North America Medical Suction Devices Market Research Report By Type, Application, Portability, End User, Country (U.S., Canada & Rest of North America) - Industry Analysis, Size, Share, Trends & Growth Forecast (2026 to 2034)

North America Medical Suction Devices Market Size

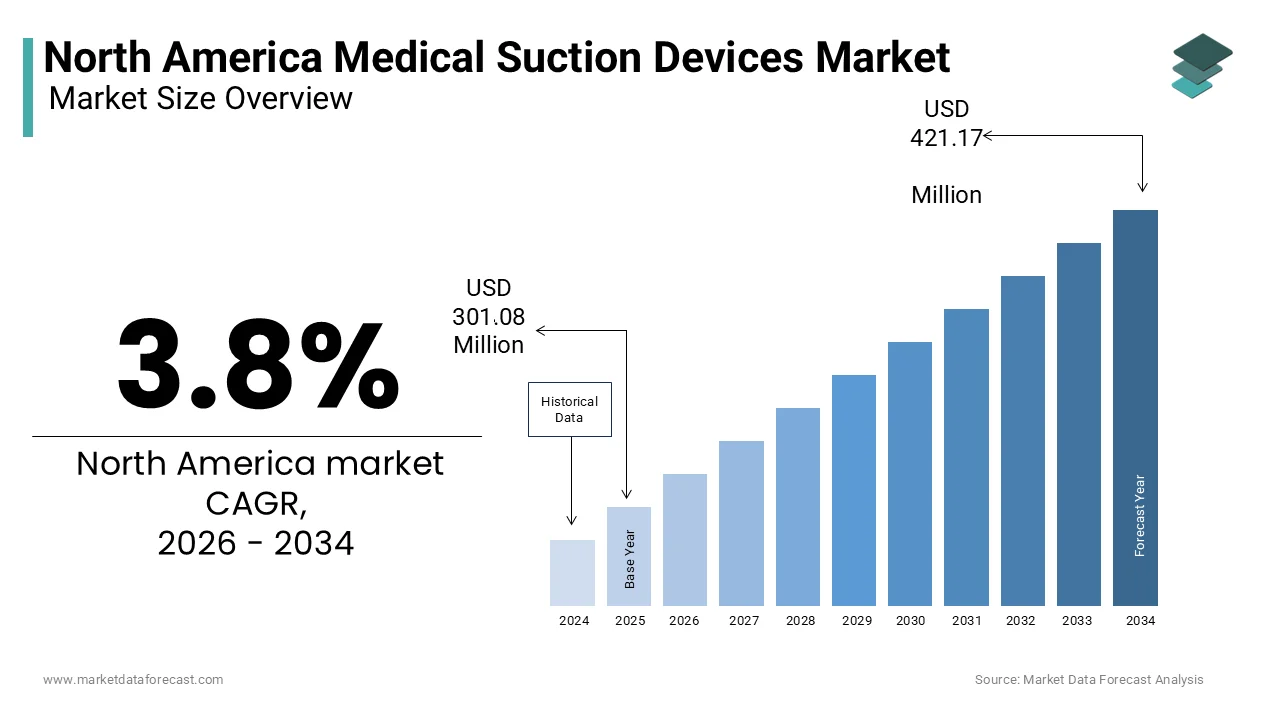

The North America Medical Suction Devices Market was valued at USD 301.08 million in 2025, is expected to have 3.8 % CAGR from 2026 to 2034, and be worth USD 421.17 million by 2034 from USD 312.56 million in 2026.

Medical suction devices, also known as aspirators, are vital medical instruments used to remove obstructions, such as mucus, saliva, blood, or other secretions, from a patient's airway or a surgical site. These devices range from portable battery-operated units utilized in emergency settings to large stationary systems integrated into hospital infrastructure. The region maintains its position as a dominant global hub due to sophisticated healthcare infrastructure and high adoption rates of advanced medical technologies. In 2024, the United States alone recorded national health expenditures reaching 5.3 trillion dollars, reflecting the substantial financial capacity to support advanced medical equipment procurement, according to data from the Centers for Medicare and Medicaid Services. Chronic lower respiratory diseases remain a leading cause of mortality, with chronic obstructive pulmonary disease accounting for the vast majority of these deaths annually in the United States, as per statistics from the Centers for Disease Control and Prevention. This high disease burden necessitates reliable suction solutions across intensive care units and emergency departments. Furthermore, the volume of surgical procedures continues to escalate, driving consistent demand for effective fluid management systems during operations. As per the Canadian Institute for Health Information, total private sector health expenditures are projected to continue their upward trend, indicating sustained investment in health services and essential medical devices. The market dynamics are heavily influenced by the aging population and the rising prevalence of conditions requiring respiratory support, ensuring sustained relevance for suction technology in clinical environments.

