North America Disinfectants and Cleaning Agents Market Size, Share, Trends & Growth Forecast Report, Segmented By Application, Product Type, Formulation Type, End Use and Country (United States, Canada, Mexico), Industry Analysis from 2025 to 2033

North America Disinfectants and Cleaning Agents Market Report Summary

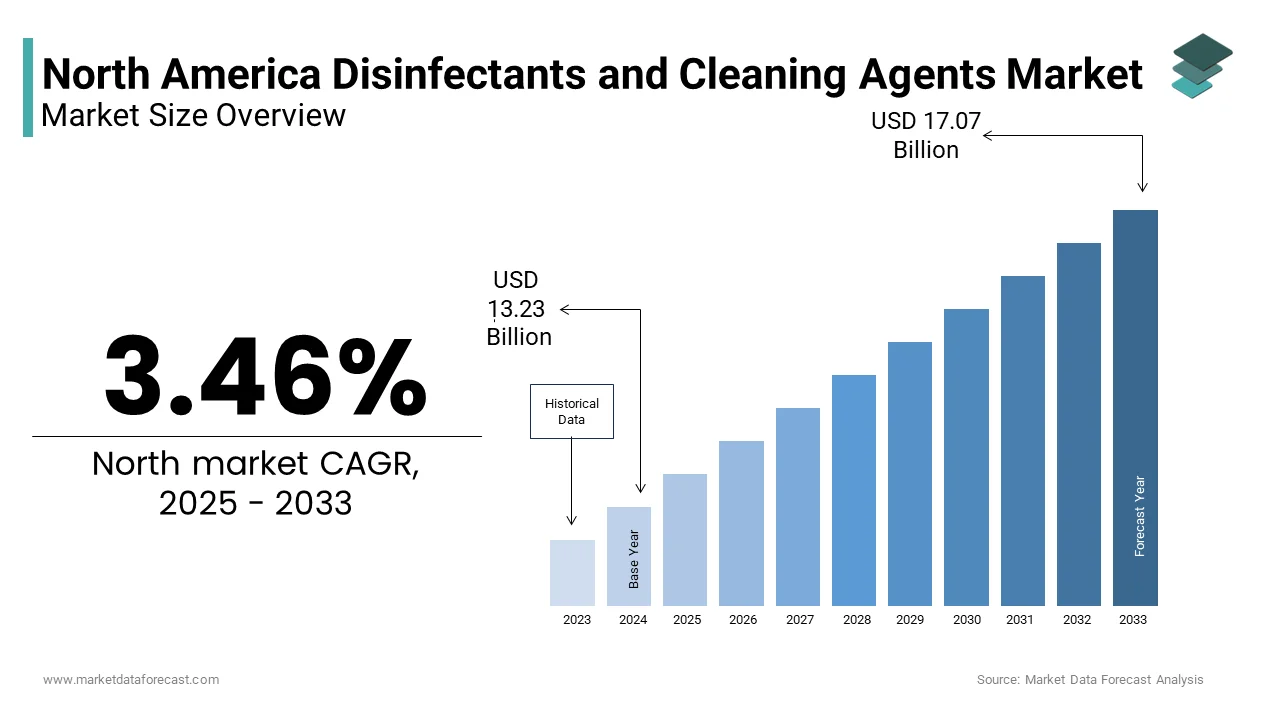

The North America disinfectants and cleaning agents market was valued at USD 12.79 billion in 2024, is estimated to reach USD 13.23 billion in 2025, and is projected to grow to USD 17.07 billion by 2033, expanding at a CAGR of 3.46% during the forecast period from 2025 to 2033. Market growth is supported by sustained hygiene awareness, routine household cleaning adoption, and continued demand from residential and institutional settings. Product innovation focused on efficacy, convenience, and environmentally responsible formulations is further reinforcing steady market expansion across the region.

Key Market Trends

- Persistent dominance of household and residential cleaning is driven by routine sanitation habits.

- Strong demand for surface cleaners suitable for multi-surface and high-touch applications.

- Preference for liquid formulations due to ease of use, dosing flexibility, and perceived effectiveness.

- Increasing shift toward eco-friendly, low-toxicity, and biodegradable formulations aligned with environmental policies.

- Brand-led innovation in convenient formats such as ready-to-use sprays and wipes.

Segmental Insights

- By application, the household segment led the market by accounting for 45.1% of the North America disinfectants and cleaning agents market share in 2024, reflecting strong penetration in everyday domestic cleaning routines.

- Based on product type, the surface cleaners segment dominated with 32.2% share in 2024, supported by widespread use across kitchens, bathrooms, and frequently touched household surfaces.

- By formulation, the liquid segment held the largest share at 52.7% in 2024, owing to its versatility, effectiveness, and compatibility with multiple application methods.

- In terms of end use, the residential segment captured 38.6% of the market share in 2024, driven by sustained consumer focus on home hygiene and cleanliness.

Regional Insights

The North American disinfectants and cleaning agents market remains highly concentrated. The

- United States dominated the region by holding 86.6% share in 2024, supported by a large consumer base, strong brand presence, and extensive retail distribution networks.

- Canada followed as a key contributor, driven by progressive environmental regulations and growing demand for sustainable cleaning products.

Competitive Landscape

The market is characterized by the presence of global consumer goods and specialty chemical companies competing on brand strength, formulation efficacy, and sustainability credentials. Leading players are investing in green chemistry, plant-based ingredients, and recyclable packaging to strengthen consumer trust and regulatory compliance. Prominent companies operating in the North America disinfectants and cleaning agents market include Procter & Gamble, Unilever, Reckitt Benckiser, SC Johnson, Henkel, Ecolab, Diversey Holdings, Clorox, BASF, and Kao Corporation.

North America Disinfectants and Cleaning Agents Market Size

The North America disinfectants and cleaning agents market was valued at USD 12.79 billion in 2024 and is anticipated to reach USD 13.23 billion in 2025 and USD 17.07 billion by 2033, growing at a CAGR of 3.46% during the forecast period from 2025 to 2033.

Current Introduction of the North America Disinfectants and Cleaning Agents Market

Disinfectants and cleaning agents are chemical formulations designed to eliminate pathogens, remove contaminants, and maintain hygienic environments across residential, commercial, and institutional settings. This market segment includes surface disinfectants, hand sanitizers, laundry detergents, floor cleaners, bathroom cleaners, kitchen cleaners, and specialized antimicrobial agents that serve essential public health functions by preventing disease transmission and maintaining environmental cleanliness. The market's evolution has been significantly influenced by advancing scientific understanding of pathogen behavior, regulatory frameworks governing antimicrobial efficacy claims, and shifting consumer preferences toward environmentally sustainable and health-conscious products. According to research, an ongoing observation is the critical link between maintaining clean environments and limiting the spread of infectious diseases. The market encompasses both ready-to-use formulations and concentrated products that require dilution, serving diverse applications ranging from routine household maintenance to critical healthcare facility sterilization. As per sources, the substantial quantities of cleaning and disinfecting products used each year demonstrate their fundamental role in both daily life and institutional operations. The industry has witnessed substantial innovation in formulation technologies, including the development of quaternary ammonium compounds, hydrogen peroxide-based systems, and alcohol-based sanitizers that offer enhanced efficacy against emerging pathogenic threats. Canadian markets have demonstrated parallel consumption patterns, and a pattern analysis reveals a significant increase in household expenditures on these products over a recent, multi-year period across specific markets.

