North America Dry Type Transformer Market Size, Share, Trends & Growth Forecast Report By Technology (Cast Resin, Vacuum Pressure Impregnated), Voltage (Low Voltage, Medium Voltage, High Voltage), Application (Industrial, Commercial, Utilities, Others), Phase (Single Phase, Three Phase), and Country (United States, Canada, Mexico, Rest of North America) – Industry Analysis From 2026 to 2034

Market Size, 2025

$2.56 BnMarket Estimate, 2026

$2.72 BnMarket Forecast, 2034

$4.41 BnCAGR, 2026–2034

6.22%North America Dry Type Transformer Market Size

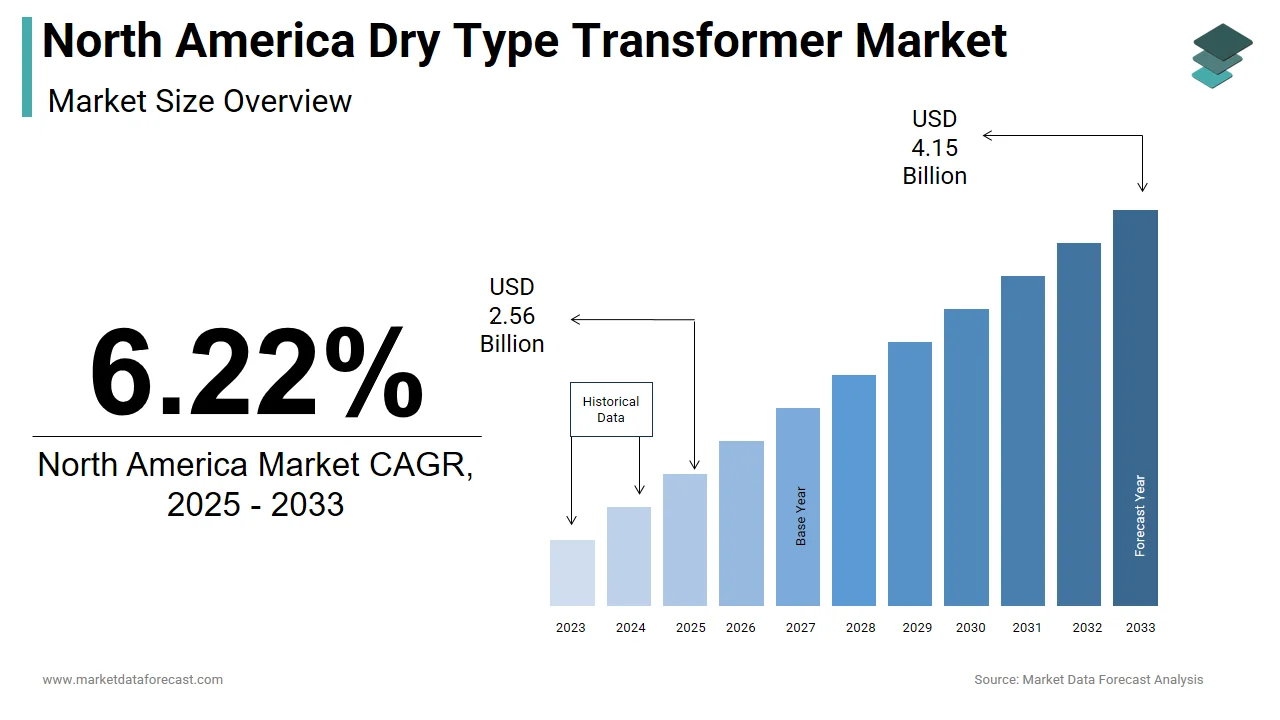

The size of the North America dry type transformer market was worth USD 2.56 billion in 2025. The North America market is anticipated to grow at a CAGR of 6.22% from 2026 to 2034 and be worth USD 4.41 billion by 2034 from USD 2.72 billion in 2026.

Dry type transformer are widely used in commercial buildings, industrial facilities, data centers, healthcare institutions, and renewable energy installations due to their fire-resistant properties, compact design, and low maintenance requirements.

