North America Hip Replacement Devices Market Research Report – Segmented By End User, Product, Material and Country (the United States, Canada and Rest of North America - Industry Analysis on Size, Share, Trends, COVID-19 Impact & Growth Forecast (2026 to 2034)

North America Hip Replacement Devices Market Summary

Market Size & Growth

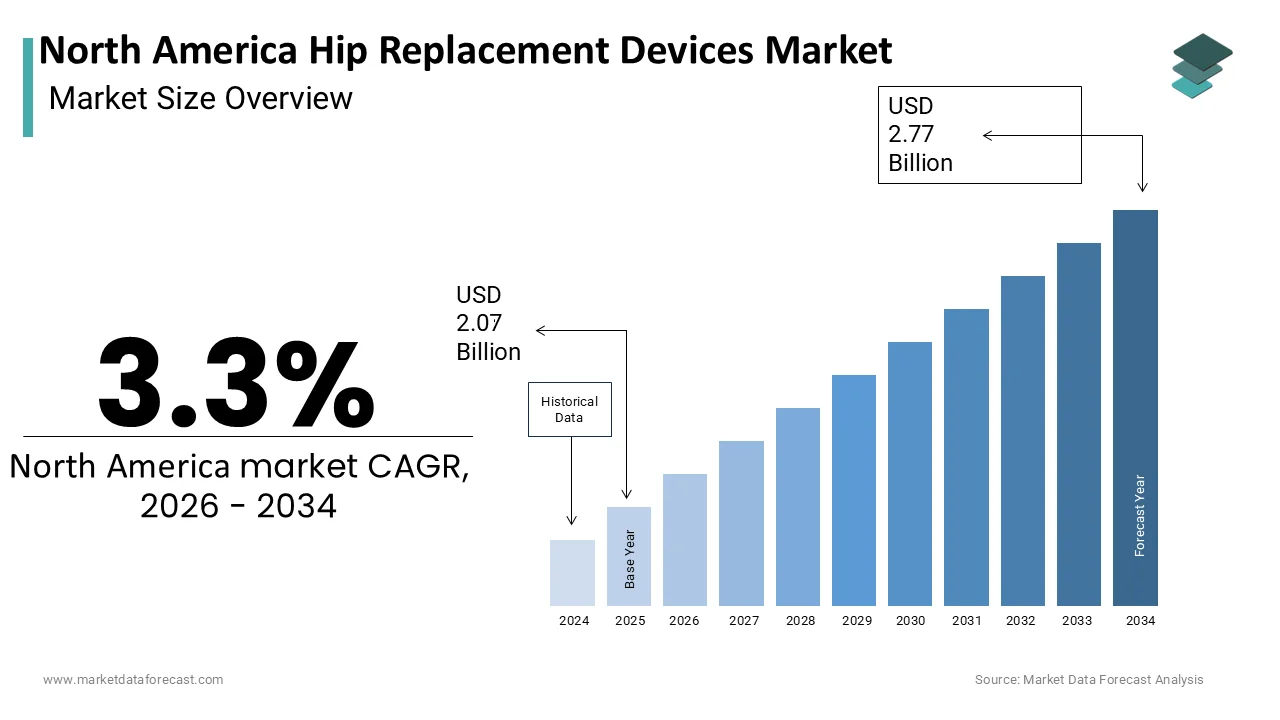

- The North America Hip Replacement Devices Market was valued at USD 2.07 billion in 2025.

- Estimated to reach USD 2.13 billion in 2026.

- Projected to grow to USD 2.77 billion by 2034, registering a CAGR of 3.3% from 2026 to 2034.

- The United States holds the dominant country share at 84.9% in 2025.

Key Market Segments

- By Product: Total Hip Replacement (65.6% share in 2025, dominant); Revision Hip Replacement (fastest growing at CAGR of 7.8% from 2026 to 2034); Partial Hip Replacement; Hip Resurfacing.

- By Material: Metal on Polyethylene (45.3% share in 2025, dominant); Ceramic on Ceramic (fastest growing at CAGR of 8.5% from 2026 to 2034).

- By End User: Hospitals (largest share in 2025); Ambulatory Surgical Centres (fastest growing at CAGR of 9.2% from 2026 to 2034); Orthopedic Clinics.

- By Geography: United States leads with 84.9% share in 2025; Canada holds a notable share supported by a publicly funded system.

Key Drivers

- Over 32 million adults in the United States suffer from osteoarthritis (Arthritis Foundation), creating sustained surgical demand.

- The U.S. population aged 65 and older is projected to reach nearly 95 million by 2060 (U.S. Census Bureau), expanding the primary candidate pool.

- Adult obesity prevalence of 40.3% in the United States (CDC) accelerates hip joint degeneration, increasing arthroplasty candidacy.

- Robotic-assisted total hip arthroplasty results in shorter hospital stays and fewer complications; the computer-assisted orthopedic surgery tools market is growing at approximately 11% annually.

- CMS expanded the ambulatory surgery center covered procedures list to include total hip arthroplasty, driving the migration of procedures to lower-cost outpatient settings.

Key Statistics by Segment

- Total hip arthroplasty volume in the United States exceeds 500,000 annual procedures (American Joint Replacement Registry).

- Ten-year survival rate for total hip replacements exceeds 95% (Journal of Bone and Joint Surgery).

