North America Concrete Superplasticizer Market Size, Share, Trends & Growth Forecast Report By Type (PCE, SNF, SMF, MLS, Others), Application, Form and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

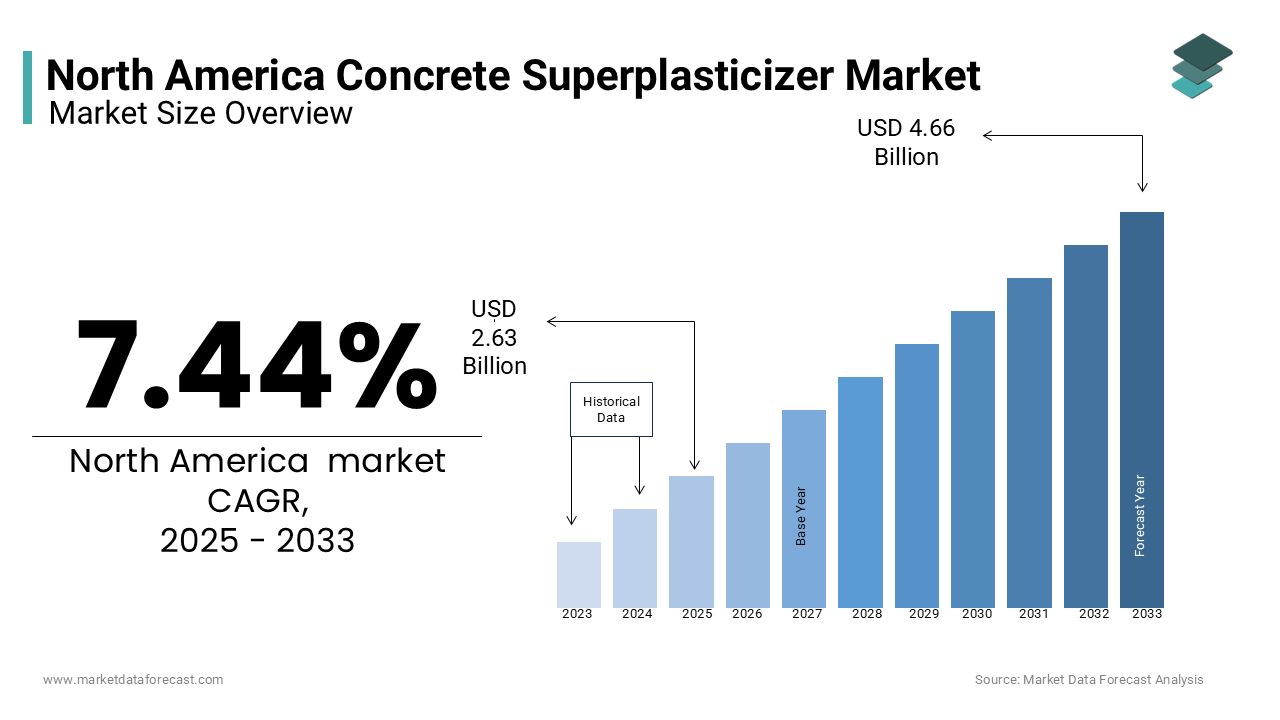

Market Size, 2025

$2.63 BnMarket Estimate, 2026

$2..83 BnMarket Forecast, 2034

$5.02 BnCAGR, 2026–2034

7.44%North America Concrete Superplasticizer Market Report Summary

The North America concrete superplasticizer market was valued at USD 2.63 billion in 2025 and is anticipated to reach USD 2.83 billion in 2026 from USD 5.02 billion by 2034, growing at a CAGR of 7.44% during the forecast period from 2026 to 2034. The growth of the North America concrete superplasticizer market is driven by rising infrastructure investments, increasing urbanization, and growing demand for high-performance and durable concrete across residential, commercial, and industrial construction projects. Expanding adoption of sustainable construction practices, increasing utilization of self-compacting and high-strength concrete, and rising investments in transportation and public infrastructure modernization are further accelerating market growth. Moreover, continuous advancements in polymer chemistry, increasing adoption of prefabricated construction methods, and growing demand for environmentally friendly admixtures are supporting the expansion of the North America concrete superplasticizer market.

Key Market Trends

-

Rising adoption of polycarboxylate ether (PCE)-based superplasticizers for high-performance concrete applications.

-

Increasing utilization of self-compacting and high-strength concrete in large-scale infrastructure projects.

-

Growing demand for sustainable and low-carbon concrete formulations incorporating supplementary cementitious materials.

-

Rising adoption of prefabricated and modular construction techniques requiring advanced concrete admixtures.

-

Increasing development of bio-based and environmentally friendly superplasticizer formulations.