According to the U.S. Energy Information Administration, electricity consumption in the commercial and industrial sectors accounts for a significant portion of total energy usage in the United States, highlighting the need for reliable and efficient power distribution systems. As per Natural Resources Canada, similar trends are observed in the Canadian economy, where increasing urbanization and infrastructure modernization efforts have spurred demand for advanced electrical equipment. This has led to a growing preference for dry type transformers, especially in densely populated areas where safety and space constraints make oil-immersed alternatives impractical.

Additionally, regulatory agencies such as OSHA and NFPA have emphasized fire safety standards in indoor electrical installations, further boosting the adoption of dry type transformers.

MARKET DRIVERS

Increasing Demand for Electrical Safety in Urban and Indoor Installations

A primary driver fueling the North America dry-type transformer market is the heightened emphasis on electrical safety, particularly in urban and indoor environments such as high-rise buildings, hospitals, universities, and data centers. Unlike traditional oil-filled transformers, dry type transformers eliminate the risk of flammable liquid leaks and fire hazards, making them the preferred choice for locations with stringent fire codes and limited ventilation.

According to the National Fire Protection Association, electrical equipment was involved in 16% of non-residential structure fires in 2023, underscoring the need for inherently safer electrical infrastructure. In response, building codes such as the National Electrical Code (NEC) and local fire regulations increasingly mandate the use of dry type transformers in commercial and institutional buildings. For example, New York City’s Department of Buildings requires dry type transformers for all new high-density residential and commercial developments within city limits.

Furthermore, as urbanization accelerates and real estate developers prioritize compact and safe electrical solutions, dry type transformers are being integrated into microgrids, modular substations, and edge computing centers.

Expansion of Renewable Energy and Grid Modernization Initiatives

Another key driver propelling the North America dry type transformer market is the rapid expansion of renewable energy projects and ongoing investments in grid modernization. As solar farms, wind parks, and battery storage systems become more prevalent, there is a growing need for transformers that can safely and efficiently integrate distributed energy resources into the grid without posing fire or environmental risks.

According to the U.S. Department of Energy, over $30 billion was allocated toward grid modernization and resilience programs between 2021 and 2023 , including upgrades to substations, transmission lines, and localized energy hubs. Dry type transformers play a crucial role in these initiatives, particularly in rooftop solar installations, electric vehicle charging stations, and behind-the-meter energy storage units where oil-based alternatives are not viable due to safety and space constraints.

Moreover, utilities and municipalities are adopting smart grid technologies that require compact and eco-friendly transformers for secondary distribution networks.

MARKET RESTRAINTS

Higher Initial Cost Compared to Oil-Immersed Transformers

One of the most significant restraints affecting the North America dry type transformer market is the higher initial capital cost compared to conventional oil-immersed transformers. While dry type transformers offer superior safety, environmental benefits, and lower long-term maintenance expenses, their upfront acquisition price remains a deterrent, especially for budget-conscious industrial and utility operators.

This cost differential is primarily attributed to the use of high-grade insulation materials, copper windings, and enhanced cooling structures necessary to dissipate heat effectively without liquid dielectric fluids.

Moreover, in large-scale industrial plants and rural substations where fire risk is relatively lower, project managers often opt for oil-immersed transformers to minimize capital expenditures.

Limited Load Capacity and Thermal Limitations

Inherent limitations in handling high voltage and heavy load applications is another notable constraint hindering the widespread adoption of dry type transformers in North America. Unlike oil-immersed transformers, which benefit from superior thermal conductivity and insulation properties, dry type transformers face challenges in maintaining optimal operating temperatures under continuous high-load conditions.

According to IEEE standards, dry type transformers typically exhibit lower thermal endurance and current-carrying capabilities, restricting their deployment in major transmission substations and high-voltage industrial settings. This limitation makes them less suitable for applications requiring transformers rated above 15 MVA at voltages exceeding 34.5 kV, which are common in large-scale utility operations.

As a result, many power generation and transmission companies continue to rely on mineral oil-based transformers for backbone grid infrastructure. Although technological advancements are improving the performance of dry type units, they remain predominantly suited for distribution-level applications rather than bulk power transfer.

MARKET OPPORTUNITIES

Growing Adoption in Data Centers and Edge Computing Facilities

A promising opportunity for the North America dry type transformer market lies in its expanding application within data centers and edge computing infrastructures. As digital transformation accelerates and cloud service providers invest heavily in localized computing nodes, there is a rising need for compact, fire-safe, and efficient power distribution solutions.