- Fewer than 7% of primary implants require revision within 15 years (National Joint Registry).

- Ceramic on Ceramic fracture rate is less than 0.01% with modern fourth-generation materials (Journal of Arthroplasty).

- ASC procedures cost approximately 40% less than hospital outpatient departments (Ambulatory Surgery Center Association).

- Total hospitalization costs for hip replacement procedures routinely exceed USD 30,000 (Healthcare Cost and Utilization Project).

- Canada performs over 175,000 hip and knee replacements annually, growing roughly 20% over five years (Canadian Institute for Health Information).

Key Players

Stryker Corporation, Zimmer Biomet Holdings Inc., Johnson & Johnson (DePuy Synthes), Smith & Nephew plc, B. Braun Melsungen AG, Exactech Inc., DJO Global Inc., MicroPort Scientific Corporation, OMNI Life Science Inc.

North America Hip Replacement Devices Market Size

The North America Hip Replacement Devices Market was valued at USD 2.07 billion in 2025 and is estimated to reach USD 2.13 billion in 2026. The market is projected to grow to USD 2.77 billion by 2034, registering a CAGR of 3.3% from 2026 to 2034.

Hip replacement devices (or prostheses) are artificial implants used in hip replacement surgery to replace damaged or arthritic bone and cartilage. These devices are designed to mimic the natural ball-and-socket action of your hip joint, helping to relieve severe pain and restore mobility. This sector primarily includes total hip arthroplasty systems, partial hip replacements and resurfacing devices crafted from advanced biomaterials such as titanium cobalt chromium alloys,, and highly cross linked polyethylene. The clinical landscape is defined by an increasing prevalence of osteoarthritis and traumatic injuries that necessitate surgical intervention to improve quality of life. In addition, the Centers for Disease Control and Prevention (CDC) indicates that nearly 1 in 4 adults in the United States have been diagnosed with arthritis, establishing the condition as a leading cause of work and activity disability nationwide. Technological advancements have shifted the paradigm toward minimally invasive techniques and robotic assisted surgeries which enhance precision and reduce recovery times. The market is characterized by stringent regulatory oversight from the Food and Drug Administration ensuring that only devices meeting rigorous safety and efficacy standards reach clinical practice. Patient demographics are shifting with a growing cohort of younger individuals seeking durable solutions that allow for active lifestyles post surgery. This dynamic interplay between clinical necessity technological innovation and regulatory compliance defines the current state of the hip replacement devices sector in North America.

MARKET DRIVERS

Rising Prevalence of Osteoarthritis and Degenerative Joint Diseases

The escalating incidence of osteoarthritis is driving demand for these devices across the region, which boosts the growth of the North America hip replacement devices market. Osteoarthritis is a chronic condition characterized by the breakdown of joint cartilage and underlying bone leading to pain stiffness and reduced mobility. Moreover, the Arthritis Foundation indicates that more than 32 million adults in the United States suffer from osteoarthritis, expanding the patient population progressively vulnerable to advanced hip joint degradation. The aging population exacerbates this trend as the risk of developing degenerative joint diseases increases significantly with age. Demographic projections from the U.S. Census Bureau indicate that the United States population aged 65 and older will expand to nearly 95 million by 2060, driving up the total volume of age-related joint interventions. This demographic shift ensures a steady influx of patients who are prime candidates for hip arthroplasty. Furthermore obesity rates contribute to the burden on hip joints as excess body weight places additional stress on weight bearing joints accelerating cartilage wear. The Centers for Disease Control and Prevention (CDC) reports an adult obesity prevalence of 40.3% in the United States, a systemic health factor that places continuous biomechanical stress on weight-bearing joints. As conservative treatments such as physical therapy and medication fail to provide long term relief surgical replacement becomes the definitive solution. The convergence of an aging populace rising obesity levels and high prevalence of joint degeneration creates a robust and sustained demand for advanced hip replacement technologies that offer durability and improved functional outcomes for patients.

Advancements in Minimally Invasive and Robotic Assisted Surgical Techniques

Technological innovation in surgical methodologies significantly propels the expansion of the North America hip replacement devices market. This surges the adoption of modern hip replacement devices by enhancing procedural precision and patient recovery profiles. The integration of robotic assisted systems allows surgeons to plan and execute hip arthroplasty with unprecedented accuracy leading to better implant positioning and alignment. Clinical data featured in the Journal of Arthroplasty demonstrates that robotic-assisted total hip arthroplasty results in shorter lengths of stay and fewer postoperative complications through highly precise mechanical positioning. These superior clinical outcomes encourage both healthcare providers and patients to opt for advanced device systems compatible with robotic platforms. Major medical device manufacturers are increasingly focusing on developing implants specifically engineered for use with navigation and robotic systems thereby creating a synergistic relationship between hardware and software. Sources indicate that the market for computer-assisted orthopedic surgery tools is expanding robustly at an annual growth rate of roughly 11%, reflecting a steady clinical shift toward technology-driven precision. Additionally minimally invasive techniques reduce tissue trauma blood loss and postoperative pain enabling faster rehabilitation and return to daily activities. Patients are becoming more informed and actively seek out facilities offering these advanced surgical options which pressures healthcare institutions to invest in state of the art equipment and compatible implants. This technological pull effect ensures that the market continues to evolve toward sophisticated device designs that support next generation surgical workflows and deliver superior value propositions to stakeholders across the care continuum.