MARKET DRIVERS

Rising Prevalence of Chronic Respiratory Diseases

The increasing incidence of chronic respiratory conditions contributes to the expansion of the North American medical suction devices market. Chronic Obstructive Pulmonary Disease affects millions of individuals and creates an urgent need for airway clearance to prevent life-threatening complications. According to the Centers for Disease Control and Prevention, the prevalence of diagnosed chronic obstructive pulmonary disease among adults aged 18 and older stands at 3.8 percent, with women exhibiting a slightly higher rate of 4.1 percent compared to men. This widespread condition often leads to excessive mucus production that obstructs airways and requires frequent suctioning to maintain adequate oxygenation levels. The significant impact of chronic respiratory conditions is reflected in their status as a leading cause of death nationally, affecting millions of individuals who have received a formal medical diagnosis. Hospitals and long-term care facilities must equip themselves with high-performance suction units to manage these patients effectively during acute exacerbations. International respiratory health organizations point out that mortality rates for chronic lung conditions remain a challenge in major population centers, driving a continuous need for advanced medical intervention tools. The growing geriatric population further amplifies this demand since older adults are disproportionately susceptible to respiratory failures. Healthcare providers are increasingly investing in portable and high-efficiency suction devices to address the needs of this expanding patient demographic in both institutional and home care settings.

Surge in Surgical Procedure Volumes

A significant increase in the number of surgical interventions performed across the region is further propelling the growth of the North America medical suction devices market. Surgical procedures invariably generate blood and fluids that must be cleared immediately to ensure visibility for surgeons and safety for patients. The healthcare sector in North America supports a massive market for surgical procedures, illustrating an immense scale of clinical activity that requires extensive supportive equipment and technology. This voluminous activity spans elective surgeries, emergency trauma responses, and complex oncological resections where precise fluid management is non-negotiable. As per sources, the United States leads the region in surgical volume due to its extensive network of specialized hospitals and ambulatory surgical centers. The shift towards minimally invasive techniques has not diminished the need for suction but rather increased the requirement for specialized low-profile devices compatible with laparoscopic and endoscopic tools. National data shows that a substantial portion of total health spending is directed toward hospital and physician services, which provide the necessary funding for the acquisition of essential surgical supplies and medical devices. The rise in bariatric and orthopedic surgeries among the aging population further contributes to this upward trend. Manufacturers are responding by developing devices with adjustable suction pressures and enhanced filtration systems to meet the rigorous demands of modern operating rooms. This sustained growth in surgical volumes ensures a steady and expanding market for advanced medical suction technologies.

MARKET RESTRAINTS

Stringent Regulatory Compliance Requirements

Rigorous regulatory frameworks imposed by government agencies are a substantial restraint on the rapid deployment and innovation within the North American medical suction devices market. Manufacturers must navigate complex approval processes that can delay product launches and increase development costs significantly. The Food and Drug Administration classifies most suction devices as Class II medical devices, requiring 510(k) clearance to demonstrate safety and efficacy before they can enter the market according to federal regulatory guidelines. Recent enforcement actions highlight the severity of these regulations, as seen when the FDA issued warning letters to companies marketing unauthorized suction rescue devices in 2025. These strict compliance measures ensure patient safety but often create bottlenecks for smaller enterprises lacking the resources to conduct extensive clinical trials. As per regulatory updates, the Code of Federal Regulations Title 21 Parts 800 to 898 outlines exhaustive standards that manufacturers must adhere to regarding design controls and sterilization protocols. The time required to secure approval can extend beyond 12 months, during which competitors may capture market share with existing compliant products. Additionally, post-market surveillance requirements mandate continuous reporting of adverse events, adding to the operational burden. The import alerts issued in October 2025 against multiple unauthorized anti-choking suction devices illustrate the zero-tolerance approach of regulators towards non-compliant products. Such stringent oversight, while necessary for public health, inevitably slows down the pace of technological introduction and limits market agility for new entrants.

