North America Intelligent Power Module Market Report Research By Power Device (IGBT , MOSFET )Voltage Rating, Application and Country (The U.S., Canada and Rest of North America) - Industry Analysis( 2026 to 2034).

Market Size, 2025

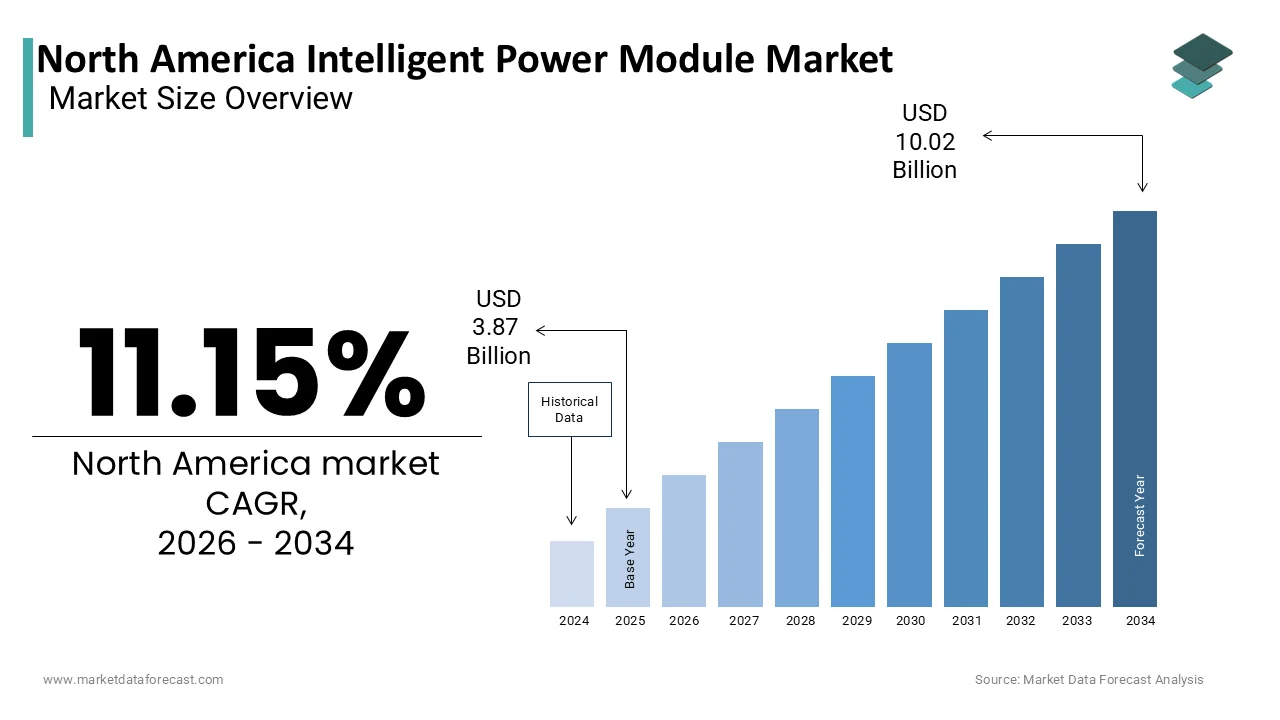

$3.87 BnMarket Estimate, 2026

$4.30 BnMarket Forecast, 2034

$10.02 BnCAGR, 2026–2034

11.15%North America Intelligent Power Module Market Size

The North America Intelligent Power Module Market Size was valued at USD 3.87 billion in 2025, is expected to have 11.15 % CAGR from 2026 to 2034, and be worth USD 10.02 billion by 2034 from USD 4.30 billion in 2026.

North America’s intelligent power module (IPM) market centers on integrated semiconductor devices that consolidate power switching and control logic, enabling compact, high-efficiency power management across emerging electrification and automation domains. IPMs are increasingly adopted across high-growth applications such as electric mobility, utility-scale renewables, and smart manufacturing, where precise power modulation and system-level efficiency are critical. Their ability to minimize thermal load, reduce switching losses, and support fault-tolerant operation positions IPMs as core enablers of next-gen energy systems.

MARKET DRIVERS

Expansion of Renewable Energy Infrastructure

One of the most significant drivers fueling the growth of the intelligent power module (IPM) market in North America is the rapid expansion of renewable energy infrastructure. Governments across the United States and Canada have set ambitious targets to reduce carbon emissions and transition toward clean energy sources. According to the International Energy Agency (IEA), North America accounted for nearly 25% of global renewable energy capacity additions in 2025, with solar and wind energy leading the charge. This energy transition demands power converters capable of bidirectional energy flow, ultra-fast switching, and real-time diagnostics capabilities delivered by IPMs.

