North America Cell Fractionation Market Research Report – Segmented By Product, Type Of Cell, End User & Country (The United States, Canada and Rest of North America) - Industry Analysis (2026 to 2034)

Market Size, 2025

$1.23 BnMarket Estimate, 2026

$1.36 BnMarket Forecast, 2034

$3.05 BnCAGR, 2026–2034

10.65%North America Cell Fractionation Market Summary

The North America Cell Fractionation Market size was valued at USD 1.11 billion in 2024 and is anticipated to reach USD 2.76 billion by 2033, growing at a CAGR of 10.65% from 2024 to 2033. The market is gaining momentum due to the rising demand for remote cardiac care, the growing burden of cardiovascular diseases, and technological advancements in AI-powered diagnostics and wearable cardiac monitoring devices.

Key Market Trends & Insights

- North America dominated the global market with a largest Share in 2024.

- North America is projected to grow at the fastest rate between 2024 and 2033.

- Based on technology, the IT services segment is the fastest-growing with a projected CAGR of 10.65%.

- AI and wearable tech adoption are key trends driving innovation in the market.

Market Size & Forecast

- 2024 Market Size: USD 1.11 billion

- 2033 Projected Market Size: USD 2.76 billion

- CAGR (2024–2033): 10.65%

- North America: Largest market in 2024

- North America: Fastest-growing region

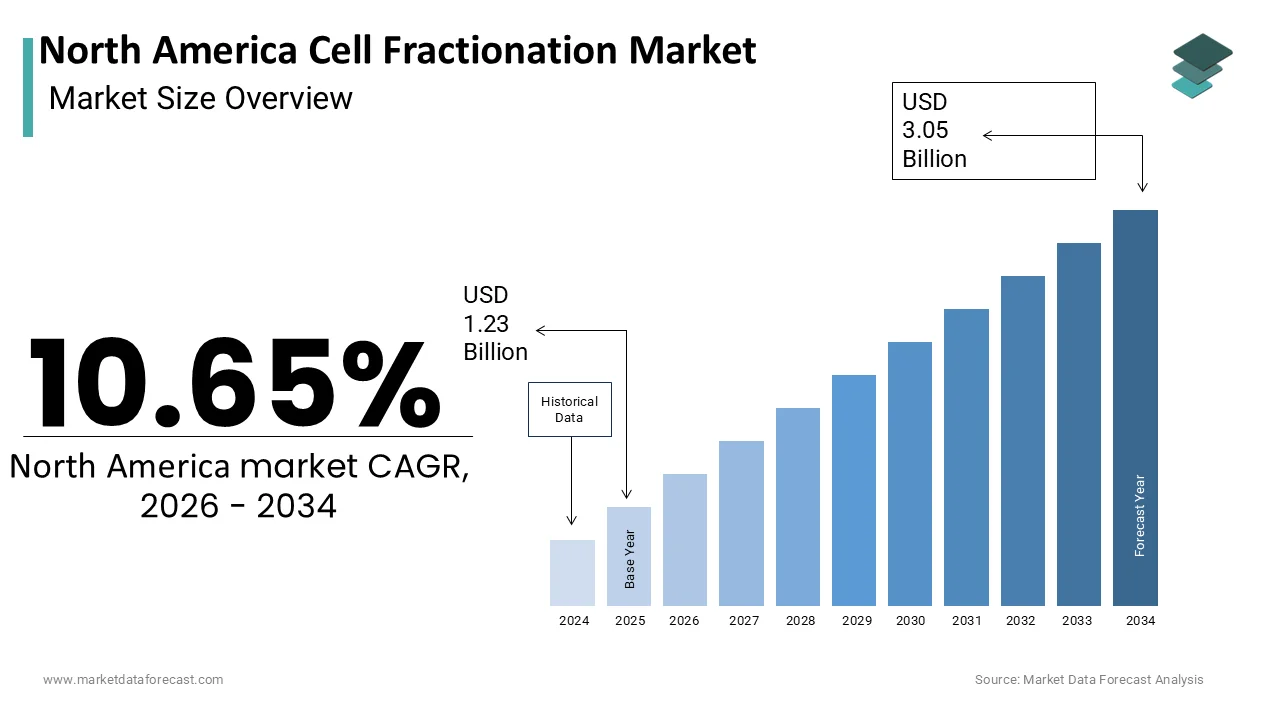

North America Cell Fractionation Market Size

The North America Cell Fractionation Market is projected to grow from USD 1.23 billion in 2025 to USD 1.36 billion in 2026 and reach USD 3.05 billion by 2034, registering a CAGR of 10.65% during the forecast period from 2026 to 2034.