Acute Shortage of Healthcare Professionals

The persistent deficit of skilled healthcare workers across the region slows down the optimal utilization and maintenance of advanced devices in the North American medical suction devices market. Effective operation of sophisticated suction equipment requires trained personnel who can manage settings, troubleshoot issues, and ensure proper hygiene protocols. Studies indicate a significant deficit of registered nurses in the near future, resulting in a staffing gap that could impact the ability of healthcare facilities to manage complex medical technology. This scarcity forces hospitals to rely on less experienced staff or overtime workers who may not be fully proficient with complex device functionalities. Research shows that a vast segment of the population lives in regions designated as having a shortage of primary care professionals, which places additional pressure on the existing healthcare infrastructure and resources. The lack of adequate staffing leads to delayed maintenance of suction units and potential misuse, which can compromise patient outcomes and increase liability risks. Sources suggest a substantial shortfall of doctors over the next decade, which may further complicate the efficient management and utilization of high-technology medical devices. Facilities often postpone the acquisition of new advanced models because they lack the human capital to operate them safely. This workforce crisis acts as a dampener on market growth despite the availability of technologically superior products. The inability to staff positions adequately means that even available devices may sit unused or be operated below their full potential, limiting overall market penetration.

MARKET OPPORTUNITIES

Expansion of Home Healthcare Services

The rapid proliferation of home healthcare services is shifting care from hospitals to residential settings. This shift offers a lucrative opportunity for the North American medical suction devices market. Patients with chronic respiratory conditions increasingly prefer receiving treatment in the comfort of their homes, driving demand for portable, user-friendly suction units. The transition necessitates the development of compact, battery-operated devices that patients or caregivers can operate without extensive medical training. Manufacturers have the opportunity to innovate by creating lightweight devices with intuitive interfaces and long-lasting battery life to cater to this decentralized care environment. The aging population prefers aging in place, which further accelerates the need for reliable home-based respiratory support systems. Companies that focus on designing durable and easy-to-clean suction devices for home use will capture significant market share. This trend represents a strategic avenue for growth as the healthcare system continues to decentralize services to reduce hospital congestion and costs.

Technological Advancements in Device Portability

Innovations in material science and battery technology are revolutionizing the medical suction devices market. These advancements offer enhanced portability and efficiency. Modern developments allow for the creation of ultra-lightweight devices that do not compromise on suction power, making them ideal for emergency response and transport scenarios. Studies note that advancements in suction technology are poised to revolutionize portable medical devices by enhancing their efficiency, reliability, and user friendliness, according to technical industry reviews. The integration of smart sensors and digital monitoring capabilities enables real-time tracking of suction pressure and battery status, improving clinical decision-making. As per sources, manufacturers are developing innovative products with improved suction power and battery-operated options to cater to diverse clinical needs. These technological leaps address previous limitations regarding device bulkiness and noise levels, thereby expanding their applicability in sensitive environments like neonatal care. The push for miniaturization allows for devices that can be easily carried by paramedics or used in remote locations with limited power access. Innovations in filtration systems also reduce the risk of cross-contamination, a critical factor in infection control. Companies leveraging these technological breakthroughs can differentiate their offerings and command premium pricing in a competitive landscape. This focus on portability and smart features aligns perfectly with the evolving demands of modern healthcare providers seeking versatile and efficient solutions.

MARKET CHALLENGES

High Cost of Advanced Equipment

Acquiring and maintaining advanced medical suction devices is prohibitively expensive. This poses a significant challenge for smaller clinics and rural hospitals within the North American medical suction devices market. State-of-the-art units equipped with digital controls, variable pressure settings, and advanced filtration systems often carry price tags that strain limited budgets. The financial burden is compounded by the need for regular maintenance, replacement of disposable canisters, and periodic calibration to ensure accuracy. As per studies, the high capital expenditure required for such equipment can delay upgrades and force facilities to rely on outdated technology that may be less efficient or safe. Smaller practices operating on thin margins find it difficult to justify the investment when cheaper, albeit less feature-rich, alternatives exist in the market. The rising cost of raw materials and components further inflates the final price of these devices, making them less accessible to budget-constrained buyers. Healthcare systems facing financial pressures may prioritize other critical investments over suction equipment, viewing it as a commodity rather than a strategic asset. This cost barrier limits the adoption of the latest innovations and slows down the overall modernization of suction capabilities across the region. Consequently, a divide emerges between well-funded urban centers and under-resourced rural areas in terms of access to high-quality suction technology.

