North America Human Growth Hormone Market Size, Share, Trends & Growth Forecast Report - Segmented By Product (long-acting human growth hormone, Others), Application, Distribution Channel and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

Market Size, 2025

$7087.20 MnMarket Estimate, 2026

$7920.65 MnMarket Forecast, 2034

$19277.55 MnCAGR, 2026–2034

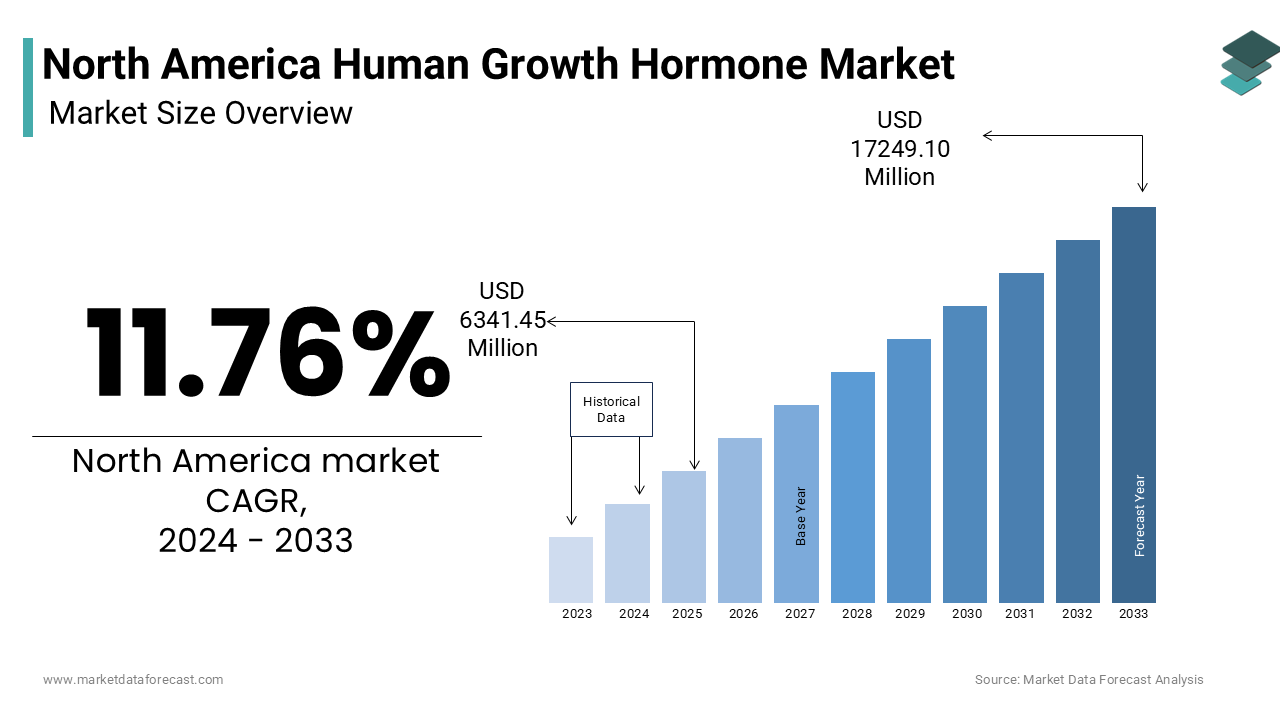

11.76%North America Human Growth Hormone Market Size

The North America human growth hormone market size was valued at USD 7087.20 million in 2025 and is anticipated to reach USD 7920.65 million in 2026 from USD 19277.56 million by 2034, growing at a CAGR of 11.76% during the forecast period from 2026 to 2034.

The clinical application of recombinant human growth hormone (rhGH) for managing endocrine-related growth pathologies and metabolic dysfunctions. Administered primarily via subcutaneous injection, rhGH is indicated for conditions such as growth hormone deficiency (GHD), Turner syndrome, Prader-Willi syndrome, and short stature associated with chronic renal insufficiency. The therapeutic mechanism involves stimulating insulin-like growth factor 1 (IGF-1) production, thereby promoting linear growth in children and lean body mass preservation in adults. Early diagnosis is facilitated by standardized growth charts adopted by the Centers for Disease Control and Prevention, which are routinely used in well-child visits by enabling timely identification of growth deviations.

