North America HEOR Services Market Size, Share, Trends & Growth Forecast Report By Service (Economic Modeling/Evaluation, Real-world Data Analysis & Information Systems, Clinical Outcome, Market Access Solutions & Reimbursement), Service Provider, And Country (US, Canada, And Rest Of North America), Industry Analysis From 2025 To 2033

North America HEOR Services Market Size

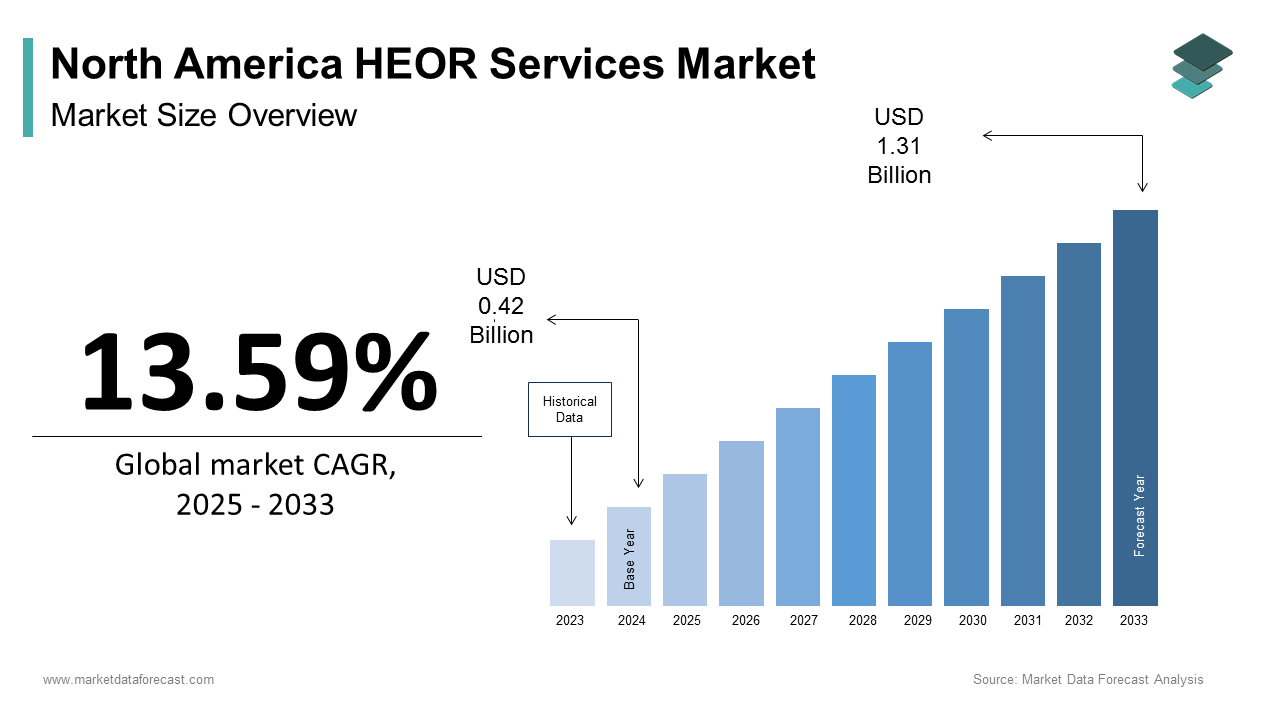

The North America HEOR Services Market Size was calculated to be USD 0.42 billion in 2024 and is anticipated to be worth USD 1.31 billion by 2033, from USD 0.47 billion in 2025, growing at a CAGR of 13.59% during the forecast period.

The HEOR (Health Economics and Outcomes Research) services are specialized segment within the broader healthcare analytics industry that focuses on generating evidence to support decision-making in drug development, reimbursement strategies, and patient care optimization. HEOR integrates epidemiology, biostatistics, economics, and clinical research to assess the real-world effectiveness, safety, cost, and value of therapeutic interventions. In recent years, the demand for robust health economic data has surged due to rising pharmaceutical R&D costs, increasing regulatory scrutiny, and payer pressure for proof of treatment value before coverage decisions.

