North America Oilseed Processing Market Size, Share, Trends & Growth Forecast Report By Type (Soybean, Rapeseed, Sunflower, And Cottonseed), Process, Application, and Country (The United States, Canada and Rest of North America), Industry Analysis From 2025 to 2033

North America Oilseed Processing Market Size

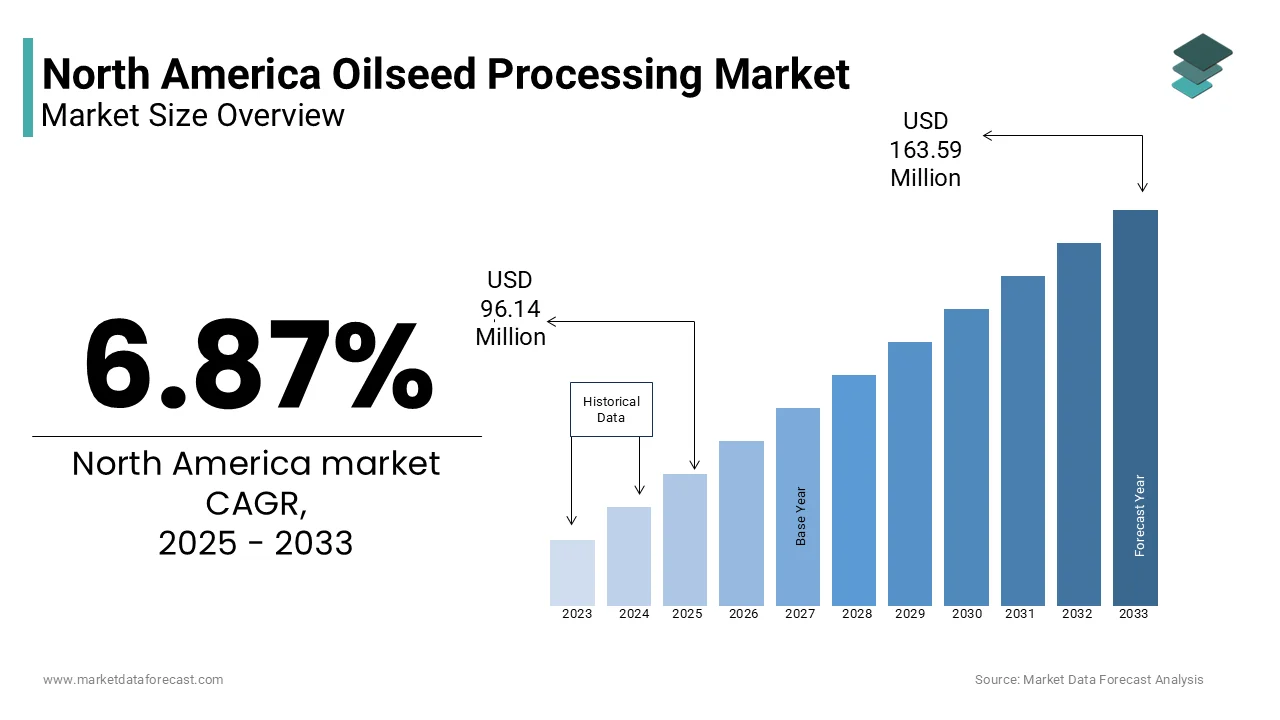

The Oilseed processing market size in North America was valued at USD 89.96 million in 2024 and the market size is predicted to be worth USD 163.59 million by 2033 from USD 96.14 million in 2025. The market is growing at a CAGR of 6.87% from 2025 to 2033.

The North America Oilseed Processing Market incorporates the mechanical and chemical transformation of oil-bearing seeds such as soybeans, canola, sunflower, flax, and safflower into edible oils, biodiesel feedstocks, and high-protein animal feed ingredients. This market plays a pivotal role in supporting both the food and energy sectors across the United States, Canada, and Mexico. The processing involves crushing, refining, and extracting oil through advanced technologies that ensure purity and efficiency.

