North America Cigarette Lighter Market Size, Share, Trends & Growth Forecast Report By Product Type (Flint Cigarette Lighter, Electronic Cigarette Lighter, Others), Material Type (Metal, Plastic, Others), Distribution Channel (Tobacco Shops, Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis, 2026 to 2034

Market Size, 2025

$1.78 BnMarket Estimate, 2026

$1.80 BnMarket Forecast, 2034

$2.02 BnCAGR, 2026–2034

1.45%North America Cigarette Lighter Market Size

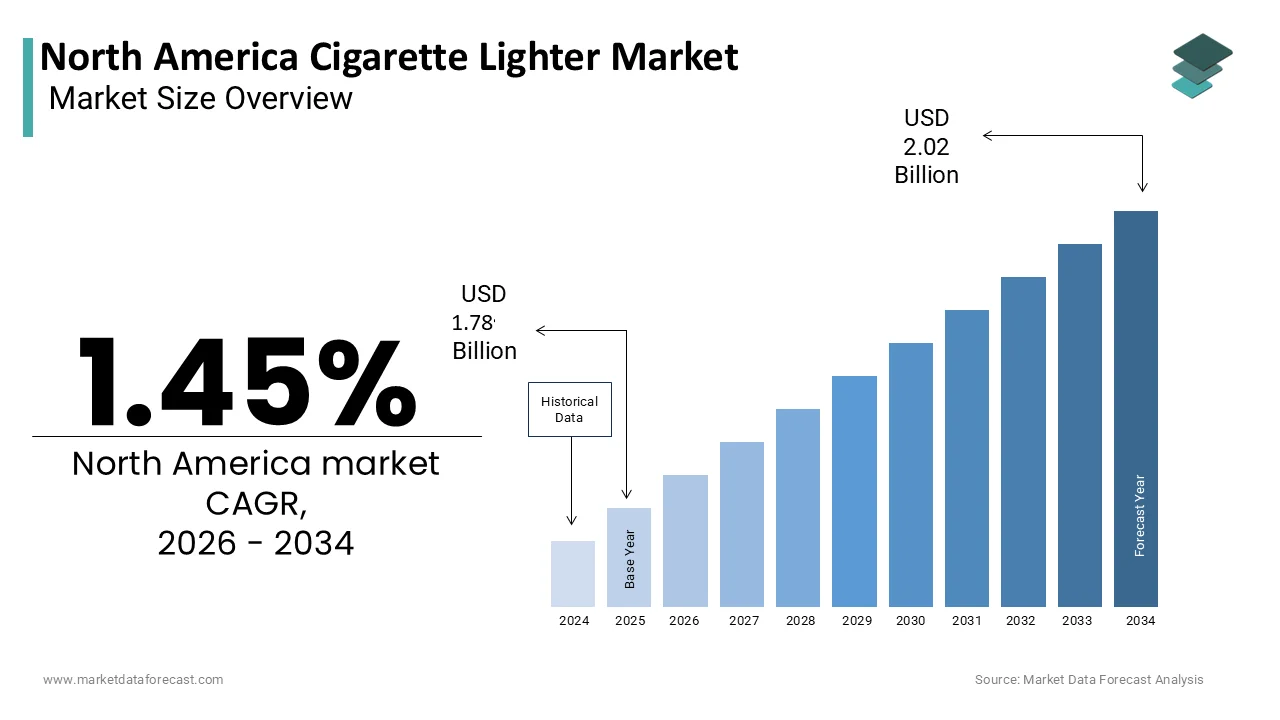

The size of the North America cigarette lighter market was worth USD 1.78 billion in 2025. The market is anticipated to grow at a CAGR of 1.45% from 2026 to 2034 and be worth USD 2.02 billion by 2034 from USD 1.80 billion in 2026.