Segmental Insights

- Based on type, the polycarboxylate ether (PCE) segment dominated the North America concrete superplasticizer market and accounted for 65.8% of the market share in 2025. The dominance of the segment is attributed to its superior water-reducing capability, excellent slump retention, enhanced compressive strength, compatibility with supplementary cementitious materials, and increasing adoption in high-performance and self-compacting concrete applications. Continuous technological advancements and widespread infrastructure development further strengthen segment growth.

- The modified lignosulphonates (MLS) segment is projected to witness a CAGR of 4.2% during the forecast period owing to its cost-effectiveness, renewable raw material base, increasing demand for bio-based construction chemicals, and expanding adoption in residential and general-purpose concrete applications. Improvements in modification technologies continue to enhance its performance and market acceptance.

- Based on application, the ready-mix concrete segment dominated the North America concrete superplasticizer market in 2025. The segment’s growth is driven by increasing construction activities, growing urbanization, rising demand for consistent concrete quality, expanding use of pumpable concrete, and increasing adoption of ready-mix solutions across residential, commercial, and infrastructure projects. The widespread utilization of superplasticizers to improve workability and transportation efficiency further supports market dominance.

- The high-performance concrete segment is anticipated to register the fastest CAGR of 6.8% during the forecast period due to increasing investments in bridges, tunnels, highways, airports, and energy infrastructure, growing demand for durable construction materials, rising implementation of stringent building standards, and expanding adoption of ultra-high-performance concrete technologies.

Regional Insights

- The United States dominated the North America concrete superplasticizer market and accounted for 75.5% of the regional market share in 2025. The country's leadership is driven by record construction spending, major federal infrastructure investments, extensive highway and bridge rehabilitation projects, strong adoption of advanced construction chemicals, and continuous innovation by leading admixture manufacturers. Expanding commercial and residential construction activities further contribute to market growth.

- Canada held a significant share of the North America concrete superplasticizer market owing to increasing government investments in public infrastructure, growing emphasis on sustainable construction, expanding high-rise residential developments, and rising demand for freeze-thaw resistant concrete. The country's strong environmental regulations and adoption of low-carbon construction materials continue to support market expansion.

- The Rest of North America, led primarily by Mexico, is witnessing steady growth supported by increasing industrialization, expanding transportation infrastructure, rising commercial construction activities, and growing investments in manufacturing facilities and logistics infrastructure. Government infrastructure development programs and increasing urbanization continue to create favorable opportunities for the adoption of advanced concrete admixtures across the region.

Competitive Landscape

The North America concrete superplasticizer market is highly competitive and characterized by the presence of multinational construction chemical manufacturers competing through product innovation, sustainability initiatives, strategic acquisitions, and expansion of manufacturing capabilities. Leading companies are focusing on developing advanced polycarboxylate ether technologies, bio-based admixtures, customized concrete solutions, and digital quality control systems to improve construction efficiency and environmental performance. Strategic collaborations with ready-mix concrete producers, infrastructure developers, and research institutions continue to strengthen competitive positioning across the North America concrete superplasticizer market. The prominent players operating in the North America concrete superplasticizer market include BASF SE, Sika AG, GCP Applied Technologies, MAPEI Corporation, Arkema Group, and RPM International Inc.

North America Concrete Superplasticizer Market Size

The North America concrete superplasticizer market was worth USD 2.63 billion in 2025. The North America market is expected to reach USD 5.02 billion by 2034 from USD 2.83 billion in 2026, rising at a CAGR of 7.44% from 2026 to 2034.

Concrete superplasticizers are high range water reducing admixtures that significantly enhance the workability and flow characteristics of concrete mixtures without compromising structural integrity. These chemical additives disperse cement particles effectively allowing for reduced water content while maintaining desired consistency which results in higher compressive strength and durability. The North America Concrete Superplasticizer Market serves critical infrastructure development needs across the United States Canada and Mexico by enabling advanced construction techniques such as self compacting concrete and high performance concrete formulations. The region benefits from robust industrial activity and continuous modernization of transportation networks which drives consistent demand for specialized construction chemicals. According to the U.S. Census Bureau, the total annual value of construction put in place in the United States reached $1,978.7 billion in 2023, representing a 7% increase over 2022 and reflecting substantial ongoing investments in residential, nonresidential, and public infrastructure projects. As per Statistics Canada macroeconomic data, the construction industry contributed 7.2% to the national Gross Domestic Product (GDP), underscoring its pivotal role in generating investments and economic stability across Canadian provinces. The Mexican Institute of Social Security (IMSS) reported that formal employment in the construction sector surged by 9.2% year-over-year in 2023, driven primarily by major public infrastructure works and expanding industrial real estate. These macroeconomic indicators underscore the foundational importance of construction activities which directly correlate with the consumption of performance enhancing admixtures like superplasticizers. The market operates within a framework of stringent environmental regulations and evolving building codes that prioritize sustainability and longevity of structures. Technological advancements in polymer chemistry continue to refine product efficacy ensuring compatibility with diverse cement types and aggregate compositions used across the continent.

