North America High Purity Alumina Market Research Report – Segmented By Product ( 5N Grade, 6N Grade ) Application and Country (The U.S., Canada and Rest of North America) - Industry Analysis, Size, Share, Growth, Trends, & Forecasts 2025 to 2033.

North America High Purity Alumina Market Size

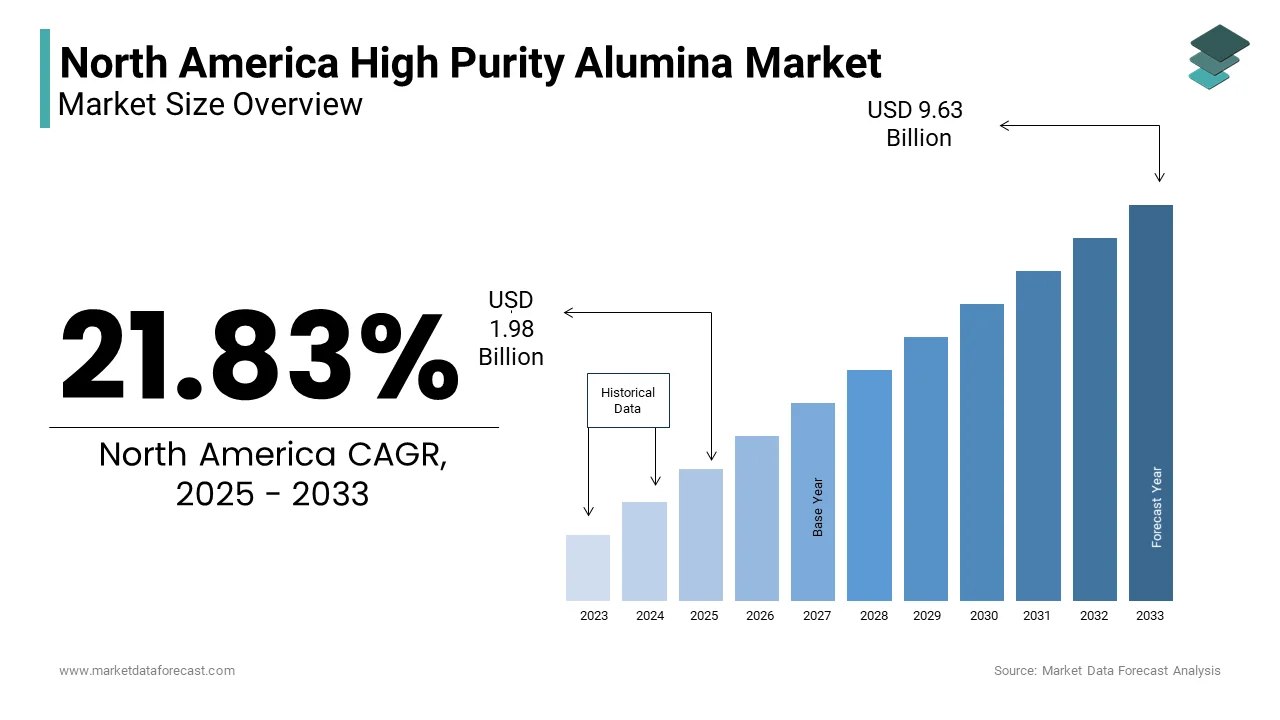

The North America High Purity Alumina Market Size was valued at USD 1.63 billion in 2024. The North America High Purity Alumina Market size is expected to have 21.83 % CAGR from 2025 to 2033 and be worth USD 9.63 billion by 2033 from USD 1.98 billion in 2025.

MARKET DRIVERS

Rising Demand in the Semiconductor Industry

A significant driver propelling the North America high purity alumina market is its critical role in the semiconductor industry, particularly in the production of sapphire wafers and CMP slurries. High purity alumina’s exceptional thermal stability and electrical insulation properties make it indispensable for fabricating advanced chips used in smartphones, automotive electronics, and data centers. Regulatory bodies like the U.S. Department of Commerce emphasize the importance of domestic semiconductor manufacturing, further amplifying demand for high-grade HPA. Like, semiconductor exports from the U.S. surged greately in recent years, showing the region’s dominance in chip fabrication. Moreover, the ongoing emphasis on miniaturization and 5G technology has spurred demand for ultra-high-purity alumina, which ensures consistent performance in extreme conditions.

