North America Green Cement Market Size, Share, Trends & Growth Forecast Report By Product Type (Fly Ash-Based Green Cement, Silica-Fume-Based Green Cement), Construction Sector, And Country (US, Canada, And Rest Of North America), Industry Analysis From 2025 To 2033

North America Green Cement Market Size

The North American Green Cement Market size was calculated to be USD 1.12 million in 2024 and is anticipated to be worth USD 2.32 million by 2033, from USD 1.21 million in 2025, growing at a CAGR of 8.45% during the forecast period.

The North American green cement market refers to the production and utilisation of eco-friendly cementitious materials that significantly reduce carbon emissions compared to conventional Portland cement. Green cement encompasses a variety of alternative binders such as geopolymer cement, calcined clay-based cement, slag-based composites, and other low-carbon derivatives designed to mitigate environmental impact without compromising structural integrity. This market has gained momentum in recent years due to increasing regulatory pressure, corporate sustainability goals, and public demand for greener infrastructure solutions.

North America, particularly the United States and Canada, is witnessing a gradual but significant shift toward sustainable construction practices. According to the U.S. Energy Information Administration, the industrial sector accounted for approximately 32% of total energy consumption in the U.S. in 2023, with the cement industry contributing disproportionately to CO₂ emissions. As per Environment and Climate Change Canada, the construction industry in Canada was responsible for around 9% of national greenhouse gas emissions in 2022. These figures underscore the urgency for alternative building materials like green cement. Additionally, the American Concrete Institute reported in 2024 that over 18% of new commercial construction projects in the U.S. now incorporate some form of low-carbon cementitious material.

MARKET DRIVERS

Increasing Government Regulations on Carbon Emissions

One of the most significant drivers of the North American green cement market is the tightening of government regulations aimed at reducing carbon emissions from industrial sectors, particularly construction and manufacturing. Cement production is among the largest industrial emitters of CO₂ globally, with traditional Portland cement alone accounting for a notable share of global emissions. In response, both the United States and Canada have implemented stringent emission reduction policies that are directly influencing the adoption of green cement alternatives. As per the EPA’s projections, these updated standards could result in a cumulative reduction of 16 million metric tons of CO₂-equivalent emissions by 2030. Similarly, Canada introduced the Output-Based Pricing System (OBPS) under its Clean Fuel Standard, which imposes carbon pricing mechanisms on large emitters, including cement manufacturers. These regulatory pressures are not only forcing existing players to adopt cleaner technologies but also encouraging innovation and investment in novel green cement formulations. For instance, companies like Carbicrete and Solexol Technologies have seen increased interest in their carbon-negative cement products, with pilot projects expanding across Ontario and California.

Rising Demand for Sustainable Infrastructure and Green Building Certifications

Another key driver of the North America green cement market is the growing emphasis on sustainable infrastructure development and the proliferation of green building certification programs. Developers and governments alike are increasingly prioritising environmentally responsible construction methods, which has led to a surge in demand for green cement—a critical component in achieving lower embodied carbon in buildings.

LEED v4.1, the latest version of the rating system, places greater emphasis on life cycle assessment and material transparency, making green cement an attractive option for earning credits. Moreover, federal and municipal incentives are playing a pivotal role in promoting green building practices. The U.S. Department of Energy’s Better Buildings Initiative, launched in 2011, supports over 900 partners committed to improving energy efficiency and adopting low-carbon materials in construction.

MARKET RESTRAINTS

High Initial Production Costs and Limited Economies of Scale

Despite growing environmental awareness, one of the primary restraints impeding the expansion of the North American green cement market is the relatively high initial production cost associated with green cement alternatives. Compared to conventional Portland cement, green cement often requires more expensive raw materials, advanced processing technologies, and specialised handling equipment, which collectively elevate manufacturing expenses. Furthermore, the lack of established supply chains and limited economies of scale prevent manufacturers from achieving cost parity with standard cement production. The IEA also noted that in North America, less than 12% of cement plants have integrated green cement production lines, largely due to the capital-intensive nature of retrofitting existing facilities. Additionally, the financial burden is passed on to end-users, including construction firms and developers, who remain hesitant to adopt green cement without clear economic incentives.

