North America Fire Protection Water Storage Tanks Market Size, Share, Trends & Growth Forecast Report - Segmented By Material Type (Steel Fiberglass, Reinforced Plastic (FRP)), Coating Type, Size, Application and Country (The United States, Canada and Rest of North America), Industry Analysis From 2024 to 2033

North America Fire Protection Water Storage Tanks Market Size

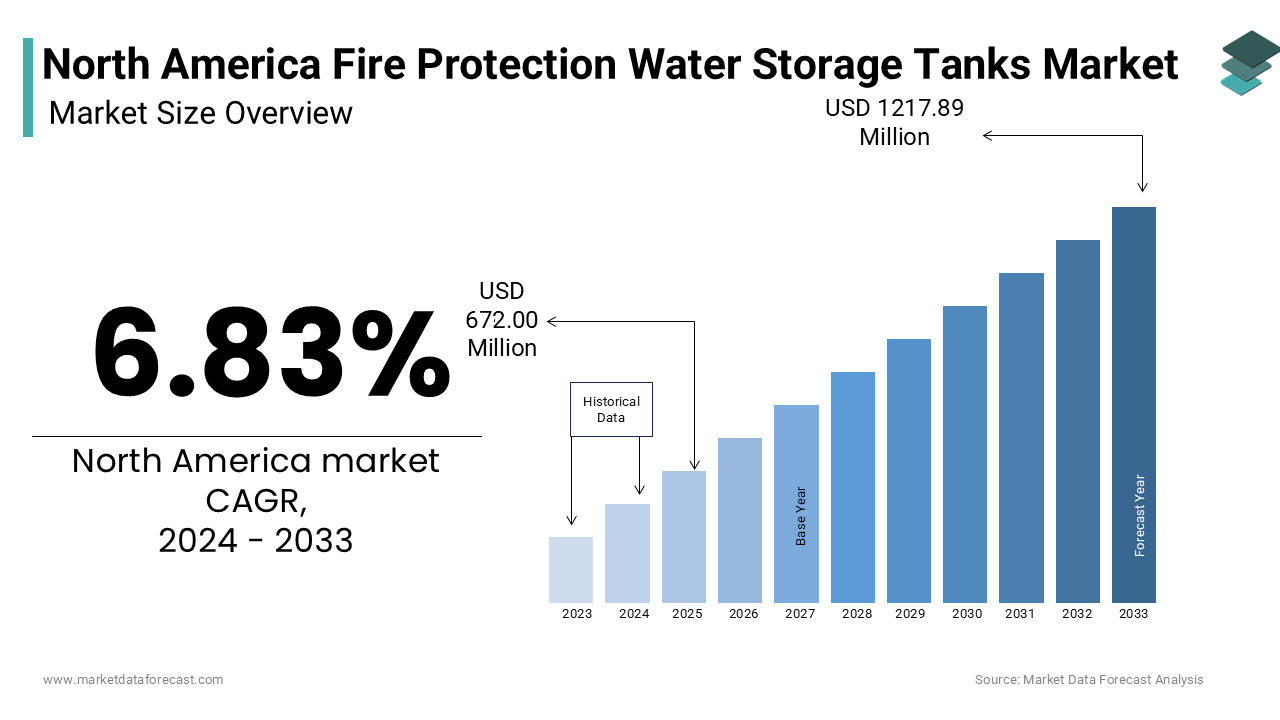

The North America Fire Protection Water Storage Tanks Market is estimated to grow from USD 672.00 million in 2024 to USD 1217.89 million in 2033, representing a CAGR of 6.83%.

The fire protection water storage tanks are engineered reservoirs designed to ensure a reliable and immediate supply of water for firefighting systems in commercial, industrial, and municipal infrastructures. These tanks are integral components of passive fire safety systems, supporting sprinklers, standpipes, and hydrant networks by maintaining pressurized water reserves independent of municipal supply fluctuations. As per the National Fire Protection Association, over 70% of industrial facilities and high-rise buildings in the United States are mandated to have on-site water storage for fire suppression, reinforcing the structural necessity of these systems.

MARKET DRIVERS

The escalating construction of high-rise and large-footprint commercial buildings in urban centers such as Toronto, Chicago, and Dallas is propelling the growth of the North America fire protection water storage tanks market. These structures inherently demand robust, code-compliant fire suppression systems due to occupant density and structural complexity. According to the Council on Tall Buildings and Urban Habitat, North America witnessed the completion of 58 buildings exceeding 200 meters in height between 2015 and 2023, each requiring dedicated fire water storage as per NFPA 22 standards. The standard mandates minimum water reserves ranging from 20,000 to over 100,000 gallons depending on building size and hazard classification. High-rise buildings, in particular, cannot rely solely on municipal water pressure with elevated or ground-level storage tanks to ensure adequate flow and pressure during emergencies.