Growing Adoption in Lithium-Ion Batteries

Another pivotal driver is the increasing adoption of high purity alumina in lithium-ion batteries, fueled by the accelerating transition to electric vehicles (EVs) and renewable energy storage solutions. High purity alumina serves as a key material in battery separators, offering superior thermal stability and preventing internal short circuits, which enhances safety and longevity. Similarly, incorporating HPA into battery designs improves cycle life considerably, driving manufacturers to prioritize its integration. Additionally, government incentives promoting clean energy initiatives have prompted innovations in HPA formulations tailored for EV applications. For example, Tesla reported a considerable increase in battery efficiency after adopting HPA-enhanced separators in its latest models, attributing this improvement to enhanced ion conductivity. Furthermore, partnerships between battery manufacturers and raw material suppliers ensure seamless integration of advanced formulations, enhancing product performance while addressing pressing environmental concerns.

MARKET RESTRAINTS

High Production Costs and Limited Supply

A significant restraint hindering broader adoption of high purity alumina in North America is the high production costs associated with achieving ultra-high purity levels. Like, the extraction and refining processes required to produce HPA are energy-intensive and technologically complex, resulting in prices that can be up to five times higher than standard alumina. This cost barrier disproportionately affects small- and medium-sized enterprises, limiting their ability to invest in advanced materials. Additionally, the limited availability of raw materials, such as bauxite and aluminum chloride, further exacerbates supply chain vulnerabilities. Industry experts estimate that production delays caused by raw material shortages result in significant annual losses, deterring potential buyers who perceive HPA as a non-essential luxury item rather than a practical investment.

Stringent Environmental Regulations

Another restraint stems from stringent environmental regulations governing the mining and processing of raw materials used in high purity alumina production. According to the Environmental Protection Agency (EPA), the extraction of bauxite and other precursors contributes significantly to greenhouse gas emissions and soil degradation, prompting regulatory bodies to impose stricter guidelines on waste management and energy consumption. Compliance with these regulations imposes financial burdens on manufacturers, who must invest in advanced filtration systems or adopt cleaner production methods to mitigate ecological impact. Also, QAC residues were detected in a noticeable portion of freshwater samples collected near industrial zones, raising concerns about long-term environmental sustainability. Such measures increase operational costs greatly deterring small- and medium-sized enterprises from adopting cost-effective solutions. Furthermore, public scrutiny of environmentally harmful practices undermines brand credibility and consumer trust, compelling companies to allocate resources toward sustainable alternatives.

MARKET OPPORTUNITIES

Expansion in LED Manufacturing

A promising opportunity for the North America high purity alumina market lies in its expanding applications within the LED manufacturing sector, where HPA serves as a critical substrate material for producing sapphire wafers. High purity alumina’s exceptional optical clarity and thermal conductivity make it indispensable for fabricating high-brightness LEDs used in automotive lighting, smartphones, and commercial displays. Similar, implementing HPA-based substrates reduced defect rates in LED production lines, showing its economic value. Furthermore, partnerships between LED manufacturers and chemical suppliers facilitate bulk procurement, ensuring timely deployment of cutting-edge technologies. With analysts predicting a notable YoY increase in LED production in the coming years, the demand for specialized substrates is poised to escalate significantly.

Surge in Aerospace Applications

Another lucrative avenue is the integration of high purity alumina into aerospace applications, driven by its versatility and compatibility with extreme environments. Industries such as aircraft manufacturing extensively utilize HPA for its abrasion resistance and dielectric properties, making it ideal for components like turbine blades, insulators, and thermal protection systems. For instance, Boeing leverages HPA-based coatings to enhance fuel efficiency and reduce maintenance costs, extending aircraft durability. Similarly, advancements in additive manufacturing techniques incorporating HPA demonstrate a reduction in weight while maintaining structural integrity, enhancing operational efficiency. These innovations not only differentiate brands in a crowded marketplace but also cater to evolving industrial preferences prioritizing automation and ease of use.