MARKET DRIVERS

Increasing Incidence of Childhood Obesity and Its Endocrine Complications

The rising prevalence of childhood obesity and its associated endocrine disruptions, which often mimic or exacerbate growth hormone deficiency is accelerating the growth of the North America human growth hormone market. According to the Centers for Disease Control and Prevention, more than 19.7% of children and adolescents aged 2–19 in the United States were obese in 2022, a figure that has tripled since the 1980s. This functional GH impairment necessitates endocrinological evaluation, with an increasing number of obese children being referred for stimulation testing. Data from the National Health and Nutrition Examination Survey (NHANES) indicates that between 2015 and 2021, referrals to pediatric endocrinologists for growth concerns increased by 28%, disproportionately driven by obese patients with delayed growth patterns.

Growing Geriatric Population and Recognition of Adult Growth Hormone Deficiency

The shift toward an aging population with intensifying clinical focus on adult growth hormone deficiency (AGHD), a condition increasingly linked to age-related physiological decline and comorbidities is propelling the growth of the North America human growth hormone market. As per the U.S. Census Bureau, adults aged 65 and over constituted 17.3% of the U.S. population in 2023, a proportion projected to reach 23% by 2050. A significant subset of this group those with a history of pituitary tumors, cranial irradiation, or traumatic brain injury is at elevated risk for AGHD. The Endocrine Society estimates that up to 30% of adults with hypopituitarism remain undiagnosed, despite exhibiting symptoms such as reduced muscle mass, increased adiposity, fatigue, and impaired quality of life.

MARKET RESTRAINTS

Limited Long-Term Safety Data in Pediatric Populations

The absence of comprehensive long-term safety data for children undergoing extended rhGH therapy, particularly regarding late-onset metabolic and oncological risks is declining the growth of the North America human growth hormone market. Although rhGH has been used clinically since the mid-1980s, longitudinal studies tracking patients into their fifth and sixth decades remain sparse. The National Hormone and Pituitary Program (NHPP) Longitudinal Study, which monitors over 24,000 individuals treated with hGH since 1985, reported in 2023 that pediatric recipients exhibit a 1.8-fold increased standardized mortality ratio for stroke and cardiovascular disease in adulthood, though causality remains under investigation. Additionally, concerns persist about potential cancer recurrence in survivors of childhood malignancies treated with rhGH. A 2021 study by the St. Jude Children’s Research Hospital found that among 1,498 childhood cancer survivors receiving rhGH, the incidence of secondary neoplasms was 3.2% over 20 years, compared to 2.1% in untreated controls. Furthermore, the lack of standardized post-treatment surveillance protocols means many patients discontinue follow-up after growth plate closure. As per the Pediatric Endocrine Society, fewer than 35% of rhGH-treated adolescents transition to adult endocrinology care.

Geographic and Socioeconomic Disparities in Access to Pediatric Endocrinology Care

The geographic maldistribution of pediatric endocrinologists and socioeconomic inequities in healthcare is degrading the growth of North America human growth hormone market. As per the American Academy of Pediatrics, there are only 1.2 pediatric endocrinologists per 100,000 children in the U.S., with severe shortages in rural regions such as the Mississippi Delta, Northern Plains, and Appalachia. Socioeconomic factors further compound the issue: families without private insurance or residing in Medicaid-expansion states with restrictive formularies often face denials for rhGH therapy. In Canada, while healthcare is publicly funded, provinces like Saskatchewan and Newfoundland report specialist wait times of over 10 months for pediatric endocrinology assessments. Additionally, Indigenous communities in northern Canada face logistical barriers, including air transport requirements for specialist visits. These structural inequities limit the effective reach of rhGH therapy, which is preventing equitable market penetration and leaving a substantial portion of the eligible patient population untreated despite medical need.