Given the confined spaces and critical uptime requirements of these facilities, dry type transformers are increasingly favored over oil-filled models due to their minimal fire risk and ease of integration within modular server racks and prefabricated electrical rooms.

Also, the proliferation of edge computing—where processing occurs closer to end-users—has intensified demand for decentralized power solutions that can operate reliably in diverse environments. Dry type transformers are well-suited for these deployments, offering a balance between performance, safety, and spatial efficiency. With the digital infrastructure boom continuing, this segment presents a lucrative growth avenue for transformer manufacturers.

Integration with Electric Vehicle Charging Infrastructure

An emerging prospect for the North America dry type transformer market is its increasing integration into electric vehicle (EV) charging networks. As EV adoption gains momentum and governments push for nationwide charging infrastructure expansion, the need for safe, compact, and resilient electrical equipment has never been greater.

According to the U.S. Department of Transportation, over 7,000 public EV charging stations were installed across the U.S. in 2023, with plans to add tens of thousands more under the National Electric Vehicle Infrastructure (NEVI) Formula Program. Many of these stations are in urban centres, shopping malls, office complexes, and highway rest stops—environments where fire safety and space efficiency are paramount. Dry type transformers are ideal for these settings due to their non-flammable nature and ability to be housed indoors or near users.

Utilities and private operators are increasingly deploying dry type transformers at these sites to step down high voltage from the grid to levels compatible with Level 3 DC fast chargers

MARKET CHALLENGES

Supply Chain Constraints and Raw Material Price Volatility

A key challenge facing the North America dry type transformer market is the volatility in raw material prices and supply chain disruptions that impact production timelines and cost structures. Transformers require substantial amounts of copper, aluminum, and insulation materials, all of which have experienced fluctuating costs due to geopolitical tensions, trade restrictions, and logistical bottlenecks.

According to the International Copper Study Group, copper prices rose by over 18% in 2023, driven by strong demand from the renewable energy and electrification sectors. Similarly, resin and epoxy suppliers—key components in dry-type transformer insulation—faced shortages due to manufacturing delays and input cost increases. As per Deloitte’s 2023 Industrial Outlook, nearly 60% of electrical equipment manufacturers in North America reported extended lead times due to material sourcing issues.

These fluctuations pose a significant challenge for manufacturers attempting to maintain stable pricing and consistent delivery schedules

Technological Complexity in Enhancing Performance Capabilities

Another pressing challenge confronting the North America dry type transformer market is the technological complexity involved in improving performance characteristics such as thermal efficiency, load capacity, and insulation longevity. While dry type transformers offer clear safety and environmental advantages, they must overcome technical limitations to compete effectively in high-demand applications.

Like, enhancing the thermal dissipation and dielectric strength of dry type transformers requires advanced engineering techniques, including vacuum pressure impregnation (VPI), cast resin encapsulation, and nanotechnology-based insulation materials. However, implementing these technologies at scale demands significant R&D investment and specialized manufacturing expertise.

This challenge is particularly pronounced in industrial settings where transformers must operate continuously under harsh conditions. Manufacturers must strike a delicate balance between performance enhancements and cost-effectiveness to ensure broad market acceptance.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Technology, Voltage, Application, Phase, and Region. |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | United States, Canada, Mexico, and the Rest of North America. |

| Market Leaders Profiled | Schneider Electric, Siemens Energy, Eaton, Hitachi Ltd., TOSHIBA CORPORATION, General Electric, Fuji Electric Co., Ltd., CG Power & Industrial Solutions Ltd., Kirloskar Electric Company, HYOSUNG HEAVY INDUSTRIES, Hammond Power Solutions, VOLTAMP, WEG, TMC TRANSFORMERS S.P.A., Hanley Energy, alfanar Group, Efacec, TBEA Co., Ltd., JST Power Equipment, INC., Raychem RPG Private Limited, and RPT Ruhstrat Power Technology GmbH, Delta Star Power Manufacturing Corp., and Others. |