Complexity of Integration with Existing Systems

The difficulty in integrating new medical suction devices with legacy hospital infrastructure and electronic health record systems is a serious obstacle to the North American medical suction devices market expansion. Many healthcare facilities operate with older infrastructure that lacks the compatibility required for modern smart suction units featuring data connectivity and automated logging. The incompatibility forces IT departments to invest additional resources in custom interfaces or middleware, increasing the total cost of ownership and implementation time. Clinicians may resist adopting new devices if they disrupt established workflows or require extensive retraining to interface with existing digital ecosystems. The fragmentation of the medical device market means that a single hospital might deal with multiple vendors, each with proprietary software that does not communicate effectively with others. This siloed environment prevents the realization of fully integrated smart hospital concepts where suction data could inform broader patient care strategies. The complexity of ensuring cybersecurity for connected devices adds another layer of difficulty, as hospitals must guarantee that new equipment does not introduce vulnerabilities to their networks. Interoperability standards need to become more universal. Until then, the full potential of advanced suction technologies will remain unrealized in many complex healthcare environments.

REPORT COVERAGE

| REPORT METRIC | DETAILS |

| Market Size Available | 2025 to 2034 |

| Base Year | 2025 |

| Forecast Period | 2026 to 2034 |

| Segments Covered | By Portability, Type, Application, End User, and Region. |

| Various Analyses Covered | Global, Regional, and Country-Level Analysis, Segment-Level Analysis, Drivers, Restraints, Opportunities, Challenges; PESTLE Analysis; Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

| Countries Covered | The United States Canada Rest of North America |

| Market Leaders Profiled | Allied Healthcare Products Inc., ATMOS MedizinTechnik GmbH & Co. KG, Drive Medical, INTEGRA Biosciences, Medela Holding AG, Medicop, Precision Medical, Inc., SSCOR, Inc., ZOLL Medical Corporation, Weinmann Geräte für Medizin GmbH + Co. KG, Laerdal Medical, MG Electric Ltd (Colchester), Labconco Corporation, Welch Vacuum, Amsino International Inc., and Olympus Corporation.

|

SEGMENTAL ANALYSIS

By Portability Insights

The wall-mounted suction devices segment maintained the prominent share of 58.9% of the North America medical suction devices market in 2025. This prominence of the segment is attributed to its ubiquitous presence in hospital infrastructure, where continuous and reliable power is available. The main driver for this segment is the extensive integration of these units into the critical care infrastructure of major medical facilities. Hospitals require constant suction capabilities for intensive care units and operating theaters where patient stability depends on uninterrupted fluid removal. These systems offer higher suction pressure consistency compared to portable alternatives, which is vital for complex surgical procedures and trauma care. The initial capital investment for installing central vacuum systems is high, but the long-term operational cost is lower than maintaining thousands of individual portable units. This economic efficiency, combined with the regulatory requirement for backup suction sources in every patient room,m solidifies the position of wall-mounted devices as the backbone of institutional respiratory care. Strict regulatory mandates regarding hospital design and safety protocols further propel the dominance of wall-mounted suction devices. Building codes and healthcare facility guidelines often stipulate that specific areas, such as operating rooms and emergency departments,s must have hardwired suction outlets that connect to a central vacuum source. These regulations ensure that during power outages or equipment failures, the central system remains operational or has dedicated backup mechanisms that portable units cannot match in scale. Consequently, new hospital constructions and renovations strictly adhere to these codes, ensuring a steady demand for wall-mounted installations. The inability of handheld or portable units to satisfy these foundational safety requirements for inpatient care cements the leading status of the wall-mounted segment in the overall market volume.

The handheld suction devices segment is likely to experience the fastest CAGR of 6.8% from 2026 to 2034 due to the shift towards decentralized care and the need for immediate response tools in non-traditional settings. Besides, the burgeoning volume of emergency medical service calls acts as a potent catalyst for the adoption of handheld suction units. Paramedics and first responders require compact, lightweight devices that can be carried into diverse environments ranging from private homes to accident scenes. Handheld devices allow responders to clear airways instantly upon arrival without relying on vehicle-mounted systems that may be inaccessible in tight spaces. The trend towards faster response times and on-scene stabilization necessitates tools that enhance mobility and speed. Furthermore, the rise in community paramedicine programs, where providers visit patients at home for acute issues, further boosts the requirement for easily transportable suction technology that fits into a standard medical bag. The increasing prevalence of acute care delivery within the home environment significantly fuels the growth of the handheld segment. Patients recovering from surgeries or managing chronic conditions increasingly receive skilled nursing care at home, where wall-mounted systems are unavailable. Handheld suction devices provide the necessary functionality for nurses to manage secretions and prevent aspiration in a residential setting without the bulk of larger machines. The convenience of cordless operation allows caregivers to move freely around the patient, improving the quality of care and reducing the risk of trips or falls associated with cords. Manufacturers are responding by enhancing battery life and suction power in smaller form factors, making these devices the preferred choice for the rapidly expanding home care workforce.