Technical Limitations and Lack of Industry-Wide Standards

A significant challenge restraining the North American green cement market is the presence of technical limitations and the absence of universally accepted industry standards for alternative cementitious materials. Unlike conventional Portland cement, which has well-established performance metrics and application guidelines, green cement variants—such as calcium aluminate cement, magnesium oxychloride cement, and alkali-activated materials—often face variability in mechanical properties, setting times, and durability under different environmental conditions. According to the American Society of Civil Engineers (ASCE), inconsistencies in curing requirements and strength development rates of green cement types pose difficulties for engineers and contractors unfamiliar with their behaviour. In a 2024 white paper, ASCE highlighted that certain green cement blends exhibit slower early-age strength gain, limiting their use in time-sensitive construction projects. Moreover, regional variations in performance due to differences in raw material composition complicate the process standardisation. This lack of harmonised standards also affects code approvals and acceptance by regulatory bodies. The National Ready Mixed Concrete Association (NRMCA) pointed out in 2023 that while ASTM C595 and C1157 standards govern blend cement, they do not comprehensively address newer green cement technologies. Consequently, many construction professionals remain cautious about specifying non-traditional cement products without explicit approval from building codes.

MARKET OPPORTUNITIES

Expansion of Carbon Capture, Utilisation, and Storage (CCUS) technologies

One of the most promising opportunities for the North American green cement market lies in the rapid advancement and deployment of carbon capture, utilisation, and storage (CCUS) technologies within the cement industry. CCUS enables cement manufacturers to significantly reduce their carbon footprint by capturing CO₂ emissions produced during clinker production and either storing them underground or converting them into usable products, such as synthetic aggregates or mineralised concrete additives. According to the Global CCS Institute, North America accounted for nearly 40% of global CCUS capacity in 2024, with over 20 commercial-scale projects either operational or under development. As per the International Energy Agency (IEA), integrating CCUS into cement production could reduce lifecycle emissions by up to 90%, making it a viable complement to green cement adoption. Also, the financial backing is expected to accelerate research into carbon-negative cement alternatives and hybrid systems combining CCUS with green cement technologies.

Growing Investment in Circular Economy Models and Industrial Symbiosis

The increasing adoption of circular economy principles and industrial symbiosis presents a substantial opportunity for the North American green cement market. By repurposing industrial by-products and waste materials into valuable cementitious resources, the industry can reduce reliance on virgin raw materials while simultaneously lowering environmental impact. These materials serve as effective supplementary cementitious materials (SCMs) that enhance the performance of green cement while diverting waste from landfills. Statistics from the U.S. Geological Survey (USGS) indicate that in 2023, over 18 million metric tons of coal fly ash were utilised in cement and concrete applications across the U.S., representing a recycling rate of nearly 40%. In Canada, initiatives like the Circular Economy Leadership Coalition have spurred collaboration between cement producers, steel mills, and power plants to optimise resource reuse.

MARKET CHALLENGES

Supply Chain Constraints for Alternative Raw Materials

A major challenge confronting the North American green cement market is the inconsistent availability and logistical complexity surrounding alternative raw materials required for green cement production. Unlike traditional cement, which relies on abundant and well-established sources of limestone and clay, green cement formulations depend heavily on industrial by-products such as fly ash, slag, calcined clay, and silica fume—materials whose supply is subject to fluctuations based on external industry cycles. According to the U.S. Geological Survey (USGS), domestic fly ash production in the U.S. declined by approximately 12% between 2020 and 2023, primarily due to the continued closure of coal-fired power plants. This decline has created supply shortages for cement manufacturers reliant on fly ash as a supplementary cementitious material (SCM). Moreover, transportation and logistics bottlenecks further exacerbate the issue. Many green cement raw materials must be sourced from specific regions, leading to increased lead times and costs.