MARKET DRIVERS

Surging Infrastructure Investment and Urbanization Trends

The relentless pace of urbanization and massive government backed infrastructure initiatives drives the growth of the North America concrete superplasticizer market. Rapid population growth in metropolitan areas necessitates the construction of high rise buildings bridges and transit systems that require high strength and durable concrete solutions. Superplasticizers enable the production of high performance concrete which is essential for these complex structures due to their ability to reduce permeability and increase load bearing capacity. The Infrastructure Investment and Jobs Act in the United States allocates 110 billion dollars specifically for roads bridges and major infrastructure projects which will significantly boost demand for advanced construction materials over the next decade. As per the American Society of Civil Engineers, the national infrastructure grade reached a "C" in its latest report card, indicating that while progress has been made, a substantial backlog of repair and maintenance projects still requires efficient and durable concrete mixes. In Canada the federal government committed 180 billion dollars through the Investing in Canada plan to support public transit green infrastructure and community projects which further stimulates market growth. Urban density increases the need for vertical construction where space constraints demand concrete with superior flow properties to ensure complete filling of complex formworks. Superplasticizers facilitate this by allowing lower water cement ratios which enhances early age strength and reduces curing time. This efficiency is crucial for meeting tight project deadlines in urban environments. The trend toward sustainable urban development also favors superplasticizers as they contribute to longer lasting structures with reduced maintenance needs. Thus, the synergy between policy driven funding and demographic shifts creates a robust demand environment for these essential chemical admixtures.

Growing Preference for Sustainable and High Performance Concrete

The increasing emphasis on sustainability and environmental responsibility in the construction industry propels the North America concrete superplasticizer market forward. Builders and developers are increasingly prioritizing green building certifications such as Leadership in Energy and Environmental Design which encourage the use of materials that reduce carbon footprints and enhance energy efficiency. Superplasticizers play a vital role in this transition by enabling the use of supplementary cementitious materials like fly ash and slag which replace portions of Portland cement and lower overall carbon emissions. According to the Portland Cement Association Roadmap to Carbon Neutrality, the broader adoption of supplementary cementitious materials (SCMs) and blended cements serves as a primary, immediate mechanism for reducing the carbon intensity of concrete manufacturing across North America. Superplasticizers ensure that these alternative mixes maintain adequate workability and strength despite the reduced cement content. The National Ready Mixed Concrete Association reports that ready-mixed concrete producers are increasingly standardizing low-carbon and high-performance mix designs, leveraging specialized high-range water reducers (superplasticizers) to satisfy rigorous carbon reduction and strength criteria. Additionally the durability imparted by superplasticizers extends the service life of structures thereby reducing the frequency of repairs and replacements which conserves resources and minimizes waste. Regulatory bodies are implementing stricter standards for concrete durability in harsh weather conditions particularly in regions prone to freeze thaw cycles. Superplasticizers help achieve the low permeability required to resist such damage. This alignment with regulatory requirements and corporate sustainability goals ensures steady demand growth. Manufacturers are also developing bio based superplasticizers to further enhance the eco friendly profile of construction projects. Hence, the drive toward greener construction practices fundamentally supports the expansion of the superplasticizer market.

MARKET RESTRAINTS

Volatility in Raw Material Prices and Supply Chain Disruptions

Fluctuating costs of key raw materials and persistent supply chain vulnerabilities impede the growth of the North America concrete superplasticizer market. Superplasticizers are primarily synthesized from petrochemical derivatives such as naphthalene formaldehyde and polycarboxylate ethers which are directly linked to crude oil prices. Geopolitical tensions and global economic uncertainties cause erratic swings in oil prices which subsequently impact the cost structure of admixture manufacturers. According to the United States Energy Information Administration the average price of West Texas Intermediate crude oil fluctuated between 70 and 95 dollars per barrel in 2023 creating unpredictability in production costs for chemical manufacturers. These cost variations often force producers to adjust pricing strategies which can dampen demand from price sensitive construction firms operating on fixed budgets. Furthermore the supply chain for specialized chemicals remains fragile due to logistical bottlenecks and labor shortages in the transportation sector. The American Trucking Associations reported a national deficit of approximately 64,000 truck drivers in 2023, creating persistent transportation bottlenecks for bulk chemical products traveling to major project sites. Delays in raw material imports from Asia and Europe exacerbate these issues leading to production slowdowns and inventory shortages. Construction projects operate on tight schedules and any delay in material availability can result in costly penalties and project extensions. Manufacturers struggle to maintain consistent profit margins amidst these volatile conditions which may limit their ability to invest in research and development. Small and medium sized enterprises are particularly vulnerable as they lack the financial buffers to absorb sudden cost spikes. This economic instability acts as a considerable restraint on market expansion and operational efficiency.