MARKET OPPORTUNITIES

Development of Long-Acting and Non-Invasive Delivery Systems

The advancement of long-acting and non-invasive delivery technologies that address adherence challenges and improve patient experience is gearing up to showcase new opportunities for the growth of the North America human growth hormone market. Traditional rhGH regimens require daily subcutaneous injections, a burden that contributes to non-compliance rates exceeding 30% among pediatric patients, as reported by the Nemours Children’s Health System. In 2023, the FDA approved somatrogon, a once-weekly rhGH analog developed by Novo Nordisk, which demonstrated non-inferiority to daily therapy with a 94% adherence rate in phase 3 trials conducted across 15 U.S. and Canadian centers. Concurrently, transdermal microneedle patches and oral rhGH formulations are advancing through clinical development. Prototypes tested at the Massachusetts Institute of Technology achieved measurable IGF-1 elevation in preclinical models, with phase 1 human trials expected by 2025.

Integration of Genomic Screening in Neonatal and Pediatric Care

The integration of genomic and molecular diagnostics into routine pediatric care through early and precise identification of genetic growth disorders is additionally to enhance the growth of the North America human growth hormone market. Advances in next-generation sequencing (NGS) have enabled the detection of monogenic causes of short stature, such as mutations in the GH1, GHRHR, and STAT5B genes, long before phenotypic manifestations become evident. As per the National Institutes of Health’s Undiagnosed Diseases Network, over 1,200 children with idiopathic short stature underwent exome sequencing between 2018 and 2022, revealing pathogenic variants in growth-related genes in 27% of cases. This molecular stratification allows for targeted rhGH therapy in genetically confirmed deficiencies, improving treatment response rates.

MARKET CHALLENGES

Regulatory Fragmentation Between U.S. and Canadian Reimbursement Policies

The lack of harmonization between U.S. and Canadian reimbursement frameworks is creating operational inefficiencies for manufacturers and access disparities for patients is to hamper the growth of the North America human growth hormone market. In the United States, coverage for rhGH is determined by a patchwork of private insurers, Medicaid programs, and Medicare, each with distinct prior authorization criteria. As per the Kaiser Family Foundation, 22 states impose different coverage rules for rhGH based on diagnosis, with only 14 states covering idiopathic short stature under Medicaid. However, adoption of CDR recommendations is not mandatory, leading to interprovincial variation. For instance, Quebec funds rhGH for Turner syndrome but excludes SHOX deficiency, while British Columbia covers both. These divergent pathways complicate market entry strategies for biopharmaceutical firms, requiring dual pricing, separate clinical dossiers, and distinct patient support programs. The absence of cross-border regulatory alignment increases commercial risk and limits economies of scale, which is hindering the efficient diffusion of new therapies across the continent.

Misuse of rhGH in Anti-Aging and Performance Enhancement Sectors

The unauthorized use of recombinant human growth hormone in anti-aging clinics and athletic performance enhancement is likely to decline the growth of the North America human growth hormone market. According to the U.S. Government Accountability Office, over 12,000 licensed practitioners in the U.S. operate in the longevity medicine sector, with an estimated 35% offering rhGH without documented deficiency, based on a 2022 field investigation. The FDA has repeatedly warned against such use, citing risks including arthralgia, insulin resistance, and cardiomyopathy. A 2023 study by the Mayo Clinic found that adults using rhGH for non-therapeutic purposes had a 2.1-fold higher incidence of type 2 diabetes over five years. In sports, the World Anti-Doping Agency continues to report elevated rhGH misuse in professional and amateur leagues; in 2022, 47 athletes across North American leagues tested positive for hGH, a 19% increase from 2020. This illicit demand distorts supply chains, inflates black-market prices, and diverts product from legitimate patients. Moreover, media portrayal of rhGH as a “fountain of youth” undermines public understanding of its medical purpose. Health Canada has responded with stricter pharmacy audits, but enforcement remains inconsistent.