The sector benefits from robust agricultural infrastructure, government subsidies, and growing demand for plant-based proteins and renewable fuels.

MARKET DRIVERS

Rising Demand for Plant-Based Proteins

One of the key drivers fueling the North America Oilseed Processing Market is the surging consumer preference for plant-based proteins. As health consciousness grows and environmental concerns intensify, consumers are increasingly shifting from animal-derived proteins to alternatives sourced from soy, canola, and other oilseeds. This dietary transition has spurred demand for protein-rich by-products such as soybean meal and canola meal, which serve as essential components in meat substitutes, dairy alternatives, and nutritional supplements.

The expanding footprint of companies like Beyond Meat and Impossible Foods, which heavily rely on soy and canola proteins, reflects this trend. Besides, as per the U.S. Soybean Export Council, domestic consumption of soybean meal increased by 5% year-over-year in 2023, driven largely by food and feed industries seeking sustainable protein sources.

This shift is also supported by regulatory developments and investments in innovation. For instance, the Canadian government allocated over CAD 60 million in 2023 toward advancing plant-based protein technologies under its Protein Industries Supercluster initiative. Such initiatives directly support upstream oilseed processors by ensuring consistent demand for raw materials and facilitating downstream value addition.

Expansion of Biodiesel Production

Another significant catalyst for the North America Oilseed Processing Market is the rapid expansion of biodiesel production, primarily driven by renewable energy mandates and carbon reduction goals. Biodiesel, derived from vegetable oils obtained through oilseed processing, serves as a cleaner alternative to petroleum diesel and is widely used in transportation and industrial applications.

In 2023, according to the U.S. Renewable Fuels Association, domestic biodiesel production reached nearly 1.9 billion gallons, marking a 6% increase compared to the previous year. Soybean oil remains the leading feedstock, accounting for over 50% of total biodiesel feedstock input in the U.S., as per the U.S. Department of Energy.

Government policies play a crucial role in sustaining this momentum. The U.S. Environmental Protection Agency’s Renewable Fuel Standard (RFS) program mandated 2.82 billion gallons of biomass-based diesel for 2023, up from 2.65 billion gallons in 2022. In parallel, Canada’s Clean Fuel Standard aims to reduce carbon intensity in transportation fuels, encouraging greater use of domestically produced biodiesel.

Moreover, private investment in bio-refineries is accelerating. Cargill and ADM have both announced multi-million-dollar expansions in their Midwest oilseed processing facilities to meet the dual demand for food-grade oils and biodiesel feedstocks.

MARKET RESTRAINTS

Volatility in Oilseed Crop Yields Due to Climate Change

One of the primary restraints affecting the North America Oilseed Processing Market is the increasing volatility in oilseed crop yields caused by climate change. Unpredictable weather patterns, prolonged droughts, and extreme temperature fluctuations are disrupting traditional growing cycles, leading to inconsistent supply and higher raw material costs.

For instance, the 2023 growing season in the Midwestern United States experienced one of the most severe droughts in the past decade, reducing soybean yields by approximately 8% compared to 2022 levels, as reported by the USDA. Similarly, in Canada, excessive rainfall in Manitoba and Saskatchewan during planting seasons led to delayed sowings and lower-than-expected canola yields, according to Statistics Canada.

These climatic disruptions not only affect the volume of available oilseeds but also lead to price instability. Such cost escalations place pressure on oilseed processors, many of whom operate on thin margins and struggle to pass these costs onto consumers or end-users.

Apart from these, changing climate conditions are influencing pest infestations and disease outbreaks. The Canola Council of Canada highlighted an uptick in clubroot and blackleg diseases in 2023, linked to warmer winters and wetter springs, further threatening yield quality and quantity.

While technological advancements in crop resilience are being pursued, the current pace of climate-induced disruptions outstrips adaptation efforts.

Regulatory and Trade Barriers Affecting Cross-Border Exports

Another major restraint impacting the North America Oilseed Processing Market is the imposition of regulatory and trade barriers that hinder cross-border exports, particularly between the U.S., Canada, and Mexico. Although the USMCA agreement replaced NAFTA to streamline trade flows, ongoing disputes and evolving regulatory standards continue to create uncertainty for exporters.