By Type Insights

The AC-powered devices segment was the largest segment in the North American market and occupied a 52.1% share in 2025. This supremacy of the segment is credited to its role as the standard for high volume, continuous use in established healthcare facilities. The unparalleled reliability of AC-powered units during lengthy and complex surgical interventions is the foremost driver of their market leadership. These devices draw continuous power from the electrical grid, eliminating the risk of battery depletion during critical moments of an operation. AC-powered suction pumps provide consistent negative pressure levels that do not fluctuate, which is essential for maintaining a clear surgical field and ensuring patient safety. The ability to run continuously without downtime for recharging makes these units indispensable for busy surgical centers and trauma bays. Hospitals prioritize these systems because the cost of a power failure during surgery far outweighs the initial investment in robust AC infrastructure. This dependency on uninterrupted power for high-stakes medical procedures ensures that AC-powered devices remain the cornerstone of institutional suction capabilities. Long-term cost efficiency serves as a major factor sustaining the dominance of AC-powered devices in large healthcare institutions. While the upfront installation cost involving electrical wiring and central vacuum connections is significant, the operational expenses are considerably lower than maintaining vast fleets of battery-dependent units. AC-powered units typically have longer lifespans and fewer moving parts subject to wear compared to the rechargeable components of battery-operated models. The Centers for Medicare and Medicaid Services reimbursement models encourage hospitals to optimize operational costs, making the durability of AC units an attractive financial proposition. Furthermore, the energy consumption of modern AC suction pumps has decreased due to improved motor efficiency, reducing the utility burden on facility budgets. This economic advantage, combined with the reliability factor, ensures that AC-powered devices remain the default choice for the majority of fixed medical installations across the region.

The battery-powered devices segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 7.4% during the forecast period, owing to advancements in lithium-ion technology and the escalating demand for mobility in diverse care settings. Breakthroughs in lithium-ion battery chemistry have revolutionized the performance capabilities of battery-powered suction devices, driving their rapid adoption. Modern batteries offer higher energy density, allowing devices to operate for extended periods on a single charge while maintaining strong suction pressure. The technological leap addresses the historical limitation of battery life that hindered the use of portable units in prolonged care scenarios. Manufacturers are integrating smart battery management systems that provide real-time status updates, preventing unexpected power loss. The reduction in battery weight also contributes to the overall portability of the device, making it easier for clinicians to carry. These technical enhancements have transformed battery-powered units from backup options into primary tools for many clinical applications, fueling their accelerated market expansion. The exceptional versatility of battery-powered devices in transport and ambulatory care settings is a key driver of their fast growth rate. These units enable seamless patient movement from emergency rooms to imaging suites or operating theaters without disconnecting from suction support. Battery-powered suction eliminates the logistical challenges of finding wall outlets or managing extension cords during these transitions. Additionally, the rise of ambulatory surgical centers, which now perform a significant percentage of outpatient procedures, favors battery-operated equipment due to flexible room configurations that may lack extensive wall vacuum infrastructure. The freedom from tethered power sources allows for greater flexibility in clinic layouts and emergency response setups. This adaptability to dynamic healthcare environments positions battery-powered devices as the fastest evolving segment in the market.