MARKET DRIVERS

Heightened Health Awareness and Infectious Disease Prevention Focus

The unprecedented elevation of health awareness and intensified focus on infectious disease prevention following recent global health crises has emerged as the primary driver propelling the North American disinfectants and cleaning agents market growth. Consumers, businesses, and institutions have fundamentally altered their hygiene practices and cleaning protocols, transitioning from reactive maintenance approaches to proactive prevention strategies that prioritize continuous environmental sanitation and pathogen elimination. Households have widely adopted routine schedules for disinfecting frequently used surfaces. Intensified cleaning protocols have been established as a new baseline standard for infection control in facilities where healthcare is provided. Educational environments have put in place thorough cleaning requirements for classrooms and shared spaces, continuing throughout the academic term. Workplace settings have similarly embraced more rigorous cleaning standards, increasing the frequency of disinfection cycles in commercial buildings. Increased public awareness of health issues appears to have led to lasting changes in consumer behavior, with many people now considering regular disinfection an essential aspect of home upkeep.

Regulatory Compliance Requirements and Institutional Standards

Comprehensive regulatory compliance requirements and institutional hygiene standards have established themselves as key accelerators of the North America disinfectants and cleaning agents market. This creates mandatory demand across healthcare, food service, educational, and hospitality sectors that must adhere to strict sanitation protocols and documented cleaning procedures. Government agencies, including the Environmental Protection Agency, Food and Drug Administration, and Occupational Safety and Health Administration,n have implemented increasingly stringent guidelines governing disinfectant efficacy, safety standards, and application protocols that require specific product categories and performance criteria. Healthcare facilities face particularly rigorous compliance requirements, with the Joint Commission mandating that hospitals maintain documented cleaning and disinfection protocols that include specific product specifications, contact times, and staff training requirements that drive consistent product demand. Food service establishments must comply with Hazard Analysis Critical Control Point protocols that require specific antimicrobial interventions at critical processing points. Educational institutions have adopted comprehensive hygiene standards, with the National Association of Elementary School Principals requiring schools to maintain detailed cleaning logs and use products that meet specific efficacy standards for pathogen elimination. The liability implications of inadequate cleaning and disinfection have created risk management incentives that extend beyond regulatory requirements. Proper sanitation practices can reduce premises liability claims.

MARKET RESTRAINTS

Environmental Concerns and Chemical Safety Regulations

Growing environmental concerns and increasingly stringent chemical safety regulations are major constraints on the North American disinfectants and cleaning agents market. Manufacturers face mounting pressure to develop formulations that balance efficacy requirements with environmental sustainability and human safety considerations. The environmental impact of traditional cleaning and disinfecting chemicals, including water system contamination, aquatic ecosystem disruption, and atmospheric volatile organic compound emissions, has prompted regulatory agencies to implement restrictive guidelines that limit product formulations and usage patterns. Many conventional cleaning products contain ingredients associated with potential health concerns. This has led to increased consumer wariness and regulatory attention, which in turn limits market expansion for traditional products. A government program sets high standards for product certification, but only a small percentage of manufacturers meet these criteria due to formulation and testing requirements that add to development costs and time-to-market. More information is available on the Environmental Working Group's website. Packaging waste and single-use container proliferation have created additional environmental concerns. The complexity of navigating multiple regulatory frameworks across different jurisdictions creates compliance challenges for manufacturers seeking to maintain broad market access while developing environmentally preferable products. Ingredient transparency requirements have intensified consumer scrutiny, with many consumers now researching product ingredient safety before purchase, creating market pressure for natural and biodegradable alternatives that may compromise efficacy standards.

Supply Chain Disruptions and Raw Material Cost Volatility

Persistent supply chain disruptions and volatile raw material costs have created substantial operational challenges and financial pressures, which hinderthe expansion of the North American disinfectants and cleaning agents market. This situation constrains production capacity, impacts product availability, increases consumer prices, and reduces market accessibility. The chemical manufacturing sector has experienced significant feedstock price fluctuations. Supply chain disruptions have led to substantial increases in raw material expenses for producers of cleaning and disinfecting goods. Logistical hurdles and transportation difficulties have contributed significantly to the overall cost of production. Shortages of shipping containers and delays in transit have complicated inventory management, leading to intermittent product unavailability. The concentration of essential raw material suppliers in limited geographic areas has increased the industry's vulnerability to localized disturbances. Geopolitical instability and environmental events pose risks to the stability of the supply chain due to this regional dependency. Staffing challenges and high turnover within the manufacturing and distribution sectors have limited the ability of companies to maintain full operational capacity. The just-in-time inventory management approaches adopted by many manufacturers have proven inadequate for managing supply chain volatility.

MARKET OPPORTUNITY

Innovation in Green and Sustainable Formulations

The accelerating demand for green and sustainable disinfectant and cleaning formulations presents substantial growth opportunities for manufacturers in the North American disinfectants and cleaning agents market. These opportunities are available to those willing to invest in environmentally responsible product development and certification programs that appeal to increasingly conscious consumers and institutional purchasers. This innovation trajectory aligns with broader environmental sustainability trends and regulatory preferences for reduced chemical impact while maintaining efficacy standards and performance expectations. Plant-based surfactant technologies and bio-based antimicrobial agents have emerged as viable alternatives to traditional petroleum-derived ingredients, with manufacturers developing formulations that achieve equivalent or superior cleaning performance while reducing environmental footprint and human health exposure risks. The certification process for green products has become increasingly rigorous, with third-party organizations including Green Seal and EcoLogo establishing comprehensive standards that encompass ingredient safety, biodegradability, packaging sustainability, and manufacturing process efficiency. Consumer willingness to pay premium prices for environmentally responsible products supports higher-margin product development strategies. The integration of smart packaging technologies and concentrated formulations reduces transportation costs and packaging waste while appealing to environmentally conscious consumers. Institutional markets, including healthcare, education, and hospitality, have established green procurement policies that favor certified sustainable products, which creates stable demand channels for manufacturers who achieve necessary certifications and performance validation.