The cell fractionation is a range of technologies, reagents, and services used to isolate and analyze subcellular components such as organelles, cytoplasmic fractions, and nuclear extracts. This process is fundamental in biomedical research, drug discovery, and molecular diagnostics which enables scientists to study cellular functions, protein localization, and metabolic pathways at a granular level. Cell fractionation techniques are widely employed across academic institutions, biotechnology firms, and pharmaceutical companies to support advanced research in oncology, neurodegenerative diseases, and immunology. In Canada, major research hubs such as Toronto’s MaRS Discovery District and Montreal’s McGill University have expanded their proteomics and metabolomics laboratories, which has increased demand for high-precision cell separation tools. Additionally, the growing presence of contract research organizations (CROs) and increasing investments in personalized medicine by private biotech firms have contributed to the region’s leadership in this field.

MARKET DRIVERS

Rising Investments in Life Sciences Research

The significant rise in funding for life sciences research, especially in the US and Canada, is one of the main factors driving the growth of the North America cell fractionation market. Universities and research institutes across the continent are leveraging these funds to expand their capabilities in cancer biology, regenerative medicine, and infectious disease research. For instance, Harvard Medical School and Stanford University have established dedicated cell biology labs equipped with advanced fractionation systems to support their genomic and proteomic initiatives. Moreover, private sector investment has surged alongside public funding with venture capital firms backing startups focused on targeted drug delivery and cellular therapies.

Expansion of Biopharmaceutical and Genomic Research Activities

A rapid growth of genomic and biopharmaceutical research initiatives throughout the region is another significant driver of the North America cell fractionation market growth expansion. The increasing number of therapeutic development programs targeting gene therapy, RNA interference, and monoclonal antibodies has created a strong demand for detailed intracellular analysis. According to the Biotechnology Innovation Organization (BIO), the U.S. biopharma industry supported over 2 million jobs in 2023, with more than 1,500 companies engaged in drug discovery and development pipelines that require extensive use of cell fractionation techniques. The rise of CRISPR and other gene-editing technologies has heightened the need for isolating specific cellular compartments to assess gene expression and protein function. Canada has also seen a surge in genomic research initiatives including Genome British Columbia and the Ontario Institute for Cancer Research, which rely heavily on cell fractionation for biomarker discovery and pathway analysis. Development in the North American market will be driven by the need for precise and scalable fractionation solutions as precision medicine gains popularity and the need for personalized therapies grows.

MARKET RESTRAINTS

High Cost of Advanced Cell Fractionation Instruments

The high cost of advanced fractionation equipment and consumables is one of the main factors restricting the North America cell fractionation market. Advanced equipment such as ultracentrifuges, flow cytometers, and automated cell sorters often come with significant upfront expenses which limits access for smaller research institutions and startup biotech firms. According to the Association of American Medical Colleges (AAMC), many regional universities and teaching hospitals face budget constraints that delay or prevent the acquisition of state-of-the-art fractionation systems. This financial burden is compounded by ongoing costs related to maintenance, calibration, and specialized training required to operate complex machinery effectively. According to the Canadian Foundation for Innovation (CFI), there is still a disparity in the distribution of resources between large research facilities and smaller community-based organizations, despite government funding for modernizing laboratory equipment.

Complexity and Technical Expertise Required for Cell Fractionation Procedures

The technical complexity involved in performing cell fractionation procedures presents another significant restraint in the North America Cell Fractionation Market. Effective execution of these techniques requires highly trained personnel who understand biochemical separation principles, contamination control, and downstream analytical methods. Improper handling during fractionation can lead to sample degradation, cross-contamination, and inaccurate experimental outcomes. This risk necessitates extensive training programs, which many institutions find difficult to implement consistently across all research teams. Furthermore, according to the Council on Undergraduate Research (CUR), there is a growing concern about the shortage of skilled technicians and researchers proficient in advanced cell biology techniques particularly in mid-sized academic and industrial labs.

MARKET OPPORTUNITIES

Integration with Single-Cell Analysis and Omics Technologies

Integrating cell fractionation with single-cell analysis and multi-omics technology presents an innovative opportunity for the North American market. The ability to isolate and analyze individual cells and their individual components has become crucial as researchers move to understand biological systems at a level of resolution never before possible. According to the Broad Institute of MIT and Harvard, single-cell sequencing and spatial transcriptomics are now central to discovering cellular heterogeneity, identifying rare cell populations, and mapping disease progression. These methodologies depend heavily on precise cell fractionation to ensure purity and integrity of isolated components before downstream processing. Fractionation techniques are used extensively in the Human Cell Atlas program, which is mostly led by North American educational institutions and aims to catalog all of the human body's cell types. Cell fractionation is positioned to play a crucial role in next-generation biomedical research due to the convergence of genomes, proteomics, and metabolomics.