Resistance to Change Among Traditional Construction Stakeholders

Resistance to change among traditional construction stakeholders represents a formidable challenge for the North American green cement market. Despite growing awareness of sustainability issues, many architects, engineers, contractors, and project owners remain reluctant to adopt green cement due to entrenched preferences for conventional materials, lack of familiarity with new technologies, and perceived risks related to performance and liability. According to a 2023 survey by the Construction Innovation Forum (CIF), only 22% of construction professionals in North America had experience specifying or using green cement in their projects. This hesitancy is compounded by the fact that many design professionals rely on decades of data and case studies built around Portland cement, creating a preference for proven methodologies over experimental ones. Furthermore, insurance and liability concerns play a role in slowing down market penetration. Insurers often require extensive documentation and third-party verification before approving the use of novel materials, adding layers of complexity and cost to project planning.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 8.45% |

| Segments Covered | By Product Type, Construction Sector, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Us, Canada, and the rest of North America |

| Market Leaders Profiled | LafargeHolcim, CEMEX, Calera Corporation, CarbonCure Technologies Inc., HeidelbergCement AG, Ecocem, Solidia Technologies, Kiran Global Chem Limited, Anhui Conch Cement Company, Taiheiyo Cement Corporation |

SEGMENTAL ANALYSIS

By Product Type Insights

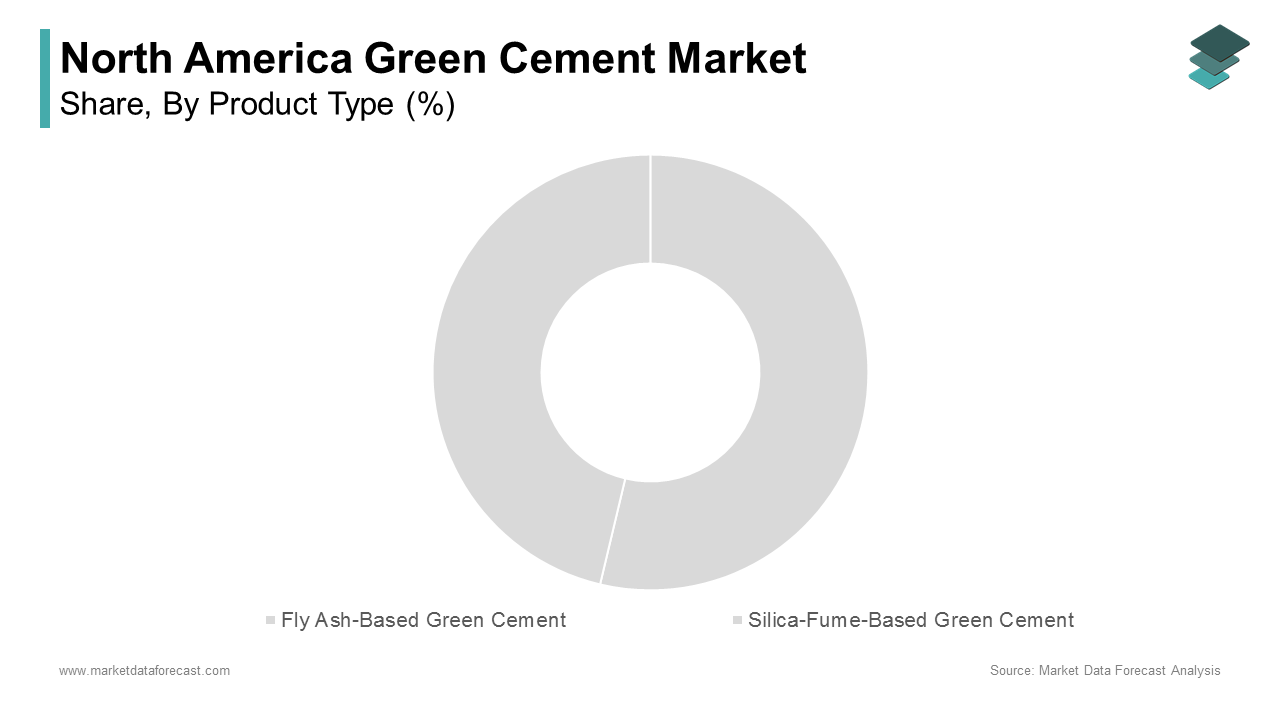

The Fly ash-based green cement held the largest share of the North American green cement market by accounting for 38.5% of total volume in 2024. This dominance is primarily attributed to the widespread availability of fly ash—a by-product of coal combustion—and its proven performance as a supplementary cementitious material (SCM) that significantly reduces the carbon footprint of concrete. The American Coal Ash Association (ACAA) reported that despite a decline in coal-fired power generation, nearly 50% of collected fly ash was still being repurposed for cement and concrete production in 2024, driven by regulatory support and industry incentives.