Smart Technology Integration and Automated Cleaning Solutions

The convergence of smart technology integration and automated cleaning solutions exhibits a potential prospect for the North American disinfectants and cleaning agents market. Manufacturers and service providers are developing innovative product-service combinations that enhance cleaning efficiency, ensure protocol compliance, and reduce labor costs while maintaining superior hygiene standards. Internet of Things connectivity and sensor technologies enable real-time monitoring of cleaning activities, automated dispensing systems, and data-driven optimization of cleaning schedules and product usage that improve operational efficiency and accountability. Electrostatic spraying systems and ultraviolet disinfection technologies have gained significant traction in institutional settings. The integration of artificial intelligence and machine learning algorithms enables predictive maintenance scheduling and optimized chemical usage that reduces waste and improves cost-effectiveness while maintaining hygiene standards. Mobile applications and cloud-based management platforms provide facility managers with comprehensive oversight of cleaning activities, compliance documentation, and performance analytics that support regulatory requirements and quality assurance objectives. The residential market has shown growing interest in smart cleaning solutions.

MARKET CHALLENGES

Efficacy Standardization and Performance Validation Requirements

The increasingly complex landscape of efficacy standardization and performance validation requirements presents significant challenges for manufacturers seeking to develop and market disinfectants and cleaning agents. This hampers the growth of the North American disinfectants and cleaning agents market. They must meet diverse regulatory standards while demonstrating consistent performance across varying application conditions and pathogenic targets. Regulatory agencies have implemented progressively stringent testing protocols and documentation requirements that necessitate extensive laboratory validation, real-world performance studies, and ongoing compliance monitoring that increase development costs and time-to-market for new products. Cross-jurisdictional regulatory compliance creates additional complexity, with products requiring separate validation studies and regulatory submissions for different states and provinces that fragment market access and increase administrative burdens. The emergence of new pathogenic threats and antimicrobial resistance patterns necessitates continuous product evaluation and reformulation efforts that require ongoing investment and regulatory navigation. Performance validation under real-world conditions presents particular challenges, as laboratory efficacy may not translate to practical application scenarios involving varying surface materials, organic load levels, and environmental conditions. The liability exposure associated with inadequate product performance has intensified scrutiny of efficacy claims and testing methodologies.

Consumer Education and Proper Usage Compliance

The challenge of consumer education and proper usage compliance is a fundamental obstacle limiting the growth of the North American disinfectants and cleaning agents market. This is because an inadequate understanding of product application requirements, contact times, and safety protocols reduces real-world efficacy and creates potential health and safety risks. Despite the availability of effective products, improper usage patterns, including insufficient contact times, incorrect dilution ratios, and inappropriate application methods, significantly compromise disinfection outcomes and undermine public health objectives. The complexity of product selection and application requirements creates confusion among consumers. Language barriers and literacy challenges further complicate proper usage compliance, particularly in multicultural communities where product labeling and instruction comprehension may be limited. The proliferation of misinformation regarding cleaning and disinfection practices through social media and informal channels has created widespread confusion about effective protocols and product selection criteria. Educational initiatives require sustained investment and coordination across multiple stakeholders, including manufacturers, retailers, healthcare organizations, and government agencies, to ensure consistent messaging and effective behavior change that supports optimal product performance and public health outcomes.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 3.46% |

| Segments Covered | By Application, Product Type, Formulation Type, End Use, and Country Analysis |

| Various Analyses Covered | Global, Regional, and Country-Level Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | United States, Canada, Mexico, etc. |

| Market Leaders Profiled | Procter & Gamble (US), Unilever (GB), Reckitt Benckiser (GB), SC Johnson (US), Henkel (DE), Ecolab (US), Diversey Holdings (US), Clorox (US), BASF (DE), Kao Corporation (JP) |

SEGMENTAL ANALYSIS

By Application Insights

The household application segment dominated the North America disinfectants and cleaning agents market by accounting for a 45.1% share in 2024. The supremacy of the household application segment is driven by the fundamental role of residential cleaning and disinfection in maintaining family health, property value preservation, and daily living standards across millions of North American households. The segment's dominance is also reinforced by consistent consumer demand for routine maintenance products, seasonal cleaning requirements, and emergency preparedness supplies that create sustained purchasing patterns throughout the year. Household consumers represent the largest demographic group in the market, with diverse needs ranging from basic cleaning solutions to specialized antimicrobial products that address specific health concerns and lifestyle preferences. The segment benefits from established retail distribution networks, consumer brand loyalty, and predictable purchasing cycles that enable manufacturers to maintain stable revenue streams and optimize production planning. Additionally, the household segment's broad demographic reach and varied application requirements create opportunities for product line extensions, seasonal promotions, and value-added formulations that enhance customer lifetime value and market penetration. Consumer health consciousness and preventive maintenance behaviors serve as primary drivers for the household segment's dominance in the North America disinfectants and cleaning agents market, reflecting fundamental shifts in consumer attitudes toward proactive health management and environmental sanitation that have emerged following heightened awareness of infectious disease transmission. Modern households increasingly view regular cleaning and disinfection as essential components of family health maintenance rather than optional household tasks, creating sustained demand for effective and convenient cleaning solutions that support daily hygiene practices. The psychological impact of health education initiatives has created lasting behavioral changes that extend beyond immediate health threats. Preventive maintenance behaviors encompass seasonal cleaning intensification, emergency preparedness stockpiling, and specialized product adoption for vulnerable household members, including elderly individuals and immunocompromised family members. The integration of cleaning and disinfection activities into daily routines has elevated the importance of convenient, effective, and safe product formulations that support consistent usage patterns. Canadian household behavior patterns demonstrate similar health consciousness trends. Product convenience and multi-surface application capabilities constitute another critical factor driving the household segment's market leadership in the North America disinfectants and cleaning agents market, as manufacturers develop innovative formulations and packaging solutions that simplify cleaning processes and reduce the complexity of household maintenance activities. Modern consumers increasingly value time-saving solutions and simplified cleaning protocols that enable effective sanitation without extensive preparation, specialized equipment, or multiple product requirements for different surface types. As per the Home Care Research Institute, 84% of household consumers prefer multi-surface disinfectants that can be used on various materials,s including wood, metal, plastic, and fabric, reducing product inventory requirements and simplifying purchasing decisions. Ready-to-use formulations and convenient packaging formats, ts including trigger sprays, wipes, and foam dispensers, have eliminated the preparation complexity associated with traditional concentrate products, making effective disinfection accessible to consumers with varying skill levels and time constraints. The development of fragrance-free and hypoallergenic formulations addresses consumer concerns about respiratory sensitivity and chemical exposure while maintaining efficacy standards for pathogen elimination. Seasonal and occasion-based product variations, including holiday cleaning concentrates, summer outdoor surface treatments, and winter germ-fighting formulations, create additional purchase opportunities and consumer engagement. Canadian household preferences demonstrate similar convenience-driven patterns.