The growing vulnerability of infrastructure to climate-induced disruptions, particularly droughts and wildfires, which compromise municipal water availability is additionally to enhance the growth of the North America fire protection water storage tanks market. As per the U.S. Drought Monitor, over 40% of the contiguous United States experienced moderate to extreme drought conditions in 2023, which is affecting water utility reliability in states like California, Arizona, and Texas. In such regions, reliance on public water systems for firefighting becomes precarious, especially during dry seasons when demand surges and reservoir levels decline. For instance, California’s State Fire Marshal now requires facilities in Very High Fire Hazard Severity Zones to maintain minimum 2-hour water supply reserves for firefighting, independent of external sources.

MARKET RESTRAINTS

The escalating cost of raw materials, particularly steel and reinforced concrete, which constitute the primary construction materials for large-capacity tanks is major factor that is limiting the growth of North America fire protection water storage tanks market. According to the U.S. Bureau of Labor Statistics, the producer price index for fabricated structural metal products increased by 28.7% between January 2021 and December 2023, driven by global supply chain disruptions and heightened demand for industrial metals. This inflation directly impacts the manufacturing and installation costs of welded steel and bolted tanks, which dominate the market due to their durability and scalability. Municipalities and private developers, particularly in mid-sized cities, are increasingly delaying or downsizing fire protection projects due to budget constraints. Additionally, the Portland Cement Association confirms that concrete prices rose by 22% during the same period, affecting precast and cast-in-place tank construction. These cost pressures are especially acute in rural areas where funding for public safety infrastructure is limited.

The prolonged permitting and inspection timelines imposed by local fire marshals and building departments, which delay the deployment of fire protection water storage systems is also restricting the growth of the North America fire protection water storage tanks market. In states like California and New York, where fire codes are regularly updated to reflect evolving risk profiles, developers must navigate complex inter-agency coordination between fire departments, water authorities, and environmental agencies. For example, in Texas, the State Office of Risk Management recorded a 30% increase in permit appeals related to water storage design compliance between 2021 and 2023. In industrial zones such as the Gulf Coast petrochemical corridor, where rapid facility commissioning is important, such delays can result in operational standstills. Moreover, inconsistencies in code interpretation across jurisdictions create uncertainty for national contractors, discouraging standardized deployment models.

MARKET OPPORTUNITIES

The integration of smart monitoring technologies within fire protection water storage systems by enabling real-time diagnostics and predictive maintenance is posing new opportunities for the growth of the North America fire protection water storage tanks market. As per the Smart Water Networks Forum, over 60% of water utilities in the United States have initiated digital transformation programs since 2021, many of which include remote sensing for fire infrastructure. Modern fire tanks are increasingly equipped with ultrasonic level sensors, pressure transducers, and corrosion monitoring systems that transmit data to centralized platforms via IoT networks. For instance, the City of Denver implemented a wireless tank monitoring system across 45 fire water reservoirs in 2022 by reducing inspection-related labor costs by 35% and improving leak detection response time by 58%, as documented by the Municipal Water District of Southern California. These technologies ensure continuous compliance with NFPA 25 inspection standards, which require monthly visual checks and annual internal assessments. Furthermore, the U.S. Department of Energy highlights that predictive analytics can extend tank service life by 15–20% by identifying early-stage corrosion or structural fatigue.

The expansion of fire protection water storage in renewable energy facilities, particularly solar farms and battery storage plants, which present novel fire hazards is greatly influencing the growth of the North America fire protection water storage tanks market. As per the North American Electric Reliability Corporation, the installed capacity of utility-scale solar in the U.S. surged from 15 gigawatts in 2018 to over 47 gigawatts in 2023, often located in arid, remote regions with limited firefighting resources. These installations are susceptible to electrical fires and thermal runaway in lithium-ion battery units, necessitating dedicated on-site water reserves. The National Renewable Energy Laboratory reports that 23% of solar-plus-storage facilities commissioned in 2023 included fire water tanks, up from 8% in 2020, reflecting heightened risk awareness. For example, the Gemini Solar Project in Nevada, one of the largest in the U.S., incorporates a 2-million-gallon fire water reservoir to support emergency response.

