- Product Description Description

- Table of Contents TOC

- List of Table & Figure LOT

- Get Free Sample PDF Sample PDF

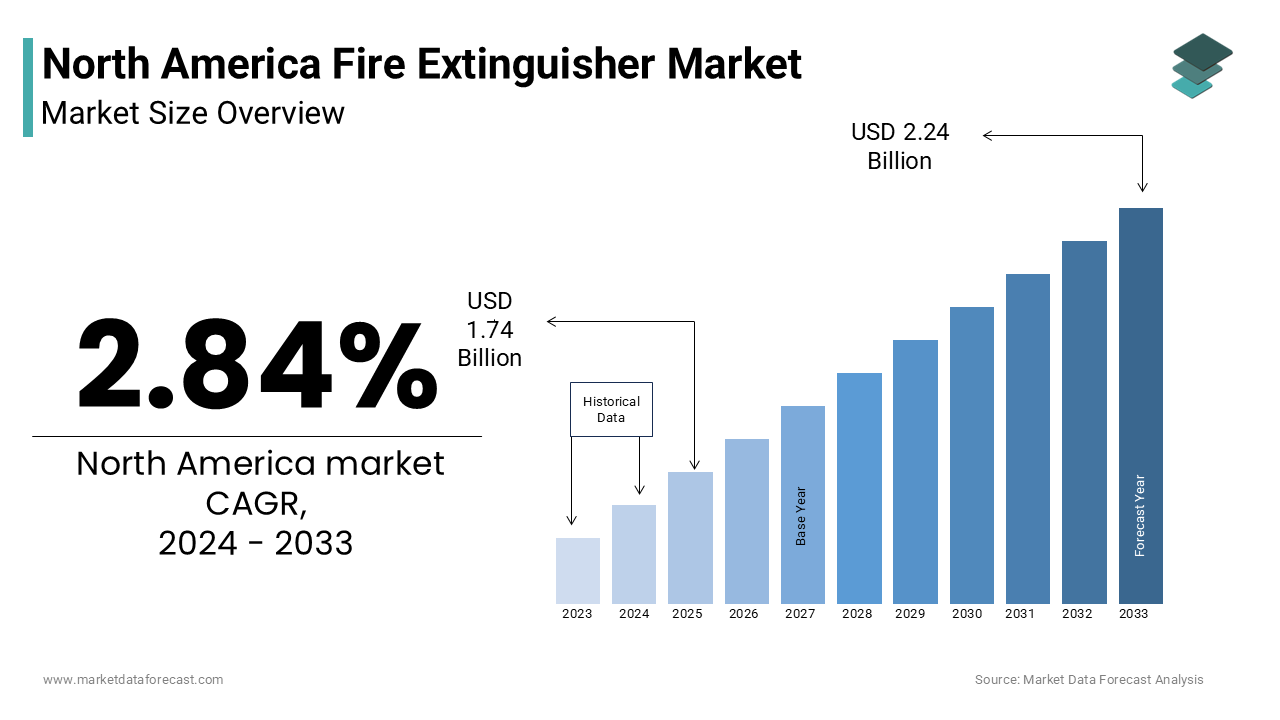

North America Fire Extinguisher Market Size

The North America Fire Extinguisher Market is anticipated to rise from USD 1.74 billion in 2024 to USD 2.24 billion in 2033, growing at a CAGR of 2.84%.

Fire extinguisher is a suppression system designed for use during a fire in residential, commercial, industrial, and institutional settings. These devices are essential components of fire safety infrastructure, aimed at minimizing damage and preventing casualties by enabling early-stage firefighting. The market includes a variety of extinguishing agents such as dry chemical powders, carbon dioxide, foam, and clean agents, each tailored to specific fire classes—A, B, C, D, and K.

Also, the persistent risk has reinforced regulatory mandates requiring fire extinguishers in both public and private buildings. In Canada, provincial fire codes mandate regular inspections and maintenance of fire extinguishers in all commercial establishments, as outlined by the Canadian Standards Association (CSA).

In addition to compliance-driven adoption, growing awareness among consumers and businesses about proactive fire safety measures has spurred demand. Technological advancements, including smart fire extinguishers equipped with pressure sensors and remote monitoring capabilities, are gaining traction, particularly in high-risk sectors like healthcare, data centers, and transportation hubs.