MARKET DRIVERS

Increasing Demand for Real-World Evidence in Regulatory and Reimbursement Decisions

The escalating reliance on real-world evidence (RWE) in regulatory and reimbursement processes is accelerating the growth of the North America HEOR services market. Regulatory agencies such as the U.S. Food and Drug Administration (FDA) have increasingly incorporated RWE into their decision-making frameworks to complement traditional randomized controlled trial (RCT) data. In 2022, the FDA released updated guidance encouraging the use of real-world data (RWD) sources, including electronic health records (EHRs), claims databases, and patient registries, to evaluate drug performance in diverse populations and long-term outcomes. As per the Duke-Margolis Center for Health Policy, more than 60% of novel therapeutics approved between 2018 and 2021 included some form of RWE in their submission packages. Additionally, payers and health technology assessment (HTA) bodies are leveraging HEOR-generated evidence to make informed coverage decisions. For example, ICER (Institute for Clinical and Economic Review) assessments, which often rely heavily on HEOR methodologies, influence reimbursement policies for approximately 75% of U.S. commercial payers, according to a 2023 analysis by the National Pharmaceutical Council.

Rising Prevalence of Chronic Diseases and Personalized Medicine Adoption

The growing burden of chronic diseases coupled with the rapid advancement of personalized medicine is escalating the growth of the North America HEOR services market. Chronic conditions such as diabetes, cardiovascular diseases, and cancer account for a substantial portion of healthcare expenditures. As per the Centers for Disease Control and Prevention (CDC), about 60% of adults in the United States live with at least one chronic disease, contributing to over $4.1 trillion in annual healthcare costs. Managing these conditions effectively requires not only medical intervention but also robust economic evaluations to justify treatment affordability and long-term benefits.

Simultaneously, the rise of personalized medicine tailoring treatments based on individual genetic profiles is reshaping therapeutic approaches. The Personalized Medicine Coalition reported that in 2023, over 40 new personalized therapies were in late-stage development or recently approved, many requiring companion diagnostics. However, these innovations come with high price tags, prompting payers and policymakers to demand rigorous HEOR analyses to assess their value proposition. For instance, CAR-T cell therapies, which can exceed $1 million per treatment, necessitate extensive cost-effectiveness modeling and budget impact analyses.

MARKET RESTRAINTS

Data Privacy Concerns and Regulatory Complexity in Handling Real-World Data

The growing complexity surrounding data privacy regulations and compliance when handling real-world data (RWD) is restraining the growth of the North America HEOR services market. The Health Insurance Portability and Accountability Act (HIPAA) in the United States mandates strict safeguards for protected health information (PHI), while state-level laws such as California’s Consumer Privacy Act (CCPA) impose additional restrictions on data usage and sharing. According to a 2023 report from Deloitte, nearly 55% of healthcare organizations face delays in conducting HEOR studies due to legal and compliance hurdles related to data access and de-identification. Moreover, cross-institutional collaborations essential for comprehensive RWD collection often require navigating multiple institutional review boards (IRBs) and data governance frameworks, further slowing down research timelines.

High Costs and Resource Intensity of Conducting Advanced HEOR Studies

The financial and operational demands associated with conducting advanced HEOR studies hampering the growth of the North America HEOPR services market. HEOR encompasses complex methodologies such as cost-effectiveness modeling, budget impact analysis, and patient-reported outcome (PRO) assessments, all of which require significant investments in skilled personnel, data infrastructure, and computational tools. According to the Tufts Center for the Study of Drug Development, the average cost of developing a single pharmacoeconomic model ranges between $250,000 and $500,000, excluding ongoing updates and validation efforts.

Moreover, the integration of artificial intelligence (AI) and machine learning (ML) into HEOR workflows aimed at improving predictive accuracy and real-time decision support rhas introduced additional capital expenditures. Small and mid-sized biotech firms often struggle to allocate sufficient resources, limiting their ability to conduct robust HEOR analyses independently. The high entry barriers and resource intensity associated with HEOR services create a bottleneck for emerging players seeking to validate novel therapies in competitive markets.

MARKET OPPORTUNITIES

Expansion of Value-Based Healthcare Models Driving Demand for Cost-Effectiveness Analysis

The widespread shift toward value-based healthcare (VBHC) models, which emphasize delivering measurable health outcomes relative to cost shall pose new opportunities for the growth of the North America HEOR services market. Traditional fee-for-service reimbursement structures are being replaced by alternative payment models (APMs) that tie provider compensation to patient outcomes rather than volume of services rendered. This transformation has intensified the need for cost-effectiveness analyses (CEAs) and budget impact models (BIMs), both core components of HEOR. Payers and providers increasingly rely on these analyses to determine whether a therapy delivers sufficient clinical benefit to justify its cost. According to a 2023 report by the National Academy for State Health Policy (NASHP), 42 U.S. states have implemented or are piloting value-based payment arrangements, many of which mandate HEOR-based evidence for contract negotiations. Additionally, organizations like the Institute for Clinical and Economic Review (ICER) continue to shape pricing discussions by publishing comparative effectiveness reports used by payers representing over 200 million Americans.

