Global Naval Vessels Market Size, Share, Trends, & Growth Forecast Report, Segmented By Vessel Type (Corvettes, Destroyers, Aircraft Carriers, Frigates, Submarines, and Other Vessel Types), & Region, Industry Forecast From 2026 to 2034

Market Size, 2025

$121.34 BnMarket Estimate, 2026

$137.54 BnMarket Forecast, 2034

$374.80 BnCAGR, 2026–2034

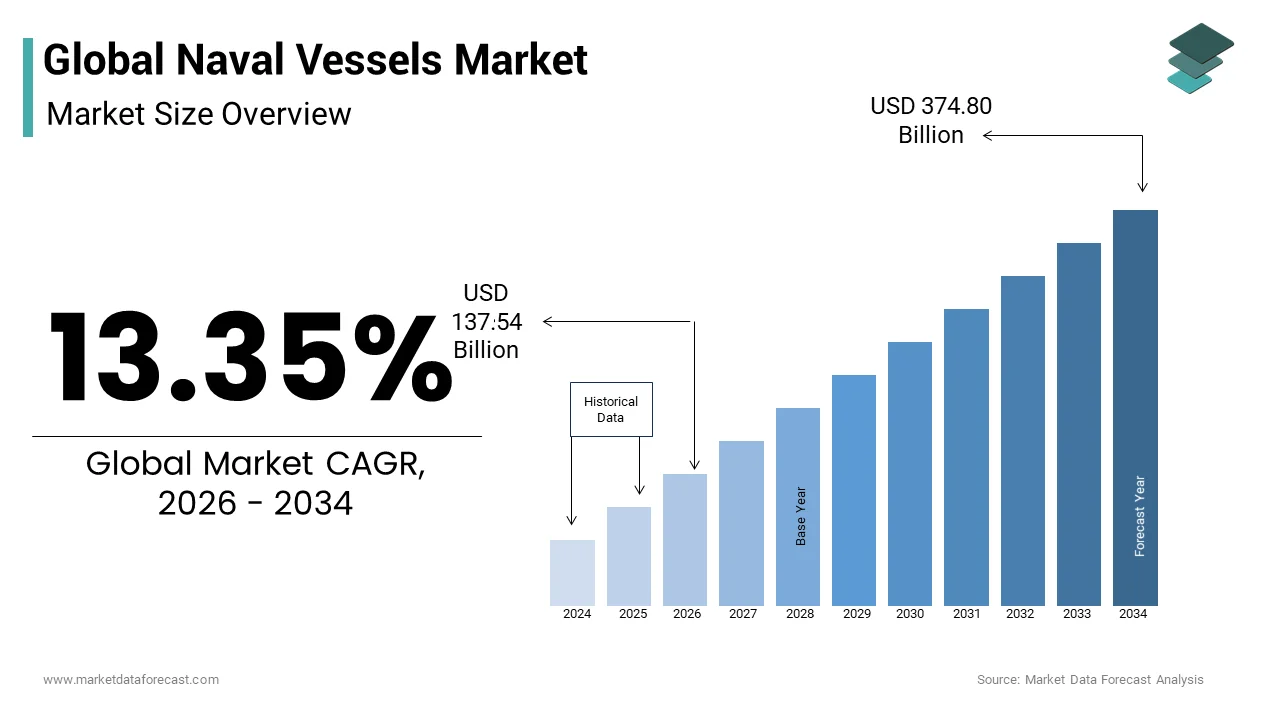

13.35%Global Naval Vessels Market Size

The global naval vessels market size was valued at USD 121.34 billion in 2025 and is anticipated to reach USD 137.54 billion in 2026 to reach USD 374.80 billion by 2034, growing at a CAGR of 13.35% during the forecast period from 2026 to 2034.