Fastest Growing Segment: Healthcare Application

The healthcare application segment is likely to experience the fastest CAGR of 11.3% from 2025 to 2033 due to the healthcare industry's intensified focus on infection prevention and control, regulatory compliance requirements, and the adoption of advanced disinfection technologies that support patient safety and operational efficiency. Healthcare facilities, including hospitals, clinics, long-term care facilities, and outpatient centers,s require specialized antimicrobial products that meet stringent efficacy standards, regulatory approvals, and safety protocols while addressing the unique challenges of the healthcare environment,,s including pathogen resistance, surface complexity, and vulnerable patient populations. The segment's acceleration is also driven by increasing healthcare-associated infection rates, regulatory mandates for enhanced cleaning protocols, and the adoption of evidence-based cleaning practices that require validated products and documented performance outcomes. The emergence of antimicrobial resistance and healthcare-associated pathogens has elevated the importance of effective disinfection products that can eliminate challenging organisms,s including Clostridioides difficile, methicillin-resistant Staphylococcus aureus, and multidrug-resistant bacteria. Advanced disinfection technologies,ies including electrostatic spraying systems, ultraviolet disinfection, and hydrogen peroxide vapor systems,tems have gained significant traction in healthcare settings. Regulatory compliance mandates and accreditation requirements serve as primary enablers driving the rapid expansion of disinfectants and cleaning agents, as healthcare facilities face increasingly stringent standards for infection prevention and control that necessitate specialized products and documented performance validation. Government agencies, es including the Centers for Disease Control and Prevention, the Joint Commission, and state health departments,s have implemented comprehensive guidelines governing healthcare facility cleaning and disinfection practices that require specific product categories, application protocols, and performance documentation to maintain operational licenses and accreditation status. The complexity of healthcare environments requires specialized disinfectants that can effectively eliminate healthcare-associated pathogens while maintaining compatibility with sensitive medical equipment and surfaces. Accreditation organizations have established rigorous standards for environmental cleaning and disinfection, with the Joint Commission requiring hospitals to conduct quarterly efficacy testing and maintain detailed documentation of cleaning activities and product performance. The liability implications of healthcare-associated infections have intensified scrutiny of cleaning and disinfection practices. Canadian healthcare facilities demonstrate similar regulatory compliance pressures. Advanced disinfection technologies and evidence-based practices represent fundamental drivers behind the healthcare segment's exceptional growth rate in the North America disinfectants and cleaning agents market, as healthcare facilities adopt innovative solutions that enhance pathogen elimination effectiveness while supporting operational efficiency and staff productivity. The integration of technology-enabled disinfection systems,s including electrostatic sprayers, ultraviolet disinfection units, and automated monitoring systems,s has revolutionized healthcare facility cleaning practices while creating new product categories and application requirements that drive market expansion. Evidence-based cleaning practices have elevated the importance of quantifiable performance metrics and documented effectiveness, with healthcare facilities requiring disinfectants that can demonstrate specific log reduction values for target pathogens under controlled testing conditions. The emergence of antimicrobial resistance and healthcare-associated pathogens has intensified the need for broad-spectrum antimicrobial products that can eliminate challenging organisms while maintaining safety profiles for healthcare workers and patients. Training and certification programs for healthcare environmental services staff have created demand for user-friendly products and standardized protocols that support consistent application and optimal performance outcomes. Canadian healthcare innovation adoption patterns demonstrate similar technology-driven growth.

By Product Insights

The surface cleaners product type segment led the North America disinfectants and cleaning agents market by capturing a share of 32.2% in 2024. Daily maintenance requirements and routine usage patterns are the main drivers for the surface cleaners segment's dominance. These products play a fundamental role in supporting basic hygiene standards and aesthetic maintenance across diverse environments and demographics. This market command is also supported by surface cleaners' fundamental role in daily maintenance activities across residential, commercial, and institutional environments,s where routine cleaning and basic disinfection requirements create sustained demand for versatile and accessible cleaning solutions. Surface cleaners encompass a broad product category, including general-purpose cleaners, glass cleaners, bathroom cleaners, and kitchen surface treatments that address diverse soil types, surface materials, and aesthetic requirements while providing essential hygiene functions. The segment's dominance is also reinforced by its accessibility through multiple retail channels, affordable price points, and familiar usage patterns that create consistent consumer demand and repeat purchase behaviors. Surface cleaners benefit from established brand recognition, extensive marketing support, and consumer familiarity with application techniques that reduce adoption barriers and support market penetration. Additionally, the versatility of surface cleaner formulations enables manufacturers to develop specialized products for specific applications,s including antimicrobial treatments, degreasing solutions, and streak-free finishes that address diverse consumer needs and preferences. The segment's broad demographic appeal and varied application requirements create opportunities for product line extensions, seasonal variations, and value-added formulations that enhance customer engagement and market share. Modern consumers and facility managers increasingly recognize the importance of regular surface cleaning for health maintenance, property value preservation, and professional image management by creating sustained demand for effective and convenient cleaning solutions that support frequent usage patterns. Residential usage patterns demonstrate similar frequency. The psychological impact of clean environments on occupant satisfaction and productivity has elevated the importance of regular surface cleaning. Seasonal variations in cleaning requirements, including increased frequency during illness seasons and special occasions, create additional purchase opportunities and consumer engagement. Canadian usage patterns demonstrate similar maintenance-driven demand. Versatility and multi-application formulations constitute another critical factor driving the surface cleaners product type segment's market leadership, as manufacturers develop innovative products that address diverse cleaning challenges while reducing inventory complexity and simplifying purchasing decisions for consumers and facility managers. Modern surface cleaners are engineered to perform effectively across multiple surface types,s including glass, metal, plastic, wood, and ceramic materials, eliminating the need for specialized products and reducing storage requirements while maintaining optimal cleaning performance. The development of concentrated formulations and refillable packaging systems addresses consumer preferences for cost-effective and environmentally responsible solutions while maintaining cleaning efficacy and convenience. Fragrance variations and aesthetic enhancement features, including streak-free finishes, shine restoration, and protective coating,,s create additional value propositions that differentiate products and support premium pricing strategies. The integration of antimicrobial properties into general surface cleaners has blurred traditional product category boundaries. Canadian consumer preferences demonstrate similar versatility-driven demand.

