North America Intragastric Balloon Market Size, Share, Trends & Growth Forecast Report By Type (Single, Dual Triple), Filling Material, End-User and Country (The United States, Canada and Rest of North America), Industry Analysis From 2026 to 2034

North America Intragastric Balloon Market Size

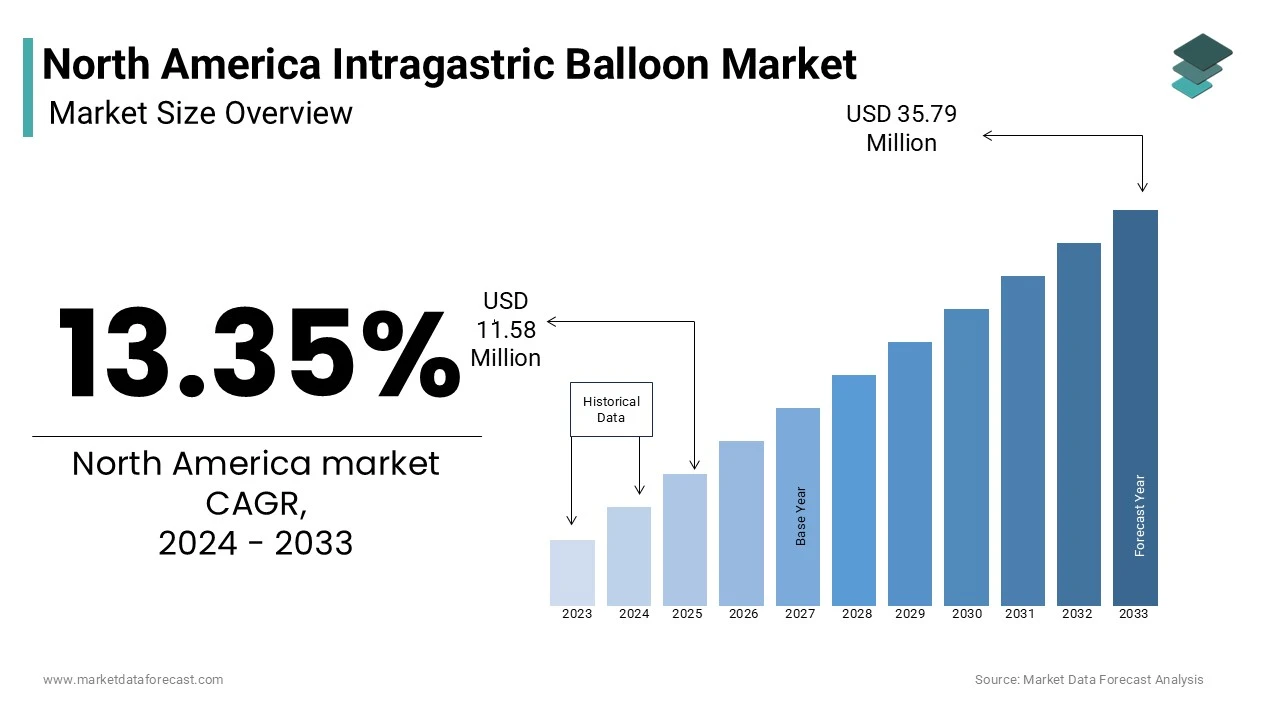

The North America Intragastric Balloon Market size was valued at USD 13.13 billion in 2025 and is anticipated to reach USD 14.88 billion in 2026 from USD 40.55 billion by 2034, growing at a CAGR of 13.35% during the forecast period from 2026 to 2034

Intragastric balloon therapy represents a minimally invasive bariatric intervention designed to facilitate weight loss through temporary gastric volume reduction and altered satiety signaling mechanisms. These medical devices consist of biocompatible, inflatable balloons that are endoscopically placed within the stomach cavity, where they occupy significant gastric volume and promote early satiation during meal consumption. The therapy typically involves balloon placement for six to twelve months, depending on the specific device type and clinical protocol, after which the device is removed via an endoscopic procedure.