Naval vessels are built to fight in wars and belong to a country's naval forces. According to the analysis, they are significantly faster, safer, and more user-friendly than merchant ships and are essential to their naval force. Countries have spent billions of dollars improving and expanding their naval vessels due to a growing focus on having more power over the sea and an ever-increasing military budget. For example, after signing a new enhanced security alliance with the United Kingdom and the United States, AUKUS, Australia has announced several major naval projects, including the construction of at least eight nuclear-powered submarines. These are worth almost billions of dollars. In addition, starting in 2024, the Australian government would spend up to $5.1 billion on enhancements to Osborne's Hobart-class destroyer combat management system.

MARKET DRIVERS

The major factors include increasing piracy, smuggling, terrorism, and defense expenditure, and conflicts among the regions that are responsible for propelling the global naval vessels market forward.

Governments have spent billions of dollars on improving and expanding their naval fleets due to a growing focus on having more power over the sea and an ever-increasing military budget. An essential part of international trade and the global economy is naval vessels. During the projected period for the worldwide naval vessel industry, an increase in seaborne trade is expected to fuel market expansion. According to Naval Publications, about 80% of global trade by volume and over 70% of global trade by value is carried out by sea, with ports throughout the world controlling it. Globalization and the rapid expansion of Asian countries such as China and South Korea will significantly influence the development of naval trade.

MARKET RESTRAINTS

However, the naval vessels market's growth is restricted by high manufacturing costs. Globally, large sums of money are being spent on expanding and upgrading the current naval fleet. Naval vessels are also used in disaster relief and humanitarian assistance operations, in addition to offensive actions.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 13.35% |

| Segments Covered | By Type, and Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview on Investment Opportunities |

| Regions Covered | North America, Europe, APAC, Latin America, Middle East & Africa |

| Market Leaders Profiled | General Dynamics Corporation, BAE Systems plc, Naval Group, Hyundai Heavy Industries Co., Ltd., Huntington Ingalls Industries, Inc., ThyssenKrupp AG, The Naval Group, Abu Dhabi Ship Building Co., Kawasaki Heavy Industries, Fincantieri, and others |

SEGMENTAL ANALYSIS

By Type Insights

Based on type, the aircraft carrier segment is predicted to hold the largest naval vessels market share. Aircraft carriers are the largest vessels in the naval force because they require a huge deck space. In addition, aircraft carriers require defensive capabilities to protect the numerous aircraft and crew on board. The Gerald R Ford class and the Type 001A class are two new aircraft carriers developed by the United States and China. Gerald R Ford's first vessel was commissioned in July 2017 and will be deployed by 2022. This aircraft carrier can carry more than 75 aircraft, while the USS Enterprise and USS John F Kennedy, two future aircraft carriers, will carry up to 90 combat aircraft. However, due to technological advancements and the growing popularity of smaller naval vessels like frigates and corvettes, the market for aircraft carriers is likely to rise modestly throughout the forecast period.

The Destroyers segment is anticipated to have a significant CAGR in the upcoming years. The destroyers' advantages, such as their speed, mobility, and long endurance, allow them to effectively escort and defend larger vessels in a fleet, convoy, or battle group against smaller, more potent short-range attackers. As a result, destroyers are currently in higher demand than other naval vessels, as numerous nations seek to purchase new destroyer ships.

REGIONAL ANALYSIS

North America region will be the fastest-growing naval vessels market during the forecast period. There are approximately 490 ships in the US Navy's active and reserve fleets, with about 90 more in the planning and ordering stages or under construction. The Navy and the Department of Defense have been working toward a more spread fleet architecture with fewer large ships, more small ships, and a new third level of huge unmanned vehicles. The Navy has been working on force structure growth plans, intending to reach 355 ships by FY 2034 through a combination of service life extensions and new construction. The US Navy's five-year shipbuilding plan includes 42 additional ships, down from 55 in the previous five-year plan. In addition, the guided-missile destroyer DDG-118, Daniel Inouye, will join the guided-missile destroyer fleet.

The Asia-Pacific region is predicted to dominate the naval vessels market during the forecast period. As conflicts between nations in the region have risen, countries have increased their military spending and naval fleets, likely driving the region's naval vessels market growth throughout the forecast period. South Korea, Australia, India, China, and Indonesia are among the countries in the region spending heavily in the development, construction, and procurement of modern naval vessels.

