulatory care centers. Its expertise in vacuum-insulated vessels and pipeline integration supports the safe and efficient use of medical gases in critical healthcare environments.

Top Strategies Used by Key Market Participants

A primary strategy employed by key players in the North America medical gas equipment market is product innovation and technological advancement. Companies are continuously developing next-generation oxygen delivery systems, smart monitoring devices, and energy-efficient gas storage solutions that align with evolving clinical needs and regulatory standards.

Another important approach is expanding service networks and after-sales support. Given the critical nature of medical gas equipment, manufacturers are investing heavily in maintenance programs, technician training, and rapid-response service teams to ensure uninterrupted supply and system reliability for healthcare providers.

Lastly, companies are focusing on strategic partnerships with healthcare institutions and government agencies. By collaborating with hospitals, home healthcare providers, and public health departments, industry leaders can better understand end-user requirements and influence policy frameworks that support broader adoption of advanced medical gas systems.

RECENT MARKET DEVELOPMENTS

- In January 2024, Linde plc launched a new line of on-site oxygen generation systems designed for mid-sized hospitals and surgical centers, aiming to reduce dependency on bulk gas deliveries while ensuring uninterrupted supply during emergencies.

- In March 2024, Air Liquide Healthcare introduced a cloud-connected oxygen concentrator platform that enables remote monitoring and predictive maintenance, enhancing patient safety and caregiver efficiency for individuals undergoing home oxygen therapy.

- In June 2024, Chart Industries expanded its manufacturing facility in Florida to increase production capacity for medical-grade cryogenic storage tanks and pipeline-ready gas distribution units, strengthening its ability to meet rising institutional demand.

- In September 2024, Invacare Corporation, a leading provider of home medical equipment, announced a partnership with a national pharmacy chain to integrate portable oxygen concentrators into prescription-based home care packages, improving consumer access and reimbursement pathways.

- In December 2024, Philips Respironics unveiled a next-generation oxygen therapy suite featuring AI-driven flow adjustment and real-time patient analytics, positioning itself at the forefront of intelligent home-based respiratory care solutions.

MARKET SEGMENTATION

This research report on the North America Medical Gas Equipment Market has been segmented and sub-segmented into the following categories.

By Product

- Medical Gases

- Medical Gas Mixtures

- Medical Gas Equipment

By Application

- Therapeutic

- Diagnostic

- Pharmaceutical Manufacturing

- Research

By End-users

- Hospitals

- Home Healthcare

- Emergency Services

- Pharmaceutical Industry

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What is driving the growth of north america medical gas equipment market?

Key drivers include rising demand for respiratory care, increasing number of surgeries and hospital admissions, growth in home healthcare services, and technological advancements in gas delivery systems.

Which countries contribute most to the North American market?

The United States dominates the market, followed by Canada and Mexico, with the U.S. accounting for the majority share due to its large healthcare infrastructure.

What are the major trends shaping this market?

Trends include the rise of portable gas delivery systems, integration of digital monitoring in gas equipment, increased demand from home-based respiratory care, and regulatory compliance upgrades in gas supply infrastructure.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com