The intragastric balloon market encompasses various device configurations including single-balloon systems, dual-balloon arrangements, and swallowable capsule-based solutions that eliminate the need for endoscopic placement procedures. The therapy mechanism operates through gastric distension, which activates stretch receptors and influences ghrelin hormone production, thereby modifying hunger signaling pathways.

MARKET DRIVERS

Rising Obesity Prevalence and Weight Management Demand

The escalating obesity epidemic across North America serves as the primary catalyst driving demand for intragastric balloon therapy, as healthcare systems and patients increasingly seek effective, minimally invasive weight management solutions. The fundamental shift in dietary patterns, sedentary lifestyles, and metabolic health challenges has created a substantial patient population seeking alternatives to traditional bariatric surgery. This prevalence has increased annually over the past decade, creating sustained demand for innovative weight management technologies. The demographic shift toward older adult populations, who often face surgical risks and comorbidities that preclude traditional bariatric procedures, has particularly favored intragastric balloon adoption. Insurance coverage expansion for obesity treatments, including intragastric balloon therapy, has further facilitated patient access and market growth.

Minimally Invasive Procedure Preference and Reduced Recovery Requirements

The inherent minimally invasive nature of intragastric balloon procedures represents a compelling driver for market adoption, as patients and healthcare providers increasingly prioritize interventions with reduced surgical risks, shorter recovery times, and lower complication rates. Unlike traditional bariatric surgeries that require general anesthesia, extensive surgical incisions, and prolonged hospitalization, intragastric balloon placement typically involves conscious sedation and outpatient procedures with same-day discharge capabilities. The reduced procedural complexity translates to significantly lower healthcare resource utilization, with average procedure costs lower than surgical alternatives. Additionally, the absence of permanent anatomical alterations appeals to patients seeking reversible weight management solutions that allow for lifestyle modification and gradual habit development. The reduced risk profile, makes intragastric balloon therapy suitable for broader patient populations including those with moderate comorbidities who might otherwise be excluded from surgical options.

MARKET RESTRAINTS

Limited Reimbursement Coverage and High Patient Out-of-Pocket Costs

The restricted reimbursement landscape for intragastric balloon therapy presents a significant barrier to widespread market adoption, as most insurance providers classify these procedures as elective or cosmetic rather than medically necessary interventions. The substantial out-of-pocket expenses required from patients create financial accessibility challenges for the broader eligible patient population. Medicare coverage remains particularly restrictive, with the Centers for Medicare and Medicaid Services indicating that intragastric balloon therapy is generally not covered except under specific investigational device protocols. Additionally, the temporary nature of treatment outcomes, with weight regain commonly occurring post-removal, raises questions regarding long-term cost-effectiveness that influence payer coverage decisions. The American Health Insurance Plans association indicates that insurers evaluate procedures based on sustained outcome data, which remains limited for intragastric balloon therapy beyond the initial treatment period. The requirement for comprehensive patient education, behavioral counseling, and follow-up care further increases total treatment costs and complexity, making reimbursement justification more challenging for payers seeking evidence-based coverage decisions.

Temporary Treatment Duration and Weight Regain Concerns

The inherently temporary nature of intragastric balloon therapy, with device removal required after 6-12 months, creates significant limitations regarding sustained weight management outcomes and long-term patient satisfaction. The fundamental treatment mechanism relies on temporary gastric volume reduction, which ceases upon device removal, often resulting in weight regain and reduced long-term efficacy perceptions among patients and healthcare providers. Many of patients experience significant weight regain within two years of balloon removal, diminishing the perceived value proposition compared to permanent surgical interventions. The requirement for repeated procedures to maintain weight loss outcomes creates additional financial and procedural burdens that limit patient acceptance and market expansion. Additionally, the temporary nature of treatment conflicts with patient expectations for permanent solutions, leading to dissatisfaction and reduced referral rates from healthcare providers. The psychological impact of weight regain can negatively affect patients mental health and motivation for continued weight management efforts. The lack of standardized protocols for post-removal weight maintenance and behavioral support further compounds the challenge of achieving sustained outcomes, limiting the therapy's appeal to both patients and referring physicians.