MARKET RESTRAINTS

Stringent Regulatory Approval Processes and Compliance Burdens

The rigorous regulatory framework governing medical devices in the region significantly restrains the expansion of the North America hip replacement devices market. This prolongs time to market and increases development costs. The U.S. Food and Drug Administration (FDA) subjects hip replacement implants to rigorous Class II regulatory pathways, mandating detailed biomechanical performance testing to achieve market clearance. Regulatory frameworks under the U.S. Food and Drug Administration (FDA) establish clear performance targets to process complex device applications within standard time-to-decision intervals to minimize commercialization delays. This lengthy approval timeline delays the introduction of innovative products and limits the ability of companies to respond quickly to emerging clinical needs. Furthermore post market surveillance requirements mandate continuous monitoring of device performance and adverse events which adds to the operational complexity and cost structure for manufacturers. The Medical Device User Fee Amendments impose significant fees on companies seeking regulatory clearance further straining resources especially for smaller enterprises. Compliance with evolving regulations such as the Unique Device Identification system requires extensive data management infrastructure and reporting capabilities. Any deviation from regulatory standards can result in product recalls fines or market withdrawal which poses severe reputational and financial risks. These regulatory hurdles create high barriers to entry discouraging new competitors and limiting the diversity of available solutions. Consequently the market remains dominated by established players who possess the resources to navigate complex regulatory landscapes while smaller innovators struggle to bring novel technologies to clinical practice thereby slowing overall market dynamism and product diversification.

High Costs Associated with Hip Replacement Procedures and Reimbursement Pressures

The substantial financial burden associated with hip replacement surgery and fluctuating reimbursement policies is a major impediment to the accessibility and growth of the North American market. Total hip arthroplasty involves significant costs including implant prices surgical fees hospital stays and postoperative care which can amount to tens of thousands of dollars per procedure. Healthcare cost tracking tools like the Healthcare Cost and Utilization Project (HCUP) demonstrate that the total hospitalization costs for a hip replacement procedure routinely exceed $30,000, highlighting the considerable economic impact of arthroplasty on the healthcare landscape. Insurance reimbursement rates have come under pressure as payers seek to control healthcare expenditures leading to tighter coverage criteria and lower payment amounts for providers. The Centers for Medicare and Medicaid Services periodically adjusts reimbursement rates which can impact hospital profitability and their willingness to adopt premium priced devices. Value based purchasing initiatives require providers to demonstrate superior clinical outcomes and cost effectiveness to maintain reimbursement levels adding another layer of financial complexity. Patients with high deductible insurance plans may face substantial out of pocket expenses which can deter them from pursuing timely surgical intervention. Economic uncertainties and healthcare budget constraints further exacerbate these financial barriers limiting access to advanced hip replacement technologies for certain patient segments. These cost related challenges force manufacturers to engage in aggressive pricing strategies and value demonstrations which can compress profit margins and limit investment in research and development. The tension between delivering high quality care and managing costs remains a persistent obstacle that constrains market expansion and influences procurement decisions across healthcare systems.

MARKET OPPORTUNITIES

Integration of Artificial Intelligence and Predictive Analytics in Patient Care

The incorporation of artificial intelligence and predictive analytics into orthopedic care offers major opportunities for the North America hip replacement devices market. This paves the way for optimizing patient selection and improving surgical outcomes in the joint replacement sector. AI algorithms can analyze vast datasets including electronic health records imaging studies and patient reported outcomes to identify individuals at highest risk for complications or poor recovery. A study demonstrates that specialized machine learning models can achieve accuracy rates exceeding 85% when utilizing preoperative patient characteristics to predict complications like dislocation or infection after a total hip arthroplasty. This predictive capability enables clinicians to tailor preoperative optimization strategies and personalize implant selection based on individual patient characteristics. Device manufacturers are leveraging AI to design implants with enhanced biomechanical properties by simulating wear patterns and stress distributions under various loading conditions. The integration of smart implants equipped with sensors allows for real time monitoring of joint function and early detection of loosening or failure. Research indicates that the integration of digital health applications and remote patient monitoring tools within the orthopedic device sector is expanding rapidly, driven by institutional demand for data-driven clinical decision support. These technologies facilitate remote patient monitoring reducing the need for frequent clinic visits and enabling timely interventions when issues arise. By harnessing the power of big data and AI stakeholders can enhance clinical efficiency reduce costs and improve patient satisfaction. This digital transformation opens new avenues for value creation allowing manufacturers to offer comprehensive solutions that extend beyond the physical implant to include ongoing care management and outcome tracking services.