MARKET DRIVERS

Increasing Incidence of Urban and Industrial Fires

The rising incidence of urban and industrial fires, which has heightened the need for accessible and reliable fire suppression tools, is one of the primary drivers fueling the growth of the North America fire extinguisher market. Manufacturing plants, warehouses, and construction sites are particularly vulnerable due to the presence of flammable materials, electrical equipment, and heavy machinery.

In response, regulatory bodies have mandated stricter fire safety protocols. The Occupational Safety and Health Administration (OSHA) requires that all workplaces maintain properly rated fire extinguishers within easy reach of employees. Apart from these, in Canada, recent amendments to the Ontario Fire Code have further emphasized the need for routine inspection and accessibility of extinguishing systems in industrial facilities.

Moreover, the increasing number of wildfires encroaching on urban areas has led to greater emphasis on preparedness at both individual and organizational levels. Businesses located in fire-prone zones are proactively installing advanced fire suppression units to protect assets and ensure employee safety. These factors drive consistent demand for fire extinguishers across North America.

Strengthened Regulatory Framework and Compliance Mandates

The strengthening of fire safety regulations and compliance requirements across multiple sectors is another significant driver of the North America fire extinguisher market. Governments and standard-setting organizations have continuously updated fire protection codes to align with evolving risks associated with modern infrastructure and industrial operations.

At the federal level, the Department of Homeland Security and the Federal Emergency Management Agency have collaborated with local authorities to enhance community fire resilience programs. These initiatives include mandatory fire extinguisher availability in schools, hospitals, office complexes, and multi-family housing units. Similarly, Transport Canada enforces stringent fire safety rules for marine vessels, rail transport, and aviation facilities, all of which must be equipped with certified fire extinguishers.

Besides, insurance providers have begun tying coverage eligibility and premium structures to fire safety compliance, encouraging businesses and homeowners to invest in certified extinguishing systems. In addition, properties with up-to-date fire suppression systems experience significantly lower claim payouts in the event of fire incidents.

MARKET RESTRAINTS

High Cost of Maintenance and Refilling Services

The relatively high cost of maintenance, recharging, and periodic inspection services, which discourages frequent replacement and upkeep, especially among small businesses and residential users, is a key restraint affecting the North America fire extinguisher market. While initial purchase costs may be moderate, ongoing compliance with fire safety standards necessitates regular servicing, including pressure testing, part replacement, and refilling of extinguishing agents.

These recurring expenses pose a financial burden, particularly for small and medium-sized enterprises (SMEs) operating on tight budgets. Many businesses delay or neglect scheduled maintenance due to cost concerns, increasing the risk of non-compliance during fire inspections. In some cases, expired or improperly maintained extinguishers fail to function during emergencies, leading to legal liabilities and potential fines from regulatory authorities.

Moreover, consumer awareness regarding proper maintenance practices remains limited, contributing to premature disposal and inefficient use of fire extinguishers. In rural and low-income communities, where budget constraints are more pronounced, this issue is even more acute.

Availability of Alternative Fire Suppression Technologies

The increasing adoption of alternative fire suppression technologies that reduce reliance on traditional handheld extinguishers is another notable restraint impacting the North America fire extinguisher market. Systems such as automatic sprinklers, gaseous suppression agents, and water mist technology are being increasingly integrated into commercial and industrial buildings as primary fire control mechanisms.

Water mist systems, in particular, have gained popularity in sensitive environments like data centers, museums, and healthcare facilities due to their ability to suppress flames without causing water damage. Similarly, inert gas-based suppression systems are preferred in server rooms and electrical substations where residue-free extinguishing is crucial. As per the California Department of Forestry and Fire Protection, large-scale industrial operators are increasingly opting for these alternatives to meet stringent fire safety regulations while minimizing human intervention during emergencies.

Furthermore, the integration of smart fire detection and suppression systems—capable of triggering automatic responses upon detecting heat or smoke—is reducing the need for manual firefighting equipment.