Increasing Use in Drug Development and Target Validation

The growing application of fractionation techniques in target validation and drug development procedures is another opportunity for the North America cell fractionation market. Pharmaceutical companies are increasingly relying on subcellular analysis to identify novel drug targets, assess mechanism of action, and monitor off-target effects at the molecular level. In order improve therapy candidates, researchers can evaluate intracellular drug concentrations, analyze receptor location, and break down signaling pathways using cell fractionation. Biotech firms specializing in targeted therapies including CAR-T cell treatments and RNA-based drugs are incorporating fractionation into their development systems to validate cellular responses and refine dosing strategies. Cell fractionation is anticipated to play an increasingly important role in pharmaceutical R&D as regulatory bodies place a higher priority on mechanistic clarity and accuracy in medication approvals.

MARKET CHALLENGES

Standardization and Reproducibility Across Laboratories

Lack of standardized protocols and reproducibility across different laboratories are the other factors challenging the North America Cell Fractionation Market. Variations in methodology, equipment settings, and reagent quality can lead to inconsistent results which may reduce confidence in experimental data and delaying scientific progress. According to the Nature Methods journal, inter-laboratory variability in cell fractionation outcomes has been identified as a critical issue in translational research, particularly in fields like cancer biology and neuroscience where reproducibility is paramount. Differences in centrifugation speeds, buffer compositions, and post-isolation handling contribute to discrepancies in sample purity and yield. According to the International Society for Advancement of Cytometry (ISAC), there is currently no agreement on the ideal process configurations for different cell types and applications which indicates that efforts to standardize best practices are still in their early stages. Inconsistencies in fractionation processes will continue to hinder accurate data interpretation and the market's ability to fully advance biomedical innovation unless universal standards are accepted and confirmed across research organizations.

Ethical and Regulatory Concerns in Human Sample Handling

Ethical and regulatory concerns surrounding the handling of human-derived samples present another significant challenge for the North America Cell Fractionation Market. When working with clinical specimens, research institutes must manage complex compliance frameworks due to growing scrutiny of bioethics, patient permission, and data protection. According to the U.S. Department of Health and Human Services (HHS), there are strict guidelines governing the collection, storage, and use of human tissue and fluids in research. Institutions are required to obtain informed consent, maintain biosafety protocols, and comply with HIPAA regulations to protect donor anonymity. Furthermore, according to the Canadian Tri-Council Policy Statement (TCPS), ethical oversight committees must review all proposed studies involving human-derived materials. This adds administrative layers that can slow down research timelines.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Type Of Cell, End User and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada and Rest of North America |

| Market Leader Profiled | Beckman Coulter, Inc., Becton, Dickinson and Company, Bio-Rad Laboratories, Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The consumables segment dominated the North America Cell Fractionation market by capturing 35% of share in 2025owing to the high-frequency usage of consumables such as centrifuge tubes, filters, and fractionation kits in research laboratories and biopharmaceutical settings. Consumables must be replenished often to sustain a steady demand cycle, as compared to instruments that are purchased once and used over a number of years. Moreover, as per the report by the American Society for Cell Biology (ASCB), advancements in microfluidic-based fractionation techniques have led to the development of specialized consumables developed for precision applications like organelle isolation and nuclear extraction.

The instruments segment is predicted to witness a CAGR of 14.6% throughout the forecast period. The growth of segment is due to increasing investments in automation and advanced analytical equipment designed to improve efficiency and reproducibility in subcellular analysis. Leading research institutions and pharmaceutical companies are upgrading their laboratory infrastructure with automated cell sorters, ultracentrifuges, and digital fraction collectors to enhance throughput and reduce manual errors. According to the National Institutes of Health (NIH), more than 15 new core research facilities have been established in 2023 alone at significant American academic institutions. Additionally, the rise of contract research organizations (CROs) specializing in drug discovery has intensified demand for scalable and integrated instrument platforms capable of handling large sample volumes with minimal human intervention.