MARKET OPPORTUNITIES

Technological Advancement and Next-Generation Device Development

Technological innovation in intragastric balloon design and deployment methodologies presents substantial market opportunities through enhanced safety profiles, improved patient comfort, and extended treatment durations. Advanced materials science and engineering developments have enabled the creation of next-generation devices with superior biocompatibility, reduced complication rates, and enhanced patient tolerance during treatment periods. Many of recent intragastric balloon patents focus on material composition improvements and surface modification technologies that reduce gastric irritation and improve device longevity. The development of swallowable capsule-based balloon systems eliminates the need for endoscopic placement procedures, significantly reducing procedural complexity and patient anxiety associated with traditional placement methods. Additionally, smart balloon technologies incorporating wireless monitoring capabilities enable real-time gastric pH monitoring, temperature sensing, and patient compliance tracking that enhance clinical outcomes and provider confidence. The integration of drug-eluting surfaces and bioactive coatings provides additional therapeutic benefits beyond mechanical volume reduction, including ghrelin suppression and metabolic modulation effects. Furthermore, the development of adjustable volume systems allows for personalized treatment protocols based on individual patient responses and tolerance levels, creating opportunities for enhanced efficacy and reduced adverse events.

Expanding Clinical Indications and Preventive Healthcare Integration

The broadening scope of clinical applications for intragastric balloon therapy beyond traditional obesity treatment presents significant market expansion opportunities through integration with preventive healthcare initiatives and metabolic disease management protocols. Healthcare providers are increasingly recognizing the potential for intragastric balloon therapy to address pre-diabetic conditions, metabolic syndrome, and cardiovascular risk reduction in addition to weight management objectives. The integration of intragastric balloon therapy with comprehensive metabolic health programs, including nutritional counseling, exercise protocols, and behavioral modification support, enhances treatment outcomes and justifies broader insurance coverage considerations. Also, intragastric balloon therapy can reduce cardiovascular risk markers including blood pressure, cholesterol levels, and inflammatory markers during treatment periods. Additionally, the application of intragastric balloon therapy in preparation for major surgical procedures, organ transplantation eligibility, and fertility treatment optimization creates new market segments with distinct clinical value propositions. The development of pediatric applications and adolescent weight management protocols further expands the addressable market, representing a growing patient population requiring specialized intervention approaches.

MARKET CHALLENGES

Safety Concerns and Adverse Event Management

Safety considerations and adverse event management represent significant challenges for the North American intragastric balloon market, as serious complications can impact patient outcomes, provider confidence, and regulatory oversight of these medical devices. The gastrointestinal system's complex physiological responses to foreign body presence can result in serious adverse events including gastric perforation, intestinal obstruction, and device migration that require immediate medical intervention. Gastric ulceration and erosion complications occur in some of cases, necessitating device removal and additional medical treatment that can negatively impact patient satisfaction and treatment continuation rates. The rare but serious risk of balloon deflation and migration into the small intestine occurs in approximately 1-2% of cases, requiring emergency endoscopic retrieval procedures that can result in significant patient morbidity and healthcare costs. Provider training and competency requirements for safe device placement and management create additional implementation challenges, particularly in facilities with limited endoscopic expertise and emergency response capabilities. The psychological impact of adverse events on patient confidence and willingness to recommend the therapy to others can significantly affect market reputation and referral patterns, creating long-term challenges for market growth and acceptance.

Patient Selection Criteria and Clinical Suitability Limitations

The complex patient selection criteria and clinical suitability requirements for intragastric balloon therapy present significant implementation challenges that limit market accessibility and treatment success rates across diverse patient populations. Healthcare providers must carefully evaluate numerous medical, psychological, and anatomical factors to determine appropriate candidates, excluding substantial portions of the obese population who might otherwise benefit from therapy. The requirement for patient motivation and commitment to lifestyle modification programs creates additional selection challenges, as clinical success depends heavily on behavioral compliance and post-procedure adherence to dietary and exercise recommendations. Anatomical variations including large hiatal hernias, gastric diverticula, and previous surgical alterations can preclude safe device placement and increase complication risks, limiting the addressable patient population. Additionally, the exclusion of patients with certain medical conditions including severe liver disease, chronic kidney disease, and immunocompromised states creates further restrictions on market expansion. The requirement for comprehensive pre-procedure evaluations, including psychological assessments, nutritional counseling, and medical optimization, increases treatment complexity and costs while extending the time from initial consultation to procedure implementation. The variability in provider selection criteria and clinical protocols across different healthcare facilities can create inconsistent patient experiences and outcomes, potentially affecting market reputation and patient satisfaction levels.