By Application Insights

In 2025, the surgical applications segment led the North America medical suction devices market and captured a 48.9% share in 2025 because of the absolute necessity of fluid management in virtually every invasive procedure performed. Apart from these, the sheer volume of surgical procedures conducted across North America is the primary engine driving the dominance of the surgical application segment. Every operation, from minor outpatient interventions to major organ transplants, requires efficient suction to remove blood, irrigation fluids, and smoke from cauterization. The high frequency of use ensures that surgical suction devices are among the most utilized tools in any operating room. The complexity of modern surgeries, including minimally invasive and robotically assisted procedures, has increased the precision requirements for suction devices, leading to frequent upgrades and replacements. The critical nature of maintaining a clear visual field for surgeons means that suction failure is not an option, driving hospitals to invest in high-quality dedicated surgical units. This relentless procedural volume secures the top position for surgical applications in the market hierarchy. Rigorous infection control protocols in operating theaters further solidify the leading status of surgical suction applications. The removal of contaminated fluids is a critical step in preventing surgical site infections, which are a major concern for healthcare regulators and providers. Surgical suction devices are designed with specialized filters and closed collection systems to contain pathogens and protect staff from exposure to bloodborne diseases. Hospitals invest heavily in surgical-grade suction units that comply with these regulations to avoid penalties and ensure patient safety. The continuous evolution of sterilization standards and the push for zero infection rates in surgeries drive the ongoing demand for specialized surgical suction technology. This regulatory and safety imperative ensures that the surgical segment remains the largest consumer of medical suction devices.

The airway clearing application segment is expected to exhibit a noteworthy CAGR of 7.1% between 2026 and 2034. This rapid growth of the segment is fueled by the rising burden of respiratory diseases and the expanding scope of prehospital and home care. Besides, the increasing incidence of respiratory distress syndromes and chronic lung conditions is a major catalyst for the rapid growth of the airway-clearing segment. Conditions such as pneumonia, chronic obstructive pulmonary disease, and severe asthma attacks often result in excessive secretions that compromise breathing and require immediate suction intervention. The aging population is particularly vulnerable to these conditions, leading to a higher frequency of emergency department visits and hospital admissions where airway suctioning is a primary intervention. Besides, the growing awareness of the importance of early airway management in improving survival rates has led to wider deployment of suction devices in various care settings. This rising disease burden creates a sustained and growing demand for equipment specifically designed for efficient and gentle airway clearing. The formal integration of advanced airway clearing techniques into standard emergency response protocols is driving the rapid expansion of this segment. Emergency medical technicians and paramedics are increasingly trained and equipped to perform suctioning as a first-line intervention for patients with compromised airways. Recent updates to cardiopulmonary resuscitation guidelines by the American Heart Association emphasize the importance of clearing the airway before ventilation, reinforcing the need for reliable suction equipment in every emergency kit. The expansion of community paramedicine programs also brings these capabilities into homes and long-term care facilities, broadening the user base beyond traditional hospitals. This systemic embedding of suctioning into emergency care workflows ensures a robust and accelerating demand for airway-clearing applications.

By End User Insights

The hospitals and clinics segment dominated the North America medical suction devices market and accounted for a 62.3% share in 2025. This dominance of the segment is driven by the concentration of acute care services and the high density of medical procedures within these facilities. The concentration of intensive care units and surgical theaters within hospitals and clinics creates an unparalleled demand for medical suction devices. These facilities serve as the primary hubs for treating critically ill patients who require constant respiratory support and fluid management. A single large hospital may utilize hundreds of suction points across its various departments, from the emergency room to the neonatal intensive care unit. The complexity of cases handled in these settings, including trauma and major surgeries, requires high-capacity and reliable suction systems that only institutional settings can fully utilize. The sheer scale of patient throughput in hospitals ensures that they remain the largest consumers of suction technology, dwarfing other end-user segments in terms of volume and value. Stringent regulatory accreditation requirements and adequate staffing levels in hospitals and clinics further cement their position as the leading end users. Accreditation bodies such as The Joint Commission mandate that hospitals maintain specific ratios of equipment to beds and ensure that all suction devices are functional and regularly tested. Unlike smaller clinics or home care settings, hospitals employ dedicated biomedical engineering teams to manage and maintain this equipment, ensuring high utilization rates and timely replacements. The Centers for Disease Control and Prevention guidelines for infection control also require hospitals to have advanced suction systems with appropriate filtration, driving the purchase of newer, compliant models. The presence of specialized medical staff who are trained to operate complex suction devices maximizes their utility and justifies the investment in high-end equipment. This combination of regulatory pressure and professional capability ensures that hospitals and clinics continue to dominate the market landscape.