Fastest Growing Segment: Disinfectant Wipes Product Type

The disinfectant wipes product type segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 14.7% during the forecast period. Portability and ease of use are key drivers behind the increasing popularity of disinfectant wipes in North America. Both professionals and general consumers desire immediate, reliable access to effective disinfection methods across various environments and situations. This impressive growth trajectory shows the convenience, portability, and immediate effectiveness advantages that disinfectant wipes offer compared to traditional liquid disinfectants and cleaning solutions, particularly in fast-paced environments where quick and reliable pathogen elimination is essential. Disinfectant wipes have gained significant traction across healthcare, educational, hospitality, and residential applications due to their ease of use, consistent dosage delivery, and elimination of preparation requirements that make effective disinfection accessible to users with varying skill levels and time constraints. The segment's acceleration is also driven by increasing demand for contactless cleaning solutions, portable disinfection options, and immediate pathogen elimination capabilities that support modern lifestyle requirements and health consciousness trends. The emergence of antimicrobial resistance and healthcare-associated pathogens has elevated the importance of effective, ready-to-use disinfection products that can eliminate challenging organisms while maintaining safety profiles for users and surfaces. Convenience factor,,s including pre-measured dosages, no-rinse requirements, and disposal simplicityhasve made disinfectant wipes particularly attractive for high-touch surface applications and emergency response situations. Immediate effectiveness and consistent dosage delivery represent fundamental drivers behind the disinfectant wipes segment's exceptional growth rate. These products eliminate variables associated with traditional liquid disinfectants and provide reliable pathogen elimination performance that supports user confidence and compliance with recommended contact times. The ready-to-use format eliminates preparation time, measurement requirements, and equipment needs that traditionally complicated disinfection processes, making pathogen elimination accessible to users regardless of technical expertise or available resources. Travel and transportation sectors have particularly embraced disinfectant wipes due to their compact size, leak-proof packaging, and immediate effectiveness that support hygiene maintenance during journeys and in confined spaces. Educational institutions utilize disinfectant wipes for classroom cleaning between sessions and student activities. Healthcare professionals rely on disinfectant wipes for equipment sanitization, patient room turnover, and mobile workstation cleaning due to their consistent performance and time-saving benefits. Canadian mobility patterns demonstrate similar convenience-driven adoption. Immediate effectiveness and consistent dosage delivery represent fundamental drivers behind the disinfectant wipes segment's exceptional growth rate in the North America disinfectants and cleaning agents market, as these products eliminate variables associated with traditional liquid disinfectants and provide reliable pathogen elimination performance that supports user confidence and compliance with recommended contact times. Pre-saturated wipes ensure consistent chemical concentration and adequate wetness levels that are essential for effective antimicrobial action, eliminating the risk of under-dosing or inadequate contact that can compromise disinfection outcomes. The tactile application method ensures complete surface coverage and appropriate contact time, with users able to visibly confirm that surfaces have been adequately treated and allowed to air dry for optimal effectiveness. Healthcare settings particularly benefit from consistent dosage delivery. Educational and childcare environments appreciate the immediate effectivenessofr quick turnaround cleaning between activities and sessions. Canadian healthcare facilities demonstrate similar effectiveness-driven adoption.

By Formulation Insights

The liquid formulation type segment was the largest in the North America disinfectants and cleaning agents market by holding a share of 52.7% in 2024. The leading position of the liquid formulation type segment is credited to its fundamental versatility, cost-effectiveness, and established consumer familiarity that create broad appeal across diverse application requirements and user demographics. Liquid formulations offer optimal concentration flexibility, allowing manufacturers to develop products with varying strength levels that address specific cleaning challenges while maintaining economic efficiency through concentrated packaging and bulk distribution. The segment's dominance is also supported by established manufacturing processes, extensive distribution networks, and consumer acceptance of traditional spray and pour application methods that require minimal behavior change or equipment investment. Liquid formulations benefit from superior shelf stability, extended storage life, and compatibility with existing dispensing equipment that reduces infrastructure requirements for commercial and institutional users. Additionally, the versatility of liquid formulations enables manufacturers to incorporate diverse active ingredients, fragrance systems, and performance enhancers that address specific market needs and preferences. The segment's broad application compatibility and familiar usage patterns create opportunities for product line extensions, seasonal variations, and specialized formulations that enhance customer engagement and market penetration. Cost-effectiveness and economic efficiency for high-volume applications are the key drivers for the liquid formulation type segment's dominance, which shows the fundamental economic advantages that liquid products offer for institutional, commercial, and industrial users who require sustained disinfection and cleaning activities across large facilities and diverse surface areas. Liquid formulations typically provide the lowest cost-per-application compared to alternative formats, with concentrated products offering particularly attractive economics for facilities that conduct frequent cleaning and disinfection activities throughout their operations. The concentration flexibility of liquid formulations enables users to adjust strength levels based on specific cleaning requirements and soil loads, reducing waste and optimizing chemical usage while maintaining effective pathogen elimination. Bulk storage and dispensing systems further enhance economic efficiency by reducing packaging waste, minimizing handling requirements, and enabling automated refilling processes that reduce labor costs and improve operational consistency. The compatibility of liquid formulations with existing dispensing equipment and infrastructure eliminates capital investment requirements for facilities upgrading their cleaning and disinfection protocols. Canadian institutional markets demonstrate similar cost-driven preferences. Versatility and customizable application methods constitute another critical factor driving the liquid formulation type segment's market leadership, as these products offer maximum flexibility in application techniques, dilution ratios, and usage scenarios that accommodate diverse user needs and environmental requirements. Liquid formulations can be applied using multiple methods,s including trigger sprays, pump dispensers, automatic dilution systems, and electrostatic spraying equipment, enabling users to select the most appropriate application technique for specific surfaces, areas, and cleaning protocols. The dilution flexibility enables users to adjust concentration levels based on soil load, pathogen challenge, and surface sensitivity, optimizing product performance while reducing chemical consumption and environmental impact. Customizable application methods include targeted spot treatment for high-risk areas, broad-area coverage for routine maintenance, and specialized techniques for sensitive equipment and surfaces. The compatibility of liquid formulations with automated cleaning equipment and integrated facility management systems enhances operational efficiency and consistency. Canadian facility management practices demonstrate similar versatility-driven adoption.

Fastest Growing Segment: Spray Formulation Type

The spray formulation type segment is on the rise and is expected to be the fastest growing segment in the market by witnessing a CAGR of 9.8% from 2025 to 2033 owing to the convenience, targeted application capabilities, and immediate effectiveness advantages that spray formulations offer compared to traditional liquid products and alternative delivery methods, particularly in residential and small commercial applications where quick and precise disinfection is essential. Spray formulations have gained significant traction across household, healthcare, and institutional applications due to their ease of use, controlled application patterns, and elimination of secondary application tools that make effective disinfection accessible to users with varying skill levels and time constraints. The segment's acceleration is also fuelled by increasing demand for contactless application methods, targeted treatment capabilities, and immediate pathogen elimination that support modern lifestyle requirements and health consciousness trends. The emergence of antimicrobial resistance and healthcare-associated pathogens has elevated the importance of effective, ready-to-use spray products that can eliminate challenging organisms while maintaining safety profiles for users and surfaces. Convenience factors,s including no-preparation requirements, precise application control, and immediate effectiveness,s have made spray formulations particularly attractive for high-touch surface applications and emergency response situations. Targeted application and precision treatment capabilities boostthe the quick spread of spray formulations, as modern users increasingly value the ability to apply disinfectants precisely where needed while minimizing waste, reducing cross-contamination risks, and optimizing product effectiveness. The controlled spray pattern enables users to focus treatment on specific high-risk areas, contaminated surfaces, and problematic zones without overspray onto adjacent surfaces or into surrounding environments. Healthcare settings particularly benefit from targeted application capabilities. Educational institutions utilize spray formulations for classroom disinfection, restroom maintenance, and cafeteria sanitation due to their ability to quickly treat multiple surfaces without extensive preparation or cleanup requirements. The development of specialized spray nozzles and application techniques has enhanced precision capabilities, with fine mist sprays suitable for delicate electronics and coarse sprays appropriate for heavily soiled surfaces. Canadian institutional adoption patterns demonstrate similar precision-driven demand. Contactless application and aerosol delivery systems represent fundamental drivers behind the spray formulation segment's surge in the North America disinfectants and cleaning agents market, as these products eliminate direct surface contact requirements and enable rapid, comprehensive disinfection that supports modern hygiene protocols and user safety preferences. Aerosol spray technologies create fine mist distributions that can penetrate crevices, coat irregular surfaces, and reach areas that would be difficult to access using traditional wiping or pouring methods, ensuring comprehensive pathogen elimination across complex surface geometries. The contactless nature of spray application reduces user exposure to potentially contaminated surfaces and minimizes the risk of cross-contamination during the disinfection process, creating safety advantages for healthcare workers, facility maintenance staff, and household users. Emergency response and rapid deployment scenarios benefit from immediate application capabilities, with first responders and facility managers able to quickly establish sanitized environments without extensive preparation or equipment requirements. The development of electrostatic spray systems has further enhanced contactless application effectiveness, with charged particles adhering to surfaces regardless of spray angle or user positioning. Canadian emergency response protocols demonstrate similar contactless-driven adoption.