SEGMENTAL ANALYSIS

By Type Insights

The single balloon systems segment was the dominant part in the North American intragastric balloon market by commanding a substantial portion of the total share in 2025. The primary driver behind single balloon systems' market dominance is their superior cost-effectiveness and enhanced economic accessibility compared to dual and triple balloon configurations. These systems typically cost less than multi-balloon alternatives while providing comparable clinical outcomes, making them particularly attractive for patients bearing significant out-of-pocket expenses. The reduced procedural complexity and shorter placement times associated with single balloon systems translate to lower healthcare facility costs and increased procedure throughput capabilities. Besides, the simplified device design reduces manufacturing costs and supply chain complexities, enabling more competitive pricing structures that benefit both providers and patients. Insurance coverage considerations also favor single balloon systems, as payers often view them as more cost-effective interventions with established safety profiles.

The extensive clinical experience and deep-rooted provider familiarity with single balloon systems represent another critical factor supporting their market dominance across North America. Decades of clinical use have created a robust ecosystem of trained healthcare professionals, established procedural protocols, and comprehensive safety guidelines that facilitate successful implementation and management. The extensive publication of clinical outcomes and safety data for single balloon configurations provides healthcare providers with confidence in treatment selection and patient counseling. Moreover, the standardized nature of single balloon procedures enables consistent training programs and competency assessments for new practitioners entering the field. The availability of comprehensive educational resources, including hands-on workshops and simulation training, further supports provider adoption and successful implementation of single balloon technologies.

The dual balloon systems segment is the fastest-growing in the North American intragastric balloon market and is exhibiting a CAGR of 12.4% from 2026 to 2034. The main catalyst for dual balloon systems' rapid market expansion is their demonstrated enhanced treatment efficacy and superior weight loss outcomes compared to single balloon alternatives. These systems utilize two separate balloons placed within the gastric cavity to achieve greater volume displacement and more pronounced satiety effects, resulting in improved clinical outcomes for patients seeking significant weight reduction. The increased gastric occupation provided by dual balloon systems creates more pronounced stretch receptor activation and hormonal response modulation, leading to enhanced satiety signaling and reduced caloric intake. Additionally, the dual balloon configuration allows for strategic placement optimization that can accommodate individual patient anatomical variations and maximize treatment effectiveness. The development of coordinated inflation and deflation protocols for dual balloon systems has improved patient tolerance and reduced adverse event rates, further supporting market acceptance and clinical adoption.

The integration of advanced technological features and innovative design elements in dual balloon systems represents a significant growth catalyst for this market segment. Modern dual balloon configurations incorporate sophisticated materials, enhanced safety mechanisms, and improved patient monitoring capabilities that address previous limitations and expand treatment accessibility. The development of radiofrequency identification tags and wireless pressure sensors enables real-time monitoring of balloon positioning and gastric environment conditions, providing healthcare providers with valuable clinical data for treatment optimization. Additionally, the introduction of dissolvable connecting tethers and independent balloon control mechanisms has improved patient comfort and reduced procedural complexity. The integration of drug-eluting surfaces that release ghrelin-suppressing compounds provides additional therapeutic benefits beyond mechanical volume reduction. The development of patient-specific sizing algorithms and customized treatment protocols based on individual anatomical characteristics has further enhanced the appeal and effectiveness of dual balloon systems.