Expansion of Ambulatory Surgical Centers for Outpatient Hip Replacements

The shift toward performing hip replacement procedures in ambulatory surgical centers rather than traditional hospitals creates a pathway for the expansion of the North America hip replacement devices market. This is driven by cost efficiency and patient preference. Advances in anesthesia techniques pain management protocols and minimally invasive surgical approaches have made it feasible to discharge patients on the same day or within 24 hours of surgery. Sources confirm that the volume of outpatient total joint replacements performed in ambulatory surgery centers has escalated significantly over the past five years as clinical confidence in same-day discharge protocols strengthens. Ambulatory surgical centers offer lower overhead costs compared to hospitals resulting in reduced procedure costs for payers and patients. Revisions implemented by the Centers for Medicare & Medicaid Services (CMS) expanded the ambulatory surgery center covered procedures list to include total hip arthroplasty, structurally driving the migration of elective joint procedures into outpatient ecosystems. Patients benefit from a more personalized care environment shorter wait times and reduced exposure to hospital acquired infections. Device manufacturers are responding by developing implant systems specifically optimized for outpatient settings including easier insertion techniques and rapid recovery profiles. This trend aligns with broader healthcare goals of reducing unnecessary hospitalizations and improving resource utilization. As more surgeons gain proficiency in outpatient joint replacement techniques the volume of procedures performed in ASCs is expected to rise substantially. This migration creates new distribution channels and partnership opportunities for manufacturers who can provide tailored support services and training programs for ASC staff. The expansion of outpatient care models thus offers a lucrative avenue for market growth while enhancing accessibility and convenience for patients seeking hip replacement solutions.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Raw Material Shortages

The global supply chain disruptions and the scarcity of critical raw materials are serious challenges to the consistent availability and pricing stability of these devices, which hinders the growth of the North America hip replacement devices market. The manufacturing of orthopedic implants relies heavily on specialized materials such as medical grade titanium cobalt chromium alloys and ultra high molecular weight polyethylene which are subject to geopolitical tensions and trade restrictions. Sources indicate that structural shifts in minor metal refining and geopolitical supply disruptions have triggered significant pricing volatility for medical-grade titanium, increasing baseline manufacturing expenses for orthopedic implant components. Dependence on single source suppliers for certain components increases vulnerability to disruptions caused by natural disasters political instability or logistical bottlenecks. The semiconductor shortage has also affected the production of robotic surgical systems and smart implants that rely on electronic components further complicating the supply landscape. Manufacturers face difficulties in maintaining adequate inventory levels while balancing cost efficiency leading to potential delays in fulfilling orders from healthcare providers. The complexity of global supply networks makes it challenging to quickly pivot to alternative sources when disruptions occur. Regulatory requirements for material traceability and quality control add another layer of complexity to supply chain management. These vulnerabilities can result in device shortages forcing hospitals to postpone surgeries or switch to less optimal alternatives. Addressing these supply chain risks requires significant investment in diversification strategies nearshoring initiatives and strategic stockpiling which can strain financial resources. The ongoing uncertainty in global trade dynamics continues to threaten the reliability of device availability impacting patient care and market stability.

Shortage of Skilled Orthopedic Surgeons and Healthcare Professionals

The deficit of trained orthopedic surgeons and specialized healthcare professionals constitutes a critical factor limiting the capacity to meet growing demand for these procedures, which further obstructs the expansion of the North America hip replacement devices market. Performing hip arthroplasty requires extensive training and expertise which takes years to develop creating a bottleneck in workforce availability. Studies project a widening deficit of practicing orthopedic specialists over the coming decade, driven by accelerating retirement rates among senior surgeons and strict federally capped limits on surgical residency allocations. This shortage is exacerbated by the increasing complexity of surgical techniques including robotic assisted procedures that require additional training and certification. Rural and underserved areas are particularly affected as fewer specialists choose to practice in these locations leading to geographic disparities in access to care. The burden on existing surgeons results in longer wait times for patients potentially worsening their condition and complicating surgical outcomes. Nursing shortages also impact postoperative care quality as specialized orthopedic nurses are essential for managing recovery and preventing complications. The Association of American Medical Colleges reports that medical school enrollment has not kept pace with population growth further straining the pipeline of future healthcare providers. Training programs require significant resources and time to produce competent practitioners limiting the speed at which the workforce can expand. This human capital constraint restricts the volume of procedures that can be performed safely and effectively capping market growth despite strong patient demand. Addressing this challenge requires coordinated efforts in education funding workforce retention and telemedicine integration to optimize resource utilization.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Product, Material, End User, and Region |

| Various Analyses Covered | Global, Regional and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | The U.S., Canada, and the rest of North America |

| Market Leaders Profiled | B. Braun Melsungen AG, Exactech, Inc., DJO Global, Inc., Johnson & Johnson (DePuy Synthes), MicroPort Scientific Corporation, OMNI Life Science, Inc., Smith & Nephew plc, Zimmer Biomet Holdings, Inc., Stryker Corporation. |

SEGMENTAL ANALYSIS

By Product Insights

The Total Hip Replacement segment led the North America hip replacement devices market and captured a share of 65.6% share in 2025. This leading position of the segment was attributed to the high prevalence of end stage osteoarthritis which necessitates complete joint reconstruction rather than partial interventions. A study shows that total hip arthroplasty volume in the United States has expanded beyond 500,000 annual procedures, reinforcing its status as a frontline intervention for end-stage joint degeneration. The comprehensive nature of total replacement addresses both the acetabular and femoral components ensuring long term stability and pain relief for patients with advanced joint damage. The escalating prevalence of advanced osteoarthritis is the primary driver for the dominance of this segment. Osteoarthritis progressively destroys cartilage leading to bone on bone friction that causes severe pain and functional impairment. The Centers for Disease Control and Prevention (CDC) reports that doctor-diagnosed arthritis impacts approximately 53.2 million adults in the United States, presenting a primary systemic driver of musculoskeletal disability. As the population ages the severity of joint degeneration increases making partial replacements insufficient for many patients. Sources reveal that the clinical utilization rate of total hip replacements surges dramatically among individuals aged 65 and older, driven by the cumulative effects of mechanical joint wear and advanced osteoarthritis. This demographic shift ensures a consistent volume of candidates who require full joint reconstruction to restore mobility. Furthermore obesity exacerbates joint wear accelerating the progression to end stage disease where total replacement becomes the only viable surgical option. The clinical superiority of total hip systems in addressing complex deformities and providing durable outcomes reinforces their preference among surgeons. Consequently the sheer volume of patients presenting with advanced degenerative changes sustains the leading position of this product segment in the regional market.