By End Use Insights

The residential end-use segment captured the majority share of 38.6% of the North America disinfectants and cleaning agents market in 2024. The segment's growth is supported by consistent consumer demand for routine maintenance products, seasonal cleaning requirements, and emergency preparedness supplies that create sustained purchasing patterns throughout the year across all income levels and geographic regions. This market command is because of the fundamental role of household cleaning and disinfection in maintaining family health, property value preservation, and daily living standards across millions of North American households with diverse demographic characteristics and lifestyle requirements. Residential consumers represent the largest demographic group in the market, with varied needs ranging from basic cleaning solutions to specialized antimicrobial products that address specific health concerns, aesthetic preferences, and convenience requirements. The segment benefits from established retail distribution networks, consumer brand loyalty, and predictable purchasing cycles that enable manufacturers to maintain stable revenue streams and optimize production planning. Additionally, the residential segment's broad demographic reach and varied application requirements create opportunities for product line extensions, seasonal promotions, and value-added formulations that enhance customer lifetime value and market penetration. Consumer health awareness and family safety priorities serve as primary drivers for the residential end-use segment's dominance, whichreflectss fundamental shifts in consumer attitudes toward proactive health management and environmental sanitation that have emerged following heightened awareness of infectious disease transmission and indoor air quality concerns. Modern households increasingly view regular cleaning and disinfection as essential components of family health maintenance rather than optional household tasks, creating sustained demand for effective and convenient cleaning solutions that support daily hygiene practices and emergency preparedness requirements. The psychological impact of health education initiatives has created lasting behavioral changes that extend beyond immediate health threats. Family safety priorities encompass seasonal cleaning intensification, specialized product adoption for vulnerable household members, and preventive maintenance behaviors that address potential health risks before they become serious concerns. The integration of cleaning and disinfection activities into daily routines has elevated the importance of convenient, effective, and safe product formulations that support consistent usage patterns and comprehensive coverage of household surfaces and areas. Convenience and multi-purpose product preferences constitute another critical factor driving the residential end-use segment's market leadership in the North America disinfectants and cleaning agents market, as modern consumers increasingly value time-saving solutions and simplified cleaning protocols that enable effective sanitation without extensive preparation, specialized equipment, or multiple product requirements for different household areas and surfaces. Ready-to-use formulations, multi-surface compatibility, and integrated cleaning-disinfection capabilities have eliminated the complexity traditionally associated with household cleaning while providing comprehensive protection against pathogens and soil accumulation. The development of concentrated formulations and refillable packaging systems addresses consumer preferences for cost-effective and environmentally responsible solutions while maintaining cleaning efficacy and reducing storage requirements. Seasonal and occasion-based product variation,s including holiday cleaning concentrates, summer outdoor surface treatments, and winter germ-fighting formulation,,s create additional purchase opportunities and consumer engagement while supporting comprehensive household maintenance programs. The integration of smart home technologies and automated dispensing systems has further enhanced convenience capabilities, with programmable cleaning schedules and remote monitoring features that reduce manual intervention requirements. Canadian residential preferences demonstrate similar convenience-driven patterns.

Fastest Growing Segment: Healthcare Facilities End Use

The healthcare facilities end-use segment is expected to exhibit a noteworthy CAGR of 12.1% during the forecast period. The swift growth of this segment is propelled by the healthcare industry's intensified focus on infection prevention and control, regulatory compliance requirements, and the adoption of advanced disinfection technologies that support patient safety and operational efficiency in increasingly complex medical environments. Healthcare facilities,s including hospitals, clinics, long-term care facilities, and outpatient centers,s require specialized antimicrobial products that meet stringent efficacy standards, regulatory approvals, and safety protocols while addressing the unique challenges of healthcare environments,t,s including pathogen resistance, surface complexity, and vulnerable patient populations. The segment's acceleration is driven by increasing healthcare-associated infection rates, regulatory mandates for enhanced cleaning protocols, and the adoption of evidence-based cleaning practices that require validated products and documented performance outcomes. The emergence of antimicrobial resistance and healthcare-associated pathogens has elevated the importance of effective disinfection products that can eliminate challenging organisms,s including Clostridioides difficile, methicillin-resistant Staphylococcus aureus, and multidrug-resistant bacteria. Advanced disinfection technologies, es including electrostatic spraying systems, ultraviolet disinfection, and hydrogen peroxide vapor systems,s have gained significant traction in healthcare settings. Infection control protocols and patient safety standardhelp thelp market grow fast of disinfectants and cleaning agents in the North America healthcare facilities end-use segment, as medical institutions face increasingly stringent requirements for environmental hygiene that directly impact patient outcomes, regulatory compliance, and operational reputation. Healthcare-associated infections represent one of the most significant challenges facing modern medical facilities. Regulatory agencies have implemented comprehensive standards governing healthcare facility cleaning practices, with the Joint Commission requiring hospitals to maintain documented cleaning protocols, validated product efficacy, and staff training records to maintain accreditation status. The complexity of healthcare environments requires specialized disinfectants that can effectively eliminate healthcare-associated pathogens while maintaining compatibility with sensitive medical equipment, electronic devices, and diverse surface materials. Patient safety considerations extend beyond immediate infection prevention to include long-term outcomes, readmission rates, and facility reputation management that influence consumer choice and referral patterns. Canadian healthcare facilities demonstrate similar infection control pressures. Advanced technology integration and automated systems exhibit drivers behind the healthcare facilities end use segment's exceptional growth rate in the North America disinfectants and cleaning agents market, as medical institutions adopt innovative solutions that enhance pathogen elimination effectiveness while supporting operational efficiency and staff productivity in resource-constrained environments. The integration of technology-enabled disinfection systems,s including electrostatic sprayers, ultraviolet disinfection units, and automated monitoring systems, ems has revolutionized healthcare facility cleaning practices while creating new product categories and application requirements that drive market expansion. Evidence-based cleaning practices have elevated the importance of quantifiable performance metrics and documented effectiveness, with healthcare facilities requiring disinfectants that can demonstrate specific log reduction values for target pathogens under controlled testing conditions. The emergence of antimicrobial resistance and healthcare-associated pathogens has intensified the need for broad-spectrum antimicrobial products that can eliminate challenging organisms while maintaining safety profiles for healthcare workers and patients. Training and certification programs for healthcare environmental services staff have created demand for user-friendly products and standardized protocols that support consistent application and optimal performance outcomes. Canadian healthcare innovation adoption patterns demonstrate similar technology-driven growth.

