North America Bitumen Market Size, Share, Trends & Growth Forecast Report By Product Type (Paving Grade Bitumen, Polymer Modified Bitumen (PMB)), Application, And Country (US, Canada, And Rest Of North America), Industry Analysis From 2025 To 2033

North America Bitumen Market Size

The North American bitumen Market size was calculated to be USD 33.60 million in 2024 and is anticipated to be worth USD 42.42 million by 2033, from USD 34.48 million in 2025, growing at a CAGR of 2.62% during the forecast period.

The North America bitumen market refers to the production, refining, distribution, and utilization of bitumen—also known as asphalt—a highly viscous petroleum-derived binder used primarily in road construction, roofing materials, and waterproofing applications. As a crucial component of asphalt concrete, bitumen is essential for paving highways, urban roads, airport runways, and parking lots across the United States and Canada.

According to the U.S. Energy Information Administration (EIA), the United States consumes over 28 million tons of bitumen annually, with road construction accounting for more than 85% of total usage. In Canada, Natural Resources Canada reports that the country produces approximately 18 million barrels of bitumen per year, largely sourced from oil sands in Alberta, making it one of the largest producers globally.

As per the Federal Highway Administration (FHWA), the U.S. has over 4 million miles of public roads, with an increasing need for maintenance, rehabilitation, and expansion projects. The Canadian Asphalt Pavement Association (CAPA) also highlights a growing focus on sustainable pavement technologies that integrate recycled bitumen and modified binders to enhance durability and reduce environmental impact. Moreover, the rise in infrastructure investments under federal initiatives such as the U.S. Infrastructure Investment and Jobs Act is expected to boost demand for bitumen in the coming decade.

MARKET DRIVERS

Rising Infrastructure Development and Road Construction Activities

One of the primary drivers of the North America bitumen market is the continuous investment in infrastructure development and road construction projects across both the United States and Canada. Government agencies at federal, state, and provincial levels are prioritizing transportation network upgrades to accommodate growing populations, freight movement, and aging infrastructure.

According to the American Road & Transportation Builders Association (ARTBA), over 4,000 major roadway projects were underway in the U.S. in 2023, representing a significant demand for bitumen-based asphalt mixes.

In Canada, Infrastructure Canada announced that the Investing in Canada Plan allocated over CAD 30 billion through 2023 for transportation and municipal infrastructure, including highway resurfacing and rural road upgrades. With increasing emphasis on cost-effective and durable surfacing solutions, bitumen remains a preferred material due to its flexibility, waterproofing properties, and compatibility with recycled content.

Expansion of Oil Sands Production and Domestic Supply Chains

A significant driver fueling the growth of the North American bitumen market is the expanding production of oil sands, particularly in Canada, which serves as a major source of raw bitumen for both domestic consumption and export. Unlike conventional crude oil, oil sands yield bitumen as a primary output, supporting downstream industries such as road paving and industrial coatings. According to Natural Resources Canada, oil sands production reached record levels in 2023, with Alberta alone contributing over 90% of national output. This abundant supply ensures competitive pricing and availability for domestic refineries and asphalt plants, reinforcing the economic viability of bitumen-based products. States like Texas, California, and Michigan have ramped up road resurfacing efforts, leveraging imported and domestically produced bitumen to meet rising demand. Additionally, regional refining capacity improvements and strategic stockpiling by government agencies have enhanced supply chain resilience.

MARKET RESTRAINTS

Environmental Regulations and Pressure to Reduce Carbon Emissions

A key restraint affecting the North American bitumen market is the tightening of environmental regulations aimed at reducing carbon emissions associated with fossil fuel extraction and asphalt production. Both the U.S. Environmental Protection Agency (EPA) and Environment and Climate Change Canada (ECCC) have introduced policies that scrutinize emissions from bitumen processing and asphalt manufacturing facilities. According to the International Energy Agency (IEA), asphalt production contributes significantly to greenhouse gas emissions, prompting calls for cleaner alternatives such as cold mix asphalt and bio-bitumen. Several U.S. states, including California and New York, have implemented low-carbon procurement guidelines that discourage excessive reliance on traditional bitumen sources. In Canada, the Clean Fuel Standard (CFS) introduced in 2023 mandates lower lifecycle emissions for petroleum-derived products, impacting bitumen suppliers and refiners. As per the Pembina Institute, compliance costs for bitumen producers have risen by an estimated 12%, pushing some firms to explore alternative formulations or invest in carbon capture technologies.