SEGMENTAL ANALYSIS

By Product Insights

The long-acting human growth hormone segment was accounted in holding a prominent share of the North America human growth hormone market in 2024 with the clinical and logistical advantages of extended-release formulations that reduce injection frequency from daily to weekly or biweekly. The approval of somatrogon (once-weekly) by the FDA in 2023 marked a pivotal shift, with over 120,000 prescriptions dispensed in its first year, according to Symphony Health claims data. Additionally, manufacturers are investing in novel delivery platforms, including sustained-release microspheres and transdermal patches in preclinical development. The U.S. Department of Health and Human Services has included long-acting rhGH in its Biomedical Advanced Development portfolio, accelerating regulatory review.

The “Others” product segment is anticipated to grow at a CAGR of 10.2% in the coming years. Brands like Genotropin, Norditropin, and Humatrope have been used for over three decades, with over 1.2 million patient-years of safety data compiled in global registries such as the Pfizer International Growth Database (KIGS). As per the FDA, 89% of rhGH prescriptions in 2023 were for daily formulations, which is reflecting entrenched prescribing habits and formulary preferences.

By Application Insights

The Growth Hormone Deficiency (GHD) segment was accounted in holding a prominent share of the North America human growth hormone market in 2024 with the high prevalence of both congenital and acquired GHD across pediatric and adult populations, coupled with well-established clinical guidelines supporting rhGH therapy. Early detection through routine growth monitoring in primary care settings has significantly expanded the diagnosed patient pool. As per the Centers for Disease Control and Prevention, over 85% of U.S. pediatric clinics now employ standardized growth velocity tracking, leading to a 24% increase in GHD diagnoses between 2017 and 2022. The National Institutes of Health reports that over 60,000 adults in the U.S. have documented hypopituitarism, with only 40% receiving rhGH replacement, indicating substantial unmet need. The FDA’s continued approval of rhGH for diverse GHD etiologies, including post-surgical and traumatic causes, reinforces its therapeutic centrality.

The turner syndrome segment is likely to grow with an expected CAGR at a CAGR of 9.4% during the forecast period with earlier diagnosis, expanded treatment duration, and improved long-term outcomes. The FDA-approved use of rhGH for Turner Syndrome since 1996 has been optimized through extended treatment regimens, with current protocols recommending therapy until final height is achieved, often beyond age 16. Data from the MAGIC Foundation indicates that early initiation of rhGH before age four increases final adult height by an average of 9.8 cm compared to late treatment. Furthermore, multidisciplinary care models integrating endocrinology, cardiology, and genetics have improved patient retention, with adherence rates exceeding 82% in specialized centers.

By Distribution Channel Insights

The hospital pharmacy segment was the largest and held a prominent share of the North America human growth hormone market in 2024 with the institutionalized nature of rhGH prescribing, where initiation, monitoring, and dispensing are tightly integrated within hospital-affiliated endocrinology departments. The majority of rhGH prescriptions originate in tertiary care centers, particularly children’s hospitals and academic medical institutions, where complex growth disorders are diagnosed and managed. As per the Children’s Hospital Association, over 88% of pediatric rhGH starts occur in hospital-based clinics, where multidisciplinary teams oversee treatment eligibility and safety. Additionally, hospital pharmacies are often linked to specialty distribution networks that ensure cold-chain integrity and compliance with Risk Evaluation and Mitigation Strategies (REMS) mandated by the FDA.

The retail pharmacy segment is likely to grow with an estimated CAGR of 8.7% from 2025 to 2033 owing to the rising adoption of home-based therapy models, increased insurance coverage for retail dispensing, and the expansion of specialty pharmacy networks. Traditionally, rhGH was dispensed exclusively through hospitals, but evolving patient preferences for convenience and privacy are shifting demand toward community and mail-order retail pharmacies. As per the National Community Pharmacists Association, over 1,200 retail pharmacies in the U.S. are now accredited as specialty pharmacies capable of handling biologics, including rhGH, with cold-chain compliance and patient support services. CVS Specialty and Walgreens Specialty Pharmacy together manage over 45% of non-hospital rhGH dispensing by offering home delivery and nurse training. Additionally, Medicare Part D and commercial plans are increasingly covering retail-dispensed rhGH, with 70% of formularies including at least one retail-specialty option, as reported by the Kaiser Family Foundation.