The preference for Total Hip Replacement devices is further reinforced by their proven long term clinical outcomes and enhanced durability compared to alternative procedures. Modern implant designs utilizing highly cross linked polyethylene and ceramic bearings have significantly reduced wear rates extending the lifespan of the prosthesis. According to a study published in The Journal of Bone and Joint Surgery the ten year survival rate for total hip replacements exceeds 95 percent providing patients with confidence in the longevity of the solution. This reliability is crucial for younger patients who are increasingly seeking surgical intervention to maintain active lifestyles. Surgeons favor total hip systems because they offer predictable results and allow for precise restoration of hip biomechanics. The ability to customize implant size and geometry to match individual patient anatomy enhances fit and function reducing the risk of complications such as dislocation or loosening. These clinical advantages drive widespread adoption across healthcare facilities as providers seek to minimize postoperative issues and maximize patient satisfaction. The robust evidence supporting the efficacy of total hip arthroplasty solidifies its position as the dominant product segment in the North American market.

The revision hip replacement segment is estimated to register the fastest CAGR of 7.8% from 2026 to 2034 due to the increasing number of primary hip replacements performed in previous decades which are now reaching the end of their functional lifespan. As the population ages and life expectancy increases the cumulative volume of implants requiring replacement due to wear loosening or infection rises steadily. The surge in revision hip replacement procedures is directly correlated with the aging cohort of patients who underwent primary arthroplasty in earlier years. Many of these initial implants were inserted when patients were younger and more active leading to accelerated wear and eventual failure. The Healthcare Cost and Utilization Project (HCUP) indicates a steady rise in the volume of complex revision hip surgeries, a trend driven by a growing population of patients outliving their primary joint implants. As medical technology improves and patients live longer the demand for secondary interventions grows proportionally. The National Joint Registry (NJR) demonstrates that modern total hip replacements maintain exceptional longevity, with fewer than 7% of primary implants requiring revision intervention within 15 years of the index surgery. This statistical trend creates a sustained pipeline of patients needing complex reconstructive surgery. Furthermore improvements in diagnostic imaging allow for earlier detection of implant loosening or osteolysis prompting timely revision before severe bone loss occurs. Surgeons are also becoming more proficient in handling complex revision cases encouraging earlier intervention. The backlog of aging implants from the peak adoption periods of the 1990s and 2000s ensures that revision volumes will continue to rise. This demographic and clinical dynamic positions revision hip replacement as the most rapidly expanding segment in the North American market.

Technological innovations specifically designed for revision scenarios are fueling the growth of this segment by improving surgical success rates and patient outcomes. Revision surgeries often involve significant bone loss requiring specialized implants such as modular stems and augments that can restore structural integrity. These advanced materials allow for better fixation in compromised bone stock reducing the risk of subsequent failure. Additionally computer assisted navigation and 3D printing technologies enable surgeons to plan complex revisions with greater precision customizing implants to fit unique anatomical defects. The integration of these tools reduces operative time and improves alignment which is critical in revision settings. Manufacturers are investing heavily in research and development to create solutions tailored for the challenging environment of revision surgery. The availability of these sophisticated options encourages surgeons to undertake revisions that might have been deemed too risky in the past. As clinical confidence grows and technology evolves the capacity to address failed primary implants expands driving the rapid growth of the revision hip replacement segment.

By Material Insights

The Metal on Polyethylene segment dominated the North America Hip Replacement Devices Market and accounted for a 45.3% share in 2025. This dominance of the segment was driven by the extensive clinical history and cost effectiveness of this bearing couple which remains the workhorse for primary hip arthroplasty. The familiarity of surgeons with this material combination and its satisfactory performance in standard risk patients sustain its market leadership. The continued dominance of Metal on Polyethylene bearings is underpinned by their extensive clinical track record and favorable cost profile. Decades of use have generated vast amounts of long term data confirming their safety and efficacy in a broad patient population. According to the National Joint Registry metal on polyethylene implants demonstrate a ten year survivorship rate of over 90 percent which meets the expectations of most patients and payers. The lower manufacturing costs associated with polyethylene liners compared to ceramic components make this option more accessible for healthcare systems operating under budget constraints. The Centers for Medicare and Medicaid Services reimbursement policies often favor cost effective solutions without compromising quality which supports the widespread use of this material combination. Surgeons appreciate the ease of insertion and the forgiving nature of polyethylene liners which accommodate minor variations in component positioning. This versatility makes metal on polyethylene suitable for a wide range of anatomical variations and surgical techniques. The balance between acceptable wear rates and affordability ensures that this segment remains the default choice for many standard primary hip replacements. Consequently the entrenched position of metal on polyethylene in clinical practice and reimbursement frameworks sustains its leading market share.