Integration of AI and Machine Learning in HEOR Analytics Enhancing Predictive Capabilities

The integration of artificial intelligence (AI) and machine learning (ML) into HEOR analytics is another opportunity for the North America HEOR services market growth. These technologies enable faster, more accurate processing of large and heterogeneous datasets including electronic health records (EHRs), claims data, and genomic information to uncover patterns and predict outcomes with greater precision than traditional statistical methods. According to a 2023 white paper by the MIT Sloan School of Management, AI-enhanced HEOR models demonstrated a 30% improvement in forecasting medication adherence and treatment discontinuation compared to conventional regression techniques.

Pharmaceutical companies and payers are increasingly adopting AI-powered HEOR tools to streamline evidence generation and support dynamic pricing strategies. For instance, Flatiron Health and Aetion have developed ML-based real-world evidence platforms that assist in generating regulatory-grade HEOR insights. A case study published in JAMA Network Open showed that AI-driven survival extrapolation models reduced time-to-insight by up to 40% in oncology HEOR studies. Additionally, the FDA’s Digital Health Pre-Cert Program is facilitating the incorporation of AI-based tools into regulatory submissions, further legitimizing their role in HEOR.

MARKET CHALLENGES

Heterogeneity in Data Sources and Interoperability Issues Across Healthcare Systems

The heterogeneity of real-world data (RWD) sources and persistent interoperability issues across healthcare systems is hampering the growth of the . HEOR relies on integrating data from disparate sources such as electronic health records (EHRs), insurance claims, pharmacy dispensing logs, and patient-reported outcomes (PROs). However, inconsistencies in data structure, coding standards, and terminology across institutions limit the reliability and comparability of findings. According to a 2023 report by the Office of the National Coordinator for Health Information Technology (ONC), fewer than 30% of U.S. hospitals had fully interoperable EHR systems capable of seamless data exchange with external providers. Furthermore, the lack of standardized data formats hampers the reproducibility of HEOR models. A study published in Medical Care revealed that variations in diagnosis codes across payer databases led to a 15–20% discrepancy in prevalence estimates for chronic diseases like diabetes and hypertension. Such inconsistencies introduce bias and reduce confidence in HEOR-derived conclusions, especially when used for regulatory or reimbursement purposes.

Shortage of Skilled Professionals and Methodological Standardization Gaps

The shortage of trained professionals and the lack of universally accepted methodological standards are to hamper the growth of the North America HEOR services market. Conducting high-quality HEOR studies requires expertise in epidemiology, biostatistics, health economics, and modeling techniques skills that remain in limited supply despite growing demand. Additionally, methodological inconsistencies across HEOR studies contribute to variability in results and interpretation. While organizations like ISPOR and the International Society for Quality of Life Research (ISOQOL) provide best practice guidelines, there remains a lack of enforceable global standards for model design, discounting rates, and utility measurement. A 2023 meta-analysis published in Value in Health found that cost-effectiveness ratios for similar oncology therapies varied by as much as 40% depending on the analytical approach used. These discrepancies undermine stakeholder confidence and complicate decision-making for payers and regulators.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 13.59% |

| Segments Covered | By Service, Service Provider, And Region |

| Various Analyses Covered | Global, Regional & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

| Regions Covered | Us, Canada, and the Rest of North America |

| Market Leaders Profiled | IQVIA, Syneos Health, ICON plc, Parexel International, Optum, McKesson Corporation, Pharmaceutical Product Development (PPD), Covance Inc., Evidera, RTI Health Solutions |