Cigarette lighters cover a broad spectrum of products, including disposable butane lighters, refillable models, torch-style variants, and novelty or luxury designs. While traditionally associated with tobacco use, cigarette lighters have also found utility in outdoor activities, culinary applications, and emergency preparedness. In recent years, the market has evolved to incorporate design innovation, safety enhancements, and eco-conscious materials, reflecting broader consumer preferences for functionality and aesthetics. The United States remains the dominant force within this regional market, followed by Canada and Mexico, each exhibiting distinct consumption patterns influenced by regulatory frameworks, cultural habits, and economic conditions.

Meanwhile, Canada reported steady sales volumes, particularly in regions with colder climates where lighters are used beyond smoking purposes, such as camping and heating devices. These dynamics illustrate that while public health initiatives continue to reduce tobacco consumption, the cigarette lighter remains a resilient and adaptive product category within North America’s broader consumer goods landscape.

MARKET DRIVERS

Persistent Demand from Outdoor and Utility-Based Applications

Its expanding utility beyond tobacco use, particularly in outdoor and recreational settings, is one of the key growth drivers of the North America cigarette lighter market. Despite declining smoking rates, lighters remain essential tools for campers, hikers, survivalists, and grill enthusiasts who rely on them for lighting stoves, lanterns, and fire pits. According to the Outdoor Industry Association, over 57.3% of Americans participated in at least one outdoor activity in 202, marking an all-time high and reinforcing the need for reliable ignition sources. This trend is especially pronounced among younger demographics and urban dwellers seeking weekend getaways into nature, where compact and wind-resistant lighters offer practical advantages.

In Canada, the demand for multi-functional lighters has grown alongside the popularity of backyard living and winter sports. Moreover, the rise of portable gas stoves and propane heaters, especially in remote and rural areas, has further diversified the usage base of these products. These figures show how evolving consumer lifestyles and a growing emphasis on self-reliance in outdoor environments are reshaping the cigarette lighter market into a more versatile and enduring consumer product segment.

Continued Use Among Niche Smoking Populations and Cultural Preferences

Despite widespread anti-smoking campaigns and declining overall smoking prevalence, certain demographic segments in North America continue to drive demand for cigarette lighters. These include individuals who prefer rolling their own cigarettes, users of cigars and pipe tobacco, and populations in correctional facilities, where disposable lighters remain a standard-issue item.

In Canada, similar patterns are observed, particularly in rural and Indigenous communities where smoking rates remain above national averages. Furthermore, cigar and hookah lounges, especially in major metropolitan areas like New York City, Los Angeles, and Toronto, continue to operate under specific regulations that allow controlled tobacco use, thereby maintaining a parallel demand for lighters. These niche markets, though smaller than in previous decades, remain resilient and contribute significantly to the ongoing relevance and commercial viability of cigarette lighters in North America.

MARKET RESTRAINTS

Stringent Regulations and Fire Safety Standards Limiting Sales and Distribution

Increasingly strict regulatory frameworks aimed at curbing youth access and reducing fire-related incidents are a major constraint on the growth of the North American cigarette lighter market. Both the United States and Canada have implemented mandatory safety standards that affect the production, packaging, and sale of lighters. In the U.S., the Consumer Product Safety Commission (CPSC) enforces regulations requiring all disposable lighters to be child-resistant, limiting the availability of low-cost, unregulated variants.

Additionally, several states have imposed outright bans or restrictions on the sale of novelty lighters, citing concerns about underage use and accidental fires. California, for instance, enacted legislation prohibiting the sale of non-compliant lighters, directly impacting import volumes and retail offerings. In Canada, similar trends are evident, with provinces like Ontario enforcing age verification processes at point-of-sale and restricting vending machine access. These regulatory pressures, while beneficial from a public safety perspective, create logistical and compliance burdens for manufacturers and retailers, ultimately constraining market expansion and altering product availability across the region.

Declining Tobacco Consumption and Public Health Campaigns Dampening Core Demand

The long-term decline in tobacco consumption, driven by aggressive public health campaigns, higher excise taxes, and shifting social attitudes toward smokin,g is one of the most persistent challenges facing the cigarette lighter market in North America. As per the Centers for Disease Control and Prevention (CDC), cigarette consumption in the U.S. fell below 200 billion units annually in 2023, a sharp drop from over 300 billion in 2010. With fewer smokers, the traditional use case for cigarette lighters continues to erode, affecting both volume and revenue projections for manufacturers.