Metal on Polyethylene bearings exhibit remarkable versatility making them suitable for a diverse range of patient demographics and surgical indications. Unlike ceramic bearings which may carry a risk of fracture or squeaking metal on polyethylene systems are robust and reliable in various clinical scenarios. The material properties of modern highly cross linked polyethylene have significantly improved wear resistance narrowing the performance gap with ceramic options. This improvement allows metal on polyethylene to be used in younger patients who previously might have been directed toward ceramic bearings. The compatibility of polyethylene liners with various femoral head sizes provides surgeons with flexibility in restoring hip stability and range of motion. Furthermore the absence of noise generation associated with some ceramic interfaces enhances patient satisfaction. The adaptability of this material combination to different surgical approaches including minimally invasive techniques further broadens its appeal. As healthcare providers seek solutions that can serve a broad patient base efficiently metal on polyethylene remains the most versatile and widely adopted material segment in the market.

The Ceramic on Ceramic segment is anticipated to witness the fastest CAGR of 8.5% during the forecast period owing to the increasing demand for ultra low wear bearings among younger and more active patients who require implants with exceptional longevity. The superior hardness and biocompatibility of ceramic materials minimize particle generation reducing the risk of osteolysis and aseptic loosening over time. The main driver for the rapid growth of Ceramic on Ceramic bearings is the shifting demographic of hip replacement patients toward younger and more active individuals. These patients place higher demands on implant durability due to increased physical activity levels which accelerate wear in traditional bearings. The extremely low wear rate of ceramic materials ensures that the implant can withstand decades of use without generating significant debris. This longevity is crucial for younger patients who wish to avoid multiple revision surgeries throughout their lifetime. The biocompatibility of ceramic also reduces the risk of adverse tissue reactions which is a concern with metal ions released from other bearing couples. Surgeons are increasingly recommending ceramic on ceramic for active patients based on evidence showing superior wear performance. The willingness of patients to invest in premium implants for long term benefits supports the adoption of this technology. As the trend toward early intervention continues the demand for ultra durable bearings like ceramic on ceramic will sustain its high growth trajectory.

Recent technological advancements have significantly mitigated historical concerns regarding ceramic fracture thereby enhancing the reliability and adoption of Ceramic on Ceramic bearings. Early generations of ceramic implants were prone to brittle fracture but modern fourth generation ceramics exhibit superior toughness and strength. According to a study in The Journal of Arthroplasty the fracture rate of modern ceramic on ceramic bearings is less than 0.01 percent which is comparable to other bearing surfaces. These improvements are achieved through advanced manufacturing processes that eliminate microstructural defects and enhance material density. The development of delta ceramics which combine alumina and zirconia offers optimal balance between hardness and fracture resistance. Surgeons feel more confident prescribing these implants knowing that the risk of catastrophic failure is negligible. Additionally improved taper designs reduce the risk of head neck junction corrosion which was another concern with earlier ceramic systems. The continuous innovation in ceramic technology reassures both clinicians and patients about the safety profile of these bearings. As confidence grows the barrier to adoption decreases allowing ceramic on ceramic to capture a larger share of the market. This technological evolution is key to sustaining the high growth rate of this segment in the coming years.

By End User Insights

In 2025, the hospitals segment held the majority share of the North America Hip Replacement Devices Market because of the capacity of hospitals to handle complex cases comorbidities and emergency revisions that require extensive resources and multidisciplinary care. The American Joint Replacement Registry (AJRR) demonstrates that inpatient and outpatient hospital settings continue to accommodate the vast majority of joint arthroplasties, particularly when managing complex revision configurations or high-acuity patient cohorts. The comprehensive infrastructure and specialized staff available in hospital settings make them the preferred choice for the majority of orthopedic surgeries. Hospitals maintain their leading position due to their unparalleled capacity to manage complex hip replacement cases and patients with significant comorbidities. Many individuals requiring hip arthroplasty suffer from concurrent conditions such as cardiovascular disease diabetes or obesity which increase surgical risk. Epidemiological studies highlighted by the Centers for Disease Control and Prevention (CDC) confirm that roughly 67% of adults aged 65 and older suffer from multiple chronic conditions, requiring careful medical optimization during major orthopedic procedures. Hospitals provide immediate access to intensive care units specialized anesthesia teams and emergency services which are critical for managing intraoperative or postoperative complications. This safety net is essential for high risk patients who cannot be treated in ambulatory settings. The presence of multidisciplinary teams including cardiologists pulmonologists and endocrinologists ensures comprehensive preoperative optimization and postoperative management. Surgeons prefer hospital environments for complex primary and revision cases where unexpected challenges may arise. The ability to extend hospital stays if necessary provides flexibility in recovery planning. Consequently the role of hospitals as the primary venue for high acuity orthopedic care sustains their dominant share in the market.