By End User Insights

The hospitals segment was the prominent end-user in the North American intragastric balloon market and is commanding 65.5% of the total share in 2025. The key factor of hospitals' dominance in the intragastric balloon market is their comprehensive healthcare infrastructure and robust emergency response capabilities that ensure patient safety and optimal treatment outcomes. Hospital facilities provide the necessary resources, including advanced endoscopy suites, intensive care capabilities, and multidisciplinary healthcare teams, to manage complex procedures and potential complications effectively. The presence of 24-hour emergency departments and surgical backup capabilities provides critical safety nets for managing rare but serious complications including gastric perforation, device migration, and severe adverse reactions. Besides, hospital facilities typically employ specialized nursing staff trained in post-procedure monitoring and patient care, ensuring optimal recovery and complication prevention. The integration of electronic health records and comprehensive patient monitoring systems enables continuous tracking of treatment progress and early identification of potential issues.

The availability of multidisciplinary care teams and comprehensive treatment programs within hospital settings represents another critical factor supporting their market dominance in intragastric balloon therapy. Hospitals typically assemble specialized teams including gastroenterologists, bariatric specialists, nutritionists, psychologists, and nursing staff to provide holistic patient care throughout the treatment continuum. The integration of behavioral health services and lifestyle modification programs within hospital settings enables more effective long-term weight management outcomes compared to standalone procedural approaches. Additionally, hospitals often provide access to advanced imaging technologies, laboratory services, and specialist consultations that support comprehensive patient evaluation and ongoing care management. The presence of research capabilities and clinical trial participation opportunities within hospital settings attracts patients seeking cutting-edge treatment options and enhanced clinical oversight.

The ambulatory surgical centers segment is the fastest-growing end-user in the North American intragastric balloon market and is demonstrating a CAGR of 15.8% from 2026 to 2034. The key accelerator for ambulatory surgical centers' rapid market expansion is the growing patient preference for convenient, outpatient care settings that minimize disruption to daily activities and reduce healthcare system resource utilization. Modern patients increasingly seek streamlined healthcare experiences that provide effective treatment with minimal time commitment and rapid recovery periods. The convenience factor of same-day procedures and discharge, without overnight hospitalization requirements, appeals particularly to working professionals and caregivers who cannot afford extended time away from responsibilities. Additionally, the more personalized attention and reduced wait times typically associated with ambulatory centers enhance patient experience and treatment compliance. The development of specialized intragastric balloon programs within ambulatory settings has enabled centers to replicate hospital-level safety standards while maintaining operational efficiency and cost advantages. The trend toward consumer-driven healthcare and transparent pricing models has particularly favored ambulatory surgical centers that can offer competitive pricing and predictable cost structures for elective procedures.

The inherent cost efficiency and operational advantages of ambulatory surgical centers represent a significant growth catalyst for intragastric balloon procedure adoption in these settings. These facilities typically operate with lower overhead costs, streamlined staffing models, and optimized scheduling systems that enable more cost-effective procedure delivery compared to hospital environments. The focused nature of ambulatory centers allows for specialized equipment utilization and staff training that enhance procedural efficiency and reduce operational complexity. Additionally, the absence of hospital administrative overhead and complex billing structures enables more transparent pricing models that benefit both patients and referring physicians. The development of specialized intragastric balloon protocols and streamlined care pathways within ambulatory settings has reduced procedure times and improved patient throughput capabilities. The trend toward value-based care and cost containment initiatives has particularly favored ambulatory surgical centers that can demonstrate superior cost-effectiveness while maintaining high-quality outcomes and patient satisfaction levels

By Filling Material Insights

The saline filled balloons segment led the North American intragastric balloon market by accounting for 63.6% of the total share in 2025. The primary driver behind saline filled balloons' market dominance is their well-established safety profile and comprehensive regulatory acceptance that has been validated through decades of clinical use and extensive regulatory review processes. These systems have undergone rigorous testing and evaluation by regulatory bodies, resulting in broad market approval and healthcare provider confidence in their safe deployment and management. The extensive clinical database supporting saline filled balloons, encompassing a large number of patient-years of experience, provides healthcare providers with comprehensive safety information and risk management guidelines. Additionally, the biocompatibility and physiological compatibility of saline solution eliminates concerns regarding toxic reactions or systemic effects that might accompany alternative filling materials. The standardized nature of saline filling procedures enables consistent manufacturing processes and quality control measures that ensure product reliability and performance consistency.