Volatility in Crude Oil Prices and Input Costs

Another critical constraint influencing the North American bitumen market is the fluctuating price of crude oil and related feedstocks, which directly impacts bitumen production costs and end-user affordability. Since bitumen is derived from crude oil refining and oil sands processing, any instability in upstream markets translates into uncertainty for downstream consumers such as contractors and municipalities. According to the U.S. Energy Information Administration (EIA), crude oil prices experienced a 20% increase in 2023 due to global geopolitical tensions and supply disruptions, leading to higher bitumen procurement costs for local governments and private construction firms. Municipalities in Ontario and British Columbia faced delays in planned resurfacing projects due to budget constraints linked to bitumen price surges. These fluctuations create challenges for procurement planning and contract bidding, discouraging long-term commitments from end-users.

MARKET OPPORTUNITIES

Growth in Sustainable and Recycled Bitumen Applications

An emerging opportunity for the NortAmericanca bitumen market lies in the increasing adoption of sustainable and recycled bitumen applications that align with evolving environmental policies and circular economy principles. Governments and industry stakeholders are promoting the use of reclaimed asphalt pavement (RAP) and warm-mix asphalt technologies that reduce energy consumption and emissions during production. The association emphasizes that incorporating RAP into new asphalt mixtures reduces dependency on virgin bitumen while lowering material costs and landfill waste. In Canada, the Canadian Asphalt Pavement Association (CAPA) estimates that more than 80% of asphalt mixtures now contain recycled components, supported by provincial incentives encouraging green procurement practices. This shift toward sustainable infrastructure is creating new revenue streams for bitumen producers who can adapt their operations to support eco-friendly formulations, positioning recycled and modified bitumen as a high-growth segment within the broader market.

Expansion of Industrial and Non-Road Applications

A significant opportunity shaping the future of the NorAmericanica bitumen market is the growing use of bitumen beyond road construction, including in industrial applications such as roofing membranes, waterproofing systems, and pipeline insulation. These non-road uses offer diversified revenue channels and reduced exposure to seasonal construction cycles. The organization notes that demand has grown steadily as building codes increasingly favor fire-resistant and thermally stable roofing solutions. So, with continued investment in housing, industrial parks, and infrastructure renewal, bitumen manufacturers are diversifying product lines to cater to these niche yet rapidly expanding segments, offering resilience against road sector slowdowns.

MARKET CHALLENGES

Increasing Adoption of Alternative Paving Materials

A major challenge facing the North American bitumen market is the growing interest in alternative paving materials such as polymer-modified concrete, permeable pavers, and synthetic binders designed to enhance durability and reduce environmental impact. These substitutes are gaining traction among urban planners and developers seeking longer-lasting and more sustainable surfacing options. According to the Portland Cement Association (PCA), concrete pavements saw a 10% increase in adoption for new interstate projects in 2023, particularly in states where extreme temperature variations affect bitumen performance. The PCA attributes this trend to improved life-cycle assessments and rising public funding for cement-based roadways. Also, pilot programs exploring rubberized asphalt and geopolymer composites have gained traction in environmentally conscious regions.

Aging Refining and Processing Infrastructure

An additional challenge confronting the North American bitumen market is the aging refining and processing infrastructure, which affects supply chain efficiency, product consistency, and environmental compliance. Many refineries and terminals that process bitumen into usable forms are operating with outdated equipment, leading to bottlenecks and quality control issues. According to the American Petroleum Institute (API), a significant share of U.S. refineries involved in bitumen processing are more than 40 years old, raising concerns about reliability and maintenance costs. Pipeline constraints and refinery outages have occasionally led to localized shortages, delaying road construction timelines and increasing procurement risks.