Intelligent power modules are crucial in photovoltaic inverters, wind turbine converters, and battery storage systems, enabling precise control and minimizing energy losses. For instance, the Solar Energy Industries Association (SEIA) reported that the U.S. installed over 32 gigawatts (GW) of solar capacity in 2025, marking a 40% increase compared to the previous year. Moreover, federal incentives such as the Inflation Reduction Act (IRA) in the U.S. have accelerated investment in green technologies, creating a favorable environment for manufacturers of intelligent power modules.

Growth in Electric Vehicle Production and Adoption

The accelerating adoption and production of electric vehicles (EVs) represent another major driver for the intelligent power module (IPM) market in North America. EV powertrains increasingly depend on SiC- and GaN-enhanced IPMs for high-frequency switching in fast-charging, traction control, and auxiliary power units. According to the Edison Electric Institute, over 1.2 million electric vehicles were sold in the United States in 2025, reflecting a year-over-year growth rate of more than 50%.

Automotive manufacturers across North America are ramping up EV production capacities, and these OEM-led capex expansions are reshaping semiconductor demand curves, shifting sourcing preferences toward localized, thermally robust IPM architectures. For example, Ford announced in 2025 that it would invest $50 billion in electrification through 2026, significantly increasing the demand for intelligent power modules used in traction inverters and auxiliary systems.

MARKET RESTRAINTS

High Manufacturing and R&D Costs

Capital intensity in substrate innovation and module-level thermal testing continues to exclude price-sensitive verticals and limit SME participation. Developing advanced IPMs requires significant investment in cutting-edge semiconductor materials, precision packaging technologies, and specialized testing equipment. These costs are driven by the need for continuous innovation to meet evolving performance demands in sectors such as automotive, industrial automation, and renewable energy.

Moreover, the complexity of integrating IGBTs, gate drivers, and protection circuits within a single module increases production expenses. Yole Développement noted that the fabrication of silicon carbide (SiC) and gallium nitride (GaN)-based IPMs, which offer superior efficiency but come at a premium, remains a costly endeavor. As a result, non-integrated players face margin compression due to high tooling and fab access costs, increasing reliance on OEM-subsidized pilot programs.

Supply Chain Disruptions and Material Shortages

Another critical restraint impacting the intelligent power module (IPM) market in North America is the persistent issue of supply chain disruptions and shortages of essential raw materials. Chronic input volatility from Si wafers to AlN substrates has pushed module lead times beyond 16 weeks, creating design delays for EV and grid OEMs.

The reliance on a limited number of global suppliers for raw materials exacerbates this challenge. For instance, many of the silicon wafers used in IPM manufacturing are sourced from just a handful of companies based in Japan, South Korea, and Taiwan. Additionally, geopolitical tensions and trade restrictions have introduced uncertainties in logistics and customs clearance processes, further complicating supply chain management.

MARKET OPPORTUNITIES

Rising Demand for Smart Industrial Automation

The increasing adoption of smart industrial automation presents a compelling opportunity for the intelligent power module (IPM) market in North America. As industries embrace digital transformation, the demand for high-efficiency, compact, and reliable power solutions has surged. These robotic systems, along with automated conveyor belts, CNC machines, and motor drives, require robust power electronics to manage complex operations efficiently.

Intelligent power modules are integral to variable frequency drives (VFDs), servo drives, and programmable logic controllers (PLCs), which are extensively deployed in modern factories. Furthermore, Canada’s Digital Technology Supercluster, a federally backed initiative, has allocated over CAD 200 million toward smart manufacturing projects, reinforcing the momentum behind automation.

Increasing Investments in Grid Modernization Programs

Another promising opportunity for the intelligent power module (IPM) market in North America lies in the growing investments aimed at modernizing the electrical grid infrastructure. Aging power distribution networks are being upgraded to support smarter, more resilient, and decentralized energy systems.

Intelligent power modules are essential components in grid-tied inverters, solid-state transformers, and dynamic voltage regulators, which enable efficient energy flow and real-time monitoring. Statistics from the National Rural Electric Cooperative Association (NRECA) indicate that over 70% of U.S. transmission lines are more than 25 years old, highlighting the urgency for technological upgrades. BloombergNEF estimated that North America’s investment in grid modernization reached over $30 billion in 2025, with a projected annual growth rate of 6.5% through 2030. As governments and utility providers continue to prioritize grid resilience and sustainability, the demand for intelligent power modules is poised to witness a steady upward trajectory.