The cost-effectiveness and manufacturing simplicity associated with saline filled balloon systems represent another critical factor supporting their market dominance across North America. The straightforward filling process and readily available materials enable efficient production methods and competitive pricing structures that benefit both manufacturers and healthcare providers. The absence of specialized gas handling equipment and pressurized filling systems reduces manufacturing complexity and facility requirements, enabling broader production capabilities and supply chain flexibility. Additionally, the stability and shelf-life characteristics of saline filled systems enable longer storage periods and reduced inventory management complexities compared to gas filled alternatives that may require specialized storage conditions. The compatibility of saline filling with standard medical device manufacturing practices and quality assurance protocols facilitates regulatory compliance and reduces time-to-market for new product introductions.

The gas filled balloons segment is the fastest-growing in the North America intragastric balloon market and is exhibiting a CAGR of 14.2% from 2026 to 2034. The main catalyst for gas filled balloons' rapid market expansion is their superior patient comfort profile and reduced gastric irritation compared to traditional saline filled alternatives. These systems utilize specialized gas mixtures that provide optimal volume displacement while minimizing gastric wall pressure and mechanical irritation that can cause patient discomfort during treatment periods. The lower density and compressibility characteristics of gas filled systems enable more physiological accommodation to gastric motility and positional changes, reducing mechanical stress on gastric tissues. Additionally, the uniform pressure distribution characteristics of gas filled balloons create more consistent gastric distension effects that enhance satiety signaling without focal pressure points that might cause localized irritation.

The development of advanced deployment capabilities and swallowable gas filled balloon technologies represents a significant growth catalyst for this market segment, eliminating the need for endoscopic placement procedures and expanding treatment accessibility to broader patient populations. These innovative systems utilize specialized gas filling mechanisms and capsule-based delivery methods that enable patient self-administration and reduce procedural complexity and associated risks. The elimination of conscious sedation requirements and specialized endoscopy equipment enables treatment delivery in diverse healthcare settings including primary care offices and ambulatory centers. Additionally, the development of timed-release filling mechanisms and bioabsorbable capsule materials has improved deployment reliability and reduced retrieval requirements. The trend toward patient-centered care and minimally invasive treatment options has particularly favored gas filled balloon technologies that provide enhanced convenience and reduced procedural burden for patients seeking weight management solutions.

REGIONAL ANALYSIS

United States Intragastric Balloon Market Insights

The United States maintained an overwhelming dominance in the North American intragastric balloon market by commanding a 92.1% of the total regional share. This commanding position is supported by the country's extensive healthcare infrastructure, robust medical device innovation ecosystem, and substantial patient population requiring weight management interventions. The United States' position as the largest healthcare market in North America naturally translates to significant medical device adoption and technological advancement opportunities.

The United States intragastric balloon market is characterized by mature healthcare delivery systems, extensive research and development capabilities, and significant investments in obesity treatment technologies and clinical research initiatives. The country's diverse healthcare landscape, encompassing academic medical centers, community hospitals, and specialized ambulatory care facilities, creates substantial demand for advanced weight management solutions. Additionally, the presence of major medical device manufacturers including Apollo Endosurgery, ReShape Lifesciences, and Allergan within domestic borders further strengthens the market ecosystem. Regional variations exist, with states like California, Texas, and Florida leading in new procedure volumes due to population density and healthcare concentration trends.

Canada Intragastric Balloon Market Insights

Canada represents a key market in North America for intragastric balloon therapy. The country's position is strengthened by its universal healthcare system, significant obesity prevalence, and growing emphasis on innovative treatment approaches for chronic disease management. Canada's healthcare integration with international standards and regulatory frameworks has enhanced its importance in regional medical device markets.