Public health authorities have played a crucial role in shaping this trajectory. As part of this initiative, federal agencies have intensified efforts to promote vaping and nicotine replacement therapies, which do not require traditional ignition methods. Consequently, even as alternative uses for lighters grow, the loss of their primary consumer base presents a fundamental challenge to the market’s long-term stability, compelling industry players to adapt through diversification and product innovation.

MARKET OPPORTUNITIES

Expansion of Premium and Branded Lighter Segments Catering to Lifestyle Consumers

The rising popularity of premium and designer lighters among lifestyle-oriented consumers is a growing opportunity in the North American cigarette lighter market. Unlike commodity-based disposable lighters, these higher-end products appeal to collectors, fashion-conscious buyers, and those seeking personalized accessories. Luxury brands such as S.T. Dupont and Zippo have capitalized on this trend by offering engraved, limited-edition, and custom-designed models that extend beyond functional utility. This evolution presents a lucrative avenue for manufacturers to enhance profitability and brand equity, even amid declining smoking rates.

Integration of Eco-Friendly and Reusable Lighters in Response to Sustainability Trends

Amid growing environmental consciousness, the NorthAmericana cigarette lighter market is witnessing a shift toward reusable and eco-friendly alternatives, creating a new growth avenue for manufacturers. Traditional disposable butane lighters, which contribute significantly to plastic waste, are increasingly being replaced by refillable and metal-based options that align with sustainability goals. This has led to a surge in demand for durable, refillable lighters made from recyclable materials, particularly among environmentally aware millennials and Gen Z consumers.

In response, companies such as Colibri and Blazer have expanded their lines of sustainable lighters, incorporating features like adjustable flame control, wind resistance, and biodegradable components. Retailers and distributors have also begun promoting eco-conscious branding, leveraging certifications and marketing strategies that emphasize carbon footprint reduction. Educational campaigns conducted by environmental advocacy groups have further reinforced this shift, encouraging consumers to adopt reusable products. By aligning with broader sustainability movements, the lighter industry is tapping into a new customer base that values responsible consumption, thereby opening fresh opportunities for market differentiation and long-term resilience.

MARKET CHALLENGES

Competition from Electronic Ignition Alternatives Eroding Traditional Lighter Usage

The proliferation of electronic ignition alternatives, particularly electric lighters, plasma arc lighters, and rechargeable USB-powered models, is an emerging challenge for the NortAmericanca cigarette lighter market. These modern ignition devices offer greater durability, eliminate the need for flammable fuel, and cater to tech-savvy consumers seeking innovative and safer options.

In the United States, online retailers such as Amazon and Etsy have seen a surge in listings for plasma and arc lighters, many of which are marketed as "flameless," "windproof," and "eco-friendly." In Canada, similar trends are evident, particularly among younger demographics who prioritize convenience and digital integration. The rise of these alternatives poses a direct threat to conventional lighter manufacturers, forcing them to either innovate or risk losing market share to newer entrants capitalizing on technological disruption and changing consumer expectations.

Economic Volatility and Inflationary Pressures Affecting Consumer Purchasing Power

The NorAmericanica cigarette lighter market faces increasing vulnerability to macroeconomic fluctuations, particularly inflationary pressures and declining disposable incomes that influence consumer purchasing behavior. As essential yet discretionary items, cigarette lighters are sensitive to shifts in economic confidence and household budget constraints. This trend has been particularly evident in lower-income households, where cost considerations often lead to extended reuse of existing lighters or switching to cheaper alternatives, thus affecting overall market growth.