The dominance of hospitals is further reinforced by their access to advanced surgical infrastructure and highly specialized staff required for modern hip replacement procedures. State of the art operating rooms equipped with robotic surgical systems navigation tools and advanced imaging capabilities are predominantly located in hospital settings. Hospitals also employ dedicated orthopedic nurses physical therapists and case managers who specialize in joint replacement care pathways. This specialized workforce ensures standardized care protocols and efficient recovery processes which improve patient outcomes. The concentration of expertise and technology in hospitals attracts patients seeking the highest level of care. Academic medical centers within hospital systems also drive innovation and training fostering a culture of excellence in orthopedic surgery. The integration of research and clinical practice in hospitals facilitates the adoption of new techniques and devices. These structural advantages make hospitals the central hub for hip replacement services maintaining their leading position in the market.

The Ambulatory Surgical Centres segment is likely to experience the fastest CAGR of 9.2% between 2026 and 2034. This rapid growth of the segment is fueled by the shift toward value based care and the increasing feasibility of performing uncomplicated hip replacements in outpatient settings. Payers and patients favor ASCs due to lower costs and enhanced convenience while advancements in anesthesia and pain management enable safe same day discharge. The swift growth of this segment is propelled by the healthcare industry's shift toward value based care models that prioritize cost efficiency without compromising quality. ASCs offer a significantly lower cost structure compared to hospitals due to reduced overhead and streamlined operations. According to the Ambulatory Surgery Center Association procedures performed in ASCs cost approximately 40 percent less than those in hospital outpatient departments. This cost advantage aligns with payer strategies to reduce healthcare expenditures and incentivizes insurers to steer patients toward ASCs. Medicare has expanded coverage for total hip arthroplasty in ASCs recognizing the safety and efficacy of this setting for appropriate candidates. Patients benefit from lower out of pocket costs which increases their willingness to choose ASCs for elective surgery. The transparency of pricing in ASCs also appeals to self pay patients seeking affordable options. Healthcare systems are increasingly partnering with or acquiring ASCs to capture this growing market segment. The financial incentives for both payers and providers create a strong momentum for the migration of hip replacements to ambulatory settings. This economic dynamic ensures that ASCs will continue to grow at a faster rate than traditional hospital settings.

Patient preference for convenience and personalized care is a significant factor driving the growth of Ambulatory Surgical Centres. ASCs provide a more comfortable and less institutional environment which reduces patient anxiety and improves overall satisfaction. The streamlined scheduling and shorter wait times in ASCs appeal to patients seeking timely access to surgery. Same day discharge allows patients to recover in the comfort of their own homes which is preferred by many individuals. Advances in multimodal pain management protocols enable effective pain control without the need for prolonged hospital stays. The focus on patient centered care in ASCs fosters a positive experience that encourages word of mouth referrals. As patients become more empowered consumers they actively seek out facilities that offer convenience and high quality service. The alignment of ASC operations with patient preferences for efficiency and comfort drives the rapid expansion of this segment. This patient centric model ensures that ASCs will continue to gain market share in the hip replacement sector.

COUNTRY LEVEL ANALYSIS

United States Hip Replacement Devices Market Analysis

The United States outperformed other countries in the North America Hip Replacement Devices Market and captured an 84.9% share in 2025. This supremacy of the US market was supported by high adoption rates of advanced technologies and a large volume of procedures driven by an aging population and high prevalence of osteoarthritis. Data from the American Joint Replacement Registry (AJRR) indicates that over 500,000 hip replacement procedures are executed annually in the United States, expanding in volume due to the rising prevalence of degenerative joint diseases and an aging population. The presence of leading medical device manufacturers and robust reimbursement frameworks support continuous innovation and accessibility. The high healthcare expenditure per capita enables the adoption of premium implants and robotic assisted surgeries. Regulatory oversight by the Food and Drug Administration ensures high safety standards which builds trust among patients and providers. The concentration of academic medical centers drives research and development fostering a competitive landscape. The widespread insurance coverage for joint replacement procedures removes financial barriers for a significant portion of the population. Geographic diversity in healthcare delivery allows for varied adoption patterns with urban centers leading in technology uptake. The strong physician network and established clinical guidelines facilitate standardized care practices. These factors collectively sustain the United States as the largest and most influential market for hip replacement devices in North America.

Canada Hip Replacement Devices Market Analysis

Canada holds a notable share of the North America Hip Replacement Devices Market due to a publicly funded healthcare system that emphasizes cost effectiveness and equitable access to care. The Canadian Institute for Health Information (CIHI) finds that the annual volume of hip and knee replacements in Canada has scaled beyond 175,000 total operations, having grown by roughly 20% over a compressed five-year window to handle structural arthritic backlogs. The provincial health plans regulate procurement leading to centralized purchasing agreements that influence device selection and pricing. Wait times for elective surgeries remain a challenge prompting efforts to increase capacity through public private partnerships. The adoption of advanced technologies is gradual due to budget constraints but growing interest in value based outcomes is driving change. Rural areas face disparities in access which the government is addressing through telemedicine and mobile surgical units. The regulatory framework governed by Health Canada ensures rigorous safety standards similar to those in the United States. Collaboration with international research networks enhances clinical evidence generation. The focus on improving efficiency and reducing wait lists is shaping market dynamics. These structural characteristics define the Canadian market as a steady growth region with a focus on sustainability and access.