MARKET CHALLENGES

Intense Competition from Alternatives

The North America high purity alumina market faces significant challenges stemming from intense competition posed by alternative materials vying for dominance in advanced applications. This saturation complicates efforts to differentiate HPA based solely on functionality, pushing companies to invest heavily in marketing and R&D initiatives. However, aggressive pricing strategies adopted by competitors frequently erode profit margins, particularly for mid-tier manufacturers struggling to match promotional budgets. Furthermore, the rise of natural and synthetic alternatives, such as silicon carbide and gallium nitride, poses additional threats, undermining HPA’s market share. Such trends distort market dynamics, forcing legitimate businesses to allocate resources toward anti-counterfeiting measures.

Supply Chain Disruptions

Another formidable challenge is the persistent disruption in supply chains, exacerbated by geopolitical tensions and logistical bottlenecks, which impede optimal availability of high purity alumina. Similarly, a large portion of chemical producers cited delays in raw material procurement as a barrier to meeting production targets, limiting access to cutting-edge solutions. This disconnect not only diminishes customer satisfaction but also tarnishes brand reputation when tools fail to deliver expected results. Additionally, training programs offered by manufacturers often lack accessibility, especially in remote regions, leaving many users ill-equipped to leverage sophisticated features. While industry leaders advocate for hands-on workshops and virtual demonstrations, scaling these initiatives poses logistical challenges. Resolving this skills deficit is imperative to ensure seamless adoption and maximize market potential.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2024 to 2033 |

| Base Year | 2024 |

| Forecast Period | 2025 to 2033 |

| CAGR | 21.83 % |

| Segments Covered | By Product, Application and Country. |

| Various Analyses Covered | Global, Regional & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada and Rest of North America |

| Market Leader Profiled | Alcoa Inc, Sumitomo Chemical Co. Ltd, Nippon Light Metal Holdings Co. Ltd |