By Cell Type Insights

The mammalian cell fractionation segment led the North America cell fractionation market by occupying a share of 62.3% in 2025. The complexity of mammalian cellular structures necessitates precise isolation of organelles and subcellular compartments to study signaling pathways, protein localization, and metabolic functions. Furthermore, according to the Allen Institute for Brain Science, nuclear and synaptic fractionation are crucial for mapping neuronal activity and understanding neurodegenerative processes in mammalian brain tissue studies.

The microbial cell fractionation segment is estimated to register a CAGR of 12.8% over the forecast period with the increasing importance of microbial proteomics and metabolomics in antibiotic resistance studies, vaccine development, and synthetic biology applications. The rise in antimicrobial-resistant infections has prompted extensive research into bacterial membrane proteins and intracellular enzymes which requires precise fractionation techniques. Furthermore, institutions like MIT and the University of British Columbia have broadened their efforts to study the microbiome by integrating microbial fractionation into investigations into industrial fermentation, gut health, and the generation of biofuel. Microbial cell separation is also being used by biotech companies creating new probiotics and live biotherapeutics to separate important functional components for therapeutic use.

By End User Insights

The research laboratories segment dominated the market and held 48.3% of share in 2025with the extensive utilization of fractionation techniques in academic and government-funded research institutions conducting fundamental studies in molecular biology, genetics, and disease pathology. Major research universities such as Stanford, Harvard, and the University of Toronto continue to invest in state-of-the-art fractionation equipment to support their proteomic and genomic research initiatives. According to the Federation of American Societies for Experimental Biology (FASEB), these labs' primary research facilities frequently service several departments, which increases the need for instruments and consumables. Research laboratories continue to serve as the major hub for the deployment of cell fractionation technology throughout North America due to continued federal support and growing industry-academia partnership.

The biopharmaceutical companies’ segment is likely to grow with a CAGR of 15.2% throughout the forecast period. This rapid adoption is fueled by the expanding pipeline of targeted therapeutics, including gene therapies, monoclonal antibodies, and cell-based vaccines, all of which require detailed intracellular analysis during preclinical and development phases. As per the report by the Tufts Centre for the Study of Drug Development, the average number of cell-based assays per drug candidate has increased by nearly 40% since 2020, This has made the need for more sophisticated fractionation tools to isolate and analyse specific cellular components. Additionally, pharmaceutical companies are using cell fractionation into their target validation and toxicity testing processes as a result of regulatory bodies like the FDA placing an increased priority on mechanistic clarity in medication approvals.

COUNTRY LEVEL ANALYSIS

The United States was the top performer in the North America Cell Fractionation market by capturing 78.3% of share in 2025. The country maintains its leadership position due to a strong presence of world-renowned research institutions, biopharmaceutical giants, and a well-established regulatory framework supporting life sciences innovation. Additionally, the U.S. biotechnology sector, represented by organizations like BIO, supports over 1,500 active drug development programs that rely on subcellular analysis for target validation and mechanism of action studies. Next-generation fractionation technologies are being developed due to the continued influx of venture capital funding from major cities like Boston, San Francisco, and New York. The United States continues to lead North America in cell fractionation innovation due to strong academic-industry partnerships and an expanding ecosystem of contract research organizations (CROs).

Canada was positioned second in the North America Cell Fractionation Market by holding 17.3% of share in 2025. The country’s growing demand is linked to increased investments in life sciences research and the expansion of biotechnology clusters in cities like Toronto, Montreal, and Vancouver. According to Genome Canada, CAD 500 million was allocated nationally in 2023 for genomes and precision medicine projects, which increased the need for high-precision fractionation tools in both clinical and academic research contexts. Additionally, the Canadian Institutes of Health Research (CIHR) has prioritized neurodegenerative and cancer research, both of which require extensive subcellular analysis. Moreover, according to BIOTECanada, the biotech sector in the nation has experienced a boom in international collaborations and startup formations, which has improved the use of sophisticated fractionation systems in drug development pipelines.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a promising role in the North American cell fractionation market profiled in the report are Beckman Coulter, Inc., Becton, Dickinson and Company, Bio-Rad Laboratories, Inc., Cell Signaling Technology, Inc., F. Hoffman-La Roche AG, Merck KGaA, Miltenyi Biotec, QIAGEN N., Qsonica and Thermo Fisher Scientific Inc.

The competition in the North America Cell Fractionation Market is intense and characterized by continuous technological advancements, strategic consolidations, and increasing demand from academic and biopharmaceutical sectors. A few dominant multinational corporations maintain strong control over the market environment, leveraging extensive distribution networks, deep R&D pipelines, and well-established brand recognition. However, the competitive environment is becoming more diversified as a result of the increasing involvement of specialist suppliers and smaller biotech companies, who are bringing more specialized offers tailored to certain research applications.