Stringent Environmental Regulations and Compliance Costs

Strict environmental regulations governing the production, disposal, and usage of chemical admixtures impose substantial compliance burdens on manufacturers within North America concrete superplasticizer market. Agencies such as the Environmental Protection Agency in the United States and Environment and Climate Change Canada enforce rigorous standards to minimize the ecological impact of industrial chemicals. These regulations mandate extensive testing monitoring and reporting which increase operational costs and extend time to market for new products. Regulatory analyses from the U.S. Environmental Protection Agency show that adapting manufacturing operations to evolving environmental standards imposes significant structural compliance costs and administrative demands on chemical and industrial producers. The restriction of certain hazardous substances in superplasticizer formulations requires manufacturers to reformulate products using safer but often more expensive alternatives. This transition involves significant research and development expenditure and potential performance trade offs that must be carefully managed. Additionally the disposal of waste generated during production is subject to strict guidelines which necessitate investment in advanced waste treatment facilities. Non compliance can result in hefty fines legal liabilities and reputational damage which deter market entry for smaller players. The complexity of navigating differing regulatory landscapes across states and provinces further complicates operations for multinational companies. For instance California has some of the strictest air quality standards which require additional mitigation measures for chemical plants. These regulatory pressures limit the flexibility of manufacturers to innovate rapidly and scale production efficiently. Therefore, the high cost of compliance acts as a barrier to growth and reduces the overall profitability of the superplasticizer segment in the region.

MARKET OPPORTUNITIES

Expansion of Prefabricated and Modular Construction Techniques

The rapid adoption of prefabricated and modular construction methods unlocks potential for the North America concrete superplasticizer market. Prefabrication involves manufacturing building components in controlled factory environments before transporting them to the construction site for assembly. This approach requires concrete mixes with precise workability and rapid setting characteristics to ensure high quality output and efficient production cycles. Superplasticizers are indispensable in this context as they enable the creation of flowable concrete that fills intricate molds uniformly without segregation. According to the Modular Building Institute (MBI), the market share for permanent modular construction in North America has continued its steady multi-year expansion, heavily driven by commercial real estate and multifamily housing developers aiming to accelerate project timelines and minimize on-site labor deficits. Factories benefit from the consistency provided by superplasticizers which minimizes defects and rework rates. The ability to produce high strength elements quickly allows manufacturers to meet tight delivery schedules demanded by commercial and residential developers. Furthermore prefabrication reduces on site waste and environmental disruption aligning with sustainability goals. Superplasticizers facilitate the use of thinner sections and lighter components which lowers transportation costs and simplifies handling. The trend toward off site construction is expected to accelerate as labor shortages persist in the traditional construction sector. Manufacturers of superplasticizers can capitalize on this shift by developing specialized formulations tailored for precast applications. Collaborations with prefabrication firms can lead to customized solutions that optimize production efficiency. This segment offers stable and growing demand as the construction industry increasingly embraces industrialized building processes to enhance productivity and quality control.

Advancements in Nanotechnology and Smart Admixtures

Emerging innovations in nanotechnology and smart admixtures offer significant growth prospects for the North America concrete superplasticizer market. Researchers are developing nano modified superplasticizers that incorporate nanoparticles such as silica alumina and carbon nanotubes to enhance mechanical properties and durability at the molecular level. These advanced admixtures improve the microstructure of concrete by filling voids and strengthening the bond between cement paste and aggregates. Multi-agency funding frameworks under the National Nanotechnology Initiative (NNI) provide key institutional grants to academic labs developing advanced, autonomous nanoscale properties, laying the groundwork for stronger, smart construction admixtures and nanomaterials. Smart admixtures equipped with sensors or responsive polymers can monitor structural health and adjust properties in real time based on environmental conditions. This capability is particularly valuable for critical infrastructure such as bridges and dams where early detection of stress or damage is crucial. The integration of digital technologies with chemical admixtures enables predictive maintenance and extends the lifespan of structures. Construction firms are increasingly interested in these high value solutions that offer long term cost savings despite higher initial prices. Partnerships between chemical manufacturers and technology firms can accelerate the commercialization of these innovative products. Regulatory agencies are beginning to recognize the benefits of smart materials which may lead to favorable policies and incentives. The premium nature of nano enhanced superplasticizers allows manufacturers to differentiate their offerings and capture higher margins. As awareness of these benefits grows adoption rates are expected to rise particularly in high profile and high risk construction projects. This technological frontier represents a transformative opportunity for market leaders to redefine performance standards.