SEGMENTAL ANALYSIS

By Product Insights

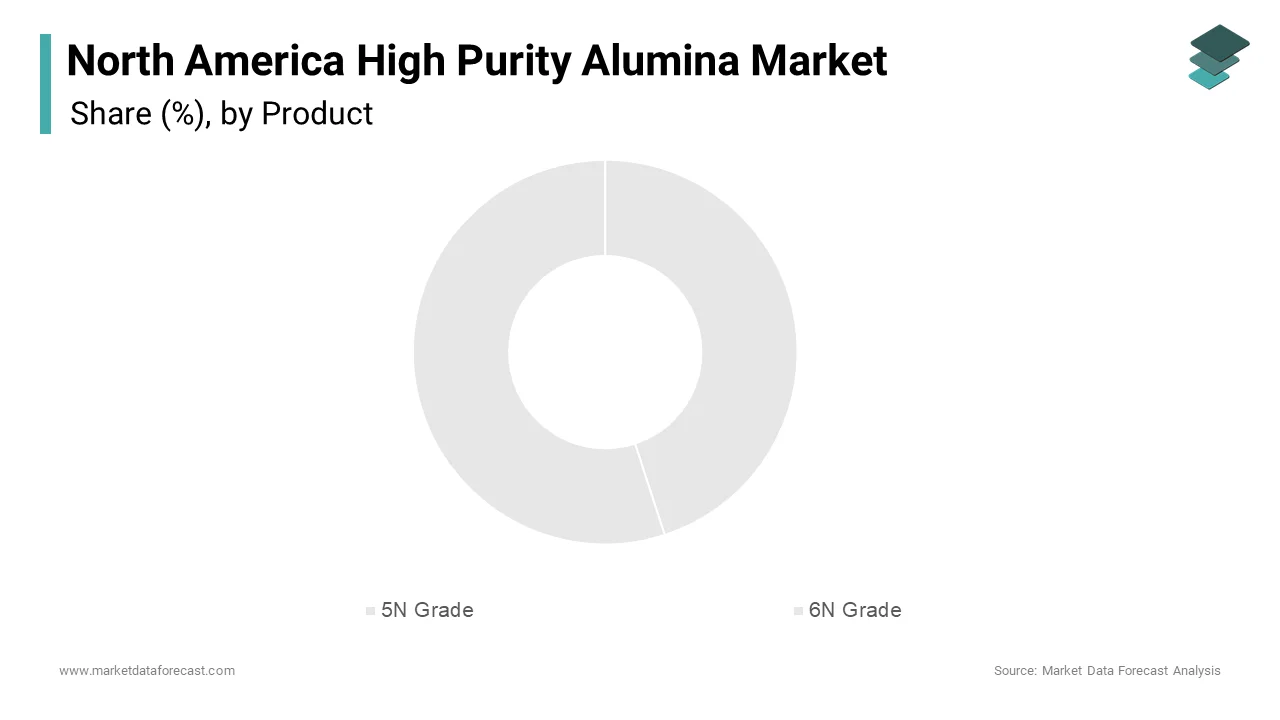

The 5N grade segment dominated the North America high purity alumina market by commanding a 45.5% share in 2024. Their versatility and precision make it indispensable across industries such as semiconductors, lithium-ion batteries, and LEDs. Professional manufacturers rely on 5N-grade HPA for its balanced purity levels ensuring compliance with stringent quality standards while remaining cost-effective. Also, 5N-grade variants exhibit superior performance compared to lower purity grades, contributing to a notable increase in sales in recent years. Additionally, innovations such as tailored particle sizes enhance user experience, driving preference among diverse demographics. Also, 5N-grade HPA accounted for a significant share of e-commerce transactions within the category, reflecting its mass appeal. Manufacturers capitalize on this demand by launching customizable options tailored to specific applications, further solidifying 5N-grade HPA’s leading position while addressing evolving consumer expectations.

The 6N grade emerges as the fastest-growing segment, boasting a CAGR of 9.5% from 2025 to 2033. This rapid expansion is fueled by its unparalleled purity levels, which are essential for cutting-edge applications such as semiconductor wafers and aerospace components. Industries such as microelectronics extensively utilize 6N-grade HPA to achieve prolonged shelf life. Technological breakthroughs enabling variable concentration adjustments and multi-purpose formulations broaden applicability across diverse sectors. Moreover, partnerships with distributors streamline accessibility, ensuring timely deployment of cutting-edge technologies. As industries embrace automation and digitization, the imperative for seamless environmental controls grows, positioning this segment as a transformative force within the market.

By Application Insights

The semiconductor application gained maximum prominence in the North America high purity alumina market by capturing 40.6% of total revenue in 2024. This arises is because of its ability to meet the stringent requirements of semiconductor fabrication, including thermal stability, electrical insulation, and chemical resistance. Like, semiconductors account for a considerable share of all HPA consumption, owing to their solubility and ease of integration into existing processes. Furthermore, innovations such as low-residue formulations enhance user comfort without inflating costs, driving preference among budget-conscious consumers. Strategic collaborations between manufacturers and suppliers ensure widespread distribution, fostering accessibility across urban and suburban markets.

The Li-ion battery applications represent the fastest-growing segment by registering a CAGR of 10.2% from 2025 to 2033. This surge is due to the indispensable role of HPA in achieving precision and durability, particularly in electric vehicle (EV) and renewable energy storage applications. For instance, high-concentration powders capable of handling viscous coatings are essential for large-scale infrastructure projects. Additionally, stringent occupational health regulations mandate comfortable working conditions, driving factories to upgrade outdated systems with energy-efficient alternatives. Technological breakthroughs, such as IoT-enabled monitoring, further bolster efficiency, allowing real-time adjustments tailored to specific production needs. As industries embrace automation and digitization, the imperative for seamless environmental controls grows, positioning this segment as a catalyst for transformative growth within the market.