The home care segment is predicted to witness the highest CAGR of 8.2% over the forecast period. This swift expansion of the segment is supported by the demographic shift towards aging in place and the economic push to reduce hospital stays. The powerful demographic trend of seniors preferring to age in their own homes rather than in institutional facilities is the primary driver for the home care segment. As the baby boomer generation ages, there is a surging demand for medical equipment that supports chronic disease management within the residential setting. Many of these individuals suffer from conditions like COPD or neurological disorders that require regular airway suctioning. The preference drives the procurement of portable, user-friendly suction devices that can be operated by patients or family caregivers. The shift in care philosophy from institutionalization to home-based support is fundamentally reshaping the market, making home care the most dynamic growth area for suction device manufacturers. Strong economic incentives aimed at reducing hospital readmissions are accelerating the adoption of suction devices in the home care sector. Payers and healthcare systems are increasingly penalized for high readmission rates, encouraging the discharge of patients to home settings with adequate support equipment. Home health agencies are expanding their capabilities to manage complex cases at home, which requires a robust inventory of portable medical devices. The cost-effectiveness of home care compared to prolonged hospital stays makes it an attractive option for insurers, further fueling the demand for home use suction equipment. This economic alignment between cost savings and patient preference creates a fertile environment for rapid market growth in the home care segment.

COUNTRY LEVEL ANALYSIS

United States Medical Suction Devices Market Analysis

The United States remained the top performer in the North America medical suction devices market and captured a 84.5% share in 2025. This dominance of the United States is mainly propelled by its massive healthcare infrastructure and the high volume of medical procedures performed annually. The US market has the world's largest healthcare expenditure and the highest density of advanced medical facilities globally. Also, the nation boasts a large number of hospitals and tens of thousands of ambulatory surgical centers, all of which require extensive suction equipment. The prevalence of chronic diseases such as COPD and heart failure is also higher in the US compared to neighboring countries, creating a sustained demand for both institutional and home care suction devices. Furthermore, the US leads in the adoption of innovative medical technologies, with early uptake of battery-operated and smart suction devices driving market value. The robust reimbursement landscape provided by private insurance and government programs like Medicare ensures that healthcare providers can afford high-quality equipment. This combination of scale, wealth, and disease burden solidifies the United States as the central pillar of the regional market.

Canada Medical Suction Devices Market Analysis

Canada holds a noteworthy position in the North American market due to its aging population and the government's commitment to maintaining high standards of care across its vast geography. The country’s market reveals a highly organized public healthcare system that prioritizes universal access to essential medical equipment. The Canadian healthcare system, funded primarily through public taxation, ensures that hospitals and home care agencies are well-equipped with the necessary devices. The country's vast rural areas necessitate the use of portable and battery-powered suction units for remote clinics and air ambulance services, driving specific segment growth. Additionally, strict regulatory oversight by Health Canada ensures that only high-quality and safe devices enter the market, fostering trust and consistent procurement. The integration of home care services into the public health framework further supports the demand for residential suction equipment. Canada's focus on equitable access and preventive care sustains a steady and reliable market for medical suction technologies.

COMPETITIVE LANDSCAPE

The competition in the North American medical suction devices market is characterized by the presence of established multinational corporations alongside specialized niche manufacturers vying for dominance through innovation and strategic positioning. Major players leverage their extensive resources to drive technological advancement,s such as smart sensors and improved battery technologies that differentiate their offerings from competitors. The market sees intense rivalry as companies strive to capture share in high-growth segments like home care and emergency medical services by launching portable and user-friendly devices. Pricing pressure exists particularly in the public sector, where procurement decisions often prioritize cost-effectiveness alongside quality. Regulatory hurdles create barriers to entry for smaller firms but also serve as a competitive moat for incumbents who have already secured necessary approvals. Collaboration with healthcare providers for product testing and feedback loops is a common practice to ensure devices meet clinical needs accurately. The landscape is dynamic with frequent mergers and acquisitions reshaping the competitive hierarchy as firms seek to consolidate their market presence and expand their technological capabilities to address evolving customer demands.

KEY MARKET PLAYERS

Notable companies leading the North American Medical Suction Devices Market profiled in this report are

- Allied Healthcare Products Inc.

- ATMOS MedizinTechnik GmbH & Co. KG

- Drive Medical

- INTEGRA Biosciences

- Medela Holding AG

- Medicop

- Precision Medical Inc.

- SSCOR Inc.

- ZOLL Medical Corporation

- Weinmann Geräte für Medizin GmbH + Co. KG

- Laerdal Medical

- MG Electric Ltd

- Labconco Corporation

- Welch Vacuum

- Amsino International Inc.