RECENT MARKET NEWS

-

September 20, 2021, despite the launch of AUKUS, a new enhanced security collaboration between Australia, the United Kingdom, and the United States, many naval projects have been confirmed for South Australia. The partnership's initial project is to purchase nuclear-powered submarines for Australia, manufactured in South Australia. Moreover, starting in 2024, the Australian government would spend up to $5.1 billion on enhancements to Osborne's Hobart-class destroyer combat management system.

-

Hyundai Heavy Industries (HHI) and Daewoo Shipbuilding & Marine Engineering jointly launched the ROKS Cheonan, the seventh Daegu-class frigate, on November 9, 2021. The Daegu class was developed from the older Incheon class to replace the outdated Ulsan class frigates and Pohang corvettes and has been in service since 2018. A total of 8 vessels are in the works. The Daegu Class has a displacement of 2,800 tonnes, is 122 meters long, 14 meters wide, and has a top speed of 30 knots. The K-SAAM, Hong Sang Eo anti-submarine missile, and Haeryong tactical ground attack cruise missile can all be launched from its 16-cell Korean Vertical Launch System. 4 naval gun systems and a Phalanx Block 1B Close-In Weapons System are also installed on the Daegu class.

KEY MARKET PLAYERS

These are the market players that are dominating the global naval vessels market.

- General Dynamics Corporation

- BAE Systems plc

- Naval Group

- Hyundai Heavy Industries Co., Ltd.

- Huntington Ingalls Industries, Inc.

- ThyssenKrupp AG

- The Naval Group

- Abu Dhabi Ship Building Co.

- Kawasaki Heavy Industries

- Fincantieri

MARKET SEGMENTATION

This research report on the global naval vessels market has been segmented and sub-segmented based on type and region.

By Type

- Corvettes

- Destroyers

- Aircraft Carriers

- Frigates

- Submarine

- Others

By Region

- North America

- Asia-Pacific

- Europe

- Latin America

- Middle-East-America

Frequently Asked Questions

What is driving the growth of the global naval vessels market?

The global naval vessels market is growing due to increasing defense budgets, rising maritime security concerns, and ongoing naval fleet modernization programs. Governments are investing in advanced warships, submarines, aircraft carriers, patrol vessels, and unmanned naval platforms to strengthen national defense capabilities, protect maritime trade routes, and address evolving geopolitical challenges.

Which types of naval vessels account for the largest share of the global naval vessels market?

Destroyers, frigates, submarines, aircraft carriers, corvettes, amphibious assault ships, offshore patrol vessels (OPVs), and mine countermeasure vessels represent major segments of the global naval vessels market. Demand varies by country based on defense priorities, coastal security requirements, and investments in blue-water naval capabilities.

What are the key trends shaping the global naval vessels market?

Key trends in the global naval vessels market include the adoption of autonomous and unmanned surface vessels, integration of advanced radar and combat management systems, hybrid and electric propulsion technologies, AI-enabled surveillance, and digital shipbuilding. Countries are also emphasizing multi-mission naval platforms that offer enhanced operational flexibility and long-term cost efficiency.

Which regions are leading the global naval vessels market?

North America, Europe, and Asia Pacific are the leading regions in the global naval vessels market. The United States maintains one of the world's largest naval fleets, while China and India continue to expand their naval capabilities. European nations are also increasing investments in fleet modernization and maritime defense to enhance regional security and NATO readiness.

What is the future outlook for the global naval vessels market?

The global naval vessels market is expected to witness sustained growth over the forecast period, driven by increasing investments in next-generation naval platforms, rising demand for maritime surveillance, and expanding defense procurement programs. Technological advancements in stealth capabilities, autonomous operations, cybersecurity, and integrated combat systems are expected to create significant growth opportunities for shipbuilders and defense contractors worldwide.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2500

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com