North America Cement Market Size, Share, Growth, Trends, And Forecasts Report, Segmented By Type, Application, And By Country (The US, Canada, And Rest of North America), Industry Analysis From (2026 to 2034)

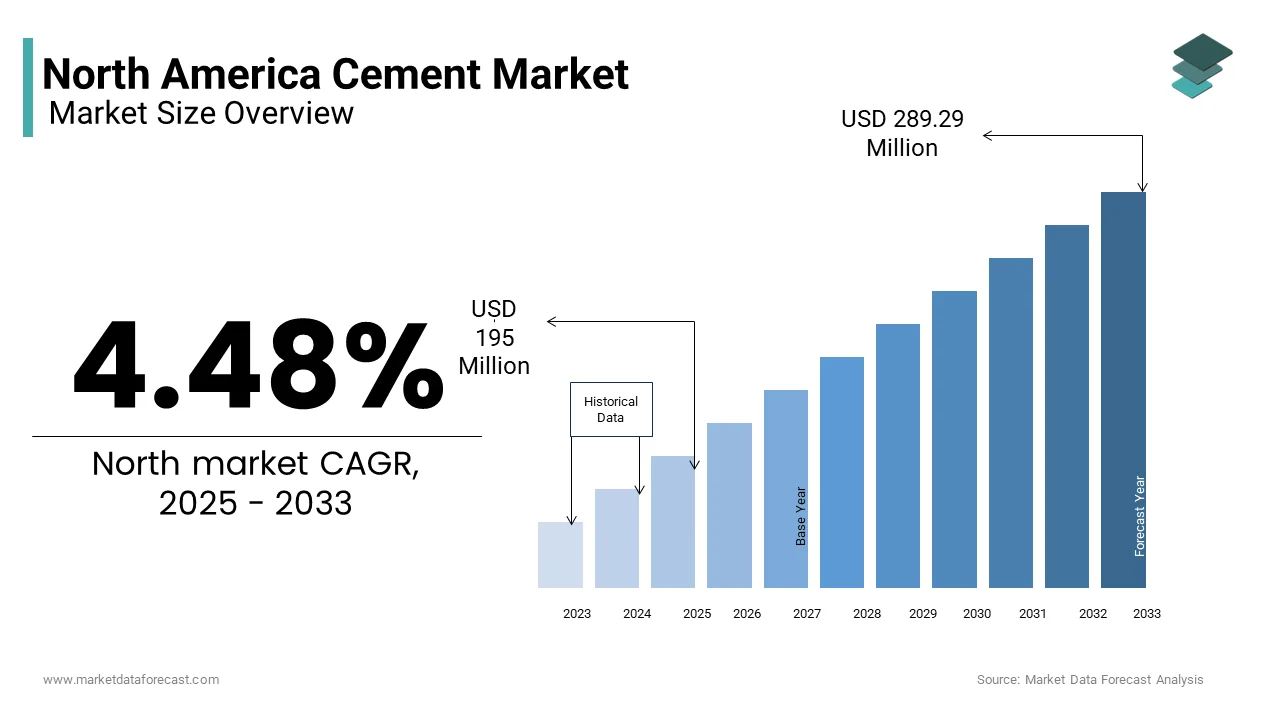

Market Size, 2025

$203.74 MnMarket Estimate, 2026

$212.87 MnMarket Forecast, 2034

$302.26 MnCAGR, 2026–2034

4.48%North America Cement Market Size

The North American cement market size was valued at USD 203.74 million in 2025 and is anticipated to reach USD 212.87 million in 2026 to reach USD 302.26 million by 2034, growing at a CAGR of 4.48% during the forecast period from 2026 to 2034.

The North American cement market plays a foundational role in the region’s construction and infrastructure development, serving as a key input for residential, commercial, and industrial building activities. Cement, primarily in the form of Portland cement, is an essential binding agent used in concrete production, which underpins roads, bridges, housing, and large-scale public works projects.

The industry benefits from well-established manufacturing facilities across states such as Texas, California, Missouri, and Florida, where proximity to raw materials like limestone and shale supports efficient production.

In Canada, the cement sector is more compact but remains integral to national infrastructure growth. Natural Resources Canada reports that domestic cement production supports both urban expansion and government-funded transportation and energy initiatives. Meanwhile, Mexico's cement industry has been growing steadily due to rapid urbanization and increased foreign investment in real estate and industrial parks.