The Canadian intragastric balloon market is driven by the country's universal healthcare system approach to obesity treatment, expanding private healthcare sector, and ongoing clinical research initiatives focused on weight management technologiesCanada's universal healthcare system covers select obesity treatments, though coverage varies by province, creating opportunities for private pay market expansion and hybrid treatment models. Provincial initiatives, particularly in Ontario and British Columbia, focus on expanding access to innovative weight management solutions and reducing obesity-related healthcare costs. Canada's participation in North American clinical research networks and medical device evaluation programs further supports market expansion through coordinated development initiatives and technology transfer opportunities.

COMPETITIVE LANDSCAPE

The North American intragastric balloon market exhibits dynamic competition characterized by the presence of established medical device companies alongside specialized obesity treatment firms and emerging technology developers. Market leaders compete primarily on technological innovation, clinical evidence, and comprehensive service offerings rather than solely on price. The competitive landscape is shaped by continuous technological advancement, with digital health integration and patient-centric solution development becoming key differentiators. Companies invest heavily in developing next-generation balloon technologies and integrated treatment platforms that address safety concerns and improve patient outcomes. Healthcare system relationships play a crucial role, with long-term contracts and strategic partnerships being common. The market also experiences competition from new entrants focusing on innovative deployment methods and advanced materials technologies. Service capabilities, including clinical support, training programs, and patient management services, have become critical competitive factors. Regulatory compliance and safety track records significantly influence market positioning and healthcare provider selection decisions, creating barriers for new market entrants while providing stability for established players.

KEY MARKET PLAYERS

The key players in the North American Intragastric Balloon Market include

- Allurion Technologies

- Apollo Endosurgery

- ReShape Lifesciences

- Obalon Therapeutics

- Spatz Medical

- Evoke Surgical

- G S Medical

- Medtronic

- Allergan

Top Players in the North America Intragastric Balloon Market

Apollo Endosurgery maintains a prominent position in the North American intragastric balloon market through its comprehensive portfolio of minimally invasive weight management solutions and commitment to technological innovation. The company's extensive product range encompasses both traditional endoscopically placed balloons and advanced swallowable capsule-based systems that eliminate the need for procedural sedation. Their Apollo Integrated Weight Management platform incorporates sophisticated device technologies with comprehensive patient support programs and digital health monitoring capabilities. Apollo has consistently invested in research and development to create next-generation balloon systems with enhanced safety profiles and improved patient outcomes. The company's strong global presence and localized clinical support network enable rapid response to healthcare provider requirements and patient needs. Their focus on evidence-based clinical research and regulatory compliance has positioned them as a trusted partner for healthcare systems seeking reliable weight management solutions.

ReShape Lifesciences ReShape Lifesciences has established itself as a key player in the North American intragastric balloon market through innovative dual balloon technology and comprehensive weight management solutions. The company specializes in developing advanced balloon systems that provide enhanced gastric volume occupation and improved satiety signaling mechanisms. Their proprietary dual balloon design incorporates sophisticated filling and monitoring technologies that optimize treatment efficacy while maintaining patient safety and comfort. ReShape's commitment to developing patient-centric solutions has resulted in successful clinical outcomes and strong healthcare provider relationships. The company's strong focus on clinical research and evidence-based treatment protocols has enabled successful market penetration and long-term customer loyalty. Their integrated approach to weight management combines device therapy with behavioral support and nutritional counseling programs. ReShape's comprehensive service network and training programs support healthcare provider success and patient treatment optimization.

Allergan (AbbVie) Allergan, now part of AbbVie, holds a significant position in the North American intragastric balloon market through its established pharmaceutical heritage and comprehensive medical device portfolio. The company's intragastric balloon offerings integrate seamlessly with their broader aesthetic and weight management product lines, creating synergistic treatment approaches for healthcare providers. Their commitment to developing integrated weight management solutions encompasses both device-based interventions and pharmaceutical adjunct therapies that enhance overall treatment outcomes. Allergan's extensive global distribution network and strong brand recognition enable rapid market penetration and healthcare provider adoption. The company's robust clinical research infrastructure supports comprehensive safety and efficacy studies that build confidence among medical professionals and regulatory bodies. Their focus on patient education and support programs has established them as a trusted partner for comprehensive weight management initiatives. Allergan's commitment to regulatory compliance and quality assurance has positioned them as a reliable supplier in the competitive intragastric balloon therapy market.