In Canada, rising interest rates and housing costs have similarly constrained consumer expenditure. As a result, retailers have observed a shift toward basic, economy-tier lighters rather than premium or specialty models. Mass discount chains have capitalized on this trend, offering private-label lighters at reduced prices, thereby squeezing margins for established brands. These economic headwinds present a significant challenge to market expansion, compelling manufacturers to recalibrate pricing strategies and promotional efforts to retain consumer interest amidst financial uncertainty.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product Type, Material Type, Distribution Channel, and Region. |

| Various Analyses Covered | Global, Regi,onal and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, Rest of North America |

| Market Leaders Profiled | BIC Corporation (BIC Group), Zippo Manufacturing Company, Tokai Corporation (Scripto brand), Clipper (Flamagas S.A.) / Cricket (Swedish Match), Colibri Group, S.T. Dupont, Visol, Integral Style, and XINHAI. |

SEGMENTAL ANALYSIS

By Product Type Insights

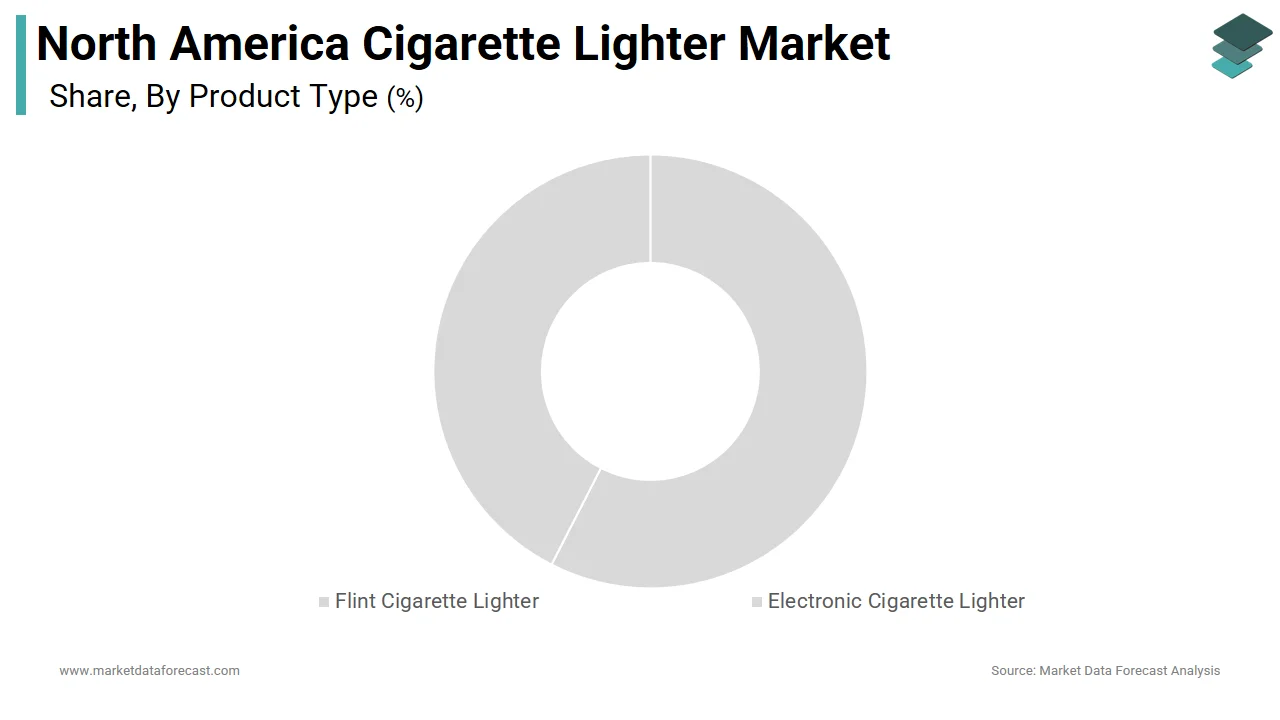

The flint cigarette lighter segment led the North America cigarette lighter market by accounting for 64.3% of total revenue in 2025. The dominance of this segment is primarily attributed to its widespread use across both traditional tobacco consumers and utility-driven applications such as camping, cooking, and emergency lighting. Despite declining smoking rates, flint lighters remain a staple due to their affordability, ease of use, and compatibility with hand-rolled cigarettes, which are preferred by a niche but persistent consumer base. Their integration into correctional facilities, military provisions, and institutional settings where safety and cost-efficiency are prioritized is also a key driver behind the continued prevalence of flint lighters. These factors strengthen the entrenched position of flint lighters within the broader market landscape.