MARKET CHALLENGES

Lack of Skilled Labor and Technical Expertise

The shortage of skilled labor and technical expertise required for the proper application and handling of advanced admixtures is a critical obstruction for the North America Concrete Superplasticizer Market. Superplasticizers require precise dosing and mixing protocols to achieve optimal performance and incorrect usage can lead to severe quality issues such as segregation excessive air entrainment or delayed setting. According to national workforce tracking data from the Associated General Contractors of America (AGC), approximately 80% of construction contractors report persistent difficulties filling skilled craft worker positions, highlighting a deep structural skills gap across the infrastructure and building sectors. Many on site personnel lack comprehensive training on the chemical properties and interaction mechanisms of superplasticizers with other concrete constituents. This knowledge deficit often results in suboptimal mix designs and compromised structural integrity which undermines confidence in the technology. Educational institutions and vocational training programs have not kept pace with the rapid evolution of construction chemicals leaving a void in practical expertise. Manufacturers face challenges in providing adequate technical support to a dispersed and transient workforce. Misapplication can lead to costly remediation efforts and legal disputes which deter contractors from adopting newer admixture technologies. The complexity of modern concrete mixes which often include multiple admixtures further exacerbates the need for specialized knowledge. Without a skilled workforce the full potential of superplasticizers cannot be realized limiting market penetration. Addressing this challenge requires coordinated efforts between industry stakeholders educational bodies and government agencies to develop standardized training curricula. Until this skills gap is bridged, the market will continue to face implementation hurdles. These barriers will continue to restrict growth and innovation.

Compatibility Issues with Diverse Cement and Aggregate Types

Ensuring compatibility between superplasticizers and the wide variety of cement types and aggregates available in the region is a significant technical challenge for the North America concrete superplasticizer market. Cement composition varies considerably depending on the source of raw materials and manufacturing processes which affects how superplasticizers interact with the mixture. Aggregates also differ in mineralogy surface texture and absorption characteristics influencing the effectiveness of dispersion. Research compiled by materials scientists and industrial bodies like the Federal Highway Administration demonstrates that chemical incompatibilities between complex cement chemistries, aggregates, and advanced chemical admixtures frequently induce rapid slump loss, cracking, and early-age stiffening in field operations. Manufacturers must conduct extensive testing to formulate superplasticizers that perform consistently across different material combinations which increases development time and costs. Field conditions often deviate from laboratory settings making it difficult to predict performance accurately. Variations in temperature humidity and mixing energy further complicate the interaction dynamics leading to unpredictable results. Contractors may encounter issues such as slump loss or excessive bleeding if the superplasticizer is not properly matched to the local materials. This uncertainty creates reluctance among specifiers to adopt new products without prolonged trial periods. The lack of universal standards for compatibility testing adds to the complexity requiring customized solutions for each project. Manufacturers struggle to balance broad applicability with specialized performance leading to a fragmented product landscape. Continuous monitoring and adjustment are necessary to maintain quality which strains resources. Overcoming this challenge requires deeper collaboration between cement producers aggregate suppliers and admixture manufacturers to establish better predictive models and standardized testing protocols.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| CAGR | 7.44% |

| Segments Covered | By Type, Application, Form, and Region. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Regions Covered | United States, Canada, and the Rest of North America. |

| Market Leaders Profiled | BASF SE, Sika AG, GCP Applied Technologies, MAPEI Corporation, Arkema Group, and RPM International Inc. |

SEGMENTAL ANALYSIS

By Product Insights

The polycarboxylate ether-based segment was the largest in the North America concrete superplasticizer market and occupied a 65.8% share in 2025. This dominance of the segment was mainly supported by the superior performance characteristics of polycarboxylate ether polymers, which offer exceptional water reduction capabilities and high slump retention compared to traditional lignosulphonates. These advanced admixtures enable the production of high strength concrete with significantly lower water cement ratios which enhances durability and compressive strength essential for modern infrastructure projects. The construction industry increasingly prioritizes long term structural integrity and reduced maintenance costs which aligns perfectly with the benefits provided by polycarboxylate ether based superplasticizers. According to technical guidelines from the American Concrete Institute, the addition of high-range water reducers drastically reduces water-to-cement ratios, allowing concrete compressive strengths to increase by more than 20% while decreasing permeability to significantly extend structural service life. Major infrastructure initiatives such as bridge repairs and highway expansions require materials that withstand harsh environmental conditions including freeze thaw cycles and chemical exposure. Polycarboxylate ether based products provide the necessary resistance to these stressors ensuring compliance with stringent building codes. Manufacturers are investing heavily in research and development to customize polycarboxylate ether formulations for specific applications such as self compacting concrete and precast elements. The versatility of these polymers allows for compatibility with various cement types and supplementary cementitious materials like fly ash and slag. This adaptability supports sustainable construction practices by facilitating the use of industrial byproducts. The widespread adoption of ready mix concrete services further boosts demand as producers seek consistent and reliable admixture performance. Consequently the technical superiority and broad applicability of polycarboxylate ether based superplasticizers secure their dominant market position.