REGIONAL ANALYSIS

United States Human Growth Hormone Market

The United States was the top performer of the North America human growth hormone market by accounting for 78.3% of share in 2024. The country has over 900 pediatric endocrinologists and more than 200 specialized children’s hospitals, which is facilitating early diagnosis and treatment initiation. According to the CDC, over 70% of children with growth disorders are diagnosed before age eight, a rate unmatched in the region. The Orphan Drug Act incentivizes rhGH development, with multiple brands enjoying market exclusivity. Additionally, private insurers cover 85% of rhGH costs on average, reducing patient burden.

Canada Human Growth Hormone Market

Canada was the ranked second by occupying 14.3% of the North America human growth hormone market share in 2024 with funded healthcare system ensures equitable access, though with administrative delays. Health Canada has approved all major rhGH products, and provincial drug plans cover eligible indications. However, approval timelines average 90–120 days, as reported by the Canadian Agency for Drugs and Technologies in Health. The Canadian Paediatric Society notes that only 40% of children with GHD receive timely treatment due to specialist shortages in remote regions. Nevertheless, initiatives like Ontario’s Rare Disease Strategy are improving access.

KEY MARKET PLAYERS

The major companies active in the North America Human Growth Hormone Market include

- Novo Nordisk

- Pfizer Inc. (in collaboration with Opko Health)

- Eli Lilly and Company

- Merck KGaA

- Ferring Pharmaceuticals

- Sandoz (a Novartis company)

- Genentech (a Roche company)

- Ipsen

- Teva Pharmaceutical Industries Ltd.

- Ascendis Pharma

- AnkeBio

COMPETITIVE LANDSCAPE

The competitive landscape of the North America human growth hormone market is characterized by a concentrated oligopoly dominated by a few established biopharmaceutical giants with deep expertise in endocrinology and rare diseases. These companies leverage their scientific heritage, regulatory experience, and extensive distribution networks to maintain strong market positions. Competition is less price-driven and more centered on innovation, patient support, and clinical differentiation. The advent of long-acting formulations has intensified rivalry, with firms racing to introduce next-generation therapies that improve convenience and adherence. Strategic differentiation is achieved through comprehensive care ecosystems, including digital health platforms, specialty pharmacy partnerships, and physician education initiatives. Biosimilar entry has introduced moderate pressure, prompting originators to emphasize value beyond the molecule, such as superior delivery systems and real-world evidence.

Top Players in the North America Human Growth Hormone Market

Novo Nordisk

Novo Nordisk is a leading innovator in the North America human growth hormone market with renowned for its robust endocrinology portfolio and patient-centric therapeutic development. The company has pioneered advancements in long-acting growth hormone formulations, emphasizing improved dosing frequency and enhanced adherence. Its commitment to endocrine care extends beyond product development to encompass comprehensive support programs that assist patients and healthcare providers in navigating treatment pathways. Its research-driven approach and focus on sustainable innovation continue to influence clinical standards by making it a key contributor to global rhGH therapy evolution and shaping treatment paradigms in both pediatric and adult populations.

Pfizer

Pfizer plays a pivotal role in the human growth hormone landscape through its long-standing presence and extensive global reach. The company’s legacy in biopharmaceuticals has enabled it to maintain a strong foothold in the endocrinology sector, supported by a well-established distribution network and enduring relationships with healthcare institutions. Pfizer emphasizes lifecycle management of its growth hormone products, combining clinical research with real-world data analytics to refine therapeutic outcomes. Its international patient registries contribute significantly to post-marketing surveillance and treatment optimization.

Genentech (Roche)

Genentech, a member of the Roche Group, is a trailblazer in recombinant biologics and has been instrumental in shaping the modern human growth hormone market. As one of the first companies to commercialize rhGH, it set foundational standards for safety, efficacy, and clinical monitoring. The company’s dedication to endocrine innovation is reflected in its comprehensive support systems, including patient assistance programs and digital adherence tools. Genentech continues to lead in pharmacovigilance through its long-running patient databases, which inform clinical practice and regulatory decisions worldwide. Its integration of research, medical education, and patient advocacy has elevated the standard of care in growth disorders.