For example, in 2023, the U.S. imposed additional tariffs on certain Canadian agricultural imports, citing unfair subsidies and pricing practices. According to Global Affairs Canada, these measures led to a 6% decline in canola exports to the U.S., which historically absorbs over 90% of Canada's canola shipments. This disruption forced Canadian processors to seek alternative markets in Asia and Europe, where certification requirements and logistical complexities added time and cost to transactions.

Similarly, the U.S. International Trade Commission (ITC) conducted investigations into alleged dumping of soybean meal imports from Argentina and Brazil, potentially triggering retaliatory measures that could affect global supply chains. These actions introduce volatility in export volumes and pricing structures, making it harder for North American processors to maintain stable revenue streams.

Moreover, differences in labeling, biotechnology approvals, and phytosanitary regulations across trade partners complicate market access. The U.S. Grains Council noted that delays in regulatory approvals for genetically modified oilseed varieties in key Asian markets slowed down export opportunities in 2023.

Such trade frictions limit the ability of North American processors to capitalize on growing international demand and force them to rely more heavily on domestic markets, which may already be saturated or subject to seasonal fluctuations.

MARKET OPPORTUNITIES

Growth in Specialty Oils and Functional Ingredients

A significant opportunity emerging in the North America Oilseed Processing Market is the growing demand for specialty oils and functional ingredients derived from oilseeds. Consumers are increasingly seeking oils with enhanced nutritional profiles, such as high-oleic soybean oil and omega-3 enriched canola oil, which offer cardiovascular benefits and longer shelf life compared to conventional oils.

According to the Institute of Shortening and Edible Oils (ISEO), the U.S. market for high-oleic oils expanded by over 15% in 2023, with major foodservice operators adopting these oils to comply with trans-fat regulations and improve product quality. Companies like DuPont Pioneer and BASF have introduced proprietary oilseed strains engineered to produce oils with improved fatty acid composition, opening new avenues for premium pricing and differentiation.

According to Canada’s Agri-Food Analytics Lab reported that consumer willingness to pay a premium for heart-healthy oils rose by 18% in 2023, indicating strong market potential for next-generation oil products. This trend is supported by regulatory endorsements.

Additionally, the functional food industry is leveraging oilseed derivatives such as tocopherols, sterols, and lecithin for fortification purposes. These compounds are widely used in nutraceuticals, infant formulas, and sports nutrition products.

Oilseed processors that invest in fractionation and refining technologies stand to benefit from this shift toward value-added products, thereby enhancing profitability and diversifying revenue streams beyond commodity oils.

Integration with Circular Economy and Waste Valorization Initiatives

The North America Oilseed Processing Market is witnessing a promising opportunity through integration with circular economy principles and waste valorization initiatives. Traditionally, oilseed processing generated large volumes of by-products such as meal, hulls, and glycerin, often treated as low-value residues. However, recent innovations have enabled the transformation of these co-products into high-value inputs for various industries, including livestock feed, biochemicals, and green chemicals.

Moreover, the development of fermentation-based technologies allows processors to extract valuable compounds such as amino acids, enzymes, and organic acids from oilseed meals, enhancing their utility beyond traditional applications.

In Canada, the federal government’s Bioindustrial Innovation Canada (BIC) program funded several pilot projects aimed at converting canola meal into bioplastics and bio-based adhesives. These initiatives align with broader sustainability goals and provide processors with alternative revenue channels.

Furthermore, the push for zero-waste operations is gaining traction among major players. As per Cargill’s 2023 sustainability report, its oilseed plants in Iowa and Alberta achieved over 95% utilization rates by repurposing waste into animal feed and soil enhancers. This shift not only improves operational efficiency but also strengthens brand positioning in eco-conscious markets.