MARKET CHALLENGES

Technological Complexity and Integration Issues

The inherent technological complexity and integration difficulties associated with these advanced power electronics are the foremost challenges facing the intelligent power module (IPM) market in North America. IPMs combine high-voltage semiconductor devices such as IGBTs and MOSFETs with embedded control circuitry, requiring precise engineering to ensure optimal performance and reliability. As per IEEE Spectrum, the integration of multiple functionalities within a confined space often leads to thermal management issues, electromagnetic interference (EMI), and signal noise problems, which can compromise system stability.

Furthermore, the rapid evolution of power semiconductor materials such as silicon carbide (SiC) and gallium nitride (GaN) has introduced additional layers of complexity in design and compatibility. Manufacturers must continuously adapt their designs to accommodate varying application requirements across industries like automotive, industrial automation, and renewable energy. Also, the lack of standardized design protocols across different manufacturers hampers interoperability, prolonging development cycles and increasing time-to-market.

Regulatory Compliance and Evolving Safety Standards

Navigating regulatory compliance and evolving safety standards poses a significant challenge for manufacturers operating in the North American intelligent power module (IPM) market. As power electronics become more integrated into critical applications such as electric vehicles, industrial machinery, and grid infrastructure, regulatory bodies have imposed stricter performance and safety requirements.

Compliance with standards such as UL 61800-5-1 for adjustable speed electrical power drive systems and ISO 26262 for functional safety in automotive applications adds complexity to the development process. Meeting these stringent regulations often requires extensive validation testing, increasing both time-to-market and production costs. Additionally, Canada’s Canadian Standards Association (CSA Group) has updated several power electronics certification protocols, mandating additional stress tests and lifecycle assessments.

REPORT COVERAGE

| METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Power Device, Voltage Rating, Application, and Country. |

| Various Analyses Covered | Global, Regional, & Country Level Analysis, Segment-Level Analysis; DROC, PESTLE Analysis, Porter's Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Country Covered | The U.S., Canada, da and the rest of North America |

| Market Leader Profiled | Mitsubishi Electric Corp, ON Semiconductor Corp, Infineon Technologies AG |

SEGMENTAL ANALYSIS

By Power Device Insights

The IGBT segment had the largest share of the North America intelligent power module market, accounting for approximately 62.4% of total revenue in 2025. This dominance is primarily due to their suitability in high-voltage traction inverters, VFDs, and utility-scale inverters, particularly in EVs and solar fields requiring ≥600V operation.

Moreover, the U.S. Department of Energy reported that in 2025, wind and solar installations accounted for more than 45 GW of new generation capacity, where IGBT modules are extensively used in power conversion units. The ability of IGBTs to offer low conduction losses and high switching performance makes them ideal for these applications.

The MOSFET segment is projected to grow at the fastest CAGR of 9.8% from 2025 to 2033 within the North America intelligent power module market. These, particularly SiC-based, are optimized for medium-voltage use cases under 900V, such as DC-DC converters, onboard chargers, and data center PSUs

For instance, Tesla’s Model 3 and Ford’s Mustang Mach-E both utilize SiC MOSFETs for improved energy efficiency and thermal management. Additionally, the growing deployment of 5G infrastructure and data centers has further boosted the need for compact, high-efficiency MOSFET-based power modules.

By Voltage Rating Insights

The 600 V to 1,199 V voltage rating segment maintained the dominant position in the North America intelligent power module market, capturing a 48.7% of total revenue in 2025. modules represent the workhorse voltage class for three-phase AC motor drives, mid-scale solar inverters, and industrial servo platforms. In addition, the Solar Energy Industries Association (SEIA) reported that central inverters used in large-scale photovoltaic installations typically operate between 600 V and 1,000 V, contributing significantly to the demand for IPMs in this voltage category.

The 1,200 V and above voltage rating segment is expected to register the highest CAGR of 10.5%. The shift toward high-voltage battery systems and long-haul HVDC corridors is making 1,200V+ IPMs indispensable for load leveling and rapid-charge EV architectures.