On the contrary, the modified lignosulphonates segment is growing at a moderate CAGR of 4.2% from 2026 to 2034 due to its affordability and suitability for general purpose concrete applications. Modified lignosulphonates are derived from renewable biomass sources specifically wood pulp processing byproducts which appeals to environmentally conscious builders seeking bio based alternatives. The production process for lignosulphonates is less energy intensive compared to synthetic polymers which reduces the overall carbon footprint of concrete manufacturing. Research shows that Canada's pulp and paper industry produces significant volumes of raw lignin liquors, with primary biorefineries processing these byproducts into commercial-grade modified lignosulphonates to ensure a stable supply chain for standard water-reducing admixtures. This abundance ensures consistent availability and competitive pricing which attracts budget sensitive construction projects such as residential housing and low rise commercial buildings. Recent advancements in modification technologies have improved the performance of lignosulphonates enhancing their water reduction efficiency and compatibility with other admixtures. These improvements expand their applicability beyond basic uses into more demanding scenarios where moderate performance is sufficient. Government incentives for using bio based construction materials further support market growth as policies encourage the reduction of fossil fuel dependence. Small and medium sized contractors prefer modified lignosulphonates due to their ease of handling and lower risk of adverse reactions with local aggregates. The segment benefits from ongoing innovation in purification processes that remove impurities and improve consistency. As sustainability becomes a central theme in construction the demand for renewable admixtures like modified lignosulphonates continues to rise steadily.

By Application Insights

The ready mix Concrete segment dominated the North America Concrete Superplasticizer Market and accounted for a substantial share in 2025. This dominance of the segment was driven by the extensive use of ready mix concrete in residential commercial and infrastructure projects across the United States Canada and Mexico. Ready mix concrete offers convenience consistency and quality control which are critical for large scale construction operations that require timely delivery and uniform performance. Superplasticizers are essential in ready mix formulations to maintain workability during transportation and placement especially in hot weather conditions or over long distances. According to data from the National Ready Mixed Concrete Association, the United States ready-mix concrete industry produced and delivered approximately 400 million cubic yards of concrete in 2023, reflecting immense market volume and widespread demand for chemical admixtures. The ability of superplasticizers to reduce water content without sacrificing flow allows producers to achieve higher strength grades while optimizing material costs. Urbanization trends drive the need for efficient construction methods where ready mix concrete plays a pivotal role in meeting tight project schedules. Contractors rely on the predictability of ready mix supplies to minimize on site mixing errors and labor requirements. Superplasticizers enhance the pumpability of concrete which is crucial for high rise buildings and complex architectural designs. The integration of digital tracking systems in ready mix trucks improves logistics and ensures timely delivery further boosting sector efficiency. Environmental regulations promoting reduced cement usage also favor ready mix producers who utilize superplasticizers to incorporate supplementary cementitious materials effectively. This segment remains robust due to its foundational role in the construction ecosystem and continuous adaptation to evolving market needs.

The high performance concrete segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 6.8% during the forecast period owing to the increasing demand for durable and high strength materials in critical infrastructure projects such as bridges tunnels and offshore platforms. High performance concrete requires precise engineering and advanced admixtures to achieve compressive strengths exceeding 6000 pounds per square inch and enhanced durability against aggressive environments. Superplasticizers are indispensable in these formulations as they enable extremely low water cement ratios while maintaining adequate workability for placement. Federal highway data and infrastructure report cards indicate that while roughly 42% of U.S. bridges are over 50 years old, roughly 7.5% are classified in poor or structurally deficient condition, creating an ongoing need for rehabilitation using high-performance repair materials. The longevity of high performance concrete reduces lifecycle costs which appeals to government agencies and private developers focused on sustainable infrastructure. Innovations in nanotechnology and fiber reinforcement are often combined with superplasticizers to create ultra high performance concrete variants with exceptional mechanical properties. The energy sector also drives demand as wind turbine foundations and nuclear power plant structures require materials capable withstanding extreme loads and radiation exposure. Research institutions collaborate with manufacturers to develop customized superplasticizer solutions that optimize microstructure and minimize shrinkage cracking. Regulatory standards for seismic resilience in earthquake prone regions further mandate the use of high performance concrete in new constructions. As infrastructure aging becomes a critical issue the adoption of high performance concrete supported by advanced superplasticizers will continue to accelerate significantly.