MARKET CHALLENGES

Rising Input Costs and Margin Compression

One of the foremost challenges confronting the North America Oilseed Processing Market is the persistent rise in input costs, which is compressing profit margins for processors. Key cost drivers include elevated prices for agricultural commodities, energy, transportation, and labor, all of which have surged due to inflationary pressures and supply chain bottlenecks.

According to the U.S. Bureau of Economic Analysis, agricultural input costs rose significantly in 2023 compared to the previous year, with fertilizer prices alone increasing due to geopolitical tensions and natural gas shortages. These increases directly impact farmers, who then pass on higher seed prices to processors. In turn, oilseed processors face mounting pressure to absorb these costs without significantly raising product prices, especially in competitive markets dominated by large buyers such as food manufacturers and biodiesel producers.

Transportation expenses have also escalated sharply. According to the American Trucking Associations, there was a 12% year-over-year increase in freight rates in 2023, attributed to labor shortages and rising diesel prices. For oilseed processors reliant on timely deliveries of raw materials and finished goods, these logistics costs represent a growing financial burden.

Labor costs have similarly risen. While automation is being adopted to mitigate labor dependency, initial capital expenditures remain high, limiting adoption among smaller players.

This combination of rising costs and stagnant selling prices has resulted in margin compression across the industry. Without strategic cost management or vertical integration, processors risk diminished returns and reduced capacity for innovation.

Technological Disruption and Capital Intensity of Modernization

Another critical challenge facing the North America Oilseed Processing Market is the rapid pace of technological disruption and the high capital intensity required to modernize aging processing infrastructure. While digitalization, automation, and precision agriculture are transforming the agri-processing sector, they also necessitate substantial upfront investments that many mid-sized and independent processors struggle to afford.

According to Deloitte’s 2023 Manufacturing Industry Outlook, over 60% of surveyed agri-processors identified equipment modernization as a top priority, yet only 28% had allocated sufficient capital to implement upgrades. Legacy systems in many North American oilseed mills, some dating back several decades, lack compatibility with smart technologies such as AI-driven process optimization, IoT-enabled monitoring, and predictive maintenance tools. Retrofitting these systems demands extensive engineering work and operational downtime, both of which incur additional costs.

As per the U.S. Department of Agriculture’s Economic Research Service, the average capital expenditure for upgrading a medium-sized oilseed facility exceeds $25 million, a prohibitive figure for many independent operators. Larger firms such as ADM and Bunge have made significant strides in deploying automated extraction systems and energy-efficient refining units, widening the technology gap between industry leaders and smaller competitors.

Moreover, workforce readiness poses another hurdle. The shift toward digitalized operations requires skilled personnel trained in data analytics and machine learning, areas where traditional agri-industries face talent shortages. Without adequate investment in both technology and human capital, many North American oilseed processors risk falling behind in productivity, compliance, and competitiveness—challenges that threaten their long-term viability in an increasingly sophisticated market environment.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 6.87% |

| Segments Covered | By Type, Process, Application, and Region |

|

Various Analyses Covered | Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | The United States, Canada, Mexico, and Rest of North America |

| Market Leaders Profiled | Wilmar International Ltd., Bunge Limited, Archer Daniels Midland Company, Efko Group, Louis Dreyfus Company B.V., CHS Inc, Richardson International Limited, and others |