COUNTRY LEVEL ANALYSIS

The United States commanded the largest share of the North America high purity alumina market by accounting for 75.6% of regional revenue in 2024. This dominance is due to pervasive urbanization trends and escalating demand for advanced materials in cutting-edge industries. Metropolitan areas like Silicon Valley exhibit exceptionally high adoption rates, with a notable share of households utilizing advanced tools during peak renovation seasons. Furthermore, the nation’s robust e-commerce infrastructure facilitates easy access to affordable models, fostering widespread accessibility. Government initiatives promoting green technologies also incentivize manufacturers to develop energy-efficient variants aligning with federal sustainability objectives.

Canada emerges as the major contributor to the North America high purity alumina market. Harsh winters spanning several provinces necessitate effective painting solutions to combat moisture damage, driving consistent demand nationwide. Ontario and Quebec, home to dense urban populations, collectively account for a major share of domestic sales. Public health advisories issued by provincial authorities emphasize the importance of maintaining adequate humidity levels to mitigate respiratory ailments, further boosting consumer confidence in these products. Additionally, stringent environmental policies incentivize eco-friendly designs are prompting local manufacturers to innovate sustainable offerings. Cross-border trade agreements facilitate seamless import-export activities, enabling Canadian firms to leverage U.S.-based R&D expertise.

Mexico is holding a modest share. Despite its smaller footprint, the country demonstrates considerable growth potential fueled by rapid urbanization and rising disposable incomes. Affordable pricing strategies adopted by domestic manufacturers make painting tools accessible to broader demographics by offsetting economic disparities prevalent in rural regions. Collaborations with international brands introduce advanced technologies previously unavailable locally, accelerating market evolution. Moreover, government-led housing programs incorporating climate control provisions enhance long-term prospects, embedding painting tools into mainstream construction practices. While challenges persist due to limited awareness and infrastructural constraints, Mexico’s burgeoning appetite for modern conveniences ensures steady progress, gradually elevating its significance within the regional framework.

The Rest of North America encompasses smaller economies such as Puerto Rico and the Caribbean islands, collectively representing a nascent yet promising segment. Also, this region benefits from unique climatic conditions requiring tailored painting solutions. Similarly, agricultural hubs adopt industrial-grade systems to preserve crop quality, as erratic rainfall patterns disrupt traditional farming methods. Limited local manufacturing capabilities necessitate reliance on imports, fostering symbiotic relationships with U.S.-based suppliers. Educational campaigns spearheaded by NGOs raise awareness about respiratory health, cultivating grassroots demand.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the North America high purity alumina market are Alcoa Inc, Sumitomo Chemical Co. Ltd, Nippon Light Metal Holdings Co. Ltd, Sasol Limited, Xuancheng Jingrui New Materials Co. Ltd, Altech Chemicals, Hebei Pengda Advanced Materials Technology, and PSB Industries SA.

The North America high purity alumina market is characterized by intense competition, marked by a delicate balance between established giants and emerging challengers. Market leaders like Alcoa Corporation and Sumitomo Chemical dominate through relentless innovation, consistently unveiling technologically advanced products that set industry benchmarks. Meanwhile, smaller firms like Orbite Technologies capitalize on affordability and niche appeal, carving out loyal customer bases. The competitive landscape is further complicated by the influx of counterfeit products, which distort pricing structures and erode brand equity. To counteract this, incumbents engage in aggressive promotional tactics, including influencer partnerships and seasonal discounts, to maintain visibility. Simultaneously, regulatory compliance serves as both a barrier and an opportunity, with companies investing in safer, greener designs to align with evolving standards.