MARKET CHALLENGES

The aging workforce and shortage of skilled technicians capable of designing, inspecting, and maintaining complex fire water systems is ascribed to limit the growth of the North America fire protection water storage tanks market. As per the U.S. Bureau of Labor Statistics, the median age of construction and maintenance workers in fire protection specialties is 52.3 years, and nearly 40% of these professionals are projected to retire by 2030. The shortage is particularly acute in rural and remote regions where access to certified inspectors is limited. Moreover, NFPA 25 mandates rigorous inspection protocols, including internal tank assessments every three to five years, which require specialized knowledge in structural integrity and corrosion control.

The increasing frequency of extreme weather events, such as hurricanes, freezing temperatures, and wildfires, which compromise the structural integrity and operational readiness of fire protection water storage tanks. As per the National Oceanic and Atmospheric Administration, the U.S. experienced 28 billion-dollar weather and climate disasters in 2023 with the highest annual count on record, with significant impacts on infrastructure. In regions like the Gulf Coast, Category 4 hurricanes have caused tank uplift, foundation erosion, and contamination of water reserves due to storm surge infiltration. The American Society of Civil Engineers documents that 17% of fire water tanks in Louisiana required post-hurricane remediation in 2021 due to structural deformation. In northern states such as Minnesota and Alberta, prolonged sub-zero temperatures lead to ice formation inside tanks, which is rendering water inaccessible during emergencies.

SEGMENTAL ANALYSIS

By Material Type Insights

The steel segment was the largest and held a prominent share of the the North America fire protection water storage tanks market in 2024 with its structural robustness and adaptability to large-scale industrial and municipal applications. According to the National Fire Protection Association, over 85% of high-hazard industrial facilities in the U.S. specify welded steel tanks due to their capacity to store over 250,000 gallons reliably. Additionally, the Steel Tank Institute confirms that steel tanks exhibit a service life exceeding 40 years when properly coated and maintained, outperforming alternatives in durability under extreme climatic and operational stress. The material’s weldability also allows for custom configurations, essential for facilities with spatial constraints or complex piping networks. The petrochemical sector, concentrated along the Gulf Coast, heavily relies on steel tanks over 70% of new refinery fire water systems installed in 2023 used bolted or welded steel, as documented by the American Petroleum Institute.

The Fiberglass Reinforced Plastic (FRP) segment is projected to grow with a CAGR of 7.8% in the next coming years with the increasing demand in corrosive environments where traditional materials degrade rapidly. Water Environment Federation reports that 42% of new wastewater facilities constructed in 2023 opted for FRP tanks due to their inherent resistance to chemical degradation. Unlike coated steel, fiberglass does not require re-lining or cathodic protection, reducing lifecycle maintenance costs by up to 30%, as noted in a 2022 study by the Structural Composites Research Network. Furthermore, the lightweight nature of FRP facilitates faster installation, cutting labor time by nearly 50% compared to field-welded steel, a factor increasingly valued in remote or hard-to-access locations.

By Coating Type Insights

The epoxy coating segment was the largest by accounting for 59.1% of the North America fire protection water storage tanks market share in 2024 with its widespread use in potable water-compatible fire tanks, particularly in commercial and municipal applications where water quality is paramount. According to the Environmental Protection Agency, over 90% of public water systems in the U.S. require NSF 61-compliant linings for any tank in contact with potable reserves, including fire protection units that may interface with drinking water networks. Additionally, epoxy provides a seamless, impermeable barrier against internal corrosion, a leading cause of tank failure. According to the American Water Works Association, internal corrosion accounts for 44% of premature tank degradation, and epoxy-lined steel tanks have demonstrated a 35% lower corrosion rate over 15 years compared to uncoated counterparts. The material’s versatility allows application in both factory-finished and field-applied settings, making it suitable for bolted, welded, and composite tanks. The prevalence of epoxy is further reinforced by insurance providers such as FM Global, which mandates epoxy lining for tanks in high-value industrial facilities to reduce risk exposure.

The Glass-Fused-to-Steel (GFS) coating segment is lucratively growing with an expected CAGR of 8.2% from 2025 to 2033 with its superior durability in aggressive external environments, particularly in wastewater and industrial zones. The fusion process involves vitrifying glass enamel onto steel at temperatures exceeding 850°C, which is creating a chemically inert surface impervious to sulfides, chlorides, and acidic vapors. Moreover, GFS tanks require minimal maintenance, with inspection intervals extending to 10 years under NFPA 25 guidelines, reducing lifecycle costs by up to 25%, as confirmed by the Infrastructure Sustainability Council of North America.