SEGMENTAL ANALYSIS

By Technology Insights

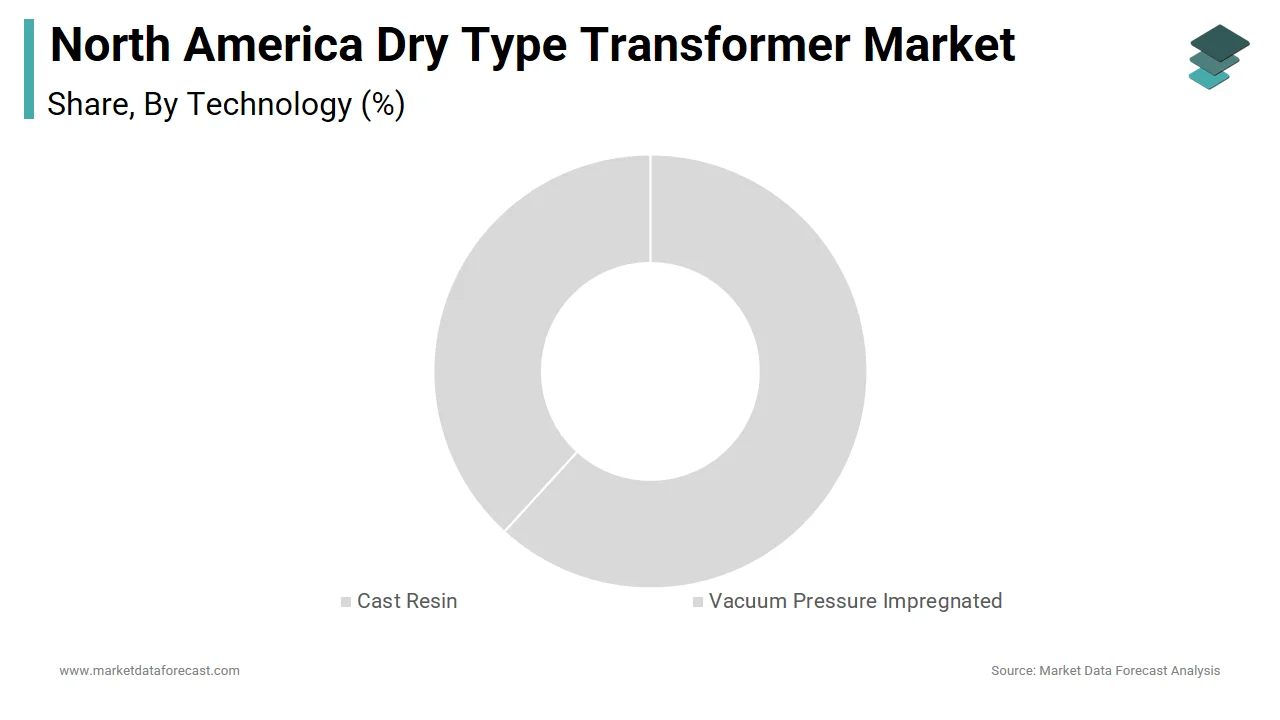

The cast resin technology dominated the North America dry type transformer market, holding a 58.7% of the total market share in 2024. This segment’s superiority is credited to its superior insulation properties, high mechanical strength, and long service life, making it ideal for applications requiring reliability and fire safety in enclosed environments.

One key driver of cast resin dominance is its widespread use in commercial buildings, data centers, and industrial facilities where compactness and safety are critical. Additionally, the National Fire Protection Association has highlighted that cast resin transformers significantly reduce the risk of electrical fires, aligning with evolving building safety regulations.

Vacuum Pressure Impregnated (VPI) dry type transformers are emerging as the fastest-growing segment in the North America market, projected to expand at a CAGR of 7.4%. This growth is primarily driven by the increasing demand for cost-effective, scalable, and customizable transformer solutions in industrial and utility applications.

A major factor fueling VPI adoption is its lower manufacturing complexity compared to cast resin alternatives, which allows for faster production cycles and reduced material costs.

Also, VPI technology offers enhanced performance in dynamic load conditions, making it suitable for renewable energy installations and electric vehicle charging stations. With ongoing advancements in impregnation techniques and rising demand for flexible power solutions, VPI dry type transformers are gaining traction across both legacy and emerging markets in North America.

By Voltage Insights

The medium voltage segment led the North America dry type transformer market by capturing a 46.2% of total revenue share in 2024. This segment serves as the backbone for power distribution in commercial buildings, industrial plants, and utility substations, where efficient voltage transformation is essential without compromising on space or safety.