MARKET DRIVERS

Resurgence in Residential Construction Activity

One of the primary drivers of the North American cement market is the resurgence in residential construction, particularly in the United States. Housing demand has rebounded significantly following a period of economic recovery and demographic shifts, directly boosting cement consumption for foundations, driveways, and structural components. This upswing was driven by strong household formation rates, historically low unemployment levels, and government-backed initiatives aimed at expanding homeownership access.

Each single-family home typically requires approximately 30 to 40 cubic yards of concrete, translating into substantial cement demand.

Moreover, population growth in Sun Belt states such as Texas, Florida, and Arizona has intensified regional demand for new housing developments, prompting developers to ramp up construction activity. These areas have also benefited from relatively lower land costs and favorable zoning regulations, further stimulating cement usage.

In addition, the rise of accessory dwelling units (ADUs) and multi-family housing complexes has contributed to sustained cement consumption, even amid rising interest rates and material cost pressures.

Expansion of Infrastructure Development Projects

A significant driver of the North American cement market is the ongoing expansion of infrastructure development projects, particularly in the United States and Canada. Governments have prioritized modernizing aging transportation networks, water systems, and energy grids, all of which require extensive use of concrete-based materials.

According to the American Society of Civil Engineers (ASCE), the U.S. allocated over $110 billion toward infrastructure upgrades in 2023 under the Infrastructure Investment and Jobs Act. A major portion of this funding was directed toward repairing highways, bridges, and transit systems—sectors heavily reliant on cement-intensive solutions.

The Federal Highway Administration reported that highway and bridge construction expenditures exceeded $120 billion in 2023, with reinforced concrete forming a core component in roadbeds, overpasses, and retaining walls. Additionally, state-level investments in mass transit and high-speed rail corridors have further amplified cement demand.

Furthermore, the push for renewable energy infrastructure, including wind farms and solar panel installations, has introduced new applications for cement in foundation construction and grid support structures. With infrastructure spending projected to remain a policy priority across North America, the cement industry stands to benefit from sustained investment cycles over the coming decade.

MARKET RESTRAINTS

Environmental Regulations and Carbon Emission Pressures

One of the most pressing restraints facing the North American cement market is the tightening regulatory environment concerning carbon emissions and environmental sustainability. Cement production is inherently energy-intensive, accounting for r notable share of global CO₂ emissions due to the calcination of limestone and combustion of fossil fuels in kilns.

According to the U.S. Environmental Protection Agency (EPA), cement manufacturing facilities are subject to increasingly stringent air quality standards under the Clean Air Act, requiring them to implement carbon capture technologies, switch to alternative fuels, or invest in energy-efficient equipment. Compliance with these regulations has led to higher capital expenditures and operational costs for producers.

Moreover, investor sentiment is shifting toward greener industries, making it harder for traditional cement producers to secure financing for plant expansions or acquisitions.

These regulatory and financial pressures pose a significant challenge to the cement industry, necessitating innovation and adaptation to align with broader climate goals while maintaining competitive production capabilities.

Volatility in Raw Materials and Energy Costs

Another significant restraint affecting the North American cement market is the volatility in raw material and energy prices, which directly impacts production costs and pricing stability. Cement manufacturing relies heavily on limestone, clay, gypsum, and coal or natural gas for thermal energy, all of which have experienced price fluctuations due to supply chain disruptions and geopolitical tensions.

Similarly, coal prices saw upward movement due to reduced domestic mining output and export demands, as highlighted by the U.S. Geological Survey.

Transportation costs have also surged due to labour shortages in logistics, increased diesel prices, and congestion at ports and rail hubs. The American Trucking Associations reported that freight rate indices climbed by 12% in 2023, adding to the overall cost burden for cement producers.

Furthermore, the availability of raw materials has been impacted by regulatory restrictions on quarrying and mineral extraction. In several U.S. states and Canadian provinces, new limestone extraction permits have been delayed due to environmental concerns and community opposition.

These challenges contribute to uncertainty in production planning and pricing strategies, constraining the market’s ability to scale efficiently in response to demand fluctuations.

MARKET OPPORTUNITY

Adoption of Green and Low-Carbon Cement Technologies

An emerging opportunity for the North American cement market lies in the adoption of green and low-carbon cement technologies designed to reduce the industry’s environmental footprint while meeting evolving regulatory and consumer expectations. Governments and investors are increasingly incentivizing sustainable construction practices, driving innovation in alternative binders, carbon capture, utilization, and storage (CCUS), and energy-efficient production methods.