COUNTRY ANALYSIS

United States Disinfectants And Cleaning Agents Market Analysis

The United States was the top performer in the North America disinfectants and cleaning agents market by holding a 86.6% share in 2024 because of the country's vast population base, extensive healthcare infrastructure, advanced retail distribution networks, and progressive regulatory frameworks that support product innovation and quality standards. The U.S. market benefits from well-established manufacturing capabilities, comprehensive research and development activities, and sophisticated consumer demand patterns that drive continuous product evolution and market expansion. American consumers have demonstrated high awareness of hygiene and sanitation requirements, driven by increased health consciousness, regulatory compliance needs, and lifestyle preferences that create sustained demand for diverse cleaning and disinfecting solutions. The market's maturity is evidenced by the presence of multiple national brands, extensive retail distribution networks, and sophisticated marketing strategies that ensure broad product availability and consumer awareness. Federal and state-level policies promoting public health and environmental safety further strengthen the market foundation, ensuring sustained growth prospects for disinfectants and cleaning agents across diverse consumer segments and application categories. The United States disinfectants and cleaning agents market demonstrates robust growth momentum supported by substantial consumer awareness and evolving regulatory requirements that prioritize public health protection and environmental sustainability. The country's large and diverse population creates extensive demand for varied product offerings that accommodate different cleaning challenges, surface types, and usage preferences across residential, commercial, and institutional environments. Consumer health consciousness has reached unprecedented levels, with the Centers for Disease Control and Prevention reporting that 84% of American adults now view regular environmental disinfection as essential for family health maintenance, creating sustained demand for effective and accessible cleaning solutions. The retail infrastructure supporting cleaning product distribution is exceptionally developed. Healthcare facility requirements have intensified following recent health awareness campaigns. Additionally, the professional cleaning and facility management sectors have embraced advanced disinfection technologies.

Canada Disinfectants And Cleaning Agents Market Analysis

Canada was the next prominent player in North America for disinfectants and cleaning agents owing to progressive environmental policies, multicultural population demographics, and a strong emphasis on public health protection and quality standards. Canadian consumers have demonstrated high awareness of hygiene requirements and a strong preference for environmentally responsible products that align with national values and sustainability objectives. The market benefits from federal and provincial health policies that support infection prevention initiatives and product safety requirements, creating favorable conditions for quality product development and consumer confidence. Canadian retail environments have shown exceptional commitment to cleaning product availability and education, with major grocery chains investing significantly in dedicated cleaning sections and staff training programs. The country's healthcare system has implemented comprehensive infection control standards that drive institutional demand for validated disinfectants and specialized cleaning solutions. Canada's commitment to sustainable development and environmental protection further supports the growth of green cleaning products and eco-friendly formulations that emphasize natural ingredients and reduced environmental impact. Provincial health authorities have established rigorous standards for healthcare facility cleaning and disinfection that create stable demand for high-quality products and documented performance validation. The Canadian disinfectants and cleaning agents market shows steady growth supported by progressive public health policies and substantial institutional demand for validated cleaning solutions that support infection prevention and environmental sustainability objectives. Health Canada has implemented comprehensive product safety and efficacy standards that exceed international requirements, creating strong consumer confidence in cleaning product safety and performance while supporting market expansion through regulatory clarity and quality assurance. Multicultural population demographics drive demand for diverse product offerings that accommodate various cultural cleaning preferences and traditional maintenance practices. Provincial healthcare systems have implemented comprehensive infection control standards and facility accreditation requirements. Canadian consumers demonstratea strong preference for environmentally responsible products. Additionally, the Canadian retail sector has shown exceptional commitment to cleaning product education and accessibility.

COMPETITIVE LANDSCAPE

The North American disinfectants and cleaning agents market exhibits moderate to high competition characterized by the presence of established multinational manufacturers, specialized chemical companies, and emerging innovative brands competing for consumer attention and market share across diverse application segments. The competitive landscape is shaped by companies differentiating themselves through product efficacy, brand positioning, and distribution strategies rather than engaging in aggressive price competition that could compromise product quality and safety standards. Large national brands compete primarily on brand recognition, distribution reach, and marketing capabilities, while specialized manufacturers focus on product expertise, regulatory compliance, and institutional relationships to establish market positions. The market features both direct competition among similar product categories and indirect competition from alternative hygiene solutions,ons including steam cleaning, ultraviolet disinfection, and antimicrobial surface treatments that offer complementary or substitute approaches to environmental sanitation. Regional market dynamics influence competitive strategies, with manufacturers adapting their approaches to address specific geographic requirements, regulatory environments, and consumer preferences. The relatively specialized nature of disinfectant products creates opportunities for companies to establish strong customer relationships and brand loyalty through superior efficacy performance and reliable consumer support services.

KEY MARKET PLAYERS

A dominating playerin the Europeand NorthAmericann disinfectants and cleaning agents market

- Procter & Gamble (US)

- Unilever (GB)

- Reckitt Benckiser (GB)

- SC Johnson (US)

- Henkel (DE)

- Ecolab (US)

- Diversey Holdings (US)

- Clorox (US)

- BASF (DE)

- Kao Corporation (JP)

Top Players In The Market

- Procter & Gamble Company Procter & Gamble Company maintains a prominent position in the North America disinfectants and cleaning agents market through its comprehensive portfolio of Mr. Clean, Febreze, and Swiffer brand products that cater to diverse consumer cleaning and disinfection needs across residential and commercial applications. The company's extensive research and development capabilities have enabled the creation of innovative formulations that combine effective pathogen elimination with consumer-friendly application methods and pleasant sensory experiences. P&G has successfully leveraged its established brand recognition and global distribution networks to achieve widespread market penetration and consumer acceptance of advanced cleaning solutions. The organization's commitment to sustainability and environmental responsibility has earned strong consumer trust and loyalty within the cleaning products community. Their investment in consumer education initiatives and usage guidance has enhanced user confidence and product adoption rates. P&G actively collaborates with healthcare professionals and environmental organizations to ensure product safety and efficacy. The company's global manufacturing footprint and supply chain capabilities enable consistent product availability and competitive pricing across diverse market segments.