COUNTRY ANALYSIS

The United States led the North America Concrete Superplasticizer Market and captured a 75.5% share in 2025. The country maintains its position due to the sheer scale of its construction industry and massive federal investment in infrastructure modernization. According to annual data released by the U.S. Census Bureau, total U.S. construction spending reached a record high of $1.979 trillion in 2023. This was heavily driven by nonresidential construction, with private nonresidential expenditures soaring by 16.7% year-over-year to $713.4 billion. The presence of major chemical manufacturers and advanced research facilities fosters innovation in superplasticizer technologies tailored to diverse regional climate conditions. The shale gas boom has also increased demand for concrete in energy infrastructure including pipelines and processing plants. Urban redevelopment projects in major cities require high performance materials to support vertical construction and dense urban fabrics. The United States benefits from a well established distribution network and strong technical support infrastructure which facilitates widespread product adoption. Collaboration between academic institutions and industry players accelerates the development of next generation admixtures. Economic stability and consumer confidence support continued investment in residential and commercial real estate. These factors collectively ensure that the United States remains the primary engine of growth for the concrete superplasticizer market in North America.

Canada was positioned second in the North America Concrete Superplasticizer Market. The country exhibits strong market status driven by significant government spending on public infrastructure and a growing focus on sustainable construction practices. Harsh winter conditions in many provinces necessitate the use of durable concrete mixes with high resistance to freeze thaw cycles which superplasticizers help achieve by reducing permeability. The prevalence of hydroelectric and mining projects in remote areas requires specialized concrete formulations that can be transported and placed efficiently under challenging conditions. Canadian manufacturers are increasingly adopting eco friendly admixtures to align with national carbon reduction targets and environmental regulations. The housing market remains active particularly in urban centers like Toronto and Vancouver where high rise developments rely on high performance concrete. Trade agreements facilitate the import of raw materials and export of finished products enhancing market dynamics. Research initiatives by universities and government labs promote innovation in bio based superplasticizers derived from local forestry byproducts. The skilled workforce and strict quality standards ensure consistent product performance and reliability. These elements support steady market growth and position Canada as a key contributor to regional demand.

COMPETITIVE LANDSCAPE

The competition in the North America concrete superplasticizer market is characterized by intense rivalry among established multinational corporations and specialized regional manufacturers. Leading companies differentiate themselves through technological innovation product reliability and comprehensive technical support services. The market features a mix of large chemical conglomerates and niche players focusing exclusively on construction admixtures. Competitive dynamics are driven by the need for continuous improvement in performance metrics such as slump retention and early strength development. Price competition remains moderate as customers prioritize quality assurance and regulatory compliance over cost savings alone. Strategic alliances with cement producers and ready mix companies are common to create integrated supply chain solutions. Intellectual property protection plays a crucial role in maintaining competitive advantages and preventing imitation of proprietary polymer technologies. Geographic expansion into underserved regions intensifies competition as local manufacturers gain technical capabilities. Customer retention strategies include long term supply contracts and customized application development support. The entry of new players with sustainable bio based products poses ongoing challenges to incumbent firms requiring constant adaptation. Regulatory standards create barriers to entry but also ensure quality consistency across the market. Overall the competitive landscape fosters innovation and drives continuous improvement in admixture technologies benefiting the construction industry globally.

KEY MARKET PLAYERS

Some of the key market players in the North America concrete superplasticizer market include

- BASF SE

- Sika AG

- GCP Applied Technologies

- MAPEI Corporation

- Arkema Group

- RPM International Inc.

Top Players in the North America Concrete Superplasticizer Market

GCP Applied Technologies

GCP Applied Technologies stands as a pivotal leader in the North America concrete admixture sector by delivering advanced chemical solutions for infrastructure and commercial construction. The company specializes in high performance polycarboxylate ether based superplasticizers that enhance workability and durability for complex projects. GCP recently expanded its production capabilities in the United States to meet rising demand from large scale infrastructure initiatives. Their commitment to sustainability drives the development of low carbon footprint admixtures that support green building certifications. The company actively collaborates with ready mix producers to optimize mix designs for specific regional climate conditions. Continuous investment in research ensures their products remain compliant with evolving environmental regulations. GCP also provides extensive technical support services to help contractors achieve optimal placement and finishing results. These strategic efforts reinforce their reputation for innovation and reliability in the competitive North American market landscape.