A primary aspect behind this segment’s dominance is the extensive deployment of medium voltage dry type transformers in commercial real estate developments. These transformers are particularly favored in indoor settings due to their fire-safe operation and ability to support large-scale HVAC, lighting, and IT infrastructure.

The integration of these transformers into microgrids and distributed energy resources further supports their widespread use.

High-voltage dry-type transformers represented the highest-growing segment in the North America market, moving ahead at a CAGR of 8.2%. While traditionally dominated by oil-immersed models, dry type transformers above 36 kV are gaining traction due to advancements in insulation technologies and increasing demand for safer, eco-friendly alternatives in specialized applications.

One key growth driver is the deployment of high-voltage dry-type transformers in renewable energy installations, particularly wind farms and solar parks located near urban or environmentally sensitive zones. According to the U.S. Department of Energy, wind capacity additions reached record levels in 2023, with many developers opting for dry type transformers at collection points to avoid oil spill risks and comply with stricter environmental regulations.

Additionally, innovations such as vacuum pressure encapsulation and hybrid cooling methods have enabled these transformers to handle higher loads while maintaining operational stability.

By Phase Insights

Three-phase dry type transformers accounted for the biggest segment in the North America market, representing approximately 68.3% of total market share in 2024. This dominance is largely due to their widespread use in industrial, commercial, and utility applications where balanced, high-efficiency power distribution is required.

A key driver behind the leadership of three-phase transformers is their integral role in supporting heavy-duty electrical equipment such as motors, compressors, and HVAC systems commonly found in manufacturing plants, data centers, and large commercial complexes.

Moreover, as per the National Electrical Manufacturers Association (NEMA), three-phase transformers offer superior load-handling capabilities and energy efficiency compared to single-phase variants, making them indispensable in applications requiring continuous and stable power supply. Utilities and independent power producers also favor three-phase dry type transformers for grid-connected renewable energy systems, ensuring smooth integration of solar and wind power into the electrical network.

Single-phase dry type transformers are the booming segment in the North America market, estimated to expand at a CAGR of 7.9%. This growth is fueled by rising demand for decentralized power solutions in residential, small commercial, and edge computing applications.

A major factor driving this segment’s expansion is the surge in rooftop solar installations and battery storage systems among homeowners and small businesses. According to the Solar Energy Industries Association (SEIA), residential solar deployments in the U.S. grew in 2023 , necessitating compact and safe power conversion units compatible with low-voltage distribution networks. Single-phase dry type transformers are ideal for these applications due to their compact size, ease of installation, and absence of flammable materials.

Apart from these, municipalities and utility companies are also incorporating these units into EV charging stations, rural electrification projects, and smart grid pilot programs.

By Application Insights

The industrial application segment prevailed in the North America dry type transformer market, accounting for 44.8% of total demand in 2024. This superiority is propelled by the sector’s reliance on reliable and fire-safe electrical infrastructure to power machinery, automation systems, and process control equipment.

A main factor contributing to this segment’s leadership is the rapid expansion of advanced manufacturing, chemical processing, and food production industries, all of which require robust electrical systems that can operate safely in confined spaces.

Moreover, companies in sectors such as pharmaceuticals, semiconductors, and automotive assembly have increasingly adopted dry type transformers to ensure uninterrupted operations and compliance with sustainability targets.

Apart from these, the integration of industrial IoT and smart factory technologies has heightened the need for compact and efficient power solutions.

The commercial application segment is the fastest-growing category in the North America dry type transformer market, expanding at a CAGR of 8.1%. This development is primarily driven by the rapid development of office buildings, retail complexes, healthcare facilities, and educational institutions that prioritize fire safety, energy efficiency, and space optimization.

A key factor fueling this segment’s expansion is the increasing number of green building certifications, such as LEED and WELL, which encourage the use of non-flammable and low-maintenance electrical equipment.

Additionally, as per the National Association of Realtors, demand for energy-efficient commercial real estate surged in 2023, with tenants showing a strong preference for buildings equipped with modern electrical infrastructure. Hospitals and universities have been early adopters of dry type transformers due to their need for continuous power supply and fire-resistant design. The proliferation of mixed-use developments and smart building technologies is further reinforcing the demand for commercial-grade dry type transformers across North America.