MARKET OPPORTUNITIES

Integration of Smart Fire Extinguishers with IoT Technology

The integration of smart fire extinguishers with Internet of Things (IoT) technology is one of the most promising opportunities emerging in the North America fire extinguisher market. Traditional fire extinguishers require manual checks and scheduled maintenance, but IoT-enabled models can provide real-time status updates, alerting users to pressure drops, tampering, or expiration dates. According to the Fire Equipment Manufacturers' Association, over 30% of commercial fire extinguishers in the U.S. were found to be out of compliance during annual inspections in 2023 due to unnoticed maintenance issues.

Smart fire extinguishers address this problem by embedding sensors and wireless communication modules that connect to centralized building management systems. These innovations are particularly valuable in high-traffic environments such as airports, hospitals, and large retail complexes, where maintaining operational readiness is critical.

Moreover, major fire safety equipment manufacturers are investing in digital platforms that allow facility managers to remotely monitor extinguisher conditions across multiple locations. This trend aligns with broader industry shifts toward predictive maintenance and automation, offering a compelling value proposition for both new installations and retrofits.

Expansion of Fire Safety Regulations in Residential Settings

The growing emphasis on fire safety in residential environments, driven by evolving building codes and increased public awareness, is an expanding opportunity in the North America fire extinguisher market. Historically, fire extinguishers were predominantly installed in commercial and industrial premises, but recent policy changes have extended requirements to multifamily dwellings and single-family homes in several jurisdictions.

In response, state and municipal governments have introduced new fire safety mandates. These regulatory developments are increasing the penetration of fire extinguishers in residential markets.

Moreover, public education campaigns led by fire departments and insurance companies have been instrumental in promoting household fire preparedness. As per the American Red Cross, fire safety outreach programs have contributed to a 12% increase in residential fire extinguisher purchases since 2021.

MARKET CHALLENGES

Lack of Standardized Training and Awareness Among End Users

The lack of standardized training and awareness among end users regarding proper fire extinguisher operation and maintenance is a significant challenge facing the North America fire extinguisher market. Despite widespread availability, many individuals remain unfamiliar with how to effectively use a fire extinguisher during an emergency.

This knowledge gap extends beyond residential users to include small business owners and employees who may not receive adequate fire safety instruction. The Occupational Safety and Health Administration mandates that employers provide fire extinguisher training to workers, yet compliance varies significantly across industries. As per a 2023 report by the U.S. Chamber of Commerce, less than half of small businesses conducted regular fire drills or provided hands-on extinguisher training to staff.

Moreover, improper handling of fire extinguishers can lead to misuse or failure to contain minor fires, escalating risks rather than mitigating them. Misuse also results in unnecessary replacements, adding to costs for businesses and households.

Supply Chain Disruptions and Raw Material Price Volatility

Supply chain disruptions and fluctuations in raw material prices, which impact production timelines and cost structures, are another pressing challenge confronting the North America fire extinguisher market. The global supply chain crisis, exacerbated by geopolitical tensions and pandemic-related bottlenecks, has affected the availability of critical components such as steel cylinders, valves, and fire-retardant chemicals. According to Deloitte’s 2023 Global Supply Chain Report, industrial equipment manufacturers, including fire extinguisher producers, experienced an average component delivery delay of six to nine weeks during the year.

Further, inflationary pressures have led to sharp increases in the cost of raw materials. The Bureau of Labor Statistics recorded a 14% year-over-year rise in steel prices in 2023, directly affecting the manufacturing costs of fire extinguisher casings. Similarly, lithium hexafluorophosphate—a key ingredient in dry chemical extinguishers—saw price volatility due to supply constraints from Asian suppliers. These cost escalations have forced manufacturers to either absorb higher expenses or pass them on to consumers, potentially dampening demand.

Smaller fire extinguisher manufacturers, in particular, struggle to manage procurement uncertainties and maintain competitive pricing.

SEGMENTAL ANALYSIS

By Product Insights

The portable fire extinguisher segment led the North America fire extinguisher market by accounting for 63.7% of total revenue in 2024. Mandatory inclusion of portable fire extinguishers in building codes is one major driver behind the growth of portable fire extinguisher segment. Their widespread use across residential, commercial, and industrial applications due to their compact size, ease of operation, and regulatory mandates requiring installation in various occupancies is also attributed to the dominance of portable fire extinguisher segment.