- Reckitt Benckiser Group plc Reckitt Benckiser Group plc has established itself as a significant player in the North America disinfectants and cleaning agents market through its Lysol, Dettol, and Harpic brand offerings that provide consumers and institutions with reliable antimicrobial solutions for health protection and environmental sanitation. The company's extensive scientific expertise and manufacturing capabilities have enabled the development of high-efficacy disinfectants that meet stringent regulatory standards and address emerging pathogenic threats. Reckitt Benckiser has successfully integrated disinfectant product development into its broader health and hygiene portfolio, leveraging existing brand equity and distribution channels to achieve market penetration. The organization's commitment to innovation is evident through continuous product improvements and new formulation introductions that address evolving consumer demands and regulatory requirements. Their focus on evidence-based efficacy and safety testing appeals to health-conscious consumers and institutional purchasers seeking validated performance claims. Reckitt Benckiser maintains strong relationships with healthcare providers and regulatory agencies to ensure optimal product positioning and regulatory compliance. The company actively participates in public health initiatives and disease prevention campaigns to build brand awareness and consumer trust. Clorox Company has emerged as a leading specialist in the North American disinfectants and cleaning agents market through its extensive range of bleach-based and quaternary ammonium compound disinfectants that serve residential, commercial, and institutional customers seeking reliable pathogen elimination and surface sanitation solutions. The company's commitment to scientific rigor and product efficacy has established strong brand loyalty among professional cleaners, healthcare facilities, and environmentally conscious consumers who prioritize proven performance and safety standards. Clorox has successfully differentiated itself through extensive product variety, including specialized formulations for specific applications such as food service, healthcare, and educational environments. The organization's expertise in chemical formulation and manufacturing has enabled the creation of superior disinfectant products that deliver exceptional pathogen elimination results while maintaining user safety and surface compatibility. Their direct-to-consumer marketing approach and strong retail partnerships have facilitated brand building and customer engagement within the cleaning products community. Clorox maintains close relationships with retailers and distributors to ensure optimal product placement and consumer accessibility. The company actively supports public health education and disease prevention initiatives, reinforcing its commitment to community health and safety.

Top Strategies Used By Key Market Participants

- Product Innovation and Formulation Advancement Leading manufacturers in the North America disinfectants and cleaning agents market have prioritized continuous product innovation and formulation advancement to maintain competitive advantages and address evolving consumer requirements and regulatory standards. Companies invest significantly in research and development activities focused on improving efficacy against emerging pathogens, enhancing user safety profiles, and developing environmentally sustainable formulations that meet modern consumer expectations. Innovation efforts encompass developing new active ingredients, optimizing delivery systems, and creating specialized formulations for specific surface types and application environments. Manufacturers also focus on sensory enhancement through improved fragrances, color systems, and texture modifications that enhance user experience and product appeal. Technical improvements in concentration efficiency, shelf stability, and packaging design enhance product performance and consumer convenience. These innovation initiatives help companies differentiate their offerings and command premium pricing while expanding addressable market segments through improved performance characteristics and broader consumer appeal.

- Strategic Partnerships and Channel Development Key players in the market have increasingly focused on forming strategic partnerships and channel development initiatives to expand market reach, enhance distribution capabilities, and leverage complementary expertise for mutual growth and market development. These collaborative arrangements enable disinfectant and cleaning agent manufacturers to access new customer segments, utilize retail partners' marketing expertise, and share development costs for advanced formulations and packaging solutions. Partnership strategies often involve exclusive product development agreements, co-marketing initiatives, and joint promotional campaigns that combine manufacturing capabilities with retail partners' customer insights and merchandising expertise. Companies also establish relationships with healthcare providers, facility management companies, and institutional purchasers to create business-to-business sales channels and expand product applications. Alliance formation extends to ingredient suppliers and technology providers to ensure consistent quality and access to innovative components. These strategic relationships provide manufacturers with enhanced market visibility and access to end-user networks while reducing individual risk exposure and development costs through shared resources and expertise.

- Consumer Education and Brand Building Leading manufacturers recognize the importance of comprehensive consumer education and brand-building programs in overcoming adoption barriers and expanding disinfectants and cleaning agents market penetration. Companies have implemented extensive educational initiatives,s including usage instruction guidance, efficacy information dissemination, and safety awareness campaigns that help consumers achieve optimal cleaning outcomes and build confidence in producperformanceceBrand-building programsms feature interactive marketing campaigns, social media engagement, and collaboration with influencers and health experts to showcase product benefits and inspire proper usage behaviors. Manufacturers also develop digital resources and mobile applications that provide personalized product recommendations and usage tips based on consumer preferences and cleaning requirements. Community involvement extends to supporting public health initiatives, participating in disaster relief efforts, and partnering with educational organizations to promote proper hygiene practices. These educational and brand-building efforts create consumer trust and facilitate broader market acceptance while establishing opportunities for brand loyalty development and long-term customer relationships.

MARKET SEGMENTATION

This research report on the Europe disinfectants and cleaning agents market is segmented and sub-segmented into the following categories.

By End-Use

- Residential

- Commercial

- Healthcare Facilities

- Educational Institutions

- Hospitality

By Application

- Household

- Industrial

- Healthcare

- Food Safety

- Institutional

By Product

- Surface Cleaners

- Disinfectant Wipes

- Hand Sanitizers

- Floor Cleaners

- Aerosol Disinfectants

By Formulation Type

- Liquid

- Gel

- Foam

- Spray

- Powder

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

Frequently Asked Questions

What is the North America disinfectants and cleaning agents market?

This market includes the production, distribution, and use of disinfectants and cleaning agents — chemical formulations designed to eliminate pathogens, maintain hygiene, and sanitize surfaces across residential, commercial, healthcare, and industrial settings.

What drives growth in the North America disinfectants and cleaning agents market?

Growth is driven by heightened hygiene awareness, stringent safety regulations, healthcare sanitation needs, pandemic-induced demand, and increased commercial and industrial cleaning practices.

What are disinfectants and cleaning agents used for?

These products are used to kill or reduce microbes, sanitize surfaces, control infections, and maintain cleanliness in homes, hospitals, schools, offices, and public facilities.

What types of products are included in this market?

Key types include surface disinfectants, sanitizers, antimicrobial cleaners, liquid detergents, wipes, sprays, and specialty industrial cleaning agents.

Which end-use industries drive demand?

Major end users include healthcare facilities, residential households, commercial establishments, hospitality, food & beverage processing, and industrial cleaning services.

How did COVID-19 impact this market?

The pandemic significantly increased demand for disinfectants, sanitizers, and high-efficacy cleaning agents as hygiene protocols intensified across public, workplace, and home environments.

What trends are influencing the disinfectants market?

Current trends include eco-friendly and biodegradable formulas, plant-based cleaners, no-VOC products, multi-surface disinfectants, and smart dispensing systems.

How do regulations affect this market?

Strict government standards for efficacy, labeling, safety, and microbial control — especially from agencies like the EPA and FDA — shape product formulations and market compliance.

What challenges does the market face?

Challenges include raw material price volatility, regulatory compliance costs, competition from private labels, and a shift in consumer preferences toward natural or green products.

Which regions in North America dominate the market?

The United States leads due to large healthcare and commercial sectors, followed by Canada with growing institutional and household hygiene demand.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com