COUNTRY-LEVEL ANALYSIS

The United States was the top performing player in the North America dry type transformer market, contributing 75.1% of total regional demand in 2024. This lead position is underpinned by a combination of robust industrial activity, rapid commercial construction, and substantial investments in grid modernization and renewable energy integration.

Major industry players such as Eaton, Siemens, and ABB have expanded their manufacturing and distribution capabilities to meet rising domestic demand. With ongoing investments in smart cities, industrial electrification, and sustainable infrastructure, the U.S. continues to drive innovation and growth in the North American dry type transformer market.

Canada is positioning it as a rapidly growing contributor to regional demand. This growth is fueled by stringent fire safety regulations, increasing investments in clean energy infrastructure, and a strong push toward decarbonization in both public and private sectors.

The Canadian Standards Association (CSA) has reinforced national electrical codes to promote the use of fire-safe transformers in commercial and institutional buildings, particularly in provinces like Ontario and British Columbia.

Also, municipalities such as Vancouver and Toronto have implemented policies encouraging the use of dry type transformers in underground and indoor substations to enhance fire safety and land-use efficiency.

The Rest of North America, comprising Mexico and select Caribbean territories, contributes a share of total regional demand for dry type transformers in 2024. Though currently a smaller market, it presents significant growth opportunities due to increasing industrialization, expanding commercial infrastructure, and evolving regulatory frameworks promoting safer electrical systems.

The Mexican government has also introduced updated electrical safety standards that encourage the adoption of dry type transformers in new commercial developments and industrial parks.

Additionally, in the Caribbean, countries like Jamaica and the Bahamas are investing in resilient and fire-safe power infrastructure following recent hurricane-related disruptions.

COMPETITIVE LANDSCAPE

The competition in the North America dry type transformer market is marked by a convergence of established global manufacturers, regional specialists, and emerging technology-driven firms striving to capture market share. As demand for safer, more sustainable, and space-efficient electrical infrastructure grows, companies are increasingly differentiating themselves through product innovation, digital integration, and enhanced service offerings. The market is witnessing heightened activity from both legacy electrical equipment providers and newer entrants focused on niche applications such as renewable energy integration and microgrid deployment. Competitive strategies revolve around expanding localized production capabilities, improving energy efficiency ratings, and ensuring compliance with stringent fire safety regulations. Additionally, with increasing emphasis on decarbonization and grid modernization, manufacturers are aligning their portfolios with evolving industry standards and customer expectations. This dynamic environment fosters continual advancement in transformer design, making the North American market a hub of technological progress and strategic expansion.

MARKET KEY PLAYERS

Companies playing a dominant role in the North America dry type transformer market profiled in this report are

- Schneider Electric

- Siemens Energy

- Eaton

- Hitachi Ltd.

- TOSHIBA CORPORATION

- General Electric

- Fuji Electric Co., Ltd.

- CG Power & Industrial Solutions Ltd.

- Kirloskar Electric Company

- HYOSUNG HEAVY INDUSTRIES

- Hammond Power Solutions

- VOLTAMP

- WEG

- TMC TRANSFORMERS S.P.A.

- Hanley Energy

- alfanar Group

- Efacec

- TBEA Co., Ltd.

- JST Power Equipment, INC.

- Raychem RPG Private Limited

- RPT Ruhstrat Power Technology GmbH

- Delta Star Power Manufacturing Corp.

TOP LEADING PLAYERS IN THE MARKET

- Eaton is a leading player in the North America dry type transformer market, known for its extensive portfolio of power management solutions. The company has consistently innovated in electrical infrastructure, offering high-performance, fire-safe transformers tailored for commercial, industrial, and utility applications. Eaton’s focus on energy efficiency, smart grid compatibility, and sustainability has reinforced its reputation as a trusted provider across diverse sectors.

- Siemens plays a pivotal role in shaping the North America dry type transformer landscape through its advanced engineering capabilities and commitment to digitalization in power systems. The company delivers highly reliable and compact transformers designed for urban substations, data centers, and renewable energy integration. Siemens' global expertise and strong regional partnerships have enabled it to maintain a competitive edge in delivering customized, high-quality electrical infrastructure.