According to the U.S. Department of Energy, several pilot projects launched in 2023 focused on integrating carbon capture technology into cement manufacturing processes to reduce facility emissions by up to 90%. Companies such as Heidelberg Materials and Cemex have already begun testing CCUS systems at their North American plants, signaling a shift toward cleaner production models.

Also, the use of supplementary cementitious materials (SCMs) such as fly ash, slag cement, and calcined clay is gaining traction to partially replace traditional Portland cement in concrete mixtures.

Moreover, advancements in geopolymer cement and alkali-activated materials offer promising alternatives that eliminate the need for limestone calcination.

Growth in Prefabricated and Modular Construction Methods

Another promising opportunity for the North American cement market is the growing adoption of prefabricated and modular construction methods, which leverage precast concrete elements to streamline building processes and enhance efficiency. This trend is reshaping the construction landscape by enabling faster project completion, reduced labor dependency, and improved material utilization.

Precast concrete panels, beams, and flooring systems play a central role in these off-site construction techniques, offering durability, precision, and scalability.

Cement suppliers are adapting to this shift by developing specialized concrete mixes tailored for factory-based casting environments.

Moreover, the use of precast concrete in infrastructure projects such as bridge decks and tunnel linings has expanded due to its superior strength and longevity. With technological advancements and supportive policy frameworks, the prefabrication trend presents a significant growth avenue for the North American cement industry.

MARKET CHALLENGES

Rising Competition from Alternative Construction Materials

A significant challenge confronting the North American cement market is the increasing competition from alternative construction materials that offer comparable strength, lighter weight, and potentially lower environmental impact. Steel, engineered wood products, fiber-reinforced polymers, and advanced composites are gradually encroaching on traditional concrete applications, particularly in residential and mid-rise commercial buildings.

According to the American Wood Council, cross-laminated timber (CLT) and other mass timber products captured an estimated 8% of the U.S. structural material market in 2023, up from just 2% in 2018. These materials are being promoted for their sustainability credentials, ease of assembly, and aesthetic appeal, particularly in urban developments seeking LEED certification.

Similarly, steel framing has gained traction in multifamily housing and industrial buildings due to its recyclability and resistance to pests and fire.

In addition, synthetic and hybrid materials such as ultra-high-performance concrete (UHPC), aerogels, and geopolymers are being developed to provide enhanced performance characteristics while minimizing cement dependency. As noted by the National Institute of Standards and Technology (NIST), research into alternative binders and composite materials is accelerating, with several prototypes demonstrating viable replacements for conventional cement in select applications.

Aging Infrastructure and Limited Plant Modernization

A critical challenge facing the North American cement market is the aging infrastructure of many production facilities, coupled with limited investment in modernization and process optimization. Many cement plants in the U.S. and Canada were constructed in the 1970s and 1980s, and despite incremental upgrades, a significant portion of the asset base remains outdated, leading to inefficiencies and rising maintenance costs.

Older kiln systems tend to consume more energy and emit higher levels of pollutants, making them less competitive in a regulatory environment that increasingly favors low-carbon operations.

Capital expenditure constraints have hindered the adoption of newer technologies such as oxyfuel combustion, electric kilns, and digital monitoring systems that could improve efficiency and reduce emissions.

Labor shortages in skilled technical roles have further slowed modernization efforts, as many cement producers struggle to recruit engineers, operators, and maintenance personnel familiar with advanced manufacturing systems. The Manufacturing Institute reported that workforce gaps in the construction materials sector widened in 2023, contributing to extended downtime and reduced production capacity.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 4.48% |

| Segments Covered | By Product, Application, and Region. |

|

Various Analyses Covered | Global, Regional, a nd Country-Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | The United States, Canada, and Mexico |

| Market Leaders Profiled | Argos USA LLC, ASH GROOVE, Buzzi S.p.A., AlPortland, CEMEX, CRH, Eagle Materials Inc., Heidelberg Materials, Holcim, Lehigh White Cement Company LLC, Martin Marietta Materials, US Concrete Products, Top Players in the Market, Cemex S.A.B. de C.V. |

SEGMENTAL ANALYSIS

By Product Type Insights

Portland cement remained the largest segment in the North American cement market, accounting for 68.1% of total consumption in 2024. This dominance is primarily attributed to its widespread use across construction sectors, including residential buildings, commercial infrastructure, and industrial applications.

According to the U.S. Geological Survey, domestic production of Portland cement reached 88 million metric tons in 2023, driven by strong demand from both new construction and renovation projects. The material’s versatility, durability, and compatibility with various admixtures make it a preferred choice for concrete formulations used in foundations, pavements, and structural elements.