The National Fire Protection Association (NFPA) standard 10 requires that all commercial buildings have easily accessible portable extinguishers rated for the specific fire hazards present. Apart from these, local fire departments across the U.S. and Canada conduct regular inspections to ensure compliance, reinforcing consistent demand. The high adoption rate in households and small businesses is another key factor.

The wheeled fire extinguisher segment is emerging as the fastest-growing category and is projected to expand at a CAGR of 6.9% from 2025 to 2033. The increasing industrialization and expansion of large-scale facilities is a primary drivers for this growth of wheeled fire extinguisher segment. These larger-capacity units are designed for high-risk environments such as warehouses, manufacturing plants, airports, and oil refineries, where extended fire suppression capabilities are required. These facilities often require wheeled extinguishers with higher agent volumes to tackle Class A, B, and C fires effectively.

Besides, enhanced safety protocols in transportation hubs and logistics centers are fueling demand. Major airport authorities, including the Federal Aviation Administration (FAA), mandate wheeled fire extinguishers in aircraft hangars and cargo terminals.

By Extinguishing Agent Insights

The dry chemical fire extinguisher segment commanded the biggest business share of 54.6% of the North America market in 2024. The broad applicability across diverse fire scenarios is one key reason for the dominance of the dry chemical fire extinguisher segment. These extinguishers are widely used due to their versatility in suppressing multiple fire types—Class A, B, and C—making them suitable for both residential and commercial settings. Dry chemical agents like monoammonium phosphate and sodium bicarbonate effectively interrupt the chemical reaction of combustion, making them ideal for electrical equipment, flammable liquids, and solid combustibles. According to the National Fire Protection Association, over 80% of commercial establishments in the U.S. use dry chemical extinguishers as part of their fire protection systems.

Regulatory support and industry standards is another major driver. OSHA mandates that workplaces handling flammable materials must have access to ABC-rated dry chemical extinguishers. Similarly, Transport Canada enforces strict fire safety requirements on transport vehicles and industrial sites, where dry chemical extinguishers are preferred due to their rapid suppression capability and wide compatibility.

The carbon dioxide-based fire extinguisher segment is witnessing the highest growth and is projected to expand at a CAGR of 7.2% through 2033. Rising demand in sensitive environments such as data centers, laboratories, and healthcare facilities, where residue-free fire suppression is essential is driving the growth of carbon dioxide-based fire extinguisher segment. The expansion of mission-critical infrastructure is another key catalyst. Moreover, stricter environmental regulations are boosting adoption. Unlike halon-based systems, which are being phased out globally due to ozone-depleting effects, CO₂ extinguishers offer an eco-friendly alternative. The Environmental Protection Agency has endorsed CO₂ systems under its SNAP program as acceptable substitutes for ozone-harming agents, further accelerating their deployment across regulated industries.

By Fire Type Insights

The Class A fire extinguisher segment secured the largest portion of the North America market by representing 44.1% of total sales in 2024. The high frequency of structural fires involving common combustible materials is a primary driver of this dominance of the Class A fire extinguisher segment. These incidents typically occur in homes, schools, and commercial buildings, necessitating widespread availability of Class A extinguishers.

Further, building code requirements reinforce the necessity of Class A-rated units. The International Building Code mandates that multi-family dwellings, hotels, and office complexes be equipped with extinguishers suitable for Class A hazards. The Canadian Standards Association also specifies Class A coverage in public buildings and educational institutions. As urbanization expands and occupancy densities rise, the demand for Class A fire extinguishers remains strong across North America.

The Class C fire extinguisher segment is the fastest-growing within the North America market and is projected to expand at a CAGR of 7.6% from 2025 to 2033. The rapid expansion of digital infrastructure is one key growth driver. Class C extinguishers using non-conductive agents such as carbon dioxide or clean agents are preferred in these environments. These extinguishers are designed for fires involving energized electrical equipment, making them indispensable in modern infrastructure reliant on electronics and power systems.

Apart from these, the rising adoption of electric vehicle charging stations and renewable energy installations is fueling demand. Class C extinguishers are increasingly installed at these locations to mitigate potential hazards. As electrification continues across sectors, the Class C segment is poised for sustained growth.