Silica-fume-based green cement is projected to be the fastest-growing segment in the North America green cement market, registering a CAGR of 9.7%. This rapid growth is primarily driven by its superior mechanical properties, including high compressive strength, reduced permeability, and enhanced resistance to chemical attack—making it particularly suitable for high-performance concrete applications. The growing demand for silica fume is closely tied to infrastructure modernisation efforts, especially in sectors such as bridges, tunnels, and marine structures, where durability is critical.

By Construction Sector Insights

The non-residential construction sector accounted for the largest share of the North American green cement market, representing 62% of total consumption in 2024. This dominance is due to the increasing implementation of sustainability mandates in commercial, institutional, and industrial building projects, which are more likely to adopt green cement to meet environmental regulations and certification requirements. According to the U.S. Census Bureau, nonresidential construction spending in the United States reached $1.2 trillion in 2023, marking a 7.5% increase from the previous year. Additionally, federal initiatives like the U.S. General Services Administration’s (GSA) Net-Zero Standard have mandated the incorporation of low-carbon materials in all new government-funded buildings, reinforcing the sustained demand for green cement in the non-residential segment.

The residential construction sector is emerging as the fastest-growing segment within the North American green cement market, projected to expand at a CAGR of 8.9%. This accelerated growth is fueled by rising consumer awareness regarding eco-friendly housing solutions and expanding incentives for energy-efficient homes. Similarly, Canada’s Greener Homes Initiative offers grants of up to CAD 5,000 for homeowners undertaking energy-efficient renovations, many of which involve the use of sustainable building materials.

REGIONAL ANALYSIS

The United States had the dominant position in the North American green cement market, capturing an estimated 68% of the regional market share in 2024. This is underpinned by aggressive climate policies, a mature construction industry, and extensive investments in alternative material technologies. In response, major players such as Lehigh Hanson and Cemex have ramped up the production of blended cement incorporating fly ash, slag, and calcined clay. The U.S. Green Building Council (USGBC) reported that in 2024, over 110,000 LEED-certified buildings existed in the country, driving procurement preferences for environmentally responsible construction materials.

Positioning reflects the country’s proactive approach to decarbonising the construction industry, supported by federal and provincial climate action plans. Additionally, companies like Carbicrete and Carbicrete X have pioneered carbon-negative cement technologies, gaining traction in both public and private infrastructure projects. With supportive regulatory frameworks and increasing R&D activity, Canada is solidifying its role as a key player in the North American green cement landscape.

The remaining North American countries, including Mexico and select Caribbean nations, collectively hold a key share of the regional green cement market in 2024. Though smaller in scale, these markets are gradually gaining traction due to cross-border collaborations, foreign direct investment, and evolving environmental regulations. CEMEX, headquartered in Mexico, has been actively promoting its Vertua line of low-carbon cement products, with pilot installations reported in border regions serving U.S. clients. In addition, the U.S. International Development Finance Corporation (DFC) has funded several sustainable infrastructure initiatives in Central America and the Caribbean, indirectly influencing the flow of green building materials into the region.

LEADING PLAYERS IN THE NORTH AMERICA GREEN CEMENT MARKET

Cemex S.A.B. de C.V.

Cemex, a global leader in building materials with a strong presence in North America, has been at the forefront of green cement innovation. The company has developed its Vertua line of low-carbon and carbon-neutral concrete solutions, emphasising circularity and alternative binders. In North America, Cemex collaborates with startups and research institutions to enhance sustainable construction practices. Its commitment to decarbonization aligns with regional regulatory trends and client demand for greener infrastructure, making it a key player in advancing green cement adoption across the continent.

Holcim Ltd. (now known as LafargeHolcim)

LafargeHolcim plays a pivotal role in the North American green cement landscape through its ECOPact line of green concrete products. Designed to reduce embodied carbon by up to 40%, these products are being increasingly integrated into major infrastructure and commercial developments across the U.S. and Canada. The company’s emphasis on sustainable sourcing, carbon capture technologies, and partnerships with green building councils positions it as a major contributor to the transition toward low-carbon construction in the region.