Regulatory Scrutiny and Permitting Delays for Extraction Projects

A major challenge affecting the NortAmericanca bitumen market is the increasing regulatory scrutiny and permitting delays for sand extraction and crude refining projects, particularly in Canada. Environmental groups and policymakers have raised concerns over the ecological footprint of bitumen mining, leading to prolonged approval processes and stricter operational conditions.

According to the Pembina Institute, new oil sands projects in Alberta have seen approval times extend beyond five years due to environmental impact assessments and Indigenous consultation requirements. In the U.S., the Bureau of Land Management (BLM) has imposed tighter restrictions on federal land drilling activities, indirectly affecting bitumen supply chains reliant on domestic crude oil. The Sierra Club and other advocacy groups have actively opposed expansion projects, citing groundwater contamination and habitat disruption as key concerns.

Seasonal Demand Fluctuations and Project Execution Constraints

An additional challenge confronting the NortAmericanca bitumen market is the pronounced seasonality of road construction and paving activity, which results in uneven demand patterns throughout the year. Bitumen consumption peaks during summer months when paving is optimal, leading to inventory management complexities and supply chain inefficiencies. These delays disrupt procurement planning and strain relationships between suppliers and government agencies. These cyclical demand patterns make it difficult for bitumen suppliers to maintain steady cash flows and justify long-term investments in logistics and storage.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

2.62% |

|

Segments Covered |

By Product Type, Application, And Region |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

Us, Canada, and Athe and Rest of North America |

|

Market Leaders Profiled |

ExxonMobil Corporation, Shell plc, BP p.l.c., Chevron Corporation, TotalEnergies SE, Valero Energy Corporation, Marathon Petroleum Corporation, Suncor Energy Inc., Imperial Oil Limited, Athabasca Oil Corporation, Syncrude Canada Ltd., NuStar Energy L.P., Nynas AB, China Petroleum & Chemical Corporation (Sinopec), Indian Oil Corporation Ltd., Petróleos Mexicanos (Pemex), Bouygues S.A., Gazprom Neft, ENEOS Corporation, JX Nippon Oil & Energy Corporation, Villas Austria GmbH, Koch Industries (Flint Hills Resources), Husky Energy, McAsphalt Industries, Owens Corning. |