One of the primary drivers is the expansion of high-voltage direct current (HVDC) transmission systems across North America. According to the Edison Institute, HVDC projects under development in the U.S. and Canada are expected to add over 35 GW of transmission capacity by 2030, requiring advanced power modules rated at 1,200 V or higher. Also, the automotive sector is witnessing a shift toward 800 V battery architectures in electric vehicles, enabling faster charging and enhanced efficiency. With these trends gaining momentum, the 1,200 V and above segment is poised for sustained high-growth performance.

By Application Insights

The industrial application segment prevailed in the North America intelligent power module market, contributing 35.7% of total revenue in 2025. This dominance is attributed to the extensive use of IPMs in automation equipment, motor drives, robotics, and factory control systems across sectors such as manufacturing, logistics, and process industries.

The integration of intelligent power modules into variable frequency drives (VFDs) and servo drives enables real-time monitoring and dynamic load adjustments, improving operational efficiency while reducing energy consumption.

The automotive application segment is anticipated to grow at the fastest CAGR of 11.2%. This surge is primarily fueled by the rapid electrification of the transportation sector, particularly the increasing production and adoption of battery electric vehicles (BEVs) and plug-in hybrid electric vehicles (PHEVs). Similarly, Natural Resources Canada reported that EV registrations in Canada reached over 140,000 in 2025, up 60% from the previous year. Each modern EV utilizes several intelligent power modules in the traction inverter, onboard charger, and auxiliary systems, driving substantial demand for high-performance semiconductor solutions. The U.S. Department of Energy highlighted that silicon carbide (SiC)-based IPMs are increasingly being adopted in EVs for their superior thermal efficiency and reduced energy loss.

COUNTRY LEVEL ANALYSIS

The United States holds the dominant position in the North America intelligent power module market, accounting for a 75.8% of total regional revenue in 2025. This is because of a combination of strong industrial infrastructure, aggressive electrification initiatives, and significant investments in semiconductor manufacturing. The U.S. is home to major automotive and industrial automation hubs, which are key consumers of intelligent power modules. Also, the Bipartisan Infrastructure Law allocated $65 billion for grid modernization, further enhancing the demand for IPMs in grid-tied inverters and smart substations.

Canada's growth is primarily driven by its expanding renewable energy sector, rising electric vehicle adoption, and increasing investments in industrial automation and smart grid technologies. Companies such as Stellantis and Volvo have expanded their EV manufacturing operations in Ontario, necessitating greater use of intelligent power modules in drivetrain systems. In the renewable energy sector, the Canadian Renewable Energy Association noted that wind and solar installations reached a combined capacity of over 28 GW by the end of 2025, with IPMs playing a crucial role in power conversion and grid synchronization.

The Rest of North America, which includes Mexico and Central American territories, accounts for a notable share of the regional intelligent power module market in 2025. While relatively smaller in size, this segment is showing promising growth, particularly due to increasing foreign direct investment (FDI) in manufacturing, automotive production, and renewable energy projects.

KEY MARKET PLAYERS AND COMPETITIVE LANDSCAPE

Companies playing a prominent role in the North American intelligent power module market are

- Mitsubishi Electric Corp,

- ON Semiconductor Corp,

- Infineon Technologies AG,

- Fuji Electric Co Ltd,

- STMicroelectronics NV,

- Ideal Power Inc.

- Alpha & Omega Semiconductor Ltd,

- Semikron International,

- Sensitron Semiconductor,

- CISSOID.

The competition in the North America intelligent power module market is characterizeAmericanblend of established semiconductor giants and emerging innovators striving to capture a larger share of a rapidly evolving industry. With increasing demand from automotive, industrial automation, and renewable energy sectors, companies are focusing on differentiation through technological advancements, application-specific designs, and enhanced thermal and electrical performance. The market is witnessing intensified rivalry as manufacturers seek to integrate more intelligence into power modules, enabling real-time diagnostics, fault detection, and adaptive control features. Strategic positioning is further shaped by the need to comply with stringent safety and efficiency standards, prompting vendors to align their product roadmaps with evolving regulatory frameworks. Additionally, the growing emphasis on sustainable energy solutions and electrification trends is driving players to tailor their offerings for high-voltage applications, particularly in electric vehicles and grid modernization projects. As competition intensifies, companies are also expanding their regional footprint through localized manufacturing, channel partnerships, and direct engagement with end-users to strengthen brand presence and improve service delivery.