- Schneider Electric is a key contributor to the North America dry type transformer market, emphasizing eco-friendly and digitally enabled power distribution solutions. The company integrates its transformers into smart building and industrial automation systems, aligning with the region’s growing emphasis on sustainable and efficient energy use. Schneider’s strategic investments in research and localized manufacturing support its leadership in meeting evolving customer needs across critical infrastructure segments.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Product Innovation and Technological Advancement

Leading players prioritize continuous innovation in insulation materials, cooling mechanisms, and digital monitoring features to enhance transformer performance and longevity. By integrating smart sensors and predictive maintenance capabilities, companies aim to offer superior reliability and energy efficiency that meet modern infrastructure demands.

Expansion of Manufacturing and Distribution Capabilities

To meet rising regional demand, manufacturers are investing in new production facilities and strengthening logistics networks across North America. This allows them to reduce lead times, improve serviceability, and better serve large-scale infrastructure and industrial clients requiring consistent supply.

Strategic Collaborations and Acquisitions

Key participants actively engage in partnerships, joint ventures, and acquisitions to expand their technological footprint and geographic reach. These collaborations often involve local engineering firms, utilities, and renewable energy developers to ensure alignment with evolving regulatory and market requirements.

RECENT MARKET DEVELOPMENTS

- In February 2024, Eaton announced the launch of a new line of low-voltage dry type transformers specifically engineered for data center applications, aiming to address rising concerns around thermal efficiency and uninterrupted power supply in high-density computing environments.

- In May 2024, Siemens partnered with a leading U.S.-based renewable energy developer to supply custom-engineered dry type transformers for a series of solar farms across the Midwest, reinforcing its presence in clean energy infrastructure projects.

- In July 2024, Schneider Electric inaugurated a new regional manufacturing facility in Texas dedicated to producing next-generation dry type transformers, enhancing its ability to meet growing demand from industrial and commercial customers across the southern United States.

- In September 2024, a major Canadian electrical equipment distributor signed an exclusive distribution agreement with ABB to expand the availability of its dry type transformer portfolio in Eastern Canada, supporting increased adoption in institutional and municipal buildings.

- In November 2024, General Electric Power launched a digital asset management platform integrated with its dry type transformer models, allowing commercial and utility clients to monitor real-time performance metrics and optimize maintenance schedules remotely.

MARKET SEGMENTATION

This research report on the North America dry type transformer market is segmented and sub-segmented into the following categories.

By Technology

- Cast Resin

- Vacuum Pressure Impregnated

By Voltage

- Low Voltage

- Medium Voltage

- High Voltage

By Application

- Industrial

- Commercial

- Utilities

- Others

By Phase

- Single Phase

- Three Phase

By Country

- United States

- Canada

- Mexico

- Rest of North America

Frequently Asked Questions

1. What are the main growth drivers for the North America dry type transformer market?

Key drivers include rising demand for energy-efficient solutions, grid modernization, renewable energy integration, and strict safety and environmental regulations

2. Which countries dominate the North America dry type transformer market?

The United States leads due to large-scale infrastructure investments and regulatory support, with Canada also contributing through renewable energy and industrial projects

3. What are the primary end-user industries for dry type transformers in North America?

Major end-users include industrial facilities, commercial buildings, inner-city substations, renewable energy plants, and utility companies

4. How does urbanization impact the demand for dry type transformers in North America?

Urbanization increases demand for safe, compact, and reliable transformers for inner-city substations and green building projects

5. What role do safety and environmental regulations play in shaping the North America dry type transformer market?

What role do safety and environmental regulations play in shaping the North America dry type transformer market?

6. What technological advancements are influencing the North America dry type transformer market?

Innovations include smart grid compatibility, advanced insulation materials, improved energy efficiency, and compact, modular designs

7. What are the key challenges facing the North America dry type transformer market?

Challenges include higher initial costs, competition from traditional oil-filled transformers, and the need for skilled installation and maintenance personnel

8. How is the rise of smart grids affecting the North America dry type transformer market?

Smart grid implementation drives demand for reliable, low-maintenance, and intelligent transformers to support grid stability and integration of distributed energy resources

9. Who are the leading manufacturers in the North America dry type transformer market?

Key players include Eaton, ABB, Siemens, Schneider Electric, and other major electrical equipment companies

10. What future trends are expected in the North America dry type transformer market?

Trends include greater adoption in renewable integration, digital monitoring, modular solutions, and expansion into emerging applications like electric vehicle charging infrastructure

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com