SEGMENTAL ANALYSIS

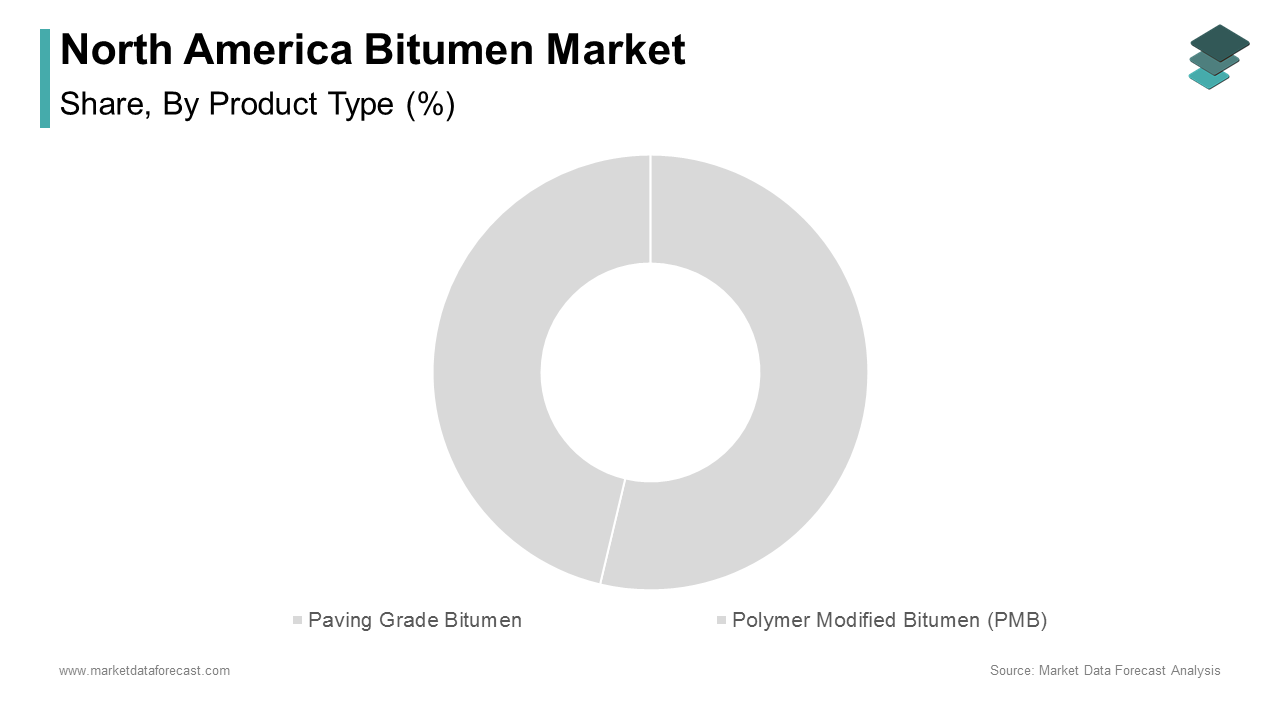

By Product Type Insights

Paving grade bitumen represented the largest segment in the North American bitumen market by capturing an estimated 45% of the total market share in 2024. This dominance is primarily attributed to its extensive use in asphalt mixtures for road construction and maintenance activities across both the United States and Canada. According to the Federal Highway Administration (FHWA), over 90% of all paved roads in the U.S. are surfaced with asphalt concrete, which relies heavily on paving grade bitumen as a binder.

The polymer-modified bitumen (PMB) segment is projected to grow at the fastest rate within the North American bitumen market, expanding at a CAGR of 7.6%. This accelerated growth is driven by increasing demand for high-performance asphalt binders capable of withstanding extreme weather conditions, heavy traffic loads, and prolonged service life requirements. According to the National Asphalt Pavement Association (NAPA), PMB usage in highway surfacing increased in 2023 compared to the previous year, particularly in high-traffic corridors and urban centers where road degradation is a persistent challenge. The association highlights that states like Texas, California, and Florida have adopted PMB extensively due to its superior resistance to rutting and thermal cracking.

By Application Insights

Road construction accounted for the largest application segment in the North American bitumen market representing approximately 83.5% of total consumption in 2024. This overwhelming dominance is attributed to the vast extent of paved road networks and continuous investment in road maintenance, expansion, and rehabilitation projects. As per the U.S. Department of Transportation, the nation has over 4 million miles of public roads, with approximately 2.3 million miles being paved surfaces. Additionally, the adoption of sustainable paving practices—such as warm mix asphalt and recycled asphalt pavement (RAP)—continues to support bitumen demand.

The waterproofing segment is coming out as the swiftest rising application area for bitumen in North America, expanding at a CAGR of 6.8% between 2024 and 2030. This development is fueled by increasing demand for durable, moisture-resistant building materials in residential, commercial, and industrial construction sectors. With continued urbanization and climate-driven infrastructure resilience planning, the waterproofing segment is poised for sustained growth, offering bitumen producers a strategic avenue beyond traditional road applications.

REGIONAL ANALYSIS

The United States had the dominant position in the North American bitumen market, capturing an estimated 62.1% of total regional consumption in 2024. This is underpinned by a massive road infrastructure network, significant domestic refining capacity, and robust government spending on transportation modernization. The passage of the Infrastructure Investment and Jobs Act (IIJA) in 2021 has allocated nearly $110 billion for road and bridge upgrades through 2026, directly boosting bitumen demand. Moreover, the U.S. Geological Survey (USGS) notes that domestic crude oil refining supports a stable supply of bitumen feedstock, reducing dependency on imports despite rising environmental scrutiny. States such as Texas, California, and Michigan have ramped up road resurfacing efforts, leveraging both domestically produced and imported bitumen to meet project deadlines.