SEGMENTAL ANALYSIS

By Type Insights

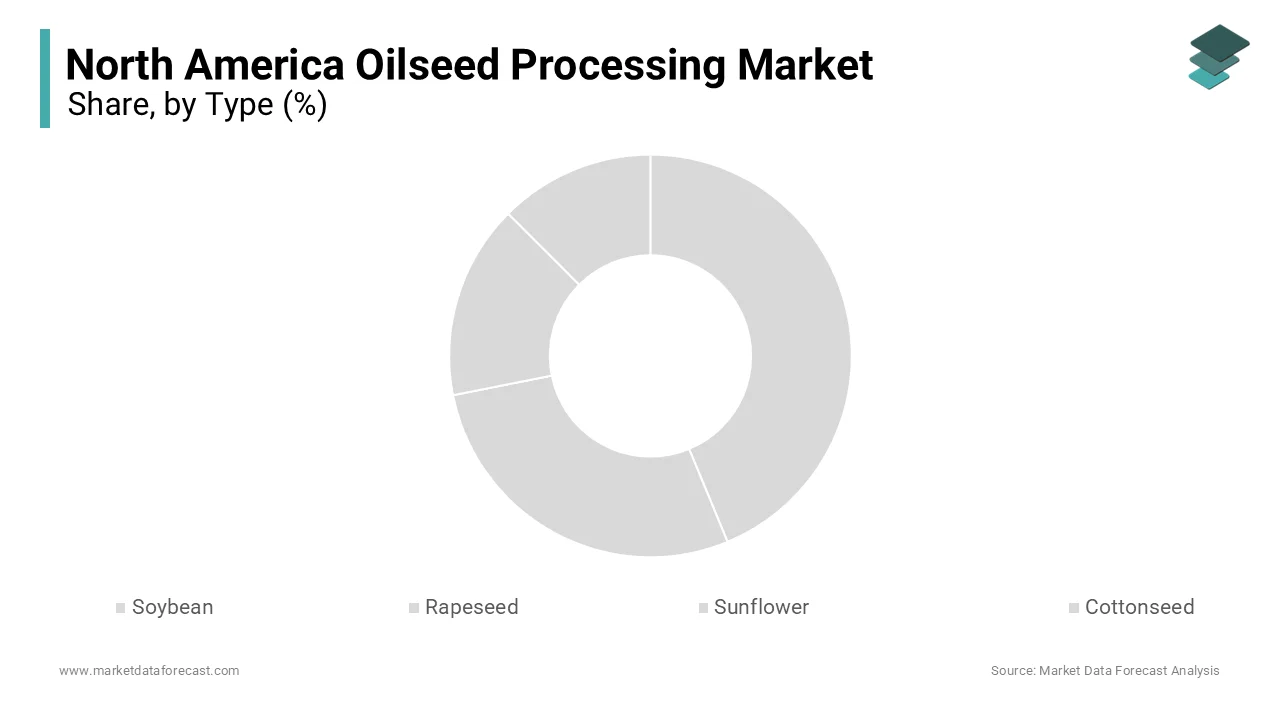

Soybean remained the largest segment in the North America Oilseed Processing Market, accounting for 62.2% of total processed oilseeds by volume in 2024.

The dominance of soybean is primarily driven by its dual utility as a source of high-protein animal feed and edible oil. According to the American Soybean Association, soybean meal constitutes nearly 70% of global protein feed demand, making it indispensable in livestock and aquaculture sectors.

Another major driver is the growing biodiesel industry, which relies heavily on soybean oil as a feedstock. This regulatory framework ensures continued demand from the energy sector, further solidifying soybean’s position as the leading oilseed in North America.

Canola (rapeseed) is emerging as the fastest-growing oilseed segment in North America, projected to expand at a CAGR of 6.8% between 2025 and 2033. Statistics Canada recorded a 7% increase in canola production in 2023 compared to the previous year, reaching over 19 million metric tons domestically, with more than 10 million metric tons processed within Canada itself.

This rapid growth is fueled by rising demand for heart-healthy oils and specialty fats. In 2023, U.S. imports of Canadian canola oil reached record levels, exceeding 1.2 billion liters, according to the U.S. Census Bureau.

Additionally, the renewable fuels sector is accelerating canola adoption. The U.S. Environmental Protection Agency (EPA) increased biomass-based diesel blending requirements under the RFS program, prompting refiners to seek non-soy alternatives. In response, Cargill and Louis Dreyfus Company expanded their canola processing facilities in Alberta and Saskatchewan, signaling strong investor confidence in this segment's long-term prospects.

By Process Insights

Mechanical processing commanded the North America Oilseed Processing Market, capturing 58.5% of total processing volume in 2024. This method, which includes pressing and expelling techniques, is widely used for initial oil extraction before further refining or chemical treatment.