Top Strategies Used by Key Market Participants

One major strategy employed by leading players is the development and commercialization of long-acting growth hormone formulations to improve patient adherence and reduce treatment burden. By shifting from daily to weekly or extended-release injections, companies enhance user experience, which in turn strengthens brand loyalty and clinical preference. This innovation-driven approach positions firms as pioneers in patient-centric care, differentiating their offerings in a competitive landscape.

Another key strategy is the expansion of integrated patient support programs that include reimbursement assistance, nurse training, and digital monitoring tools. These services streamline access, improve continuity of care, and foster trust between patients, providers, and manufacturers. By embedding support into the therapy journey, companies ensure sustained engagement and reduce discontinuation rates.

Another important strategy is the pursuit of lifecycle management through regulatory submissions for new indications, delivery devices, and combination therapies. This enables firms to extend product relevance, defend market share, and respond to emerging clinical needs. Companies maintain its dominance in a dynamic and highly specialized market by continuously evolving their therapeutic applications.

REGIONAL ANALYSIS

- In March 2023, Novo Nordisk launched a nationwide digital adherence program for its long-acting growth hormone therapy, integrating smart injection pens with a mobile application to support pediatric patients and caregivers across the United States and Canada. This initiative is anticipated to improve treatment consistency and strengthen patient engagement.

- In June 2023, Pfizer expanded its partnership with a leading U.S. specialty pharmacy to enhance direct-to-patient delivery and home-based nursing support for rhGH users, which is aiming to streamline access and reduce treatment initiation delays.

- In September 2023, Genentech introduced an updated version of its patient support portal, offering real-time insurance verification, financial assistance, and virtual consultations with endocrinology nurses, reinforcing its commitment to end-to-end care management.

- In January 2024, Novo Nordisk announced a collaboration with a pediatric telehealth network to integrate growth monitoring and rhGH prescription services into virtual care platforms, which is broadening access in underserved rural regions.

- In May 2024, Pfizer initiated a multicenter clinical registry to collect long-term outcomes data on adult growth hormone deficiency patients by aiming to strengthen evidence-based prescribing and support payer negotiations.

MARKET SEGMENTATION

This research report on the North America Human Growth Hormone Market is segmented and sub-segmented based on categories.

By Product

- long-acting human growth hormone

- Others

By Application

- Growth Hormone (GH) Deficiency

- Adult GH Deficiency

- Pediatric GH Deficiency

- Turner Syndrome

- Idiopathic Short Stature

- Prader-Willi Syndrome

- Small For Gestational Age

- Other

By Distribution Channel

- Hospital Pharmacy

- Retail Pharmacy

- Online Pharmacy

- Specialty Pharmacy

By Country

- U.S.

- Canada

- Rest of North America

Frequently Asked Questions

What is the North America Human Growth Hormone Market?

The North America Human Growth Hormone Market refers to the industry focused on the production, distribution, and usage of recombinant human growth hormone (HGH) therapies used for treating growth hormone deficiencies and related conditions.

What is driving the growth of the North America Human Growth Hormone Market?

The market growth is driven by rising cases of growth hormone deficiency, increasing awareness about hormone therapies, advancements in long-acting formulations, and approvals of innovative HGH products.

Who are the key players in the North America Human Growth Hormone Market?

Key players include Novo Nordisk, Pfizer (with Opko Health), Eli Lilly, Merck KGaA, Ferring Pharmaceuticals, Sandoz (Novartis), Genentech (Roche), Ipsen, Teva, and Ascendis Pharma.

What are the major challenges in the North America Human Growth Hormone Market?

Challenges include high treatment costs, stringent regulatory requirements, and potential side effects of long-term hormone usage.

What is the growth outlook for the North America Human Growth Hormone Market?

The market is expected to witness steady growth over the next decade, supported by rising demand for innovative and long-acting therapies along with strong R&D investments.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com