The electronic cigarette lighter segment is emerging as the fastest-growing category in the North America market and is projected to expand at a CAGR of 13.6% from 2026 to 2034. A major growth catalyst of this segment is the rising popularity of rechargeable, USB-powered lighters among outdoor enthusiasts and urban users seeking windproof, long-lasting alternatives. Unlike conventional flint-based models, electronic lighters utilize plasma arc or electric ignition systems that eliminate open flames, offering enhanced safety and durability. This technological shift is particularly resonating with younger demographics who prioritize innovation, environmental sustainability, and digital convenience. Environmental advocacy groups have also endorsed these alternatives due to their reduced plastic waste footprint, further reinforcing market momentum and regulatory alignment.

By Material Type Insights

The plastic material segment continued to command the North America cigarette lighter market by capturing 59.3% of total sales volume in 2025. The overwhelming preference for plastic-based lighters stems from their low production costs, lightweight portability, and mass manufacturing scalability, which aligns well with the high-volume demands of discount retailers and tobacco vendors. Disposable plastic lighters, in particular, remain ubiquitous in convenience stores, gas stations, and vending outlets across the U.S. and Canada. This dominance is largely driven by the economic advantage they offer to both manufacturers and consumers. Despite growing environmental concerns, the sheer affordability and accessibility of plastic lighters continue to make them the most widely used material type, maintaining their stronghold in the regional market structure.

The metal-based cigarette lighters are experiencing the highest CAGR of 12.2% between 2025 and 2033. The growth of this segment is fueled by increasing demand for durable, refillable, and premium products, particularly among lifestyle-oriented consumers and outdoor activity enthusiasts. Unlike disposable plastic models, metal lighters are often associated with longevity, reusability, and aesthetic appeal, making them attractive to environmentally conscious buyers and collectors alike. With rising awareness around sustainability and personal expression, metal lighters are gaining traction not just as functional devices but as lifestyle accessories, contributing to their accelerated market expansion.

By Distribution Channel Insights

The convenience stores segment represented the largest distribution channel for cigarette lighters in North America by accounting for a 37.3% of total sales in 2025. The dominance of this segment is rooted in the strategic placement of lighters near point-of-sale areas, impulse buying tendencies, and the high foot traffic typical of these retail formats. Gas stations, mini-marts, and corner stores serve as primary access points for smokers seeking immediate replacements, particularly in urban and rural locations where tobacco availability is tightly regulated. A further strong driver of this segment is the integration of lighters into bundled promotions with tobacco products. In Canada, provincial liquor and tobacco control boards have also permitted lighter sales through authorized convenience outlets, ensuring a consistent supply. These factors solidify the stronghold of convenience stores in the lighter market distribution landscape.

The online distribution channel is emerging as the fastest-growing segment in the North America cigarette lighter market and is expanding at a CAGR of 14.8% from 2026 to 2034. This rapid ascent reflects shifting consumer preferences toward e-commerce platforms, where a wider variety of products, including luxury, novelty, and electronic lighters, are readily available with doorstep delivery. Unlike traditional retail environments, online stores offer curated selections, customer reviews, and direct brand engagement, enhancing the purchasing experience. Etsy also witnessed a surge in artisanal and personalized lighter sales, particularly among millennial buyers looking for unique gifts or collectibles. With rising smartphone adoption, improved logistics networks, and targeted digital marketing campaigns, online sales are reshaping the competitive dynamics of the lighter market, positioning it as a key growth engine moving forward.