Its adaptability allows for customization through additives, enabling performance enhancements such as rapid setting, sulfate resistance, and high early strength—features critical in diverse environmental conditions.

Also, the continued reliance on traditional construction methods in major urban centers supports sustained demand. With robust infrastructure investment and ongoing housing development, Portland cement maintains its stronghold in the regional market, underpinning the broader construction ecosystem.

Blended cement is emerging as the fastest-growing segment in the North American cement market, projected to expand at a CAGR of 5.1%. This growth is primarily fueled by increasing awareness of sustainability benefits and regulatory support for low-carbon construction materials.

According to the National Ready Mixed Concrete Association, blended cement accounted for 25.8% of total cementitious content in U.S. concrete mixes in 2024, with growing adoption in both residential and infrastructure projects. Blended cements incorporate supplementary cementitious materials (SCMs) such as fly ash, slag cement, and silica fume, which reduce the overall carbon footprint while maintaining or enhancing performance characteristics.

Environment and Climate Change Canada noted that blended cement usage increased by 18% in 2023, particularly in green-certified buildings and municipal infrastructure initiatives aiming to meet provincial emissions targets. In the U.S., the Green Building Council observed a surge in LEED-certified projects specifying blended cement blends, reflecting shifting preferences among architects and developers.

Moreover, advancements in SCM availability and quality control have improved consistency and workability, making blended cement a viable alternative to traditional Portland cement in many applications. With heightened emphasis on sustainable construction and regulatory incentives promoting decarbonization, blended cement is poised for accelerated growth across North America.

By Application Insights

Residential construction represented the largest application segment in the North American cement market, capturing 42% of total demand in 2024. This dominance is directly linked to the resurgence in housing starts, particularly in the United States, where population growth and favourable mortgage conditions have stimulated new homebuilding activity.

The National Association of Home Builders (NAHB) highlighted that single-family homes accounted for a significant portion of all residential permits issued, reinforcing cement’s central role in this sector. Growth was particularly pronounced in Sun Belt states such as Texas, Florida, and Arizona, where land availability and lower costs supported large-scale developments.

In Canada, CMHC (Canada Mortgage and Housing Corporation) recorded over 240,000 housing starts nationwide in 202, with urban centers like Toronto, Montreal, and Vancouver driving multi-family construction. These projects also rely heavily on concrete for basement walls, parking structures, and load-bearing components.

Additionally, accessory dwelling units (ADUs), manufactured housing, and modular construction trends have further expanded cement-based applications.

Infrastructure development is the fastest-growing application segment in the North American cement market, anticipated to grow at a CAGR of 5.6% through 2033. This expansion is primarily driven by government investments in transportation networks, water systems, and energy infrastructure aimed at modernizing aging public assets.

According to the American Society of Civil Engineers (ASCE), the U.S. allocated over $110 billion toward infrastructure upgrades in 2023 under the Infrastructure Investment and Jobs Act. A significant portion of these funds was directed toward road rehabilitation, bridge replacements, and transit system expansions—all of which require extensive use of concrete.

The Federal Highway Administration reported that highway and bridge construction expenditures exceeded $120 billion in 2023, with reinforced concrete forming a core component in roadbeds, overpasses, and retaining walls. In addition, state-level investments in mass transit and high-speed rail corridors have further amplified cement demand.

Moreover, the push for renewable energy infrastructure, including wind farms and solar panel installations, has introduced new applications for cement in foundation construction and grid support structures. With infrastructure spending projected to remain a policy priority across North America, this segment is set to outpace others in terms of growth rate.

COUNTRY LEVEL ANALYSIS

United States Cement Market Analysis

- The United States dominated the North American cement market, accounting for 85.2% of total regional production and consumption in 2024. As one of the largest economies globally, the U.S. sustains a vast construction and infrastructure network that drives consistent demand for cement products.

- Like, domestic cement production surpassed 79 million metric tons in 2023, with manufacturing concentrated in key states such as Texas, California, Missouri, and Florida. These regions benefit from proximity to limestone deposits and well-established distribution channels, ensuring efficient supply to construction hubs.

- The National Association of Home Builders (NAHB) emphasized that each new single-family home required an average of 30–40 cubic yards of concrete, reinforcing cement’s integral role in residential development.