Canada's positioning reflects the country’s status as one of the world’s leading bitumen producers, particularly from oil sands in Alberta, which fuels both domestic use and export markets. A significant portion of this output is processed into paving-grade bitumen used in highway resurfacing and municipal road projects. Provinces like Ontario, Quebec, and British Columbia have implemented green procurement policies encouraging the use of modified bitumen to extend pavement life and reduce lifecycle costs. Furthermore, Environment and Climate Change Canada (ECCC) highlighted that climate adaptation strategies have led to increased use of high-performance bitumen in flood-prone regions.

The remaining North American countries, including Mexico and select Caribbean territories, collectively hold around notable share of the regional bitumen market in 2024. Though smaller in scale, these markets are gradually gaining traction due to cross-border trade agreements, improving road infrastructure, and rising foreign direct investment in transport development. While still a minor contributor to the overall market, this segment presents long-term potential for established players seeking geographic diversification and new consumer bases beyond traditional North American markets.

LEADING PLAYERS IN THE NORTH AMERICA BITUMEN MARKET

Suncor Energy Inc.

Suncor Energy plays a pivotal role in the North American bitumen market through its integrated oil sand operations and downstream refining capabilities. As one of Canada’s largest petroleum producers, Suncor supplies raw and refined bitumen for both domestic consumption and export markets. The company has invested heavily in upgrading processing technologies to improve yield efficiency and environmental performance, aligning with evolving sustainability standards. Globally, Suncor contributes to shaping responsible oil sands development by participating in industry forums and advocating for carbon-neutral extraction pathways, reinforcing Canada's position as a major bitumen supplier.

Imperial Oil Limited (ExxonMobil Subsidiary)

Imperial Oil is a key player in the North American bitumen market, leveraging its extensive upstream and downstream infrastructure to supply high-quality bitumen products for road construction and industrial applications. With deep integration into ExxonMobil’s global supply chain, the company ensures consistent product quality and availability across major transportation corridors in Canada and the northern United States. Imperial Oil also supports research initiatives aimed at improving asphalt durability and reducing emissions during bitumen production. Its long-standing presence in the energy and infrastructure sectors enhances its influence on regional bitumen pricing and technical specifications used across the continent.

Valero Energy Corporation

Valero Energy is a leading refiner supplying processed bitumen to road paving and roofing industries throughout North America. Through its asphalt and heavy oil refining divisions, Valero delivers essential bitumen grades that meet stringent performance requirements set by state and provincial agencies. The company's strategic focus on expanding refining capacity and integrating sustainable practices has positioned it as a reliable supplier in both urban and rural infrastructure projects. On the global stage, Valero contributes to advancing cleaner refining techniques and participates in international discussions regarding alternative binders and low-carbon paving solutions, strengthening North America’s leadership in bitumen innovation.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players in the North American bitumen market is investing in refining and processing upgrades to enhance product quality and consistency. Companies are modernizing their facilities to produce modified and performance-grade bitumen that meets evolving regulatory and engineering standards, particularly in road construction and waterproofing applications.

Another key approach is expanding partnerships with government agencies, contractors, and research institutions to support innovation in sustainable bitumen usage, including warm mix asphalt, recycled pavement materials, and polymer-modified blends. These collaborations allow companies to stay ahead of environmental mandates and maintain relevance in a shifting policy landscape.