By Application Insights

The industrial application segment commanded the North America fire extinguisher market by capturing 39.2% of total usage in 2024. The presence of numerous flammable substances and high-heat processes in industrial settings is one key driver. This dominance is also due to stringent fire safety regulations and the inherently high-risk nature of operations in manufacturing, chemical processing, and energy production. The Occupational Safety and Health Administration mandates that all manufacturing facilities maintain fire extinguishers rated for the specific hazards present, including Class B and C fires. According to the NFPA, industrial fire incidents accounted for nearly 25% of all reported structural fires in the U.S. in 2023, underscoring the critical need for reliable fire suppression tools. Besides, growing investment in plant expansions and automation is increasing fire load risks.

The public areas application segment is experiencing the highest growth, with a projected CAGR of 8.1%. The increase in mass gathering venues and infrastructure modernization projects is a major growth driver. Each of these facilities is required to install fire extinguishers by NFPA 10 and local fire codes. Furthermore, heightened security concerns following recent fire-related incidents in public spaces have prompted stricter enforcement of fire safety measures. With growing emphasis on emergency preparedness and crowd safety, the public areas segment is set to remain a key growth engine for the North America fire extinguisher market.

REGIONAL ANALYSIS

United States Fire Extinguisher Market Insights

The United States secured the dominant position in the North America fire extinguisher market by accounting for 76.4% of regional revenue in 2024. This lead position is underpinned by a robust regulatory framework, extensive industrial activity, and high levels of public awareness regarding fire safety. A key factor driving market strength is the comprehensive fire safety legislation enforced at both the federal and state levels. The National Fire Protection Association regularly updates fire protection codes, mandating fire extinguisher installation in commercial buildings, schools, hospitals, and residential complexes. The Federal Emergency Management Agency collaborates with local fire departments to ensure compliance, reinforcing consistent demand for fire suppression equipment.

Moreover, frequent fire incidents across densely populated urban centers contribute to ongoing market expansion. According to the U.S. Fire Administration, over 1.3 million fires were reported nationwide in 2023, highlighting the persistent need for fire prevention tools. The insurance sector also plays a role by linking property coverage eligibility to fire extinguisher presence, further incentivizing adoption across sectors.

Canada Fire Extinguisher Market Insights

Canada is maintaining steady growth supported by strong fire safety regulations and increasing infrastructure development. A key growth driver is the enforcement of mandatory fire extinguisher provisions in commercial and institutional buildings. The Canadian Standards Association mandates that all public facilities, including schools, hospitals, and office complexes, be equipped with certified fire extinguishers. Provinces like Ontario and British Columbia have introduced stricter inspection regimes, ensuring that extinguishers remain functional and up to date.

Moreover, industrial expansion in mining, oil & gas, and manufacturing sectors is boosting demand for specialized fire suppression equipment. Also, remote industrial sites increasingly rely on wheeled and portable extinguishers to manage fire risks in off-grid locations. With growing emphasis on workplace safety and regulatory compliance, Canada’s fire extinguisher market is expected to maintain a stable upward trajectory.

Rest of North America Fire Extinguisher Market Insights

The Rest of North America, comp rising Mexico and smaller Caribbean economies, accounts for a notable share of the regional fire extinguisher market, showing gradual but promising growth. One key growth factor is the surge in nearshoring and manufacturing investments, particularly in northern Mexican states. As industrial zones develop, fire extinguisher adoption is expanding alongside. Further, weaker grid reliability in parts of Mexico and the Caribbean has led to increased reliance on fire safety equipment. While still an emerging market, this region presents significant long-term potential for fire safety equipment providers.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Johnson Controls (Ansul), Kidde (a brand of Carrier Global Corporation), Amerex Corporation, Buckeye Fire Equipment Company, Badger Fire Protection, Minimax USA, Fireboy-Xintex, H3R Performance, Kanex Fire, and Globe Fire Sprinkler Corporation are some of the key market players.

The competition in the North America fire extinguisher market is marked by a mix of established global players and dynamic regional manufacturers striving to capture market share through innovation, compliance, and enhanced service offerings. As fire safety regulations become more stringent and public awareness grows, companies are under pressure to deliver high-quality, reliable, and technologically advanced fire suppression solutions. Product differentiation has become a key battleground, with manufacturers introducing smart fire extinguishers, environmentally friendly agents, and customized systems tailored to specific industries such as healthcare, data centers, and transportation.