COUNTRY-LEVEL ANALYSIS

United States Cigarette Lighter Market Insights

The United States dominated the North American cigarette lighter market by holding an estimated 66the % of regional revenue share in 2025. Despite declining smoking rates, the U.S. remains the largest consumer base due to its vast population, entrenched cultural habits, and robust retail infrastructure. Lighters are not only essential for tobacco users but also widely utilized in camping, culinary, and emergency preparedness contexts, broadening their functional reach beyond smoking. Coupled with strong brand presence from companies like Zippo and Bic, the U.S. market maintains a dominant yet evolving role in shaping North America’s cigarette lighter industry.

Canada Cigarette Lighter Market Insights

Canada is another key player in the North American cigarette lighter market, placing it second in regional significance. While smoking rates have steadily declined over the past decade, lighter consumption remains stable due to diverse usage scenarios, including outdoor recreation, utility applications, and institutional requirements. The Canadian government has implemented progressive tobacco control policies, yet lighters continue to be legally accessible, subject to age verification and packaging restrictions. With regulatory oversight balancing public health concerns and consumer needs, Canada’s cigarette lighter market remains resilient, adapting to changing behavioural and lifestyle patterns while maintaining a substantial regional footprint.

KEY MARKET PLAYERS

Noteworthy Companies dominating the North America cigarette lighter market profiled in the report are BIC Corporation (BIC Group), Zippo Manufacturing Company, Tokai Corporation (Scripto brand), Clipper (Flamagas S.A.) / Cricket (Swedish Match), Colibri Group, S.T. Dupont, Visol, Integral Style, and XINHAI.

TOP LEADING PLAYERS IN THE MARKET

Zippo Manufacturing Company is a dominant force in the North American cigarette lighter market, renowned for its durable, windproof, and refillable metal lighters. Beyond functionality, Zippo has built a strong brand identity through customization, collectibility, and lifestyle branding. The company continues to expand its presence by catering to niche markets such as outdoor enthusiasts, military personnel, and fashion-conscious consumers. Zippo’s long-standing reputation and innovation in design have allowed it to remain relevant even amid declining smoking rates.

Société Bic S.A., commonly known as BIC, is a global leader in disposable products and holds a substantial share of the cigarette lighter market in North America. BIC lighters are synonymous with affordability, reliability, and mass-market availability. Their products are widely distributed through convenience stores, gas stations, and vending machines, making them easily accessible to a broad consumer base. BIC's consistent product quality and strategic retail partnerships have solidified its position as a go-to brand for everyday users.

Colibri Lighters specializes in premium and luxury cigarette lighters tailored for cigar aficionados and discerning consumers. Known for their high-performance torch lighters, Colibri focuses on craftsmanship, durability, and aesthetic appeal. The brand has cultivated a loyal customer base within specialty tobacco shops and online platforms. By emphasizing superior build quality and advanced ignition technology, Colibri has successfully positioned itself in the upscale segment of the North American lighter market.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the NorthAmericana cigarette lighter market employ a range of strategies to maintain and enhance their competitive edge. One major approach is product diversification, where companies introduce a wide array of lighter types from disposable flint models to luxury and electronic variants to cater to different consumer preferences and usage scenarios. This allows brands to serve both traditional smokers and utility-driven buyers.

Another key strategy is brand differentiation, particularly through design, customization, and lifestyle marketing. Leading manufacturers invest in aesthetic appeal, limited editions, and engraving options to create emotional connections with consumers beyond functional utility.

Lastly, expanding distribution channels, especially into e-commerce and specialty retail, helps companies reach broader audiences. Brands are leveraging digital platforms, direct-to-consumer models, and partnerships with tobacconists to ensure greater visibility and accessibility across diverse consumer segments.