Lastly, strengthening logistics and distribution networks has become a priority for major players. By optimizing supply chains—particularly in remote regions and high-demand states—companies ensure timely delivery, reduce storage costs, and improve customer satisfaction, reinforcing their competitive advantage in a highly seasonal and location-dependent market.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the North American bitumen market include ExxonMobil Corporation, Shell plc, BP p.l.c., Chevron Corporation, TotalEnergies SE, Valero Energy Corporation, Marathon Petroleum Corporation, Suncor Energy Inc., Imperial Oil Limited, Athabasca Oil Corporation, Syncrude Canada Ltd., NuStar Energy L.P., Nynas AB, China Petroleum & Chemical Corporation (Sinopec), Indian Oil Corporation Ltd., Petróleos Mexicanos (Pemex), Bouygues S.A., Gazprom Neft, ENEOS Corporation, JX Nippon Oil & Energy Corporation, Villas Austria GmbH, Koch Industries (Flint Hills Resources), Husky Energy, McAsphalt Industries, Owens Corning.

The competition in the North American bitumen market is shaped by a combination of vertically integrated energy giants, specialized refiners, and regional suppliers vying for dominance in an industry closely tied to infrastructure spending and crude oil dynamics. Established players such as Suncor Energy, Imperial Oil, and Valero Energy benefit from well-developed supply chains, technical expertise, and longstanding relationships with government procurement agencies, giving them a significant edge in volume contracts and large-scale projects.

At the same time, mid-sized refining firms and independent asphalt producers are gaining traction by offering cost-effective alternatives, customized formulations, and localized service models tailored to municipal and private-sector needs. Their agility allows them to respond quickly to fluctuating demand cycles and regional supply constraints, making them formidable competitors in niche segments.

Emerging trends around sustainability, recycled content, and alternative binders are further reshaping the competitive landscape, compelling traditional bitumen suppliers to invest in greener solutions or risk losing ground to innovators in the space. Regulatory pressures and public scrutiny over environmental impact have prompted many firms to reposition their offerings toward cleaner production methods and reduced lifecycle emissions.

To remain relevant, companies must continuously adapt through product differentiation, strategic acquisitions, and proactive engagement with policymakers, ensuring they not only meet current demands but also anticipate future shifts in the evolving bitumen ecosystem.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Suncor Energy launched a new line of low-carbon bitumen derived from solvent-assisted oil sands extraction, targeting environmentally conscious infrastructure clients and aligning with Canadian federal emissions reduction goals.

- In June 2024, Imperial Oil announced a joint venture with a U.S.-based asphalt blending firm to expand its refined bitumen distribution network into Midwest and Northeast U.S. markets, enhancing cross-border access and supply chain reliability.

- In September 2024, Valero Energy upgraded its Quebec City refinery to increase output of polymer-modified bitumen, aiming to capture growing demand from provinces mandating enhanced pavement performance standards for high-traffic roadways.

- In November 2024, a Canadian mid-tier bitumen producer secured a multi-year contract with a national highway maintenance agency, positioning itself as a preferred supplier for winter-resilient bitumen blends designed for cold climate durability.

- In March 2025, a Texas-based specialty asphalt company introduced a proprietary bio-enhanced bitumen additive, developed in collaboration with academic researchers, to improve flexibility and reduce reliance on conventional fossil-derived binders in public works projects.

MARKET SEGMENTATION

This research report on the North American bitumen market has been segmented and sub-segmented based on product type, application, and region.

By Product Type

- Paving Grade Bitumen

- Polymer Modified Bitumen (PMB)

By Application

- Road Construction

- Waterproofing

By Region

- Us

- Canada

- Rest of North America

Frequently Asked Questions

1. What is driving the growth of the North American bitumen market?

Key drivers include infrastructure development, increased road construction projects, urbanization, and rising demand for durable roofing materials.

2. Which countries contribute the most to the North American bitumen market?

The United States is the largest contributor, followed by Canada and Mexico.

3. How is sustainability being addressed in the bitumen industry?

Companies are investing in recycled asphalt pavement (RAP), warm mix asphalt technologies, and exploring bio-based bitumen alternatives

4. Who are the key players in the North America bitumen market?

Important players include ExxonMobil, Shell, BP, Chevron, TotalEnergies, Suncor, and Marathon Petroleum.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com