Top Players in the Market

Infineon Technologies AG

Infineon is a dominant player in the intelligent power module market, with a strong presence across North America. The company offers a broad portfolio of IPMs based on IGBT and silicon carbide (SiC) technologies, catering to automotive, industrial automation, and renewable energy sectors. Infineon’s innovation in high-efficiency power semiconductors has positioned it as a preferred supplier for electric vehicle manufacturers and industrial equipment providers. Its collaboration with major automakers and continuous investment in R&D have reinforced its leadership in delivering compact, high-performance modules tailored for advanced applications.

STMicroelectronics

STMicroelectronics plays a crucial role in shaping the intelligent power module landscape in North America through its advanced integration technologies and system-level solutions. The company specializes in producing IPMs that combine power switches with intelligent control features, making them ideal for consumer electronics, motor drives, and smart grid systems. With a focus on energy-efficient designs and robust thermal management, STMicroelectronics supports a wide range of industries seeking reliable and scalable power solutions. Its strategic partnerships with leading industrial and automotive firms further enhance its market influence.

Texas Instruments Incorporated

Texas Instruments (TI) contributes significantly to the growth of the intelligent power module market by offering highly integrated power management ICs and modules designed for precision and efficiency. TI's IPM solutions are widely used in industrial automation, robotics, and EV charging infrastructure across North America. The company emphasizes compact design, low power consumption, and real-time diagnostics, enabling customers to optimize performance while reducing system complexity. Through continuous innovation and a strong distribution network, Texas Instruments remains a key enabler of next-generation power electronics across multiple sectors.

Top Strategies Used by Key Players

One of the primary strategies employed by leading players in the North American intelligent power module market is product innovation and technology advancement. Companies continuously invest in R&D to develop more efficient, compact, and thermally optimized IPMs that meet evolving industry demands. This includes integrating wide-bandgap semiconductors like silicon carbide and gallium nitride into power modules for superior performance in electric vehicles and industrial applications.

Another key approach is strategic collaborations and partnerships. Market leaders engage in joint ventures with automobile manufacturers, industrial equipment producers, and semiconductor material suppliers to accelerate product development and ensure compatibility across diverse applications. These alliances also help companies align their offerings with regional regulatory standards and customer-specific requirements.

Lastly, expanding manufacturing and supply chain capabilities within North America is a critical strategy. To mitigate global supply chain disruptions and reduce lead times, key players are investing in localized production facilities and strengthening their regional distribution networks. This enables faster delivery, improved customer support, and greater responsiveness to market dynamics.

RECENT HAPPENINGS IN THE MARKET

- In February 2025, Infineon Technologies announced the launch of its new hybridPACK Dual Performance IGBT module specifically designed for electric vehicle traction inverters. This product aims to enhance efficiency and thermal performance in next-generation EVs, reinforcing Infineon’s position as a leading supplier in the automotive segment.

- In March 2025, STMicroelectronics entered into a long-term partnership with a major North American electric vehicle manufacturer to co-develop customized intelligent power modules for onboard chargers and DC-DC converters. This collaboration is expected to streamline power system integration and improve overall vehicle efficiency.

- In May 2025, Texas Instruments introduced an expanded portfolio of high-integration power management ICs designed for industrial motor drives and factory automation systems. The release strengthens TI’s foothold in the industrial segment by offering compact, high-efficiency solutions for intelligent power module developers.

- In June 2025, ON Semiconductor completed the expansion of its wafer fabrication facility in Oregon, enhancing local production capacity for silicon carbide-based intelligent power modules. This move is intended to reduce supply chain dependencies and support growing demand from Ethe V and renewable energy sectors.

- In July 2025, FujiElectricc partnered with a Canadian energy storage provider to deploy intelligent power modules in large-scale battery energy storage systems. This initiative is aimed at improving grid stability and supporting North America’s transition toward clean and resilient power infrastructure.

MARKET SEGMENTATION

This research on the North America intelligent power Module market has been segmented and sub-segmented into the following.

By Power Device

- IGBT

- MOSFET

By Voltage Rating

- 600 V To 1,199 V

- 1,200 V And Above

By Application

- Industrial

- Automotive

By Country

- The U.S.

- Canada

- Rest of North America

Frequently Asked Questions

Which industries drive demand for IPMs in North America?

Key industries include industrial automation, electric vehicles (EVs), HVAC systems, renewable energy (solar/wind), and consumer electronics.

Which countries in North America dominate the IPM market?

The United States holds the largest share due to strong industrial infrastructure, followed by Canada and Mexico.

Who are the major players in the North American IPM market?

Leading companies include Mitsubishi Electric, Infineon Technologies, ON Semiconductor, STMicroelectronics, Fuji Electric, and Texas Instruments.

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com