- Olympus Corporation

TOP LEADING PLAYERS IN THE MARKET

- Medtronic plc stands as a global titan in medical technology with a profound impact on the North American medical suction devices sector through its extensive portfolio of surgical and respiratory solutions. The company integrates advanced suction capabilities into its broader surgical ecosystems, providing hospitals with seamless fluid management systems that enhance operative efficiency. Medtronic recently focused on refining its product lines to include smarter suction devices equipped with digital monitoring features that allow clinicians to track performance metrics in real time. Their commitment to innovation involves substantial investment in research and development to create devices that minimize noise and maximize portability for diverse clinical settings. By leveraging its vast distribution network and strong relationships with major healthcare providers, Medtronic ensures widespread availability of its high-quality suction equipment. The company actively engages in strategic collaborations with surgical centers to gather feedback and iterate on product designs, ensuring their offerings meet the evolving needs of modern surgery and critical care environments across the region.

- Stryker Corporation is a leading contributor to the North American medical suction devices market,t known for its robust engineering and focus on emergency and surgical care technologies. The company offers a range of portable and stationary suction units designed to withstand the rigorous demands of trauma centers and operating rooms. Stryker has recently intensified its efforts to enhance product durability and battery life, addressing critical needs for uninterrupted operation during prolonged procedures or patient transport. Their strategic initiatives include launching next-generation devices that feature intuitive user interfaces and improved filtration systems to protect healthcare workers from airborne pathogens. Stryker also prioritizes sustainability by developing energy-efficient motors and recyclable components for their suction product lines. Through active participation in industry conferences and continuous engagement with clinical staff, Stryker stays ahead of market trends and regulatory changes. These actions solidify their reputation as a reliable partner for healthcare facilities seeking high-performance suction solutions that integrate smoothly with existing medical infrastructure.

- Allied Healthcare Products Inc maintains a significant presence in the North American medical suction devices market by specializing in respiratory care and emergency response equipment. The company is renowned for manufacturing versatile suction units that cater to both hospital and prehospital settings, including ambulances and home care environments. Allied Healthcare recently expanded its product catalog to include lightweight battery-operated models that offer extended run times and rapid recharge capabilities for emergency medical technicians. Their focus on affordability and reliability makes their devices a preferred choice for public health agencies and rural clinics with budget constraints. The company has also invested in upgrading its manufacturing facilities to increase production capacity and reduce lead times for critical orders. Allied Healthcare actively collaborates with training institutions to ensure proper usage of their equipment, thereby enhancing patient safety outcomes. Allied Healthcare delivers consistently cost-effective and durable suction solutions. This strengthens their position as a vital supplier in the North American healthcare landscape.

TOP STRATEGIES USED BY KEY MARKET PARTICIPANTS

Key players in the North American medical suction devices market employ several strategic approaches to maintain competitiveness and drive growth. Product innovation remains a primary strategy where companies invest heavily in research and development to create devices with enhanced portability, longer battery life,e and smart connectivity features. Strategic acquisitions allow firms to expand their product portfolios and enter new geographic markets or technology segments rapidly. Partnerships with hospitals and research institutions facilitate clinical trials and product refinement based on real-world feedback. Companies also focus on regulatory compliance to ensure their devices meet stringent safety standards set by agencies like the Food and Drug Administration. Expanding distribution networks through collaborations with local distributors helps reach remote areas and underserved markets effectively. Additionally, manufacturers emphasize sustainability by designing energy-efficient devices and using recyclable materials to appeal to environmentally conscious healthcare providers. These combined strategies enable market participants to adapt to changing healthcare demands and secure long-term success.

MARKET SEGMENTATION

This research report on the North American Medical Suction Devices Market has been segmented & sub-segmented into the following categories.

By Portability

- Handheld Suction Devices

- Wall-Mounted Suction Devices

By Type

- Ac-Powered Devices

- Battery-Powered Devices

- Dual-Powered Devices

- Manually Operated Devices

By Application

- Airway Clearing

- Surgical Applications

- Research and Diagnostics

By End User

- Hospitals and Clinics

- Home Care

- Prehospital

- Other End Users

By Country

- The United States

- Canada

- Rest of North America

Related Reports

Access the study in MULTIPLE FORMATS

Purchase options starting from

$ 2000

Didn’t find what you’re looking for?

TALK TO OUR ANALYST TEAM

Need something within your budget?

NO WORRIES! WE GOT YOU COVERED!

Call us on: +1 888 702 9696 (U.S Toll Free)

Write to us: sales@marketdataforecast.com