Innovation remains a central battleground as companies strive to develop automated, high-precision, and user-friendly systems that can handle complex subcellular separations with greater efficiency and reproducibility. Additionally, the rising focus on personalized medicine and biomarker discovery is driving demand for more sophisticated fractionation workflows, which prompts manufacturers to align their product development strategies accordingly.

Collaborations between industry leaders and academic research centers are also becoming increasingly common with the aim of accelerating the translation of laboratory discoveries into real-world applications. The North America Cell Fractionation Market is expected to remain highly dynamic which demads constant adaptation and differentiation among key players as research funding continues to grow and new therapeutic modalities emerge.

Top Players in the Market

The North America Cell Fractionation Market is shaped by several key players known for their innovation, product diversity, and global reach. Among them, Thermo Fisher Scientific, Merck KGaA (Sigma-Aldrich), and BD Biosciences stand out as industry leaders.

Thermo Fisher Scientific offers a comprehensive portfolio of cell fractionation tools including reagents, kits, and instruments designed to support high-throughput and precision research. The company's commitment to developing scalable solutions has made it a preferred partner for academic institutions and biopharma firms across the region.

Merck KGaA provides a wide range of biochemicals, proteomics tools, and specialized reagents essential for isolating cellular components. Its strong presence in life sciences research markets supports widespread adoption of cell fractionation workflows in both academic and industrial settings.

BD Biosciences is a division of Becton Dickinson focuses on flow cytometry-based cell analysis and sorting technologies. BD Biosciences plays a crucial role in advancing cell separation techniques used in immunology, cancer research, and regenerative medicine particularly in clinical and translational applications.

Top Strategies Used by Key Players

Leading companies in the North America Cell Fractionation Market are employing strategic initiatives to strengthen their market position and expand their influence. One major approach is product innovation and portfolio expansion, where manufacturers continuously develop advanced consumables, reagents, and instrumentation tailored for specific applications such as organelle isolation and single-cell analysis.

Another key strategy involves strategic acquisitions and partnerships with companies acquiring niche biotech firms or forming collaborations with research institutions to enhance technological capabilities and gain access to emerging innovations in subcellular research.

Firms are actively investing in customer engagement and technical support by offering customized training programs, application-specific consulting, and digital platforms that streamline workflow integration. These strategies collectively help reinforce brand loyalty, drive adoption and ensure sustained leadership in a highly competitive environment.

RECENT HAPPENINGS IN THE MARKET

In March 2023, Thermo Fisher Scientific launched a new line of microfluidic-based cell fractionation kits designed to improve organelle isolation efficiency which targets academic and pharmaceutical research labs seeking higher resolution in subcellular studies.

In October 2023, Merck KGaA acquired a U.S.-based startup specializing in nuclear extraction technologies in order to expand its offers in gene regulation and epigenetics research and integrate innovative approaches into its current portfolio.

In June 2025, BD Biosciences introduced an upgraded version of its fluorescence-activated cell sorting (FACS) system optimized for rare cell isolation, which caters to expand applications in immunotherapy and stem cell research within the biopharma sector.

In November 2025, Bio-Rad Laboratories expanded its facility in Hercules, California to increase production capacity for cell lysis and fractionation reagents in response to rising demand from contract research organizations and academic institutions.

In February 2025, Agilent Technologies partnered with a leading AI-driven drug discovery firm to co-develop intelligent fractionation workflows that incorporate machine learning algorithms for improved data interpretation and experimental reproducibility in preclinical studies.

MARKET SEGMENTATION

This research report has been segmented and sub-segmented the North America Cell Fractionation Market into the following categories.

By Product

- Consumables

- Reagent

- Beads

- Disposables

- Instruments

By Cell Type

- Microbial

- Mammalian

By End User

- Research Laboratories

- Biopharmaceuticals

- Biotechnology Companies

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What is cell fractionation and why is it important in North America?

Cell fractionation is the process of breaking up cells and separating their components based on size, density, or other properties. It is widely used in North America for research in cell biology, drug development, and diagnostics.

What are the key drivers of the North America Cell Fractionation Market?

Major drivers include the rise in chronic diseases, advancements in cell biology research, growth in biotechnology and pharmaceutical industries, and increased government funding for research.

Which countries in North America are the major contributors to this market?

The United States is the dominant contributor, followed by Canada and Mexico due to strong healthcare infrastructure and research funding.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com