By Size Insights

The 100,000–250,000-gallon capacity segment was the largest and held 38.2% of the North America fire protection water storage tanks market share in 2024 with its alignment with mid-sized commercial and industrial facilities, which constitute the bulk of new construction activity. Additionally, this size range offers optimal balance between cost and functionality tanks in this category can be pre-fabricated and transported via standard flatbed trucks, which is avoiding the logistical complexities and site assembly costs associated with larger units. Furthermore, insurance underwriters such as ISO Rating Services classify facilities with 150,000-gallon reserves as having superior fire protection ratings, directly lowering property insurance premiums.

The >250,000-gallon segment is anticipated to grow with a CAGR of 8.7% throughout the forecast period owing to the rise of mega-industrial facilities and energy infrastructure projects requiring massive on-site water reserves. According to the Uptime Institute, the average hyperscale data center now requires over 500,000 gallons of fire water storage, with some facilities in Virginia and Ontario installing dual-tank systems exceeding 1 million gallons. The 2023 expansion of the Cameron LNG terminal in Louisiana included a 750,000-gallon fire water reservoir, as documented by the project’s environmental impact statement.

By Application Insights

The industrial application segment was the largest by occupying 54.3% of the North America fire protection water storage tanks market share in 2024 with the high fire load and regulatory rigor associated with manufacturing, chemical processing, and energy production facilities. NFPA 30 and NFPA 652 mandate dedicated water storage for such operations, with minimum reserves often exceeding 200,000 gallons. Additionally, industrial facilities face stringent insurance requirements—FM Global mandates that facilities in high-hazard classifications maintain on-site water storage with no reliance on municipal supply.

The commercial application segment is projected to expand at a CAGR of 7.5% from 2025 to 2033 with the rapid development of mixed-use complexes, data centers, and logistics hubs, which integrate fire protection into core design. These facilities, often classified as Group F or S occupancies under the International Building Code, require automatic sprinkler systems supported by dedicated water tanks in areas with inadequate municipal pressure. The retrofitting of aging commercial buildings to meet modern fire codes in downtown districts of cities like Atlanta and Vancouver, which is prompting the growth of the segment. The General Services Administration notes that federal building upgrades between 2021 and 2023 included fire water tank installations in 41% of retrofitted facilities. Additionally, commercial developers are adopting performance-based fire safety designs that require engineered water reserves, further boosting demand.

REGIONAL ANALYSIS

The United States was the top performer in the North America fire protection water storage tanks market by capturing 78.3% of the share in 2024 with its vast industrial base, stringent fire safety regulations, and high volume of commercial construction. Additionally, the U.S. leads in non-residential construction, with spending reaching $1.14 trillion in 2023, according to the U.S. Census Bureau. Urbanization in Sun Belt states like Texas and Florida is fueling demand for high-rise buildings and data centers, both of which rely on on-site water reserves. The National Fire Protection Association confirms that 48 states have adopted NFPA 22 into their building codes, ensuring widespread compliance. Moreover, the Federal Emergency Management Agency identifies over 12,000 U.S. communities with inadequate municipal water pressure for firefighting, necessitating private storage solutions.

Canada was positioned second by holding 14.3% of share in 2024 with its vast geography, decentralized population, and growing industrial development in western provinces. A key driver is the reliance on private fire protection systems in remote and rural communities, where municipal water infrastructure is sparse. According to the Natural Resources Canada, over 60% of industrial facilities in Alberta and Saskatchewan are located more than 20 kilometers from a fire hydrant with on-site water storage. Additionally, Canada’s National Building Code mandates fire water storage for buildings exceeding 60 meters in height, which is spurring demand in urban centers like Toronto and Vancouver.

KEY MARKET PLAYERS AND COMPETETIVE LANDSCAPE

Superior Tank Co., Inc., Tank Connection LLC, T.F. Warren Group Inc., CST Industries Inc., National Storage Tank Inc., Fisher Tank Company, DN Tanks Inc., Gulf Coast Tank and Construction Co., and Pittsburg Tank & Tower Co. Inc.

The competitive landscape of the North America fire protection water storage tanks market is characterized by a blend of established manufacturers, regional specialists, and innovators leveraging material science and engineering excellence. Companies differentiate themselves not only through product durability and compliance but also via technical expertise, customization capabilities, and after-sales support. The market is moderately consolidated, with several key players dominating large-scale industrial and municipal contracts, while niche suppliers thrive in specialized segments such as corrosion-prone environments or remote installations. Competitive advantage is increasingly tied to engineering precision, adherence to NFPA and AWWA standards, and the ability to deliver integrated solutions that align with broader infrastructure goals.