COMPETITIVE LANDSCAPE

The competition in the North America Hip Replacement Devices Market is intense and characterized by the presence of several large multinational corporations alongside specialized niche players. Market leaders compete primarily on technological innovation product quality and clinical evidence rather than price alone. The introduction of robotic assisted surgery has become a key differentiator with companies vying for surgeon preference through superior platform capabilities. Regulatory compliance and safety records are critical factors influencing hospital procurement decisions. Smaller companies often focus on specific niches such as revision implants or novel biomaterials to carve out market share. The high barriers to entry due to regulatory requirements and capital intensity limit new competitors but encourage consolidation through mergers and acquisitions. Intellectual property rights play a significant role in maintaining competitive advantages. Companies invest substantially in marketing and surgeon education to build brand loyalty. The shift toward value based care pressures manufacturers to demonstrate cost effectiveness and superior outcomes. Collaborative relationships with healthcare systems are essential for long term success. This dynamic landscape drives continuous improvement and innovation benefiting patients and providers alike.

KEY MARKET PLAYERS

Some of the companies that are playing a dominating role in the North America Hip Replacement Market include

- B. Braun Melsungen AG

- Exactech, Inc.

- DJO Global, Inc.

- Johnson & Johnson (DePuy Synthes)

- MicroPort Scientific Corporation

- OMNI Life Science, Inc.

- Smith & Nephew plc

- Zimmer Biomet Holdings, Inc.

- Stryker Corporation

TOP LEADING PLAYERS IN THE MARKET

- Stryker Corporation is a global leader in orthopedic solutions with a strong presence in the North America Hip Replacement Devices Market. The company focuses on innovation in joint reconstruction technologies including the Mako robotic arm assisted surgery system which enhances precision in hip arthroplasty. Stryker recently expanded its portfolio with advanced acetabular cups and femoral stems designed for improved osseointegration and longevity. The company invests heavily in research and development to introduce next generation materials and digital health solutions. Strategic partnerships with healthcare providers facilitate the adoption of its robotic platforms. Stryker’s commitment to clinical education and surgeon training strengthens its market position. The company’s comprehensive product range covers primary and revision surgeries catering to diverse patient needs. Its global distribution network ensures widespread availability of products. Stryker continues to drive growth through acquisitions and organic innovation maintaining its competitive edge in the orthopedic sector.

- Zimmer Biomet Holdings Inc is a major participant in the hip replacement market known for its extensive portfolio of joint reconstruction products. The company offers a wide array of hip implants including the Persona personalized knee system adapted for hip applications and the Vanguard complete hip solution. Zimmer Biomet emphasizes personalized medicine through its ROSA robotic platform which assists surgeons in achieving optimal implant placement. The company has recently launched new bearing surfaces and minimally invasive instruments to improve surgical outcomes. Zimmer Biomet collaborates with clinical experts to validate the performance of its devices. Its focus on data analytics and patient reported outcomes helps refine product designs. The company’s global reach and strong brand reputation support its market leadership. Zimmer Biomet continues to invest in digital surgery ecosystems to enhance value for healthcare providers. Its strategic initiatives aim to improve efficiency and patient satisfaction in hip replacement procedures.

- Johnson and Johnson through its DePuy Synthes subsidiary is a key player in the North America Hip Replacement Devices Market. The company offers the Corail and Pinnacle hip systems which are widely used in primary and revision surgeries. DePuy Synthes focuses on advancing biomaterials such as oxidized zirconium to reduce wear and improve durability. The company integrates digital tools like the VELYS robotic assisted solution to support surgeons in hip arthroplasty. Recent actions include expanding its manufacturing capacity and enhancing supply chain resilience. Johnson and Johnson leverages its vast resources to drive innovation and clinical research. The company collaborates with orthopedic associations to promote best practices in joint replacement. Its strong regulatory compliance and quality assurance processes ensure product reliability. DePuy Synthes continues to strengthen its market position through product launches and strategic alliances. The company’s holistic approach to patient care supports its leadership in the orthopedic devices sector.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the North America Hip Replacement Devices Market employ several strategic initiatives to maintain competitiveness and drive growth. Product innovation remains central with companies investing heavily in research and development to create advanced implants with improved durability and biocompatibility. The integration of robotic assisted surgery platforms is a major strategy enabling precise implant placement and better clinical outcomes. Companies are also focusing on digital health solutions such as remote patient monitoring and data analytics to enhance postoperative care and value based reimbursement models. Strategic mergers and acquisitions allow firms to expand their product portfolios and enter new geographic markets. Partnerships with healthcare providers and academic institutions facilitate clinical validation and adoption of new technologies. Cost optimization through supply chain efficiency and localized manufacturing helps mitigate pricing pressures. Educational programs for surgeons ensure proper utilization of complex devices and foster brand loyalty. These strategies collectively enable market participants to navigate regulatory challenges and meet evolving patient needs effectively.

MARKET SEGMENTATION

This research report on the North America hip replacement devices market has been segmented and sub-segmented into the following categories

By Product

- Total Procedure

- Fixed

- Mobile-Bearing

- Partial Hip Replacement

- Hip Resurfacing

- Revision Hip Replacement

By Material

- Metal

- Metal on Polyethylene

- Ceramic on Metal

- Ceramic on Polyethylene

- Ceramic on Ceramic

By End-user

- Ambulatory Surgical Centres

- Hospitals

- Orthopedic Clinics

By Country

- The United States

- Canada

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com