Customer service and maintenance support have also emerged as differentiators, with leading players offering comprehensive inspection, recharging, and training programs to ensure long-term product effectiveness. Apart from these, strategic acquisitions and partnerships are being leveraged to expand geographic reach and integrate complementary technologies. While large multinational corporations dominate due to their brand strength and extensive distribution networks, mid-sized firms are gaining traction by focusing on niche applications and localized support structures. This evolving competitive landscape ensures continuous innovation and improvement in fire safety standards across the region.

Top Players in the North America Fire Extinguisher Market

Kidde Fire Safety

Kidde, a division of UTC Climate, Controls & Security, is a leading manufacturer of fire safety products with a strong presence across North America. The company offers a comprehensive range of portable and industrial-grade fire extinguishers tailored for residential, commercial, and institutional use. Known for its innovation and reliability, Kidde plays a crucial role in setting industry standards and advancing fire suppression technologies globally.

Amerex Corporation

Amerex is one of the largest manufacturers of fire extinguishers in the United States, recognized for its durable and high-performance fire suppression systems. The company serves diverse sectors including aviation, marine, industrial, and commercial facilities. Amerex's commitment to quality and customization has made it a trusted name in both domestic and international markets, contributing significantly to global fire safety initiatives.

Ansul Company

A subsidiary of Carrier Global Corporation, Ansul specializes in advanced fire suppression solutions, particularly for commercial kitchens and industrial applications. With a focus on engineered systems and specialized agents, Ansul delivers tailored fire protection that meets stringent regulatory requirements. Its expertise in complex fire risk environments has positioned it as a key player in shaping modern fire safety protocols worldwide.

Top Strategies Used by Key Market Participants

One major strategy employed by leading fire extinguisher manufacturers is product innovation and diversification, aimed at addressing evolving fire risks and regulatory demands. Companies are investing in R&D to develop advanced extinguishing agents, eco-friendly alternatives, and smart-enabled fire suppression systems that offer real-time monitoring and improved performance.

Another critical approach is strategic partnerships and distribution network expansion, allowing companies to strengthen their regional foothold and ensure faster service delivery. By collaborating with local distributors, fire departments, and safety consultants, market leaders enhance product accessibility and after-sales support, reinforcing customer trust and brand loyalty.

Lastly, firms are increasingly focusing on certifications and compliance alignment with international fire safety standards. This not only facilitates cross-border market entry but also reassures end users of product reliability and adherence to the latest safety benchmarks, thereby reinforcing competitive positioning.

RECENT MARKET DEVELOPMENTS

- In February 2024, Kidde Fire Safety introduced a new line of smart fire extinguishers equipped with IoT-based monitoring features, enabling real-time status updates and predictive maintenance alerts for commercial building managers.

- In May 2024, Amerex Corporation expanded its manufacturing facility in Oklahoma to increase production capacity and improve supply chain efficiency, ensuring the timely delivery of fire extinguishers to customers across the U.S.

- In July 2024, Ansul Company launched a dedicated training initiative in partnership with fire departments across North America to educate businesses and institutions on proper fire extinguisher usage and maintenance procedures.

- In October 2024, Badger Fire Protection announced a strategic collaboration with a green chemical supplier to develop next-generation clean agent fire extinguishers that align with environmental sustainability goals without compromising performance.

- In December 2024, First Alert, a leading consumer fire safety brand, rolled out an integrated fire safety campaign targeting residential users, combining fire extinguisher sales with free online training modules and home safety assessments.

MARKET SEGMENTATION

This research report on the North America Fire Extinguisher Market has been segmented and sub-segmented into the following categories.

By Product

- Portable

- Wheeled

- Knapsack

By Extinguishing Agent

- Dry Chemicals

- Carbon Dioxide (CO₂)

- Foam

- Others

By Fire Type

- Class A

- Class B

- Class C

- Others

By Application

- Industrial

- Public Areas

- Commercial

- Households

- Others

By Country

- U.S.

- Canada

- Rest of North America