One key driver of mechanical processing dominance is the growing consumer preference for cold-pressed and minimally refined oils. Apart from these, regulatory scrutiny around hexane residues from chemical solvent extraction has prompted some processors to adopt mechanical methods exclusively. As per a 2023 survey by the Organic Trade Association, 43% of organic-certified oil producers in North America relied solely on mechanical extraction to meet labeling standards, reinforcing its relevance in niche but expanding market segments.

Chemical processing is the fastest-growing segment in the North America Oilseed Processing Market, expanding at a CAGR of 7.2% through 2033. This method involves solvent extraction using hexane to maximize oil yield, followed by refining, bleaching, and deodorization steps to produce high-purity oils suitable for commercial food and industrial applications.

A primary factor behind its rapid growth is the efficiency gains it offers in high-volume production environments. Moreover, advancements in solvent recovery systems and environmental controls have mitigated earlier concerns about emissions.

By Application Insights

Animal feed remained the biggest application segment in the North America Oilseed Processing Market, accounting for 45.2% of total processed output in 2024. The primary product derived from this segment is soybean meal, which serves as a rich protein supplement in livestock, poultry, and aquaculture diets.

According to the Canadian Food Inspection Agency (CFIA), there were similar trends with more than 7 million metric tons of canola meal were utilized in animal feed formulations in 2023, predominantly in dairy and swine rations.

One key driver of this dominance is the increasing demand for meat and dairy products across North America. The USDA Economic Research Service indicated that U.S. per capita meat consumption rose in 2023, necessitating greater feed production to support intensive farming operations.

In addition, the nutritional profile of oilseed meals—high in lysine, methionine, and other essential amino acids—makes them indispensable in balanced animal nutrition. The University of Guelph’s Animal Nutrition Research Group emphasized in 2023 that replacing soybean meal with alternative proteins often results in reduced weight gain and lower feed conversion ratios, reinforcing its continued reliance in commercial feed mills.

Industrial applications are the fastest-growing segment in the North America Oilseed Processing Market, expanding at a CAGR of 8.1%. This category encompasses uses such as bio-lubricants, surfactants, coatings, and biodegradable polymers derived from oilseed-based triglycerides and fatty acids.

Companies like BASF, Arkema, and DuPont are increasingly incorporating oilseed derivatives into green chemistry solutions to replace petroleum-based compounds.

A key driver of this growth is the tightening of environmental regulations aimed at reducing carbon footprints and hazardous waste. Furthermore, the rise of sustainable aviation fuels (SAFs) and renewable diesel has spurred interest in oilseed-derived feedstocks.

REGIONAL ANALYSIS

United States

The United States led the North America Oilseed Processing Market with a dominant share of 65.2% in 2024. As the world’s largest producer and exporter of soybeans, the U.S. plays a central role in shaping the region’s oilseed dynamics. According to the U.S. Department of Agriculture (USDA), the country harvested over 120 million metric tons of soybeans in 2023, with a large portion of this volume undergoing crushing and refining.

The U.S. market is supported by a well-established infrastructure of oilseed processing plants, concentrated largely in the Midwest Corn Belt states such as Iowa, Illinois, and Nebraska. Major agribusiness firms including ADM, Bunge, and Cargill operate extensive processing networks that supply both domestic and international markets with edible oils, protein meals, and biodiesel feedstocks.

Government policies such as the Renewable Fuel Standard (RFS) continue to bolster demand for soybean oil in the biofuels sector. The U.S. Energy Information Administration (EIA) reported that biodiesel production exceeded 1.9 billion gallons in 2023, with soybean oil accounting for over 50% of total feedstock input.

Besides, the expansion of plant-based protein markets has reinforced the need for high-quality soybean meal. These factors collectively underline the U.S.’s entrenched leadership in the regional oilseed processing landscape.