- Infrastructure spending also remained a major catalyst. Furthermore, the shift toward prefabricated construction and green building certifications encouraged the adoption of specialized cement blends designed for sustainability and durability. With sustained economic momentum and policy-backed investment cycles, the U.S. cement market remains the cornerstone of North America’s construction landscape.

Canada Cement Market Analysis

- Canada is maintaining a stable but smaller presence compared to the United States. Despite its modest scale, Canada sustains a fully integrated cement industry, serving key domestic markets such as residential construction, infrastructure, and industrial applications.

- The country benefits from hydroelectric-powered cement facilities in Quebec, which offer lower energy costs and reduced carbon emissions compared to fossil-fuel-based alternatives.

- Urban expansion in cities like Toronto, Montreal, and Vancouver has driven demand for both residential and commercial construction. Infrastructure development also contributed significantly to cement consumption. Additionally, the push for sustainable construction led to increased adoption of blended cement and alternative binders. With continued investment in smart cities and resilient infrastructure, Canada's cement market remains strategically positioned within the broader North American framework.

- The Rest of North America is gradually expanding due to growing industrial activity, foreign direct investment, and cross-border trade dynamics. Urbanization trends and real estate development have been key drivers. Industrial parks, particularly in northern states like Nuevo León and Chihuahua, have also boosted cement demand due to rising automotive and electronics manufacturing activities. Moreover, the Mexican government has intensified efforts to modernize water infrastructure, leading to higher procurement of cement-based drainage and sanitation systems. While still developing, the cement market in the Rest of North America presents emerging opportunities for expansion, particularly as regional economies continue to integrate with North American supply chains and adopt more stringent hygiene and industrial standards.

COMPETITIVE LANDSCAPE

The competition within the North American cement market is shaped by a mix of global conglomerates, regional producers, and independent manufacturers vying for market share amid fluctuating economic conditions and evolving sustainability expectations. While a few dominant multinational players control the majority of production capacity, numerous regional and local firms continue to operate by focusing on niche applications and localized supply chains. This dynamic fosters both collaboration and rivalry, particularly as companies seek to optimize costs, comply with environmental regulations, and invest in next-generation technologies.

Market participants face challenges related to aging infrastructure, energy-intensive operations, and rising input costs, all of which necessitate strategic planning and innovation. Some firms differentiate themselves through product diversification, while others emphasize sustainability initiatives and process optimization to enhance their competitive edge. Additionally, trade dynamics, particularly between the U.S., Canada, and Mexico, influence market positioning and distribution networks.

With increasing emphasis on decarbonization, smart construction, and resource efficiency, the cement industry must continuously adapt to remain resilient. As a result, the competitive landscape remains fluid, driven by technological advancements, regulatory pressures, and shifting end-user demands across key industrial sectors.

KEY MARKET PLAYERS

These are the market players that are dominating the North American cement market:

- Argos USA LLC

- ASH GROOVE

- Votorantim Cimentos

- Buzzi S.p.A.

- Al Portland CEMEX

- CRH

- Eagle Materials Inc.

- Heidelberg Materials

- Holcim

- Lehigh White Cement Company LLC

- Martin Marietta Materials

- US Concrete Products

- Cemex S.A.B. de C.V.

TOP PLAYERS IN THE MARKET

- Cemex is a global leader in building materials with a strong presence in the North American market. The company operates extensive production and distribution networks across the United States, Canada, and Mexico. Known for its innovation and sustainability initiatives, Cemex has been at the forefront of developing low-carbon construction solutions and digital tools for construction efficiency. Its strategic acquisitions and investments in green technologies have reinforced its regional leadership while contributing to global advancements in sustainable infrastructure development.

- Holcim is one of the largest cement producers worldwide and holds a dominant position in North America through its legacy operations under LafargeHolcim. The company has significantly influenced the regional cement industry by integrating advanced manufacturing practices, investing in carbon reduction technologies, and expanding into value-added construction materials. Holcim’s emphasis on circular economy principles and sustainable urban development has positioned it as a key player shaping both regional and global cement market trends.

- Votorantim Cimentos is a major international cement producer with a growing footprint in North America. The company has strategically expanded its U.S. operations through plant acquisitions and modernization programs aimed at enhancing production efficiency and product quality. Votorantim focuses on customer-centric solutions and sustainable development, aligning its regional activities with global best practices in environmental stewardship and operational excellence. Its contributions extend beyond North America, influencing global supply chains and construction material standards.