Top Strategies Used by Key Market Participants

Clinical Research and Evidence-Based Development Leading players in the North American intragastric balloon market actively pursue comprehensive clinical research strategies focused on generating robust evidence supporting the safety, efficacy, and long-term outcomes of their device technologies. These initiatives encompass multi-center randomized controlled trials, post-market surveillance studies, and comparative effectiveness research that build healthcare provider confidence and support regulatory approvals. Companies invest heavily in developing standardized clinical protocols, patient selection criteria, and outcome measurement methodologies that enhance treatment consistency and reproducibility. The focus on long-term follow-up studies and real-world evidence generation enables manufacturers to demonstrate sustained benefits and address weight concerns regain and treatment durability. Collaborative research partnerships with academic medical centers and research institutions accelerate innovation and provide access to diverse patient populations and clinical expertise. Publication of peer-reviewed research findings and presentation at major medical conferences enhances scientific credibility and thought leadership positioning in the marketplace.

Integrated Solution Development and Digital Health Integration Major market participants emphasize integrated solution development strategies that combine device technologies with comprehensive patient support programs, digital health monitoring capabilities, and behavioral intervention components. These approaches involve extensive customer engagement to understand healthcare provider workflow requirements and patient treatment journey needs. Companies establish dedicated digital health teams that work closely with clinical partners to develop connected device platforms, mobile applications, and remote monitoring systems that enhance treatment outcomes and patient engagement. The development of artificial intelligence-powered analytics and predictive modeling capabilities enables personalized treatment protocols and early intervention strategies for potential complications. Integration with electronic health records and healthcare system platforms facilitates seamless workflow integration and comprehensive patient data management. Regional customization capabilities allow manufacturers to adapt solution components to local market requirements, regulatory standards, and cultural preferences while maintaining global technology platforms.

Strategic Partnerships and Healthcare System Integration.n Key players pursue strategic partnership strategies that involve collaboration with healthcare systems, bariatric centers, and integrated delivery networks to enhance market penetration and treatment accessibility. These partnerships enable access to established patient referral networks, shared clinical expertise, and coordinated care delivery models that improve treatment outcomes and patient satisfaction. Collaborations with insurance providers and managed care organizations facilitate coverage expansion and reimbursement pathway development that increase patient access and market adoption. Joint development initiatives with technology companies and software providers accelerate innovation in digital health integration and connected care solutions. Geographic partnerships and distribution agreements enable market expansion into new regions while maintaining local presence and support capabilities. Strategic alliances with professional medical societies and clinical guideline development organizations enhance scientific credibility and treatment standardization efforts that support broader market acceptance and adoption.

RECENT MARKET DEVELOPMENTS

- In March 2024, Apollo Endosurgery received FDA approval for its next-generation swallowable intragastric balloon system featuring wireless monitoring capabilities and extended treatment duration protocols for North American market deployment.

- In December 2023, ReShape Lifesciences announced a strategic partnership with Teladoc Health to integrate remote patient monitoring and virtual consultation capabilities into their dual balloon weight management platform across North American healthcare systems.

- In October 2023, Allergan (AbbVie) acquired Obalon Therapeutics' assets to expand its intragastric balloon portfolio and enhance its integrated weight management solution offerings in the North American market.

- In July 2023, Apollo Endosurgery launched its Apollo Integrated Digital Platform, a comprehensive cloud-based patient management system that connects healthcare providers with patients throughout the intragastric balloon treatment journey in North America.

- In May 2023, ReShape Lifesciences received Health Canada approval for their advanced dual balloon system with smart filling technology and received strategic investment from a major Canadian healthcare investment firm to expand their North American manufacturing capabilities.

MARKET SEGMENTATION

By Type

- Single

- Dual

- Triple

By Filling Material

- Gas Filled

- Saline Filled

By End User

- Hospitals

- Ambulatory Surgical Centers

- Others

By Country

- U.S.

- Canada

- Rest of North America

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com