SEGMENTAL ANALYSIS

By Service Insights

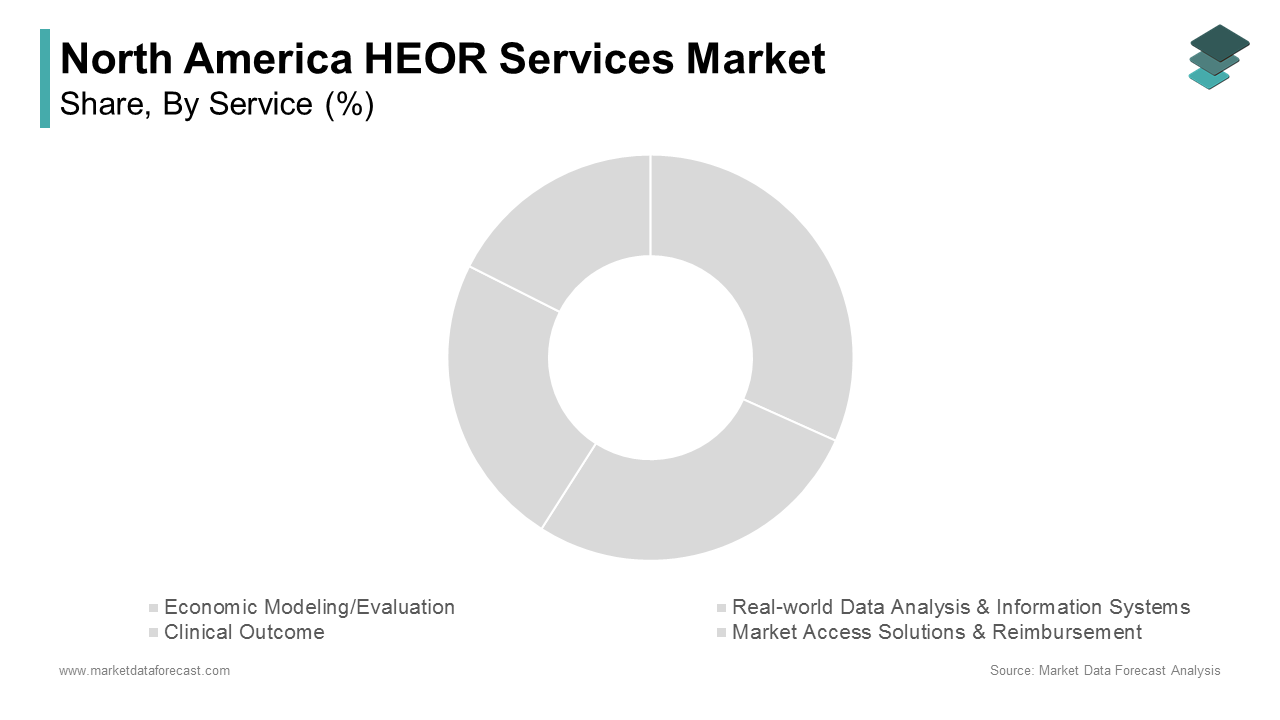

The Real-World Data Analysis & Information Systems segment was the largest and held 38.4% of the North America HEOR services market share in 2024 with the increasing reliance on real-world evidence (RWE) to support regulatory submissions, reimbursement decisions, and post-market surveillance strategies. As per the U.S. Food and Drug Administration (FDA), over 45% of novel drug approvals between 2019 and 2023 incorporated real-world data (RWD) as part of their evaluation process with the growing importance of this service category. Moreover, the expansion of electronic health record (EHR) adoption across healthcare institutions has significantly enhanced access to longitudinal patient data. According to the Office of the National Coordinator for Health Information Technology (ONC), over 96% of U.S. hospitals were using certified EHR technology by the end of 2022. This surge in digitized clinical data has fueled demand for advanced analytics platforms capable of extracting meaningful insights from heterogeneous datasets.

The clinical outcome assessments segment is projected to register a CAGR of 11.7% in the next coming years due to the increasing emphasis on patient-reported outcomes (PROs) and quality-of-life metrics in regulatory and payer decision-making processes. The U.S. Food and Drug Administration’s 2023 guidance update on PRO measures reinforced their role in evaluating treatment effectiveness, particularly in oncology and rare disease indications where traditional endpoints may be insufficient.

Additionally, payers and health technology assessment (HTA) bodies are increasingly demanding robust clinical outcome data to assess the comparative value of high-cost therapies. A 2023 report by the Institute for Clinical and Economic Review (ICER) indicated that more than 60% of its recent drug evaluations included PRO-based analyses to inform coverage determinations.

By Service Provider Insights

The consultancy firms segment held a prominent share of the North America HEOR services market in 2024 with the increasing complexity of health technology assessments (HTAs) and the demand for tailored evidence generation strategies. According to the International Society for Pharmacoeconomics and Outcomes Research (ISPOR), over 70% of biopharma firms outsourced at least one HEOR function to consultancies in 2023 to navigate evolving payer requirements. Additionally, the implementation of value-based contracting models has heightened the need for expert consultation in designing cost-effectiveness frameworks.