Top Players in the Market

Contech Engineered Solutions

Contech Engineered Solutions is a leading provider of infrastructure solutions, including fire protection water storage tanks, with a strong footprint across North America. The company specializes in engineered stormwater and emergency water storage systems, integrating sustainability and regulatory compliance into its designs. Contech’s fire protection tanks are widely deployed in municipal, transportation, and industrial sectors, where reliability and resilience are paramount. Its integrated approach to site development allows seamless incorporation of fire water storage within broader infrastructure projects. Contech’s reputation for technical innovation and long-term durability has positioned it as a trusted partner for public agencies and private developers alike, contributing significantly to the advancement of resilient fire safety infrastructure across the continent.

Nova Cell Ltd.

Nova Cell Ltd. is a prominent manufacturer of polyethylene water storage tanks, serving both residential and commercial fire protection applications. Known for its corrosion-resistant and maintenance-free designs, the company has carved a niche in markets where chemical exposure and longevity are concerns. Nova Cell’s tanks are engineered to meet CSA and NSF standards, ensuring compatibility with potable water systems and fire suppression networks. The company emphasizes sustainable manufacturing practices and offers scalable solutions tailored to site-specific requirements. With a focus on innovation, Nova Cell continues to expand its product range to accommodate evolving fire safety codes and environmental conditions. Its tanks are increasingly specified in remote and rural installations where durability and ease of installation are essential.

Harper Tanks

Harper Tanks is a well-established manufacturer specializing in bolted and welded steel water storage systems for fire protection, industrial, and municipal applications. The company is recognized for its robust engineering, precision fabrication, and adherence to NFPA and AWWA standards. Harper Tanks offers a wide range of customizable solutions, including elevated and ground-level configurations, designed to withstand extreme environmental and operational conditions. The company’s commitment to quality control, long service life, and lifecycle support has earned it a loyal client base across North America. Its consistent performance and technical expertise have made it a preferred supplier in infrastructure projects.

Top Strategies Used by Key Market Participants

One major strategy employed by leading companies is product differentiation through advanced material engineering and coating technologies. Firms are increasingly investing in corrosion-resistant composites, fusion-bonded coatings, and hybrid designs to enhance durability and reduce maintenance, allowing them to cater to high-risk industrial environments and extend service life.

Another key approach is vertical integration of design, manufacturing, and installation services. This end-to-end capability strengthens client trust and reduces dependency on third parties, improving project outcomes and customer retention.

RECENT MARKET DEVELOPMENTS

- In March 2023, Contech Engineered Solutions launched a new line of precast concrete fire protection tanks with integrated monitoring sensors by enabling real-time water level and structural integrity tracking, enhancing compliance and operational reliability for municipal and industrial clients.

- In August 2023, Harper Tanks expanded its manufacturing facility in Tulsa, Oklahoma, to increase production capacity for bolted steel tanks, which is allowing faster delivery times and improved service coverage across the central and western United States.

- In January 2024, Nova Cell Ltd. introduced a next-generation polyethylene tank series with enhanced UV stabilization and seismic resistance, which is specifically designed for deployment in wildfire-prone and seismically active regions of the western U.S. and Canada.

- In June 2023, Contech Engineered Solutions partnered with a leading civil engineering firm to offer bundled stormwater and fire water storage solutions with infrastructure planning for large-scale commercial and industrial developments.

- In February 2024, Harper Tanks announced a collaboration with a fire safety certification body to develop a third-party verification program for tank installations by reinforcing trust in compliance and performance across high-risk industrial sectors.

MARKET SEGMENTATION

This research report on the North America fire protection water storage tanks market is segmented and sub-segmented based on categories.

By Material Type

- Steel

- Fiberglass Reinforced Plastic (FRP)

By Coating Type

- Epoxy Coating

- Glass-Fused-to-Steel (GFS) Coating

By Size

- 100,000–250,000 gallons

- 250,000 gallons

By Application

- Industrial

- Commercial

By Country

- U.S.

- Canada

- Rest of North America

Frequently Asked Questions

What is the North America Fire Protection Water Storage Tanks Market?

The market focuses on the design, manufacturing, and installation of dedicated storage tanks that supply water for fire suppression systems in industrial, commercial, and municipal facilities across North America.

Which material type dominates the market?

Steel tanks hold the largest share due to their durability, adaptability to large-scale applications, and proven long service life when properly maintained.

What is driving the demand for fire protection water tanks in North America?

Rising industrial safety regulations, growth in hyperscale data centers, energy infrastructure expansion, and stricter insurance requirements are fueling demand.

What is the future outlook for this market?

The market is expected to grow steadily with rising investments in industrial safety, retrofitting of commercial buildings, and expansion of mega-infrastructure projects requiring >250,000-gallon storage systems.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com