Sika AG

Sika AG contributes significantly to the North America concrete superplasticizer market through its comprehensive portfolio of construction chemicals and specialized admixtures. The company emphasizes digital integration and automated dosing systems to improve precision and efficiency for concrete producers. Sika recently launched new generations of superplasticizers designed for self compacting concrete applications which align with modern architectural trends. Their focus on lifecycle cost reduction helps clients achieve long term durability and lower maintenance expenses. The company strengthens its regional presence by acquiring local distributors and expanding manufacturing facilities in key states. Strategic partnerships with engineering firms foster innovation in high strength and ultra high performance concrete formulations. Sika prioritizes customer education through technical workshops and on site training programs. These initiatives solidify their position as a trusted partner for complex construction challenges across the continent.

BASF SE

BASF SE plays a vital role in the North America concrete superplasticizer market by offering master builders solutions that optimize concrete performance and sustainability. The company leverages its global expertise in polymer chemistry to develop customized admixtures for diverse application needs. BASF recently strengthened its market position by introducing bio based superplasticizers derived from renewable resources to support eco friendly construction practices. The company focuses on reducing water consumption and cement usage which lowers the overall carbon footprint of concrete production. Collaborations with academic institutions enable the development of next generation materials with enhanced mechanical properties. BASF invests heavily in digital tools that allow real time monitoring of concrete quality during mixing and placement. Their commitment to circular economy principles drives innovation in recycling compatible admixtures. These actions ensure sustained growth and competitiveness in the evolving North American construction chemicals landscape.

Top Strategies Used by the Key Market Participants

Key players in the North America concrete superplasticizer market primarily focus on product innovation and strategic expansions to maintain competitive advantage. Companies invest heavily in research and development to create advanced polycarboxylate ether formulations with higher water reduction capabilities. Expansion into emerging infrastructure markets through localized production facilities helps capture growing demand in urban centers. Strategic acquisitions allow firms to broaden their distribution networks and access proprietary technologies quickly. Collaboration with ready mix concrete producers enables customization of solutions for specific regional climate challenges. Emphasis on sustainable and bio based admixtures supports green building initiatives and regulatory compliance. Digital integration and automated dosing features enhance process control and consistency for large scale projects. Customer education and technical support services strengthen long term relationships and brand loyalty. These strategies collectively drive market growth and ensure sustained leadership positions for major participants in the regional industry.

RECENT MARKET DEVELOPMENTS

- In March 2023, BASF SE launched MasterGlenium ACE 8800, a next-generation polycarboxylate ether (PCE) superplasticizer designed for high-performance concrete applications. This product introduction expanded BASF’s offerings and addressed consumer demands for superior slump retention and early strength development.

- In June 2023, Sika AG partnered with Habitat for Humanity, donating over 500 tons of concrete admixtures for affordable housing projects across North America. This initiative not only supported community development but also enhanced Sika’s brand visibility and reputation.

- In September 2023, W.R. Grace & Co. acquired Allentown Technologies, a leader in sustainable admixture formulations. This acquisition broadened Grace’s product range, enabling it to offer comprehensive eco-friendly solutions for modern construction needs.

- In December 2023, Fosroc introduced Conplast SP430, a bio-based superplasticizer crafted from renewable resources. This launch aligned with growing consumer demand for sustainable and eco-friendly construction materials, reinforcing Fosroc’s commitment to environmental stewardship.

- In February 2024, Mapei Corporation implemented AI-driven quality control systems across its production facilities. This technological upgrade improved operational efficiency, reduced waste, and ensured consistent product quality, strengthening Mapei’s competitive position in the market.

MARKET SEGMENTATION

This research report on the North America concrete superplasticizer market is segmented and sub-segmented into the following categories.

By Type

- PCE

- SNF

- SMF

- MLS

- Others

By Application

- Ready-Mix Concrete

- Precast Concrete

- High Performance Concrete

- Others

By Form

- Liquid

- Powder

By Country

- The United States

- Canada

- Rest of North America

Frequently Asked Questions

What is driving the growth of the concrete superplasticizer market in North America?

The market is being driven by increasing construction and infrastructure development, the demand for high-performance concrete, a shift towards sustainable and green building practices, greater adoption of ready-mix concrete, and supportive government initiatives for urban development.

What trends are shaping the future of this market?

Key trends include the rising demand for eco-friendly admixtures, the growing use of polycarboxylate-based superplasticizers, the development of smart concrete solutions, and innovations involving nanotechnology in concrete mixtures.

What is the future outlook of the North America concrete superplasticizer market?

The market is expected to grow steadily, driven by increasing construction activity, demand for high-performance concrete, and sustainable building practices. Advancements in admixture technologies and infrastructure development will further support this growth.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com