Canada

Canada is globally recognized as the largest producer and exporter of canola, which forms the backbone of its oilseed industry. The Canadian oilseed sector benefits from strategic government investments aimed at enhancing value-added processing capabilities. The Protein Industries Supercluster initiative, funded with over CAD 230 million in public-private investment, has accelerated innovation in canola-based protein and oil extraction technologies. This has enabled processors to develop premium products tailored for functional foods, nutraceuticals, and industrial applications.

Another critical driver is the country’s expanding renewable diesel industry. Natural Resources Canada reported that domestic biodiesel consumption grew by 9% in 2023, with canola oil emerging as a preferred feedstock due to its low cloud point and compatibility with cold climate conditions.

Exports remain a cornerstone of Canada’s oilseed economy. With ongoing investments in logistics and biorefinery upgrades, Canada continues to strengthen its competitive edge in the North American oilseed value chain.

Rest of North America

The Rest of North America, comprising Mexico and Central American territories, holds a modest but growing share of the regional oilseed processing market. While not a major oilseed producer like the U.S. or Canada, Mexico plays a pivotal role as a key importer and processor of soybean and cottonseed oils to meet domestic food and industrial needs.

According to Mexico’s Secretaría de Agricultura y Desarrollo Rural (SADER), the country imported over 6 million metric tons of soybeans in 2023, primarily from the U.S., to support its expanding edible oil refining sector.

A notable development is the debate surrounding genetically modified (GM) soybean imports. The Mexican government’s temporary suspension of GM soybean permits in early 2023 led to supply chain disruptions and price volatility, highlighting the sensitivity of this market to policy shifts.

Despite these challenges, the country’s proximity to the U.S. and participation in the USMCA trade agreement provide logistical advantages. As North American integration deepens, Mexico’s role as a downstream processing hub is expected to grow, albeit from a smaller base compared to its northern neighbors.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Key players in the North America Oilseed Processing Market are Wilmar International Ltd., Bunge Limited, Archer Daniels Midland Company, Efko Group, Louis Dreyfus Company B.V., CHS Inc, and Richardson International Limited

The competition in the North America Oilseed Processing Market is characterized by a highly consolidated structure dominated by a few large multinational corporations that control significant shares of production, distribution, and innovation. These firms leverage economies of scale, well-established supply chains, and advanced processing technologies to maintain their market positions. However, mid-sized regional processors also play a vital role, especially in niche segments such as organic or specialty oils, where localized operations offer flexibility and responsiveness to consumer preferences. The market is marked by ongoing investments in facility modernization, product diversification, and sustainability initiatives aimed at differentiating offerings and meeting regulatory expectations. Strategic acquisitions and joint ventures are frequently used tools to expand capabilities and geographic reach. Additionally, companies are increasingly aligning their operations with environmental, social, and governance (ESG) goals to appeal to conscious consumers and institutional investors alike. The interplay between these factors creates a dynamic yet fiercely competitive environment, where technological advancement and supply chain resilience are key differentiators among market participants.

TOP PLAYERS IN THE MARKET

Archer Daniels Midland Company (ADM)

ADM is a global leader in agricultural processing and one of the most influential players in the North America Oilseed Processing Market. The company operates an extensive network of oilseed crushing and refining facilities across the United States, handling soybeans, canola, and other oilseeds at industrial scale. ADM plays a crucial role in supplying edible oils, protein meals, and biofuel feedstocks to both domestic and international markets. Its vertically integrated model ensures control over sourcing, processing, and distribution, allowing it to respond efficiently to market demands. The company also invests heavily in innovation, particularly in sustainable extraction methods and value-added products, reinforcing its leadership position in the global agri-processing industry.

Cargill Incorporated

Cargill is a dominant force in the North American oilseed sector, with a vast footprint in soybean and canola processing. The privately held corporation manages numerous processing plants across key agricultural regions, ensuring a steady supply of oils and meals for food, feed, and industrial applications. Cargill’s strength lies in its integration across the supply chain—from farm to end-user—allowing it to optimize production efficiency and mitigate risks. The company emphasizes sustainability and digital transformation, incorporating advanced technologies to enhance yield and reduce environmental impact. With its strong presence in export markets and strategic partnerships, Cargill significantly influences global trade flows and pricing dynamics in the oilseed industry.