The CROs (Contract Research Organizations) segment is anticipated to grow with a CAGR of 12.4% during the forecast period owing to the rising outsourcing of HEOR-related clinical and post-marketing studies by pharmaceutical and biotech firms seeking cost-effective and efficient execution capabilities. CROs like Parexel, PPD, and ICON offer integrated HEOR services that align seamlessly with clinical trial workflows, thereby reducing time-to-market for new therapies. According to a 2023 analysis by EvaluatePharma, nearly 40% of Phase III clinical trials initiated in the U.S. now include embedded health economics and outcomes research components. Additionally, CROs are investing heavily in real-world evidence (RWE) platforms and digital health technologies to enhance data collection efficiency. Global RWE investments by CROs surpassed $2.5 billion in 2023, with North America accounting for over 55% of that spending.

REGIONAL ANALYSIS

United States HEOR Services Market

United States led the North America HEOR services market with 83.2% of the share in 2024. As the world’s largest pharmaceutical market, the U.S. spends over $600 billion annually on prescription drugs , according to IQVIA, necessitating robust HEOR frameworks to justify pricing and ensure reimbursement. The presence of well-established regulatory bodies like the FDA and influential HTA organizations such as ICER has further institutionalized the use of HEOR evidence in decision-making.

Canada HEOR Services Market

Canada North America HEOR services market was accounted in holding 12.35 of share in 2024. Canada plays a crucial role in generating health economic evidence due to its centralized healthcare system and strong emphasis on cost-effectiveness reviews through agencies like the Canadian Agency for Drugs and Technologies in Health (CADTH). The latter evaluates over 100 new drug submissions annually, mandating rigorous pharmacoeconomic analyses as part of reimbursement decisions.

In recent years, Canada has emerged as a preferred location for HEOR pilot studies and real-world evidence (RWE) generation, supported by its universal healthcare infrastructure and richly linked administrative databases. Canada, over 90% of physician visits are documented in provincial electronic medical records (EMRs), providing a comprehensive source of longitudinal patient data. Moreover, the Pan-Canadian Oncology Drug Review (pCODR) program has intensified the demand for outcomes-based evidence to guide cancer therapy funding decisions.

LEADING PLAYERS IN THE NORTH AMERICA HEOR SERVICES MARKET

IQVIA stands as a dominant force in the North America HEOR services market, offering end-to-end solutions that span real-world evidence generation, health economic modeling, and outcomes research. The company plays a pivotal role in supporting pharmaceutical and biotech firms with regulatory submissions, payer dossiers, and market access strategies. IQVIA’s deep integration of data analytics, AI-driven insights, and therapeutic expertise enables clients to demonstrate value across complex healthcare landscapes.

Parexel is another leading player contributing significantly to the global and regional HEOR ecosystem. With a strong focus on patient-centered outcomes and evidence-based decision-making, Parexel delivers tailored HEOR services that align with evolving regulatory expectations and reimbursement frameworks. Its strategic collaborations with payers, providers, and life sciences companies have enhanced its ability to generate actionable insights that influence market access and drug commercialization pathways.

Wolters Kluwer Health distinguishes itself through its integrated clinical and economic decision support tools, particularly in real-world data analysis and outcomes modeling. The company supports healthcare stakeholders by providing robust evidence solutions that inform policy, treatment guidelines, and value-based care models. Its emphasis on digital platforms and predictive analytics has made it a trusted partner for HEOR initiatives aimed at improving patient outcomes while managing healthcare costs effectively.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

The strategic partnerships and collaborations is one of the important strategies by the key participants. Companies are increasingly forming alliances with academic institutions, healthcare providers, and technology firms to enhance their data access and analytical capabilities. These collaborations allow for more comprehensive real-world evidence generation and improve the credibility and relevance of HEOR outputs.

Another key approach is investment in digital transformation and advanced analytics . Leading firms are integrating artificial intelligence, machine learning, and cloud-based platforms into their HEOR workflows to streamline data processing, improve model accuracy, and deliver faster insights. This technological advancement strengthens their competitive edge and responsiveness to client needs.

The expansion of service portfolios to include value-based care consulting has become a priority. As healthcare systems shift toward outcome-based reimbursement models, HEOR service providers are offering specialized advisory services to help pharmaceutical companies align their products with evolving payment structures and demonstrate long-term value to payers and providers.