Top Strategies Used by Key Market Participants

- One of the primary strategies employed by leading cement companies in North America is investment in sustainable and low-carbon technologies. Recognizing the increasing regulatory pressure and consumer demand for environmentally friendly construction materials, firms are adopting alternative fuels, carbon capture systems, and blended cements to reduce their carbon footprint and align with global climate goals.

- Another key strategy is the modernization of production facilities and digital transformation. Companies are upgrading kiln systems, implementing automation, and leveraging data analytics to improve energy efficiency, lower operational costs, and enhance product consistency, ensuring long-term competitiveness in a capital-intensive industry.

- Lastly, strategic acquisitions and geographic expansion play a crucial role in strengthening market positions. Leading players are acquiring smaller regional cement producers and expanding into high-growth areas to consolidate their presence, diversify revenue streams, and better serve local construction markets across North America.

RECENT MARKET NEWS

- In February 2024, Cemex announced the launch of a new line of carbon-neutral concrete products tailored for North American infrastructure projects, reinforcing its commitment to sustainable construction and positioning itself ahead of tightening emissions regulations.

- In May 2024, Holcim completed the acquisition of a mid-sized cement plant in the Midwest United States, expanding its regional footprint and enhancing its ability to serve growing construction demand in the central part of the country.

- In July 2024, Votorantim Cimentos initiated a multi-phase upgrade at its Florida facility, incorporating advanced kiln technology designed to improve energy efficiency and reduce greenhouse gas emissions while boosting production reliability.

- In September 2024, Titan Cement Company entered into a strategic joint venture with a U.S.-based green building materials firm to co-develop innovative cementitious blends that incorporate recycled industrial byproducts and reduce reliance on traditional Portland cement.

- In November 2024, Buzzi Unicem launched a digital logistics platform across its North American operations, aiming to streamline cement delivery, reduce transportation emissions, and enhance customer service through real-time tracking and optimized routing.

MARKET SEGMENTATION

This research report on the North American market is segmented and sub-segmented into the following categories.

By Product Type

- Ordinary Portland Cement (OPC)

- Blended Cement

- Others

By End-User Industry

- Residential

- Commercial

- Industrial and Institutional

- Infrastructure

By Country

- The United States

- Canada

- Mexico

Frequently Asked Questions

What is the projected CAGR of the North America Cement Market from 2025 to 2033?

The North America cement market is expected to grow at a CAGR of 4.48% from 2025 to 2033 , driven by infrastructure investment, housing demand, and green building initiatives across the U.S. and Canada.

Which country accounts for the largest share of cement consumption in North America?

The U.S. accounts for over 85% of total cement consumption , with major demand coming from states like Texas, California, Florida, and New York due to high construction activity and population growth.

How many million metric tons of cement were consumed in North America in 2023?

In 2023, North America consumed approximately 98 million metric tons of cement , according to the U.S. Geological Survey (USGS) , with U.S. domestic production reaching nearly 90 million metric tons .

Which type of cement dominates the North American market?

Portland Cement (Type I) remains the most widely used, accounting for over 60% of all cement sales , particularly in residential and commercial construction projects due to its versatility and strength.

How much has green cement adoption grown in North America since 2021?

Adoption of low-carbon and blended cements increased by over 25% since 2021 , as manufacturers and contractors aim to meet federal Buy Clean standards and reduce embodied carbon in construction materials.

What percentage of new U.S. buildings use cement with recycled content?

Over 35% of new commercial buildings in the U.S. now specify cement blends containing fly ash or slag , helping reduce CO₂ emissions and qualify for LEED certification points under the USGBC program.

Which states in the U.S. have the highest per capita cement consumption?

Texas, Utah, and Idaho lead in per capita cement use, driven by rapid urbanization, highway expansion, and rising homebuilding permits, with Texas alone consuming over 10 million metric tons annually .

How has inflation and supply chain disruption affected cement prices in North America?

Cement prices in the U.S. rose by nearly 18% between 2021 and 2023 , due to higher energy costs, labor shortages, and logistics bottlenecks, impacting affordability for small-scale contractors and DIY consumers.

What role does rail transportation play in cement distribution in North America?

Approximately 45% of bulk cement shipments in the U.S. are transported via rail, especially for long-haul movements from Midwest production hubs to East and West Coast markets, ensuring cost-effective and scalable delivery.

How is AI being used in cement manufacturing processes in North America?

Major producers like Lehigh Hanson and Holcim U.S. are integrating AI-driven predictive maintenance and quality control systems , improving kiln efficiency and reducing unplanned downtime by up to 20% in modern facilities.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com