Heidelberg Materials North America

Heidelberg Materials is actively transforming its North American operations by investing in green cement technologies and carbon capture projects. The company’s subsidiary in Canada launched one of the first full-scale carbon capture facilities at a cement plant in Edmonton, setting a precedent for the industry. Its focus on developing alternative cement using calcined clays and industrial by-products supports the broader market shift toward sustainability. With strategic investments and a forward-looking approach, Heidelberg Materials is shaping the future of green cement in North America.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

One major strategy employed by leading players in the North American green cement market is product innovation and the development of low-carbon alternatives. Companies are investing heavily in R&D to create novel formulations that reduce reliance on traditional Portland cement while maintaining structural integrity and performance standards. These innovations often incorporate industrial by-products or carbon-negative materials.

Another critical approach is strategic partnerships and collaborations with academic institutions, startups, and government bodies. By working with external entities, companies can accelerate the development and commercialisation of green cement technologies, gain access to funding, and align with evolving sustainability regulations and standards in the construction sector.

Lastly, the expansion of production capabilities and integration of green technologies within existing manufacturing facilities is gaining traction. Major players are retrofitting plants to accommodate alternative fuels, carbon capture systems, and blended cement production lines to meet rising demand for environmentally responsible building materials.

KEY MARKET PLAYERS AND COMPETITION OVERVIEW

Major Players in the North American green cement market include LafargeHolcim, CEMEX, Calera Corporation, CarbonCure Technologies Inc., HeidelbergCement AG, Ecocem, Solidia Technologies, Kiran Global Chem Limited, Anhui Conch Cement Company, and Taiheiyo Cement Corporation.

The competitive landscape of the North American green cement market is characterised by a mix of established multinational cement producers and emerging innovators focused on sustainability-driven solutions. Traditional industry leaders are leveraging their extensive distribution networks and financial resources to develop and scale green cement offerings, often integrating them into mainstream product portfolios. At the same time, niche players and startups are introducing disruptive technologies such as carbon-negative binders and alkali-activated materials, challenging conventional production models. The market is witnessing increased collaboration between manufacturers, academia, and regulatory bodies to drive standardisation and acceptance of alternative cementitious materials. As environmental policies tighten and demand for sustainable infrastructure grows, competition is intensifying not only on product performance but also on cost-efficiency, scalability, and supply chain resilience. This evolving dynamic is reshaping the industry, pushing all stakeholders to innovate rapidly and differentiate themselves in a rapidly maturing market.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Cemex announced the expansion of its Vertua green concrete production capacity across multiple U.S. facilities, reinforcing its commitment to offering carbon-neutral construction solutions tailored for urban infrastructure projects.

- In June 2024, Heidelberg Materials initiated a pilot project in Ontario to test the viability of calcined clay-based cement blends, aiming to reduce clinker content and support the company’s broader decarbonization roadmap in North America.

- In September 2024, Holcim partnered with a leading North American university to establish a dedicated research centre focused on enhancing the durability and performance of green cement under varying climatic conditions.

- In November 2024, Lehigh Hanson introduced a new line of blended cement incorporating recycled industrial by-products, targeting large-scale commercial developers seeking LEED-certified construction materials.

- In March 2025, startup Carbicrete signed a strategic agreement with a major U.S. construction firm to integrate its carbon-negative cement into upcoming residential and mixed-use developments, marking a significant step toward mainstream adoption.

MARKET SEGMENTATION

This research report on the North America Green Cement Market has been segmented and sub-segmented based on product type, construction sector, and region.

By Product Type

- Fly Ash-Based Green Cement

- Silica-Fume-Based Green Cement

By Construction Sector

- Non-Residential Construction

- Residential Construction

By Region

- Us

- Canada

- Rest of North America

Frequently Asked Questions

1. What factors are driving the green cement market in North America?

Key drivers include government regulations on emissions, increasing adoption of sustainable construction practices, urbanization, and corporate sustainability initiatives.

2. Which are the leading countries in the North America green cement market?

The United States and Canada lead the market due to strong environmental policies, construction activities, and investment in green technologies.

3. Who are the major players in the North America green cement market?

Key players include LafargeHolcim, CEMEX, Calera Corporation, CarbonCure Technologies Inc., and HeidelbergCement AG.

4. How does green cement contribute to environmental sustainability?

Green cement reduces greenhouse gas emissions, utilizes waste materials like fly ash or slag, and decreases reliance on non-renewable resources.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com