COMPETITION OVERVIEW

The competition in the NortAmericanca cigarette lighter market is shaped by a mix of established global brands and emerging niche players, each striving to capture distinct consumer segments. While traditional disposable lighter manufacturers focus on affordability and widespread availability, premium and specialty brands emphasize durability, aesthetics, and performance. This segmentation has led to a highly diversified marketplace where differentiation through product innovation, branding, and targeted marketing plays a crucial role in maintaining market relevance. As smoking rates continue to decline, companies are adapting by expanding into utility-based applications such as camping, survival gear, and personal accessories. Additionally, the rise of electronic and eco-friendly alternatives is introducing new players and technologies into the space, further intensifying competition. Retail partnerships, especially with convenience stores and online marketplaces, are also key battlegrounds for securing shelf space and consumer preference. In this evolving landscape, only those brands that can effectively balance tradition with innovation will sustain long-term success.

RECENT MARKET DEVELOPMENTS

- In January 2025, Zippo Manufacturing Company launched a new line of sustainable lighters made from recycled brass and biodegradable components, aiming to align with growing environmental consciousness among consumers while reinforcing its premium brand positioning.

- In March 2025, Société Bic S.A. expanded its distribution network by entering into exclusive supply agreements with several major U.S. convenience store chains, ensuring broader retail visibility and reinforcing its dominance in the disposable lighter segment.

- In June 2025, Colibri Lighters introduced an updated collection of dual-torch lighters featuring adjustable flame control and ergonomic designs, targeting premium cigar users and enhancing its foothold in the luxury segment of the market.

- In September 2025, a leading independent lighter distributor partnered with a major e-commerce logistics provider to streamline delivery times and improve inventory management across North America, strengthening online sales capabilities and customer satisfaction.

- In November 2025, a consortium of North American lighter manufacturers collaborated on a joint initiative to promote responsible use and safety awareness, engaging in public education campaigns to counter regulatory pressures and support continued market access.

MARKET SEGMENTATION

This North America cigarette lighter market research report is segmented and sub-segmented into the following categories.

By Product Type

- Flint Cigarette Lighter

- Electronic Cigarette Lighter

- Others

By Material Type

- Metal

- Plastic

- Others

By Distribution Channel

- Tobacco Shops

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What product types are most common in the North America Cigarette Lighter Market?

Flint cigarette lighters hold the largest share, followed by electronic lighters and other variants, catering to both affordability and innovation preferences

2. Which material dominates the North America Cigarette Lighter Market?

Plastic cigarette lighters are the most dominant, valued for their affordability, durability, and widespread availability; metal lighters remain significant for premium and decorative segments

3. What are the key growth drivers for the North America Cigarette Lighter Market?

Growth is driven by the steady smoking population, the launch of new flavored cigarettes and cigars, optionality in lighter types, busy urban lifestyles, and growing demand for both utility and collectible lighters

4. How is innovation shaping the North America Cigarette Lighter Market?

Manufacturers are introducing advanced models—such as battery-powered, rechargeable, windproof, and luxury decorative lighters—to enhance functionality and appeal

5. How are distribution channels structured in the North America Cigarette Lighter Market?

Key channels include tobacco shops, supermarkets/hypermarkets, convenience stores, and, increasingly, online retail platforms reflecting the digital buying trend

6. Which regions lead the North America Cigarette Lighter Market?

The United States is the leading market, supported by high consumer numbers and robust retail infrastructure, followed by Canada

7. What are the main consumer trends in the North America Cigarette Lighter Market?

Trends include rising demand for luxury and customizable lighters, premium gifting, and increased use of lighters for outdoor activities beyond smoking

8. What is the impact of online sales on the North America Cigarette Lighter Market?

E-commerce is rapidly growing, with consumers shifting from brick-and-mortar stores to online channels for greater variety and convenience

9. How is the market responding to sustainability and regulation in the North America Cigarette Lighter Market?

There is a shift toward recyclable plastic lighters and compliance with safety standards, as well as increased adoption of refillable and rechargeable lighters to reduce waste

10. Who are the leading players in the North America Cigarette Lighter Market?

Major brands include Zippo Manufacturing Company, BIC SA, S.T. Dupont, Calico Brands Inc., and several regional manufacturers

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com