Bunge Limited

Bunge has a long-standing presence in the North American oilseed processing landscape, playing a pivotal role in transforming raw commodities into essential food and energy products. The company's operations span oilseed crushing, refining, and packaging, serving diverse sectors including food manufacturing, livestock feed, and renewable fuels. Bunge leverages its deep market insights and logistical expertise to maintain competitiveness in a dynamic industry. The company actively engages in sustainability initiatives, aiming to source responsibly and reduce carbon emissions from processing activities. Through continuous investment in infrastructure and technology upgrades, Bunge strengthens its position as a key contributor to both regional and global oilseed markets.

TOP STRATEGIES USED BY KEY PLAYERS

One of the primary strategies employed by leading players in the North America Oilseed Processing Market is vertical integration. Companies are expanding their reach across the supply chain by acquiring upstream farms, logistics networks, and downstream refining and packaging units. This approach enhances operational control, stabilizes raw material supply, and improves cost efficiencies.

Another critical strategy is investing in sustainable and innovative processing technologies. Major players are adopting cleaner extraction methods, implementing energy-efficient systems, and developing high-value co-products such as functional oils and plant-based proteins to meet evolving consumer and regulatory demands.

Lastly, strengthening global market presence through strategic partnerships and exports is a key focus area. Companies are forming alliances with international buyers, securing long-term contracts, and establishing export hubs to capitalize on growing demand in Asia-Pacific and Europe, thereby reinforcing their competitive edge in the global oilseed industry.

RECENT HAPPENINGS IN THE MARKET

- In January 2023, ADM announced the expansion of its canola crushing facility in Regina, Canada, to increase capacity and meet rising demand for plant-based oils and biodiesel feedstock.

- In May 2023, Cargill launched a new line of high-oleic canola oil designed for foodservice applications, emphasizing improved frying performance and heart health benefits.

- In September 2023, Bunge entered into a strategic partnership with a European biotech firm to develop enzymatic oil refining processes that reduce chemical usage and improve sustainability.

- In February 2024, ADM acquired a specialty oils business from a European manufacturer, enhancing its portfolio of premium oils for the North American market.

- In June 2024, Cargill unveiled a major investment in digital monitoring systems across its U.S. oilseed processing plants to optimize efficiency and reduce downtime through predictive maintenance.

North America Oilseed Processing Market Result

In April 2024, DynaTouch, a kiosk solutions provider, acquired KioWare, a kiosk management software company. This acquisition is anticipated to allow DynaTouch to offer more comprehensive kiosk solutions and strengthen their market presence.

MARKET SEGMENTATION

This research report on the North America oilseed processing market has been segmented and sub-segmented based on the following categories.

By Type

- Soybean

- Rapeseed

- Sunflower

- Cottonseed

By Process

- Introduction

- Mechanical

- Chemical

By Application

- Introduction

- Food

- Feed

- Industrial

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

1. What is the current market size of the North America oilseed processing market?

The North America oilseed processing market was valued at USD 89.96 million in 2024.

2. What is the projected North America oilseed processing market size by 2033?

The North America oilseed processing market is expected to reach USD 163.59 million by 2033.

3. What factors are driving the growth of the oilseed processing market in North America?

Rising demand for vegetable oil, protein-rich feed, and processed food is driving market growth.

4. Which oilseeds are predominantly processed in this market?

Soybean, canola, sunflower, and cottonseed are among the major oilseeds processed.

5. What trends are shaping the oilseed processing market?

Trends include the adoption of mechanical and chemical extraction methods and sustainable processing.

6. Which industries benefit most from processed oilseeds?

The food, animal feed, and biodiesel sectors are the primary end-users of processed oilseeds.

7. What are the major challenges in this market?

Challenges include high energy costs, environmental regulations, and supply chain fluctuations.

8. Are there opportunities for innovation in this market?

Yes, innovations in enzyme-assisted extraction and eco-friendly solvents present growth opportunities.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com