KEY MARKET PLAYERS AND COMPETITIVE OVERVIEW

Major Players of the North America HEOR services market include IQVIA, Syneos Health, ICON plc, Parexel International, Optum, McKesson Corporation, Pharmaceutical Product Development (PPD), Covance Inc., Evidera, RTI Health Solutions

The competition in the North America HEOR services market is marked by a convergence of established consultancies, contract research organizations (CROs), and emerging tech-driven analytics firms. Market participants are continuously adapting to shifting healthcare dynamics, including increased demand for real-world evidence, stricter regulatory expectations, and the need for cost-effective therapeutic interventions. In this environment, differentiation is achieved through methodological rigor, proprietary data assets, and domain-specific expertise across therapeutic areas. Strategic positioning often involves expanding service offerings beyond traditional HEOR functions into broader health economics, patient-reported outcomes, and digital biomarker integration.

RECENT HAPPENINGS IN THE MARKET

- In January 2024, IQVIA launched a new AI-powered real-world evidence platform designed to accelerate health economic and outcomes research processes. The platform integrates diverse data sources and enhances predictive modeling capabilities by allowing for faster and more accurate evidence generation to support regulatory and reimbursement decisions.

- In March 2024, Parexel announced a strategic partnership with a leading U.S.-based academic medical center to co-develop patient-reported outcome tools tailored for rare disease therapies. This initiative aims to strengthen HEOR capabilities in high-impact therapeutic areas where patient-centric evidence is important for market access success.

- In June 2024, Wolters Kluwer Health expanded its HEOR division by introducing a suite of digital dashboards that provide real-time insights into treatment effectiveness and cost implications across multiple disease states. This enhancement supports payers and providers in making informed decisions aligned with value-based care objectives.

- In September 2024, Optum, a UnitedHealth Group subsidiary, acquired a boutique HEOR consultancy specializing in oncology outcomes research. This move was intended to bolster Optum’s capabilities in generating evidence for high-cost specialty therapies and support personalized medicine adoption.

- In November 2024, ICON plc integrated blockchain technology into its HEOR data management framework to enhance transparency and traceability in real-world data studies. This innovation addresses growing concerns around data integrity and audit readiness in regulatory submissions and payer negotiations.

MARKET SEGMENTATION

This research report on the North America HEOR Services Market has been segmented and sub-segmented based on service, service provider, and region.

By Service

- Economic Modeling/Evaluation

- Real-world Data Analysis & Information Systems

- Clinical Outcome

- Market Access Solutions & Reimbursement

By Service Provider

- Consultancy

- CROs

By Region

- US

- Canada

- Rest Of North America

Frequently Asked Questions

1. What factors are driving the growth of the HEOR services market in North America?

Key drivers include rising healthcare costs, demand for cost-effective treatments, increasing R&D in pharmaceuticals, and the need for real-world evidence to support market access.

2. Which industries commonly use HEOR services?

Pharmaceutical companies, biotechnology firms, medical device manufacturers, healthcare providers, and payers frequently use HEOR services.

3. What are the main service segments in the HEOR market?

Core services include market access strategy, pharmacoeconomic modeling, real-world evidence (RWE), patient-reported outcomes research, value dossiers, and literature reviews.

4. What role does real-world evidence (RWE) play in HEOR?

RWE provides data on how treatments perform outside of clinical trials, helping healthcare stakeholders make informed decisions about effectiveness and costs.

5. Who are the key players in the North America HEOR services market?

IQVIA, Syneos Health, ICON plc, Parexel International, Optum, McKesson Corporation, PPD, Covance Inc., Evidera, and RTI Health Solutions.

6. What challenges are faced by the HEOR services market?

Challenges include data privacy regulations, the complexity of integrating diverse data sources, high service costs, and regulatory hurdles.

7. How does HEOR contribute to drug pricing and reimbursement?

HEOR analyses provide evidence of value, helping manufacturers negotiate pricing and secure reimbursement from insurers and healthcare payers.

8. What is the impact of digital health trends on the HEOR market?

Digital health tools are generating more real-world data, expanding opportunities for HEOR services in patient outcome tracking and cost-effectiveness analysis.

9. How is AI and big data analytics influencing the HEOR market?

AI and advanced analytics help process large healthcare datasets faster, improving predictive modeling, cost assessments, and outcome evaluations.

10. What future opportunities exist in the HEOR services market?

Opportunities include expansion into personalized medicine evaluations, telehealth outcome studies, value-based care analysis, and the integration of patient-centric data.

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com