Top Players in the Market

Alcoa Corporation

Alcoa Corporation stands out as a leading player in the North America high purity alumina market, leveraging its reputation for innovation and reliability. Renowned for producing advanced formulations like ultra-high-purity grades tailored for semiconductor applications, Alcoa addresses key consumer pain points such as stability and efficacy. Strategic partnerships with major retailers like Walmart and Target ensure widespread distribution, while investments in R&D yield cutting-edge features like enhanced solubility and reduced environmental impact. Its commitment to sustainability is evident in eco-friendly offerings, appealing to environmentally conscious buyers.

Sumitomo Chemical Co., Ltd.

Sumitomo Chemical occupies a prominent position, credited with revolutionizing the market through sleek, high-performance tools integrated with precision engineering. The Sumitomo Advanced Material Line exemplifies this synergy, combining high-concentration delivery with adjustable formulations to deliver unparalleled finishes. Its emphasis on aesthetics and functionality resonates with design-oriented consumers, bolstered by aggressive digital marketing campaigns. Furthermore, Sumitomo’s global supply chain network enables efficient scaling, reinforcing its competitive edge.

Orbite Technologies Inc.

Orbite Technologies rounds out the top three, specializing in affordable yet stylish tools catering to budget-conscious households. Known for its EcoPure Benzalkonium Chloride Series popular among DIY enthusiasts. Its focus on durability and ease of use fosters brand loyalty, particularly in suburban communities. Collaborations with online platforms enhance visibility, while periodic discounts drive impulse purchases. Orbite’s adaptability to shifting consumer preferences ensures sustained relevance amidst fierce competition.

Top Strategies Used by Key Players

Key players in the North America high purity alumina market employ diverse strategies to consolidate their positions and stimulate growth. Product differentiation emerges as a cornerstone tactic, with companies like Alcoa Corporation and Sumitomo Chemical investing heavily in R&D to introduce multifunctional variants combining precision with durability. Strategic alliances with e-commerce giants facilitate extensive reach, enabling brands to tap into burgeoning online sales channels. Pricing strategies also play a pivotal role; premium manufacturers like Sumitomo adopt skimming models targeting affluent demographics, whereas Orbite focuses on penetration pricing to attract budget-conscious buyers. Additionally, sustainability initiatives, including eco-friendly coatings and recyclable materials, resonate with environmentally aware consumers. Marketing campaigns emphasizing health benefits further amplify demand, particularly during peak seasons like winter.

RECENT HAPPENINGS IN THE MARKET

- In April 2023, Alcoa Corporation launched the UltraPure Series, featuring enhanced solubility technology. This move strengthened its portfolio of precision-focused products.

- In June 2023, Sumitomo Chemical unveiled the Advanced Material Line, introducing adjustable formulations alongside high-concentration delivery. This reinforced its reputation for multifunctional innovation.

- In August 2023, Orbite Technologies partnered with AmazonBasics to offer exclusive bundles, enhancing affordability and accessibility for budget-conscious consumers.

- In October 2023, Nippon Light Metal introduced the GreenGuard HPA Series, combining eco-friendly formulations with IoT-enabled monitoring. This addressed diverse consumer preferences effectively.

- In December 2023, Showa Denko collaborated with Home Depot to launch a DIY workshop series, educating amateur painters on advanced techniques, appealing to tech-savvy users.

MARKET SEGMENTATION

This research report on the north america polyisoprene market has been segmented and sub-segmented into the following.

By Product

- 5N Grade

- 6N Grade

By Application

- Semiconductor

- Li-ion Battery

By Country

- The U.S.

- Canada

- Rest of North America.

Frequently Asked Questions

What are the key applications of HPA in North America?

In North America, HPA is primarily used in LED lighting Lithium-ion battery separators Sapphire substrates Semiconductors Optical lenses and bio-ceramics.

How is the HPA market segmented in North America?

The market is segmented by Purity Level (4N, 5N, 6N) Application (LEDs, batteries, semiconductors, etc.) End-Use Industry (automotive, electronics, medical, etc.) Country (U.S., Canada, Mexico)

What are the challenges facing the HPA market in North America?

Key challenges include are High production costs Complex and energy-intensive manufacturing processes Dependence on specific raw materials (like aluminum feedstock)

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com